Financial Management Report: Business Finance Project Analysis

VerifiedAdded on 2021/02/19

|9

|2602

|42

Report

AI Summary

This report provides a comprehensive analysis of a business finance project focusing on financial management. It begins with an introduction to business finance and its importance, followed by a detailed examination of the accounting equation, including calculations of changes in balance sheet components and a comparison of capital at the beginning and end of the year. The report then delves into the effects of incorrect identification of capital and revenue expenditures, the differences between net and gross profit, and the distinctions between cost of sales and turnover. Further, it explores the interpretation of cash flow statements and explains discrepancies between bank statements and cash books. The report concludes with an analysis of benchmarking in measuring performance, including its benefits and limitations, and an analysis of ratios for ShowerPak Ltd, such as debtor's payment period, creditor's payment period, inventory turnover period, and cash operating cycle. Overall, the report provides a thorough overview of key financial concepts and their practical application within a business context.

Business Finance project 5

Financial Management

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

MAIN BODY.......................................................................................................................................3

LO 1 .....................................................................................................................................................3

1.1 Discussion of Accounting Equation ..........................................................................................3

1.2 Calculation of changes in the Balance Sheet Components and their effects on those

components......................................................................................................................................3

1.3 Comparison of Capital at the beginning of the year to end of the year.....................................5

LO 2......................................................................................................................................................5

2.1 Effect on profit of incorrect identification of capital and revenue expenditure.........................5

2.2 Difference between net Profit and Gross Profit of Shower Pak Limited...................................5

2.3 Difference between Cost of Sales and Turnover of Shower Pak Limited.................................5

LO 3......................................................................................................................................................6

3.1 Interpreting meaning of cash flow statement.............................................................................6

3.2 Explaining reasons for discrepancies between bank statement and cash book.........................6

LO 4......................................................................................................................................................7

4.1 Analysing use of Benchmarking in measuring performance along with benefits and

limitations........................................................................................................................................7

4.2 Analysis of Ratio of ShowerPak Ltd .........................................................................................7

CONCLUSION....................................................................................................................................8

REFERENCES.....................................................................................................................................9

INTRODUCTION................................................................................................................................3

MAIN BODY.......................................................................................................................................3

LO 1 .....................................................................................................................................................3

1.1 Discussion of Accounting Equation ..........................................................................................3

1.2 Calculation of changes in the Balance Sheet Components and their effects on those

components......................................................................................................................................3

1.3 Comparison of Capital at the beginning of the year to end of the year.....................................5

LO 2......................................................................................................................................................5

2.1 Effect on profit of incorrect identification of capital and revenue expenditure.........................5

2.2 Difference between net Profit and Gross Profit of Shower Pak Limited...................................5

2.3 Difference between Cost of Sales and Turnover of Shower Pak Limited.................................5

LO 3......................................................................................................................................................6

3.1 Interpreting meaning of cash flow statement.............................................................................6

3.2 Explaining reasons for discrepancies between bank statement and cash book.........................6

LO 4......................................................................................................................................................7

4.1 Analysing use of Benchmarking in measuring performance along with benefits and

limitations........................................................................................................................................7

4.2 Analysis of Ratio of ShowerPak Ltd .........................................................................................7

CONCLUSION....................................................................................................................................8

REFERENCES.....................................................................................................................................9

INTRODUCTION

Business finance has been considered as one of the most important business aspect without which

no business function can be carried out. Financial management is related with the process of

managing, planning, organising and controlling the financial activities of the business for making

better allocation of available and limited business resources. By conducting effective financial

management process, it can help in smooth business functioning thereby achieving the set defined

business goals in a cost effective manner. The present report is based on ShowerPark limited whcihc

is a family owned manufacturer of moulded shower room units. It will define better understanding

of accounting equation and its concept. It will elaborate reason which brings changes in the capital

at starting and ending of year. How net profit is different from gross profit will be explain along

with cost of sales and turnover difference. Further, cocnept of cash flow statements will be

discussed. At last, efficiency measures by assessing the current trend and benchmarking comparison

will be define.

MAIN BODY

LO 1

1.1 Discussion of Accounting Equation

Accounting Equation is the base of double- entry accounting system (Juárez 2015).

