S2 2018 FIN20014: KKP Ltd Capital Budgeting and Financial Report

VerifiedAdded on 2023/06/10

|16

|2453

|303

Report

AI Summary

This report provides a detailed capital budgeting analysis for KKP Ltd, focusing on the potential launch of a new proximity sensor for the food industry. The analysis includes an executive summary, introduction to capital budgeting techniques, and a comprehensive examination of the project's financial aspects using both quantitative and qualitative methods. Quantitative tools such as Net Present Value (NPV), Internal Rate of Return (IRR), payback period, discounted payback period, and profitability index are employed to evaluate the project's feasibility. The report also considers qualitative factors like environmental and ethical concerns. Based on the financial findings, the report recommends against the project due to its negative NPV, IRR, and low profitability index, along with a payback period exceeding the machine's lifespan. Further recommendations involve increasing sales to improve profitability. The conclusion emphasizes the importance of thorough investment appraisal for sound financial decision-making, considering both financial and non-financial aspects.

RUNNING HEAD: FINANCIAL MANAGEMENT

capital budgeting

capital budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management 1

Executive Summary

This report provides a brief summary about the applications of tools and techniques of capital

budgeting into business. The first part of the report deals with an overview of such methods

along with the introduction of the company named as KKP Ltd. The second part focuses on

the findings of the research that include both the quantitative and qualitative approaches. All

the findings are been clearly stated in that part which, forms the basis of decision for the

managers of the company related to the investments. The third part deals with the

recommendations and justifications given on the basis of the analysis or evaluation performed

in the report. In the last a conclusion is been provided which closes all the findings and

justifications of the analysis done in the report.

Executive Summary

This report provides a brief summary about the applications of tools and techniques of capital

budgeting into business. The first part of the report deals with an overview of such methods

along with the introduction of the company named as KKP Ltd. The second part focuses on

the findings of the research that include both the quantitative and qualitative approaches. All

the findings are been clearly stated in that part which, forms the basis of decision for the

managers of the company related to the investments. The third part deals with the

recommendations and justifications given on the basis of the analysis or evaluation performed

in the report. In the last a conclusion is been provided which closes all the findings and

justifications of the analysis done in the report.

Financial management 2

Contents

Introduction...........................................................................................................................................3

Findings.................................................................................................................................................4

Quantitative.......................................................................................................................................4

Qualitative.........................................................................................................................................6

Recommendations and Justifications.....................................................................................................6

Further Recommendations.....................................................................................................................7

Conclusion.............................................................................................................................................7

References.............................................................................................................................................8

Appendix...............................................................................................................................................9

Workings.............................................................................................................................................12

Contents

Introduction...........................................................................................................................................3

Findings.................................................................................................................................................4

Quantitative.......................................................................................................................................4

Qualitative.........................................................................................................................................6

Recommendations and Justifications.....................................................................................................6

Further Recommendations.....................................................................................................................7

Conclusion.............................................................................................................................................7

References.............................................................................................................................................8

Appendix...............................................................................................................................................9

Workings.............................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial management 3

Introduction

Capital budgeting is a process followed by the companies or organizations in order to

evaluate their investment projects and to take the related decisions. It is a concept which

consists of some methods that are been used by management for examining the proposals and

select the best alternative. These techniques allows the companies to choose the investment,

which is more feasible and profitable for the business. Making an investment related decision

is considered to be a challenging task for the management as it involves allocation and

application of business’s funds to the most viable and suitable project that is expected to give

high returns in future (Ahmed, 2013). Therefore, it is very important for the organization to

critically evaluate a project from all its financial aspects in order to take appropriate

decisions. There are several reasons why companies go for capital budgeting techniques. Out

of them, some are to know about the most profitable capital expenditure, to determine the

returns derived by replacing old and existing asset and to select the best proposal among the

available ones. In addition, the methods help in identifying the amount required for making

the investment along with the sources from where the funds can be raised (Gotze, Northcott

& Schuster, 2016).

