Analyzing the Importance of Financial Management & Accounting Records

VerifiedAdded on 2023/06/11

|11

|2512

|130

Report

AI Summary

This report discusses the significance of financial management in achieving organizational goals, covering resource acquisition, operational efficiency, and strategic decision-making. It highlights the role of financial management in ensuring the availability of funds, effective resource allocation, and overall business performance. The report also examines the importance of accounting records such as cash flow statements, income statements, and balance sheets in providing a comprehensive view of a company's financial health. Furthermore, it delves into the application of financial ratios for evaluating earning margins and financial leverage, emphasizing their utility in managerial decision-making, financial budgeting, and comparative analysis. The analysis includes a practical review of a company's financial data, calculating key ratios like gross profit margin, net profit margin, current ratio, and quick ratio to assess its profitability and liquidity. The report concludes that effective financial management and insightful accounting practices are crucial for long-term business viability and success.

Importance of Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION 1.....................................................................................................................................1

The Significance of Fiscal Administration..................................................................................1

SECTION 2.....................................................................................................................................2

Accounting records and the usage of ratios are discussed...........................................................2

REFERENCES................................................................................................................................6

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION 1.....................................................................................................................................1

The Significance of Fiscal Administration..................................................................................1

SECTION 2.....................................................................................................................................2

Accounting records and the usage of ratios are discussed...........................................................2

REFERENCES................................................................................................................................6

INTRODUCTION

Financial management relates to the money and financing that a company uses to achieve its

aims and ambitions (Bouveret, 2018). From the purchase of primary materials to the delivery of

products and services to customers, financing is critical to the success of a corporation. Financial

management refers to the acquisition of resources for the purpose of meeting corporate needs. It

provides funding for a company's operating flow and investment needs, as well as flexibility of

resources. The necessity of fiscal administration in company as well as the examination of how it is

very crucial and critical for a firm in the long run scenario as it aids a business in taking relevant and

appropriate decisions based on it is discussed in this study. It also covers various monetary

statements as well as the usage of ratios in fiscal planning.

SECTION 1

The Significance of Fiscal Administration

Monetary administration is the procedure of an organization's money and finance-related

operations being managed. It ensures that finances are available to satisfy everyday operations needs

and that monies are used efficiently. Monetary planning entails taking decisions on investments,

immovable property purchases, and funding sources, among other things. It aids in the strategy,

organisation, and supervision of financial activities. It also includes judgments about the yield on

capital for investors. It gives data about the net value, revenue, and costs, allowing managers to

make informed selections. Managers would be able to see where their company's money is being

spent and would be able to cut down on waste (Foyeke, Olusola and Aderemi, 2016). Money

planning plays a vital part in the achievement of a company for the following reasons:

Monetary choices as it assists managers in making fiscal selections that impact the

organization's operation. Monetary decisions would have a bearing on some other

departments of a company because each division's activities need funding. Such choices

assist the company in achieving its longer-term objectives.

Increased performance as it aids in the efficient use of finances, resulting in increased firm

revenue. It improves company's value by controlling costs via budgeting management,

financial estimation, as well as other tools. It also encourages employees to save, lowering

the expense of acquiring finance.

Financial management relates to the money and financing that a company uses to achieve its

aims and ambitions (Bouveret, 2018). From the purchase of primary materials to the delivery of

products and services to customers, financing is critical to the success of a corporation. Financial

management refers to the acquisition of resources for the purpose of meeting corporate needs. It

provides funding for a company's operating flow and investment needs, as well as flexibility of

resources. The necessity of fiscal administration in company as well as the examination of how it is

very crucial and critical for a firm in the long run scenario as it aids a business in taking relevant and

appropriate decisions based on it is discussed in this study. It also covers various monetary

statements as well as the usage of ratios in fiscal planning.

SECTION 1

The Significance of Fiscal Administration

Monetary administration is the procedure of an organization's money and finance-related

operations being managed. It ensures that finances are available to satisfy everyday operations needs

and that monies are used efficiently. Monetary planning entails taking decisions on investments,

immovable property purchases, and funding sources, among other things. It aids in the strategy,

organisation, and supervision of financial activities. It also includes judgments about the yield on

capital for investors. It gives data about the net value, revenue, and costs, allowing managers to

make informed selections. Managers would be able to see where their company's money is being

spent and would be able to cut down on waste (Foyeke, Olusola and Aderemi, 2016). Money

planning plays a vital part in the achievement of a company for the following reasons:

Monetary choices as it assists managers in making fiscal selections that impact the

organization's operation. Monetary decisions would have a bearing on some other

departments of a company because each division's activities need funding. Such choices

assist the company in achieving its longer-term objectives.

Increased performance as it aids in the efficient use of finances, resulting in increased firm

revenue. It improves company's value by controlling costs via budgeting management,

financial estimation, as well as other tools. It also encourages employees to save, lowering

the expense of acquiring finance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Monetary strategy as it aids in company personal finance. It entails budgeting for company

sources, expenditures, and funding requirements, among other things. It aids businesses in

preparing for challenging situations that arise as a result of environmental changes. Personal

finance assists businesses in accomplishing their intended objectives. It has authority over

the company's costs, expenditures, loans, and earnings.

