Financial Management Online Exam: Solutions and Stakeholder Approach

VerifiedAdded on 2023/06/15

|8

|2107

|407

Homework Assignment

AI Summary

This document presents solutions to an online exam in Financial Management, covering key concepts and applications. It begins by discussing activity-based costing (ABC), its features, and reasons for development, along with key decisions under break-even and cost-profit volume analysis. The solution then calculates capital asset pricing using the CAPM model and the weighted average cost of capital (WACC), evaluating the effectiveness of CAPM in determining the cost of equity. Furthermore, the role of budgeting as a control and performance aid is critically discussed, contrasting traditional budgeting limitations with the features of beyond budgeting. The document also outlines various sources of finance for SMEs, excluding listing, and emphasizes the importance of the stakeholder approach and related factors in appraising corporate strategy. This comprehensive solution provides valuable insights into essential financial management principles and practices.

ONLINE EXAM-Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1...................................................................................................................................3

Features of activity based costing and reason for its development.............................................3

Key decision taken under break even and cost profit volume....................................................3

QUESTION 2...................................................................................................................................4

Calculating capital asset pricing..................................................................................................4

Calculating weighted average cost of capital..............................................................................4

Evaluating CAPM and whether it is good way for determining the cost of equity....................4

QUESTION 3...................................................................................................................................5

a. Critically discussing how budgeting may be used as a tool to aid control and performance..5

Limitation of traditional budgeting and features of beyond budgeting.......................................5

QUESTION 4...................................................................................................................................6

Outlining the sources of finance for SME other than listing......................................................6

QUESTION 5...................................................................................................................................6

Discussing the requirement of stakeholder approach and related factors while appraising

corporate strategy........................................................................................................................6

REFERENCES................................................................................................................................8

QUESTION 1...................................................................................................................................3

Features of activity based costing and reason for its development.............................................3

Key decision taken under break even and cost profit volume....................................................3

QUESTION 2...................................................................................................................................4

Calculating capital asset pricing..................................................................................................4

Calculating weighted average cost of capital..............................................................................4

Evaluating CAPM and whether it is good way for determining the cost of equity....................4

QUESTION 3...................................................................................................................................5

a. Critically discussing how budgeting may be used as a tool to aid control and performance..5

Limitation of traditional budgeting and features of beyond budgeting.......................................5

QUESTION 4...................................................................................................................................6

Outlining the sources of finance for SME other than listing......................................................6

QUESTION 5...................................................................................................................................6

Discussing the requirement of stakeholder approach and related factors while appraising

corporate strategy........................................................................................................................6

REFERENCES................................................................................................................................8

QUESTION 1

a. Features of activity based costing and reason for its development

Activity based costing is being referred to as the tool which assist company in dividing

the cost and attributing to the product and services. This involves focusing on the identification

of activities for a particular job and different activities are grouped together and relates to single

cost driver (Liu, 2021). The features of ABC involves the following-

The total cost is being divided in two different types that is fixed and variable cost.

In addition to this another key feature of ABC is the there is proper distinction being

made within the cost behaviour pattern.

Moreover, the cost driver needs to be identified in order to trace the overhead to the

product directly.

With the above analysis it is clear that the use of ABC is very important for the

companies in managing cost. The reason for the development of the ABC is that this method is

more accurate and assists in better costing of product and services. This costing method

highlights the most costly and the non- value adding activities more visible and this assist

manager in improving those areas.

b. Key decision taken under break even and cost profit volume

The break even or the cost profit volume is being defined as the level of production

wherein the company is at no profit no loss situation. This is necessary for the company to

analyse and take proper decision relating to the production level. This BEP or cost profit volume

in taking major decision that is the sales quantity where the company can be in no profit and no

loss situation.

On the other hand, there is some of the limitation relating to break- even point. The major

limitation of the break even or cost profit volume is that it assumed the fixed cost is constant

whether be it short run or long run production (Villasanti, Giraldo and Passino, 2018). Another

limitation of using the BEP or cost profit volume is that this method assumes that average

variable cost is constant per unit for at least quantity of sales.

a. Features of activity based costing and reason for its development

Activity based costing is being referred to as the tool which assist company in dividing

the cost and attributing to the product and services. This involves focusing on the identification

of activities for a particular job and different activities are grouped together and relates to single

cost driver (Liu, 2021). The features of ABC involves the following-

The total cost is being divided in two different types that is fixed and variable cost.

In addition to this another key feature of ABC is the there is proper distinction being

made within the cost behaviour pattern.

Moreover, the cost driver needs to be identified in order to trace the overhead to the

product directly.

