Financial Management Homework: Investment and Bond Valuation Analysis

VerifiedAdded on 2019/10/30

|8

|1022

|128

Homework Assignment

AI Summary

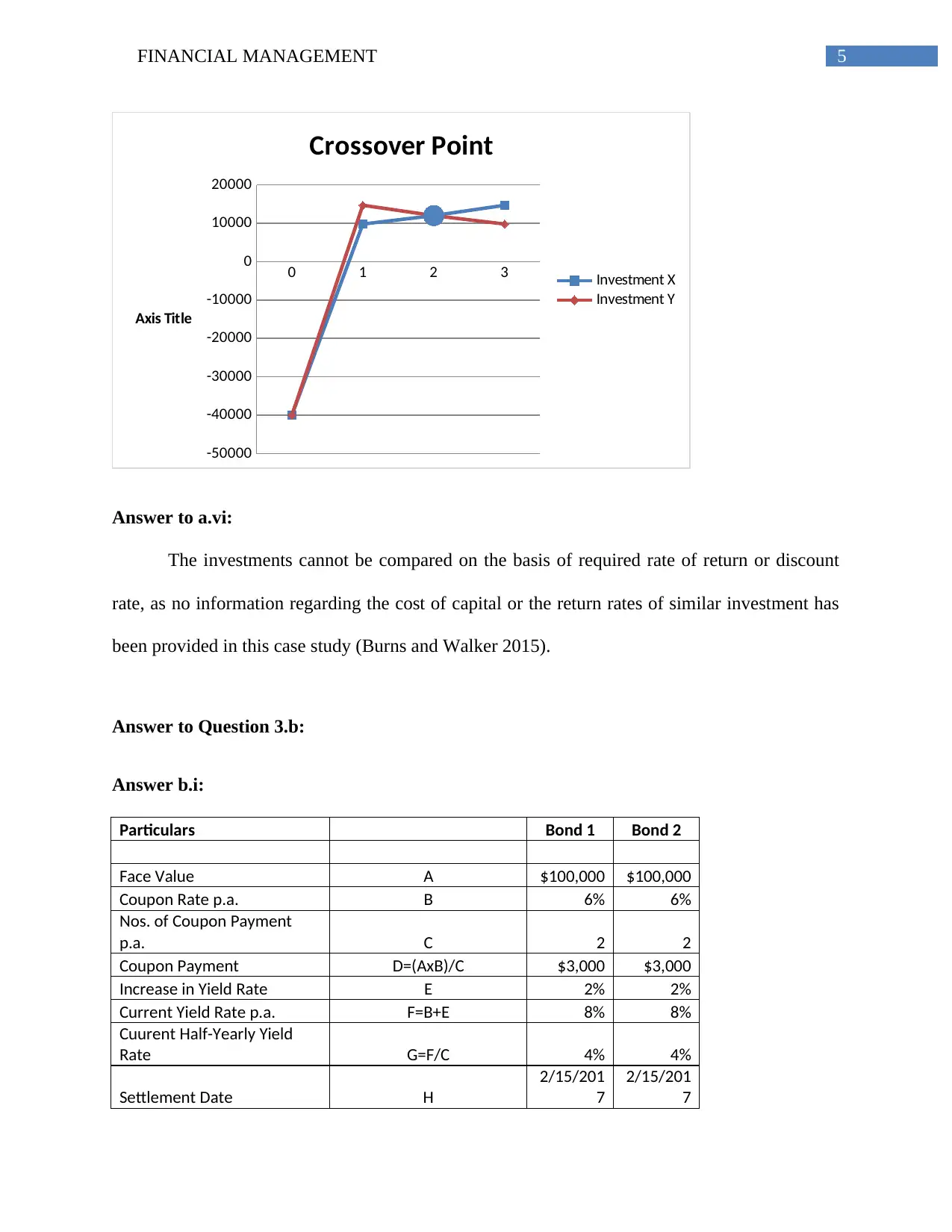

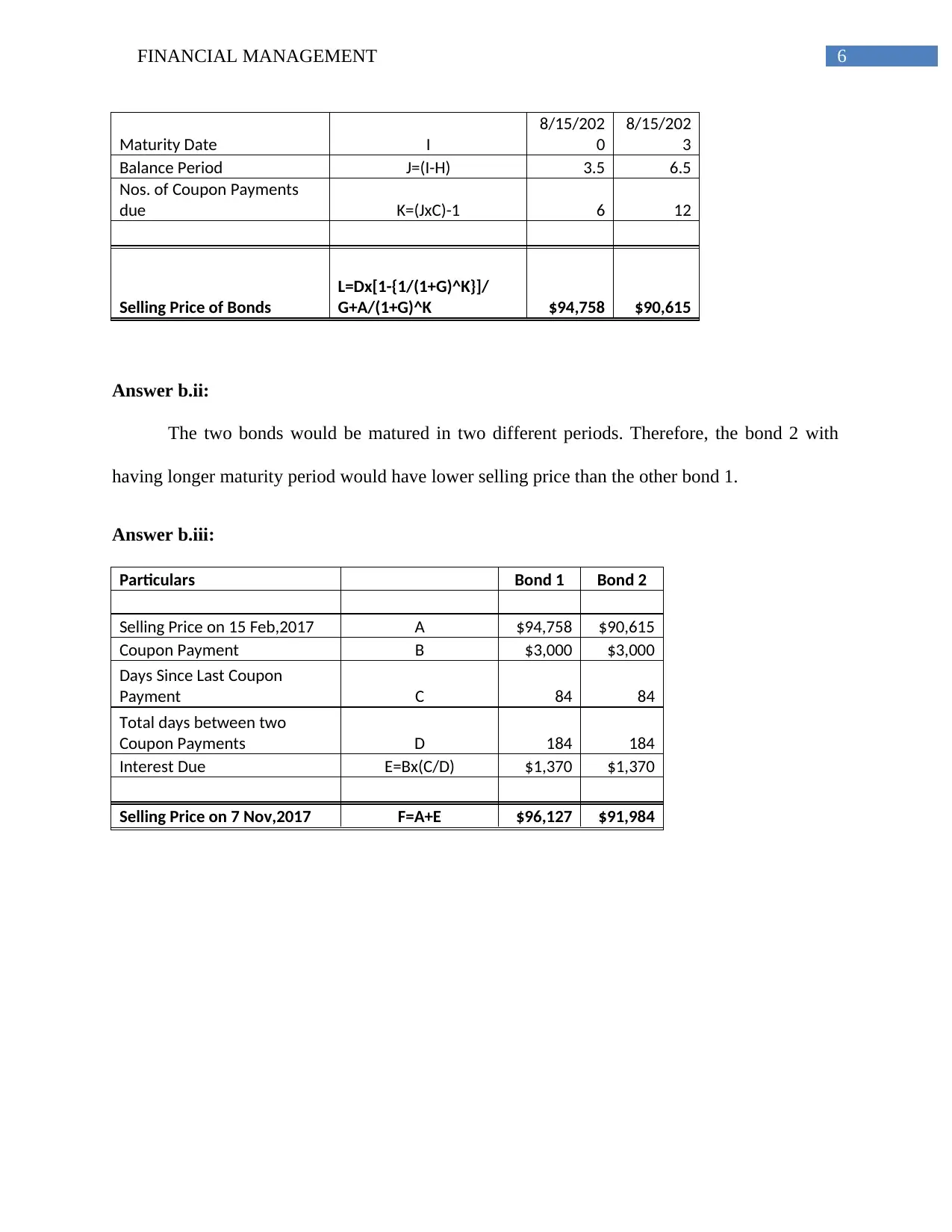

This document presents a comprehensive solution to a financial management homework assignment. The solution begins with an analysis of two investment projects, comparing them based on payback period, cumulative cash flow, and net cash flow. The analysis explores the limitations of comparing investments without a discount rate and discusses the calculation of Internal Rate of Return (IRR). The assignment then transitions to bond valuation, calculating the selling prices of two bonds with different maturity dates and coupon rates. The solution also considers the impact of yield rate increases on bond prices and calculates the interest due on the bonds. The analysis uses a detailed table format to present calculations and includes a reference list of relevant academic sources.

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.