APC 308 Financial Management Assessment: WACC, Rights Issue, & Capital

VerifiedAdded on 2023/01/17

|20

|3920

|69

Report

AI Summary

This comprehensive financial management report analyzes Kadlex plc, focusing on weighted average cost of capital (WACC) calculations, rights issues, and capital structure adjustments. The assessment explores both book value and market value approaches to WACC, evaluating the impact of capital restructuring on minimizing the cost of capital. It delves into the implications of short-termism on bankruptcy and agency problems, supported by academic research. The report also covers the calculation of the number of shares to be issued, the theoretical ex-right price, and the expected value of earnings per share. Furthermore, it evaluates project evaluation methods, comparing the benefits and limitations of various investment appraisal techniques such as payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR). The report provides detailed tables and calculations to support its findings and recommendations regarding the finance director's projections, emphasizing the importance of capital structure in financial decision-making.

APC 308 FINANCIAL

MANAGEMENT ASSESSMENT 2019

MANAGEMENT ASSESSMENT 2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

a) Calculation of Book Value and Market value cost of Capital (WACC) for Kadlex plc.........1

b) Cost of Capital of company as per the new structure of Kadlex plc......................................5

c) Minimising the cost of capital using gearing in the capital structure.....................................9

(d) Critically evaluate the effects of short-termism on bankruptcy and the agency problem in a

company, ensuring the response is supported with relevant academic research.........................9

Question 2......................................................................................................................................10

1 & 2 Number of Shares to be issued and theoretical ex right price.........................................10

3. Calculating expected value of earnings per share.................................................................11

4&5. form of an issue for price of each right issue & Presenting all the three options of the

right issue in the tabular form...................................................................................................11

©Advantage of scrip dividend for shareholders and company.................................................13

Question 3......................................................................................................................................13

(a)Project evaluation methods...................................................................................................13

(b) Critically evaluate the benefits and limitations of each of the differing investment

appraisal techniques..................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................................17

Table 1Weighted Average Cost of Capital......................................................................................1

Table 2Cost of equity.......................................................................................................................2

Table 3Cost of Preference Share Capital (Kp)................................................................................2

Table 4Cost of Debt (Kd)................................................................................................................3

Table 5Capital Structure of Kadlex as on 31 December 2017........................................................3

Table 6Total Value of Debt and Equity...........................................................................................4

Table 7Calculation of Weights........................................................................................................4

Table 8Weighted average cost of capital.........................................................................................5

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

a) Calculation of Book Value and Market value cost of Capital (WACC) for Kadlex plc.........1

b) Cost of Capital of company as per the new structure of Kadlex plc......................................5

c) Minimising the cost of capital using gearing in the capital structure.....................................9

(d) Critically evaluate the effects of short-termism on bankruptcy and the agency problem in a

company, ensuring the response is supported with relevant academic research.........................9

Question 2......................................................................................................................................10

1 & 2 Number of Shares to be issued and theoretical ex right price.........................................10

3. Calculating expected value of earnings per share.................................................................11

4&5. form of an issue for price of each right issue & Presenting all the three options of the

right issue in the tabular form...................................................................................................11

©Advantage of scrip dividend for shareholders and company.................................................13

Question 3......................................................................................................................................13

(a)Project evaluation methods...................................................................................................13

(b) Critically evaluate the benefits and limitations of each of the differing investment

appraisal techniques..................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................................17

Table 1Weighted Average Cost of Capital......................................................................................1

Table 2Cost of equity.......................................................................................................................2

Table 3Cost of Preference Share Capital (Kp)................................................................................2

Table 4Cost of Debt (Kd)................................................................................................................3

Table 5Capital Structure of Kadlex as on 31 December 2017........................................................3

Table 6Total Value of Debt and Equity...........................................................................................4

Table 7Calculation of Weights........................................................................................................4

Table 8Weighted average cost of capital.........................................................................................5

Table 9Cost of Equity (Ke)..............................................................................................................5

Table 10Cost of Preference Share Capital (kp)...............................................................................6

Table 11Cost of Debt (kd)...............................................................................................................6

Table 12Capital structure.................................................................................................................7

Table 13Total Capital......................................................................................................................7

Table 14Calculation of Weights......................................................................................................8

Table 15New share issue and theoretical ex share price...............................................................10

Table 16Earning per share (EPS)..................................................................................................11

Table 17Ex- rights value per share................................................................................................11

Table 18Ex- rights value per share................................................................................................11

Table 19Ex- rights value per share................................................................................................12

Table 20Calculation of depreciation..............................................................................................13

Table 21Payback period................................................................................................................13

Table 22Calculation of ARR.........................................................................................................14

Table 23Calculation of NPV.........................................................................................................14

Table 24Calculation of IRR...........................................................................................................15

Table 10Cost of Preference Share Capital (kp)...............................................................................6

Table 11Cost of Debt (kd)...............................................................................................................6

Table 12Capital structure.................................................................................................................7

Table 13Total Capital......................................................................................................................7

Table 14Calculation of Weights......................................................................................................8

Table 15New share issue and theoretical ex share price...............................................................10

Table 16Earning per share (EPS)..................................................................................................11

Table 17Ex- rights value per share................................................................................................11

Table 18Ex- rights value per share................................................................................................11

Table 19Ex- rights value per share................................................................................................12

Table 20Calculation of depreciation..............................................................................................13

Table 21Payback period................................................................................................................13

Table 22Calculation of ARR.........................................................................................................14

Table 23Calculation of NPV.........................................................................................................14

Table 24Calculation of IRR...........................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