With the above analysis it is clear that the use of ABC is very important for the

companies in managing cost. The reason for the development of the ABC is that this method is

more accurate and assists in better costing of product and services. This costing method

highlights the most costly and the non- value adding activities more visible and this assist

manager in improving those areas.

b. Key decision taken under break even and cost profit volume

The break even or the cost profit volume is being defined as the level of production

wherein the company is at no profit no loss situation. This is necessary for the company to

analyse and take proper decision relating to the production level. This BEP or cost profit volume

in taking major decision that is the sales quantity where the company can be in no profit and no

loss situation.

On the other hand, there is some of the limitation relating to break- even point. The major

limitation of the break even or cost profit volume is that it assumed the fixed cost is constant

whether be it short run or long run production (Villasanti, Giraldo and Passino, 2018). Another

limitation of using the BEP or cost profit volume is that this method assumes that average

variable cost is constant per unit for at least quantity of sales.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

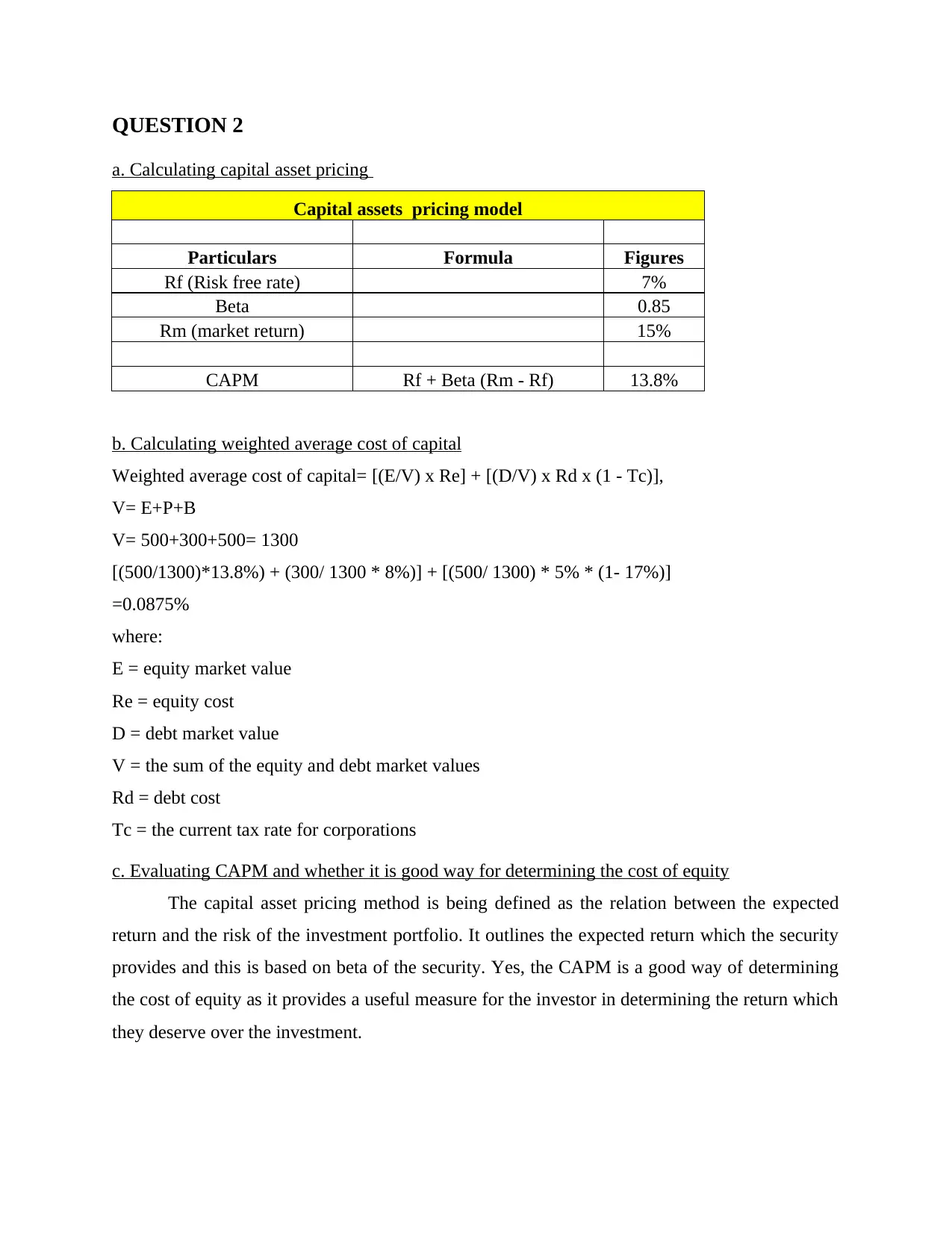

QUESTION 2

a. Calculating capital asset pricing

Capital assets pricing model

Particulars Formula Figures

Rf (Risk free rate) 7%

Beta 0.85

Rm (market return) 15%

CAPM Rf + Beta (Rm - Rf) 13.8%

b. Calculating weighted average cost of capital

Weighted average cost of capital= [(E/V) x Re] + [(D/V) x Rd x (1 - Tc)],

V= E+P+B

V= 500+300+500= 1300

[(500/1300)*13.8%) + (300/ 1300 * 8%)] + [(500/ 1300) * 5% * (1- 17%)]

=0.0875%

where:

E = equity market value

Re = equity cost

D = debt market value

V = the sum of the equity and debt market values

Rd = debt cost

Tc = the current tax rate for corporations

c. Evaluating CAPM and whether it is good way for determining the cost of equity

The capital asset pricing method is being defined as the relation between the expected

return and the risk of the investment portfolio. It outlines the expected return which the security

provides and this is based on beta of the security. Yes, the CAPM is a good way of determining

the cost of equity as it provides a useful measure for the investor in determining the return which

they deserve over the investment.

a. Calculating capital asset pricing

Capital assets pricing model

Particulars Formula Figures

Rf (Risk free rate) 7%

Beta 0.85

Rm (market return) 15%

CAPM Rf + Beta (Rm - Rf) 13.8%

b. Calculating weighted average cost of capital

Weighted average cost of capital= [(E/V) x Re] + [(D/V) x Rd x (1 - Tc)],

V= E+P+B

V= 500+300+500= 1300

[(500/1300)*13.8%) + (300/ 1300 * 8%)] + [(500/ 1300) * 5% * (1- 17%)]

=0.0875%

where:

E = equity market value

Re = equity cost

D = debt market value

V = the sum of the equity and debt market values

Rd = debt cost

Tc = the current tax rate for corporations

c. Evaluating CAPM and whether it is good way for determining the cost of equity

The capital asset pricing method is being defined as the relation between the expected

return and the risk of the investment portfolio. It outlines the expected return which the security

provides and this is based on beta of the security. Yes, the CAPM is a good way of determining