Money planning aids the organisation in obtaining finances from less expensive sources that

are appropriate for the company's needs. Resources are necessary for a company's operations

to run smoothly. This offers accessibility of resources whenever company have the necessity

of finances. It is required for day-to-day operations, expansion, debt repayment, and the

acquisition of raw materials, among other things (Gomber, Koch and Siering, 2017).

Monetary strategy aids the firm's administrator in making the best use of finances by

allocating money in a manner that allows them to be used successfully. It gives data on

budget allocations, allowing businesses to see where their money is going and lowering

corporate costs.

SECTION 2

Accounting records and the usage of ratios are discussed

Accounting information are indications which aid the firm in conducting the assessment year and

in providing a complete view of the corporation's fiscal status and achievements. The following are

3 different kinds of accounting records which aid in the management of operations and processes:

Cash flow statements- As this assessment relates to the financial transactions and payments

made by a company over a duration of time. This fiscal report shows how much money is

flowing through and receiving back from 3 different types of operations: operational,

investment, and finance (Husain and Sunardi, 2020). Such operations collect and monitor a

company's monetary success, making it easier for creditors and stockholders to identify the

effectiveness appropriately. This aids in the making of educated managerial choices and the

avoidance of economic burden. This section summarises the financial balances, which

indicate how effectively the corporation can repay its borrowing obligations and operational

costs.

Income statements- This report displays a firm's success through time, as well as the group's

production and the supplies necessary to acquire such outcome. This is the P&L statement,

which justifies the organisation's monetary status by displaying comprehensive earnings and

sources, expenditures, and funding requirements, among other things. It aids businesses in

preparing for challenging situations that arise as a result of environmental changes. Personal

finance assists businesses in accomplishing their intended objectives. It has authority over

the company's costs, expenditures, loans, and earnings.

Money planning aids the organisation in obtaining finances from less expensive sources that

are appropriate for the company's needs. Resources are necessary for a company's operations

to run smoothly. This offers accessibility of resources whenever company have the necessity

of finances. It is required for day-to-day operations, expansion, debt repayment, and the

acquisition of raw materials, among other things (Gomber, Koch and Siering, 2017).

Monetary strategy aids the firm's administrator in making the best use of finances by

allocating money in a manner that allows them to be used successfully. It gives data on

budget allocations, allowing businesses to see where their money is going and lowering

corporate costs.

SECTION 2

Accounting records and the usage of ratios are discussed

Accounting information are indications which aid the firm in conducting the assessment year and

in providing a complete view of the corporation's fiscal status and achievements. The following are

3 different kinds of accounting records which aid in the management of operations and processes:

Cash flow statements- As this assessment relates to the financial transactions and payments

made by a company over a duration of time. This fiscal report shows how much money is

flowing through and receiving back from 3 different types of operations: operational,

investment, and finance (Husain and Sunardi, 2020). Such operations collect and monitor a

company's monetary success, making it easier for creditors and stockholders to identify the

effectiveness appropriately. This aids in the making of educated managerial choices and the

avoidance of economic burden. This section summarises the financial balances, which

indicate how effectively the corporation can repay its borrowing obligations and operational

costs.

Income statements- This report displays a firm's success through time, as well as the group's

production and the supplies necessary to acquire such outcome. This is the P&L statement,

which justifies the organisation's monetary status by displaying comprehensive earnings and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

spending. This is a crucial element of comparing earnings and spending from various

variances in operational costs, investment and development costs, and basic component costs

that influence the firm's results.

