Financial Management Report: Plaggio Limited Company Analysis

VerifiedAdded on 2021/04/17

|21

|3940

|118

Report

AI Summary

This report provides a detailed financial analysis of Plaggio Limited, focusing on investment appraisal techniques. It evaluates three investment tenders using Net Present Value (NPV), Internal Rate of Return (IRR), payback period, and average accounting return to determine the best investment option. The report also discusses the company's capital structure, the weighted average cost of capital (WACC), and factors affecting the cost of capital. Furthermore, it critically examines different ways capital can be raised by an organization, offering recommendations and conclusions based on the financial data and analysis. The report concludes that none of the tenders are recommended but if a decision has to be made, Tender A is more preferable.

RUNNING HEAD: Financial management 1 | P a g e

Name of the student

Topic- Financial management

University name-

Name of the student

Topic- Financial management

University name-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management 2 | P a g e

Table of Contents

Task-1....................................................................................................................................................3

Introduction...........................................................................................................................................3

Task-2....................................................................................................................................................4

Evaluation technique of investment appraisal........................................................................................4

Evaluation of the Tender-A...........................................................................................................4

Evaluation of the Tender-B............................................................................................................6

Evaluation of the Tender-C............................................................................................................7

Discussion of the Evaluation techniques of investment appraisal..........................................................9

Task-3..................................................................................................................................................12

Discussion of the capital structure.......................................................................................................12

Task-4..................................................................................................................................................12

Discussion of the weighted average cost of capital of Plaggio Limited Company...............................12

Task-5..................................................................................................................................................14

Discussion on the factors that could affect the cost of capital............................................................14

Task-6..................................................................................................................................................15

A critical discussion of the different ways capital can be raised by an organisation............................15

Raising funds in market...................................................................................................................15

Recommendatio...................................................................................................................................16

Conclusion...........................................................................................................................................17

References...........................................................................................................................................18

Table of Contents

Task-1....................................................................................................................................................3

Introduction...........................................................................................................................................3

Task-2....................................................................................................................................................4

Evaluation technique of investment appraisal........................................................................................4

Evaluation of the Tender-A...........................................................................................................4

Evaluation of the Tender-B............................................................................................................6

Evaluation of the Tender-C............................................................................................................7

Discussion of the Evaluation techniques of investment appraisal..........................................................9

Task-3..................................................................................................................................................12

Discussion of the capital structure.......................................................................................................12

Task-4..................................................................................................................................................12

Discussion of the weighted average cost of capital of Plaggio Limited Company...............................12

Task-5..................................................................................................................................................14

Discussion on the factors that could affect the cost of capital............................................................14

Task-6..................................................................................................................................................15

A critical discussion of the different ways capital can be raised by an organisation............................15

Raising funds in market...................................................................................................................15

Recommendatio...................................................................................................................................16

Conclusion...........................................................................................................................................17

References...........................................................................................................................................18

Financial management 3 | P a g e

Task-1

Introduction

This report emphasizes upon the financial analysis tools and investment .decisions of

company. There are several financial analysis tools such as ratio analysis, NPV and IRR to

evaluate the particular investment decisions. This report reflects the key understanding on the

capital costing and investment appraisal technique of organization. In this report, Plaggio

Limited Company has been taken into consideration. This report is prepared on the basis of

particular case study and investment decisions of Plaggio Limited Company. In the starting of

this report, investment decision to replace the production machinery of Plaggio Limited

Company has been taken into consideration. However, NPV and internal rate of return and

other appraisal methods have been taken into consideration to evaluate the project proposals.

In addition to this, pay-back period and accounting average rate of return of company. It is

evaluated that these financial analysis tools assist in identifying the best possible investment

option which company needs to take in its business. In the main body part, capital assets price

model has been used to evaluate the cost of equity and cost of debt of the company. It is

evaluated that management of company could use this CAPM method and capital budgeting

methods to evaluate which tender would bring more benefits to an organization. The main

objective of this assignment is to evaluate all the three projects and determine which project

would give more benefits to Plaggio Limited Company.

Task-1

Introduction

This report emphasizes upon the financial analysis tools and investment .decisions of

company. There are several financial analysis tools such as ratio analysis, NPV and IRR to

evaluate the particular investment decisions. This report reflects the key understanding on the

capital costing and investment appraisal technique of organization. In this report, Plaggio

Limited Company has been taken into consideration. This report is prepared on the basis of

particular case study and investment decisions of Plaggio Limited Company. In the starting of

this report, investment decision to replace the production machinery of Plaggio Limited

Company has been taken into consideration. However, NPV and internal rate of return and

other appraisal methods have been taken into consideration to evaluate the project proposals.

In addition to this, pay-back period and accounting average rate of return of company. It is

evaluated that these financial analysis tools assist in identifying the best possible investment

option which company needs to take in its business. In the main body part, capital assets price

model has been used to evaluate the cost of equity and cost of debt of the company. It is

evaluated that management of company could use this CAPM method and capital budgeting

methods to evaluate which tender would bring more benefits to an organization. The main

objective of this assignment is to evaluate all the three projects and determine which project

would give more benefits to Plaggio Limited Company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial management 4 | P a g e

