Financial Management of Nestle UK: Analysis and Evaluation

VerifiedAdded on 2020/01/06

|23

|8255

|1052

Report

AI Summary

This report provides a comprehensive analysis of the financial management of Nestle UK, examining its financial performance for the years 2013 and 2014. It delves into the importance of financial data, exploring both internal and external sources, and assessing the validity and reliability of the information. The report reviews Nestle UK's financial statements, including income statements, balance sheets, and cash flow statements, and compares its financial data with a competitor. It also analyzes key financial ratios, such as gross profit ratio and COGS, to evaluate the company's efficiency and profitability. Furthermore, the report addresses budget constraints, reviews financial data, and evaluates the impact of financial proposals on Nestle UK's objectives. The study highlights the significance of internal and external auditing in ensuring the accuracy and reliability of financial data, and how it is used for decision-making and strategic planning.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction:...............................................................................................................................1

Background of the Company:....................................................................................................1

A.C 1.1:-.................................................................................................................................2

A.C 1.4 Review and Question financial data.........................................................................4

A.C 1.2:-.................................................................................................................................5

A.C 1.3 Comparative analyses of financial data of Nestle:...................................................8

A.C 2.1:-...............................................................................................................................10

A.C 2.2:-...............................................................................................................................11

A.C 3.1:-...............................................................................................................................12

A.C 3.2:-...............................................................................................................................13

A.C 3.3:-...............................................................................................................................14

A.C:3.4:-...............................................................................................................................15

Conclusion:..............................................................................................................................15

REFERENCES.........................................................................................................................16

Introduction:...............................................................................................................................1

Background of the Company:....................................................................................................1

A.C 1.1:-.................................................................................................................................2

A.C 1.4 Review and Question financial data.........................................................................4

A.C 1.2:-.................................................................................................................................5

A.C 1.3 Comparative analyses of financial data of Nestle:...................................................8

A.C 2.1:-...............................................................................................................................10

A.C 2.2:-...............................................................................................................................11

A.C 3.1:-...............................................................................................................................12

A.C 3.2:-...............................................................................................................................13

A.C 3.3:-...............................................................................................................................14

A.C:3.4:-...............................................................................................................................15

Conclusion:..............................................................................................................................15

REFERENCES.........................................................................................................................16

Index of Tables

Table 1: Financial data of Nestle and its competitor..................................................................6

Table 2: Financial ratios for Nestle UK for 2014.......................................................................7

Table 3: Horizontal analysis of the Profit and loss statement..................................................10

Table 4: Cash Flow Statement..................................................................................................10

Table 5: Horizontal analysis of the Balance sheet statement...................................................11

Table 6: Variance calculation ..................................................................................................11

Table 7: Budgeted income statement.......................................................................................12

Table 8: Expansion Proposal information ...............................................................................16

Table 9: Pay back period calculation ......................................................................................16

Table 10: Net present value calculation ..................................................................................16

1

Table 1: Financial data of Nestle and its competitor..................................................................6

Table 2: Financial ratios for Nestle UK for 2014.......................................................................7

Table 3: Horizontal analysis of the Profit and loss statement..................................................10

Table 4: Cash Flow Statement..................................................................................................10

Table 5: Horizontal analysis of the Balance sheet statement...................................................11

Table 6: Variance calculation ..................................................................................................11

Table 7: Budgeted income statement.......................................................................................12

Table 8: Expansion Proposal information ...............................................................................16

Table 9: Pay back period calculation ......................................................................................16

Table 10: Net present value calculation ..................................................................................16

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction:

This task has been designed with the purpose of assessing the financial management of a

company. In this study, Nestle UK has been used as a case study. The financial management

of Nestle UK is assessed for the years 2013 and 2014 and their financial data is compared and

analysed. To understand the financial management in a better way, the researcher has made

an effort to identify methods for procuring budgets and analyse the impact of budget

constraints. In this study, the criteria on which proposals are judged for managing finance is

assessed and the outcomes of the mentioned proposals on objectives of Nestle UK are

evaluated.

Background of the Company:

Nestle UK is a subsidiary company of Nestle SA. It is the world’s best company on nutrition

as well as health. Nestle UK is a major player in the food industry of UK and Ireland and has

employed around 8000 employees across the 23 sites (About us., 2016). The most popular

food brands that Nestle UK provides its customer base include KitKat, Nescafe, Smarties,

Buxton, Go Cat and Shreddies (Nestle.co.uk, 2015).

Figure 1: Logo of the company

(Source: Nestle.co.uk, 2015)

In addition to their immense popularity, Nestle UK is one of UK and Ireland’s major

exporters of food products. They export over £346 million worth of food products every year

to over 70 nations globally (Nestle.com, 2015).

2

This task has been designed with the purpose of assessing the financial management of a

company. In this study, Nestle UK has been used as a case study. The financial management

of Nestle UK is assessed for the years 2013 and 2014 and their financial data is compared and

analysed. To understand the financial management in a better way, the researcher has made

an effort to identify methods for procuring budgets and analyse the impact of budget

constraints. In this study, the criteria on which proposals are judged for managing finance is

assessed and the outcomes of the mentioned proposals on objectives of Nestle UK are

evaluated.

Background of the Company:

Nestle UK is a subsidiary company of Nestle SA. It is the world’s best company on nutrition

as well as health. Nestle UK is a major player in the food industry of UK and Ireland and has

employed around 8000 employees across the 23 sites (About us., 2016). The most popular

food brands that Nestle UK provides its customer base include KitKat, Nescafe, Smarties,

Buxton, Go Cat and Shreddies (Nestle.co.uk, 2015).

