Managing Finance in Health and Social Care: NHS Trust Hospital Project

VerifiedAdded on 2023/06/10

|20

|4727

|482

Report

AI Summary

This report provides a comprehensive financial analysis of an NHS Trust hospital's proposal to open a trust hospital. The analysis includes an executive summary, introduction, and detailed examination of the original and revised proposals. The report focuses on investment appraisal techniques such as payback period, accounting rate of return, and net present value to evaluate the financial viability of the project. The report compares the initial proposal, which was deemed financially unviable, with a revised proposal that aims to reduce expenses and increase revenue. Calculations and recommendations are provided based on these techniques, with the final recommendation to accept the revised proposal. The report highlights the importance of both financial and non-financial factors in making investment decisions and emphasizes the need for effective budget management to identify and control costs, ultimately aiming to maximize returns and improve healthcare facilities. The report is contributed by a student and is available on Desklib, a platform providing AI-based study tools for students.

MANAGING FINANCE IN

HEALTH AND SOCIAL CARE

ORGANISATION

HEALTH AND SOCIAL CARE

ORGANISATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

In this report, health and social care organisation is seeking for a most suitable and beneficial proposal for opening a trust hospital

through which society will be served with most efficient healthcare facilities. Health and social care organisation should consider the

revised proposal as it will be more beneficial to generate higher revenues to the trust which can further used in providing more

facilities in the best manner. Decision for the revised proposal can be undertaken by following investment appraisal techniques.

Organisation should develop a most suitable and informative budget which will assist the management in identifying relevant costs

and ways to manage and control those costs.

In this report, health and social care organisation is seeking for a most suitable and beneficial proposal for opening a trust hospital

through which society will be served with most efficient healthcare facilities. Health and social care organisation should consider the

revised proposal as it will be more beneficial to generate higher revenues to the trust which can further used in providing more

facilities in the best manner. Decision for the revised proposal can be undertaken by following investment appraisal techniques.

Organisation should develop a most suitable and informative budget which will assist the management in identifying relevant costs

and ways to manage and control those costs.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

PART A...........................................................................................................................................4

PART B............................................................................................................................................8

PART C..........................................................................................................................................14

PART D.........................................................................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................19

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

PART A...........................................................................................................................................4

PART B............................................................................................................................................8

PART C..........................................................................................................................................14

PART D.........................................................................................................................................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

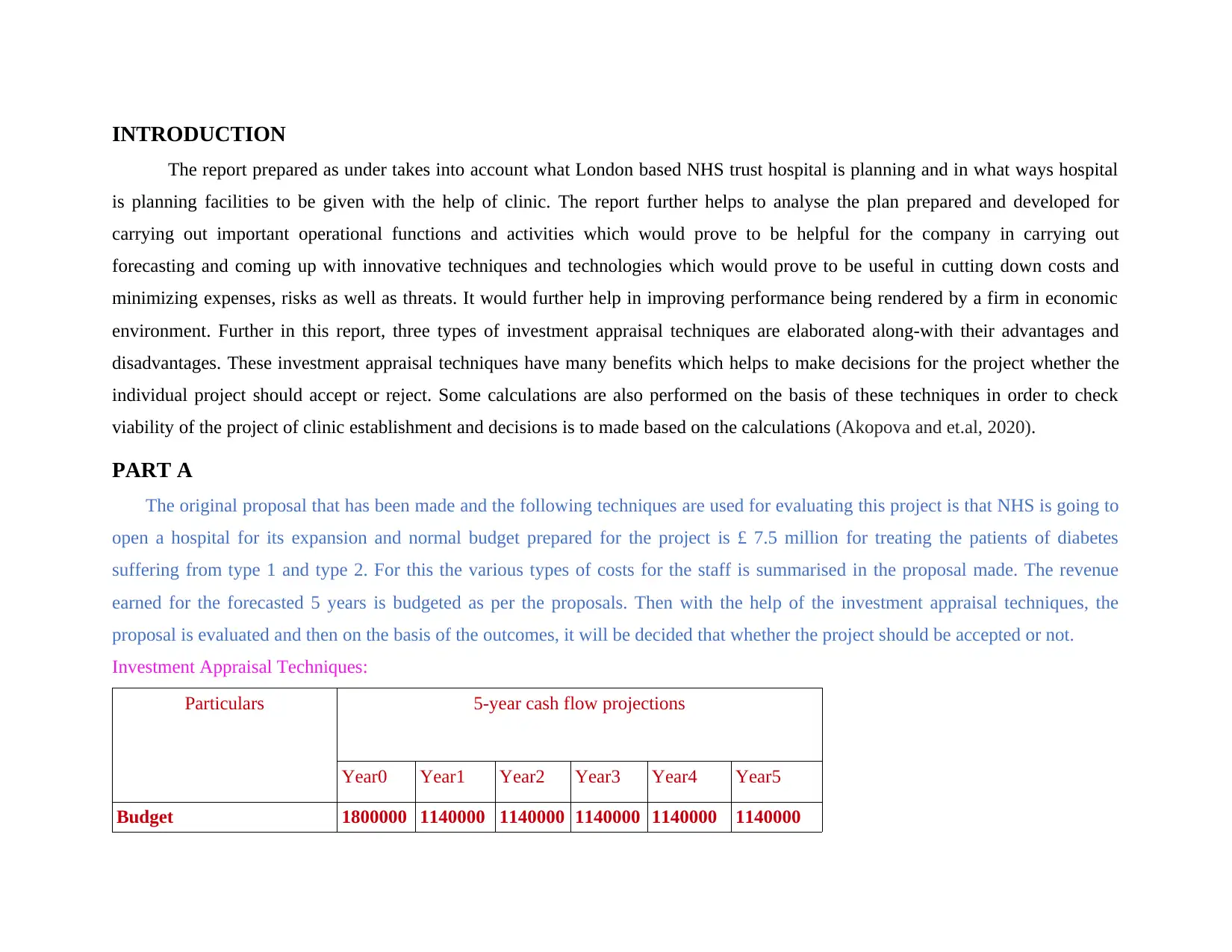

INTRODUCTION

The report prepared as under takes into account what London based NHS trust hospital is planning and in what ways hospital

is planning facilities to be given with the help of clinic. The report further helps to analyse the plan prepared and developed for

carrying out important operational functions and activities which would prove to be helpful for the company in carrying out

forecasting and coming up with innovative techniques and technologies which would prove to be useful in cutting down costs and

minimizing expenses, risks as well as threats. It would further help in improving performance being rendered by a firm in economic

environment. Further in this report, three types of investment appraisal techniques are elaborated along-with their advantages and

disadvantages. These investment appraisal techniques have many benefits which helps to make decisions for the project whether the

individual project should accept or reject. Some calculations are also performed on the basis of these techniques in order to check

viability of the project of clinic establishment and decisions is to made based on the calculations (Akopova and et.al, 2020).