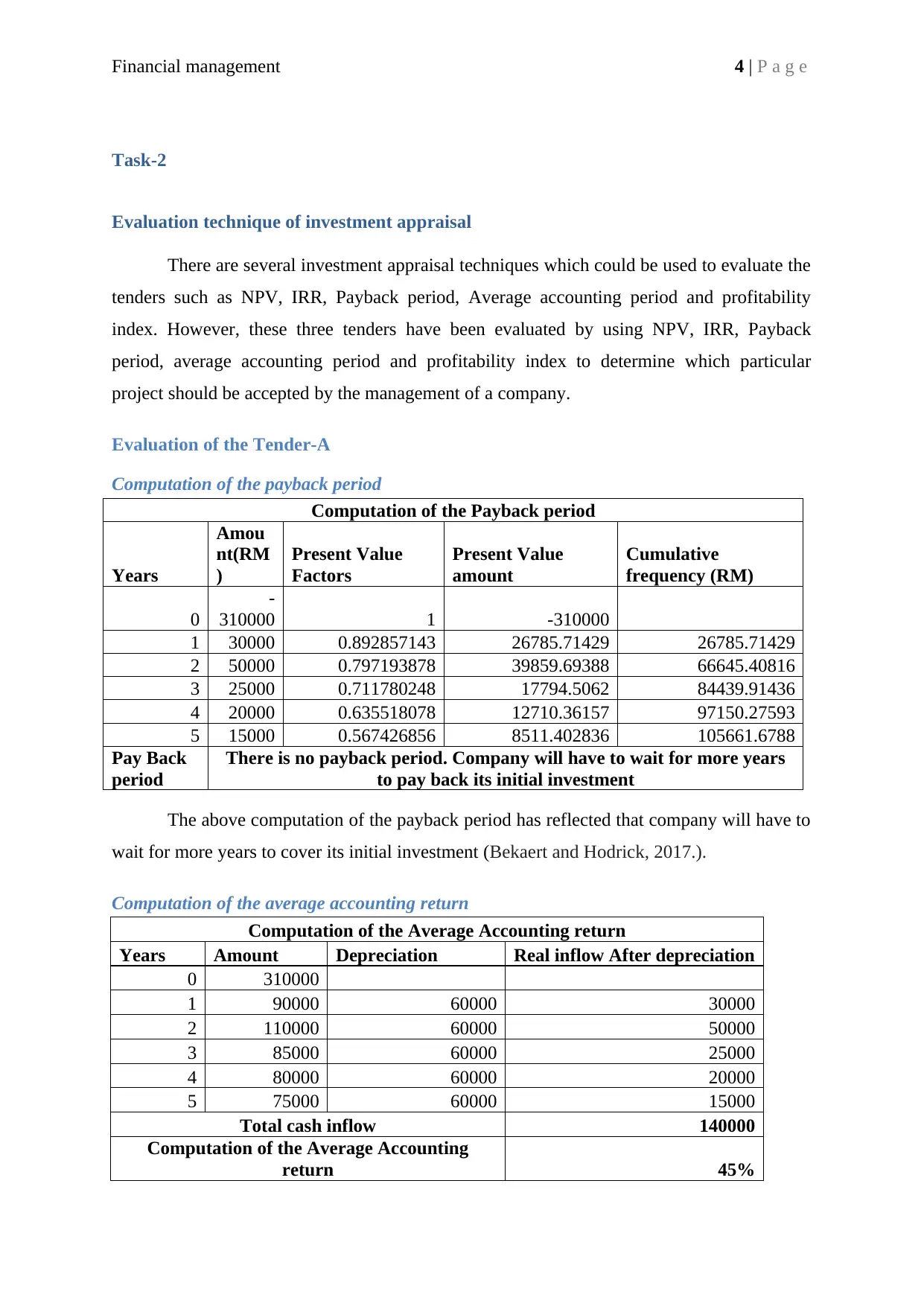

Task-2

Evaluation technique of investment appraisal

There are several investment appraisal techniques which could be used to evaluate the

tenders such as NPV, IRR, Payback period, Average accounting period and profitability

index. However, these three tenders have been evaluated by using NPV, IRR, Payback

period, average accounting period and profitability index to determine which particular

project should be accepted by the management of a company.

Evaluation of the Tender-A

Computation of the payback period

Computation of the Payback period

Years

Amou

nt(RM

)

Present Value

Factors

Present Value

amount

Cumulative

frequency (RM)

0

-

310000 1 -310000

1 30000 0.892857143 26785.71429 26785.71429

2 50000 0.797193878 39859.69388 66645.40816

3 25000 0.711780248 17794.5062 84439.91436

4 20000 0.635518078 12710.36157 97150.27593

5 15000 0.567426856 8511.402836 105661.6788

Pay Back

period

There is no payback period. Company will have to wait for more years

to pay back its initial investment

The above computation of the payback period has reflected that company will have to

wait for more years to cover its initial investment (Bekaert and Hodrick, 2017.).

Computation of the average accounting return

Computation of the Average Accounting return

Years Amount Depreciation Real inflow After depreciation

0 310000

1 90000 60000 30000

2 110000 60000 50000

3 85000 60000 25000

4 80000 60000 20000

5 75000 60000 15000

Total cash inflow 140000

Computation of the Average Accounting

return 45%

Task-2

Evaluation technique of investment appraisal

There are several investment appraisal techniques which could be used to evaluate the

tenders such as NPV, IRR, Payback period, Average accounting period and profitability

index. However, these three tenders have been evaluated by using NPV, IRR, Payback

period, average accounting period and profitability index to determine which particular

project should be accepted by the management of a company.

Evaluation of the Tender-A

Computation of the payback period

Computation of the Payback period

Years

Amou

nt(RM

)

Present Value

Factors

Present Value

amount

Cumulative

frequency (RM)

0

-

310000 1 -310000

1 30000 0.892857143 26785.71429 26785.71429

2 50000 0.797193878 39859.69388 66645.40816

3 25000 0.711780248 17794.5062 84439.91436

4 20000 0.635518078 12710.36157 97150.27593

5 15000 0.567426856 8511.402836 105661.6788

Pay Back

period

There is no payback period. Company will have to wait for more years

to pay back its initial investment

The above computation of the payback period has reflected that company will have to

wait for more years to cover its initial investment (Bekaert and Hodrick, 2017.).