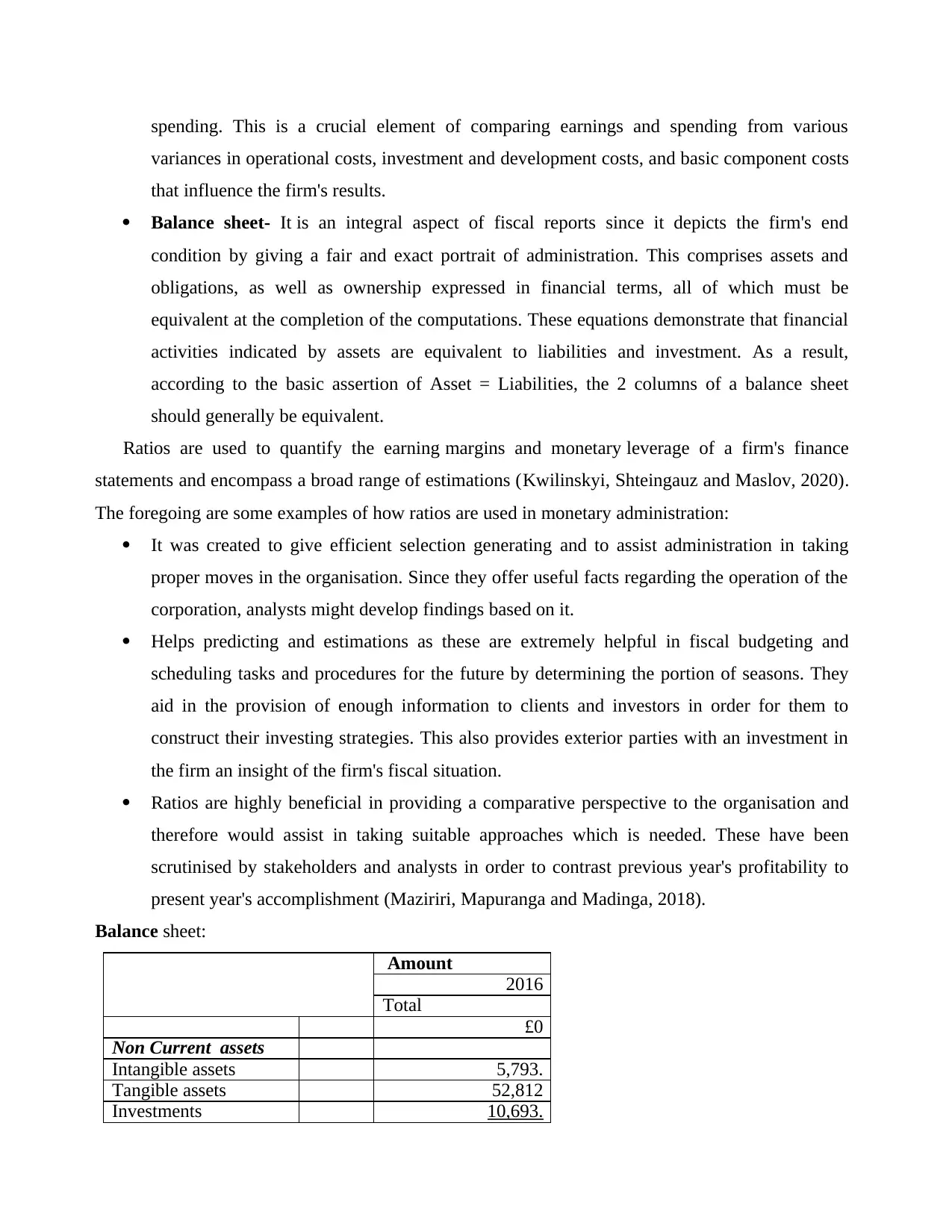

Balance sheet- It is an integral aspect of fiscal reports since it depicts the firm's end

condition by giving a fair and exact portrait of administration. This comprises assets and

obligations, as well as ownership expressed in financial terms, all of which must be

equivalent at the completion of the computations. These equations demonstrate that financial

activities indicated by assets are equivalent to liabilities and investment. As a result,

according to the basic assertion of Asset = Liabilities, the 2 columns of a balance sheet

should generally be equivalent.

Ratios are used to quantify the earning margins and monetary leverage of a firm's finance

statements and encompass a broad range of estimations (Kwilinskyi, Shteingauz and Maslov, 2020).

The foregoing are some examples of how ratios are used in monetary administration:

It was created to give efficient selection generating and to assist administration in taking

proper moves in the organisation. Since they offer useful facts regarding the operation of the

corporation, analysts might develop findings based on it.

Helps predicting and estimations as these are extremely helpful in fiscal budgeting and

scheduling tasks and procedures for the future by determining the portion of seasons. They

aid in the provision of enough information to clients and investors in order for them to

construct their investing strategies. This also provides exterior parties with an investment in

the firm an insight of the firm's fiscal situation.

Ratios are highly beneficial in providing a comparative perspective to the organisation and

therefore would assist in taking suitable approaches which is needed. These have been

scrutinised by stakeholders and analysts in order to contrast previous year's profitability to

present year's accomplishment (Maziriri, Mapuranga and Madinga, 2018).

Balance sheet:

Amount

2016

Total

£0

Non Current assets

Intangible assets 5,793.

Tangible assets 52,812

Investments 10,693.

variances in operational costs, investment and development costs, and basic component costs

that influence the firm's results.

Balance sheet- It is an integral aspect of fiscal reports since it depicts the firm's end

condition by giving a fair and exact portrait of administration. This comprises assets and

obligations, as well as ownership expressed in financial terms, all of which must be

equivalent at the completion of the computations. These equations demonstrate that financial

activities indicated by assets are equivalent to liabilities and investment. As a result,

according to the basic assertion of Asset = Liabilities, the 2 columns of a balance sheet

should generally be equivalent.

Ratios are used to quantify the earning margins and monetary leverage of a firm's finance

statements and encompass a broad range of estimations (Kwilinskyi, Shteingauz and Maslov, 2020).

The foregoing are some examples of how ratios are used in monetary administration:

It was created to give efficient selection generating and to assist administration in taking

proper moves in the organisation. Since they offer useful facts regarding the operation of the

corporation, analysts might develop findings based on it.