According to this equation, Balance Sheet is are prepared in Shower Pak Limited. The equation

shows the two sides of Balance Sheet in which assets and liabilities of Shower Pak Limited should

be equal. Both the sides of the balance sheet should made in equal amount. This system should

ensure that both the debit side and credit side should match with each other. In Balance Sheet, assets

are the valuable resources which are owned by Shower Pak Ltd and liabilities are their obligations.

Both liabilities and owner's capital represents that how the assets of a company are financed. The

Accounting Equation can be represented as :-

Asset= Shareholders Fund + Liabilities

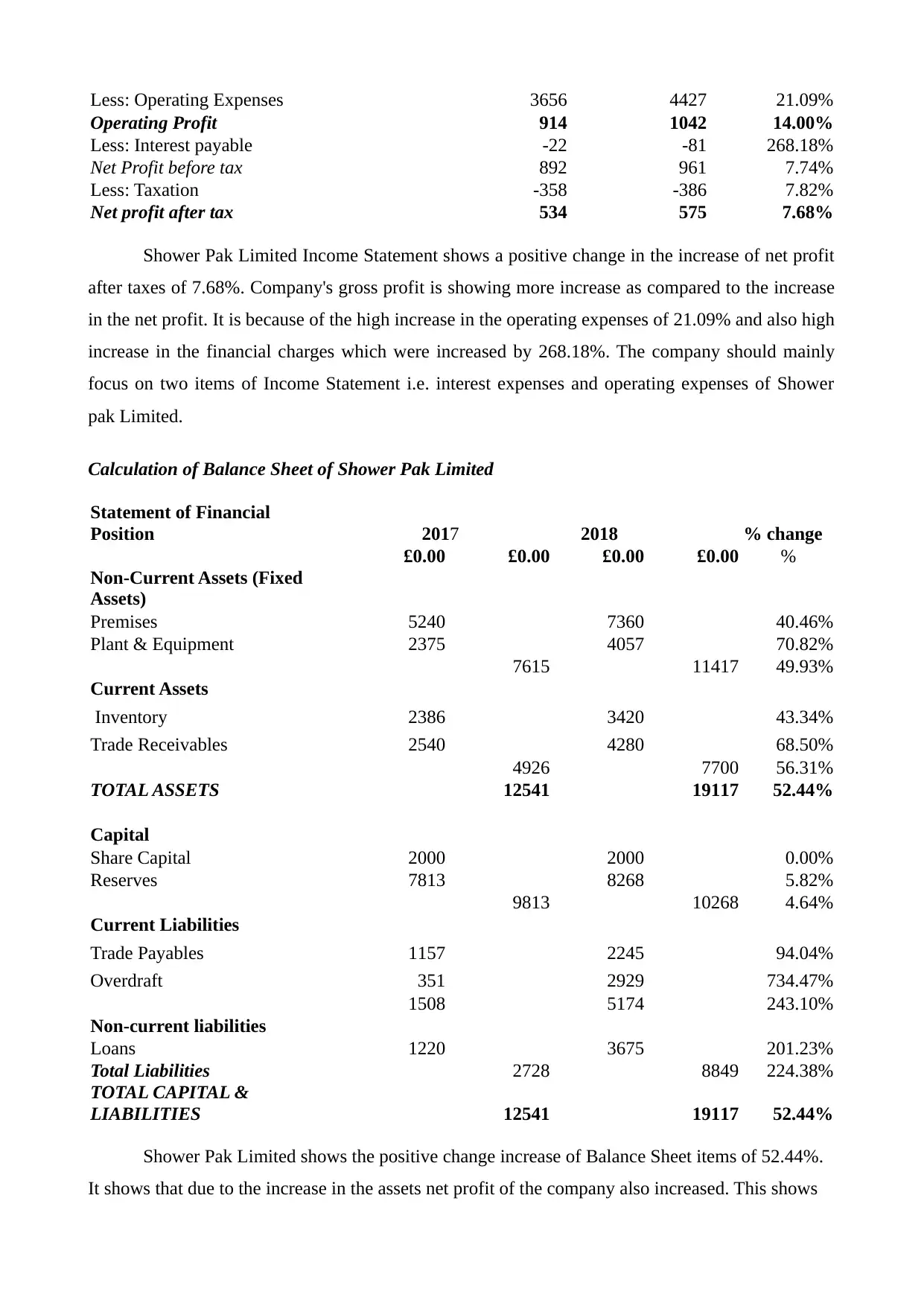

1.2 Calculation of changes in the Balance Sheet Components and their effects on those components

Calculation of changes in Income Statement of Shower Pak Limited

Income Statement

2017

£ 000

2018

£ 000 % change

Revenue 9482 11365 19.86%

Less: Cost of Sales 4912 5896 20.03%

Gross Profit 4570 5469 19.67%

Business finance has been considered as one of the most important business aspect without which

no business function can be carried out. Financial management is related with the process of

managing, planning, organising and controlling the financial activities of the business for making

better allocation of available and limited business resources. By conducting effective financial

management process, it can help in smooth business functioning thereby achieving the set defined

business goals in a cost effective manner. The present report is based on ShowerPark limited whcihc

is a family owned manufacturer of moulded shower room units. It will define better understanding

of accounting equation and its concept. It will elaborate reason which brings changes in the capital

at starting and ending of year. How net profit is different from gross profit will be explain along

with cost of sales and turnover difference. Further, cocnept of cash flow statements will be

discussed. At last, efficiency measures by assessing the current trend and benchmarking comparison

will be define.

MAIN BODY

LO 1

1.1 Discussion of Accounting Equation

Accounting Equation is the base of double- entry accounting system (Juárez 2015).

According to this equation, Balance Sheet is are prepared in Shower Pak Limited. The equation