KKP Ltd is leading company engaged in the instrumentation and automation business. The

executives and the directors of the corporation are looking forward to launch a new type of

proximity sensor for the food industry. For that, the organization has incurred a lot of money

in conducting a market research along with the start-up cost of building the new machinery.

The company has adopted some quantitative and qualitative techniques to evaluate this

proposal. Quantitative tools include capital budgeting methods such as NPV, payback period,

profitability index and IRR. On the other side, qualitative tools comprises of some non-

financial issues that are been discussed in the later part of the report.

Introduction

Capital budgeting is a process followed by the companies or organizations in order to

evaluate their investment projects and to take the related decisions. It is a concept which

consists of some methods that are been used by management for examining the proposals and

select the best alternative. These techniques allows the companies to choose the investment,

which is more feasible and profitable for the business. Making an investment related decision

is considered to be a challenging task for the management as it involves allocation and

application of business’s funds to the most viable and suitable project that is expected to give

high returns in future (Ahmed, 2013). Therefore, it is very important for the organization to

critically evaluate a project from all its financial aspects in order to take appropriate

decisions. There are several reasons why companies go for capital budgeting techniques. Out

of them, some are to know about the most profitable capital expenditure, to determine the

returns derived by replacing old and existing asset and to select the best proposal among the

available ones. In addition, the methods help in identifying the amount required for making

the investment along with the sources from where the funds can be raised (Gotze, Northcott

& Schuster, 2016).

KKP Ltd is leading company engaged in the instrumentation and automation business. The

executives and the directors of the corporation are looking forward to launch a new type of

proximity sensor for the food industry. For that, the organization has incurred a lot of money

in conducting a market research along with the start-up cost of building the new machinery.

The company has adopted some quantitative and qualitative techniques to evaluate this

proposal. Quantitative tools include capital budgeting methods such as NPV, payback period,

profitability index and IRR. On the other side, qualitative tools comprises of some non-

financial issues that are been discussed in the later part of the report.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management 4

Findings

In order to evaluate the investment proposal of KKP, the managers of the organization has

used certain quantitative and qualitative methods that are been discussed below. Based on

such findings, the organization will decide whether to go further with the project or not.

Quantitative

Various investment appraisal methods are been used in this approach. These techniques

measures a project from all the financial aspects such as profitability, feasibility and viability.

They are as follows:

1. Payback period

It is the simplest method used for evaluating an investment project. It identifies the number of

years taken by a project to recoup its initial investment. In other words, it reflects the time-

period within which the proposal will recover its initial outlay of cash. The payback period

calculated so that management can have an idea about the sustainability of the project and

can decide that whether it will be profitable to take this project further or not. Generally,

companies has a standard payback period against which the calculated one is compared. If the

standard one is more than the calculated that means the project should be accepted and must

be rejected in case of vice versa (Atrill & McLaney, 2009).