the cost of equity as it provides a useful measure for the investor in determining the return which

they deserve over the investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 3

a. Critically discussing how budgeting may be used as a tool to aid control and performance

Budgeting may be defined as a quantitative tool which presents estimated revenue and

expenses pertaining to a specific time frame. In the context of business unit, budgeting may be

served as the most effectual tool which provides deeper insight about the extent to which money

need to be spent. In addition to this, by using budgets business unit can assess deviations which

take place in company’s performance (Lukač and et.al., 2019). In other words, by comparing

current performance in against to the standards firm can easily determine the extent which

specific department failed to meet benchmarks. Referring causes of deviations business unit can

take corrective measures performance control and enhancement. Hence, by considering all such

aspects it can be stated that budgeting plays a vital role in performance evaluation and control to

the significant level.

The benefit of using budgeting is that this improves effective resource allocation and as a

result of this the working of the business will be improved. Moreover, another benefit is that this

tool also assists in effective reallocation of work in better and effective manner. on the other

hand, the drawback of using the budgeting as a planning tool is that the budget cannot be always

correct as no person can predict the future correctly.

b. Limitation of traditional budgeting and features of beyond budgeting

The traditional budget is a type of budget which is being prepared by keeping in mind the

past data and records. This is the type of budgeting which involves the past data and because of

this it is stated as the traditional form of budgeting. The limitation of using the traditional

budgeting is as follows-

The major limitation being faced by using the traditional budgeting is that there are

chances of high human error. This is because of the reason that the budget is being

prepared by undertaking the past data. There can be human error and this can lead to

issues.

In addition to this, another limitation is that the prediction can be wrong as the working is

based on future working (Astiti, Warmana and Hidayah, 2019). This is pertaining to the

a. Critically discussing how budgeting may be used as a tool to aid control and performance

Budgeting may be defined as a quantitative tool which presents estimated revenue and

expenses pertaining to a specific time frame. In the context of business unit, budgeting may be

served as the most effectual tool which provides deeper insight about the extent to which money

need to be spent. In addition to this, by using budgets business unit can assess deviations which

take place in company’s performance (Lukač and et.al., 2019). In other words, by comparing

current performance in against to the standards firm can easily determine the extent which

specific department failed to meet benchmarks. Referring causes of deviations business unit can

take corrective measures performance control and enhancement. Hence, by considering all such

aspects it can be stated that budgeting plays a vital role in performance evaluation and control to

the significant level.

