Financial Management Report: NPV Analysis for Hamilton Inc. Project

VerifiedAdded on 2023/01/12

|13

|3851

|57

Report

AI Summary

This report delves into financial management principles, particularly focusing on Net Present Value (NPV) and investment appraisal techniques. It uses a case study of Hamilton Inc., a sports equipment manufacturer, to illustrate the application of NPV in evaluating capital investment projects, specifically the replacement of manufacturing machinery. The report calculates and compares the NPV of two proposals: continuing with existing equipment versus investing in new machinery. It provides detailed calculations, working notes, and recommendations for Hamilton Inc., considering factors like cash flows, discount rates, and initial investments. Furthermore, the report critically discusses the use of NPV as an investment appraisal method, outlining its advantages and disadvantages, and suggesting alternative appraisal techniques. The report is a valuable resource for students studying financial management and investment analysis. The report also stresses the importance of brand value and equity for Hamilton Inc. It further recommends that the company should not rely on just one investment appraisal technique like NPV and should also use other techniques like payback period, internal rate of return and annual rate of return to arrive at a more informed decision.

Financial management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

Calculating the net present value.................................................................................................1

Explaining which project should be accepted.............................................................................4

Recommendations........................................................................................................................5

Critically discussing the use of net present value as a method of investment appraisal..............6

Use of alternative approaches to capital investment appraisal....................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

Calculating the net present value.................................................................................................1

Explaining which project should be accepted.............................................................................4

Recommendations........................................................................................................................5

Critically discussing the use of net present value as a method of investment appraisal..............6

Use of alternative approaches to capital investment appraisal....................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial management is the procedure of managing the financial resources, recording and

presentation of an organisation which can assist in procedure of decision making. The concept of

financial management is said to be used in three parameters which are investment decision,

financing decision and dividend decision (Altman and et.al., 2017). The main aim of this report

is to develop an understanding about the concepts of quantitative and qualitative accounting

information in an organisation. For this purpose, an organisation is selected which is Hamilton

Inc. This organisation is a sports equipment manufacturer which is located in USA. This

company is a growing organisation and continuously advancing their technologies. This

company is considering purchase of a new machinery and for this proposal technique of NPV is

used in order to analyse its viability.

In this report, financial analysis will be conducted in which net present value of both the

proposals will be evaluated along with a detailed explanation. Further, this report will cover

recommendations for this company which will be based on NPV computation. At last, the

investment appraisal technique of net present value will be analysed along with few alternative

approaches of net present value.

QUESTION 1

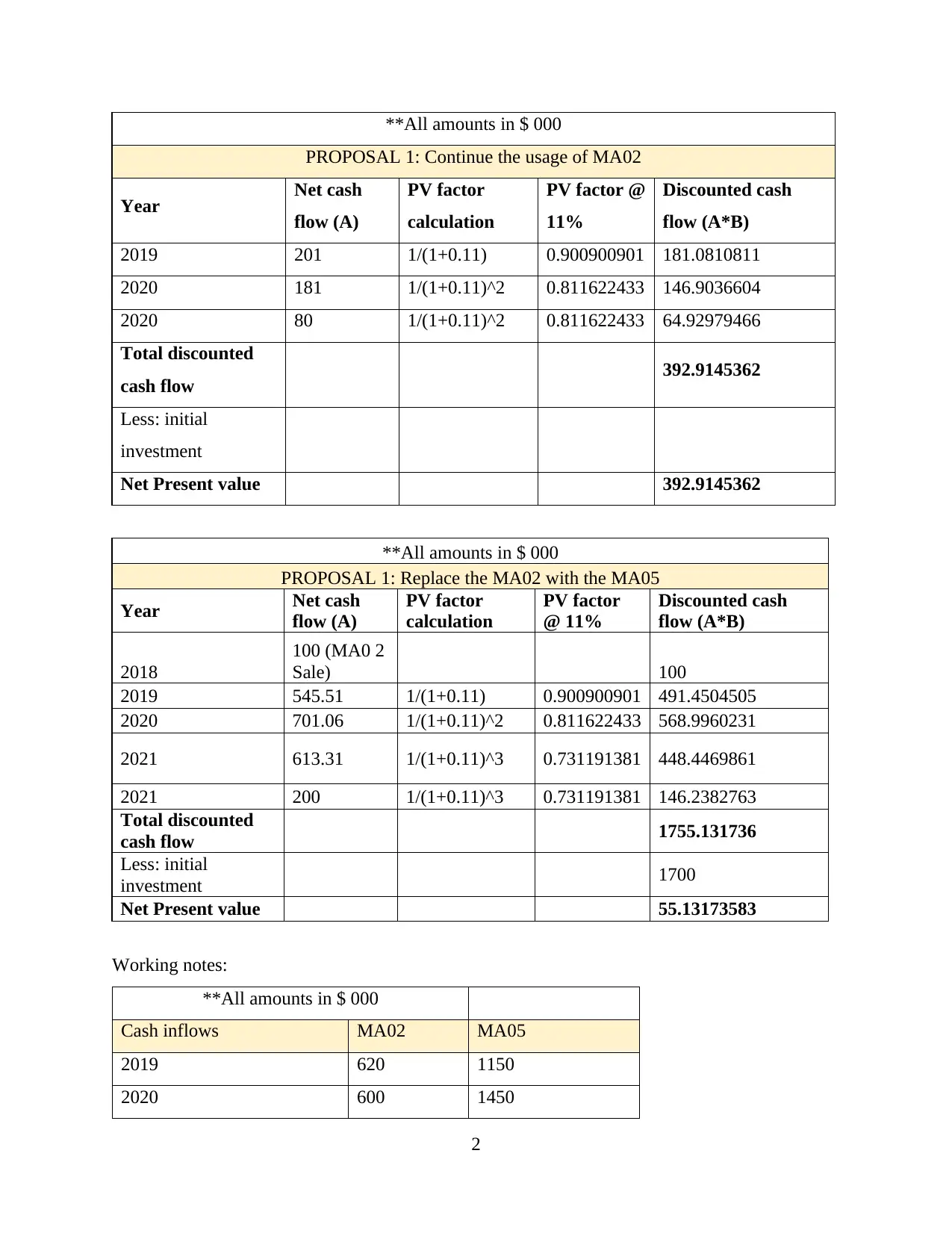

Calculating the net present value

Hamilton Inc. is an organisation which manufacture sports equipment. This company is

considering replacing one of their basketball manufacturing machinery (MA02) with an

advanced machinery (MA05). It is believed that MA05 will produce higher quality basketballs

which will result in increase in sales.

