Financial Management Report: Dividend Policies and Appraisal

VerifiedAdded on 2023/01/10

|15

|3303

|100

Report

AI Summary

This report delves into the core concepts of financial management, specifically focusing on dividend policies and investment appraisal strategies. It examines the factors influencing dividend decisions, including the size of the annual dividend and practical considerations for listed companies. The report further analyzes Squeezeco's dividend options, including cash dividends, scrip dividends, and share repurchases, evaluating their implications. Furthermore, the report explores investment appraisal techniques such as payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR), providing calculations and interpretations. The analysis covers how companies make decisions that affect investment opportunities, offering a comprehensive overview of financial management principles and their application in real-world scenarios.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Financial management relies on the study of the ratios, equity capital. This is useful for asset

administration, earnings distribution, investment funding, seeking to protect and track the

fluctuations of foreign exchange and product cycles (Anthony, 2019). A business has to manage

the finances wisely to maximise their earnings and it is important that the finances it obtains are

invested in such a manner that the investment profits are higher than the financing costs. The

study is focused on two separate topics related to dividend policies and investment appraisal

strategies that executives use to determine best-favourable investment initiative. Such concepts

assist in making strategic investment decisions, and also what activities they must take to

maximize their share of the market.

MAIN BODY

Question 1

1. Size of the annual dividend which return to its shareholders

Dividend is really just the proportion of the company's earnings 'income under the board

members' decision and selection; it is announced and charged as a percentage of par shares or per

security (Khan, 2020). Furthermore, dividend is a proportion of the surplus that occurs after

sufficient allocation has been made for different types of services and taxation etc. after all

spending has been subtracted in total revenue. Representative have such a duty to make this

profit, however though they can not commit to its immediate selling. When the business requires

profits then the company can retain the entire share of the income even without dividend being

paid. Dividend is therefore not reported in the event that the total income is required to be in the

form of specific funds or surplus. When deciding on dividends paid, proprietors will take into

consideration the usual two things listed below:

Fair consideration:

Managers must have a fair assessment of the level with which owners expects to receive

money benefit and take risks in return. When it is not completed, it can be difficult to keep the

creditors absolutely happy and that will also have a negative effect on the market results of

goodwill shares of the group.

1

Financial management relies on the study of the ratios, equity capital. This is useful for asset

administration, earnings distribution, investment funding, seeking to protect and track the

fluctuations of foreign exchange and product cycles (Anthony, 2019). A business has to manage

the finances wisely to maximise their earnings and it is important that the finances it obtains are

invested in such a manner that the investment profits are higher than the financing costs. The

study is focused on two separate topics related to dividend policies and investment appraisal

strategies that executives use to determine best-favourable investment initiative. Such concepts

assist in making strategic investment decisions, and also what activities they must take to

maximize their share of the market.

MAIN BODY

Question 1

1. Size of the annual dividend which return to its shareholders

Dividend is really just the proportion of the company's earnings 'income under the board

members' decision and selection; it is announced and charged as a percentage of par shares or per

security (Khan, 2020). Furthermore, dividend is a proportion of the surplus that occurs after

sufficient allocation has been made for different types of services and taxation etc. after all

spending has been subtracted in total revenue. Representative have such a duty to make this

profit, however though they can not commit to its immediate selling. When the business requires

profits then the company can retain the entire share of the income even without dividend being

paid. Dividend is therefore not reported in the event that the total income is required to be in the

form of specific funds or surplus. When deciding on dividends paid, proprietors will take into

consideration the usual two things listed below:

Fair consideration:

Managers must have a fair assessment of the level with which owners expects to receive

money benefit and take risks in return. When it is not completed, it can be difficult to keep the

creditors absolutely happy and that will also have a negative effect on the market results of

goodwill shares of the group.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Company’s requirement:

Managing the ultimate financial position is executives' main responsibility, particularly

when leaders are being forced into making other concessions to do so. It is therefore incredibly

critical for the lender to be able to assess exactly how much additional capital the business

requires to prosper and develop.

Factors determined at the time making dividend decisions:

At the time of making decision in respect of dividend which going to distribute to the

shareholders; managers consider some factors which are as follow:

Nature of business: It would be only Squeezeco Company who periodically distributes

profits, and who provides dividend on monthly basis. Firms in this category have companies

producing products for everyday use (Greve and Man Zhang, 2017). Only companies that

participate in the public service shall regularly pay shareholder dividends. Industries dealing with

producing costly goods could not manage to pay dividend on a regular basis.

Life of firm: Emerging companies are therefore reluctant to pay decent dividends within

a few times to shareholders. In their early years they would require sufficient capital for growth

that they are never in a position to obtain easily through the marketplace. And they'd come back

with their very own inner financial capital. In contrast, older companies may require relatively

less capital but they collect it from the economy even though they do. Under such a case a

Medium Dividend Plan should be enforced.

Financial position: However, if the Squeezeco receives enough money to pay dividends

owing to its profit status, those who have not been able to pay cash dividends. Despite the

revenue and excess a corporation's liquid placement can worsen. For this situation, the

corporation needs to pay dividends in the form of shareholdings.

Financial requirement: The dividend payout plan also affects financial goals of the

Squeezeco. When a specific development program happens before the company, instead such a

organization would need to follow a strict dividend policy so that new money can be efficiently

handled by limited access. In this circumstances, greater emphasis should be given to the re-

appropriation of income.

2

Managing the ultimate financial position is executives' main responsibility, particularly

when leaders are being forced into making other concessions to do so. It is therefore incredibly

critical for the lender to be able to assess exactly how much additional capital the business

requires to prosper and develop.

