Financial Resources Management: A Hospitality Industry Report

VerifiedAdded on 2023/06/16

|13

|3168

|484

Report

AI Summary

This report provides an overview of managing financial resources within the hospitality industry. It begins by explaining general accounting principles such as regularity, consistency, sincerity, permanence, non-compensation, prudence, continuity, periodicity, materiality and fantastic faith. It identifies various users of financial information, including owners, investment analysts, and managers, and their reasons for needing financial data. The report then discusses three key financial statements: the balance sheet, income statement, and cash flow statement, detailing their components and importance to stakeholders like loan creditors and trade creditors. The concept of financial reporting is explored, emphasizing its role in investment decision-making and managing accountability. Finally, the report includes a calculation of Return on Assets (ROA) and Return on Equity (ROE) for the years 2018 and 2019, demonstrating ratio analysis techniques.

Managing Financial Resources in the Hospitality Industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Explanation of general accounting principles:.............................................................................3

The discussion of three financial statements:..............................................................................5

The components in the financial statements:...............................................................................6

Financial report concept:..............................................................................................................7

Calculation of the ratio:...............................................................................................................8

CONCLUSION..............................................................................................................................12

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Explanation of general accounting principles:.............................................................................3

The discussion of three financial statements:..............................................................................5

The components in the financial statements:...............................................................................6

Financial report concept:..............................................................................................................7

Calculation of the ratio:...............................................................................................................8

CONCLUSION..............................................................................................................................12

REFERENCES................................................................................................................................1

INTRODUCTION

Managing financial resources means handling and managing financial issue, this

management includes performance measure tools such as cost analysis, profitability and methods

of controlling finance of the company (Block, Hirt, and Danielsen, 2018). Management financial

resources help company to calculate all necessary data by applying basic accounting principles

and mainly help the company in making financial decision. In this report we will discuss general

accounting principles and identify various user whop wish to see the financial statements of the

company. Later we will assess the information to in decision-making process. Later we will

discuss various financial statements and components. At last we will discuss and calculate the

various ratios.

MAIN BODY

Explanation of general accounting principles:

General accounting principles are the accounting practices which provide help in

reporting the accounting of the company (Armour, et.al., 2016). This accounting standards are

very beneficial for the company in management and putting together financial statements to

understand the performance of the company. General accounting principles provide clear and

consistence results which allow company to compare various financial information. There are ten

most important accounting principles such as:

Principles of regularity: the principles of regularity allow business to regularly assess the

financial information of the company and help them to make regular financial decisions. Every

business organizations and accountant use principles of regularity to understand the financial

stability of the company.

Principles of consistency: principles of consistency allow business organizations to report the

financial information of the company from one period to another. The gap between these two

period needs to be consistence (Brigham and Houston, 2021). The accountant of the company

have to explain and provide clear disclose about the changes that have occurred during this

period.

Principles of sincerity: principles of sincerity help accountant of the company provide clear and

accurate accounting results which help company to understand the financial situation of the

Managing financial resources means handling and managing financial issue, this

management includes performance measure tools such as cost analysis, profitability and methods

of controlling finance of the company (Block, Hirt, and Danielsen, 2018). Management financial

resources help company to calculate all necessary data by applying basic accounting principles

and mainly help the company in making financial decision. In this report we will discuss general

accounting principles and identify various user whop wish to see the financial statements of the

company. Later we will assess the information to in decision-making process. Later we will

discuss various financial statements and components. At last we will discuss and calculate the

various ratios.

MAIN BODY

Explanation of general accounting principles:

General accounting principles are the accounting practices which provide help in

reporting the accounting of the company (Armour, et.al., 2016). This accounting standards are

very beneficial for the company in management and putting together financial statements to

understand the performance of the company. General accounting principles provide clear and

consistence results which allow company to compare various financial information. There are ten

most important accounting principles such as:

Principles of regularity: the principles of regularity allow business to regularly assess the

financial information of the company and help them to make regular financial decisions. Every

business organizations and accountant use principles of regularity to understand the financial

stability of the company.

Principles of consistency: principles of consistency allow business organizations to report the

financial information of the company from one period to another. The gap between these two

period needs to be consistence (Brigham and Houston, 2021). The accountant of the company

have to explain and provide clear disclose about the changes that have occurred during this

period.

Principles of sincerity: principles of sincerity help accountant of the company provide clear and

accurate accounting results which help company to understand the financial situation of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company (Titman and Keown, 2018). These principles allow accountant to sincerely interpret the

data and information of financial statements of the company which keep the company stable in

the position.

Principles of permanence: these principles of permanence is mainly used in the financial report

and comparing these reports with each other, when the company try to compare one financial

information with another, they get the clear idea about the stability and growth performance of

the company.

Principles of non compensation: the principles of non compensation help the company to

identify both, the negative as well as the positive report and compare them to find the

transparency between two reports. Accountant of the company can compare the report without

the debt compensation.

Principles of prudence: the principles of prudence help accountant of the company to interpret

the data on the basis of facts. This fact based data is represented clear data without any

speculation.

Principles of continuity: these principles of continuity help accountant to find the value of the

assets of the company, this valuation help company to understand whether the business will

continue in profit or continue in the loss.