shows the two sides of Balance Sheet in which assets and liabilities of Shower Pak Limited should

be equal. Both the sides of the balance sheet should made in equal amount. This system should

ensure that both the debit side and credit side should match with each other. In Balance Sheet, assets

are the valuable resources which are owned by Shower Pak Ltd and liabilities are their obligations.

Both liabilities and owner's capital represents that how the assets of a company are financed. The

Accounting Equation can be represented as :-

Asset= Shareholders Fund + Liabilities

1.2 Calculation of changes in the Balance Sheet Components and their effects on those components

Calculation of changes in Income Statement of Shower Pak Limited

Income Statement

2017

£ 000

2018

£ 000 % change

Revenue 9482 11365 19.86%

Less: Cost of Sales 4912 5896 20.03%

Gross Profit 4570 5469 19.67%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Operating Expenses 3656 4427 21.09%

Operating Profit 914 1042 14.00%

Less: Interest payable -22 -81 268.18%

Net Profit before tax 892 961 7.74%

Less: Taxation -358 -386 7.82%

Net profit after tax 534 575 7.68%

Shower Pak Limited Income Statement shows a positive change in the increase of net profit

after taxes of 7.68%. Company's gross profit is showing more increase as compared to the increase

in the net profit. It is because of the high increase in the operating expenses of 21.09% and also high

increase in the financial charges which were increased by 268.18%. The company should mainly

focus on two items of Income Statement i.e. interest expenses and operating expenses of Shower

pak Limited.

Calculation of Balance Sheet of Shower Pak Limited

Statement of Financial

Position 2017 2018 % change

£0.00 £0.00 £0.00 £0.00 %

Non-Current Assets (Fixed

Assets)

Premises 5240 7360 40.46%

Plant & Equipment 2375 4057 70.82%

7615 11417 49.93%

Current Assets

Inventory 2386 3420 43.34%

Trade Receivables 2540 4280 68.50%

4926 7700 56.31%

TOTAL ASSETS 12541 19117 52.44%

Capital

Share Capital 2000 2000 0.00%

Reserves 7813 8268 5.82%

9813 10268 4.64%

Current Liabilities

Trade Payables 1157 2245 94.04%

Overdraft 351 2929 734.47%

1508 5174 243.10%

Non-current liabilities

Loans 1220 3675 201.23%

Total Liabilities 2728 8849 224.38%

TOTAL CAPITAL &

LIABILITIES 12541 19117 52.44%

Shower Pak Limited shows the positive change increase of Balance Sheet items of 52.44%.