PART A

The original proposal that has been made and the following techniques are used for evaluating this project is that NHS is going to

open a hospital for its expansion and normal budget prepared for the project is £ 7.5 million for treating the patients of diabetes

suffering from type 1 and type 2. For this the various types of costs for the staff is summarised in the proposal made. The revenue

earned for the forecasted 5 years is budgeted as per the proposals. Then with the help of the investment appraisal techniques, the

proposal is evaluated and then on the basis of the outcomes, it will be decided that whether the project should be accepted or not.

Investment Appraisal Techniques:

Particulars 5-year cash flow projections

Year0 Year1 Year2 Year3 Year4 Year5

Budget 1800000 1140000 1140000 1140000 1140000 1140000

The report prepared as under takes into account what London based NHS trust hospital is planning and in what ways hospital

is planning facilities to be given with the help of clinic. The report further helps to analyse the plan prepared and developed for

carrying out important operational functions and activities which would prove to be helpful for the company in carrying out

forecasting and coming up with innovative techniques and technologies which would prove to be useful in cutting down costs and

minimizing expenses, risks as well as threats. It would further help in improving performance being rendered by a firm in economic

environment. Further in this report, three types of investment appraisal techniques are elaborated along-with their advantages and

disadvantages. These investment appraisal techniques have many benefits which helps to make decisions for the project whether the

individual project should accept or reject. Some calculations are also performed on the basis of these techniques in order to check

viability of the project of clinic establishment and decisions is to made based on the calculations (Akopova and et.al, 2020).

PART A

The original proposal that has been made and the following techniques are used for evaluating this project is that NHS is going to

open a hospital for its expansion and normal budget prepared for the project is £ 7.5 million for treating the patients of diabetes

suffering from type 1 and type 2. For this the various types of costs for the staff is summarised in the proposal made. The revenue

earned for the forecasted 5 years is budgeted as per the proposals. Then with the help of the investment appraisal techniques, the

proposal is evaluated and then on the basis of the outcomes, it will be decided that whether the project should be accepted or not.

Investment Appraisal Techniques:

Particulars 5-year cash flow projections

Year0 Year1 Year2 Year3 Year4 Year5

Budget 1800000 1140000 1140000 1140000 1140000 1140000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