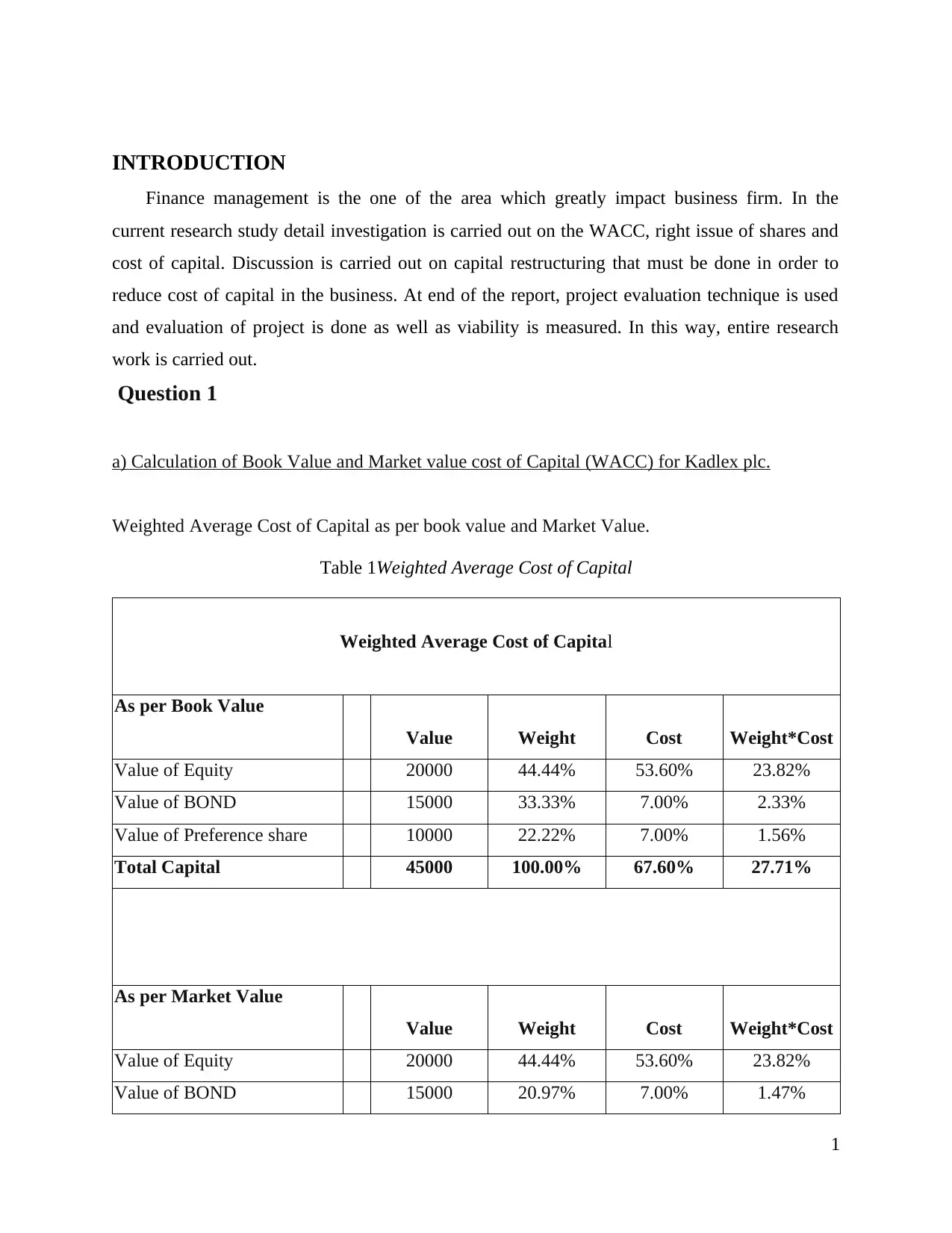

INTRODUCTION

Finance management is the one of the area which greatly impact business firm. In the

current research study detail investigation is carried out on the WACC, right issue of shares and

cost of capital. Discussion is carried out on capital restructuring that must be done in order to

reduce cost of capital in the business. At end of the report, project evaluation technique is used

and evaluation of project is done as well as viability is measured. In this way, entire research

work is carried out.

Question 1

a) Calculation of Book Value and Market value cost of Capital (WACC) for Kadlex plc.

Weighted Average Cost of Capital as per book value and Market Value.

Table 1Weighted Average Cost of Capital

Weighted Average Cost of Capital

As per Book Value

Value Weight Cost Weight*Cost

Value of Equity 20000 44.44% 53.60% 23.82%

Value of BOND 15000 33.33% 7.00% 2.33%

Value of Preference share 10000 22.22% 7.00% 1.56%

Total Capital 45000 100.00% 67.60% 27.71%

As per Market Value

Value Weight Cost Weight*Cost

Value of Equity 20000 44.44% 53.60% 23.82%

Value of BOND 15000 20.97% 7.00% 1.47%

1

Finance management is the one of the area which greatly impact business firm. In the

current research study detail investigation is carried out on the WACC, right issue of shares and

cost of capital. Discussion is carried out on capital restructuring that must be done in order to

reduce cost of capital in the business. At end of the report, project evaluation technique is used

and evaluation of project is done as well as viability is measured. In this way, entire research

work is carried out.

Question 1

a) Calculation of Book Value and Market value cost of Capital (WACC) for Kadlex plc.

Weighted Average Cost of Capital as per book value and Market Value.