There are total of two proposals which Hamilton Inc. is considering. The first proposal

states that company will continue the use of MA02 till 2020 and then sell it with the residual

value of $80,000. The Second proposal states that the company will replace MA02 with MA05

in which MA05 will be acquired for $ 1.7 million and MA02 will immediately sold for $100,000

and after three years MA05 will also be sold for $200,000. Considering determinants for both the

proposals and inflation rates. The NPV for both the projects are computed below along with

extensive working notes:

1

Financial management is the procedure of managing the financial resources, recording and

presentation of an organisation which can assist in procedure of decision making. The concept of

financial management is said to be used in three parameters which are investment decision,

financing decision and dividend decision (Altman and et.al., 2017). The main aim of this report

is to develop an understanding about the concepts of quantitative and qualitative accounting

information in an organisation. For this purpose, an organisation is selected which is Hamilton

Inc. This organisation is a sports equipment manufacturer which is located in USA. This

company is a growing organisation and continuously advancing their technologies. This

company is considering purchase of a new machinery and for this proposal technique of NPV is

used in order to analyse its viability.

In this report, financial analysis will be conducted in which net present value of both the

proposals will be evaluated along with a detailed explanation. Further, this report will cover

recommendations for this company which will be based on NPV computation. At last, the

investment appraisal technique of net present value will be analysed along with few alternative

approaches of net present value.

QUESTION 1

Calculating the net present value

Hamilton Inc. is an organisation which manufacture sports equipment. This company is

considering replacing one of their basketball manufacturing machinery (MA02) with an

advanced machinery (MA05). It is believed that MA05 will produce higher quality basketballs

which will result in increase in sales.

There are total of two proposals which Hamilton Inc. is considering. The first proposal

states that company will continue the use of MA02 till 2020 and then sell it with the residual

value of $80,000. The Second proposal states that the company will replace MA02 with MA05

in which MA05 will be acquired for $ 1.7 million and MA02 will immediately sold for $100,000

and after three years MA05 will also be sold for $200,000. Considering determinants for both the

proposals and inflation rates. The NPV for both the projects are computed below along with

extensive working notes:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

**All amounts in $ 000

PROPOSAL 1: Continue the usage of MA02

Year Net cash

flow (A)

PV factor

calculation

PV factor @

11%

Discounted cash

flow (A*B)

2019 201 1/(1+0.11) 0.900900901 181.0810811

2020 181 1/(1+0.11)^2 0.811622433 146.9036604

2020 80 1/(1+0.11)^2 0.811622433 64.92979466

Total discounted

cash flow 392.9145362

Less: initial

investment

Net Present value 392.9145362

**All amounts in $ 000

PROPOSAL 1: Replace the MA02 with the MA05

Year Net cash

flow (A)

PV factor

calculation

PV factor

@ 11%

Discounted cash

flow (A*B)

2018

100 (MA0 2

Sale) 100

2019 545.51 1/(1+0.11) 0.900900901 491.4504505

2020 701.06 1/(1+0.11)^2 0.811622433 568.9960231

2021 613.31 1/(1+0.11)^3 0.731191381 448.4469861

2021 200 1/(1+0.11)^3 0.731191381 146.2382763

Total discounted

cash flow 1755.131736

Less: initial

investment 1700

Net Present value 55.13173583

Working notes:

**All amounts in $ 000

Cash inflows MA02 MA05

2019 620 1150

2020 600 1450

2

PROPOSAL 1: Continue the usage of MA02

Year Net cash

flow (A)

PV factor

calculation

PV factor @

11%

Discounted cash

flow (A*B)

2019 201 1/(1+0.11) 0.900900901 181.0810811

2020 181 1/(1+0.11)^2 0.811622433 146.9036604

2020 80 1/(1+0.11)^2 0.811622433 64.92979466

Total discounted

cash flow 392.9145362

Less: initial

investment

Net Present value 392.9145362

**All amounts in $ 000

PROPOSAL 1: Replace the MA02 with the MA05

Year Net cash

flow (A)

PV factor

calculation

PV factor

@ 11%

Discounted cash

flow (A*B)

2018

100 (MA0 2

Sale) 100

2019 545.51 1/(1+0.11) 0.900900901 491.4504505

2020 701.06 1/(1+0.11)^2 0.811622433 568.9960231

2021 613.31 1/(1+0.11)^3 0.731191381 448.4469861

2021 200 1/(1+0.11)^3 0.731191381 146.2382763

Total discounted

cash flow 1755.131736

Less: initial

investment 1700

Net Present value 55.13173583

Working notes:

**All amounts in $ 000

Cash inflows MA02 MA05

2019 620 1150

2020 600 1450

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

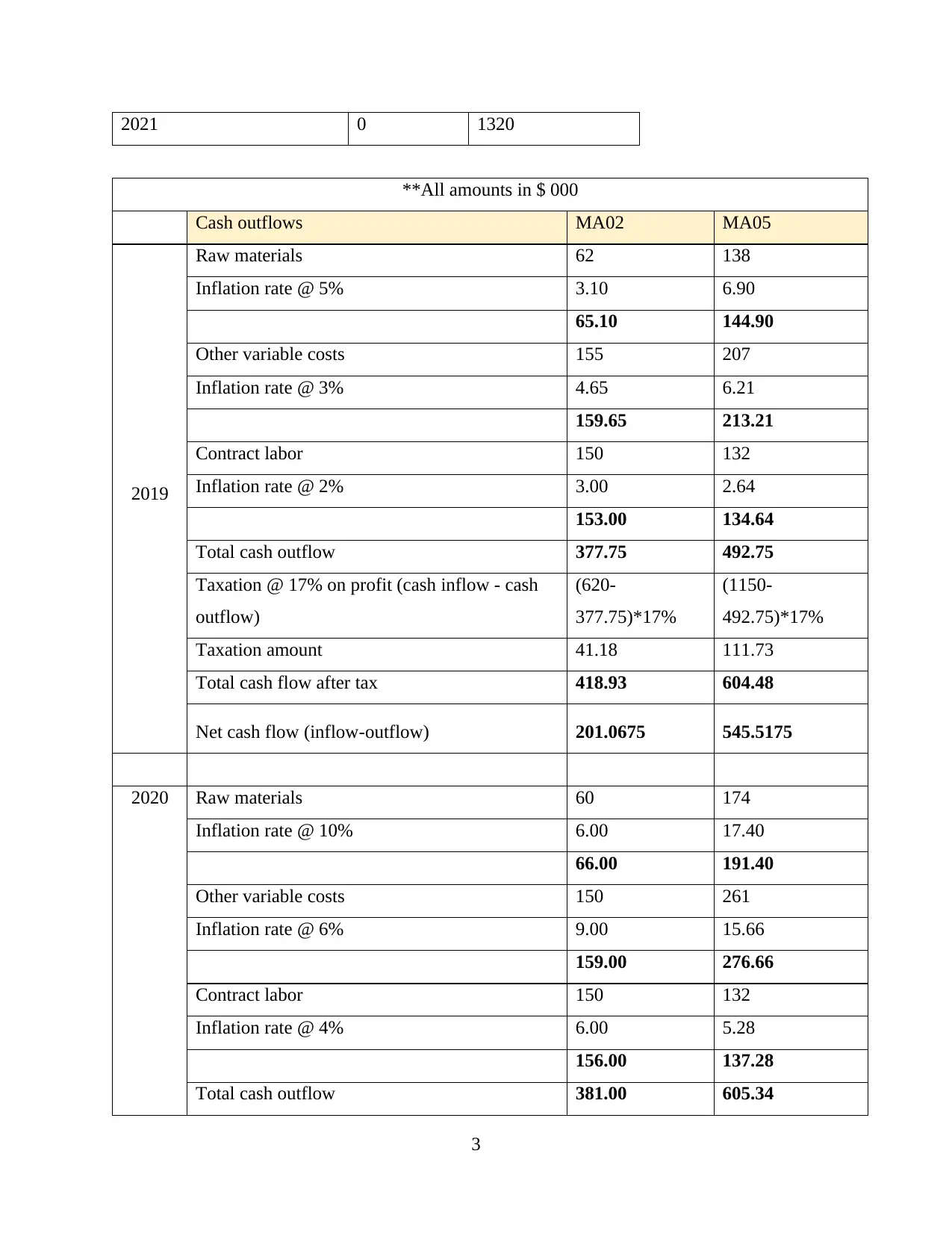

2021 0 1320

**All amounts in $ 000

Cash outflows MA02 MA05

2019

Raw materials 62 138

Inflation rate @ 5% 3.10 6.90

65.10 144.90

Other variable costs 155 207

Inflation rate @ 3% 4.65 6.21

159.65 213.21

Contract labor 150 132

Inflation rate @ 2% 3.00 2.64

153.00 134.64

Total cash outflow 377.75 492.75

Taxation @ 17% on profit (cash inflow - cash

outflow)

(620-

377.75)*17%

(1150-

492.75)*17%

Taxation amount 41.18 111.73

Total cash flow after tax 418.93 604.48

Net cash flow (inflow-outflow) 201.0675 545.5175

2020 Raw materials 60 174

Inflation rate @ 10% 6.00 17.40

66.00 191.40

Other variable costs 150 261

Inflation rate @ 6% 9.00 15.66

159.00 276.66

Contract labor 150 132

Inflation rate @ 4% 6.00 5.28

156.00 137.28

Total cash outflow 381.00 605.34

3

**All amounts in $ 000

Cash outflows MA02 MA05

2019

Raw materials 62 138

Inflation rate @ 5% 3.10 6.90

65.10 144.90

Other variable costs 155 207

Inflation rate @ 3% 4.65 6.21

159.65 213.21

Contract labor 150 132

Inflation rate @ 2% 3.00 2.64

153.00 134.64

Total cash outflow 377.75 492.75

Taxation @ 17% on profit (cash inflow - cash

outflow)