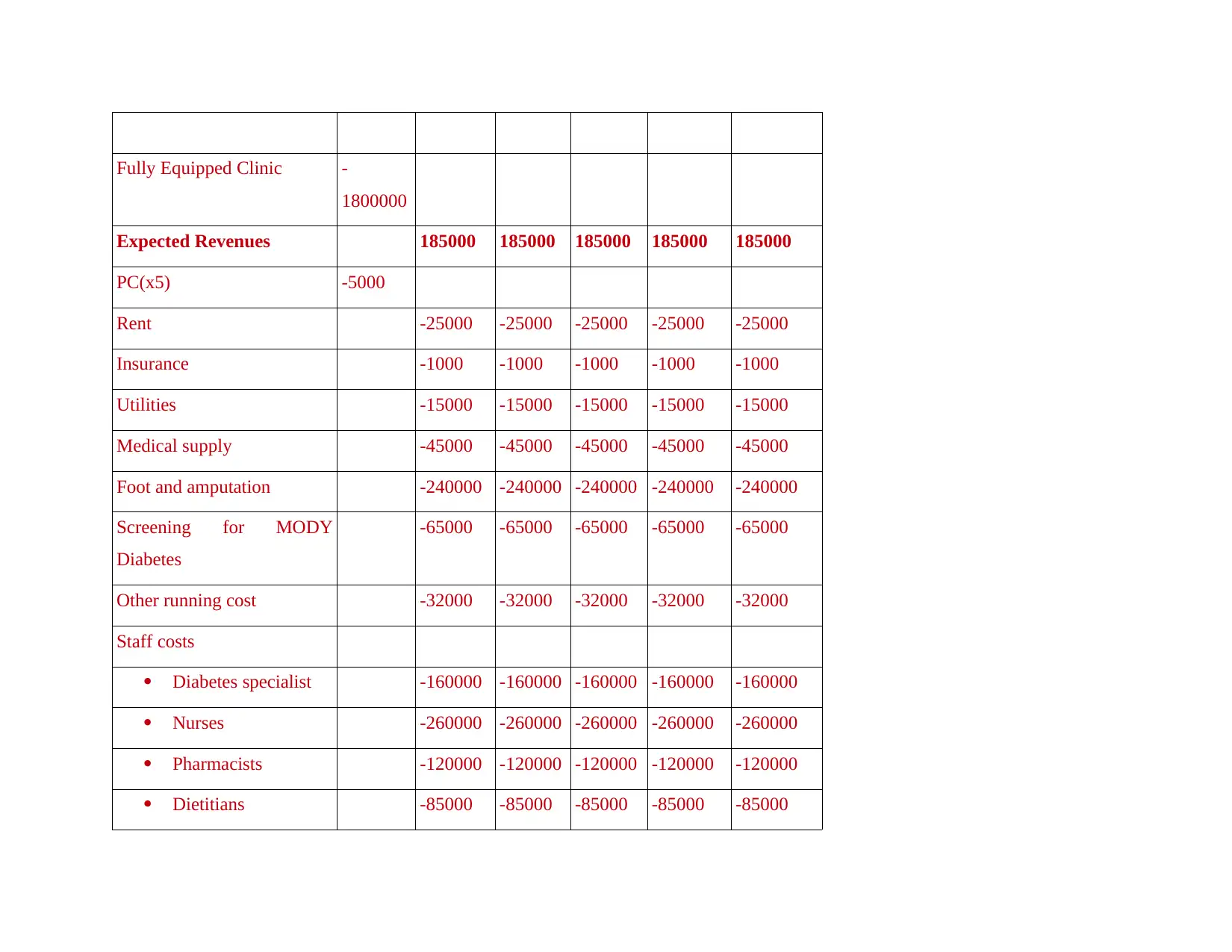

Fully Equipped Clinic -

1800000

Expected Revenues 185000 185000 185000 185000 185000

PC(x5) -5000

Rent -25000 -25000 -25000 -25000 -25000

Insurance -1000 -1000 -1000 -1000 -1000

Utilities -15000 -15000 -15000 -15000 -15000

Medical supply -45000 -45000 -45000 -45000 -45000

Foot and amputation -240000 -240000 -240000 -240000 -240000

Screening for MODY

Diabetes

-65000 -65000 -65000 -65000 -65000

Other running cost -32000 -32000 -32000 -32000 -32000

Staff costs

Diabetes specialist -160000 -160000 -160000 -160000 -160000

Nurses -260000 -260000 -260000 -260000 -260000

Pharmacists -120000 -120000 -120000 -120000 -120000

Dietitians -85000 -85000 -85000 -85000 -85000

1800000

Expected Revenues 185000 185000 185000 185000 185000

PC(x5) -5000

Rent -25000 -25000 -25000 -25000 -25000

Insurance -1000 -1000 -1000 -1000 -1000

Utilities -15000 -15000 -15000 -15000 -15000

Medical supply -45000 -45000 -45000 -45000 -45000

Foot and amputation -240000 -240000 -240000 -240000 -240000

Screening for MODY

Diabetes

-65000 -65000 -65000 -65000 -65000

Other running cost -32000 -32000 -32000 -32000 -32000

Staff costs

Diabetes specialist -160000 -160000 -160000 -160000 -160000

Nurses -260000 -260000 -260000 -260000 -260000

Pharmacists -120000 -120000 -120000 -120000 -120000

Dietitians -85000 -85000 -85000 -85000 -85000

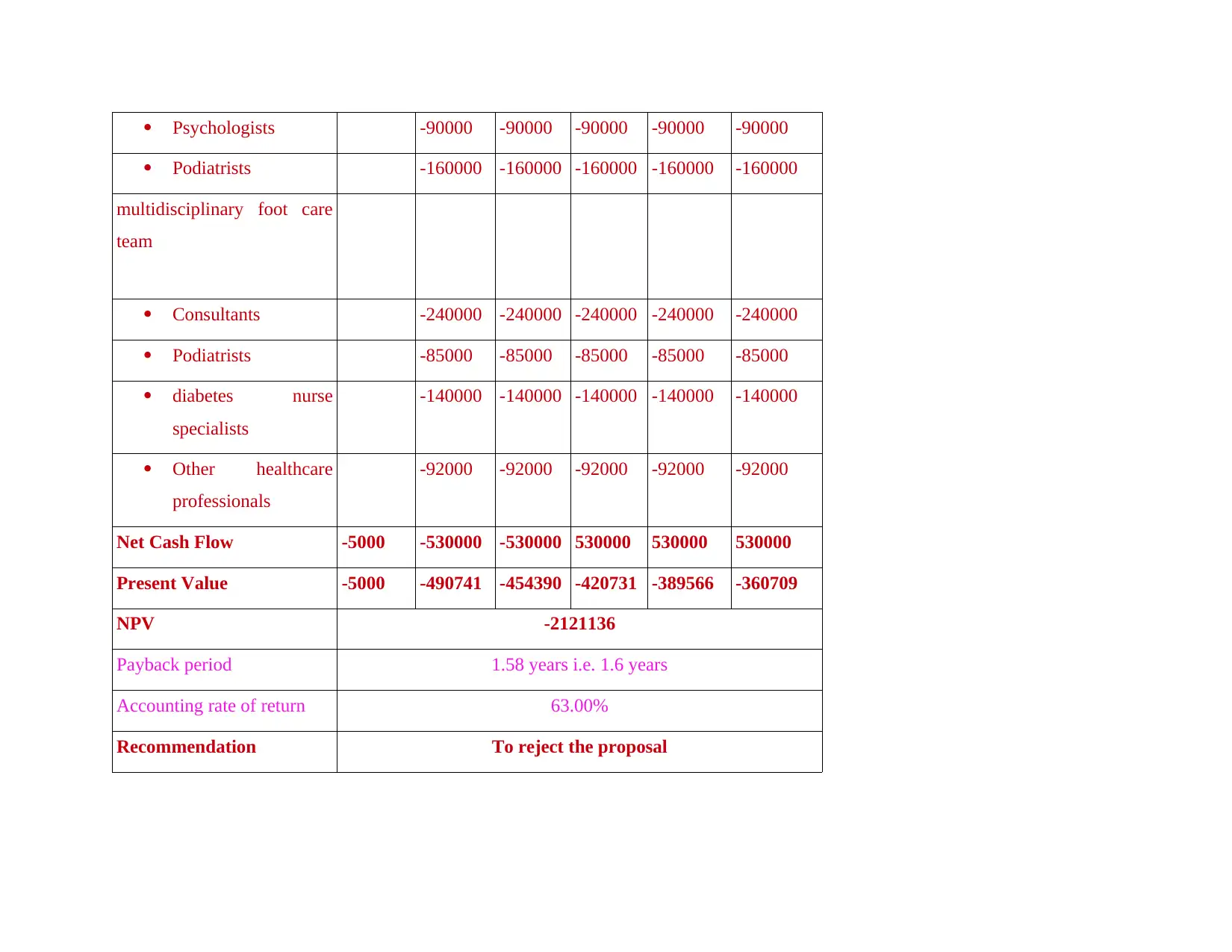

Psychologists -90000 -90000 -90000 -90000 -90000

Podiatrists -160000 -160000 -160000 -160000 -160000

multidisciplinary foot care

team

Consultants -240000 -240000 -240000 -240000 -240000

Podiatrists -85000 -85000 -85000 -85000 -85000

diabetes nurse

specialists

-140000 -140000 -140000 -140000 -140000

Other healthcare

professionals

-92000 -92000 -92000 -92000 -92000

Net Cash Flow -5000 -530000 -530000 530000 530000 530000

Present Value -5000 -490741 -454390 -420731 -389566 -360709

NPV -2121136

Payback period 1.58 years i.e. 1.6 years

Accounting rate of return 63.00%

Recommendation To reject the proposal

Podiatrists -160000 -160000 -160000 -160000 -160000

multidisciplinary foot care

team

Consultants -240000 -240000 -240000 -240000 -240000

Podiatrists -85000 -85000 -85000 -85000 -85000

diabetes nurse

specialists

-140000 -140000 -140000 -140000 -140000

Other healthcare

professionals

-92000 -92000 -92000 -92000 -92000

Net Cash Flow -5000 -530000 -530000 530000 530000 530000

Present Value -5000 -490741 -454390 -420731 -389566 -360709

NPV -2121136

Payback period 1.58 years i.e. 1.6 years

Accounting rate of return 63.00%

Recommendation To reject the proposal

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In order to maximise the returns for the potential owners and stakeholders of the NHS Trust, management should ensure that

profitable investment projects will be selected. It would be disastrous for the firm for selecting an incapable investment project in

terms of strategic and financially (Chesak and et.al., 2019). There are several investment appraisal techniques which can be used to

check the viability of different investment projects. The table above shows an assessment of centres opened at NHS Foundation Trust

Hospitals in London. The total planned expenditure to open such a centre is £7.5m to treat both type 1 and type 2 diabetes. The base

capital expenditure for hardware is £1.8m, which will be spent on full facilities in year 0, and the trust expects the centre should

generate annual revenue of £185,000. It can be seen very well that out of the £7.5m, £1.8m was spent on fully prepared centres in year

0, while the overspending scheme was similarly applied over the next 5 years, i.e. £1.14m per annum, until the 5th year. Given this

information, a speculative evaluation strategy is being used to examine whether the launch of the new centre will pay off over the next

five years. These techniques are outlined below sequentially which are as follows:

Payback period can be termed as originally period required to recuperate the total cost incurred for the project. It is the period

in which earned cash flow will surpass the cash outflow initially. Total time required by the investment to generate the income to

equalise the total cash outlays. In case of even cash flows over the total period of the project, payback period is calculating by this

formula which is as under:

Payback period = Total initial capital investment/Annual cash flows

It is the simplest technique which required less computation than other techniques (Cottam, H., 2018). It is simple to

understand as the terms used in it are easy. It also depicts the risk associated with the projects as lengthy the project, higher will be the

risk and vice-versa. On the other hand, the biggest limitation of this technique is that it avoids time value of money. It ignores the