Principles of periodicity: these principles of periodicity allow business to distribute entries in

perfect manner to avoid any kind of speculation and misunderstanding. This help accountant of

the company to report data within the accounting period.

Principles of materiality: these principles of materiality help accountant to stay materialistic in

interpreting the financial data, they want all the financial data clear and materialist without any

speculation in the report.

Principles of fantastic faith: these principles of fantastic faith help company to build trust and

honest between their customer, in these principles is very important for the companies who deal

in insurance and financial services.

There are certain user of financial information who need financial data to make financial

decision regarding investment. These users need financial information to make further decision

regarding the investment in the company. There are certain financial user to interpret the

financial data such as:

data and information of financial statements of the company which keep the company stable in

the position.

Principles of permanence: these principles of permanence is mainly used in the financial report

and comparing these reports with each other, when the company try to compare one financial

information with another, they get the clear idea about the stability and growth performance of

the company.

Principles of non compensation: the principles of non compensation help the company to

identify both, the negative as well as the positive report and compare them to find the

transparency between two reports. Accountant of the company can compare the report without

the debt compensation.

Principles of prudence: the principles of prudence help accountant of the company to interpret

the data on the basis of facts. This fact based data is represented clear data without any

speculation.

Principles of continuity: these principles of continuity help accountant to find the value of the

assets of the company, this valuation help company to understand whether the business will

continue in profit or continue in the loss.

Principles of periodicity: these principles of periodicity allow business to distribute entries in

perfect manner to avoid any kind of speculation and misunderstanding. This help accountant of

the company to report data within the accounting period.

Principles of materiality: these principles of materiality help accountant to stay materialistic in

interpreting the financial data, they want all the financial data clear and materialist without any

speculation in the report.

Principles of fantastic faith: these principles of fantastic faith help company to build trust and

honest between their customer, in these principles is very important for the companies who deal

in insurance and financial services.

There are certain user of financial information who need financial data to make financial

decision regarding investment. These users need financial information to make further decision

regarding the investment in the company. There are certain financial user to interpret the

financial data such as:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Owners: the owners keep eye on the financial information to understand whether the company is

making profit or in loss. Owners are the first user who want to see the these informations.

Investment analysts: investment analysts want these financial data to understand the performance

and stability of the company, these analysts plays a vital role.

Managers: managers always look at the financial information to understand where is the

company heading towards, the manager have responsibility of whole company including the

financial department. Managers keep eye on these informations to stop any kind of speculations

and try to keep control on the financial position of the company.

The discussion of three financial statements:

Financial statements are very important for every parties who are connected with the

company to deal in the trade, these parties analyse and understand the financial information by

understanding the financial statements, these statements have all the important information such

as performance of the company (Weygandt, Kimmel and Kieso, 2018). Many third parties

compulsory examine these statements such as government, speculation agencies and audit of

other firms. Government interferes in the financial statement of the company to find out whether

the company us paying tax. There are certain financial statement such as:

Balance sheet: the balance sheet provide the overview of financial elements such as assets and

liabilities, shares and equity and stakeholder snapshot. Balance sheets of the company is very

important for all the third parties of the company and mainly for the loan creditors and trade

creditors. The load creditors plays an vital role in the growth of the company, they provide the

required loan to the company (Castillo, 2016). Before making any loan decision, the loan

creditors understand the balance sheet of the company, if the company is making profit then the

loan creditor will provide loan but if the company is under the loss then loan creditor can strictly

prohibit their loan to the company. Whereas the trade creditors are supplier who provide raw

material to the company, they analyse the balance sheet because business often order raw

material from these suppliers and payment of such raw material are delayed, this delay is

acceptable by both the parties because of the trust. These trade creditors examine the balance

before providing any further goods to the company.

Income statements: income statements are the revenue details of the company, this provides

information about the company's earning capacity and income level. The company have various

third parties mainly, loan creditors only provide loans by understand the income statements of

making profit or in loss. Owners are the first user who want to see the these informations.

Investment analysts: investment analysts want these financial data to understand the performance

and stability of the company, these analysts plays a vital role.

Managers: managers always look at the financial information to understand where is the

company heading towards, the manager have responsibility of whole company including the

financial department. Managers keep eye on these informations to stop any kind of speculations

and try to keep control on the financial position of the company.

The discussion of three financial statements:

Financial statements are very important for every parties who are connected with the

company to deal in the trade, these parties analyse and understand the financial information by

understanding the financial statements, these statements have all the important information such

as performance of the company (Weygandt, Kimmel and Kieso, 2018). Many third parties

compulsory examine these statements such as government, speculation agencies and audit of

other firms. Government interferes in the financial statement of the company to find out whether

the company us paying tax. There are certain financial statement such as:

Balance sheet: the balance sheet provide the overview of financial elements such as assets and

liabilities, shares and equity and stakeholder snapshot. Balance sheets of the company is very

important for all the third parties of the company and mainly for the loan creditors and trade

creditors. The load creditors plays an vital role in the growth of the company, they provide the

required loan to the company (Castillo, 2016). Before making any loan decision, the loan

creditors understand the balance sheet of the company, if the company is making profit then the

loan creditor will provide loan but if the company is under the loss then loan creditor can strictly

prohibit their loan to the company. Whereas the trade creditors are supplier who provide raw

material to the company, they analyse the balance sheet because business often order raw

material from these suppliers and payment of such raw material are delayed, this delay is

acceptable by both the parties because of the trust. These trade creditors examine the balance

before providing any further goods to the company.