The benefit of using budgeting is that this improves effective resource allocation and as a

result of this the working of the business will be improved. Moreover, another benefit is that this

tool also assists in effective reallocation of work in better and effective manner. on the other

hand, the drawback of using the budgeting as a planning tool is that the budget cannot be always

correct as no person can predict the future correctly.

b. Limitation of traditional budgeting and features of beyond budgeting

The traditional budget is a type of budget which is being prepared by keeping in mind the

past data and records. This is the type of budgeting which involves the past data and because of

this it is stated as the traditional form of budgeting. The limitation of using the traditional

budgeting is as follows-

The major limitation being faced by using the traditional budgeting is that there are

chances of high human error. This is because of the reason that the budget is being

prepared by undertaking the past data. There can be human error and this can lead to

issues.

In addition to this, another limitation is that the prediction can be wrong as the working is

based on future working (Astiti, Warmana and Hidayah, 2019). This is pertaining to the

fact that future cannot be predicted and as a result of this the prediction can be prove

wrong.

Other than, this there is also a concept of beyond budgeting which states that traditional

budgeting must be abolished in order to improve the management control of the company. The

use of beyond budgeting is very important in order to make the working better and effective

(Ramírez-Urquidy, Aguilar-Barceló and Portal-Boza, 2018). Some of the features of using

beyond budgeting are as follows-

The key feature is that this method is much faster and adaptive in comparison to the

process of traditional budgeting.

Along with this, another key feature is that the process is decentralised and this makes the

budgeting much easier and effective.

QUESTION 4

Outlining the sources of finance for SME other than listing

Without the use of finance no company can work in better and effective manner. The

reason pertaining to the fact is that without the money no activity can be undertaken within the

business. Thus there are many different types of sources through which finance can be generated.

Other then listing the sources of finance being available for both the companies is as follows-

Loan- this is a type of finance wherein the company can borrow the money from any

bank or financial service provider. In this present source of finance the person has to give

interest against the money borrowed or some collateral against the loan taken.

Debenture- this is another source of finance through which money can be borrowed in

order to fulfil the need of the business. In this source of finance, the money is being

borrowed by issuing the debenture to the public. In this source of finance, the ownership

is not being provided to the person getting debenture.

Venture capital- in addition to this, it is another source of finance wherein both the

companies can arrange for the money. This is a source of private equity financing which

provides the fund for the start-up (Gherasim and Ionescu, 2019). Both the companies can

also take or borrow money from the venture capital and fulfil their need and requirement

of the business.

wrong.

Other than, this there is also a concept of beyond budgeting which states that traditional

budgeting must be abolished in order to improve the management control of the company. The

use of beyond budgeting is very important in order to make the working better and effective

(Ramírez-Urquidy, Aguilar-Barceló and Portal-Boza, 2018). Some of the features of using

beyond budgeting are as follows-

The key feature is that this method is much faster and adaptive in comparison to the

process of traditional budgeting.

Along with this, another key feature is that the process is decentralised and this makes the

budgeting much easier and effective.

QUESTION 4

Outlining the sources of finance for SME other than listing

Without the use of finance no company can work in better and effective manner. The

reason pertaining to the fact is that without the money no activity can be undertaken within the

business. Thus there are many different types of sources through which finance can be generated.

Other then listing the sources of finance being available for both the companies is as follows-

Loan- this is a type of finance wherein the company can borrow the money from any

bank or financial service provider. In this present source of finance the person has to give

interest against the money borrowed or some collateral against the loan taken.

Debenture- this is another source of finance through which money can be borrowed in

order to fulfil the need of the business. In this source of finance, the money is being

borrowed by issuing the debenture to the public. In this source of finance, the ownership

is not being provided to the person getting debenture.

Venture capital- in addition to this, it is another source of finance wherein both the

companies can arrange for the money. This is a source of private equity financing which

provides the fund for the start-up (Gherasim and Ionescu, 2019). Both the companies can

also take or borrow money from the venture capital and fulfil their need and requirement

of the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 5

Discussing the requirement of stakeholder approach and related factors while appraising

corporate strategy

When the business is operating then there are many different types of people being

involved. Hence it is very important for the business that they keep all the people involved

within the business happy and satisfied. The reason underlying this fact is that when the business

will not be providing satisfaction to various stakeholders then this will be affecting their business

and its development. The stakeholders are the people who are interested in better working of the

company. These are the people who always think for the development and growth of business.