returns after the payback period as it considers only returns which required to cover its initial cost. This technique would avoid lengthy

projects having a long time duration.

profitable investment projects will be selected. It would be disastrous for the firm for selecting an incapable investment project in

terms of strategic and financially (Chesak and et.al., 2019). There are several investment appraisal techniques which can be used to

check the viability of different investment projects. The table above shows an assessment of centres opened at NHS Foundation Trust

Hospitals in London. The total planned expenditure to open such a centre is £7.5m to treat both type 1 and type 2 diabetes. The base

capital expenditure for hardware is £1.8m, which will be spent on full facilities in year 0, and the trust expects the centre should

generate annual revenue of £185,000. It can be seen very well that out of the £7.5m, £1.8m was spent on fully prepared centres in year

0, while the overspending scheme was similarly applied over the next 5 years, i.e. £1.14m per annum, until the 5th year. Given this

information, a speculative evaluation strategy is being used to examine whether the launch of the new centre will pay off over the next

five years. These techniques are outlined below sequentially which are as follows:

Payback period can be termed as originally period required to recuperate the total cost incurred for the project. It is the period

in which earned cash flow will surpass the cash outflow initially. Total time required by the investment to generate the income to

equalise the total cash outlays. In case of even cash flows over the total period of the project, payback period is calculating by this

formula which is as under:

Payback period = Total initial capital investment/Annual cash flows

It is the simplest technique which required less computation than other techniques (Cottam, H., 2018). It is simple to

understand as the terms used in it are easy. It also depicts the risk associated with the projects as lengthy the project, higher will be the

risk and vice-versa. On the other hand, the biggest limitation of this technique is that it avoids time value of money. It ignores the

returns after the payback period as it considers only returns which required to cover its initial cost. This technique would avoid lengthy

projects having a long time duration.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting rate of return is the rate shows percentage of income generated in the overall period of project on the initial cost

incurred (Getzen and et.al, 2022). This technique assists the management to check whether the project is capable to generate income

equal to standard return or otherwise it will be non-beneficial for the business. This can be calculated as follows:

Average rate of return = Average net income/Initial cost outflow

This technique uses financial data from the financial reports prepared at the year end. It does not require any specified data.

This technique can be used to evaluate performance of the project over the period. This is a commonly used technique. It undertakes

all the return generated over the period without making any differentiation. Likewise, the above technique, it also avoids time value of

money concept which is an essential concept. It requires pre-determined data in financial reports which can be based upon different

accounting processes followed by the business entity. This technique requires net income generated by the project rather than original

cash flow. It only considers total cash outflow regarding the project and avoids other required cash outflows.

Net Present Value is most popular technique for capital appraisal. This undertakes the concept of time value of money (Huang

and et.al, 2019). In this technique, cash inflows and cash outflows occurred are adjusted with the discounting rate. Discounting rate is

determined by considering the return factor. It takes into account view that cash flow earned in recent years is more precious than cash

flows earned within the late years of the project. NPV is calculated as under:

Net present value = Present value of cash inflows – present value of cash outflows

Recommendations: On the basis of above calculations, it can be said that as the payback period is less than the complete life of

project which depicts that project is able to recuperate the cost which have incurred earlier. Further, ARR also present that project is

able to generate revenue but net present value of project is negative which shows that even the project is able to generate revenue but

it would not be efficient for enhance the profit earning capability. As the NPV is an absolute measure therefore management should

reject the project.