Computation of the average accounting return

Computation of the Average Accounting return

Years Amount Depreciation Real inflow After depreciation

0 310000

1 90000 60000 30000

2 110000 60000 50000

3 85000 60000 25000

4 80000 60000 20000

5 75000 60000 15000

Total cash inflow 140000

Computation of the Average Accounting

return 45%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management 5 | P a g e

Financial management 6 | P a g e

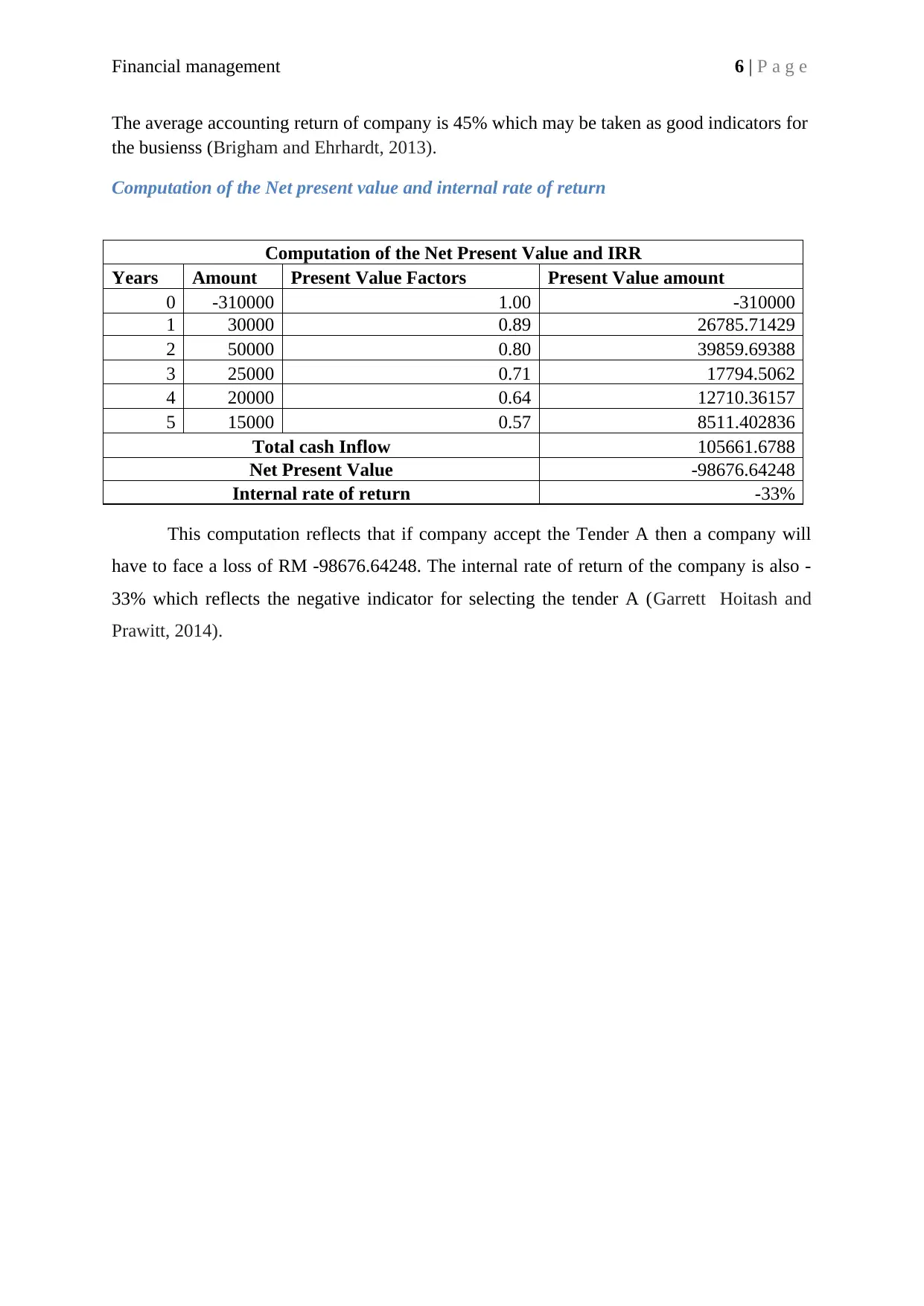

The average accounting return of company is 45% which may be taken as good indicators for

the busienss (Brigham and Ehrhardt, 2013).

Computation of the Net present value and internal rate of return

Computation of the Net Present Value and IRR

Years Amount Present Value Factors Present Value amount

0 -310000 1.00 -310000

1 30000 0.89 26785.71429

2 50000 0.80 39859.69388

3 25000 0.71 17794.5062

4 20000 0.64 12710.36157

5 15000 0.57 8511.402836

Total cash Inflow 105661.6788

Net Present Value -98676.64248

Internal rate of return -33%

This computation reflects that if company accept the Tender A then a company will

have to face a loss of RM -98676.64248. The internal rate of return of the company is also -

33% which reflects the negative indicator for selecting the tender A (Garrett Hoitash and

Prawitt, 2014).

The average accounting return of company is 45% which may be taken as good indicators for

the busienss (Brigham and Ehrhardt, 2013).

Computation of the Net present value and internal rate of return

Computation of the Net Present Value and IRR

Years Amount Present Value Factors Present Value amount

0 -310000 1.00 -310000

1 30000 0.89 26785.71429

2 50000 0.80 39859.69388

3 25000 0.71 17794.5062

4 20000 0.64 12710.36157

5 15000 0.57 8511.402836

Total cash Inflow 105661.6788

Net Present Value -98676.64248

Internal rate of return -33%

This computation reflects that if company accept the Tender A then a company will

have to face a loss of RM -98676.64248. The internal rate of return of the company is also -

33% which reflects the negative indicator for selecting the tender A (Garrett Hoitash and

Prawitt, 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial management 7 | P a g e