Helps predicting and estimations as these are extremely helpful in fiscal budgeting and

scheduling tasks and procedures for the future by determining the portion of seasons. They

aid in the provision of enough information to clients and investors in order for them to

construct their investing strategies. This also provides exterior parties with an investment in

the firm an insight of the firm's fiscal situation.

Ratios are highly beneficial in providing a comparative perspective to the organisation and

therefore would assist in taking suitable approaches which is needed. These have been

scrutinised by stakeholders and analysts in order to contrast previous year's profitability to

present year's accomplishment (Maziriri, Mapuranga and Madinga, 2018).

Balance sheet:

Amount

2016

Total

£0

Non Current assets

Intangible assets 5,793.

Tangible assets 52,812

Investments 10,693.

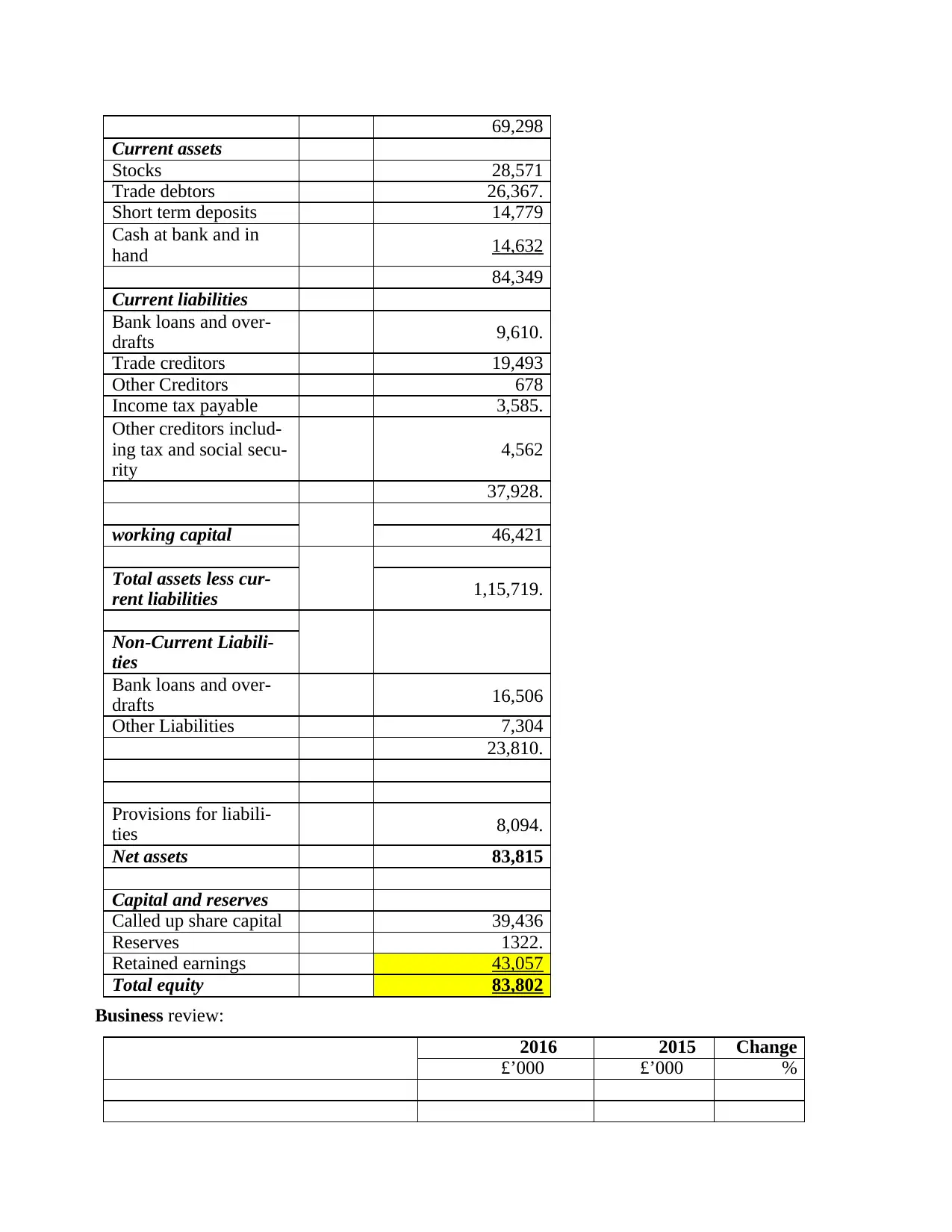

69,298

Current assets

Stocks 28,571

Trade debtors 26,367.

Short term deposits 14,779

Cash at bank and in

hand 14,632

84,349

Current liabilities

Bank loans and over-

drafts 9,610.

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585.

Other creditors includ-

ing tax and social secu-

rity

4,562

37,928.

working capital 46,421

Total assets less cur-

rent liabilities 1,15,719.

Non-Current Liabili-

ties

Bank loans and over-

drafts 16,506

Other Liabilities 7,304

23,810.

Provisions for liabili-

ties 8,094.

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322.