(620-

377.75)*17%

(1150-

492.75)*17%

Taxation amount 41.18 111.73

Total cash flow after tax 418.93 604.48

Net cash flow (inflow-outflow) 201.0675 545.5175

2020 Raw materials 60 174

Inflation rate @ 10% 6.00 17.40

66.00 191.40

Other variable costs 150 261

Inflation rate @ 6% 9.00 15.66

159.00 276.66

Contract labor 150 132

Inflation rate @ 4% 6.00 5.28

156.00 137.28

Total cash outflow 381.00 605.34

3

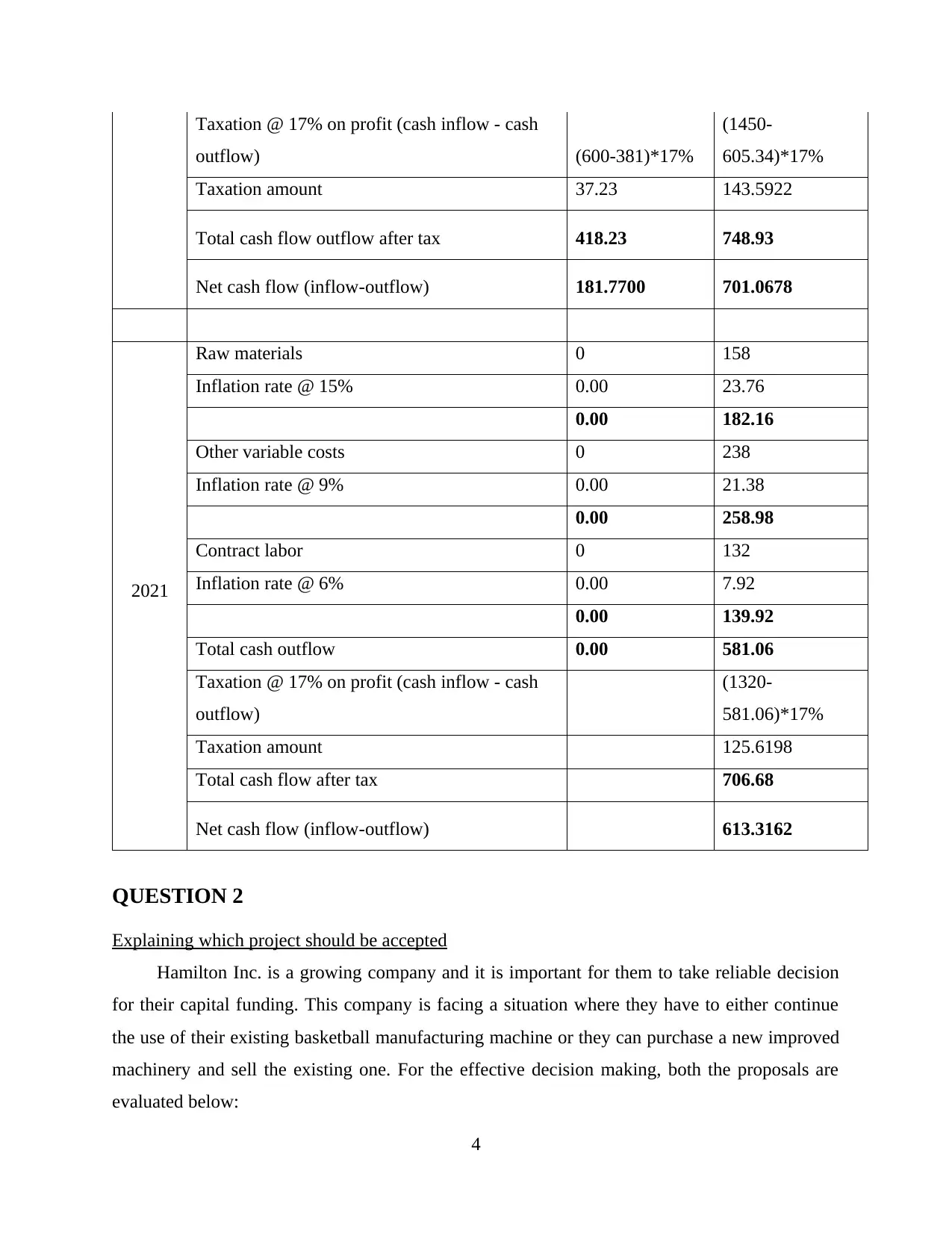

Taxation @ 17% on profit (cash inflow - cash

outflow) (600-381)*17%

(1450-

605.34)*17%

Taxation amount 37.23 143.5922

Total cash flow outflow after tax 418.23 748.93

Net cash flow (inflow-outflow) 181.7700 701.0678

2021

Raw materials 0 158

Inflation rate @ 15% 0.00 23.76

0.00 182.16

Other variable costs 0 238

Inflation rate @ 9% 0.00 21.38

0.00 258.98

Contract labor 0 132

Inflation rate @ 6% 0.00 7.92

0.00 139.92

Total cash outflow 0.00 581.06

Taxation @ 17% on profit (cash inflow - cash

outflow)

(1320-

581.06)*17%

Taxation amount 125.6198

Total cash flow after tax 706.68

Net cash flow (inflow-outflow) 613.3162

QUESTION 2

Explaining which project should be accepted

Hamilton Inc. is a growing company and it is important for them to take reliable decision

for their capital funding. This company is facing a situation where they have to either continue

the use of their existing basketball manufacturing machine or they can purchase a new improved

machinery and sell the existing one. For the effective decision making, both the proposals are

evaluated below:

4

outflow) (600-381)*17%

(1450-

605.34)*17%

Taxation amount 37.23 143.5922

Total cash flow outflow after tax 418.23 748.93

Net cash flow (inflow-outflow) 181.7700 701.0678

2021

Raw materials 0 158

Inflation rate @ 15% 0.00 23.76

0.00 182.16

Other variable costs 0 238

Inflation rate @ 9% 0.00 21.38

0.00 258.98

Contract labor 0 132

Inflation rate @ 6% 0.00 7.92

0.00 139.92

Total cash outflow 0.00 581.06

Taxation @ 17% on profit (cash inflow - cash

outflow)

(1320-

581.06)*17%

Taxation amount 125.6198

Total cash flow after tax 706.68

Net cash flow (inflow-outflow) 613.3162

QUESTION 2

Explaining which project should be accepted

Hamilton Inc. is a growing company and it is important for them to take reliable decision

for their capital funding. This company is facing a situation where they have to either continue

the use of their existing basketball manufacturing machine or they can purchase a new improved

machinery and sell the existing one. For the effective decision making, both the proposals are

evaluated below:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Proposal 1:

In first proposal, company is considering continuing the use of their existing basketball

manufacturing machine which is MA02. If company continue the use of this machinery, then

they can gain the total cash inflow of $1220000 in the period of two years. Net present value of

this proposal is $393000 approximately. This NPV is the sum of total net cash flows of the

company and the residual value which will be gained in 2020 after the sale of this machine.