Figure 1: Logo of the company

(Source: Nestle.co.uk, 2015)

In addition to their immense popularity, Nestle UK is one of UK and Ireland’s major

exporters of food products. They export over £346 million worth of food products every year

to over 70 nations globally (Nestle.com, 2015).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A.C 1.1:-

According to Brigham and Houston (2014, p.221), financial data availability is

helpful for analysts and all the stakeholders to assess the financial performance and viability

of the company. There is greater importance of the financial data for the organization in

drawing conclusion not only for decision making purpose but for overall strategic decision

making of the firm. The decision making quality to a significant level is dependent on the

financial data quality. It is important that financial data are being gathered from authentic

sources in right manner in order to make sure that it offer suitable information and

knowledge. Any individual or an organisation can obtain financial statement of a particular

company through external sources and internal sources. Bull (2013, p.215) opined that the

internal sources that can help in collecting financial data include books of accounts, internal

accounting systems and sales representatives’ reports. Van Horne (2013, p.115) added that

the external sources that can be used for collecting financial data are through company

websites, suppliers, Company houses and financial statements released by the company.

The supplier’s reports provide data about the amount spent in procuring materials and the

expenses incurred in transactions. There is greater responsibility of the manager to maintain

the accounts of expenses so that it can pass such data to the organization's accounting

department. The main sources of financial data that is available from within and outside the

company include the financial statements that present the financial accounts statement,

balance sheet and the cash inflow. Nestle is relying Companies House website for the

purpose of getting financial data in order to monitor financial activities of its competitors.

In order to assess the validity of the financial data gathered from internal and external

sources Nestle makes sure that it has audited both auditors that is internal and external. The

auditors present outside makes assessment of the financial statement in relation with

reliability, accuracy and timeliness. In case of Nestle it is necessary for organization to ensure

that the financial data being undertaken is valid. Further, with the motive to ensure reliability

of financial data main focus must be on controls along with the central transaction

processing. This system can directly assist in reducing the chances of errors which are being

present in the financial records of Nestle. It can directly assist company in meeting its desired

goals and objectives. Moreover, internal auditing is also one of the most appropriate way

which is generally self consulting activity and in turn improves the effectiveness of risk

management. Main role of internal auditor is to provide support to external auditor where in

depth analysis of financial statements take place during financial audit. On the other hand to

3

According to Brigham and Houston (2014, p.221), financial data availability is

helpful for analysts and all the stakeholders to assess the financial performance and viability

of the company. There is greater importance of the financial data for the organization in

drawing conclusion not only for decision making purpose but for overall strategic decision

making of the firm. The decision making quality to a significant level is dependent on the

financial data quality. It is important that financial data are being gathered from authentic

sources in right manner in order to make sure that it offer suitable information and

knowledge. Any individual or an organisation can obtain financial statement of a particular

company through external sources and internal sources. Bull (2013, p.215) opined that the

internal sources that can help in collecting financial data include books of accounts, internal

accounting systems and sales representatives’ reports. Van Horne (2013, p.115) added that

the external sources that can be used for collecting financial data are through company

websites, suppliers, Company houses and financial statements released by the company.

The supplier’s reports provide data about the amount spent in procuring materials and the

expenses incurred in transactions. There is greater responsibility of the manager to maintain

the accounts of expenses so that it can pass such data to the organization's accounting

department. The main sources of financial data that is available from within and outside the

company include the financial statements that present the financial accounts statement,

balance sheet and the cash inflow. Nestle is relying Companies House website for the

purpose of getting financial data in order to monitor financial activities of its competitors.

In order to assess the validity of the financial data gathered from internal and external

sources Nestle makes sure that it has audited both auditors that is internal and external. The

auditors present outside makes assessment of the financial statement in relation with

reliability, accuracy and timeliness. In case of Nestle it is necessary for organization to ensure

that the financial data being undertaken is valid. Further, with the motive to ensure reliability

of financial data main focus must be on controls along with the central transaction

processing. This system can directly assist in reducing the chances of errors which are being

present in the financial records of Nestle. It can directly assist company in meeting its desired

goals and objectives. Moreover, internal auditing is also one of the most appropriate way

which is generally self consulting activity and in turn improves the effectiveness of risk

management. Main role of internal auditor is to provide support to external auditor where in

depth analysis of financial statements take place during financial audit. On the other hand to

3

ensure validity of the data external auditor is also appointed by shareholders to verify that

financial statements are true and fair. Along with this, it is known whether the funds of

business are utilized in proper manner or not. Therefore, it is also fruitful in case of Nestle

where business can assess the validity of the data.

The benefits of divulging financial data is extremely important as it assists the

processes of audit and allows the necessary party to assess the financial viability of the

company. The financial data can be assessed in terms of possibilities of internal checks or

whether it is based on the culture of the organisation.

The external sources of financial data that can be obtained are generated from

company websites, suppliers’ reports (Cheng, 2013). This information is beneficial to the

company to review their performance in years and allows the owners to make decisions for

improving output. It also assists auditors to prepare audit reports of the company. The data

sources from outside the company are helpful for investors and stakeholders to assess the

performance of the company.

In the context of entering into a partnership, the financial data is beneficial for

companies to judge the performance of the other organisation before deciding on finalising

the deal. Sole proprietorship, joint ventures and partnerships all provide varied structures of

working ethics and financial statements provide the financial performance of the company.

The validity of the data can be verified by looking into their annual reports, financial

statements and auditor reports (McCafferry, 2014). These present a firm idea of the

company’s actual performance. Different types of investment decision needs to made for

entering new business environment. Firstly, financial investor needs to decide where to invest

and how to invest. For a careful investment decision considered the country’s GDP rate,

exchange rate and government policy regarding foreign investment.

The higher the GDP rate higher the return from investment. Good GDP rate indicates

the developed market which consists of largest and most industrialised country which is

lawful and unwavering government properly maintained that’s why developed market is

considered as the safest investment decision with a stable economic growth and profitability,

which are G8 countries and others European countries. Countries exchange rate influences

the financial investment decision as the share values increases and company can make profits.

Countries with different types trade restrictions with international body is risky for

investment decisions as they got low liquidity which affect the future return during periods.

4

financial statements are true and fair. Along with this, it is known whether the funds of

business are utilized in proper manner or not. Therefore, it is also fruitful in case of Nestle

where business can assess the validity of the data.

The benefits of divulging financial data is extremely important as it assists the

processes of audit and allows the necessary party to assess the financial viability of the

company. The financial data can be assessed in terms of possibilities of internal checks or

whether it is based on the culture of the organisation.