Retained earnings 43,057

Total equity 83,802

Business review:

2016 2015 Change

£’000 £’000 %

Current assets

Stocks 28,571

Trade debtors 26,367.

Short term deposits 14,779

Cash at bank and in

hand 14,632

84,349

Current liabilities

Bank loans and over-

drafts 9,610.

Trade creditors 19,493

Other Creditors 678

Income tax payable 3,585.

Other creditors includ-

ing tax and social secu-

rity

4,562

37,928.

working capital 46,421

Total assets less cur-

rent liabilities 1,15,719.

Non-Current Liabili-

ties

Bank loans and over-

drafts 16,506

Other Liabilities 7,304

23,810.

Provisions for liabili-

ties 8,094.

Net assets 83,815

Capital and reserves

Called up share capital 39,436

Reserves 1322.

Retained earnings 43,057

Total equity 83,802

Business review:

2016 2015 Change

£’000 £’000 %

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

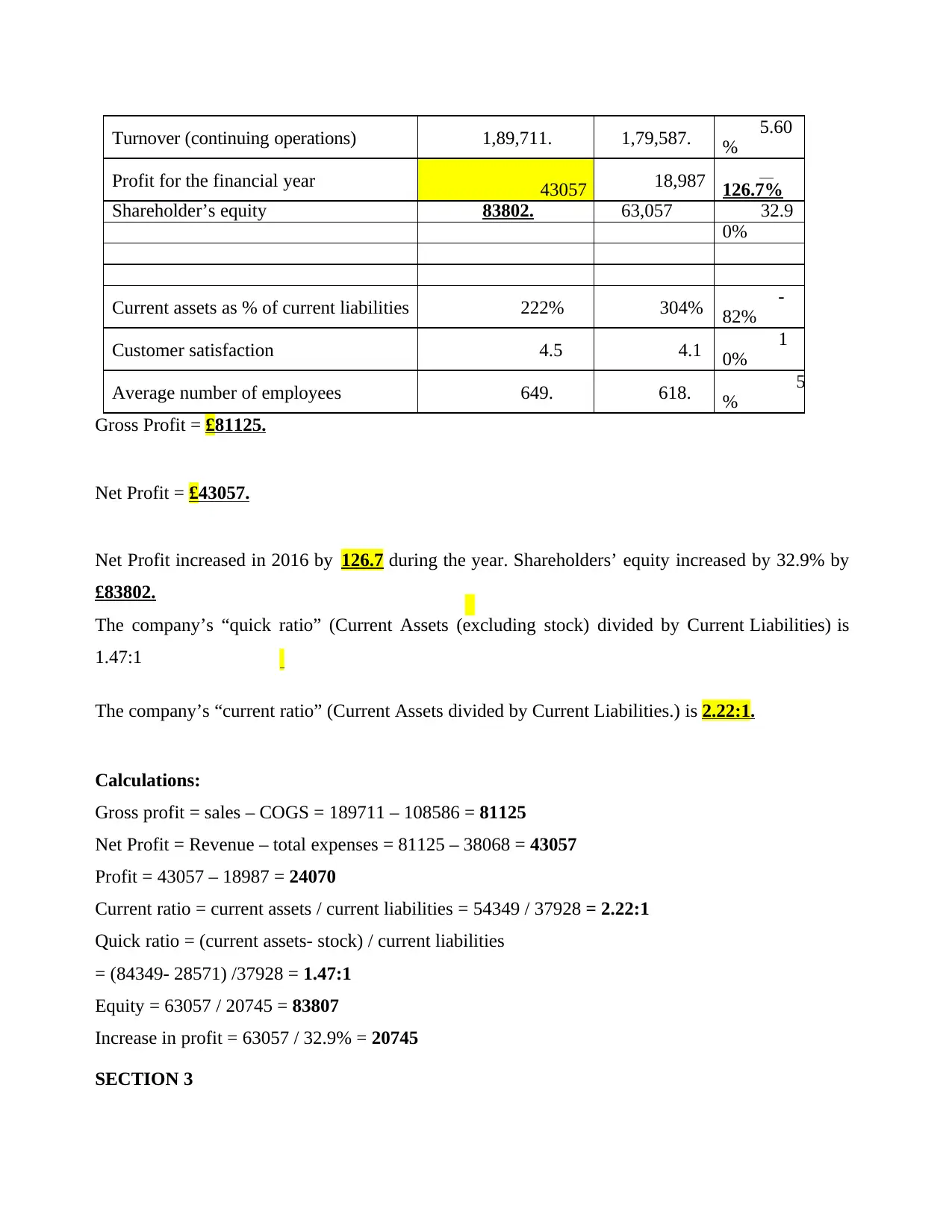

Turnover (continuing operations) 1,89,711. 1,79,587. 5.60

%

Profit for the financial year 43057 18,987 126.7%

Shareholder’s equity 83802. 63,057 32.9

0%

Current assets as % of current liabilities 222% 304% -

82%

Customer satisfaction 4.5 4.1 1

0%

Average number of employees 649. 618. 5