Factors determined at the time making dividend decisions:

At the time of making decision in respect of dividend which going to distribute to the

shareholders; managers consider some factors which are as follow:

Nature of business: It would be only Squeezeco Company who periodically distributes

profits, and who provides dividend on monthly basis. Firms in this category have companies

producing products for everyday use (Greve and Man Zhang, 2017). Only companies that

participate in the public service shall regularly pay shareholder dividends. Industries dealing with

producing costly goods could not manage to pay dividend on a regular basis.

Life of firm: Emerging companies are therefore reluctant to pay decent dividends within

a few times to shareholders. In their early years they would require sufficient capital for growth

that they are never in a position to obtain easily through the marketplace. And they'd come back

with their very own inner financial capital. In contrast, older companies may require relatively

less capital but they collect it from the economy even though they do. Under such a case a

Medium Dividend Plan should be enforced.

Financial position: However, if the Squeezeco receives enough money to pay dividends

owing to its profit status, those who have not been able to pay cash dividends. Despite the

revenue and excess a corporation's liquid placement can worsen. For this situation, the

corporation needs to pay dividends in the form of shareholdings.

Financial requirement: The dividend payout plan also affects financial goals of the

Squeezeco. When a specific development program happens before the company, instead such a

organization would need to follow a strict dividend policy so that new money can be efficiently

handled by limited access. In this circumstances, greater emphasis should be given to the re-

appropriation of income.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Practical issues that need to consider at the time of deciding size of dividend payment

When determining the volume of the dividend to also be charged by providing ranking to

its owners, the board members must provide it. They face multiple challenges that are addressed

below:

Investor selection: The biggest thing is the choice of shareholders, as they have different

tastes and feelings. Creditors also don't care about profits; they just need to retain the

organization where they earned compensation in order to develop new operations or expand

existing business. Since this innovation reduces the expense of the offer even though it rises the

market price of the bid’s supply that would benefit the customers at the stage of selling.

Various alternative solutions: There have been two schemes that the members of

businesses must pursue to produce gains like cash revenue and benefit divide. The main

challenge for the company is choosing that choice to satisfy investors by meeting their profit and

capital gain preferences

Investor's desire: It is difficult for a business to assess customer preferences for profit

esteem. If the firm does not focus on growth, consumers may plan to pay more than anticipated,

and expect the offer to decrease later.

Guidelines Act: The legal regime has decided to a set of corporate guidelines wherein the

organization would have to invest what it could spend. It enables the managers to maintain a

certain amount of profits for income, for example. If the business produced a 15 per cent profit, it

will in any case retain 7.5 per cent of the profits.

3. Calculate the three options

Cash dividend:

It indicates that dividend which would be paid in cash or in bank account to the investors.

If a business will have no funds to pay dividends even though they pays dividends in terms of

bonds or they could say the proprietor to given additional stock of the business (Hashim and

Piatti-Fünfkirchen, 2018). The term is called a dividend on property.

3

When determining the volume of the dividend to also be charged by providing ranking to

its owners, the board members must provide it. They face multiple challenges that are addressed

below:

Investor selection: The biggest thing is the choice of shareholders, as they have different

tastes and feelings. Creditors also don't care about profits; they just need to retain the

organization where they earned compensation in order to develop new operations or expand

existing business. Since this innovation reduces the expense of the offer even though it rises the

market price of the bid’s supply that would benefit the customers at the stage of selling.

Various alternative solutions: There have been two schemes that the members of

businesses must pursue to produce gains like cash revenue and benefit divide. The main

challenge for the company is choosing that choice to satisfy investors by meeting their profit and

capital gain preferences

Investor's desire: It is difficult for a business to assess customer preferences for profit

esteem. If the firm does not focus on growth, consumers may plan to pay more than anticipated,

and expect the offer to decrease later.

Guidelines Act: The legal regime has decided to a set of corporate guidelines wherein the

organization would have to invest what it could spend. It enables the managers to maintain a

certain amount of profits for income, for example. If the business produced a 15 per cent profit, it

will in any case retain 7.5 per cent of the profits.

3. Calculate the three options

Cash dividend:

It indicates that dividend which would be paid in cash or in bank account to the investors.

If a business will have no funds to pay dividends even though they pays dividends in terms of

bonds or they could say the proprietor to given additional stock of the business (Hashim and

Piatti-Fünfkirchen, 2018). The term is called a dividend on property.