Proposal 2:

In second proposal, company is considering sale of their existing machinery and purchase

of a new one. In this situation, company will gain the residual value of MA02 as $100000. Net

present value which this company will gain by this proposal is $55000.

After analysing both the projects, it has been observed that Proposal 1 is better than

proposal 2. By selecting proposal 1, company can use their existing machine and after the year

2020, they can sell their existing machine and then buy a new improved machinery. This will

reduce the loss which company would have gain due to sell of MA02 at residual value and will

also save the cost 1.7 million of new machine. Selection of proposal 2 is also an option for this

company as in this improved quality products will be manufactured which will improve the

brand equity of this company but company has to gather funds to bear the loss of not selecting a

high NPV proposal.

QUESTION 3

Recommendations

The proposal of buying a new machinery MA05 will help Hamilton Inc. to enhance their

brand equity as by this company can manufacture quality basketball by the use of new improved

technique. This machinery will enhance the sales of this company. From the NPV calculation, it

is evident that net sales of this company by the use of MA05 will be $1150000 in 2019,

$1450000 in 2012. These sales are way better than the sales from MA02 which are $620000 in

2019 and $600000 in 2020.

Even after the high sales, the NPV of this proposal is only $55000. This low NPV is the

result of high initial investment value of this company 1.7 million.

After the above analysis, there are few recommendations for Hamilton Inc. mentioned as

follows:

5

In first proposal, company is considering continuing the use of their existing basketball

manufacturing machine which is MA02. If company continue the use of this machinery, then

they can gain the total cash inflow of $1220000 in the period of two years. Net present value of

this proposal is $393000 approximately. This NPV is the sum of total net cash flows of the

company and the residual value which will be gained in 2020 after the sale of this machine.

Proposal 2:

In second proposal, company is considering sale of their existing machinery and purchase

of a new one. In this situation, company will gain the residual value of MA02 as $100000. Net

present value which this company will gain by this proposal is $55000.

After analysing both the projects, it has been observed that Proposal 1 is better than

proposal 2. By selecting proposal 1, company can use their existing machine and after the year

2020, they can sell their existing machine and then buy a new improved machinery. This will

reduce the loss which company would have gain due to sell of MA02 at residual value and will

also save the cost 1.7 million of new machine. Selection of proposal 2 is also an option for this

company as in this improved quality products will be manufactured which will improve the

brand equity of this company but company has to gather funds to bear the loss of not selecting a

high NPV proposal.

QUESTION 3

Recommendations

The proposal of buying a new machinery MA05 will help Hamilton Inc. to enhance their

brand equity as by this company can manufacture quality basketball by the use of new improved

technique. This machinery will enhance the sales of this company. From the NPV calculation, it

is evident that net sales of this company by the use of MA05 will be $1150000 in 2019,

$1450000 in 2012. These sales are way better than the sales from MA02 which are $620000 in

2019 and $600000 in 2020.

Even after the high sales, the NPV of this proposal is only $55000. This low NPV is the

result of high initial investment value of this company 1.7 million.

After the above analysis, there are few recommendations for Hamilton Inc. mentioned as

follows:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is necessary to enhance the brand value and equity of Hamilton Inc., but this can also

be done once the MA02 is sold to its residual value in 2020.

The net present value of proposal 1 is more than proposal 2 which is $392000 and

$55000 respectively. Due to this, Hamilton Inc. is recommended to continue the use of

their existing machine by which they will be able to fully utilise their machinery and once

the machine is obsolete they can buy an improved one.

It is also recommended to this company that they should not rely their decisions on just

one investment appraisal technique that is NPV. Hamilton Inc. should also use other

techniques as well such as Payback period, internal rate of return and annual rate of

return. By using these techniques company will also have an alternative to rely upon.

Hamilton Inc. is also recommended to charge depreciation on its machineries as by this

company will be able to know the actual value of their machineries and their books of

accounts will also be improved. The recommended technique to charge depreciation is

written down value method.

QUESTION 4

Critically discussing the use of net present value as a method of investment appraisal

Investment appraisal is the process of analysing an investment in order to check its

reliability and viability for the purpose of assisting an organisation in decision making

(Antonopoulos and Hall, 2016). There are various techniques by which, investment can be

appraised. One of these techniques is Net present value.

Net present value is the difference between all cash inflows and cash outflows of a

company. This technique is used by an organisation to calculate the intrinsic value of their

organisation’s investment (Banerjee and et.al., 2016). This technique includes cash inflows such

as sales revenues and cash flows such as raw materials, taxes, rent, wages etc. These inflows and

outflows are subtracted to calculate the net cash flows in a specific period. The value of this net

cash flow is then discounted using a cost of capital. The reason behind discounting these cash

flows is to adjust the risk which can be occurred due to the investment and to account the time

value of the money. The reason behind the appropriateness of this technique is its discounting

procedure as by this, contingencies which can be faced in future are well accounted by

discounting the cash flows (Chand, 2019).

Net present value can be calculated by using the below formula:

6

be done once the MA02 is sold to its residual value in 2020.

The net present value of proposal 1 is more than proposal 2 which is $392000 and

$55000 respectively. Due to this, Hamilton Inc. is recommended to continue the use of

their existing machine by which they will be able to fully utilise their machinery and once

the machine is obsolete they can buy an improved one.

It is also recommended to this company that they should not rely their decisions on just

one investment appraisal technique that is NPV. Hamilton Inc. should also use other

techniques as well such as Payback period, internal rate of return and annual rate of

return. By using these techniques company will also have an alternative to rely upon.

Hamilton Inc. is also recommended to charge depreciation on its machineries as by this

company will be able to know the actual value of their machineries and their books of

accounts will also be improved. The recommended technique to charge depreciation is

written down value method.

QUESTION 4

Critically discussing the use of net present value as a method of investment appraisal

Investment appraisal is the process of analysing an investment in order to check its

reliability and viability for the purpose of assisting an organisation in decision making

(Antonopoulos and Hall, 2016). There are various techniques by which, investment can be

appraised. One of these techniques is Net present value.