%

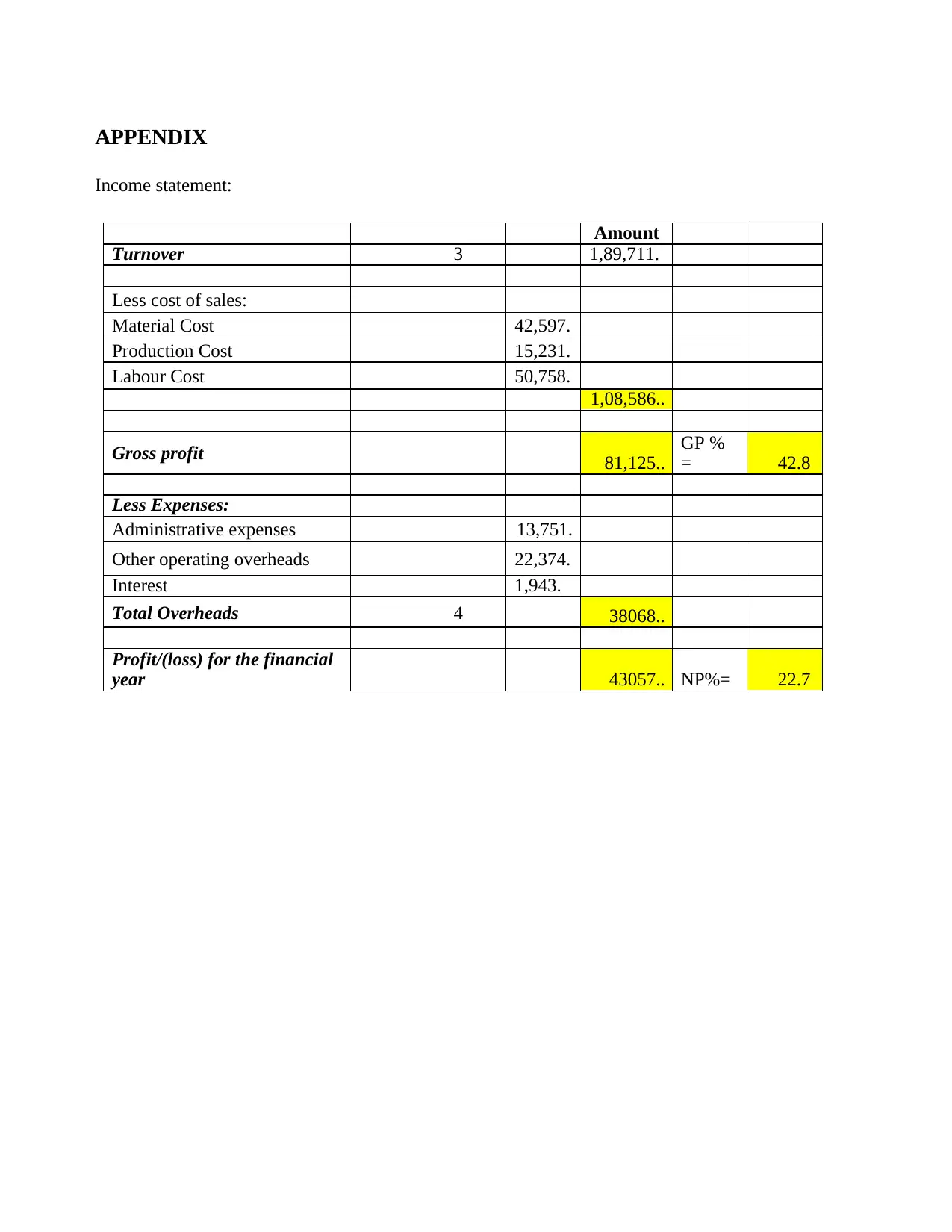

Gross Profit = £81125.

Net Profit = £43057.

Net Profit increased in 2016 by 126.7 during the year. Shareholders’ equity increased by 32.9% by

£83802.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current Liabilities) is

1.47:1

The company’s “current ratio” (Current Assets divided by Current Liabilities.) is 2.22:1.

Calculations:

Gross profit = sales – COGS = 189711 – 108586 = 81125

Net Profit = Revenue – total expenses = 81125 – 38068 = 43057

Profit = 43057 – 18987 = 24070

Current ratio = current assets / current liabilities = 54349 / 37928 = 2.22:1

Quick ratio = (current assets- stock) / current liabilities

= (84349- 28571) /37928 = 1.47:1

Equity = 63057 / 20745 = 83807

Increase in profit = 63057 / 32.9% = 20745

SECTION 3

%

Profit for the financial year 43057 18,987 126.7%

Shareholder’s equity 83802. 63,057 32.9

0%

Current assets as % of current liabilities 222% 304% -

82%

Customer satisfaction 4.5 4.1 1

0%

Average number of employees 649. 618. 5

%

Gross Profit = £81125.

Net Profit = £43057.

Net Profit increased in 2016 by 126.7 during the year. Shareholders’ equity increased by 32.9% by

£83802.

