University Financial Management 1: Investment Proposal Analysis Report

VerifiedAdded on 2023/05/29

|29

|4738

|108

Report

AI Summary

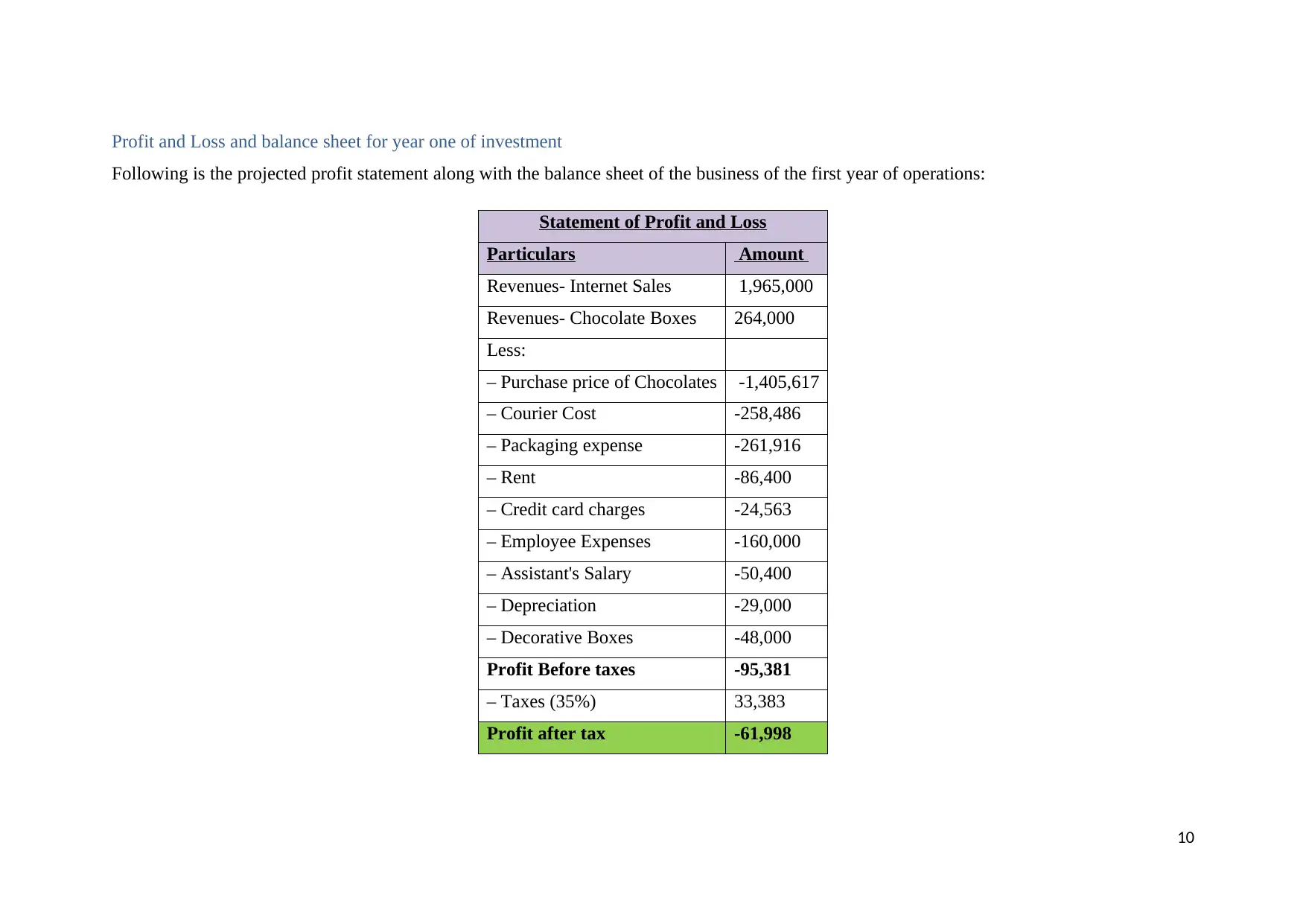

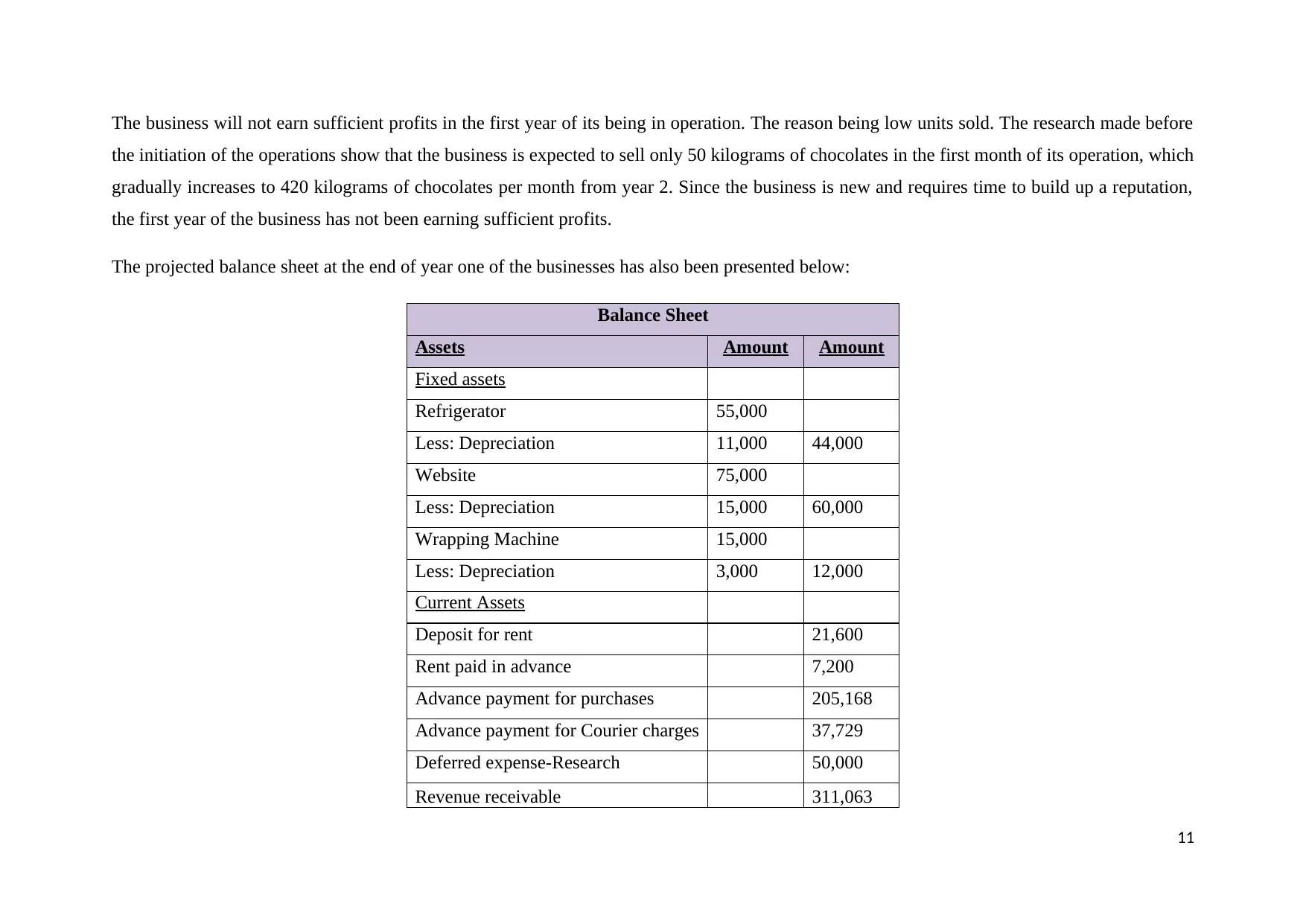

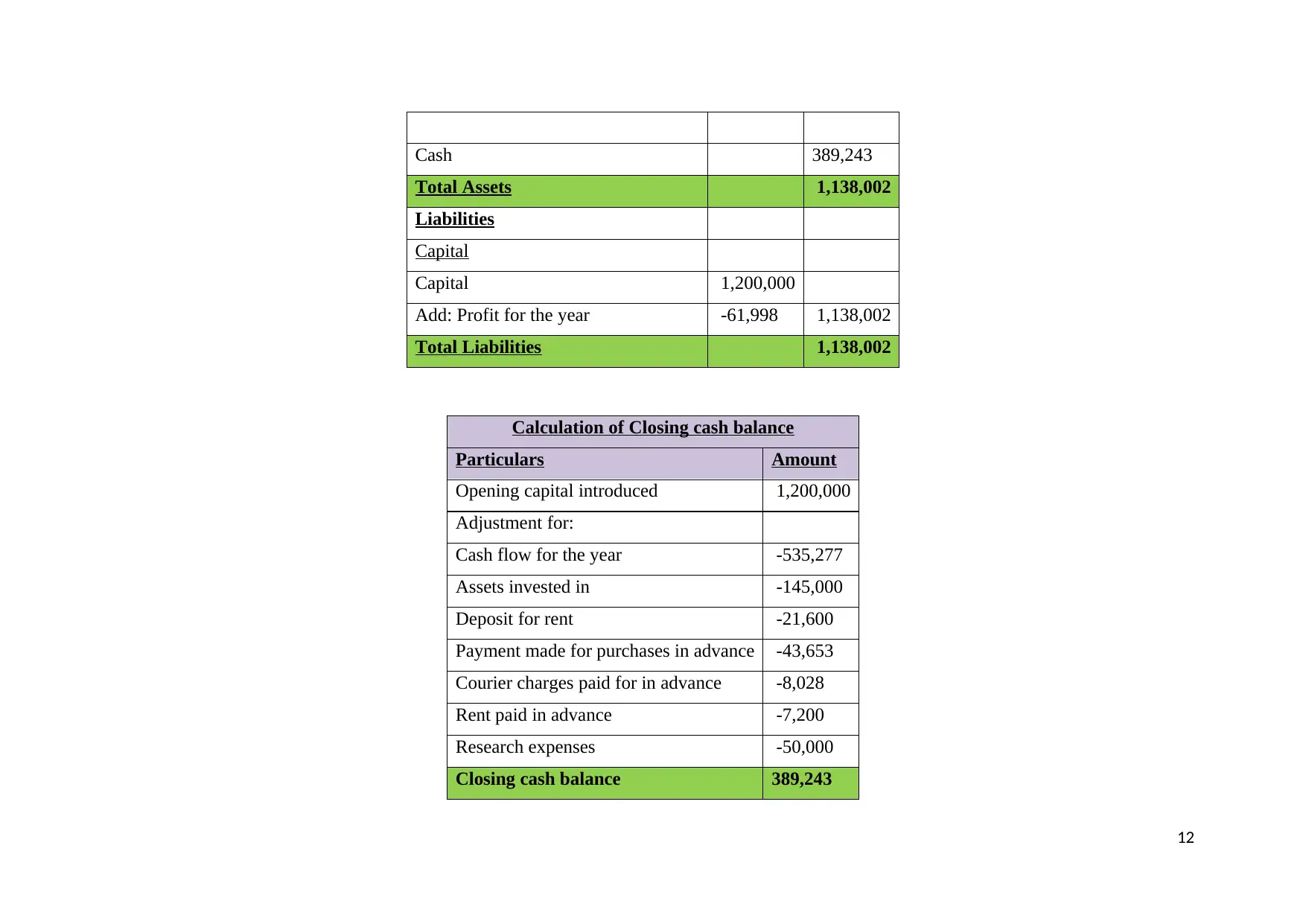

This report provides a comprehensive financial analysis of an investment proposal for a gourmet chocolate retail business. It includes an executive summary, introduction, and detailed assumptions. The analysis encompasses break-even analysis, projecting both internet sales and chocolate box sales, and presents a profit and loss statement and balance sheet for the first year of operations. The report also includes monthly cash flow projections, an annual cash flow statement, and a discussion of initial investments. Furthermore, it incorporates financial analysis, sensitivity analysis, and non-financial factors to be considered. The report concludes with reflections, conclusions, and recommendations regarding the investment proposal, assessing its viability and potential profitability based on the provided financial data and assumptions. The analysis includes key financial tools to make recommendations on whether to accept or reject the investment proposal.

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.