Net present value is the difference between all cash inflows and cash outflows of a

company. This technique is used by an organisation to calculate the intrinsic value of their

organisation’s investment (Banerjee and et.al., 2016). This technique includes cash inflows such

as sales revenues and cash flows such as raw materials, taxes, rent, wages etc. These inflows and

outflows are subtracted to calculate the net cash flows in a specific period. The value of this net

cash flow is then discounted using a cost of capital. The reason behind discounting these cash

flows is to adjust the risk which can be occurred due to the investment and to account the time

value of the money. The reason behind the appropriateness of this technique is its discounting

procedure as by this, contingencies which can be faced in future are well accounted by

discounting the cash flows (Chand, 2019).

Net present value can be calculated by using the below formula:

6

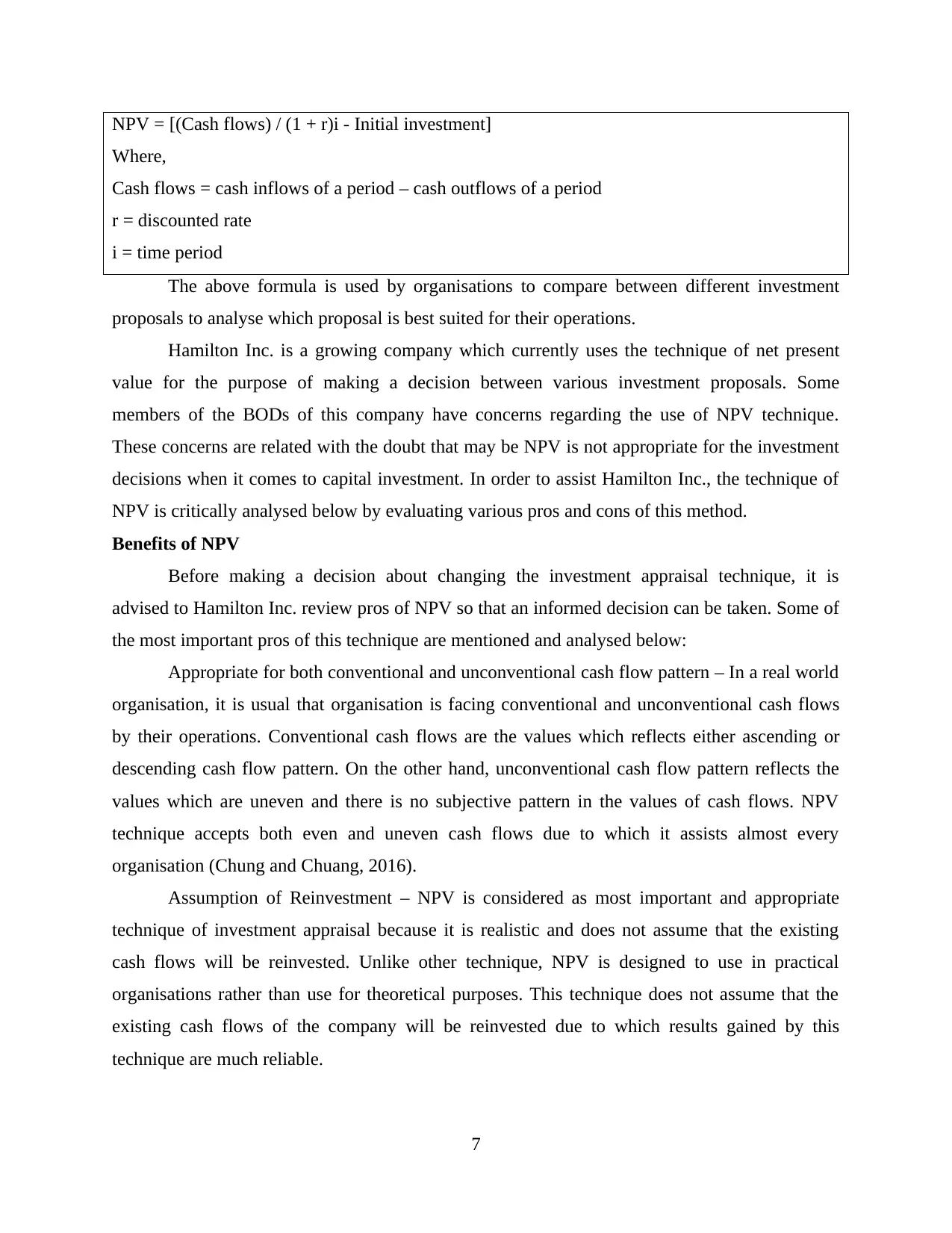

NPV = [(Cash flows) / (1 + r)i - Initial investment]

Where,

Cash flows = cash inflows of a period – cash outflows of a period

r = discounted rate

i = time period

The above formula is used by organisations to compare between different investment

proposals to analyse which proposal is best suited for their operations.

Hamilton Inc. is a growing company which currently uses the technique of net present

value for the purpose of making a decision between various investment proposals. Some

members of the BODs of this company have concerns regarding the use of NPV technique.

These concerns are related with the doubt that may be NPV is not appropriate for the investment

decisions when it comes to capital investment. In order to assist Hamilton Inc., the technique of

NPV is critically analysed below by evaluating various pros and cons of this method.

Benefits of NPV

Before making a decision about changing the investment appraisal technique, it is

advised to Hamilton Inc. review pros of NPV so that an informed decision can be taken. Some of

the most important pros of this technique are mentioned and analysed below:

Appropriate for both conventional and unconventional cash flow pattern – In a real world

organisation, it is usual that organisation is facing conventional and unconventional cash flows

by their operations. Conventional cash flows are the values which reflects either ascending or

descending cash flow pattern. On the other hand, unconventional cash flow pattern reflects the

values which are uneven and there is no subjective pattern in the values of cash flows. NPV

technique accepts both even and uneven cash flows due to which it assists almost every

organisation (Chung and Chuang, 2016).