The external sources of financial data that can be obtained are generated from

company websites, suppliers’ reports (Cheng, 2013). This information is beneficial to the

company to review their performance in years and allows the owners to make decisions for

improving output. It also assists auditors to prepare audit reports of the company. The data

sources from outside the company are helpful for investors and stakeholders to assess the

performance of the company.

In the context of entering into a partnership, the financial data is beneficial for

companies to judge the performance of the other organisation before deciding on finalising

the deal. Sole proprietorship, joint ventures and partnerships all provide varied structures of

working ethics and financial statements provide the financial performance of the company.

The validity of the data can be verified by looking into their annual reports, financial

statements and auditor reports (McCafferry, 2014). These present a firm idea of the

company’s actual performance. Different types of investment decision needs to made for

entering new business environment. Firstly, financial investor needs to decide where to invest

and how to invest. For a careful investment decision considered the country’s GDP rate,

exchange rate and government policy regarding foreign investment.

The higher the GDP rate higher the return from investment. Good GDP rate indicates

the developed market which consists of largest and most industrialised country which is

lawful and unwavering government properly maintained that’s why developed market is

considered as the safest investment decision with a stable economic growth and profitability,

which are G8 countries and others European countries. Countries exchange rate influences

the financial investment decision as the share values increases and company can make profits.

Countries with different types trade restrictions with international body is risky for

investment decisions as they got low liquidity which affect the future return during periods.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

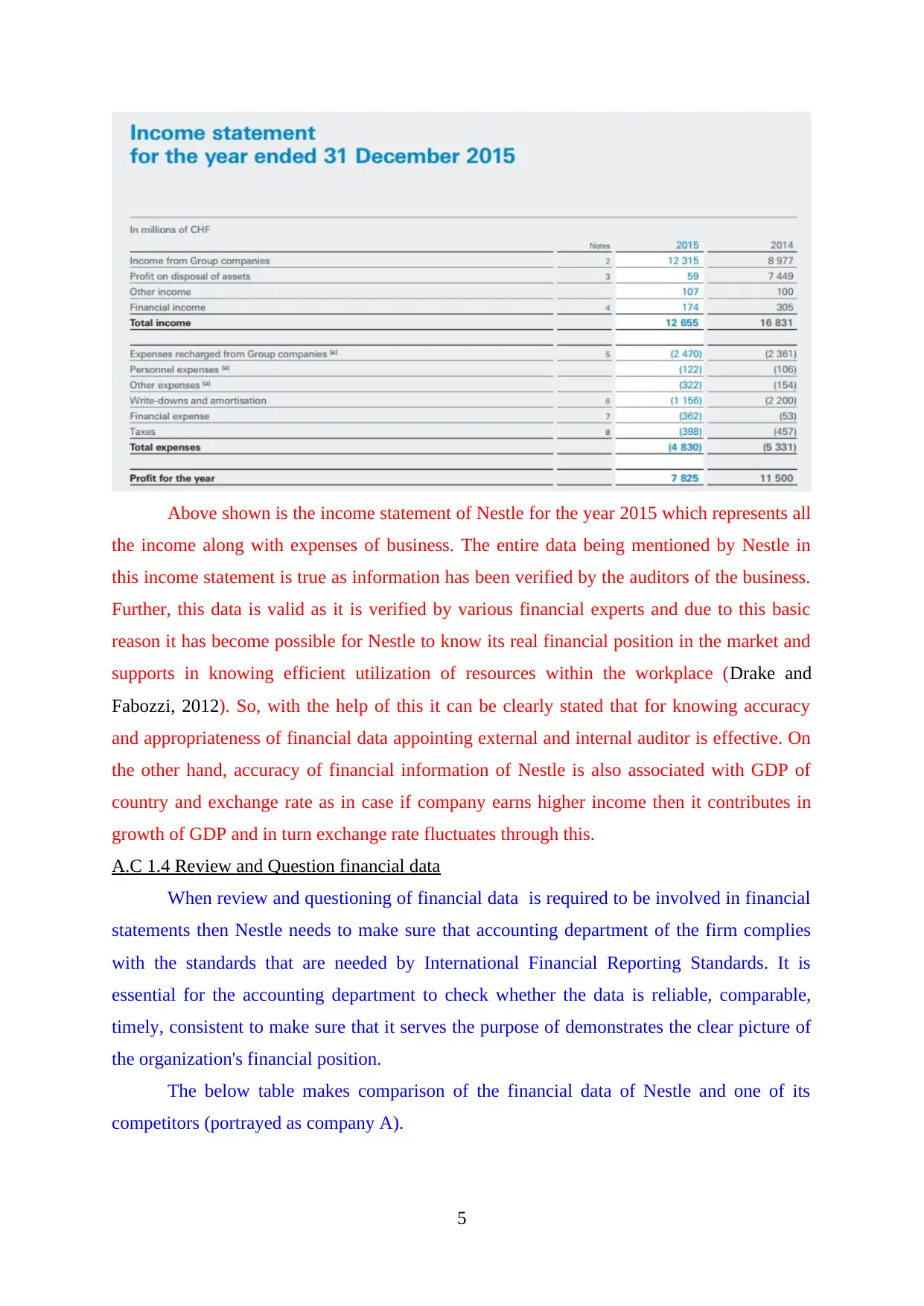

Above shown is the income statement of Nestle for the year 2015 which represents all

the income along with expenses of business. The entire data being mentioned by Nestle in

this income statement is true as information has been verified by the auditors of the business.

Further, this data is valid as it is verified by various financial experts and due to this basic

reason it has become possible for Nestle to know its real financial position in the market and

supports in knowing efficient utilization of resources within the workplace (Drake and

Fabozzi, 2012). So, with the help of this it can be clearly stated that for knowing accuracy

and appropriateness of financial data appointing external and internal auditor is effective. On

the other hand, accuracy of financial information of Nestle is also associated with GDP of

country and exchange rate as in case if company earns higher income then it contributes in

growth of GDP and in turn exchange rate fluctuates through this.