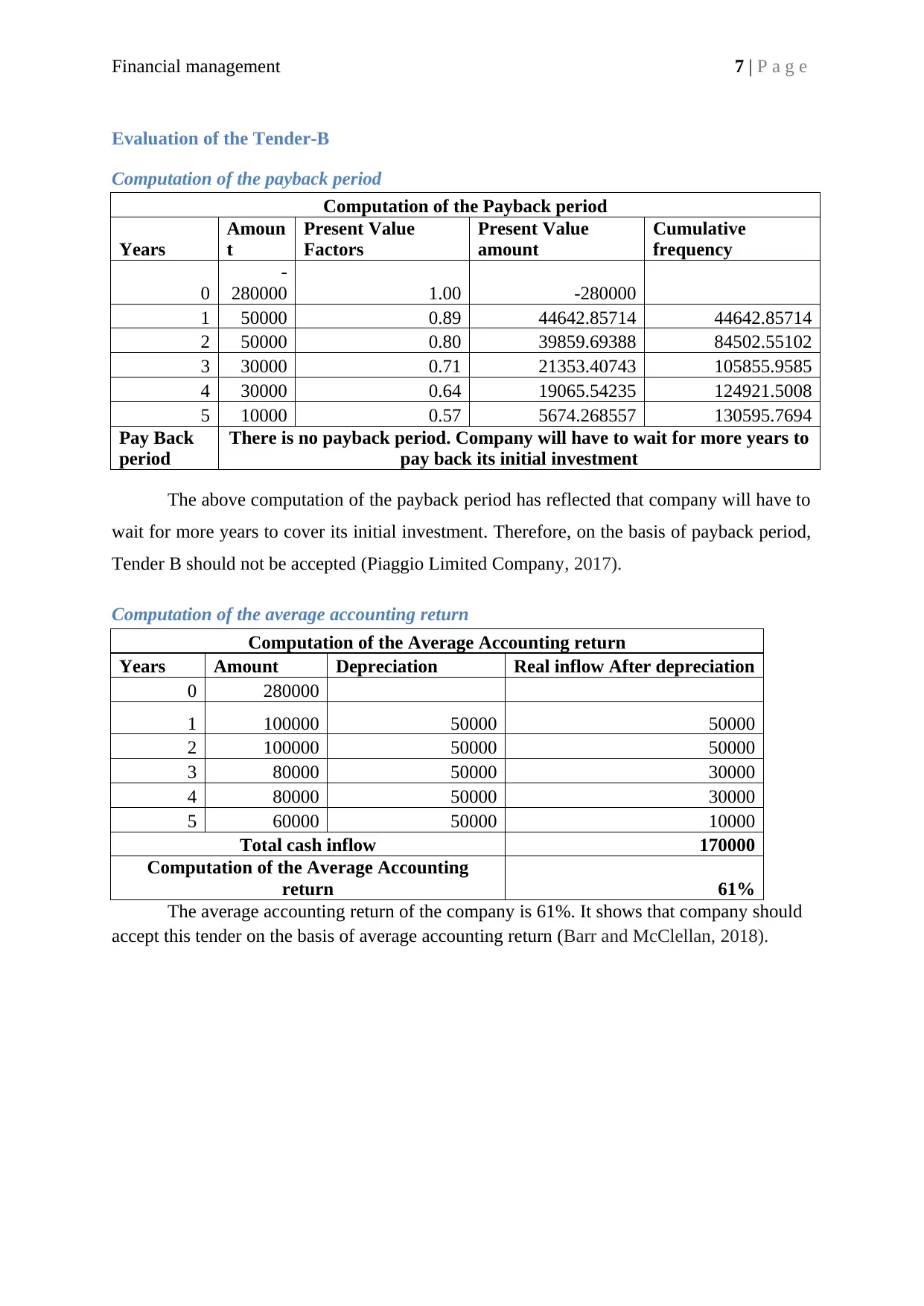

Evaluation of the Tender-B

Computation of the payback period

Computation of the Payback period

Years

Amoun

t

Present Value

Factors

Present Value

amount

Cumulative

frequency

0

-

280000 1.00 -280000

1 50000 0.89 44642.85714 44642.85714

2 50000 0.80 39859.69388 84502.55102

3 30000 0.71 21353.40743 105855.9585

4 30000 0.64 19065.54235 124921.5008

5 10000 0.57 5674.268557 130595.7694

Pay Back

period

There is no payback period. Company will have to wait for more years to

pay back its initial investment

The above computation of the payback period has reflected that company will have to

wait for more years to cover its initial investment. Therefore, on the basis of payback period,

Tender B should not be accepted (Piaggio Limited Company, 2017).

Computation of the average accounting return

Computation of the Average Accounting return

Years Amount Depreciation Real inflow After depreciation

0 280000

1 100000 50000 50000

2 100000 50000 50000

3 80000 50000 30000

4 80000 50000 30000

5 60000 50000 10000

Total cash inflow 170000

Computation of the Average Accounting

return 61%

The average accounting return of the company is 61%. It shows that company should

accept this tender on the basis of average accounting return (Barr and McClellan, 2018).

Evaluation of the Tender-B

Computation of the payback period

Computation of the Payback period

Years

Amoun

t

Present Value

Factors

Present Value

amount

Cumulative

frequency

0

-

280000 1.00 -280000

1 50000 0.89 44642.85714 44642.85714

2 50000 0.80 39859.69388 84502.55102

3 30000 0.71 21353.40743 105855.9585

4 30000 0.64 19065.54235 124921.5008

5 10000 0.57 5674.268557 130595.7694

Pay Back

period

There is no payback period. Company will have to wait for more years to

pay back its initial investment

The above computation of the payback period has reflected that company will have to

wait for more years to cover its initial investment. Therefore, on the basis of payback period,

Tender B should not be accepted (Piaggio Limited Company, 2017).