3

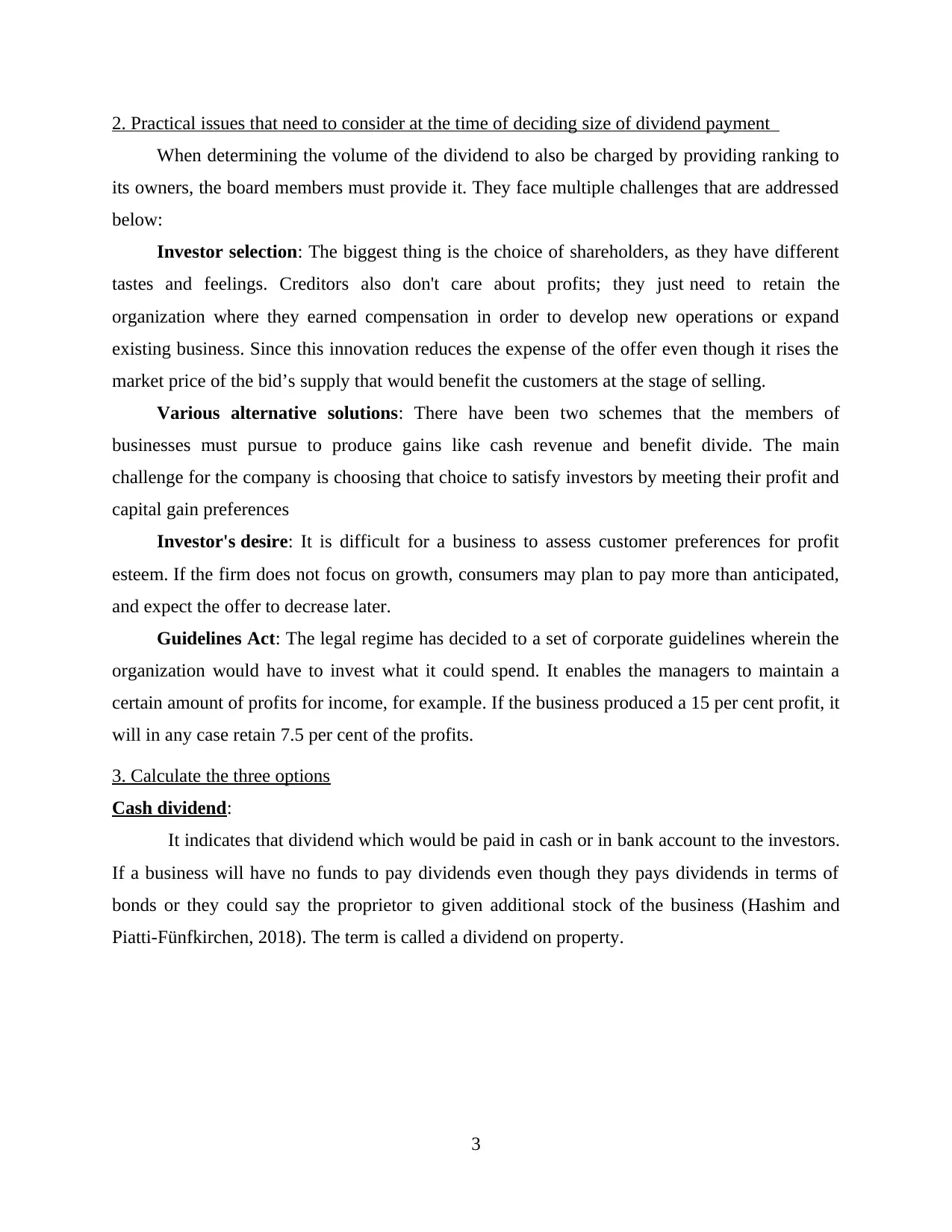

Interpretation: Abovementioned table shows that a minimum of 1250 shares

outstanding are required to support revenue; the reward money is the option made to generate

profits. This is why the full capital gain is £ 187.5 per client, at 15 pesa.

5% Script dividend:

The corporate entity is actually selling shares of the predetermined company to existing

shareholders rather than charging cash dividends for shareholders. This allows investors to

access the system and purchase extra shares without the normally paid purchasing costs when

those financial instruments were acquired on the market. Cash funds are the primary justification

for scrip dividends being paid by the firm, as it is a beneficial tactic for a firm. Equation of the

minimum dividend referred to in table below:

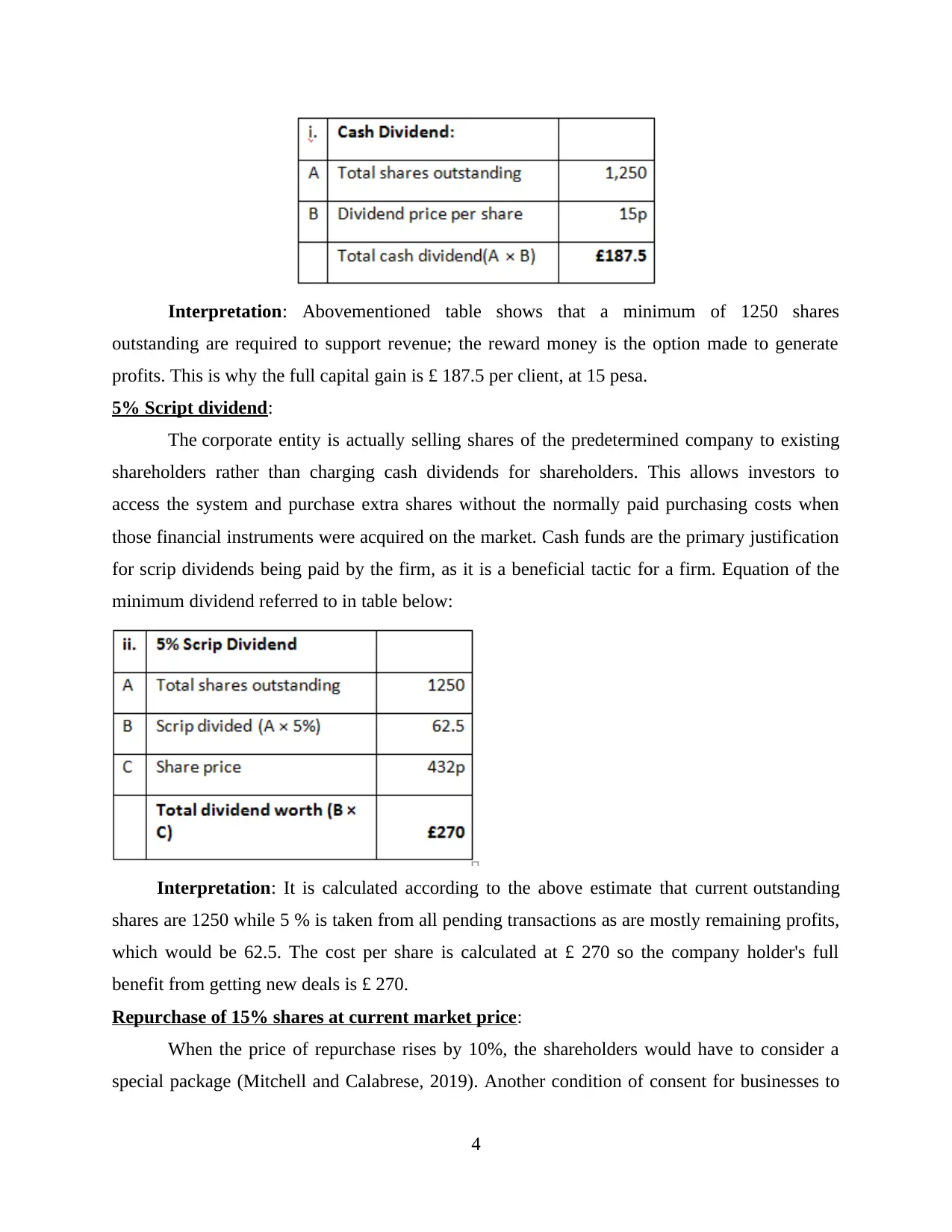

Interpretation: It is calculated according to the above estimate that current outstanding