Table 1Weighted Average Cost of Capital

Weighted Average Cost of Capital

As per Book Value

Value Weight Cost Weight*Cost

Value of Equity 20000 44.44% 53.60% 23.82%

Value of BOND 15000 33.33% 7.00% 2.33%

Value of Preference share 10000 22.22% 7.00% 1.56%

Total Capital 45000 100.00% 67.60% 27.71%

As per Market Value

Value Weight Cost Weight*Cost

Value of Equity 20000 44.44% 53.60% 23.82%

Value of BOND 15000 20.97% 7.00% 1.47%

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

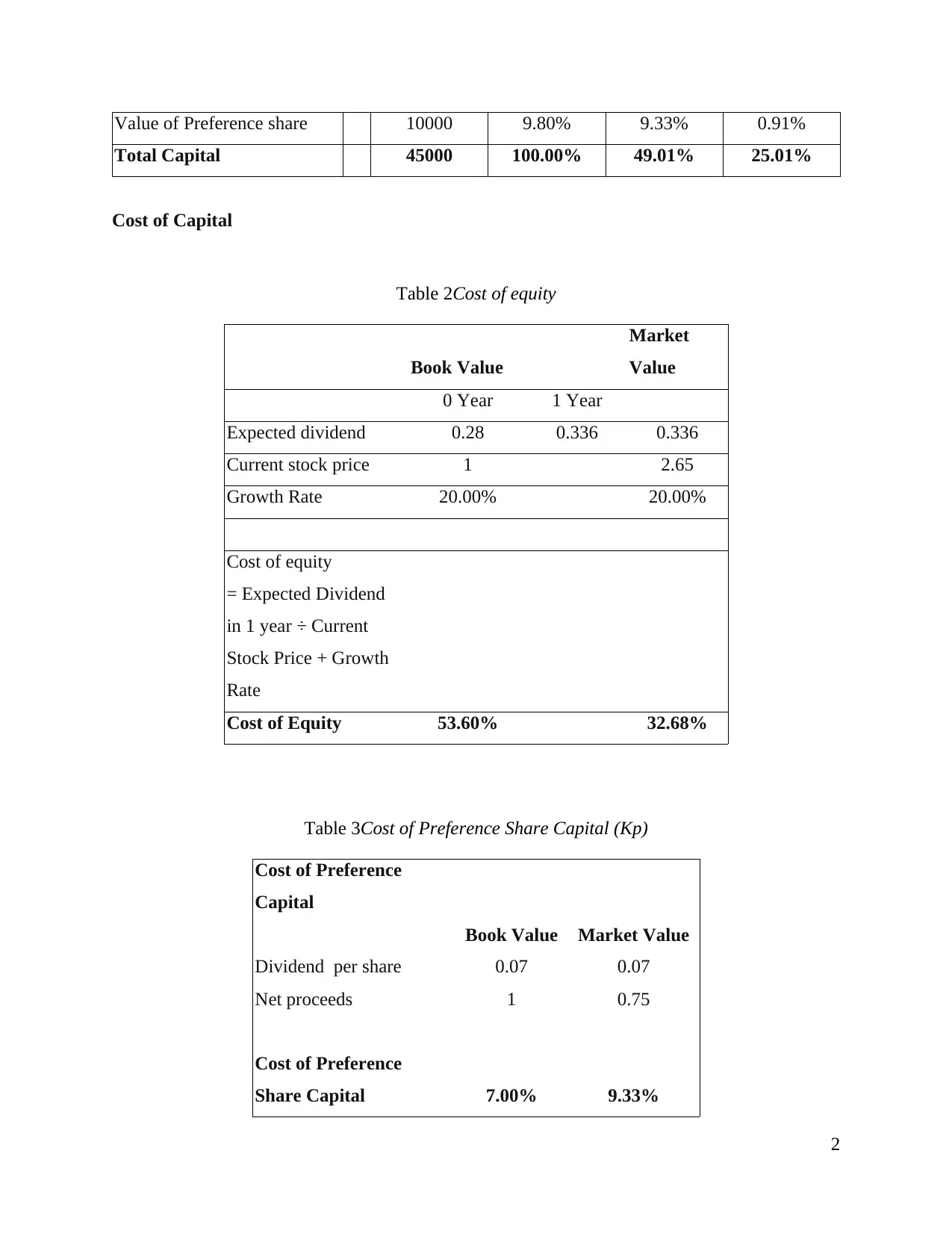

Value of Preference share 10000 9.80% 9.33% 0.91%

Total Capital 45000 100.00% 49.01% 25.01%

Cost of Capital

Table 2Cost of equity

Book Value

Market

Value

0 Year 1 Year

Expected dividend 0.28 0.336 0.336

Current stock price 1 2.65

Growth Rate 20.00% 20.00%

Cost of equity

= Expected Dividend

in 1 year ÷ Current

Stock Price + Growth

Rate

Cost of Equity 53.60% 32.68%

Table 3Cost of Preference Share Capital (Kp)

Cost of Preference

Capital

Book Value Market Value

Dividend per share 0.07 0.07

Net proceeds 1 0.75

Cost of Preference

Share Capital 7.00% 9.33%

2

Total Capital 45000 100.00% 49.01% 25.01%

Cost of Capital

Table 2Cost of equity

Book Value

Market

Value

0 Year 1 Year

Expected dividend 0.28 0.336 0.336

Current stock price 1 2.65

Growth Rate 20.00% 20.00%

Cost of equity

= Expected Dividend

in 1 year ÷ Current

Stock Price + Growth

Rate

Cost of Equity 53.60% 32.68%

Table 3Cost of Preference Share Capital (Kp)

Cost of Preference

Capital

Book Value Market Value

Dividend per share 0.07 0.07

Net proceeds 1 0.75

Cost of Preference

Share Capital 7.00% 9.33%

2

Table 4Cost of Debt (Kd)

Cost of debt 10.00%

After tax debt (1 – 30%)

Cost of debt 7.00%

Table 5Capital Structure of Kadlex as on 31 December 2017

Capital Structure

Book Value Market Value

Current Value of Equity

Number of shares 20000 20000

Price per share 1 2.65

Value of Equity 20000 53000

Current Value of Debt

Number of Bonds 150 150

Price per bond 100 107

Value of BOND 15000 16050

Current Value of

Preference Capital

Number of Preference Shares 10000 10000

3

Cost of debt 10.00%

After tax debt (1 – 30%)

Cost of debt 7.00%

Table 5Capital Structure of Kadlex as on 31 December 2017

Capital Structure

Book Value Market Value

Current Value of Equity

Number of shares 20000 20000

Price per share 1 2.65

Value of Equity 20000 53000

Current Value of Debt

Number of Bonds 150 150

Price per bond 100 107

Value of BOND 15000 16050

Current Value of

Preference Capital

Number of Preference Shares 10000 10000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