Income statements: income statements are the revenue details of the company, this provides

information about the company's earning capacity and income level. The company have various

third parties mainly, loan creditors only provide loans by understand the income statements of

the company, if the company is making surplus profit then loan creditors will be ready to provide

loan to the company but if the there is no profit in the income statements then their might change

the decision (Charitou, et.al., 2018). Whereas the trade creditor examine the income statements

to analyse whether the company is making profit and then make decision to supply raw material.

Cash flow statements: the cash flow statements allow third parties to look at the flow of the

cash in the company, this flow needs to be continued. Cash flow mainly provide details of the

transaction activities and total cash used in the expense of the company. Accountant of the

company maintain the cash flow statements on the regular basis to stop any kind of speculation

in the company (Deo, 2016). The loan creditors examine the cash flow statements because they

can identify the growth of the company just by understanding the flow of cash in the company.

Whereas the trade creditors carefully examine the cash flow statements because many suppliers

trade in cash and want to understand whether the company have enough cash to buy the goods.

The components in the financial statements:

The financial reporting help business to understand the financial and overall growth of

the company, when the investor plan to invest in the business organization they identify, examine

and understand the component of the financial statements such as:

Balance sheet: balance sheet is the overview of the financial statements, this help business and

investor to understand the growth and performance of the company. Balance sheet is very

beneficial for the company as this help them to calculate assets and liabilities (Flower and

Ebbers, 2018). There are various components of the financial statements such as assets and

liabilities, stockholder's details, capital details and information. Balance sheet is been prepared to

snapshot the performance of the company within a financial year.

Formula of balance sheet:

Assets= liabilities + owner's equity.

Income statement: income statements are details and information about the inflow income in

the business organization. The income statements provide overview of the revenue, expense,

income, spending and earning per share (Fraser, Ormiston and Fraser, 2016). These statements

are very important for the company's stakeholder as they carefully understand where is company

is heading towards and what precautions and strategies are been required. Income statements

provide data from at least two to three years. This provides total of revenue and sales within a

period of time.

loan to the company but if the there is no profit in the income statements then their might change

the decision (Charitou, et.al., 2018). Whereas the trade creditor examine the income statements

to analyse whether the company is making profit and then make decision to supply raw material.

Cash flow statements: the cash flow statements allow third parties to look at the flow of the

cash in the company, this flow needs to be continued. Cash flow mainly provide details of the

transaction activities and total cash used in the expense of the company. Accountant of the

company maintain the cash flow statements on the regular basis to stop any kind of speculation

in the company (Deo, 2016). The loan creditors examine the cash flow statements because they

can identify the growth of the company just by understanding the flow of cash in the company.

Whereas the trade creditors carefully examine the cash flow statements because many suppliers

trade in cash and want to understand whether the company have enough cash to buy the goods.

The components in the financial statements:

The financial reporting help business to understand the financial and overall growth of

the company, when the investor plan to invest in the business organization they identify, examine

and understand the component of the financial statements such as:

Balance sheet: balance sheet is the overview of the financial statements, this help business and

investor to understand the growth and performance of the company. Balance sheet is very

beneficial for the company as this help them to calculate assets and liabilities (Flower and

Ebbers, 2018). There are various components of the financial statements such as assets and

liabilities, stockholder's details, capital details and information. Balance sheet is been prepared to

snapshot the performance of the company within a financial year.

Formula of balance sheet:

Assets= liabilities + owner's equity.

Income statement: income statements are details and information about the inflow income in

the business organization. The income statements provide overview of the revenue, expense,

income, spending and earning per share (Fraser, Ormiston and Fraser, 2016). These statements

are very important for the company's stakeholder as they carefully understand where is company

is heading towards and what precautions and strategies are been required. Income statements

provide data from at least two to three years. This provides total of revenue and sales within a

period of time.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Formula of income statements:

Net income= (revenue-expense)

Cash flow statement: cash flow statements means the statements which highlight the flow of the

cash in the business organization, this cash flow statements provide clear details and information

to the investors and the people of the to understand the ability of the company to pay the cash

and the cash available with the company. The cash flow statements allow all the stakeholders and

the investors of the company to view the performance of the operation of the company. These

statements help investor to understand that from where the cash is coming from and how

company is utilizing the money.

Financial report concept:

Financial report is the end and complete result of the business organization, this financial

report have various purpose and are been designed to provide all the important and crucial

financial details and information. Financial report is been analysed by the stakeholder and people

who are been connected to the company (Lasher, 2016). When the business organization keep

the report in a perfect manner then they get the idea to plan the up coming financial things of the

business such as to set the budget and other finance related things. If the business organization

deals in the public, then they have to keep maintain the report every year to show the pubic and

the stakeholder about the performance of the company. Financial report help company to

communicate with the people by publishing their financial statements which show the stability

and performance. There are certain purpose of financial reporting such as;

Investment decision-making: stakeholder and the people who are interested in the company and

want to invest in it always prefer financial report which provide them all the necessary

information such as the profitability and growth rate of the company. Investment are been done

by various investors such as stakeholders, public and employees of the company.