The company’s “quick ratio” (Current Assets (excluding stock) divided by Current Liabilities) is

1.47:1

The company’s “current ratio” (Current Assets divided by Current Liabilities.) is 2.22:1.

Calculations:

Gross profit = sales – COGS = 189711 – 108586 = 81125

Net Profit = Revenue – total expenses = 81125 – 38068 = 43057

Profit = 43057 – 18987 = 24070

Current ratio = current assets / current liabilities = 54349 / 37928 = 2.22:1

Quick ratio = (current assets- stock) / current liabilities

= (84349- 28571) /37928 = 1.47:1

Equity = 63057 / 20745 = 83807

Increase in profit = 63057 / 32.9% = 20745

SECTION 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit ratio: It is a measure of a company's revenue. It displays a firm's financial

performance by subtracting all of the corporation's expenditures from the income earned through

selling.

Net profit margin = Net profit/ Sales* 100

=43057 / 189711 * 100

= 22.69%

Gross profit: This quantitative measurement allows a group's revenue generated out of its

primary activities to be expressed. It is calculated by subtracting a firm's operating expenditures

from its aggregate revenues (Panos and Wilson, 2020).

Gross profit margin= Gross profit/Sales*100

=81125 / 189711 * 100

= 42.76%

Current ratio: This liquidity coefficient guarantees that an organization's capacity to repay is

assessed in the perspective of short-term commitments. It includes both current liabilities and

current assets.

Current ratio = Current assets / current liabilities

= 54349 / 37928

= 2.22:1

Quick ratio: It shows a firm's short-term financial status and allows for the analysis of a

corporation's capacity to repay off short-term borrowing. It's also known as the acid test ratio. A

good quick ratio is one to one which implies that quick assets are equal to current liabilities.

Liquidity ratio is a measurement of an institution's liquidity standing.

Quick ratio = (Current assets – inventory) / current liabilities

= (84349 – 28571) / 37928

= 1.47: 1

According to the aforementioned ratio assessment, a group's overall effectiveness is creating a

significant degree of earnings in relation to its main activities. It could be indicated by examining a

company's current gross profitability margins, as the organisation generates a higher net profitability

percentage (Subires and Bolivar, 2017). On the other hand, the business strives to improve its

aggregate profitability percentage, which may be measured by lowering superfluous expenditures.

Aside from that, a company's fiscal standing is sound. As a result, the firm must improve its

performance by subtracting all of the corporation's expenditures from the income earned through

selling.

Net profit margin = Net profit/ Sales* 100

=43057 / 189711 * 100

= 22.69%

Gross profit: This quantitative measurement allows a group's revenue generated out of its

primary activities to be expressed. It is calculated by subtracting a firm's operating expenditures

from its aggregate revenues (Panos and Wilson, 2020).

Gross profit margin= Gross profit/Sales*100

=81125 / 189711 * 100

= 42.76%

Current ratio: This liquidity coefficient guarantees that an organization's capacity to repay is

assessed in the perspective of short-term commitments. It includes both current liabilities and

current assets.

Current ratio = Current assets / current liabilities

= 54349 / 37928

= 2.22:1

Quick ratio: It shows a firm's short-term financial status and allows for the analysis of a

corporation's capacity to repay off short-term borrowing. It's also known as the acid test ratio. A

good quick ratio is one to one which implies that quick assets are equal to current liabilities.

Liquidity ratio is a measurement of an institution's liquidity standing.

Quick ratio = (Current assets – inventory) / current liabilities

= (84349 – 28571) / 37928

= 1.47: 1

According to the aforementioned ratio assessment, a group's overall effectiveness is creating a

significant degree of earnings in relation to its main activities. It could be indicated by examining a

company's current gross profitability margins, as the organisation generates a higher net profitability

percentage (Subires and Bolivar, 2017). On the other hand, the business strives to improve its

aggregate profitability percentage, which may be measured by lowering superfluous expenditures.

Aside from that, a company's fiscal standing is sound. As a result, the firm must improve its

effectiveness by removing superfluous expenses and maintaining effective finance

administration that allows the organisation to improve its commercial competence degree.

CONCLUSION

The above analysis indicates that fiscal administration is a company's soul. It denotes the

activity of controlling or regulating a company's monetary operations. Financial administration

allows a group's effectiveness to be assessed. This strategy combines a number of finance-related

operations, including static wealth monitoring, income identification, bookkeeping, and transaction

handling. Furthermore, accounting information include an overall vision of an institution's stance

financially. A report of fiscal position provided an outline of a company's monetary condition. It

refers to a documented document which details a company's monetary actions. It contains all

finance-related information that is important to company. As a result, accounting records assist an

organisation in creating successful plans for improving a company's revenue situation. Furthermore,

accounting report calculation allows an institution's executive staff to make well-informed actions,

which allows the companies improve its productivity and ensure long-term effectiveness and

viability. The balance sheet, income statement, and cash flow statement are all examples of finance

reports. Besides that, accounting ratios aids an institution in examining an institution's solvency,

competitiveness, operating, and effectiveness levels in order to assess its output and effectiveness.

administration that allows the organisation to improve its commercial competence degree.