Assumption of Reinvestment – NPV is considered as most important and appropriate

technique of investment appraisal because it is realistic and does not assume that the existing

cash flows will be reinvested. Unlike other technique, NPV is designed to use in practical

organisations rather than use for theoretical purposes. This technique does not assume that the

existing cash flows of the company will be reinvested due to which results gained by this

technique are much reliable.

7

Where,

Cash flows = cash inflows of a period – cash outflows of a period

r = discounted rate

i = time period

The above formula is used by organisations to compare between different investment

proposals to analyse which proposal is best suited for their operations.

Hamilton Inc. is a growing company which currently uses the technique of net present

value for the purpose of making a decision between various investment proposals. Some

members of the BODs of this company have concerns regarding the use of NPV technique.

These concerns are related with the doubt that may be NPV is not appropriate for the investment

decisions when it comes to capital investment. In order to assist Hamilton Inc., the technique of

NPV is critically analysed below by evaluating various pros and cons of this method.

Benefits of NPV

Before making a decision about changing the investment appraisal technique, it is

advised to Hamilton Inc. review pros of NPV so that an informed decision can be taken. Some of

the most important pros of this technique are mentioned and analysed below:

Appropriate for both conventional and unconventional cash flow pattern – In a real world

organisation, it is usual that organisation is facing conventional and unconventional cash flows

by their operations. Conventional cash flows are the values which reflects either ascending or

descending cash flow pattern. On the other hand, unconventional cash flow pattern reflects the

values which are uneven and there is no subjective pattern in the values of cash flows. NPV

technique accepts both even and uneven cash flows due to which it assists almost every

organisation (Chung and Chuang, 2016).

Assumption of Reinvestment – NPV is considered as most important and appropriate

technique of investment appraisal because it is realistic and does not assume that the existing

cash flows will be reinvested. Unlike other technique, NPV is designed to use in practical

organisations rather than use for theoretical purposes. This technique does not assume that the

existing cash flows of the company will be reinvested due to which results gained by this

technique are much reliable.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Factors both risk and inflation – Every organisation including Hamilton Inc. works in a

practical world where change is constant. These changes result in inflation where value of the

expenses usually rise in every year and there are various risks which subject to contingencies.

The technique of NPV accounts for both the risk and inflation by discounting the net cash flows

with discounted rate. In the case of Hamilton Inc., the cash flows of this company are discounted

using their cost of capital of 11%.

Assist in comparative assessment – This method helps in comparing between two or

more projects. This technique involves extensive calculations but at the end this procedure

computes the profitability which company will gain. It is easier to interpret by simply implying

that project with higher NPV is better (Engel and et.al., 2016).

Limitations of NPV

Restrictive use – If an organisation has complex equations and investments then the

technique of NPV cannot be used. In organisations like Hamilton Inc. in which there is no

information given for the initial investment of MA02 machinery, the NPV for the project of

using MA02 has higher NPV. In such situations, it is difficult to just rely upon the method of

NPV.

Requires financial skills and time – Net present value has a complex procedure in which

effective financial skills are required. In context of Hamilton Inc., NPV computation is done by

professionals which takes time and money, this result in additional financial burden on the

organisation.

Do not account for hidden costs – NPV is a set structure which only accounts for specific

cash inflows and outflows. Expenses like miscellaneous expenses are not considered in

calculating net cash flows due to which NPV varies (Ferguson and Morton-Huddleston, 2016).

From the above analysis, it can be said that there are various benefits of NPV which helps

organisation to make informed and effective investment decisions but there are few restrictions

as well. The reason behind high NPV for proposal 1 in context of Hamilton Inc. is the no account

for initial investment for existing machinery. The concern of board about non appropriateness of

NPV as a capital investment decision making is genuine and it must be addressed by using other

techniques.

QUESTION 5

8

practical world where change is constant. These changes result in inflation where value of the

expenses usually rise in every year and there are various risks which subject to contingencies.

The technique of NPV accounts for both the risk and inflation by discounting the net cash flows

with discounted rate. In the case of Hamilton Inc., the cash flows of this company are discounted

using their cost of capital of 11%.

Assist in comparative assessment – This method helps in comparing between two or

more projects. This technique involves extensive calculations but at the end this procedure

computes the profitability which company will gain. It is easier to interpret by simply implying

that project with higher NPV is better (Engel and et.al., 2016).

Limitations of NPV

Restrictive use – If an organisation has complex equations and investments then the

technique of NPV cannot be used. In organisations like Hamilton Inc. in which there is no

information given for the initial investment of MA02 machinery, the NPV for the project of

using MA02 has higher NPV. In such situations, it is difficult to just rely upon the method of

NPV.

Requires financial skills and time – Net present value has a complex procedure in which

effective financial skills are required. In context of Hamilton Inc., NPV computation is done by

professionals which takes time and money, this result in additional financial burden on the

organisation.

Do not account for hidden costs – NPV is a set structure which only accounts for specific

cash inflows and outflows. Expenses like miscellaneous expenses are not considered in

calculating net cash flows due to which NPV varies (Ferguson and Morton-Huddleston, 2016).

From the above analysis, it can be said that there are various benefits of NPV which helps

organisation to make informed and effective investment decisions but there are few restrictions

as well. The reason behind high NPV for proposal 1 in context of Hamilton Inc. is the no account

for initial investment for existing machinery. The concern of board about non appropriateness of

NPV as a capital investment decision making is genuine and it must be addressed by using other

techniques.