A.C 1.4 Review and Question financial data

When review and questioning of financial data is required to be involved in financial

statements then Nestle needs to make sure that accounting department of the firm complies

with the standards that are needed by International Financial Reporting Standards. It is

essential for the accounting department to check whether the data is reliable, comparable,

timely, consistent to make sure that it serves the purpose of demonstrates the clear picture of

the organization's financial position.

The below table makes comparison of the financial data of Nestle and one of its

competitors (portrayed as company A).

5

the income along with expenses of business. The entire data being mentioned by Nestle in

this income statement is true as information has been verified by the auditors of the business.

Further, this data is valid as it is verified by various financial experts and due to this basic

reason it has become possible for Nestle to know its real financial position in the market and

supports in knowing efficient utilization of resources within the workplace (Drake and

Fabozzi, 2012). So, with the help of this it can be clearly stated that for knowing accuracy

and appropriateness of financial data appointing external and internal auditor is effective. On

the other hand, accuracy of financial information of Nestle is also associated with GDP of

country and exchange rate as in case if company earns higher income then it contributes in

growth of GDP and in turn exchange rate fluctuates through this.

A.C 1.4 Review and Question financial data

When review and questioning of financial data is required to be involved in financial

statements then Nestle needs to make sure that accounting department of the firm complies

with the standards that are needed by International Financial Reporting Standards. It is

essential for the accounting department to check whether the data is reliable, comparable,

timely, consistent to make sure that it serves the purpose of demonstrates the clear picture of

the organization's financial position.

The below table makes comparison of the financial data of Nestle and one of its

competitors (portrayed as company A).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

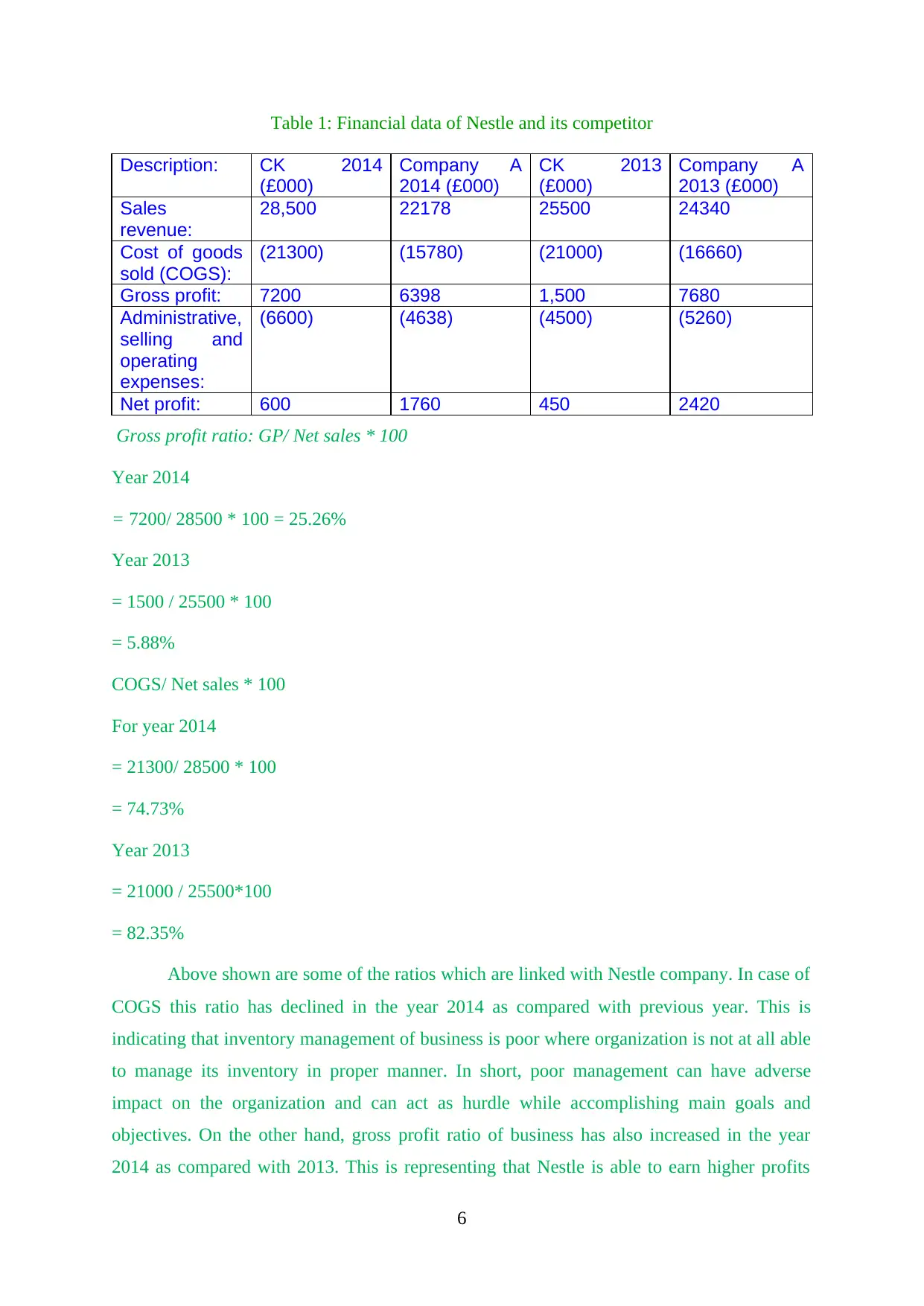

Table 1: Financial data of Nestle and its competitor

Description: CK 2014

(£000)

Company A

2014 (£000)

CK 2013

(£000)

Company A

2013 (£000)

Sales

revenue:

28,500 22178 25500 24340

Cost of goods

sold (COGS):

(21300) (15780) (21000) (16660)

Gross profit: 7200 6398 1,500 7680

Administrative,

selling and

operating

expenses:

(6600) (4638) (4500) (5260)