shares are 1250 while 5 % is taken from all pending transactions as are mostly remaining profits,

which would be 62.5. The cost per share is calculated at £ 270 so the company holder's full

benefit from getting new deals is £ 270.

Repurchase of 15% shares at current market price:

When the price of repurchase rises by 10%, the shareholders would have to consider a

special package (Mitchell and Calabrese, 2019). Another condition of consent for businesses to

4

outstanding are required to support revenue; the reward money is the option made to generate

profits. This is why the full capital gain is £ 187.5 per client, at 15 pesa.

5% Script dividend:

The corporate entity is actually selling shares of the predetermined company to existing

shareholders rather than charging cash dividends for shareholders. This allows investors to

access the system and purchase extra shares without the normally paid purchasing costs when

those financial instruments were acquired on the market. Cash funds are the primary justification

for scrip dividends being paid by the firm, as it is a beneficial tactic for a firm. Equation of the

minimum dividend referred to in table below:

Interpretation: It is calculated according to the above estimate that current outstanding

shares are 1250 while 5 % is taken from all pending transactions as are mostly remaining profits,

which would be 62.5. The cost per share is calculated at £ 270 so the company holder's full

benefit from getting new deals is £ 270.

Repurchase of 15% shares at current market price:

When the price of repurchase rises by 10%, the shareholders would have to consider a

special package (Mitchell and Calabrese, 2019). Another condition of consent for businesses to

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

purchase back securities would be that the sum of the total debt, both secured and unregulated,

must not be upwards of double the sum of paid-up capital and unused assets for the organization

after the stock redemption. This can only be achieved if a greater average debt-equity ratio is set

out in the corporate law.

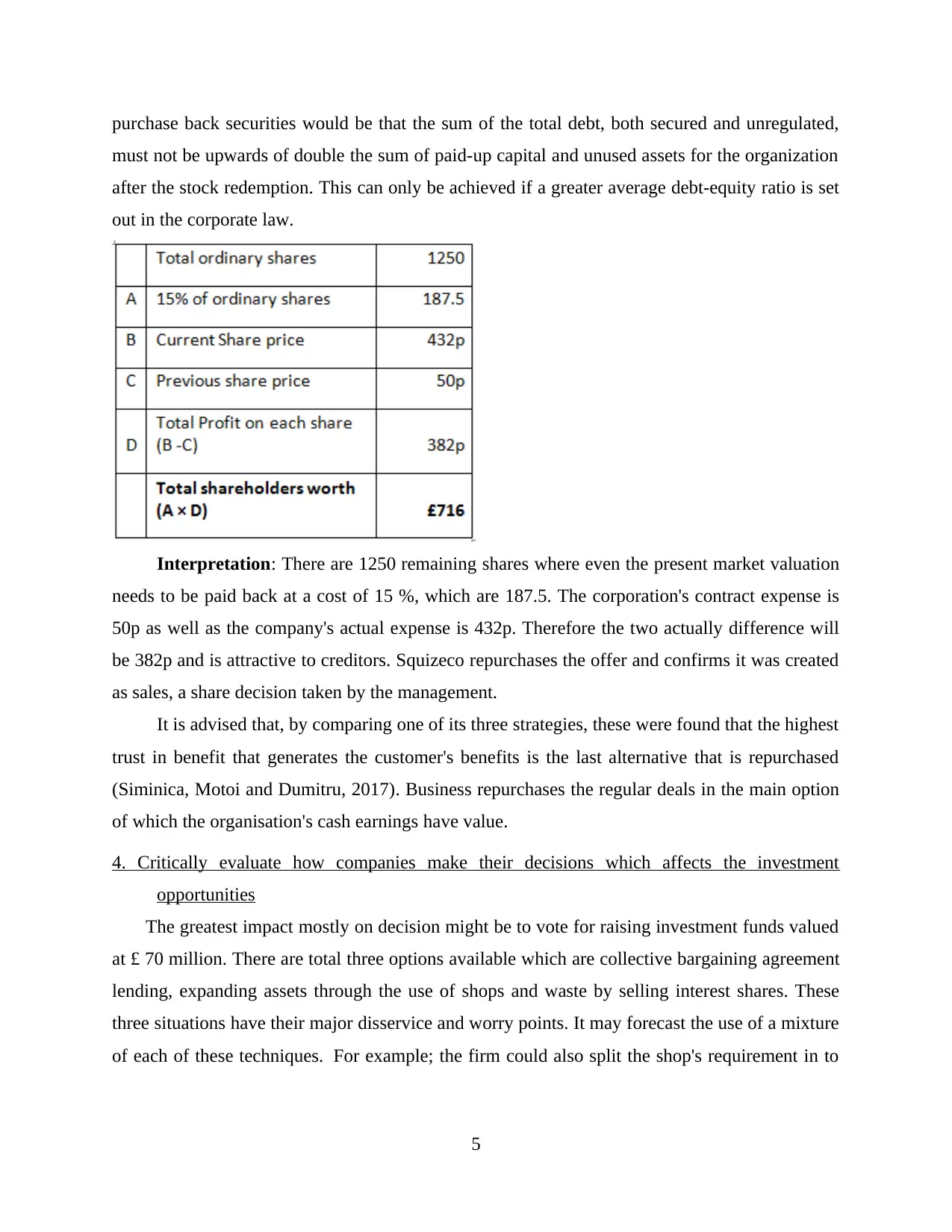

Interpretation: There are 1250 remaining shares where even the present market valuation

needs to be paid back at a cost of 15 %, which are 187.5. The corporation's contract expense is

50p as well as the company's actual expense is 432p. Therefore the two actually difference will

be 382p and is attractive to creditors. Squizeco repurchases the offer and confirms it was created

as sales, a share decision taken by the management.