Managing accountability: the financial report provide management team a clear and perfect

details and the information of the stability and growth of the company. The management team,

ask finance team to provide financial report to make future plan and management strategies

(Penman, 2016). The management team have the responsibility to make the flow of the

organization smooth in terms of management of company's resources. When the finance team

provide budegt to the management team they ensure to provide financial report which help the

management team to spend the money accordingly.

Net income= (revenue-expense)

Cash flow statement: cash flow statements means the statements which highlight the flow of the

cash in the business organization, this cash flow statements provide clear details and information

to the investors and the people of the to understand the ability of the company to pay the cash

and the cash available with the company. The cash flow statements allow all the stakeholders and

the investors of the company to view the performance of the operation of the company. These

statements help investor to understand that from where the cash is coming from and how

company is utilizing the money.

Financial report concept:

Financial report is the end and complete result of the business organization, this financial

report have various purpose and are been designed to provide all the important and crucial

financial details and information. Financial report is been analysed by the stakeholder and people

who are been connected to the company (Lasher, 2016). When the business organization keep

the report in a perfect manner then they get the idea to plan the up coming financial things of the

business such as to set the budget and other finance related things. If the business organization

deals in the public, then they have to keep maintain the report every year to show the pubic and

the stakeholder about the performance of the company. Financial report help company to

communicate with the people by publishing their financial statements which show the stability

and performance. There are certain purpose of financial reporting such as;

Investment decision-making: stakeholder and the people who are interested in the company and

want to invest in it always prefer financial report which provide them all the necessary

information such as the profitability and growth rate of the company. Investment are been done

by various investors such as stakeholders, public and employees of the company.

Managing accountability: the financial report provide management team a clear and perfect

details and the information of the stability and growth of the company. The management team,

ask finance team to provide financial report to make future plan and management strategies

(Penman, 2016). The management team have the responsibility to make the flow of the

organization smooth in terms of management of company's resources. When the finance team

provide budegt to the management team they ensure to provide financial report which help the

management team to spend the money accordingly.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

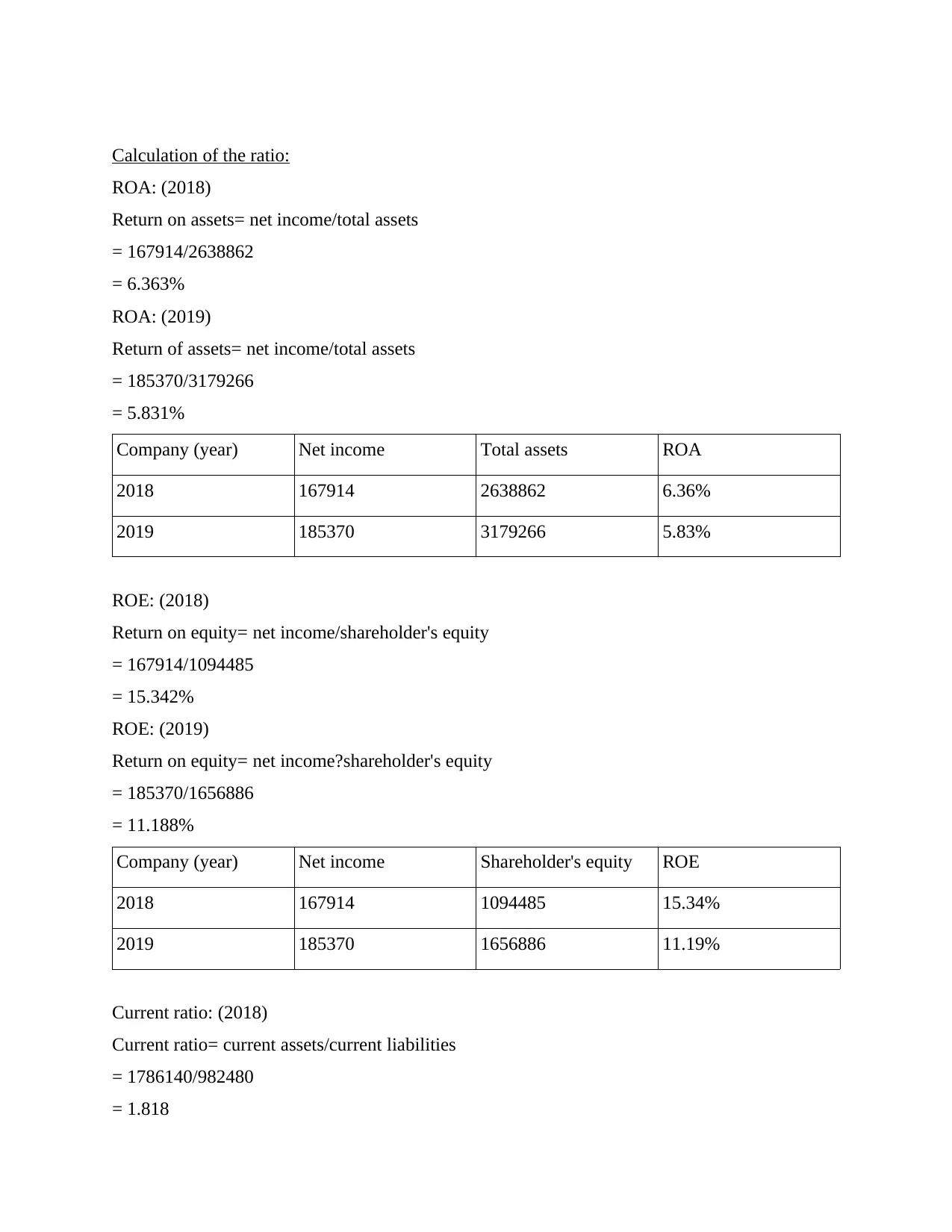

Calculation of the ratio:

ROA: (2018)

Return on assets= net income/total assets

= 167914/2638862

= 6.363%

ROA: (2019)

Return of assets= net income/total assets

= 185370/3179266

= 5.831%

Company (year) Net income Total assets ROA

2018 167914 2638862 6.36%

2019 185370 3179266 5.83%

ROE: (2018)

Return on equity= net income/shareholder's equity

= 167914/1094485

= 15.342%

ROE: (2019)

Return on equity= net income?shareholder's equity

= 185370/1656886

= 11.188%

Company (year) Net income Shareholder's equity ROE

2018 167914 1094485 15.34%

2019 185370 1656886 11.19%

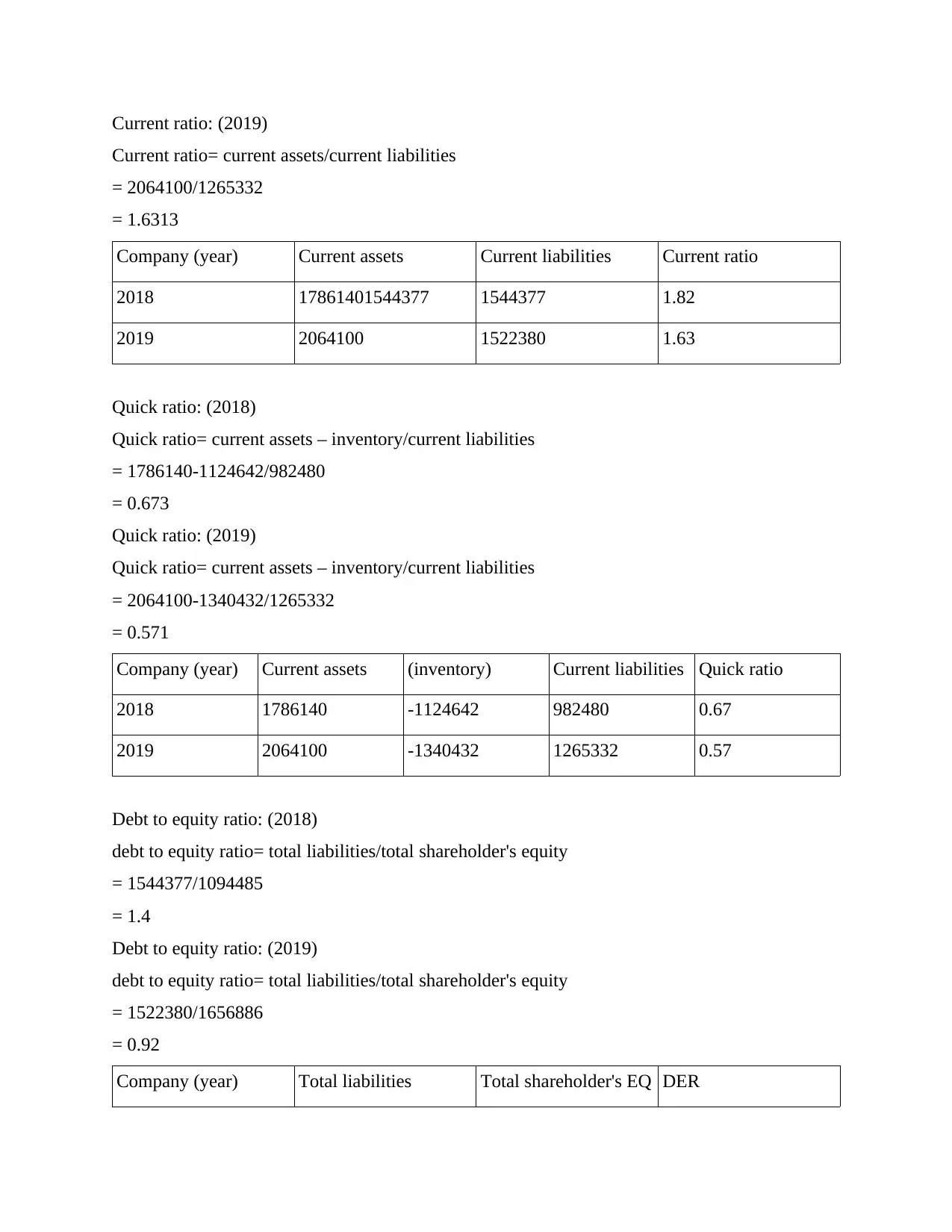

Current ratio: (2018)

Current ratio= current assets/current liabilities

= 1786140/982480

= 1.818

ROA: (2018)

Return on assets= net income/total assets

= 167914/2638862

= 6.363%

ROA: (2019)

Return of assets= net income/total assets

= 185370/3179266

= 5.831%

Company (year) Net income Total assets ROA

2018 167914 2638862 6.36%

2019 185370 3179266 5.83%

ROE: (2018)