Net profit: 600 1760 450 2420

Gross profit ratio: GP/ Net sales * 100

Year 2014

= 7200/ 28500 * 100 = 25.26%

Year 2013

= 1500 / 25500 * 100

= 5.88%

COGS/ Net sales * 100

For year 2014

= 21300/ 28500 * 100

= 74.73%

Year 2013

= 21000 / 25500*100

= 82.35%

Above shown are some of the ratios which are linked with Nestle company. In case of

COGS this ratio has declined in the year 2014 as compared with previous year. This is

indicating that inventory management of business is poor where organization is not at all able

to manage its inventory in proper manner. In short, poor management can have adverse

impact on the organization and can act as hurdle while accomplishing main goals and

objectives. On the other hand, gross profit ratio of business has also increased in the year

2014 as compared with 2013. This is representing that Nestle is able to earn higher profits

6

Description: CK 2014

(£000)

Company A

2014 (£000)

CK 2013

(£000)

Company A

2013 (£000)

Sales

revenue:

28,500 22178 25500 24340

Cost of goods

sold (COGS):

(21300) (15780) (21000) (16660)

Gross profit: 7200 6398 1,500 7680

Administrative,

selling and

operating

expenses:

(6600) (4638) (4500) (5260)

Net profit: 600 1760 450 2420

Gross profit ratio: GP/ Net sales * 100

Year 2014

= 7200/ 28500 * 100 = 25.26%

Year 2013

= 1500 / 25500 * 100

= 5.88%

COGS/ Net sales * 100

For year 2014

= 21300/ 28500 * 100

= 74.73%

Year 2013

= 21000 / 25500*100

= 82.35%

Above shown are some of the ratios which are linked with Nestle company. In case of

COGS this ratio has declined in the year 2014 as compared with previous year. This is

indicating that inventory management of business is poor where organization is not at all able

to manage its inventory in proper manner. In short, poor management can have adverse

impact on the organization and can act as hurdle while accomplishing main goals and

objectives. On the other hand, gross profit ratio of business has also increased in the year

2014 as compared with 2013. This is representing that Nestle is able to earn higher profits

6

and have proper control on all the major expenses of the business. Apart from this, firm is

able to perform efficiently in the market and this has allowed in accomplishing the desired

objectives of the entity.

On considering this data related with financial analysis the accounting department of

the firm would make sure that they possess reliability. For instance, when making

computation of gross profit the accounting department can question that whether such figures

of COGS calculated are reliable or not. For COGS of Nestle they can question that is there is

probability that figures of 21300 and 21000 can enhance to demonstrate lower profit for tax

benefit. In order to make sure such the gross profit is comparable. The department of

accounting would make sure that data can be compared with both, the organization's

historical data.

Before making collection of competitors data question can be raised regarding

whether it has been gathered from credible sources and how reliable they are. Before making

any conclusion or drawing recommendation it is important that accounting department would

question regarding the timeliness of the data in terms that whether it is one year old. Further

they can review on external factors that has influenced the competitors as it resulted in terms

of lower gross profit.

Changes in the accounting policy can put significant effect in use of assumptions

estimations which is related to the consolidated financial statement. If an accounting policy

relates specifically to a note (balance or transaction) it is presented within the relevant note so

from a balanced statement investor might get wrong information about the company (Dyson,

2003). Year under year review can create the misconceptions as every years environmental

factors are not same which also can create the wrong signals to the investor. “Creative

accounting practices” and “window dressing” which involves alterations of accounting data

and information which affect the future revenue, policies, assets and liabilities from those

report future investor might get wrong message about the current company.

Most of the investor wants to increase their long term purchasing power but inflation

creates a threat to investor as its put their goals at risk then investors might move their money

at a lower inflation rates market because increased inflation rate tends to raise interest rates

too or where government can put the fixed interest rates for certain period. In addition, fast

moving sector where technology can play an important role because investor can’t judge the

decision by seeing only the past year financial information as environmental factors are not

same for every year as it’s a fast moving sector.

7

able to perform efficiently in the market and this has allowed in accomplishing the desired

objectives of the entity.

On considering this data related with financial analysis the accounting department of

the firm would make sure that they possess reliability. For instance, when making

computation of gross profit the accounting department can question that whether such figures

of COGS calculated are reliable or not. For COGS of Nestle they can question that is there is

probability that figures of 21300 and 21000 can enhance to demonstrate lower profit for tax

benefit. In order to make sure such the gross profit is comparable. The department of

accounting would make sure that data can be compared with both, the organization's

historical data.

Before making collection of competitors data question can be raised regarding

whether it has been gathered from credible sources and how reliable they are. Before making

any conclusion or drawing recommendation it is important that accounting department would

question regarding the timeliness of the data in terms that whether it is one year old. Further

they can review on external factors that has influenced the competitors as it resulted in terms

of lower gross profit.

Changes in the accounting policy can put significant effect in use of assumptions

estimations which is related to the consolidated financial statement. If an accounting policy

relates specifically to a note (balance or transaction) it is presented within the relevant note so

from a balanced statement investor might get wrong information about the company (Dyson,

2003). Year under year review can create the misconceptions as every years environmental

factors are not same which also can create the wrong signals to the investor. “Creative

accounting practices” and “window dressing” which involves alterations of accounting data

and information which affect the future revenue, policies, assets and liabilities from those

report future investor might get wrong message about the current company.

Most of the investor wants to increase their long term purchasing power but inflation

creates a threat to investor as its put their goals at risk then investors might move their money

at a lower inflation rates market because increased inflation rate tends to raise interest rates

too or where government can put the fixed interest rates for certain period. In addition, fast

moving sector where technology can play an important role because investor can’t judge the

decision by seeing only the past year financial information as environmental factors are not

same for every year as it’s a fast moving sector.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