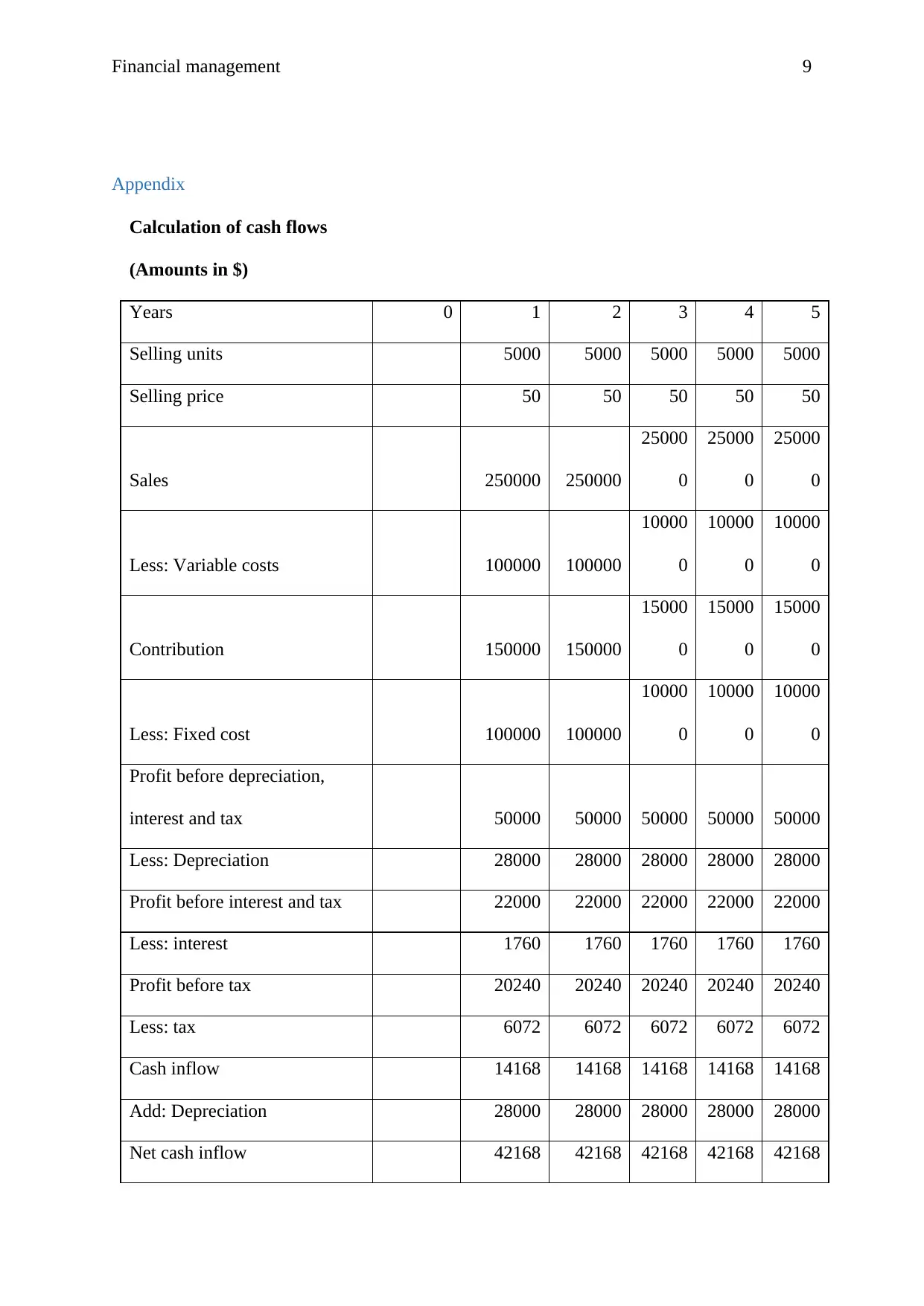

Refer to Appendix, it is observed that in case of KKP Ltd., when calculated the payback

period is more than the useful life of the machine. This means the machine is not capable

enough to generate cash inflows throughout its entire life of five years. All the cash flows are

in negative, which means the project should not be accepted, as it will take many more years

to recoup the initial investment and to generate profitable cash inflows in future. Moreover,

the targeted value for the payback period is 3 years and the calculated one is way more than

that. Therefore, it will be better to reject the proposal.

Findings

In order to evaluate the investment proposal of KKP, the managers of the organization has

used certain quantitative and qualitative methods that are been discussed below. Based on

such findings, the organization will decide whether to go further with the project or not.

Quantitative

Various investment appraisal methods are been used in this approach. These techniques

measures a project from all the financial aspects such as profitability, feasibility and viability.