It shows that due to the increase in the assets net profit of the company also increased. This shows

Operating Profit 914 1042 14.00%

Less: Interest payable -22 -81 268.18%

Net Profit before tax 892 961 7.74%

Less: Taxation -358 -386 7.82%

Net profit after tax 534 575 7.68%

Shower Pak Limited Income Statement shows a positive change in the increase of net profit

after taxes of 7.68%. Company's gross profit is showing more increase as compared to the increase

in the net profit. It is because of the high increase in the operating expenses of 21.09% and also high

increase in the financial charges which were increased by 268.18%. The company should mainly

focus on two items of Income Statement i.e. interest expenses and operating expenses of Shower

pak Limited.

Calculation of Balance Sheet of Shower Pak Limited

Statement of Financial

Position 2017 2018 % change

£0.00 £0.00 £0.00 £0.00 %

Non-Current Assets (Fixed

Assets)

Premises 5240 7360 40.46%

Plant & Equipment 2375 4057 70.82%

7615 11417 49.93%

Current Assets

Inventory 2386 3420 43.34%

Trade Receivables 2540 4280 68.50%

4926 7700 56.31%

TOTAL ASSETS 12541 19117 52.44%

Capital

Share Capital 2000 2000 0.00%

Reserves 7813 8268 5.82%

9813 10268 4.64%

Current Liabilities

Trade Payables 1157 2245 94.04%

Overdraft 351 2929 734.47%

1508 5174 243.10%

Non-current liabilities

Loans 1220 3675 201.23%

Total Liabilities 2728 8849 224.38%

TOTAL CAPITAL &

LIABILITIES 12541 19117 52.44%

Shower Pak Limited shows the positive change increase of Balance Sheet items of 52.44%.

It shows that due to the increase in the assets net profit of the company also increased. This shows

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that the company should more invest in its productive assets in order to increase the sales of the

company.

1.3 Comparison of Capital at the beginning of the year to end of the year

Shower Pak Limited capital increased by 4.64% which shows the positive sign for the

company. It shows that the company is retaining back its profits rather than giving dividends to the

company. Company's retained earnings are increased which shows that for funding purpose

company is using its own profits to purchase the assets of the company.

LO 2

2.1 Effect on profit of incorrect identification of capital and revenue expenditure

Shower Pak limited incorrectly recognises the capital expenditure as revenue expenditure

than the profits of the company will be understated and expenses will be shown more and non-

current assets of the company will also be understated (Sandford 2015).

Shower Pak Limited recognising revenue expenditure as capital expenditure than the profits

of the company will be overstated and revenues will be increased and non- current assets will be

overstated.

2.2 Difference between net Profit and Gross Profit of Shower Pak Limited

Net Profit Gross Profit

Net Profit is calculated after charging all the

direct and indirect expenses of Shower Pak

Limited (Amar 2018)

Gross Profit is calculated after charging only

direct expenses i.e. cost of goods sold of Shower

Pak Limited.

Net Profit shows the each dollar earned by the

company as revenue translates into profit.

Gross Profit shows the absolute dollar amount

revenue generated by the company.

2.3 Difference between Cost of Sales and Turnover of Shower Pak Limited

Cost of Sales Turnover

Cost of Sales is the total cost charged by Shower

Pak Limited that includes all the cost from

conversion of raw material into finished goods.

Turnover is known as the revenue of the Shower

Pak Limited which shows the sales of the

company (Skiba 2016).

It represents the cost of the company. It represents the revenue of the company.

LO 3

company.

1.3 Comparison of Capital at the beginning of the year to end of the year

Shower Pak Limited capital increased by 4.64% which shows the positive sign for the

company. It shows that the company is retaining back its profits rather than giving dividends to the

company. Company's retained earnings are increased which shows that for funding purpose

company is using its own profits to purchase the assets of the company.

LO 2

2.1 Effect on profit of incorrect identification of capital and revenue expenditure

Shower Pak limited incorrectly recognises the capital expenditure as revenue expenditure

than the profits of the company will be understated and expenses will be shown more and non-

current assets of the company will also be understated (Sandford 2015).