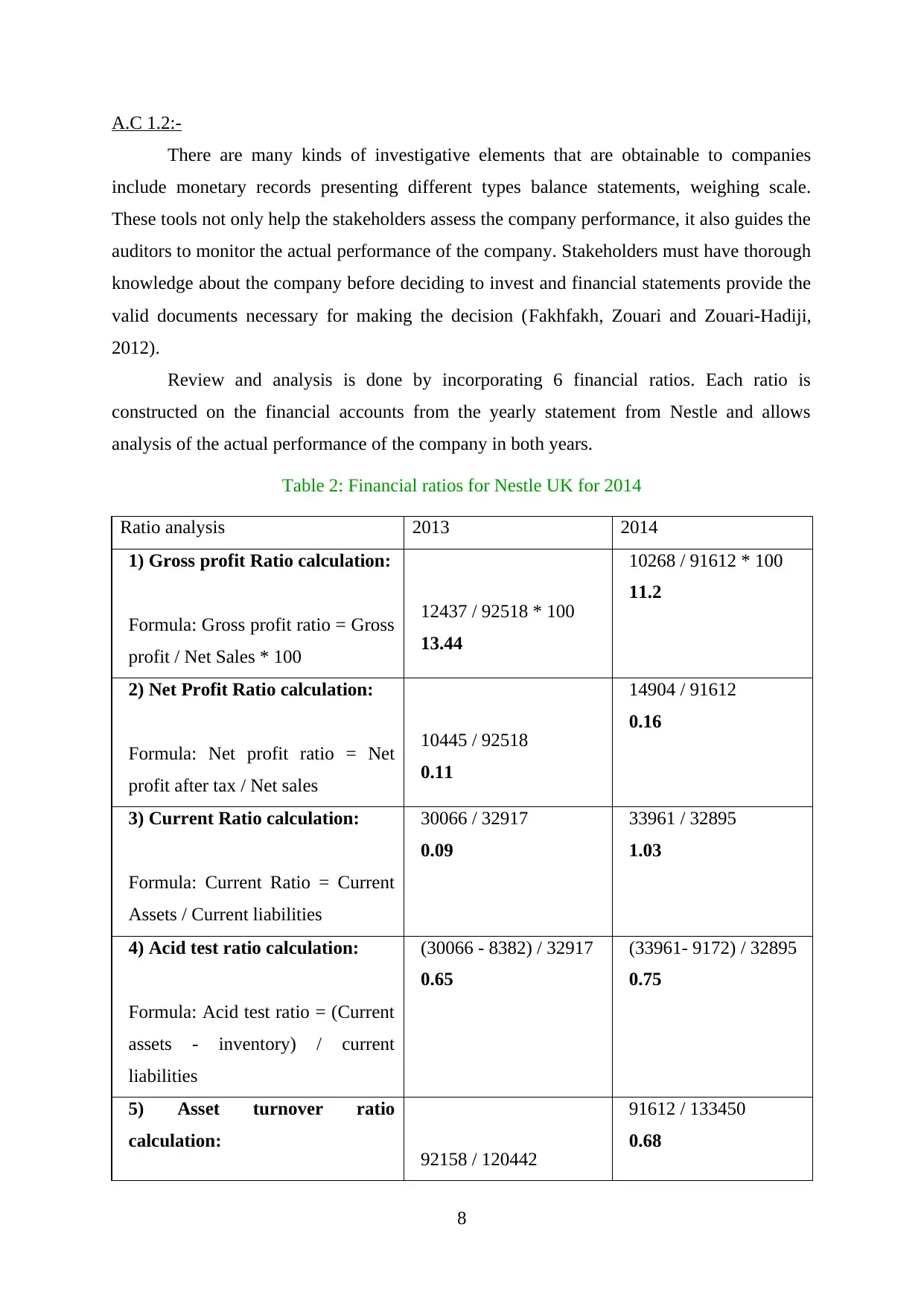

A.C 1.2:-

There are many kinds of investigative elements that are obtainable to companies

include monetary records presenting different types balance statements, weighing scale.

These tools not only help the stakeholders assess the company performance, it also guides the

auditors to monitor the actual performance of the company. Stakeholders must have thorough

knowledge about the company before deciding to invest and financial statements provide the

valid documents necessary for making the decision (Fakhfakh, Zouari and Zouari-Hadiji,

2012).

Review and analysis is done by incorporating 6 financial ratios. Each ratio is

constructed on the financial accounts from the yearly statement from Nestle and allows

analysis of the actual performance of the company in both years.

Table 2: Financial ratios for Nestle UK for 2014

Ratio analysis 2013 2014

1) Gross profit Ratio calculation:

Formula: Gross profit ratio = Gross

profit / Net Sales * 100

12437 / 92518 * 100

13.44

10268 / 91612 * 100

11.2

2) Net Profit Ratio calculation:

Formula: Net profit ratio = Net

profit after tax / Net sales

10445 / 92518

0.11

14904 / 91612

0.16

3) Current Ratio calculation:

Formula: Current Ratio = Current

Assets / Current liabilities

30066 / 32917

0.09

33961 / 32895

1.03

4) Acid test ratio calculation:

Formula: Acid test ratio = (Current

assets - inventory) / current

liabilities

(30066 - 8382) / 32917

0.65

(33961- 9172) / 32895

0.75

5) Asset turnover ratio

calculation: 92158 / 120442

91612 / 133450

0.68

8

There are many kinds of investigative elements that are obtainable to companies

include monetary records presenting different types balance statements, weighing scale.

These tools not only help the stakeholders assess the company performance, it also guides the

auditors to monitor the actual performance of the company. Stakeholders must have thorough

knowledge about the company before deciding to invest and financial statements provide the

valid documents necessary for making the decision (Fakhfakh, Zouari and Zouari-Hadiji,

2012).

Review and analysis is done by incorporating 6 financial ratios. Each ratio is

constructed on the financial accounts from the yearly statement from Nestle and allows

analysis of the actual performance of the company in both years.