PART B

incurred (Getzen and et.al, 2022). This technique assists the management to check whether the project is capable to generate income

equal to standard return or otherwise it will be non-beneficial for the business. This can be calculated as follows:

Average rate of return = Average net income/Initial cost outflow

This technique uses financial data from the financial reports prepared at the year end. It does not require any specified data.

This technique can be used to evaluate performance of the project over the period. This is a commonly used technique. It undertakes

all the return generated over the period without making any differentiation. Likewise, the above technique, it also avoids time value of

money concept which is an essential concept. It requires pre-determined data in financial reports which can be based upon different

accounting processes followed by the business entity. This technique requires net income generated by the project rather than original

cash flow. It only considers total cash outflow regarding the project and avoids other required cash outflows.

Net Present Value is most popular technique for capital appraisal. This undertakes the concept of time value of money (Huang

and et.al, 2019). In this technique, cash inflows and cash outflows occurred are adjusted with the discounting rate. Discounting rate is

determined by considering the return factor. It takes into account view that cash flow earned in recent years is more precious than cash

flows earned within the late years of the project. NPV is calculated as under:

Net present value = Present value of cash inflows – present value of cash outflows

Recommendations: On the basis of above calculations, it can be said that as the payback period is less than the complete life of

project which depicts that project is able to recuperate the cost which have incurred earlier. Further, ARR also present that project is

able to generate revenue but net present value of project is negative which shows that even the project is able to generate revenue but

it would not be efficient for enhance the profit earning capability. As the NPV is an absolute measure therefore management should

reject the project.