It is advised that, by comparing one of its three strategies, these were found that the highest

trust in benefit that generates the customer's benefits is the last alternative that is repurchased

(Siminica, Motoi and Dumitru, 2017). Business repurchases the regular deals in the main option

of which the organisation's cash earnings have value.

4. Critically evaluate how companies make their decisions which affects the investment

opportunities

The greatest impact mostly on decision might be to vote for raising investment funds valued

at £ 70 million. There are total three options available which are collective bargaining agreement

lending, expanding assets through the use of shops and waste by selling interest shares. These

three situations have their major disservice and worry points. It may forecast the use of a mixture

of each of these techniques. For example; the firm could also split the shop's requirement in to

5

must not be upwards of double the sum of paid-up capital and unused assets for the organization

after the stock redemption. This can only be achieved if a greater average debt-equity ratio is set

out in the corporate law.

Interpretation: There are 1250 remaining shares where even the present market valuation

needs to be paid back at a cost of 15 %, which are 187.5. The corporation's contract expense is

50p as well as the company's actual expense is 432p. Therefore the two actually difference will

be 382p and is attractive to creditors. Squizeco repurchases the offer and confirms it was created

as sales, a share decision taken by the management.

It is advised that, by comparing one of its three strategies, these were found that the highest

trust in benefit that generates the customer's benefits is the last alternative that is repurchased

(Siminica, Motoi and Dumitru, 2017). Business repurchases the regular deals in the main option

of which the organisation's cash earnings have value.

4. Critically evaluate how companies make their decisions which affects the investment

opportunities

The greatest impact mostly on decision might be to vote for raising investment funds valued

at £ 70 million. There are total three options available which are collective bargaining agreement

lending, expanding assets through the use of shops and waste by selling interest shares. These

three situations have their major disservice and worry points. It may forecast the use of a mixture

of each of these techniques. For example; the firm could also split the shop's requirement in to

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

other three amounts, e.g. 30 % by duty, 60 % by interest issue and 10 % by store holding. When

a sales problem can arise, the organization has 3 options such as:

Right issuing of financial instruments to current shareholders.

Grant preferred stock with fixed interest rate of dividend payout.

Trading common shares at a lower price.

Question 3

1. Calculate the following investment appraisal techniques

Payback period: This is among the most accessible source of capital budgeting that lets

companies determine their investment turnaround time (Setiawan And et.al., 2016). Business

benefits from short payback time that required original investments to be recovered as well as

their returns to improve. Executives of the company's financial plan must agree on future

acquisitions together. It is really important to quantify the overall project risk of the businesses as

managers prefer the project which carries less danger than other programs. Moreover, because

executives have several choices, lower recovery time is appropriate or higher one is denied, and

they can make investments appropriately.