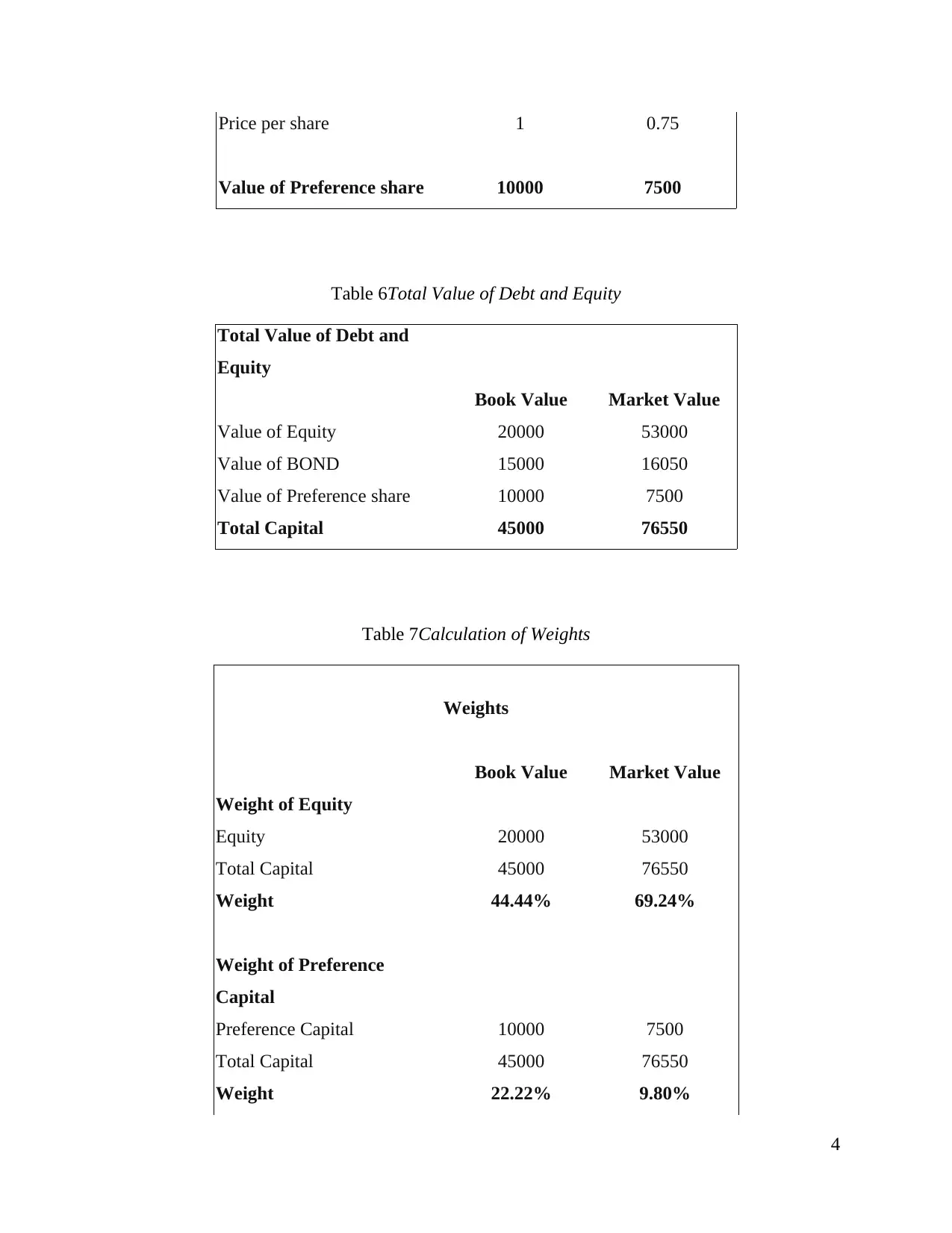

Price per share 1 0.75

Value of Preference share 10000 7500

Table 6Total Value of Debt and Equity

Total Value of Debt and

Equity

Book Value Market Value

Value of Equity 20000 53000

Value of BOND 15000 16050

Value of Preference share 10000 7500

Total Capital 45000 76550

Table 7Calculation of Weights

Weights

Book Value Market Value

Weight of Equity

Equity 20000 53000

Total Capital 45000 76550

Weight 44.44% 69.24%

Weight of Preference

Capital

Preference Capital 10000 7500

Total Capital 45000 76550

Weight 22.22% 9.80%

4

Value of Preference share 10000 7500

Table 6Total Value of Debt and Equity

Total Value of Debt and

Equity

Book Value Market Value

Value of Equity 20000 53000

Value of BOND 15000 16050

Value of Preference share 10000 7500

Total Capital 45000 76550

Table 7Calculation of Weights

Weights

Book Value Market Value

Weight of Equity

Equity 20000 53000

Total Capital 45000 76550

Weight 44.44% 69.24%

Weight of Preference

Capital

Preference Capital 10000 7500

Total Capital 45000 76550

Weight 22.22% 9.80%

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Weight of Debt