Computation of the average accounting return

Computation of the Average Accounting return

Years Amount Depreciation Real inflow After depreciation

0 280000

1 100000 50000 50000

2 100000 50000 50000

3 80000 50000 30000

4 80000 50000 30000

5 60000 50000 10000

Total cash inflow 170000

Computation of the Average Accounting

return 61%

The average accounting return of the company is 61%. It shows that company should

accept this tender on the basis of average accounting return (Barr and McClellan, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management 8 | P a g e

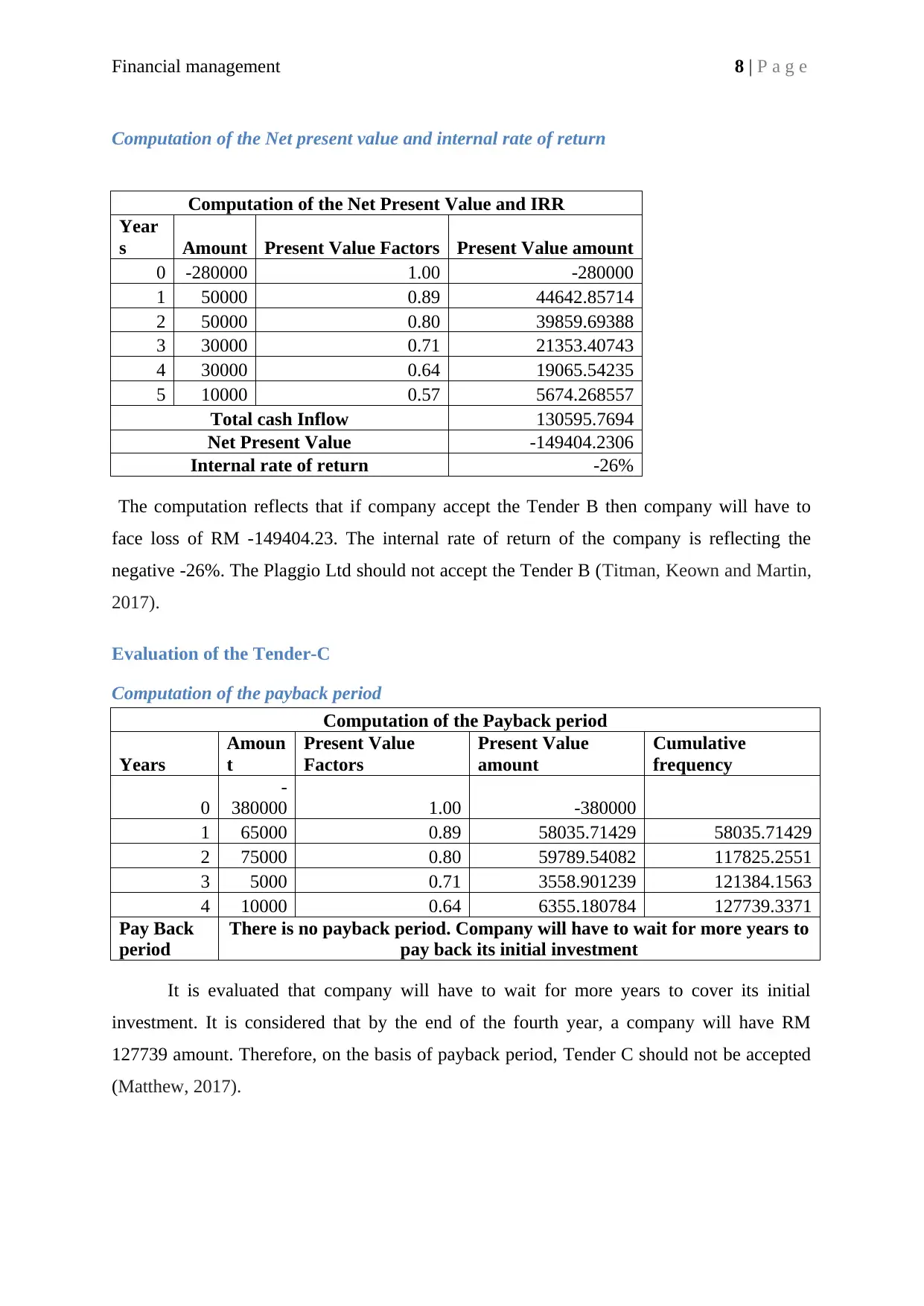

Computation of the Net present value and internal rate of return

Computation of the Net Present Value and IRR

Year

s Amount Present Value Factors Present Value amount

0 -280000 1.00 -280000

1 50000 0.89 44642.85714

2 50000 0.80 39859.69388

3 30000 0.71 21353.40743

4 30000 0.64 19065.54235

5 10000 0.57 5674.268557

Total cash Inflow 130595.7694

Net Present Value -149404.2306

Internal rate of return -26%

The computation reflects that if company accept the Tender B then company will have to

face loss of RM -149404.23. The internal rate of return of the company is reflecting the

negative -26%. The Plaggio Ltd should not accept the Tender B (Titman, Keown and Martin,

2017).

Evaluation of the Tender-C

Computation of the payback period

Computation of the Payback period

Years

Amoun

t

Present Value

Factors

Present Value

amount

Cumulative

frequency

0

-

380000 1.00 -380000

1 65000 0.89 58035.71429 58035.71429

2 75000 0.80 59789.54082 117825.2551

3 5000 0.71 3558.901239 121384.1563

4 10000 0.64 6355.180784 127739.3371

Pay Back

period

There is no payback period. Company will have to wait for more years to

pay back its initial investment

It is evaluated that company will have to wait for more years to cover its initial

investment. It is considered that by the end of the fourth year, a company will have RM

127739 amount. Therefore, on the basis of payback period, Tender C should not be accepted

(Matthew, 2017).

Computation of the Net present value and internal rate of return

Computation of the Net Present Value and IRR

Year

s Amount Present Value Factors Present Value amount

0 -280000 1.00 -280000

1 50000 0.89 44642.85714

2 50000 0.80 39859.69388

3 30000 0.71 21353.40743

4 30000 0.64 19065.54235

5 10000 0.57 5674.268557

Total cash Inflow 130595.7694

Net Present Value -149404.2306

Internal rate of return -26%

The computation reflects that if company accept the Tender B then company will have to

face loss of RM -149404.23. The internal rate of return of the company is reflecting the

negative -26%. The Plaggio Ltd should not accept the Tender B (Titman, Keown and Martin,

2017).