Payback period = Initial Investment / Cash Inflow

= £ 275,000 / £ 85,000

= 3.79 years

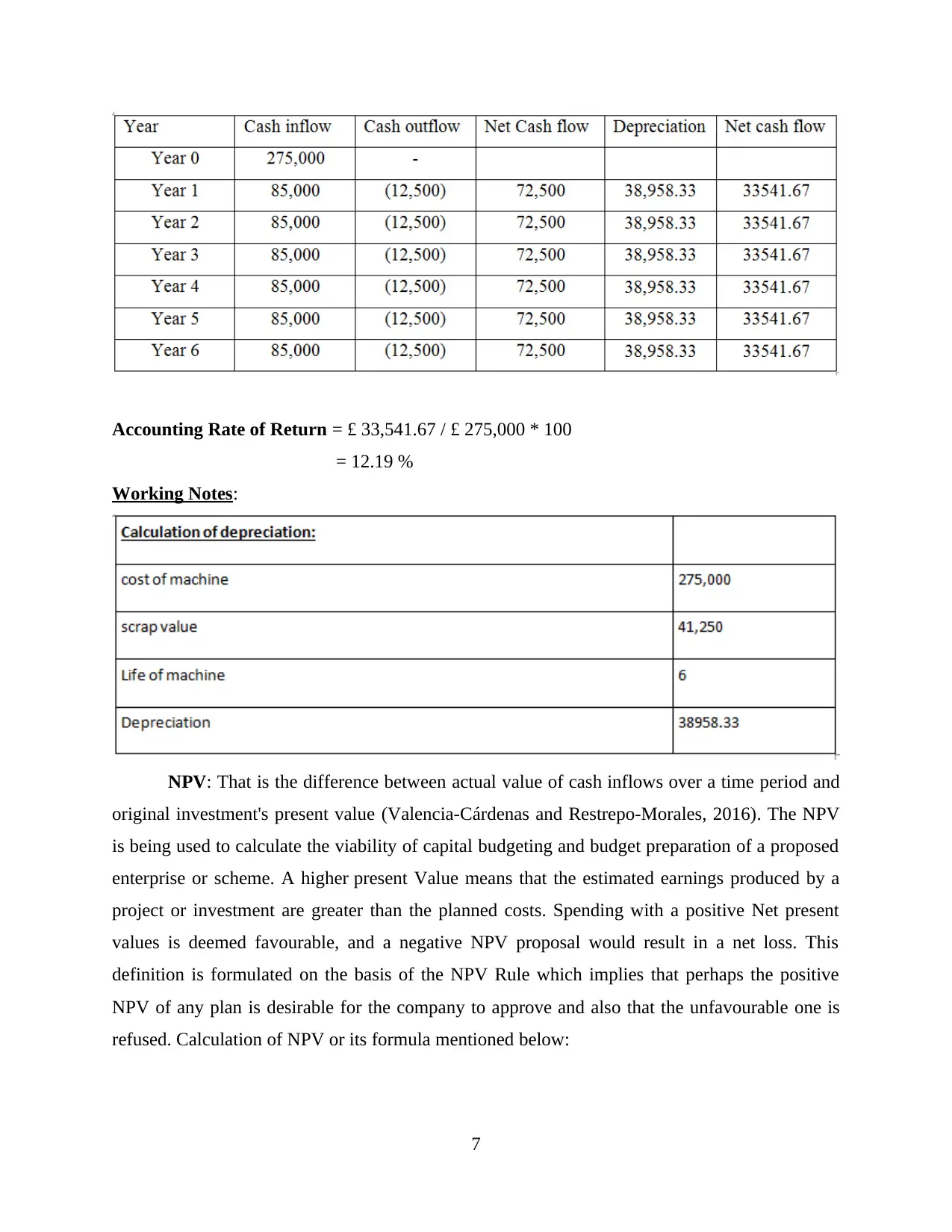

ARR: ARR also estimated the expected return probability for the acquisition or the

selling of the company in actual numbers. That's one of the easiest or fastest forms of investment

evaluation commonly used in planning process. The incremental profits are derived from original

investment. ARR is the method of capital budgeting and does not take into account all the cash

flows. The higher the yield on customer earnings is advantageous, the lesser the ARR on the

other side is no more competitive. Constantly strengthened results on various projects and

making proper management decisions. Supervisors at the corporation assess their decisions and

determine whether it should select this proposal for additional expenditure. The projection is

estimated below for 6 year and its calculation along with formula mentioned below:

6

a sales problem can arise, the organization has 3 options such as:

Right issuing of financial instruments to current shareholders.

Grant preferred stock with fixed interest rate of dividend payout.

Trading common shares at a lower price.

Question 3

1. Calculate the following investment appraisal techniques

Payback period: This is among the most accessible source of capital budgeting that lets

companies determine their investment turnaround time (Setiawan And et.al., 2016). Business

benefits from short payback time that required original investments to be recovered as well as

their returns to improve. Executives of the company's financial plan must agree on future

acquisitions together. It is really important to quantify the overall project risk of the businesses as

managers prefer the project which carries less danger than other programs. Moreover, because

executives have several choices, lower recovery time is appropriate or higher one is denied, and

they can make investments appropriately.

Payback period = Initial Investment / Cash Inflow

= £ 275,000 / £ 85,000

= 3.79 years

ARR: ARR also estimated the expected return probability for the acquisition or the

selling of the company in actual numbers. That's one of the easiest or fastest forms of investment

evaluation commonly used in planning process. The incremental profits are derived from original

investment. ARR is the method of capital budgeting and does not take into account all the cash

flows. The higher the yield on customer earnings is advantageous, the lesser the ARR on the

other side is no more competitive. Constantly strengthened results on various projects and

making proper management decisions. Supervisors at the corporation assess their decisions and

determine whether it should select this proposal for additional expenditure. The projection is

estimated below for 6 year and its calculation along with formula mentioned below:

6

Accounting Rate of Return = £ 33,541.67 / £ 275,000 * 100

= 12.19 %

Working Notes:

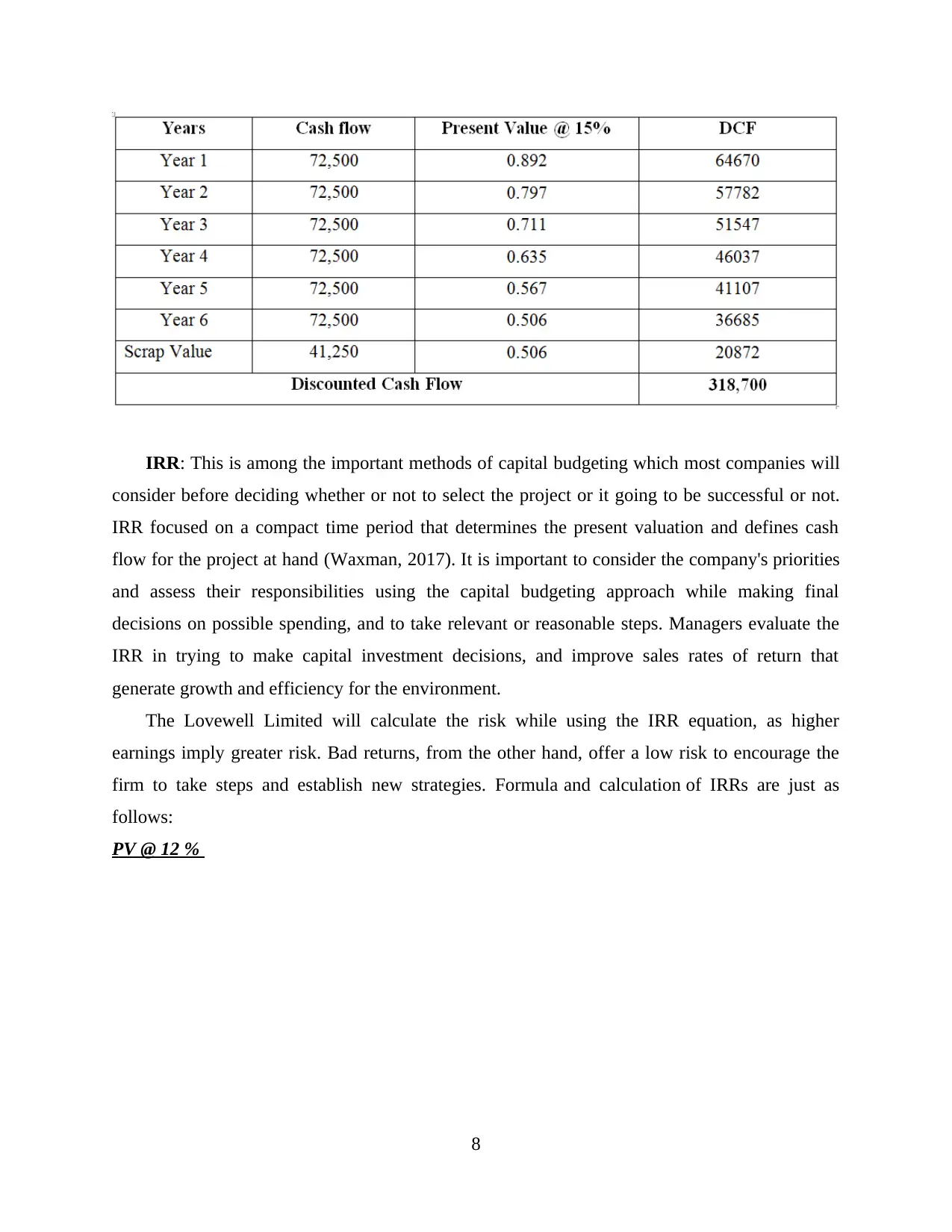

NPV: That is the difference between actual value of cash inflows over a time period and

original investment's present value (Valencia-Cárdenas and Restrepo-Morales, 2016). The NPV

is being used to calculate the viability of capital budgeting and budget preparation of a proposed

enterprise or scheme. A higher present Value means that the estimated earnings produced by a

project or investment are greater than the planned costs. Spending with a positive Net present

values is deemed favourable, and a negative NPV proposal would result in a net loss. This

definition is formulated on the basis of the NPV Rule which implies that perhaps the positive

NPV of any plan is desirable for the company to approve and also that the unfavourable one is

refused. Calculation of NPV or its formula mentioned below:

7

= 12.19 %

Working Notes:

NPV: That is the difference between actual value of cash inflows over a time period and

original investment's present value (Valencia-Cárdenas and Restrepo-Morales, 2016). The NPV

is being used to calculate the viability of capital budgeting and budget preparation of a proposed

enterprise or scheme. A higher present Value means that the estimated earnings produced by a

project or investment are greater than the planned costs. Spending with a positive Net present

values is deemed favourable, and a negative NPV proposal would result in a net loss. This

definition is formulated on the basis of the NPV Rule which implies that perhaps the positive

NPV of any plan is desirable for the company to approve and also that the unfavourable one is

refused. Calculation of NPV or its formula mentioned below:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

IRR: This is among the important methods of capital budgeting which most companies will

consider before deciding whether or not to select the project or it going to be successful or not.

IRR focused on a compact time period that determines the present valuation and defines cash

flow for the project at hand (Waxman, 2017). It is important to consider the company's priorities

and assess their responsibilities using the capital budgeting approach while making final

decisions on possible spending, and to take relevant or reasonable steps. Managers evaluate the

IRR in trying to make capital investment decisions, and improve sales rates of return that

generate growth and efficiency for the environment.

The Lovewell Limited will calculate the risk while using the IRR equation, as higher

earnings imply greater risk. Bad returns, from the other hand, offer a low risk to encourage the

firm to take steps and establish new strategies. Formula and calculation of IRRs are just as

follows:

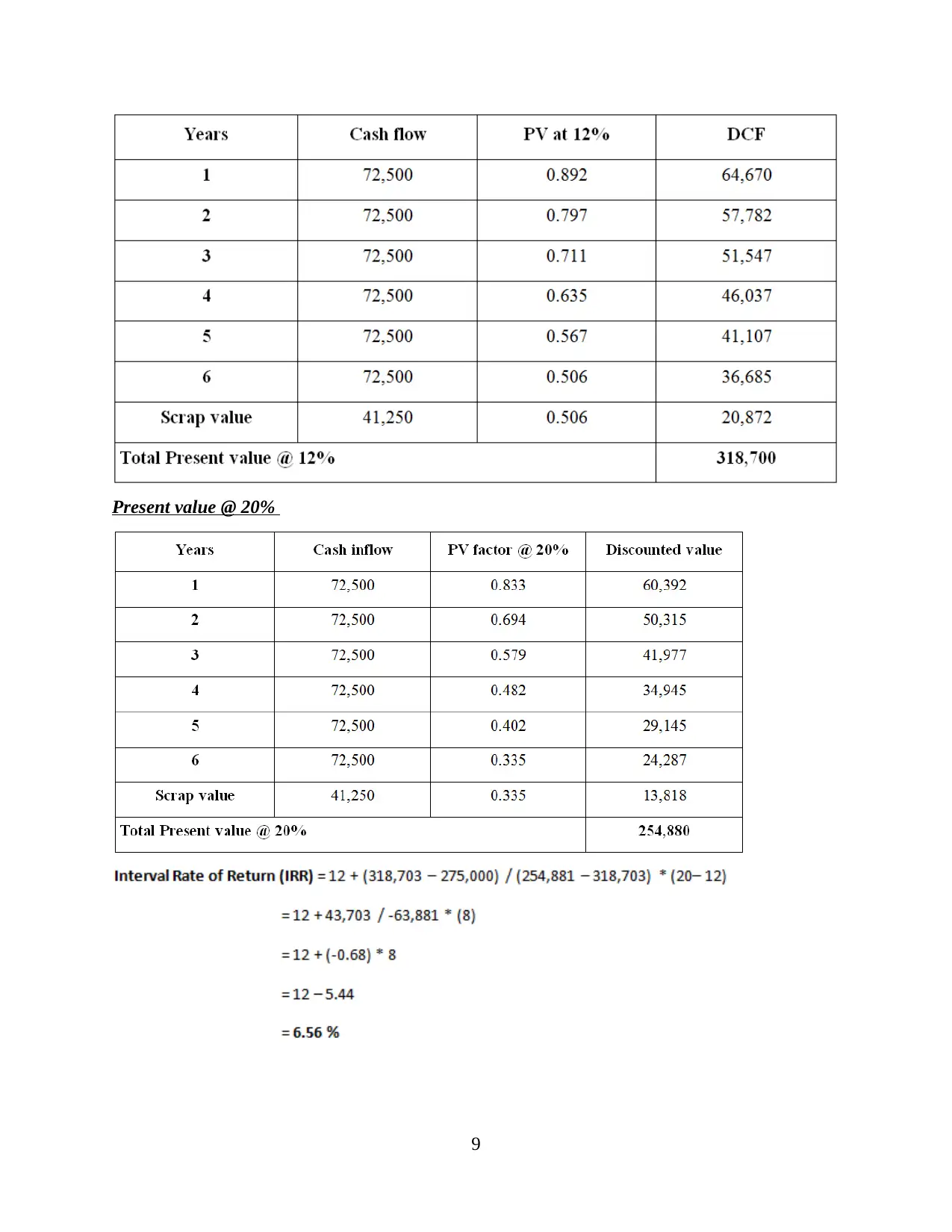

PV @ 12 %

8

consider before deciding whether or not to select the project or it going to be successful or not.

IRR focused on a compact time period that determines the present valuation and defines cash

flow for the project at hand (Waxman, 2017). It is important to consider the company's priorities

and assess their responsibilities using the capital budgeting approach while making final

decisions on possible spending, and to take relevant or reasonable steps. Managers evaluate the

IRR in trying to make capital investment decisions, and improve sales rates of return that

generate growth and efficiency for the environment.

The Lovewell Limited will calculate the risk while using the IRR equation, as higher

earnings imply greater risk. Bad returns, from the other hand, offer a low risk to encourage the

firm to take steps and establish new strategies. Formula and calculation of IRRs are just as

follows:

PV @ 12 %

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Present value @ 20%

9

9

Recoimmendation: From the overall evaluation, it has been observed that Lovewell

copmpany should adopt this project because it is quite beneficial for organbization to invest in it.

Net present value of this project is 43700 which is positive as well as profitable to invest, on the

other side, recovery period is also low that is around 4 years. IRR of this project is 6.56 % and

ARR is 12.19 % which are also in favoure in the organization. Managers should invest in this

project because it is priofitable as well as beneficial which helps in maximisng company’s retun

and overall earnings.

2. Critically evaluate the benefits and limitations of each investment appraisal techniques

Payback period:

Benefits: Payback period is great benefit to a company's owner and does not need to

make more complicated calculations trying to take account of such considerations like

product costs and advertisement impacts. The decision about whether or not to pick a

proposal is one of the most important decisions that can be done entirely by

implementing this technique of capital budgeting. With the help of this method, managers

can pick the right portfolio distribution. This would encourage accelerated reaction, as it

would make the business to regain the original price in a minimum of time.

Limitations: Among the most important drawbacks of the payback period approach is

that it wasn't measured by time value. During the project initiation years, the cash flow is

given greater value than in later life. The very same payback period extends to two

businesses (Moortgat, Annaert and Deloof, 2017). Nevertheless, one spends more money

during the first three years to generate more cash flow. The second investment offers

additional cash returns in later years. This example does not specify which organization

they choose to repay for. Managers can stop uncomfortable NPVs, as often make big

choices that do no harm. The strategy does not recognize money investments and will

depend on an average duration, as each spending would have had the same cash flow as

some other choices.

Accounting rate of return (ARR):

Benefits: ARR offers businesses the chance to make high investments. Powerful

revenues are safe and productive for the firm. The management reviews the plan for an

ARR by choosing the correct one before taking final decisions. This approach recognizes

10

copmpany should adopt this project because it is quite beneficial for organbization to invest in it.

Net present value of this project is 43700 which is positive as well as profitable to invest, on the

other side, recovery period is also low that is around 4 years. IRR of this project is 6.56 % and

ARR is 12.19 % which are also in favoure in the organization. Managers should invest in this

project because it is priofitable as well as beneficial which helps in maximisng company’s retun

and overall earnings.

2. Critically evaluate the benefits and limitations of each investment appraisal techniques

Payback period:

Benefits: Payback period is great benefit to a company's owner and does not need to

make more complicated calculations trying to take account of such considerations like

product costs and advertisement impacts. The decision about whether or not to pick a

proposal is one of the most important decisions that can be done entirely by

implementing this technique of capital budgeting. With the help of this method, managers

can pick the right portfolio distribution. This would encourage accelerated reaction, as it

would make the business to regain the original price in a minimum of time.

Limitations: Among the most important drawbacks of the payback period approach is

that it wasn't measured by time value. During the project initiation years, the cash flow is

given greater value than in later life. The very same payback period extends to two

businesses (Moortgat, Annaert and Deloof, 2017). Nevertheless, one spends more money

during the first three years to generate more cash flow. The second investment offers

additional cash returns in later years. This example does not specify which organization

they choose to repay for. Managers can stop uncomfortable NPVs, as often make big

choices that do no harm. The strategy does not recognize money investments and will

depend on an average duration, as each spending would have had the same cash flow as

some other choices.

Accounting rate of return (ARR):

Benefits: ARR offers businesses the chance to make high investments. Powerful

revenues are safe and productive for the firm. The management reviews the plan for an

ARR by choosing the correct one before taking final decisions. This approach recognizes

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.