Hence, it is the responsibility of business that they undertake the use of stakeholder approach in

order to keep the stakeholder happy and satisfied (Li and et.al., 2020). Hence when the

stakeholder will be happy then this will result in the effective attainment of the objectives of the

business. In addition to this it is also necessary for the business to keep other factors as well in

mind while working. This is because of the reason that when the working of the business will be

good then this will be improving the working efficiency of the business. Thus, for implementing

any of the strategy or any other decision it is necessary that stakeholders are being taken care off

while making strategies.

Discussing the requirement of stakeholder approach and related factors while appraising

corporate strategy

When the business is operating then there are many different types of people being

involved. Hence it is very important for the business that they keep all the people involved

within the business happy and satisfied. The reason underlying this fact is that when the business

will not be providing satisfaction to various stakeholders then this will be affecting their business

and its development. The stakeholders are the people who are interested in better working of the

company. These are the people who always think for the development and growth of business.

Hence, it is the responsibility of business that they undertake the use of stakeholder approach in

order to keep the stakeholder happy and satisfied (Li and et.al., 2020). Hence when the

stakeholder will be happy then this will result in the effective attainment of the objectives of the

business. In addition to this it is also necessary for the business to keep other factors as well in

mind while working. This is because of the reason that when the working of the business will be

good then this will be improving the working efficiency of the business. Thus, for implementing

any of the strategy or any other decision it is necessary that stakeholders are being taken care off

while making strategies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Astiti, N. P. Y., Warmana, G. O. and Hidayah, M., 2019. Financial literation and investment

decision behavior of entrepreneurs in Bali. International Journal of Applied Business

and International Management (IJABIM). 4(3). pp.64-68.

Gherasim, Z. and Ionescu, L., 2019. The financial accountability of e-government: the

information transparency of decision-making processes in public organizations. Annals

of Spiru Haret University. Economic Seriesˮ. 3. pp.23-32.

Li, W., and et.al., 2020. Data mining optimization model for financial management information

system based on improved genetic algorithm. Information Systems and e-Business

Management. 18(4). pp.747-765.

Liu, B., 2021, April. Research on Enterprise Financial Management Supervision Mode Based on

Data Mining. In Journal of Physics: Conference Series (Vol. 1881, No. 4, p. 042074).

IOP Publishing.

Lukač, J., and et.al., 2019. Use of Statistical Methods as an Educational Tool in the Financial

Management of Enterprises in the Implementation of International Financial Reporting

Standards. TEM Journal. 8(3). p.819.

Ramírez-Urquidy, M., Aguilar-Barceló, J. G. and Portal-Boza, M., 2018. The Impact of

Economic and Financial Management Practices on the Performance of Mexican Micro-

Enterprises: A Multivariate Analysis. Revista Brasileira de Gestão de Negócios. 20.

pp.319-337.

Villasanti, H. G., Giraldo, L. F. and Passino, K. M., 2018. Feedback control engineering for

cooperative community development: Tools for financial management advice for low-

income individuals. IEEE Control Systems Magazine. 38(3). pp.87-101.

Books and Journals

Astiti, N. P. Y., Warmana, G. O. and Hidayah, M., 2019. Financial literation and investment

decision behavior of entrepreneurs in Bali. International Journal of Applied Business

and International Management (IJABIM). 4(3). pp.64-68.

Gherasim, Z. and Ionescu, L., 2019. The financial accountability of e-government: the

information transparency of decision-making processes in public organizations. Annals

of Spiru Haret University. Economic Seriesˮ. 3. pp.23-32.

Li, W., and et.al., 2020. Data mining optimization model for financial management information

system based on improved genetic algorithm. Information Systems and e-Business

Management. 18(4). pp.747-765.

Liu, B., 2021, April. Research on Enterprise Financial Management Supervision Mode Based on

Data Mining. In Journal of Physics: Conference Series (Vol. 1881, No. 4, p. 042074).

IOP Publishing.

Lukač, J., and et.al., 2019. Use of Statistical Methods as an Educational Tool in the Financial

Management of Enterprises in the Implementation of International Financial Reporting

Standards. TEM Journal. 8(3). p.819.

Ramírez-Urquidy, M., Aguilar-Barceló, J. G. and Portal-Boza, M., 2018. The Impact of

Economic and Financial Management Practices on the Performance of Mexican Micro-

Enterprises: A Multivariate Analysis. Revista Brasileira de Gestão de Negócios. 20.

pp.319-337.

Villasanti, H. G., Giraldo, L. F. and Passino, K. M., 2018. Feedback control engineering for

cooperative community development: Tools for financial management advice for low-

income individuals. IEEE Control Systems Magazine. 38(3). pp.87-101.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.