They are as follows:

1. Payback period

It is the simplest method used for evaluating an investment project. It identifies the number of

years taken by a project to recoup its initial investment. In other words, it reflects the time-

period within which the proposal will recover its initial outlay of cash. The payback period

calculated so that management can have an idea about the sustainability of the project and

can decide that whether it will be profitable to take this project further or not. Generally,

companies has a standard payback period against which the calculated one is compared. If the

standard one is more than the calculated that means the project should be accepted and must

be rejected in case of vice versa (Atrill & McLaney, 2009).

Refer to Appendix, it is observed that in case of KKP Ltd., when calculated the payback

period is more than the useful life of the machine. This means the machine is not capable

enough to generate cash inflows throughout its entire life of five years. All the cash flows are

in negative, which means the project should not be accepted, as it will take many more years

to recoup the initial investment and to generate profitable cash inflows in future. Moreover,

the targeted value for the payback period is 3 years and the calculated one is way more than

that. Therefore, it will be better to reject the proposal.

Financial management 5

2. Discounted payback period

Another capital budgeting procedure that measures the profitability of a project. Unlike the

simple payback period, it uses the discounted cash flows to calculate the amount of time

required to breakeven from the initial capital expenditure. As per the calculation done and

shown in appendix, it is observed that by this method also the project of KPP Ltd is not

feasible as it is not able to recuperate the funds invested in it initially, within the period of

five years (Baker & English, 2011). In addition, the calculated DPBP is more than the

targeted period of 1.5 years. So, the project is not suitable.

3. Net present value

It is the most commonly used method, which measures the profitability of a project. It is the

amount, which is in excess of the present values of cash inflow over the PV of cash outflow.

It is the most reliable and authentic technique used by the managers for evaluating their

investment proposals. The decision rule of NPV is that accept the project only when the net

present value of that particular proposal is greater than zero and is positive. This implies that

the projected earnings generated by the project are more than the anticipated costs. If the

NPV is less than zero than it become negative and it is better to reject the proposal. It takes

into account the concept of time value of money (Bierman & Smidt, 2012).

Referring to Appendix, the NPV of building new machinery is negative which means the

cash inflows generated in the coming five years are less than the initial investment made.

This indicates that the project is not profitable for the company as for the next five years;

KKP Ltd will be facing losses only. The project has a negative NPV of -$474204.81 which

means the project will not give positive returns in its whole life of five years.

4. Internal Rate of return

2. Discounted payback period

Another capital budgeting procedure that measures the profitability of a project. Unlike the

simple payback period, it uses the discounted cash flows to calculate the amount of time

required to breakeven from the initial capital expenditure. As per the calculation done and

shown in appendix, it is observed that by this method also the project of KPP Ltd is not

feasible as it is not able to recuperate the funds invested in it initially, within the period of

five years (Baker & English, 2011). In addition, the calculated DPBP is more than the

targeted period of 1.5 years. So, the project is not suitable.

3. Net present value

It is the most commonly used method, which measures the profitability of a project. It is the

amount, which is in excess of the present values of cash inflow over the PV of cash outflow.

It is the most reliable and authentic technique used by the managers for evaluating their

investment proposals. The decision rule of NPV is that accept the project only when the net

present value of that particular proposal is greater than zero and is positive. This implies that

the projected earnings generated by the project are more than the anticipated costs. If the

NPV is less than zero than it become negative and it is better to reject the proposal. It takes

into account the concept of time value of money (Bierman & Smidt, 2012).

Referring to Appendix, the NPV of building new machinery is negative which means the

cash inflows generated in the coming five years are less than the initial investment made.

This indicates that the project is not profitable for the company as for the next five years;

KKP Ltd will be facing losses only. The project has a negative NPV of -$474204.81 which

means the project will not give positive returns in its whole life of five years.