Evaluation of the Tender-C

Computation of the payback period

Computation of the Payback period

Years

Amoun

t

Present Value

Factors

Present Value

amount

Cumulative

frequency

0

-

380000 1.00 -380000

1 65000 0.89 58035.71429 58035.71429

2 75000 0.80 59789.54082 117825.2551

3 5000 0.71 3558.901239 121384.1563

4 10000 0.64 6355.180784 127739.3371

Pay Back

period

There is no payback period. Company will have to wait for more years to

pay back its initial investment

It is evaluated that company will have to wait for more years to cover its initial

investment. It is considered that by the end of the fourth year, a company will have RM

127739 amount. Therefore, on the basis of payback period, Tender C should not be accepted

(Matthew, 2017).

Financial management 9 | P a g e

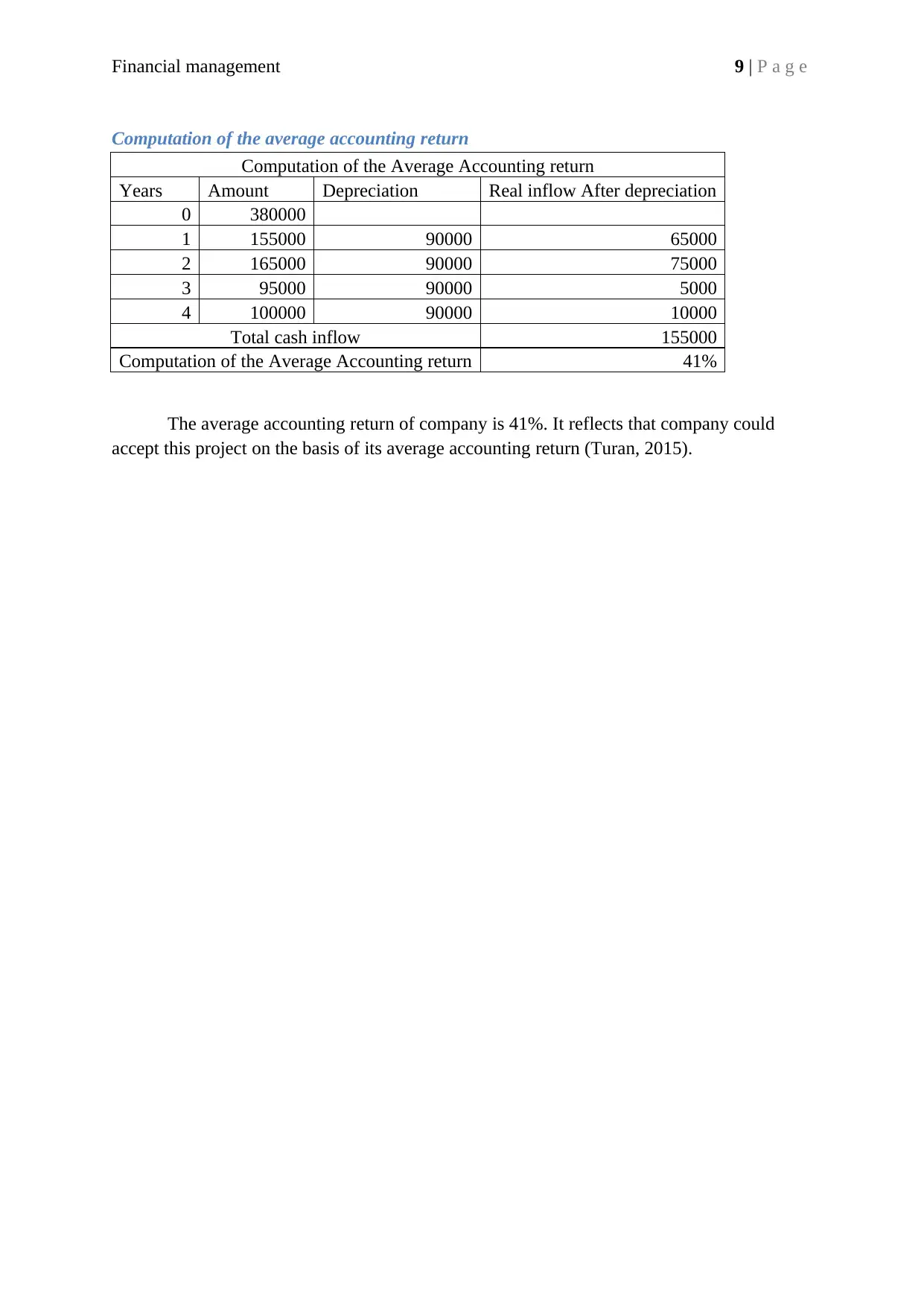

Computation of the average accounting return

Computation of the Average Accounting return

Years Amount Depreciation Real inflow After depreciation

0 380000

1 155000 90000 65000

2 165000 90000 75000

3 95000 90000 5000

4 100000 90000 10000

Total cash inflow 155000

Computation of the Average Accounting return 41%

The average accounting return of company is 41%. It reflects that company could

accept this project on the basis of its average accounting return (Turan, 2015).