PART B

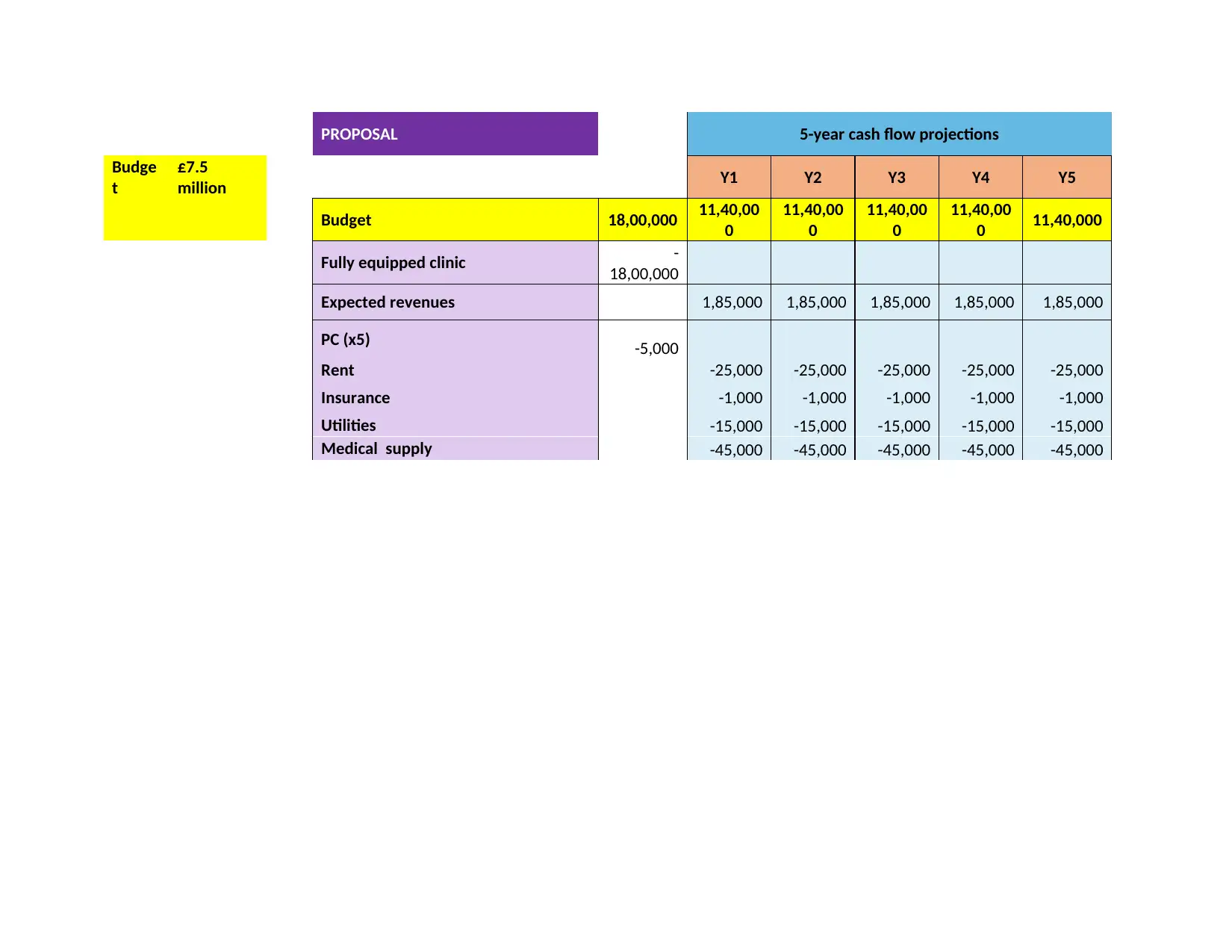

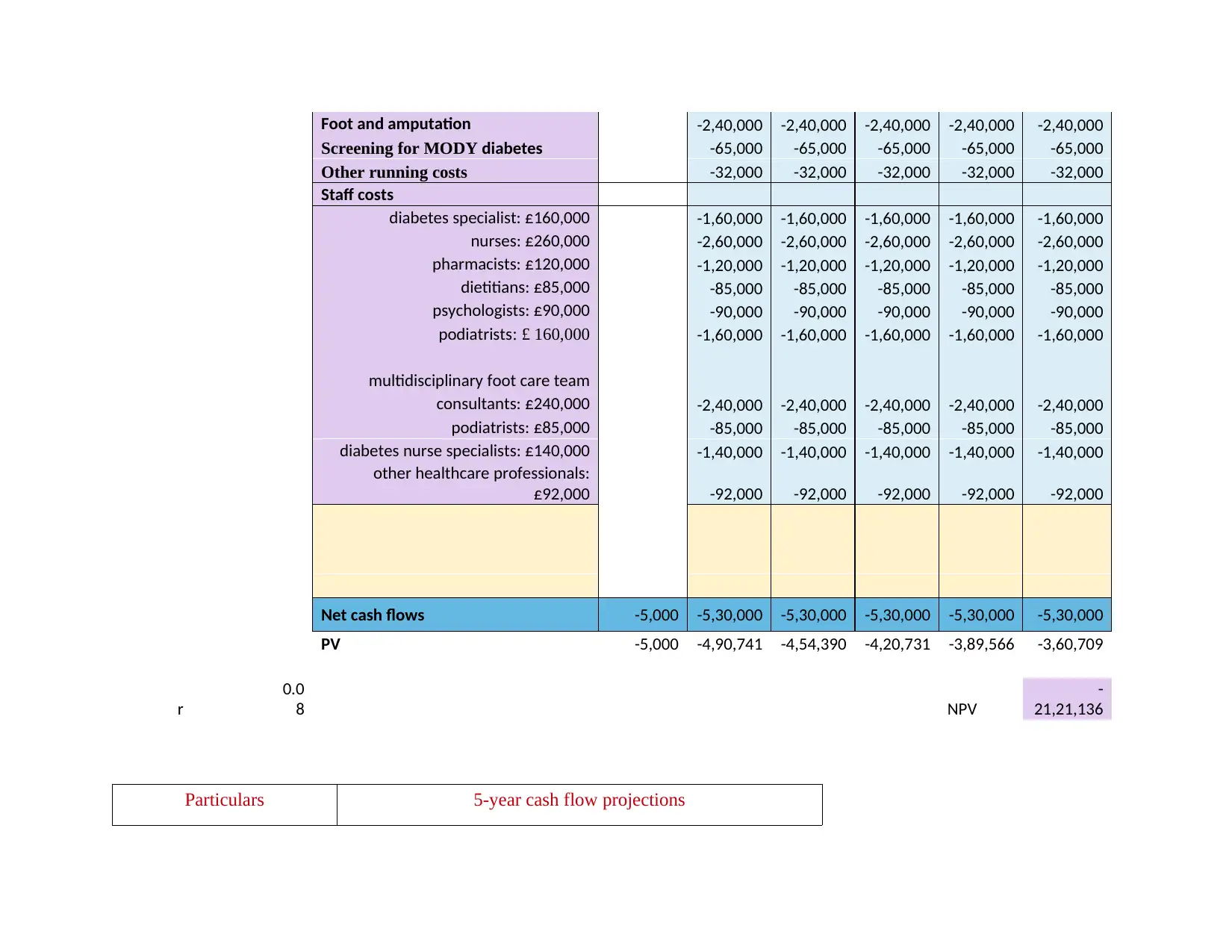

PROPOSAL 5-year cash flow projections

Budge

t

£7.5

million Y1 Y2 Y3 Y4 Y5

Budget 18,00,000 11,40,00

0

11,40,00

0

11,40,00

0

11,40,00

0 11,40,000

Fully equipped clinic -

18,00,000

Expected revenues 1,85,000 1,85,000 1,85,000 1,85,000 1,85,000

PC (x5) -5,000

Rent -25,000 -25,000 -25,000 -25,000 -25,000

Insurance -1,000 -1,000 -1,000 -1,000 -1,000

Utilities -15,000 -15,000 -15,000 -15,000 -15,000

Medical supply -45,000 -45,000 -45,000 -45,000 -45,000

Budge

t

£7.5

million Y1 Y2 Y3 Y4 Y5

Budget 18,00,000 11,40,00

0

11,40,00

0

11,40,00

0

11,40,00

0 11,40,000

Fully equipped clinic -

18,00,000

Expected revenues 1,85,000 1,85,000 1,85,000 1,85,000 1,85,000

PC (x5) -5,000

Rent -25,000 -25,000 -25,000 -25,000 -25,000

Insurance -1,000 -1,000 -1,000 -1,000 -1,000

Utilities -15,000 -15,000 -15,000 -15,000 -15,000

Medical supply -45,000 -45,000 -45,000 -45,000 -45,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Foot and amputation -2,40,000 -2,40,000 -2,40,000 -2,40,000 -2,40,000

Screening for MODY diabetes -65,000 -65,000 -65,000 -65,000 -65,000

Other running costs -32,000 -32,000 -32,000 -32,000 -32,000

Staff costs

diabetes specialist: £160,000 -1,60,000 -1,60,000 -1,60,000 -1,60,000 -1,60,000

nurses: £260,000 -2,60,000 -2,60,000 -2,60,000 -2,60,000 -2,60,000

pharmacists: £120,000 -1,20,000 -1,20,000 -1,20,000 -1,20,000 -1,20,000

dietitians: £85,000 -85,000 -85,000 -85,000 -85,000 -85,000

psychologists: £90,000 -90,000 -90,000 -90,000 -90,000 -90,000

podiatrists: £ 160,000 -1,60,000 -1,60,000 -1,60,000 -1,60,000 -1,60,000

multidisciplinary foot care team

consultants: £240,000 -2,40,000 -2,40,000 -2,40,000 -2,40,000 -2,40,000

podiatrists: £85,000 -85,000 -85,000 -85,000 -85,000 -85,000

diabetes nurse specialists: £140,000 -1,40,000 -1,40,000 -1,40,000 -1,40,000 -1,40,000

other healthcare professionals:

£92,000 -92,000 -92,000 -92,000 -92,000 -92,000

Net cash flows -5,000 -5,30,000 -5,30,000 -5,30,000 -5,30,000 -5,30,000

PV -5,000 -4,90,741 -4,54,390 -4,20,731 -3,89,566 -3,60,709

r

0.0

8 NPV

-

21,21,136

Particulars 5-year cash flow projections

Screening for MODY diabetes -65,000 -65,000 -65,000 -65,000 -65,000

Other running costs -32,000 -32,000 -32,000 -32,000 -32,000

Staff costs

diabetes specialist: £160,000 -1,60,000 -1,60,000 -1,60,000 -1,60,000 -1,60,000

nurses: £260,000 -2,60,000 -2,60,000 -2,60,000 -2,60,000 -2,60,000

pharmacists: £120,000 -1,20,000 -1,20,000 -1,20,000 -1,20,000 -1,20,000

dietitians: £85,000 -85,000 -85,000 -85,000 -85,000 -85,000

psychologists: £90,000 -90,000 -90,000 -90,000 -90,000 -90,000

podiatrists: £ 160,000 -1,60,000 -1,60,000 -1,60,000 -1,60,000 -1,60,000

multidisciplinary foot care team

consultants: £240,000 -2,40,000 -2,40,000 -2,40,000 -2,40,000 -2,40,000

podiatrists: £85,000 -85,000 -85,000 -85,000 -85,000 -85,000

diabetes nurse specialists: £140,000 -1,40,000 -1,40,000 -1,40,000 -1,40,000 -1,40,000

other healthcare professionals:

£92,000 -92,000 -92,000 -92,000 -92,000 -92,000

Net cash flows -5,000 -5,30,000 -5,30,000 -5,30,000 -5,30,000 -5,30,000

PV -5,000 -4,90,741 -4,54,390 -4,20,731 -3,89,566 -3,60,709

r

0.0

8 NPV

-

21,21,136

Particulars 5-year cash flow projections

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

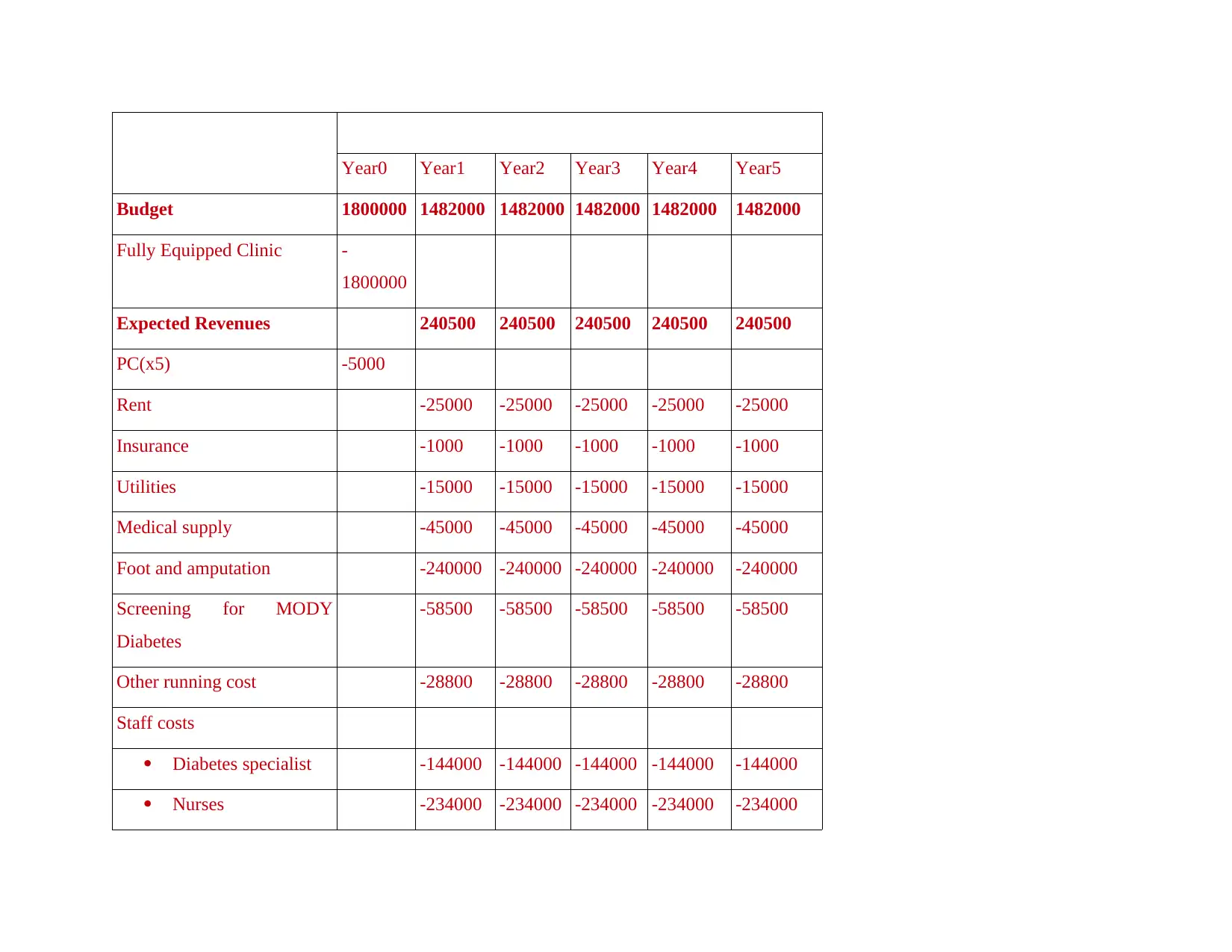

Year0 Year1 Year2 Year3 Year4 Year5

Budget 1800000 1482000 1482000 1482000 1482000 1482000

Fully Equipped Clinic -

1800000

Expected Revenues 240500 240500 240500 240500 240500

PC(x5) -5000

Rent -25000 -25000 -25000 -25000 -25000

Insurance -1000 -1000 -1000 -1000 -1000

Utilities -15000 -15000 -15000 -15000 -15000

Medical supply -45000 -45000 -45000 -45000 -45000

Foot and amputation -240000 -240000 -240000 -240000 -240000

Screening for MODY

Diabetes

-58500 -58500 -58500 -58500 -58500

Other running cost -28800 -28800 -28800 -28800 -28800

Staff costs

Diabetes specialist -144000 -144000 -144000 -144000 -144000

Nurses -234000 -234000 -234000 -234000 -234000

Budget 1800000 1482000 1482000 1482000 1482000 1482000

Fully Equipped Clinic -

1800000

Expected Revenues 240500 240500 240500 240500 240500

PC(x5) -5000

Rent -25000 -25000 -25000 -25000 -25000

Insurance -1000 -1000 -1000 -1000 -1000

Utilities -15000 -15000 -15000 -15000 -15000

Medical supply -45000 -45000 -45000 -45000 -45000

Foot and amputation -240000 -240000 -240000 -240000 -240000

Screening for MODY

Diabetes

-58500 -58500 -58500 -58500 -58500

Other running cost -28800 -28800 -28800 -28800 -28800

Staff costs

Diabetes specialist -144000 -144000 -144000 -144000 -144000

Nurses -234000 -234000 -234000 -234000 -234000

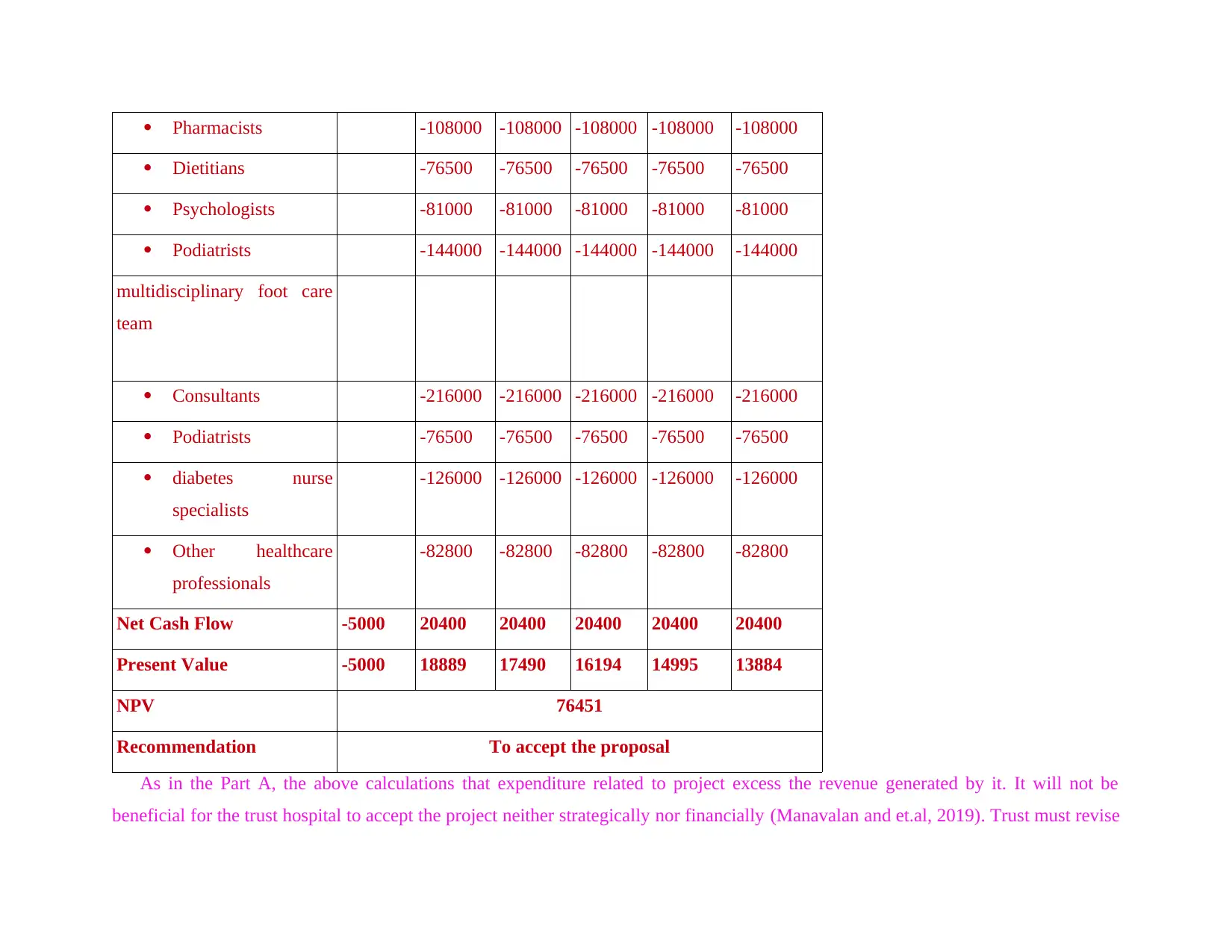

Pharmacists -108000 -108000 -108000 -108000 -108000

Dietitians -76500 -76500 -76500 -76500 -76500

Psychologists -81000 -81000 -81000 -81000 -81000

Podiatrists -144000 -144000 -144000 -144000 -144000

multidisciplinary foot care

team

Consultants -216000 -216000 -216000 -216000 -216000

Podiatrists -76500 -76500 -76500 -76500 -76500

diabetes nurse

specialists

-126000 -126000 -126000 -126000 -126000

Other healthcare

professionals

-82800 -82800 -82800 -82800 -82800

Net Cash Flow -5000 20400 20400 20400 20400 20400

Present Value -5000 18889 17490 16194 14995 13884

NPV 76451

Recommendation To accept the proposal

As in the Part A, the above calculations that expenditure related to project excess the revenue generated by it. It will not be

beneficial for the trust hospital to accept the project neither strategically nor financially (Manavalan and et.al, 2019). Trust must revise

Dietitians -76500 -76500 -76500 -76500 -76500

Psychologists -81000 -81000 -81000 -81000 -81000

Podiatrists -144000 -144000 -144000 -144000 -144000

multidisciplinary foot care

team

Consultants -216000 -216000 -216000 -216000 -216000

Podiatrists -76500 -76500 -76500 -76500 -76500

diabetes nurse

specialists

-126000 -126000 -126000 -126000 -126000

Other healthcare

professionals

-82800 -82800 -82800 -82800 -82800

Net Cash Flow -5000 20400 20400 20400 20400 20400

Present Value -5000 18889 17490 16194 14995 13884

NPV 76451

Recommendation To accept the proposal

As in the Part A, the above calculations that expenditure related to project excess the revenue generated by it. It will not be

beneficial for the trust hospital to accept the project neither strategically nor financially (Manavalan and et.al, 2019). Trust must revise

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.