Table 2: Financial ratios for Nestle UK for 2014

Ratio analysis 2013 2014

1) Gross profit Ratio calculation:

Formula: Gross profit ratio = Gross

profit / Net Sales * 100

12437 / 92518 * 100

13.44

10268 / 91612 * 100

11.2

2) Net Profit Ratio calculation:

Formula: Net profit ratio = Net

profit after tax / Net sales

10445 / 92518

0.11

14904 / 91612

0.16

3) Current Ratio calculation:

Formula: Current Ratio = Current

Assets / Current liabilities

30066 / 32917

0.09

33961 / 32895

1.03

4) Acid test ratio calculation:

Formula: Acid test ratio = (Current

assets - inventory) / current

liabilities

(30066 - 8382) / 32917

0.65

(33961- 9172) / 32895

0.75

5) Asset turnover ratio

calculation: 92158 / 120442

91612 / 133450

0.68

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

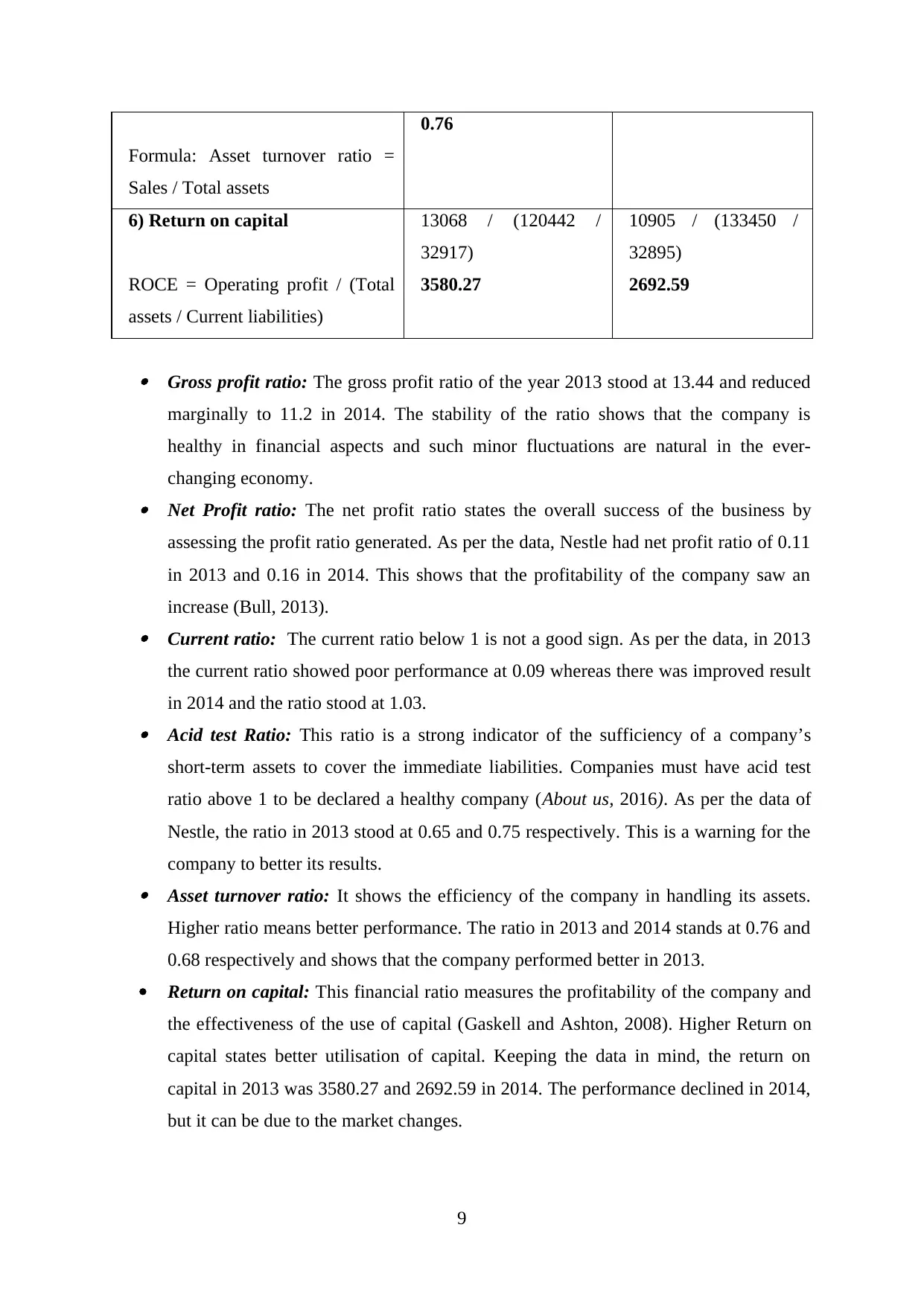

Formula: Asset turnover ratio =

Sales / Total assets

0.76

6) Return on capital

ROCE = Operating profit / (Total

assets / Current liabilities)

13068 / (120442 /

32917)

3580.27

10905 / (133450 /

32895)

2692.59

Gross profit ratio: The gross profit ratio of the year 2013 stood at 13.44 and reduced

marginally to 11.2 in 2014. The stability of the ratio shows that the company is

healthy in financial aspects and such minor fluctuations are natural in the ever-

changing economy. Net Profit ratio: The net profit ratio states the overall success of the business by

assessing the profit ratio generated. As per the data, Nestle had net profit ratio of 0.11

in 2013 and 0.16 in 2014. This shows that the profitability of the company saw an

increase (Bull, 2013). Current ratio: The current ratio below 1 is not a good sign. As per the data, in 2013

the current ratio showed poor performance at 0.09 whereas there was improved result

in 2014 and the ratio stood at 1.03. Acid test Ratio: This ratio is a strong indicator of the sufficiency of a company’s

short-term assets to cover the immediate liabilities. Companies must have acid test

ratio above 1 to be declared a healthy company (About us, 2016). As per the data of

Nestle, the ratio in 2013 stood at 0.65 and 0.75 respectively. This is a warning for the

company to better its results. Asset turnover ratio: It shows the efficiency of the company in handling its assets.

Higher ratio means better performance. The ratio in 2013 and 2014 stands at 0.76 and

0.68 respectively and shows that the company performed better in 2013.

Return on capital: This financial ratio measures the profitability of the company and

the effectiveness of the use of capital (Gaskell and Ashton, 2008). Higher Return on

capital states better utilisation of capital. Keeping the data in mind, the return on

capital in 2013 was 3580.27 and 2692.59 in 2014. The performance declined in 2014,

but it can be due to the market changes.