Computation of the average accounting return

Computation of the Average Accounting return

Years Amount Depreciation Real inflow After depreciation

0 380000

1 155000 90000 65000

2 165000 90000 75000

3 95000 90000 5000

4 100000 90000 10000

Total cash inflow 155000

Computation of the Average Accounting return 41%

The average accounting return of company is 41%. It reflects that company could

accept this project on the basis of its average accounting return (Turan, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial management 10 | P a g e

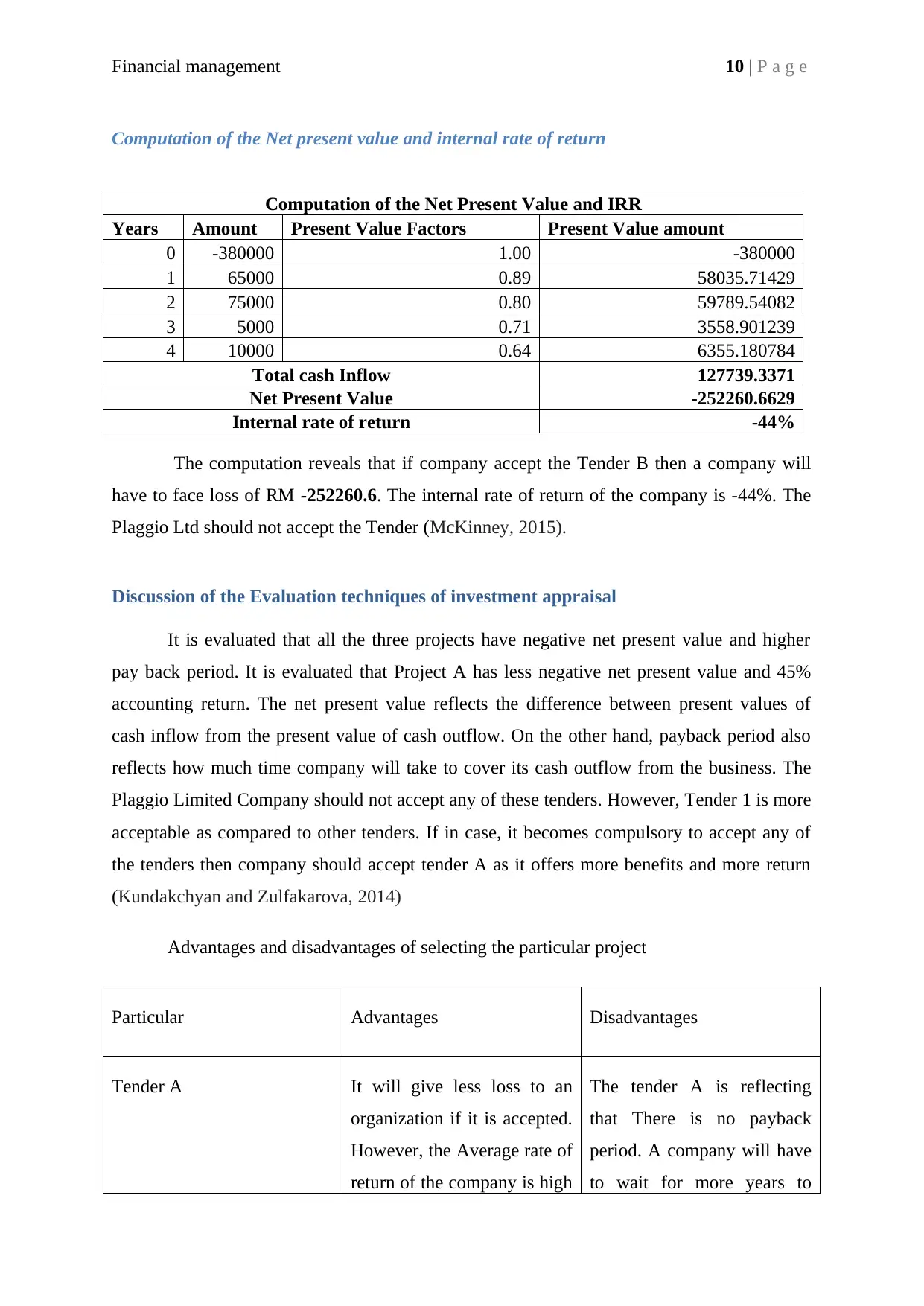

Computation of the Net present value and internal rate of return

Computation of the Net Present Value and IRR

Years Amount Present Value Factors Present Value amount

0 -380000 1.00 -380000

1 65000 0.89 58035.71429

2 75000 0.80 59789.54082

3 5000 0.71 3558.901239

4 10000 0.64 6355.180784

Total cash Inflow 127739.3371

Net Present Value -252260.6629

Internal rate of return -44%

The computation reveals that if company accept the Tender B then a company will

have to face loss of RM -252260.6. The internal rate of return of the company is -44%. The

Plaggio Ltd should not accept the Tender (McKinney, 2015).

Discussion of the Evaluation techniques of investment appraisal

It is evaluated that all the three projects have negative net present value and higher

pay back period. It is evaluated that Project A has less negative net present value and 45%

accounting return. The net present value reflects the difference between present values of

cash inflow from the present value of cash outflow. On the other hand, payback period also

reflects how much time company will take to cover its cash outflow from the business. The

Plaggio Limited Company should not accept any of these tenders. However, Tender 1 is more

acceptable as compared to other tenders. If in case, it becomes compulsory to accept any of

the tenders then company should accept tender A as it offers more benefits and more return

(Kundakchyan and Zulfakarova, 2014)

Advantages and disadvantages of selecting the particular project

Particular Advantages Disadvantages

Tender A It will give less loss to an

organization if it is accepted.

However, the Average rate of

return of the company is high

The tender A is reflecting

that There is no payback

period. A company will have

to wait for more years to

Computation of the Net present value and internal rate of return

Computation of the Net Present Value and IRR

Years Amount Present Value Factors Present Value amount

0 -380000 1.00 -380000

1 65000 0.89 58035.71429

2 75000 0.80 59789.54082

3 5000 0.71 3558.901239

4 10000 0.64 6355.180784

Total cash Inflow 127739.3371

Net Present Value -252260.6629

Internal rate of return -44%

The computation reveals that if company accept the Tender B then a company will

have to face loss of RM -252260.6. The internal rate of return of the company is -44%. The

Plaggio Ltd should not accept the Tender (McKinney, 2015).