Return on equity= net income/shareholder's equity

= 167914/1094485

= 15.342%

ROE: (2019)

Return on equity= net income?shareholder's equity

= 185370/1656886

= 11.188%

Company (year) Net income Shareholder's equity ROE

2018 167914 1094485 15.34%

2019 185370 1656886 11.19%

Current ratio: (2018)

Current ratio= current assets/current liabilities

= 1786140/982480

= 1.818

Current ratio: (2019)

Current ratio= current assets/current liabilities

= 2064100/1265332

= 1.6313

Company (year) Current assets Current liabilities Current ratio

2018 17861401544377 1544377 1.82

2019 2064100 1522380 1.63

Quick ratio: (2018)

Quick ratio= current assets – inventory/current liabilities

= 1786140-1124642/982480

= 0.673

Quick ratio: (2019)

Quick ratio= current assets – inventory/current liabilities

= 2064100-1340432/1265332

= 0.571

Company (year) Current assets (inventory) Current liabilities Quick ratio

2018 1786140 -1124642 982480 0.67

2019 2064100 -1340432 1265332 0.57

Debt to equity ratio: (2018)

debt to equity ratio= total liabilities/total shareholder's equity

= 1544377/1094485

= 1.4

Debt to equity ratio: (2019)

debt to equity ratio= total liabilities/total shareholder's equity

= 1522380/1656886

= 0.92

Company (year) Total liabilities Total shareholder's EQ DER

Current ratio= current assets/current liabilities

= 2064100/1265332

= 1.6313

Company (year) Current assets Current liabilities Current ratio

2018 17861401544377 1544377 1.82

2019 2064100 1522380 1.63

Quick ratio: (2018)

Quick ratio= current assets – inventory/current liabilities

= 1786140-1124642/982480

= 0.673

Quick ratio: (2019)

Quick ratio= current assets – inventory/current liabilities

= 2064100-1340432/1265332

= 0.571

Company (year) Current assets (inventory) Current liabilities Quick ratio

2018 1786140 -1124642 982480 0.67

2019 2064100 -1340432 1265332 0.57

Debt to equity ratio: (2018)

debt to equity ratio= total liabilities/total shareholder's equity

= 1544377/1094485

= 1.4

Debt to equity ratio: (2019)