Shower Pak Limited recognising revenue expenditure as capital expenditure than the profits

of the company will be overstated and revenues will be increased and non- current assets will be

overstated.

2.2 Difference between net Profit and Gross Profit of Shower Pak Limited

Net Profit Gross Profit

Net Profit is calculated after charging all the

direct and indirect expenses of Shower Pak

Limited (Amar 2018)

Gross Profit is calculated after charging only

direct expenses i.e. cost of goods sold of Shower

Pak Limited.

Net Profit shows the each dollar earned by the

company as revenue translates into profit.

Gross Profit shows the absolute dollar amount

revenue generated by the company.

2.3 Difference between Cost of Sales and Turnover of Shower Pak Limited

Cost of Sales Turnover

Cost of Sales is the total cost charged by Shower

Pak Limited that includes all the cost from

conversion of raw material into finished goods.

Turnover is known as the revenue of the Shower

Pak Limited which shows the sales of the

company (Skiba 2016).

It represents the cost of the company. It represents the revenue of the company.

LO 3

3.1 Interpreting meaning of cash flow statement.

A Cash flow statement is also known as Statement of cash flow, is one of the essential

financial statement which depicts the effectiveness of changes in the amount of balance sheet and

income for a relevant accounting period thereby affecting the position of cash and cash equivalents

of the business operations. It further breaks down the amount of cash and cash equivalents into

different activities named as Operating, Financial and Investing.

The main purpose of cash flow statement is that it helps the investor, business management,

other stakeholders in assessing the current cash positions, flow of cash and money amount taking

place during a specific time period. It provides deep insight about receipts, payments and changes

which has taken place in the cash position because of several business transactions taking place in

an accounting year under the heading of operational, investing and financial business activities

(Reid and Myddelton, 2017). It defines the position of cash which the company is having at the

financial year starting and at the ending i.e. Financial position of company for that year.

3.2 Explaining reasons for discrepancies between bank statement and cash book.

Bank statement is a record either in printed or written form which defines the balance of

amount remaining in the bank account. It also defines the amount which has been withdrawn from

bank account and amount that has been deposited or paid into such account. It is issued or made on

the periodical basis to the bank account holder for better understanding. On the other hand cash

book is a type of financial journals which contains all the information about receipts and payments

of cash nature thereby including all the withdrawals, bank deposits. Possibilities are there that

balance of bank statement and cash book can match because of following reasons:

1. Outstanding cheques – The amount for which cheque has been issued has not yet made its

recording in the books of company can bring such discrepancies.

2. Bank service and cheque printing charges – Amount as deducted by the bank for

rendering banking services such cheque book printing, atm cards etc. Can bring difference

in the amount of bank statement and cash book (Berger, Imbierowicz and Rauch, 2016).

3. Error made on the company's book – At the time of making recording of business

transactions, there can be error or mistake in relation with maintaining correct record of any

business transaction.

4. Omission – In case of electronic charges, deposit made as appearing on the banl statement

but not yet recorded in the record of company book.

A Cash flow statement is also known as Statement of cash flow, is one of the essential

financial statement which depicts the effectiveness of changes in the amount of balance sheet and

income for a relevant accounting period thereby affecting the position of cash and cash equivalents

of the business operations. It further breaks down the amount of cash and cash equivalents into

different activities named as Operating, Financial and Investing.

The main purpose of cash flow statement is that it helps the investor, business management,

other stakeholders in assessing the current cash positions, flow of cash and money amount taking

place during a specific time period. It provides deep insight about receipts, payments and changes

which has taken place in the cash position because of several business transactions taking place in

an accounting year under the heading of operational, investing and financial business activities

(Reid and Myddelton, 2017). It defines the position of cash which the company is having at the

financial year starting and at the ending i.e. Financial position of company for that year.

3.2 Explaining reasons for discrepancies between bank statement and cash book.

Bank statement is a record either in printed or written form which defines the balance of

amount remaining in the bank account. It also defines the amount which has been withdrawn from

bank account and amount that has been deposited or paid into such account. It is issued or made on

the periodical basis to the bank account holder for better understanding. On the other hand cash

book is a type of financial journals which contains all the information about receipts and payments

of cash nature thereby including all the withdrawals, bank deposits. Possibilities are there that

balance of bank statement and cash book can match because of following reasons:

1. Outstanding cheques – The amount for which cheque has been issued has not yet made its

recording in the books of company can bring such discrepancies.