QUESTION 5

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Use of alternative approaches to capital investment appraisal

Capital investment appraisal is the procedure of checking the viability of a capital investment

(Idris, Krishnan and Azmi, 2017). These investments are usually done against procurement of

fixed machineries and equipment. Apart from Net present value, there are various alternative

capital investment appraisal techniques as well which includes pay back period, internal rate of

return and accounting rate of return. The use of these techniques are analysed below in context of

Hamilton Inc.:

Pay back period – This technique is used by an organisation to identify the period in which

their investment can re coup from the organisation’s operations. This technique is regarded as the

selection criterion in capital investment appraisal (Mehra and et.al., 2018). This technique has

the potential by which an organisation can ascertain the time period in which their initial

investment can be earned again by the use of that investment. In context of Hamilton Inc., the

use of NPV is not adequate due to the absence of initial investment information of existing

machinery. In such cases, payback period technique can be used to determine which proposal is

better.

This technique also has few issues; Hamilton Inc. cannot completely rely upon this

technique as it does not factor risk or time value of money. The result from this technique will be

biased as one proposal involves usage of machinery for 2 years and one proposals involves usage

of machinery for 3 years.

Internal rate of return – Under this technique, efficiency of a capital investment is analysed

(Mitchell, 2017). In internal rate of return of an investment is calculated and then compared with

cost of capital; if the cost of capital happens to be greater than IRR then the proposal is rejected.

Hamilton Inc. can use this technique and can identify whether IRR of this company is greater or

smaller than their cost of capital that is 11%.

This technique has certain restrictions too (Prawitz and Cohart, 2016). These restrictions

include no accountability of future costs, project duration and size of the project. This technique

can be used by Hamilton Inc. but it cannot assist them effectively as the size of both the

proposals of this company varies.

Accounting rate of return – This is the simplest technique for capital investment appraisal in

which profit of a project is calculated which can be gained by investing initial investment

(Nkundabanyanga and et.al., 2017). Profits of multiple alternatives are compared and the project

9

Capital investment appraisal is the procedure of checking the viability of a capital investment

(Idris, Krishnan and Azmi, 2017). These investments are usually done against procurement of

fixed machineries and equipment. Apart from Net present value, there are various alternative

capital investment appraisal techniques as well which includes pay back period, internal rate of

return and accounting rate of return. The use of these techniques are analysed below in context of

Hamilton Inc.:

Pay back period – This technique is used by an organisation to identify the period in which

their investment can re coup from the organisation’s operations. This technique is regarded as the

selection criterion in capital investment appraisal (Mehra and et.al., 2018). This technique has

the potential by which an organisation can ascertain the time period in which their initial

investment can be earned again by the use of that investment. In context of Hamilton Inc., the

use of NPV is not adequate due to the absence of initial investment information of existing

machinery. In such cases, payback period technique can be used to determine which proposal is

better.

This technique also has few issues; Hamilton Inc. cannot completely rely upon this

technique as it does not factor risk or time value of money. The result from this technique will be

biased as one proposal involves usage of machinery for 2 years and one proposals involves usage

of machinery for 3 years.

Internal rate of return – Under this technique, efficiency of a capital investment is analysed

(Mitchell, 2017). In internal rate of return of an investment is calculated and then compared with

cost of capital; if the cost of capital happens to be greater than IRR then the proposal is rejected.

Hamilton Inc. can use this technique and can identify whether IRR of this company is greater or

smaller than their cost of capital that is 11%.

This technique has certain restrictions too (Prawitz and Cohart, 2016). These restrictions

include no accountability of future costs, project duration and size of the project. This technique

can be used by Hamilton Inc. but it cannot assist them effectively as the size of both the

proposals of this company varies.

Accounting rate of return – This is the simplest technique for capital investment appraisal in

which profit of a project is calculated which can be gained by investing initial investment

(Nkundabanyanga and et.al., 2017). Profits of multiple alternatives are compared and the project

9

with highest rate of return is selected. This technique can be used by Hamilton Inc. in which they

can calculate rate of return of both the projects. But this method has ample limitations. There is

no information regarding initial investment of existing machinery is given due to which the result

of ARR will be biased. Also this technique does not account for time value of money, inflation

or risk due to which usage of this technique will not provide relying results.

From the above analysis of alternative approaches of capital investment appraisal, it has

been analysed that, Net present value is still the best technique for this company which must be

used by the management of Hamilton Inc. For the purpose of fulfilling the limitations of NPV,

Company is recommended to use Payback period as an additional source of information.

Hamilton Inc. should use both NPV and pay back period technique of capital investment

appraisal by which an appropriate decision can be made by this company.

CONCLUSION

From the above report, it has been concluded that financial management is a procedure

which is used for widely three purposes which are finance decisions, investment decisions and

dividend decisions. It has been also found that organisations can use multiple investment

appraisal techniques to make an informed decision. Using this finding, it is recommended that

capital investment techniques of net present value and payback period should be used by

Hamilton Inc. which will assist them in gaining the insights about which proposal is best suited

for them. From the numerical analysis of NPV, it is concluded that proposal 1 which involves

continuing the usage of existing machinery is more suitable for this company.

10

can calculate rate of return of both the projects. But this method has ample limitations. There is

no information regarding initial investment of existing machinery is given due to which the result

of ARR will be biased. Also this technique does not account for time value of money, inflation

or risk due to which usage of this technique will not provide relying results.

From the above analysis of alternative approaches of capital investment appraisal, it has

been analysed that, Net present value is still the best technique for this company which must be

used by the management of Hamilton Inc. For the purpose of fulfilling the limitations of NPV,

Company is recommended to use Payback period as an additional source of information.

Hamilton Inc. should use both NPV and pay back period technique of capital investment

appraisal by which an appropriate decision can be made by this company.

CONCLUSION

From the above report, it has been concluded that financial management is a procedure

which is used for widely three purposes which are finance decisions, investment decisions and

dividend decisions. It has been also found that organisations can use multiple investment

appraisal techniques to make an informed decision. Using this finding, it is recommended that

capital investment techniques of net present value and payback period should be used by

Hamilton Inc. which will assist them in gaining the insights about which proposal is best suited

for them. From the numerical analysis of NPV, it is concluded that proposal 1 which involves

continuing the usage of existing machinery is more suitable for this company.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.