debt to equity ratio= total liabilities/total shareholder's equity

= 1522380/1656886

= 0.92

Company (year) Total liabilities Total shareholder's EQ DER

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

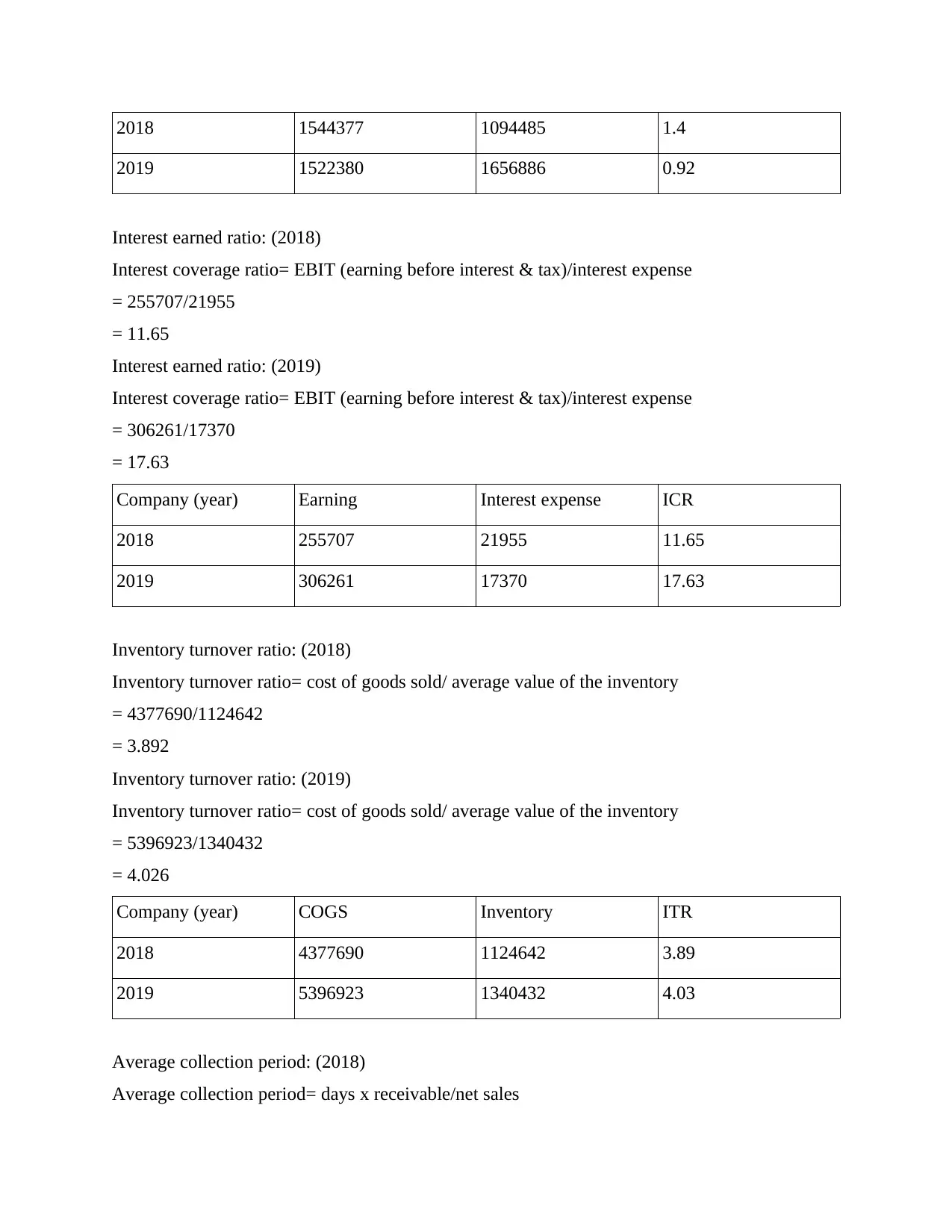

2018 1544377 1094485 1.4

2019 1522380 1656886 0.92

Interest earned ratio: (2018)

Interest coverage ratio= EBIT (earning before interest & tax)/interest expense

= 255707/21955

= 11.65

Interest earned ratio: (2019)

Interest coverage ratio= EBIT (earning before interest & tax)/interest expense

= 306261/17370

= 17.63

Company (year) Earning Interest expense ICR

2018 255707 21955 11.65

2019 306261 17370 17.63

Inventory turnover ratio: (2018)

Inventory turnover ratio= cost of goods sold/ average value of the inventory

= 4377690/1124642

= 3.892

Inventory turnover ratio: (2019)

Inventory turnover ratio= cost of goods sold/ average value of the inventory

= 5396923/1340432

= 4.026

Company (year) COGS Inventory ITR

2018 4377690 1124642 3.89

2019 5396923 1340432 4.03

Average collection period: (2018)

Average collection period= days x receivable/net sales

2019 1522380 1656886 0.92

Interest earned ratio: (2018)

Interest coverage ratio= EBIT (earning before interest & tax)/interest expense

= 255707/21955

= 11.65

Interest earned ratio: (2019)

Interest coverage ratio= EBIT (earning before interest & tax)/interest expense

= 306261/17370

= 17.63

Company (year) Earning Interest expense ICR

2018 255707 21955 11.65

2019 306261 17370 17.63

Inventory turnover ratio: (2018)

Inventory turnover ratio= cost of goods sold/ average value of the inventory

= 4377690/1124642

= 3.892

Inventory turnover ratio: (2019)

Inventory turnover ratio= cost of goods sold/ average value of the inventory

= 5396923/1340432

= 4.026

Company (year) COGS Inventory ITR

2018 4377690 1124642 3.89

2019 5396923 1340432 4.03

Average collection period: (2018)

