M5X01922 Financial Management: Hotel Industry Budgeting Report

VerifiedAdded on 2023/01/16

|7

|1177

|55

Report

AI Summary

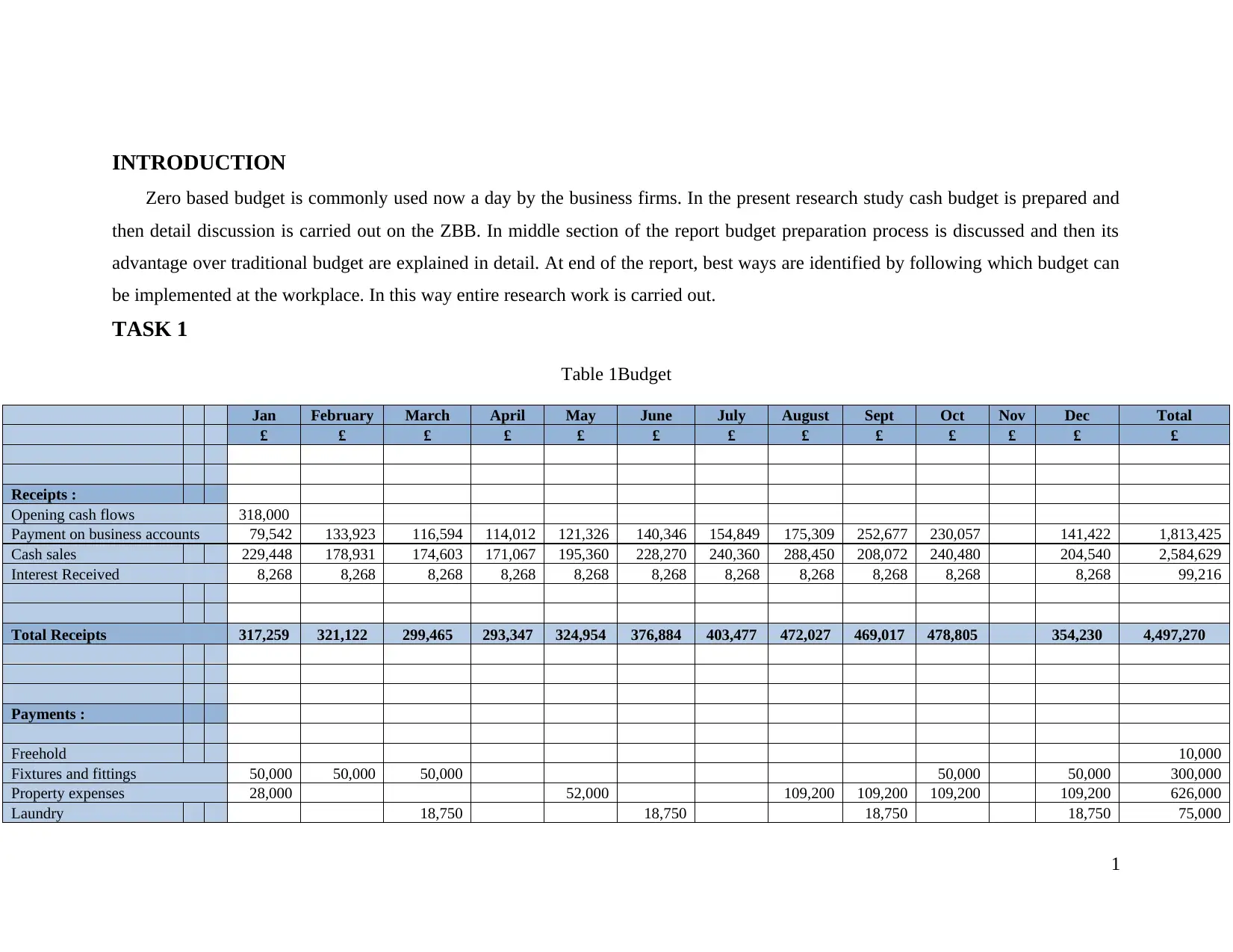

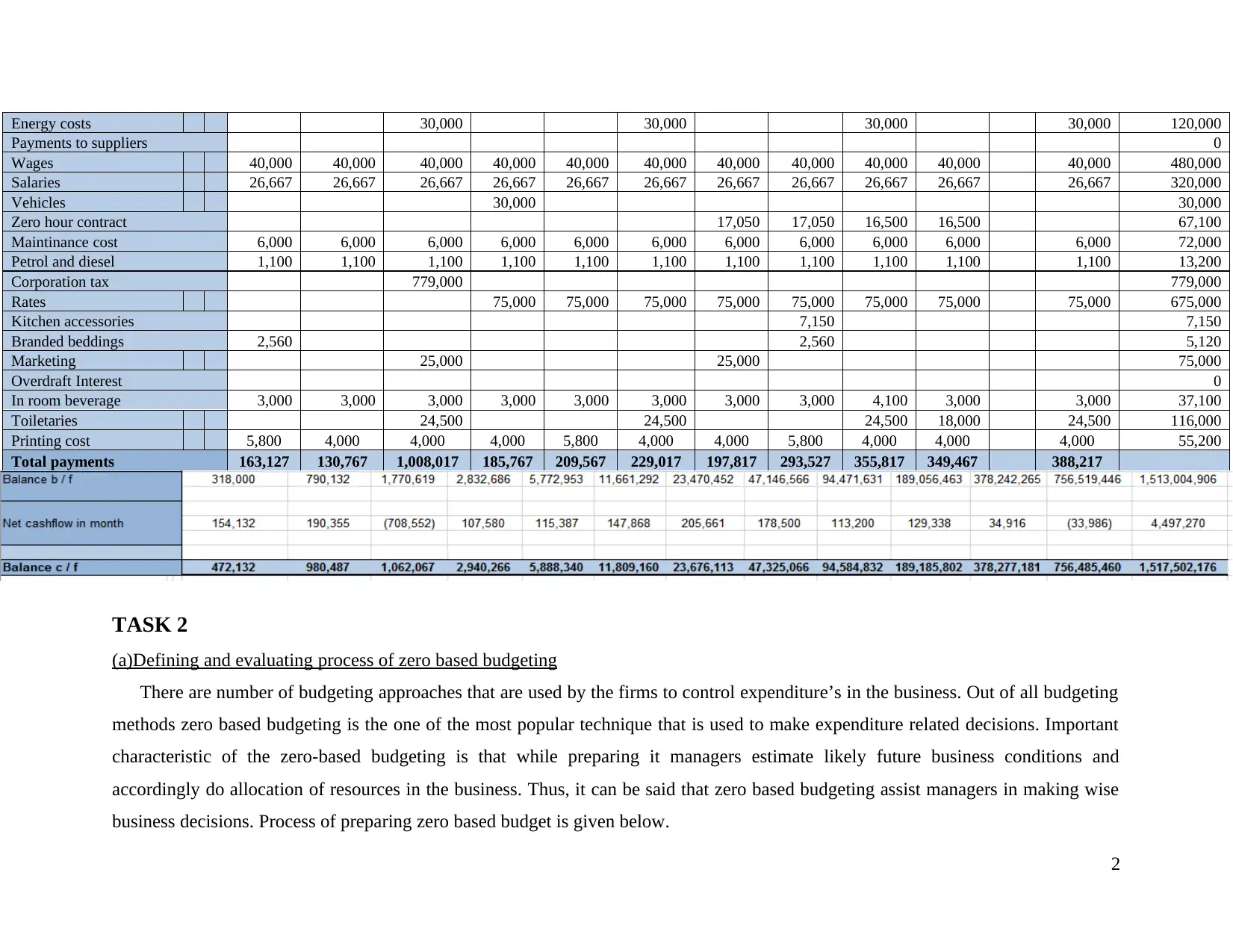

This report, focusing on financial management within the hotel industry, provides a detailed analysis of budgeting techniques. It begins with the preparation of a cash budget, followed by an in-depth discussion of zero-based budgeting (ZBB). The report defines ZBB, outlines its process, and compares its advantages to traditional budgeting methods. Furthermore, it explores effective strategies for ZBB implementation within an organization. The document includes a comprehensive cash budget table and concludes with key takeaways for improved financial planning and performance evaluation in the hotel industry. The report draws on several academic sources to support its analysis.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.