CONCLUSION

The above analysis indicates that fiscal administration is a company's soul. It denotes the

activity of controlling or regulating a company's monetary operations. Financial administration

allows a group's effectiveness to be assessed. This strategy combines a number of finance-related

operations, including static wealth monitoring, income identification, bookkeeping, and transaction

handling. Furthermore, accounting information include an overall vision of an institution's stance

financially. A report of fiscal position provided an outline of a company's monetary condition. It

refers to a documented document which details a company's monetary actions. It contains all

finance-related information that is important to company. As a result, accounting records assist an

organisation in creating successful plans for improving a company's revenue situation. Furthermore,

accounting report calculation allows an institution's executive staff to make well-informed actions,

which allows the companies improve its productivity and ensure long-term effectiveness and

viability. The balance sheet, income statement, and cash flow statement are all examples of finance

reports. Besides that, accounting ratios aids an institution in examining an institution's solvency,

competitiveness, operating, and effectiveness levels in order to assess its output and effectiveness.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and journals

Bouveret, A., 2018. Cyber risk for the financial sector: A framework for quantitative assessment.

International Monetary Fund.

Foyeke, O.I., Olusola, F.S. and Aderemi, A.K., 2016. Financial structure and the profitability of

manufacturing companies in Nigeria.

Gomber, P., Koch, J. A. and Siering, M., 2017. Digital Finance and FinTech: current research and

future research directions. Journal of Business Economics. 87(5). pp.537-580.

Husain, T. and Sunardi, N., 2020. Firm's Value Prediction Based on Profitability Ratios and

Dividend Policy. Finance & Economics Review, 2(2), pp.13-26.

Kwilinskyi, O., Shteingauz, D. and Maslov, V., 2020. Financial and credit instruments for ensuring

effective functioning of the residential real estate market.

Maziriri, E. T., Mapuranga, M. and Madinga, N. W., 2018. Self-service banking and financial

literacy as prognosticators of business performance among rural small and medium-sized

enterprises in Zimbabwe. The Southern African Journal of Entrepreneurship and Small

Business Management. 10(1). p.10.

Panos, G.A. and Wilson, J.O., 2020. Financial literacy and responsible finance in the FinTech era:

capabilities and challenges.

Subires, M.D.L. and Bolivar, M.P.R., 2017. Financial Sustainability in Governments. A New

Concept and Measure for Meeting New Information Needs. In Financial Sustainability in

Public Administration (pp. 3-20). Palgrave Macmillan, Cham.

Books and journals

Bouveret, A., 2018. Cyber risk for the financial sector: A framework for quantitative assessment.

International Monetary Fund.

Foyeke, O.I., Olusola, F.S. and Aderemi, A.K., 2016. Financial structure and the profitability of

manufacturing companies in Nigeria.

Gomber, P., Koch, J. A. and Siering, M., 2017. Digital Finance and FinTech: current research and

future research directions. Journal of Business Economics. 87(5). pp.537-580.

Husain, T. and Sunardi, N., 2020. Firm's Value Prediction Based on Profitability Ratios and

Dividend Policy. Finance & Economics Review, 2(2), pp.13-26.

Kwilinskyi, O., Shteingauz, D. and Maslov, V., 2020. Financial and credit instruments for ensuring

effective functioning of the residential real estate market.

Maziriri, E. T., Mapuranga, M. and Madinga, N. W., 2018. Self-service banking and financial

literacy as prognosticators of business performance among rural small and medium-sized

enterprises in Zimbabwe. The Southern African Journal of Entrepreneurship and Small

Business Management. 10(1). p.10.

Panos, G.A. and Wilson, J.O., 2020. Financial literacy and responsible finance in the FinTech era:

capabilities and challenges.

Subires, M.D.L. and Bolivar, M.P.R., 2017. Financial Sustainability in Governments. A New

Concept and Measure for Meeting New Information Needs. In Financial Sustainability in

Public Administration (pp. 3-20). Palgrave Macmillan, Cham.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

Income statement:

Amount

Turnover 3 1,89,711.

Less cost of sales:

Material Cost 42,597.

Production Cost 15,231.

Labour Cost 50,758.

1,08,586..

Gross profit 81,125..

GP %

= 42.8

Less Expenses:

Administrative expenses 13,751.

Other operating overheads 22,374.

Interest 1,943.

Total Overheads 4 38068..

Profit/(loss) for the financial

year 43057.. NP%= 22.7

Income statement:

Amount

Turnover 3 1,89,711.

Less cost of sales:

Material Cost 42,597.

Production Cost 15,231.

Labour Cost 50,758.

1,08,586..

Gross profit 81,125..

GP %

= 42.8

Less Expenses:

Administrative expenses 13,751.

Other operating overheads 22,374.

Interest 1,943.

Total Overheads 4 38068..

Profit/(loss) for the financial

year 43057.. NP%= 22.7

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.