2. Bank service and cheque printing charges – Amount as deducted by the bank for

rendering banking services such cheque book printing, atm cards etc. Can bring difference

in the amount of bank statement and cash book (Berger, Imbierowicz and Rauch, 2016).

3. Error made on the company's book – At the time of making recording of business

transactions, there can be error or mistake in relation with maintaining correct record of any

business transaction.

4. Omission – In case of electronic charges, deposit made as appearing on the banl statement

but not yet recorded in the record of company book.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LO 4

4.1 Analysing use of Benchmarking in measuring performance along with benefits and limitations.

Benchmarking is a tool which assist ShowerPark in measuring and comparing its business

performance with that business organisation which is considered as one of the best performing

industry in the market. It helps in assessing the level of company's business operations, processes by

comparing it will the most profit making company following best and better standards, norms and

concepts. Following are the benefits and limitations:

Advantages Disadvantages

It focuses on bringing

improvements in the level of

performance of both the

employees and business ,

increasing its competitiveness.

It assist ShowerPark in adopting

relevant changes by suggesting

best business processes.

It only emphasises on measuring

performance of business operation

and not evaluate overall business

effectiveness (Bligaard and et.al.,

2016).

It assess best standards as followed

by its competitor without

determining its applicability.

4.2 Analysis of Ratio of ShowerPak Ltd

1. Debtor’s Payment Period – In 2017, it was 98 days and in 2018 it reaches to 137 days. For

every business organisation, it is very important to focus on reducing this period for having

enough liquidity in the business. It is increasing which is not good for company as it may

have to face issue related to cash flow.

2. Creditor’s Payment Period – This ratio depicts time period in which company will pay

back all its due amount in case of credit purchase it has made. It is better for company to

increase this period for having cash and money in meeting currrent or upcoming business

obligtions.

3. Inventory Turnover Period – There has been increase in the inventory turnover period

from 2017 to 2018 i.e. By 177 days to 211 days respectively which is not good as it depicts

that company is not able to convert its inventory in sales effectively.

4. Cash Operating Cycle – It defines the time in which company will be able to convert its

purchase into cash. It is better for ShowerPark to focus on reducing this time period

otherwise it can result in decrease in customer retention base (Robinson and et.al., 2015).

5. Asset Turnover Ratio – It defines how effectively company has uses its assets in generating

4.1 Analysing use of Benchmarking in measuring performance along with benefits and limitations.

Benchmarking is a tool which assist ShowerPark in measuring and comparing its business

performance with that business organisation which is considered as one of the best performing

industry in the market. It helps in assessing the level of company's business operations, processes by

comparing it will the most profit making company following best and better standards, norms and

concepts. Following are the benefits and limitations:

Advantages Disadvantages

It focuses on bringing

improvements in the level of

performance of both the

employees and business ,

increasing its competitiveness.

It assist ShowerPark in adopting

relevant changes by suggesting

best business processes.

It only emphasises on measuring

performance of business operation

and not evaluate overall business

effectiveness (Bligaard and et.al.,

2016).

It assess best standards as followed

by its competitor without

determining its applicability.

4.2 Analysis of Ratio of ShowerPak Ltd

1. Debtor’s Payment Period – In 2017, it was 98 days and in 2018 it reaches to 137 days. For

every business organisation, it is very important to focus on reducing this period for having

enough liquidity in the business. It is increasing which is not good for company as it may

have to face issue related to cash flow.

2. Creditor’s Payment Period – This ratio depicts time period in which company will pay

back all its due amount in case of credit purchase it has made. It is better for company to

increase this period for having cash and money in meeting currrent or upcoming business

obligtions.

3. Inventory Turnover Period – There has been increase in the inventory turnover period

from 2017 to 2018 i.e. By 177 days to 211 days respectively which is not good as it depicts

that company is not able to convert its inventory in sales effectively.