4. Internal Rate of return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial management 6

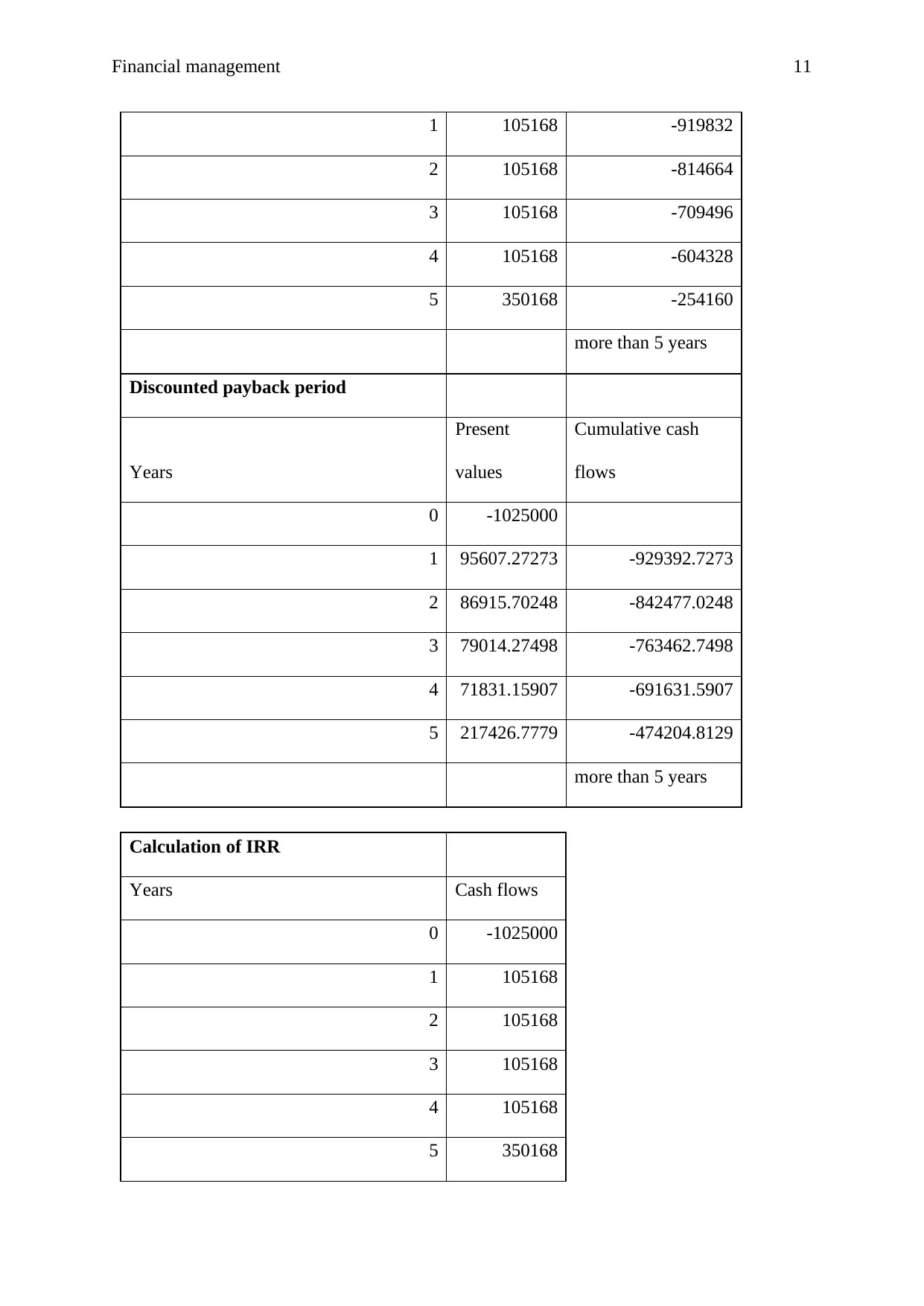

It is a rate where the NPV is zero, which means the PV of cash outflow is equal to PV of cash

inflow. Generally, projects having high IRR are considered more desirable and are acceptable

if the rate is more than the required cost of capital. An IRR can also be negative in case where

the cash flows are less than the initial outlay. Negative IRR is the rate at which the project or

the investment made is losing money (Brigham & Houston, 2015).