9

Sales / Total assets

0.76

6) Return on capital

ROCE = Operating profit / (Total

assets / Current liabilities)

13068 / (120442 /

32917)

3580.27

10905 / (133450 /

32895)

2692.59

Gross profit ratio: The gross profit ratio of the year 2013 stood at 13.44 and reduced

marginally to 11.2 in 2014. The stability of the ratio shows that the company is

healthy in financial aspects and such minor fluctuations are natural in the ever-

changing economy. Net Profit ratio: The net profit ratio states the overall success of the business by

assessing the profit ratio generated. As per the data, Nestle had net profit ratio of 0.11

in 2013 and 0.16 in 2014. This shows that the profitability of the company saw an

increase (Bull, 2013). Current ratio: The current ratio below 1 is not a good sign. As per the data, in 2013

the current ratio showed poor performance at 0.09 whereas there was improved result

in 2014 and the ratio stood at 1.03. Acid test Ratio: This ratio is a strong indicator of the sufficiency of a company’s

short-term assets to cover the immediate liabilities. Companies must have acid test

ratio above 1 to be declared a healthy company (About us, 2016). As per the data of

Nestle, the ratio in 2013 stood at 0.65 and 0.75 respectively. This is a warning for the

company to better its results. Asset turnover ratio: It shows the efficiency of the company in handling its assets.

Higher ratio means better performance. The ratio in 2013 and 2014 stands at 0.76 and

0.68 respectively and shows that the company performed better in 2013.

Return on capital: This financial ratio measures the profitability of the company and

the effectiveness of the use of capital (Gaskell and Ashton, 2008). Higher Return on

capital states better utilisation of capital. Keeping the data in mind, the return on

capital in 2013 was 3580.27 and 2692.59 in 2014. The performance declined in 2014,

but it can be due to the market changes.

9

Overview of ratio analysis: It is clear from the financial data and ratio analysis of Nestle

that their performance has shown steady growth in terms of revenue and their performance

has been marginally better than 2013. These minor changes can be attributed to the effect of

inflation on the prices of raw materials and commodities for production. The ripple effect of

inflation falls on the interest rates and it influences the prices of imports and duties for which

the company needs to pay more. Nestle being a food industry deals in commodities that must

be distributed as quickly as possible. These kinds of companies require quick decision

making as there is barely any time to assess the performance of the past performances.

Financial data can indeed help the company but in fast moving industries, the need to adapt

strategies quickly is very important (Götze, Northcott and Schuster, 2008). If the figures

obtained from ratio analysis are to be noted, the profit margins showed improvement whereas

the gross profit margin reduced slightly. This proves that the brand strength of Nestle is

capable of maintaining sustainable profit margins. However, the market conditions in UK

have slightly dented the profit margins of the company. The ratio analysis show growth of

Nestle and provides the information that despite market conditions, Nestle has achieved

sustainable profit. However, the limitations that curb their performance are the performance

of its rivals by creating substitute products and disturbing the level of profits.

There is greater need among stakeholders regarding the information presented through

financial analysis. As such assist in decision making process in an effective manner. All the

range of financial ratios being calculated are effective for stakeholders associated with

Nestle. Further, different parties are associated with company such as customers, suppliers,

shareholders, government etc and they are interested in knowing financial position of

business. Therefore, different type of ratios computed supports in satisfying this need. Gross

and net profit ratio is interesting for shareholders and financial institutions. Through these

ratios it becomes easy for them to know the earning capacity of the business (Grewal and

et.al., 2011). Further, in case of current and quick ratio it is being used by internal

management of the business through which it is possible to know the liquid funds present

with Nestle. Asset turnover and return on capital employed are used by investors so as to

ascertain the amount of return. Therefore, in this way different ratios are being undertaken by

stakeholders for knowing the financial performance of business.

A.C 1.3 Comparative analyses of financial data of Nestle:

Financial statements of Nestle UK are taken to conduct a comparative analysis of their

performance in the fiscal years 2013 and 2014. Wholey (2014, p.69) commented that

comparison of performances of the company using financial details can help the company,

10

that their performance has shown steady growth in terms of revenue and their performance

has been marginally better than 2013. These minor changes can be attributed to the effect of

inflation on the prices of raw materials and commodities for production. The ripple effect of

inflation falls on the interest rates and it influences the prices of imports and duties for which

the company needs to pay more. Nestle being a food industry deals in commodities that must

be distributed as quickly as possible. These kinds of companies require quick decision

making as there is barely any time to assess the performance of the past performances.

Financial data can indeed help the company but in fast moving industries, the need to adapt

strategies quickly is very important (Götze, Northcott and Schuster, 2008). If the figures

obtained from ratio analysis are to be noted, the profit margins showed improvement whereas

the gross profit margin reduced slightly. This proves that the brand strength of Nestle is

capable of maintaining sustainable profit margins. However, the market conditions in UK

have slightly dented the profit margins of the company. The ratio analysis show growth of

Nestle and provides the information that despite market conditions, Nestle has achieved

sustainable profit. However, the limitations that curb their performance are the performance

of its rivals by creating substitute products and disturbing the level of profits.

There is greater need among stakeholders regarding the information presented through

financial analysis. As such assist in decision making process in an effective manner. All the

range of financial ratios being calculated are effective for stakeholders associated with

Nestle. Further, different parties are associated with company such as customers, suppliers,

shareholders, government etc and they are interested in knowing financial position of

business. Therefore, different type of ratios computed supports in satisfying this need. Gross

and net profit ratio is interesting for shareholders and financial institutions. Through these

ratios it becomes easy for them to know the earning capacity of the business (Grewal and

et.al., 2011). Further, in case of current and quick ratio it is being used by internal

management of the business through which it is possible to know the liquid funds present

with Nestle. Asset turnover and return on capital employed are used by investors so as to

ascertain the amount of return. Therefore, in this way different ratios are being undertaken by

stakeholders for knowing the financial performance of business.

A.C 1.3 Comparative analyses of financial data of Nestle:

Financial statements of Nestle UK are taken to conduct a comparative analysis of their

performance in the fiscal years 2013 and 2014. Wholey (2014, p.69) commented that

comparison of performances of the company using financial details can help the company,

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.