Debt 15000 16050

Total Capital 45000 76550

Weight 33.33% 20.97%

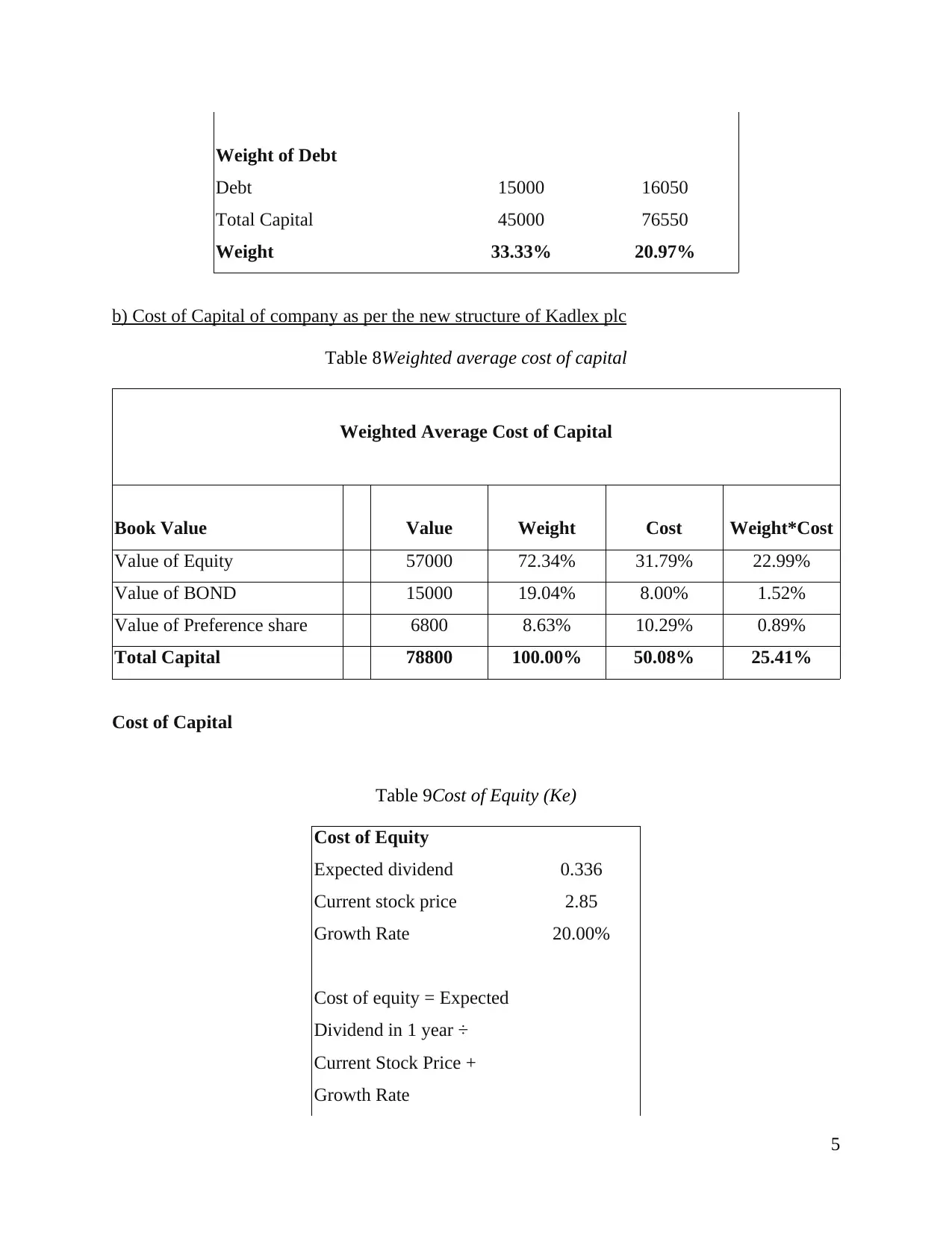

b) Cost of Capital of company as per the new structure of Kadlex plc

Table 8Weighted average cost of capital

Weighted Average Cost of Capital

Book Value Value Weight Cost Weight*Cost

Value of Equity 57000 72.34% 31.79% 22.99%

Value of BOND 15000 19.04% 8.00% 1.52%

Value of Preference share 6800 8.63% 10.29% 0.89%

Total Capital 78800 100.00% 50.08% 25.41%

Cost of Capital

Table 9Cost of Equity (Ke)

Cost of Equity

Expected dividend 0.336

Current stock price 2.85

Growth Rate 20.00%

Cost of equity = Expected

Dividend in 1 year ÷

Current Stock Price +

Growth Rate

5

Debt 15000 16050

Total Capital 45000 76550

Weight 33.33% 20.97%

b) Cost of Capital of company as per the new structure of Kadlex plc

Table 8Weighted average cost of capital

Weighted Average Cost of Capital

Book Value Value Weight Cost Weight*Cost

Value of Equity 57000 72.34% 31.79% 22.99%

Value of BOND 15000 19.04% 8.00% 1.52%

Value of Preference share 6800 8.63% 10.29% 0.89%

Total Capital 78800 100.00% 50.08% 25.41%

Cost of Capital

Table 9Cost of Equity (Ke)