Average collection period= days x receivable/net sales

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

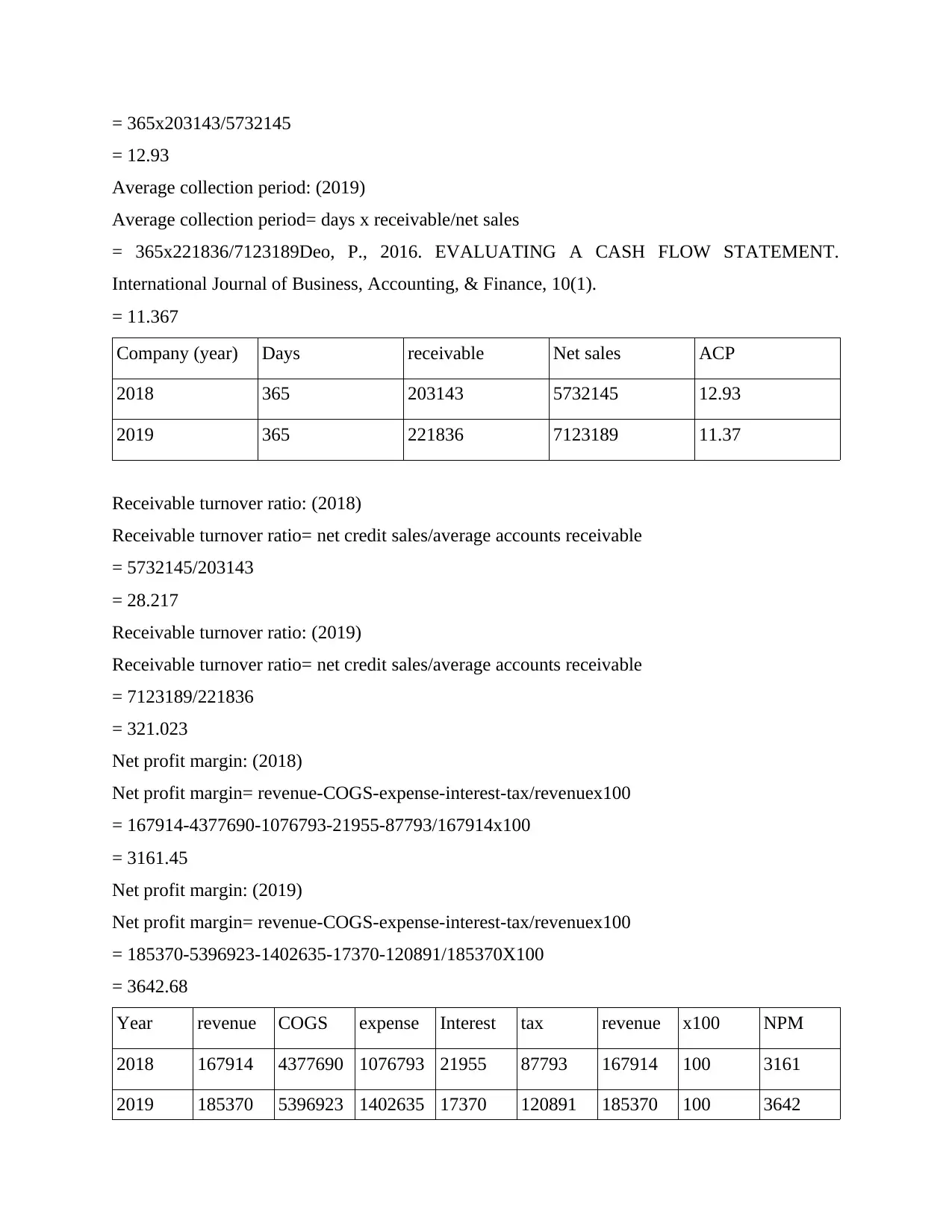

= 365x203143/5732145

= 12.93

Average collection period: (2019)

Average collection period= days x receivable/net sales

= 365x221836/7123189Deo, P., 2016. EVALUATING A CASH FLOW STATEMENT.

International Journal of Business, Accounting, & Finance, 10(1).

= 11.367

Company (year) Days receivable Net sales ACP

2018 365 203143 5732145 12.93

2019 365 221836 7123189 11.37

Receivable turnover ratio: (2018)

Receivable turnover ratio= net credit sales/average accounts receivable

= 5732145/203143

= 28.217

Receivable turnover ratio: (2019)

Receivable turnover ratio= net credit sales/average accounts receivable

= 7123189/221836

= 321.023

Net profit margin: (2018)

Net profit margin= revenue-COGS-expense-interest-tax/revenuex100

= 167914-4377690-1076793-21955-87793/167914x100

= 3161.45

Net profit margin: (2019)

Net profit margin= revenue-COGS-expense-interest-tax/revenuex100

= 185370-5396923-1402635-17370-120891/185370X100

= 3642.68

Year revenue COGS expense Interest tax revenue x100 NPM

2018 167914 4377690 1076793 21955 87793 167914 100 3161

2019 185370 5396923 1402635 17370 120891 185370 100 3642

= 12.93

Average collection period: (2019)

Average collection period= days x receivable/net sales

= 365x221836/7123189Deo, P., 2016. EVALUATING A CASH FLOW STATEMENT.

International Journal of Business, Accounting, & Finance, 10(1).

= 11.367

Company (year) Days receivable Net sales ACP

2018 365 203143 5732145 12.93

2019 365 221836 7123189 11.37

Receivable turnover ratio: (2018)

Receivable turnover ratio= net credit sales/average accounts receivable

= 5732145/203143

= 28.217

Receivable turnover ratio: (2019)

Receivable turnover ratio= net credit sales/average accounts receivable

= 7123189/221836

= 321.023

Net profit margin: (2018)

Net profit margin= revenue-COGS-expense-interest-tax/revenuex100

= 167914-4377690-1076793-21955-87793/167914x100

= 3161.45

Net profit margin: (2019)

Net profit margin= revenue-COGS-expense-interest-tax/revenuex100

= 185370-5396923-1402635-17370-120891/185370X100

= 3642.68

Year revenue COGS expense Interest tax revenue x100 NPM

2018 167914 4377690 1076793 21955 87793 167914 100 3161

2019 185370 5396923 1402635 17370 120891 185370 100 3642

CONCLUSION

In this report we have discussed financial accounting of the business organization. This

report discuss general accounting principles which include all the ten principles such as

principles of regularity, principles of consistency and other which help the company in basic

accounting. Later in this report we have identified the users of financial statements, these users

are the people who are connected to the company. These users are owner, investment analysts

and manager. This financial report allow these users to make the decision regarding the company

and its betterment. Later in this report we have discusses how financial statements help user to

make decision in regarding the company and the business organization. Later in this report

understand the purpose of financial statements and how third party of the company use these

statements, these third parties are loan creditors and trade creditors. Later we have discussed the

components of financial statements and later we have discussed financial reporting concept. At

last we have discussed and calculated various ratio.

In this report we have discussed financial accounting of the business organization. This

report discuss general accounting principles which include all the ten principles such as

principles of regularity, principles of consistency and other which help the company in basic

accounting. Later in this report we have identified the users of financial statements, these users

are the people who are connected to the company. These users are owner, investment analysts

and manager. This financial report allow these users to make the decision regarding the company

and its betterment. Later in this report we have discusses how financial statements help user to

make decision in regarding the company and the business organization. Later in this report

understand the purpose of financial statements and how third party of the company use these

statements, these third parties are loan creditors and trade creditors. Later we have discussed the

components of financial statements and later we have discussed financial reporting concept. At

last we have discussed and calculated various ratio.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.