The proposal of building a new machinery gives KKP an IRR of -7%. (Refer appendix). This

is due to the negative NPV of the project. It indicates that required rate of return of the

proposal is more than its IRR. Therefore, the project should be rejected.

5. Profitability Index

It identifies the relationship between the cost and benefits of a project by calculating an

index. If PI is equal to one or less than one, then it means that present values of the proposal

are less than its initial investment. In case of KKP Ltd., the PI is 0.54 that is less than one and

indicates that the project is not feasible.

Qualitative

There are some non-financial issues also which are to be considered by KKP Ltd while

making investment in building a new machinery. These include the environmental concerns

as the decision of such capital investment can have varying degree of impact on the

environment. Before launching the sensor, the management must take into account its effects

on the environment. Apart from this, some ethical considerations like safety of employee and

local employment can be affected by investing into a new machinery, irrespective of the

financial benefits.

Recommendations and Justifications

From the above discussed issues, it is recommended that the company should not go for this

project as it has negative NPV, IRR and a low profitability index. Moreover, the discounted

It is a rate where the NPV is zero, which means the PV of cash outflow is equal to PV of cash

inflow. Generally, projects having high IRR are considered more desirable and are acceptable

if the rate is more than the required cost of capital. An IRR can also be negative in case where

the cash flows are less than the initial outlay. Negative IRR is the rate at which the project or

the investment made is losing money (Brigham & Houston, 2015).

The proposal of building a new machinery gives KKP an IRR of -7%. (Refer appendix). This

is due to the negative NPV of the project. It indicates that required rate of return of the

proposal is more than its IRR. Therefore, the project should be rejected.

5. Profitability Index

It identifies the relationship between the cost and benefits of a project by calculating an

index. If PI is equal to one or less than one, then it means that present values of the proposal

are less than its initial investment. In case of KKP Ltd., the PI is 0.54 that is less than one and

indicates that the project is not feasible.

Qualitative

There are some non-financial issues also which are to be considered by KKP Ltd while

making investment in building a new machinery. These include the environmental concerns

as the decision of such capital investment can have varying degree of impact on the

environment. Before launching the sensor, the management must take into account its effects

on the environment. Apart from this, some ethical considerations like safety of employee and

local employment can be affected by investing into a new machinery, irrespective of the

financial benefits.

Recommendations and Justifications

From the above discussed issues, it is recommended that the company should not go for this

project as it has negative NPV, IRR and a low profitability index. Moreover, the discounted

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management 7

and non-discounted payback period of the project are more than its entire life. This means

that the proposal is not able to generate cash flows that are enough for recovering the initial

outlay made. Moreover, it is not profitable as the present value of future cash inflows is less

than the PV of cash outflow. Furthermore, making investment in it can affect the environment

of the company and may affect the employees. However, the recommendations can be

justified by looking at the quantitative methods used for the evaluation. The tools used

provide the most reliable basis for taking decisions related to capital investments. Overall, the

company should avoid investing in the proposal, as it will not be profitable.

Further Recommendations

Apart from the above given recommendation, it can be further recommended to the company

that in order to generate profits it should increase the number of units sold per year. This will

led to the inflow of cash in the business and recover the reduction of $17,000 in the sale of

gas analysers that happened due to the launch of proximity sensor. If the net cash inflows

increases, the present value of them will also rise which ultimately make the project feasible

and profitable. So in order to launch the proximity sensors in the food industry, the company

needs to increase its sales as reduction in the same have a negative effect on the new venture.