Cost of Equity

Expected dividend 0.336

Current stock price 2.85

Growth Rate 20.00%

Cost of equity = Expected

Dividend in 1 year ÷

Current Stock Price +

Growth Rate

5

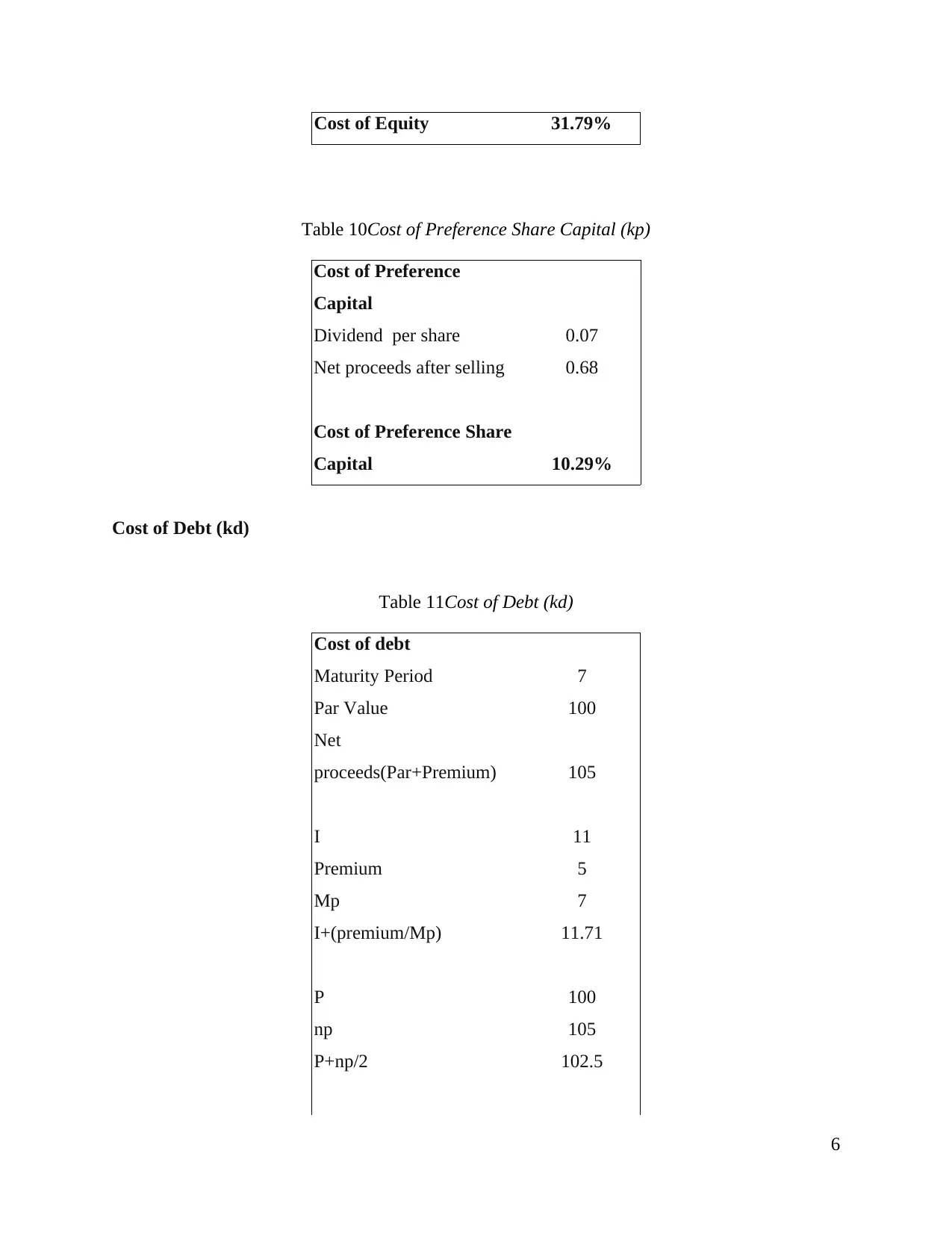

Cost of Equity 31.79%

Table 10Cost of Preference Share Capital (kp)

Cost of Preference

Capital

Dividend per share 0.07

Net proceeds after selling 0.68

Cost of Preference Share

Capital 10.29%

Cost of Debt (kd)

Table 11Cost of Debt (kd)

Cost of debt

Maturity Period 7

Par Value 100

Net

proceeds(Par+Premium) 105

I 11

Premium 5

Mp 7

I+(premium/Mp) 11.71

P 100

np 105

P+np/2 102.5

6

Table 10Cost of Preference Share Capital (kp)

Cost of Preference

Capital

Dividend per share 0.07

Net proceeds after selling 0.68

Cost of Preference Share

Capital 10.29%

Cost of Debt (kd)

Table 11Cost of Debt (kd)