4. Cash Operating Cycle – It defines the time in which company will be able to convert its

purchase into cash. It is better for ShowerPark to focus on reducing this time period

otherwise it can result in decrease in customer retention base (Robinson and et.al., 2015).

5. Asset Turnover Ratio – It defines how effectively company has uses its assets in generating

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit. 0.59 times depicts that company is performing much better as compared to 2017.

CONCLUSION

The report is summarized of the basic accounting of Shower Pak Limited. It includes the

various evaluation and calculation of Income Statement and Balance Sheet and also interpretation

of the company using ratio analysis. Company's performance is overall good and shows the positive

sign and company should try to maintain the same position.

CONCLUSION

The report is summarized of the basic accounting of Shower Pak Limited. It includes the

various evaluation and calculation of Income Statement and Balance Sheet and also interpretation

of the company using ratio analysis. Company's performance is overall good and shows the positive

sign and company should try to maintain the same position.

REFERENCES

Books and Journals

Amar, S.N., (2018). Pengaruh Gross Profit Margin (GPM), Net Profit Margin (NPM), Return On

Asset (ROA), dan Return On Equity (ROE) Terhadap Pertumbuhan Laba pada Perusahaan

property yang Terdaftardi Bursa Efek Indonesia (BEI) Periode 2012-2016.

Berger, A. N., Imbierowicz, B. and Rauch, C., 2016. The roles of corporate governance in bank

failures during the recent financial crisis. Journal of Money, Credit and Banking. 48(4). pp.729-

770.

Bligaard, T. and et.al., 2016. Toward benchmarking in catalysis science: best practices, challenges,

and opportunities. ACS Catalysis. 6(4). pp.2590-2602.

Juárez, F., (2015). The accounting equation inequality: A set theory approach. Global Journal of

Business Research. 9(3). pp.97-104.

Reid, W. and Myddelton, D. R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Robinson, T. R. and et.al., 2015. International financial statement analysis. John Wiley & Sons.

Sandford, C. T., (2015). Economics of public finance: an economic analysis of government

expenditure and revenue in the United Kingdom. Elsevier.

Skiba, J., Saini, A. and Friend, S. B., (2016). The effect of managerial cost prioritization on sales

force turnover. Journal of Business Research. 69(12). pp.5917-5924.

Online

Bank statement and cah book discrepancies. 2019. [Online]. Available through:

<https://www.accountingcoach.com/blog/balance-bank-statement-difference>.

Pros and cons of benchmarking. 2016. [Online]. Available through: <https://brandongaille.com/10-

pros-and-cons-of-benchmarking/>.

Books and Journals

Amar, S.N., (2018). Pengaruh Gross Profit Margin (GPM), Net Profit Margin (NPM), Return On

Asset (ROA), dan Return On Equity (ROE) Terhadap Pertumbuhan Laba pada Perusahaan

property yang Terdaftardi Bursa Efek Indonesia (BEI) Periode 2012-2016.

Berger, A. N., Imbierowicz, B. and Rauch, C., 2016. The roles of corporate governance in bank

failures during the recent financial crisis. Journal of Money, Credit and Banking. 48(4). pp.729-

770.

Bligaard, T. and et.al., 2016. Toward benchmarking in catalysis science: best practices, challenges,

and opportunities. ACS Catalysis. 6(4). pp.2590-2602.

Juárez, F., (2015). The accounting equation inequality: A set theory approach. Global Journal of

Business Research. 9(3). pp.97-104.

Reid, W. and Myddelton, D. R., 2017. Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Robinson, T. R. and et.al., 2015. International financial statement analysis. John Wiley & Sons.

Sandford, C. T., (2015). Economics of public finance: an economic analysis of government

expenditure and revenue in the United Kingdom. Elsevier.

Skiba, J., Saini, A. and Friend, S. B., (2016). The effect of managerial cost prioritization on sales

force turnover. Journal of Business Research. 69(12). pp.5917-5924.

Online

Bank statement and cah book discrepancies. 2019. [Online]. Available through:

<https://www.accountingcoach.com/blog/balance-bank-statement-difference>.

Pros and cons of benchmarking. 2016. [Online]. Available through: <https://brandongaille.com/10-

pros-and-cons-of-benchmarking/>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.