Conclusion

From the above report, it is concluded that it is very important for the management to

consider the authentic investment appraisal methods to evaluate the proposal before making

an investment in it. Overall, it is very essential for the companies to consider all the financial

and non-financial aspects of the investment project while taking the decision related to the

feasibility and profitability of the proposal.

and non-discounted payback period of the project are more than its entire life. This means

that the proposal is not able to generate cash flows that are enough for recovering the initial

outlay made. Moreover, it is not profitable as the present value of future cash inflows is less

than the PV of cash outflow. Furthermore, making investment in it can affect the environment

of the company and may affect the employees. However, the recommendations can be

justified by looking at the quantitative methods used for the evaluation. The tools used

provide the most reliable basis for taking decisions related to capital investments. Overall, the

company should avoid investing in the proposal, as it will not be profitable.

Further Recommendations

Apart from the above given recommendation, it can be further recommended to the company

that in order to generate profits it should increase the number of units sold per year. This will

led to the inflow of cash in the business and recover the reduction of $17,000 in the sale of

gas analysers that happened due to the launch of proximity sensor. If the net cash inflows

increases, the present value of them will also rise which ultimately make the project feasible

and profitable. So in order to launch the proximity sensors in the food industry, the company

needs to increase its sales as reduction in the same have a negative effect on the new venture.

Conclusion

From the above report, it is concluded that it is very important for the management to

consider the authentic investment appraisal methods to evaluate the proposal before making

an investment in it. Overall, it is very essential for the companies to consider all the financial

and non-financial aspects of the investment project while taking the decision related to the

feasibility and profitability of the proposal.

Financial management 8

References

Ahmed, I.E. (2013). Factors determining the selection of capital budgeting

techniques. Journal of Finance and Investment Analysis, 2(2),77-88.

Atrill, P. &McLaney, E. (2009). Management accounting for decision makers (4th ed.).

England: Pearson Education.

Baker, H.K. &English, P. (2011). Capital Budgeting Valuation: Financial Analysis for

Today's Investment Projects. New Jersey: John Wiley & Sons.

Bierman Jr, H., &Smidt, S. (2012). The capital budgeting decision: economic analysis of

investment projects (9th ed.). New York: Routledge.

Brigham, E.F. &Houston, J.F. (2015). Fundamentals of Financial Management. Cengage

Learning.

Gotze, U., Northcott, D. &Schuster, P. (2016). INVESTMENT APPRAISAL (2nd ed.).

New York: SPRINGER-VERLAG BERLIN AN.

References

Ahmed, I.E. (2013). Factors determining the selection of capital budgeting

techniques. Journal of Finance and Investment Analysis, 2(2),77-88.

Atrill, P. &McLaney, E. (2009). Management accounting for decision makers (4th ed.).

England: Pearson Education.

Baker, H.K. &English, P. (2011). Capital Budgeting Valuation: Financial Analysis for

Today's Investment Projects. New Jersey: John Wiley & Sons.

Bierman Jr, H., &Smidt, S. (2012). The capital budgeting decision: economic analysis of

investment projects (9th ed.). New York: Routledge.

Brigham, E.F. &Houston, J.F. (2015). Fundamentals of Financial Management. Cengage

Learning.

Gotze, U., Northcott, D. &Schuster, P. (2016). INVESTMENT APPRAISAL (2nd ed.).

New York: SPRINGER-VERLAG BERLIN AN.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial management 9

Appendix

Calculation of cash flows

(Amounts in $)

Years 0 1 2 3 4 5

Selling units 5000 5000 5000 5000 5000

Selling price 50 50 50 50 50

Sales 250000 250000

25000

0

25000

0

25000

0

Less: Variable costs 100000 100000

10000

0

10000

0

10000

0

Contribution 150000 150000

15000

0

15000

0

15000

0

Less: Fixed cost 100000 100000

10000

0

10000

0

10000

0

Profit before depreciation,

interest and tax 50000 50000 50000 50000 50000

Less: Depreciation 28000 28000 28000 28000 28000

Profit before interest and tax 22000 22000 22000 22000 22000

Less: interest 1760 1760 1760 1760 1760

Profit before tax 20240 20240 20240 20240 20240

Less: tax 6072 6072 6072 6072 6072

Cash inflow 14168 14168 14168 14168 14168

Add: Depreciation 28000 28000 28000 28000 28000

Net cash inflow 42168 42168 42168 42168 42168

Appendix

Calculation of cash flows

(Amounts in $)