Cost of debt

Maturity Period 7

Par Value 100

Net

proceeds(Par+Premium) 105

I 11

Premium 5

Mp 7

I+(premium/Mp) 11.71

P 100

np 105

P+np/2 102.5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

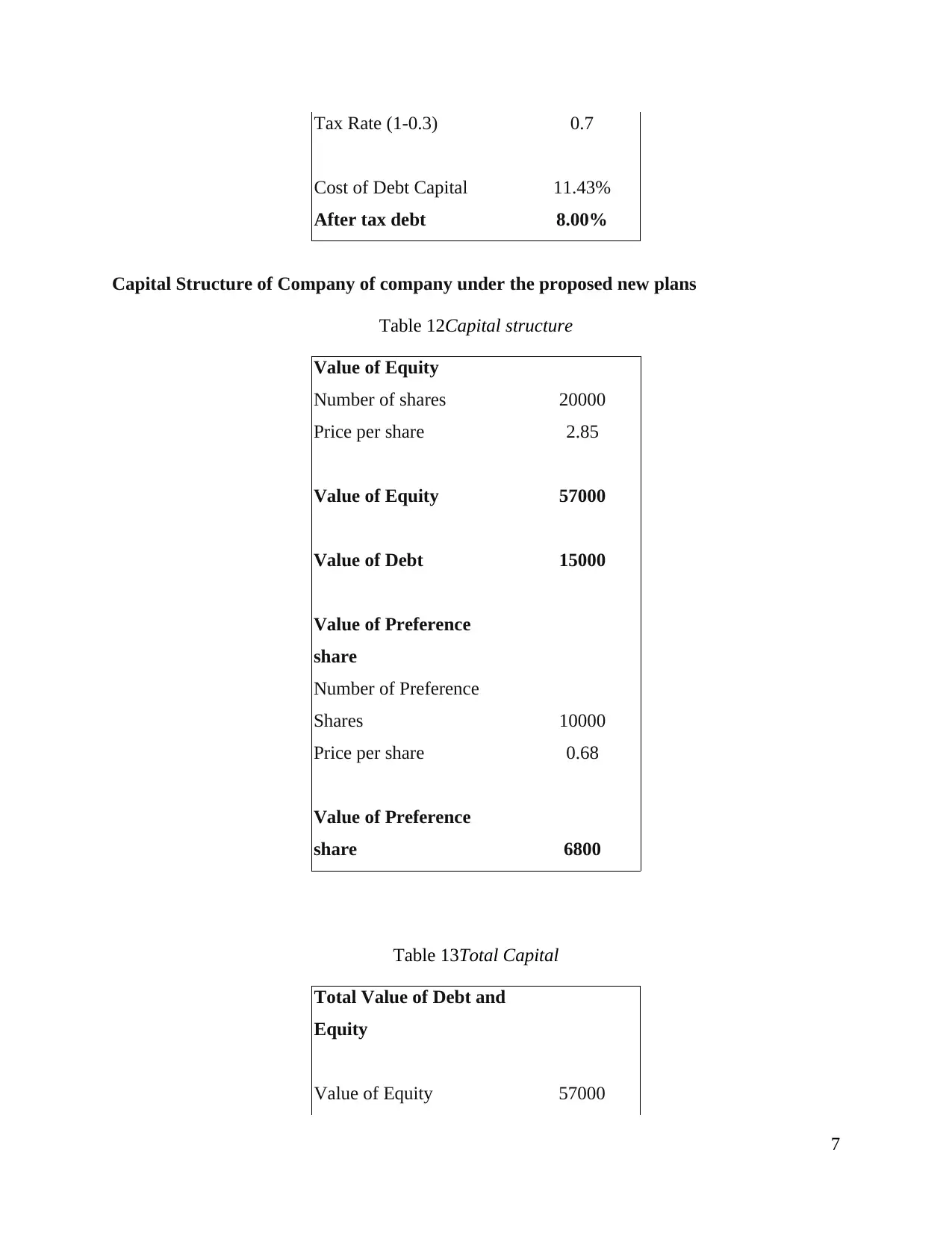

Tax Rate (1-0.3) 0.7

Cost of Debt Capital 11.43%

After tax debt 8.00%

Capital Structure of Company of company under the proposed new plans

Table 12Capital structure

Value of Equity

Number of shares 20000

Price per share 2.85

Value of Equity 57000

Value of Debt 15000

Value of Preference

share

Number of Preference

Shares 10000

Price per share 0.68

Value of Preference

share 6800

Table 13Total Capital

Total Value of Debt and

Equity

Value of Equity 57000

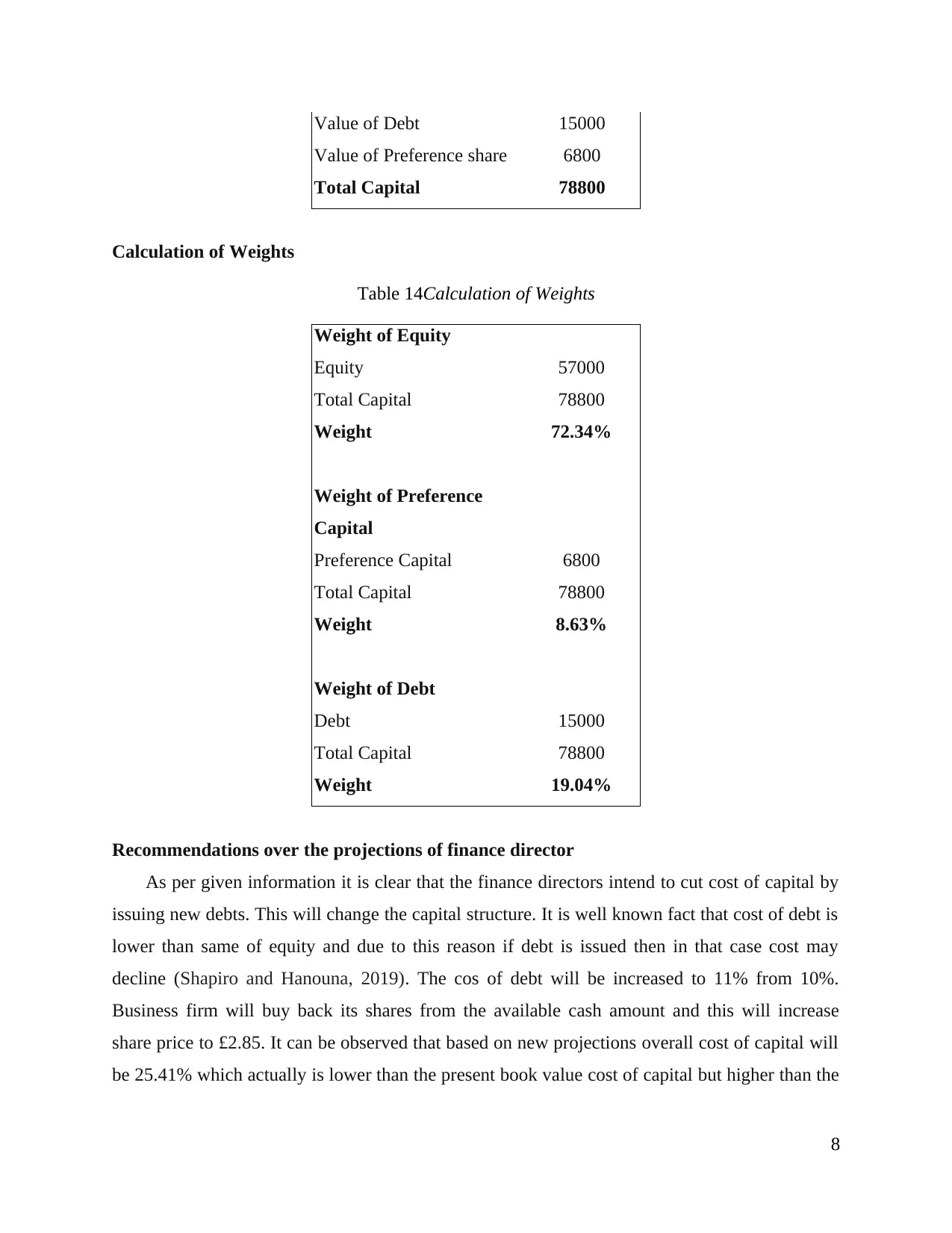

7

Cost of Debt Capital 11.43%

After tax debt 8.00%

Capital Structure of Company of company under the proposed new plans

Table 12Capital structure

Value of Equity

Number of shares 20000

Price per share 2.85

Value of Equity 57000

Value of Debt 15000

Value of Preference

share

Number of Preference

Shares 10000

Price per share 0.68

Value of Preference

share 6800

Table 13Total Capital

Total Value of Debt and

Equity

Value of Equity 57000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Value of Debt 15000

Value of Preference share 6800

Total Capital 78800

Calculation of Weights

Table 14Calculation of Weights

Weight of Equity

Equity 57000

Total Capital 78800

Weight 72.34%

Weight of Preference

Capital

Preference Capital 6800

Total Capital 78800

Weight 8.63%

Weight of Debt

Debt 15000

Total Capital 78800

Weight 19.04%

Recommendations over the projections of finance director

As per given information it is clear that the finance directors intend to cut cost of capital by

issuing new debts. This will change the capital structure. It is well known fact that cost of debt is

lower than same of equity and due to this reason if debt is issued then in that case cost may

decline (Shapiro and Hanouna, 2019). The cos of debt will be increased to 11% from 10%.