Discussion of the Evaluation techniques of investment appraisal

It is evaluated that all the three projects have negative net present value and higher

pay back period. It is evaluated that Project A has less negative net present value and 45%

accounting return. The net present value reflects the difference between present values of

cash inflow from the present value of cash outflow. On the other hand, payback period also

reflects how much time company will take to cover its cash outflow from the business. The

Plaggio Limited Company should not accept any of these tenders. However, Tender 1 is more

acceptable as compared to other tenders. If in case, it becomes compulsory to accept any of

the tenders then company should accept tender A as it offers more benefits and more return

(Kundakchyan and Zulfakarova, 2014)

Advantages and disadvantages of selecting the particular project

Particular Advantages Disadvantages

Tender A It will give less loss to an

organization if it is accepted.

However, the Average rate of

return of the company is high

The tender A is reflecting

that There is no payback

period. A company will have

to wait for more years to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management 11 | P a g e

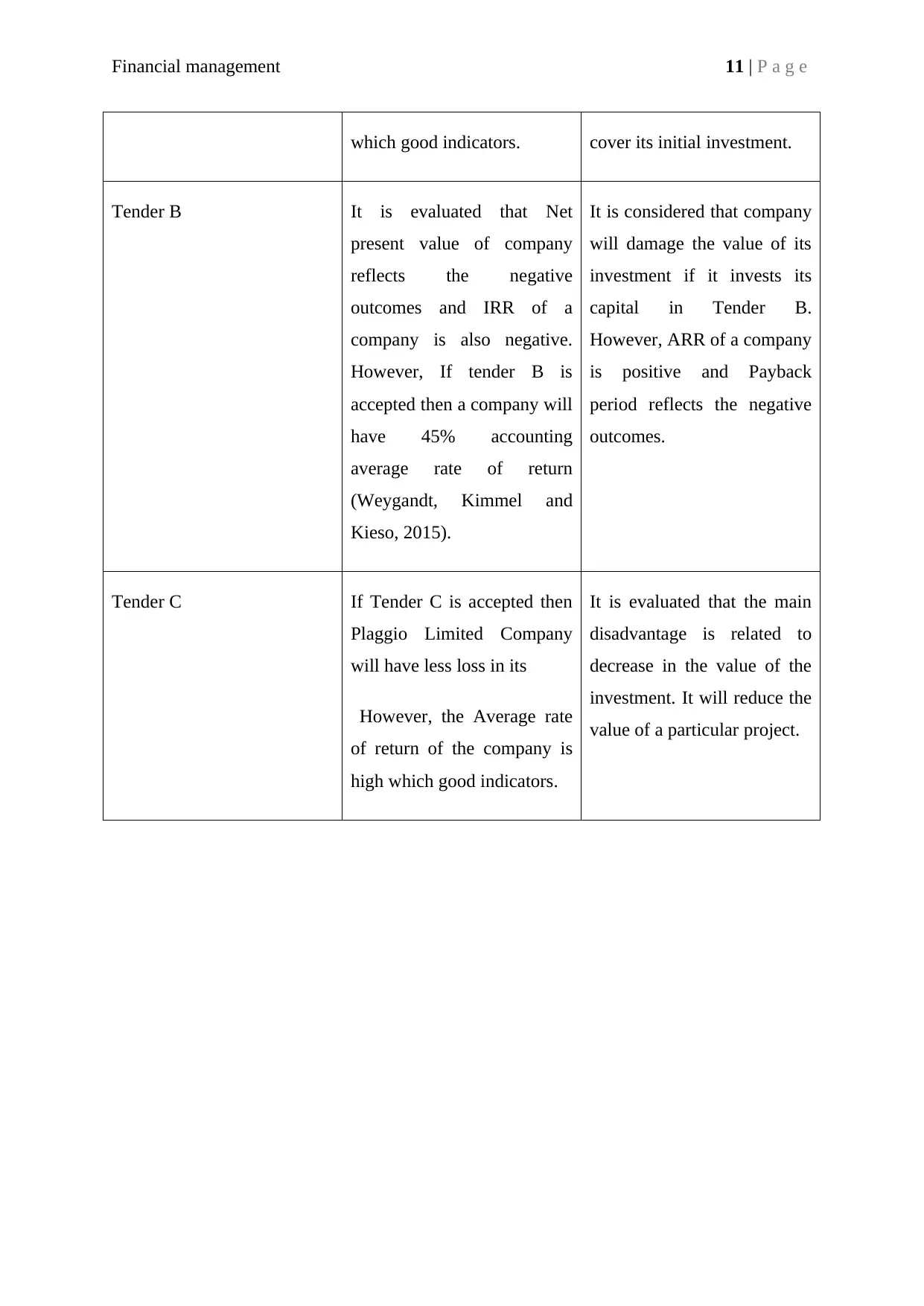

which good indicators. cover its initial investment.

Tender B It is evaluated that Net

present value of company

reflects the negative

outcomes and IRR of a

company is also negative.

However, If tender B is

accepted then a company will

have 45% accounting

average rate of return

(Weygandt, Kimmel and

Kieso, 2015).

It is considered that company

will damage the value of its

investment if it invests its

capital in Tender B.

However, ARR of a company

is positive and Payback

period reflects the negative

outcomes.

Tender C If Tender C is accepted then

Plaggio Limited Company

will have less loss in its

However, the Average rate

of return of the company is

high which good indicators.

It is evaluated that the main

disadvantage is related to

decrease in the value of the

investment. It will reduce the

value of a particular project.

which good indicators. cover its initial investment.

Tender B It is evaluated that Net

present value of company

reflects the negative

outcomes and IRR of a

company is also negative.

However, If tender B is

accepted then a company will

have 45% accounting

average rate of return

(Weygandt, Kimmel and

Kieso, 2015).

It is considered that company

will damage the value of its

investment if it invests its

capital in Tender B.

However, ARR of a company

is positive and Payback

period reflects the negative

outcomes.

Tender C If Tender C is accepted then

Plaggio Limited Company

will have less loss in its

However, the Average rate

of return of the company is

high which good indicators.

It is evaluated that the main

disadvantage is related to

decrease in the value of the

investment. It will reduce the

value of a particular project.

Financial management 12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.