Years 0 1 2 3 4 5

Selling units 5000 5000 5000 5000 5000

Selling price 50 50 50 50 50

Sales 250000 250000

25000

0

25000

0

25000

0

Less: Variable costs 100000 100000

10000

0

10000

0

10000

0

Contribution 150000 150000

15000

0

15000

0

15000

0

Less: Fixed cost 100000 100000

10000

0

10000

0

10000

0

Profit before depreciation,

interest and tax 50000 50000 50000 50000 50000

Less: Depreciation 28000 28000 28000 28000 28000

Profit before interest and tax 22000 22000 22000 22000 22000

Less: interest 1760 1760 1760 1760 1760

Profit before tax 20240 20240 20240 20240 20240

Less: tax 6072 6072 6072 6072 6072

Cash inflow 14168 14168 14168 14168 14168

Add: Depreciation 28000 28000 28000 28000 28000

Net cash inflow 42168 42168 42168 42168 42168

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management 10

Cash outflow 1000000

Working capital changes 25000 25000

Reduction in production cost 80000 80000 80000 80000 80000

Reduction in sale -17000 -17000

-

17000

-

17000

-

17000

Sale of the machine

22000

0

Net cash flows 1025000 105168 105168

10516

8

10516

8

35016

8

Calculation of NPV

Years Cash flows pvf@10%

Present

values

0 -1025000 1 -1025000

1 105168 0.909090909 95607.27273

2 105168 0.826446281 86915.70248

3 105168 0.751314801 79014.27498

4 105168 0.683013455 71831.15907

5 350168 0.620921323 217426.7779

NPV -474204.81

calculation of payback period

Years Cash flows

Cumulative cash

flows

0 -1025000

Cash outflow 1000000

Working capital changes 25000 25000

Reduction in production cost 80000 80000 80000 80000 80000

Reduction in sale -17000 -17000

-

17000

-

17000

-

17000

Sale of the machine

22000

0

Net cash flows 1025000 105168 105168

10516

8

10516

8

35016

8

Calculation of NPV

Years Cash flows pvf@10%

Present

values

0 -1025000 1 -1025000

1 105168 0.909090909 95607.27273

2 105168 0.826446281 86915.70248

3 105168 0.751314801 79014.27498

4 105168 0.683013455 71831.15907

5 350168 0.620921323 217426.7779

NPV -474204.81

calculation of payback period

Years Cash flows

Cumulative cash

flows

0 -1025000

Financial management 11

1 105168 -919832

2 105168 -814664

3 105168 -709496

4 105168 -604328

5 350168 -254160

more than 5 years

Discounted payback period

Years

Present

values

Cumulative cash

flows

0 -1025000

1 95607.27273 -929392.7273

2 86915.70248 -842477.0248

3 79014.27498 -763462.7498

4 71831.15907 -691631.5907

5 217426.7779 -474204.8129

more than 5 years

Calculation of IRR

Years Cash flows

0 -1025000

1 105168

2 105168

3 105168

4 105168

5 350168

1 105168 -919832

2 105168 -814664

3 105168 -709496

4 105168 -604328

5 350168 -254160

more than 5 years

Discounted payback period

Years

Present

values

Cumulative cash

flows

0 -1025000

1 95607.27273 -929392.7273

2 86915.70248 -842477.0248

3 79014.27498 -763462.7498

4 71831.15907 -691631.5907

5 217426.7779 -474204.8129

more than 5 years

Calculation of IRR

Years Cash flows

0 -1025000

1 105168

2 105168

3 105168

4 105168

5 350168

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.