Business firm will buy back its shares from the available cash amount and this will increase

share price to £2.85. It can be observed that based on new projections overall cost of capital will

be 25.41% which actually is lower than the present book value cost of capital but higher than the

8

Value of Preference share 6800

Total Capital 78800

Calculation of Weights

Table 14Calculation of Weights

Weight of Equity

Equity 57000

Total Capital 78800

Weight 72.34%

Weight of Preference

Capital

Preference Capital 6800

Total Capital 78800

Weight 8.63%

Weight of Debt

Debt 15000

Total Capital 78800

Weight 19.04%

Recommendations over the projections of finance director

As per given information it is clear that the finance directors intend to cut cost of capital by

issuing new debts. This will change the capital structure. It is well known fact that cost of debt is

lower than same of equity and due to this reason if debt is issued then in that case cost may

decline (Shapiro and Hanouna, 2019). The cos of debt will be increased to 11% from 10%.

Business firm will buy back its shares from the available cash amount and this will increase

share price to £2.85. It can be observed that based on new projections overall cost of capital will

be 25.41% which actually is lower than the present book value cost of capital but higher than the

8

market value cost of capital. Therefore, the projections made by finance manager should be

adopted as it will increase the share value by reducing the cost of capital of company.

c) Minimising the cost of capital using gearing in the capital structure

Cost of the capital is the one of the main focal point of the most business firms. This is

because if cost of capital is high then in that case business firm have to pay more to banks and

other financial institutions. Thus, it can be said that cost of capital creates extra payment burden

on the business firm. Thus, main focus of manager always remains on reducing cost of capital in

the business. In order to reduce capital structure many business firms focus on reducing equity

and increasing debt (Finkler, Smith and Calabrese, 2018). This is known as capital restructuring.

Many times, when capital structure become imbalanced business firms restructure their capital

structure. It is well known fact that cost of debt is relatively lower then same of equity. This is

because equity shareholders are considered as real owner of the company and due to this reason

high rate is paid to them relative to interest rate on debt. Cost of debt refers to the interest that is

charged by the banks on loan amount that is taken by the firm from it. Interest paid on

debentures and corporate bond is also considered as cost of debt. Cost of debt is always lower

then cost of equity and due to this reason always it is suggested that portion of equity in the

capital structure must be low and portion of debt must be high so that cost of finance can be

controlled in the business (Renz. and Herman, 2016). However, this does not mean that firm

consistently increase bank loan or other debt instruments at fast rate in its business. This is

because many times it happened that debt burden increase in the business out of tolerable limit

and cost of debt rose sharply. Hence, firm take debt from the market only to certain level.

(d) Critically evaluate the effects of short-termism on bankruptcy and the agency problem in a

company, ensuring the response is supported with relevant academic research.

Short termism refers to the situation where firm focus on short term gain or opportunity at

the expense of the long-term opportunity of gain. Firms mainly do this when they are extremely

on pressure or competition is fierce. Many times, due to cut throat competition firms earn less

profit in their business and to ensure survival and sustainability they make efforts to earn profit

for short term. Hence, in order to earn short term profit business firm, make change in its

business operations which can be not be considered good from long term time period. If any

company is operating in mobile phone manufacturing business and face loss then it may focus on

9

adopted as it will increase the share value by reducing the cost of capital of company.

c) Minimising the cost of capital using gearing in the capital structure

Cost of the capital is the one of the main focal point of the most business firms. This is

because if cost of capital is high then in that case business firm have to pay more to banks and

other financial institutions. Thus, it can be said that cost of capital creates extra payment burden

on the business firm. Thus, main focus of manager always remains on reducing cost of capital in

the business. In order to reduce capital structure many business firms focus on reducing equity

and increasing debt (Finkler, Smith and Calabrese, 2018). This is known as capital restructuring.

Many times, when capital structure become imbalanced business firms restructure their capital

structure. It is well known fact that cost of debt is relatively lower then same of equity. This is

because equity shareholders are considered as real owner of the company and due to this reason

high rate is paid to them relative to interest rate on debt. Cost of debt refers to the interest that is

charged by the banks on loan amount that is taken by the firm from it. Interest paid on

debentures and corporate bond is also considered as cost of debt. Cost of debt is always lower

then cost of equity and due to this reason always it is suggested that portion of equity in the

capital structure must be low and portion of debt must be high so that cost of finance can be

controlled in the business (Renz. and Herman, 2016). However, this does not mean that firm

consistently increase bank loan or other debt instruments at fast rate in its business. This is

because many times it happened that debt burden increase in the business out of tolerable limit

and cost of debt rose sharply. Hence, firm take debt from the market only to certain level.

(d) Critically evaluate the effects of short-termism on bankruptcy and the agency problem in a

company, ensuring the response is supported with relevant academic research.

Short termism refers to the situation where firm focus on short term gain or opportunity at

the expense of the long-term opportunity of gain. Firms mainly do this when they are extremely

on pressure or competition is fierce. Many times, due to cut throat competition firms earn less

profit in their business and to ensure survival and sustainability they make efforts to earn profit

for short term. Hence, in order to earn short term profit business firm, make change in its

business operations which can be not be considered good from long term time period. If any

company is operating in mobile phone manufacturing business and face loss then it may focus on

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.