Financial Management: Investment Appraisal and Company Valuation

VerifiedAdded on 2023/01/09

|17

|4000

|45

Report

AI Summary

This report delves into financial management, analyzing mergers and acquisitions alongside investment appraisal techniques. It examines the valuation of Trojan plc, considering price-earnings ratios, dividend valuation models, and discounted cash flow methods, while also discussing the associated drawbacks of each. Additionally, the report evaluates Love-well plc's potential machinery purchase, applying payback period and accounting rate of return methods to determine investment viability. The report provides recommendations based on these analyses, offering insights into financial decision-making processes.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.....................................................................................................................................3

MAIN BODY.............................................................................................................................................3

Question 2 – Mergers and Takeovers......................................................................................................3

Question 3: Investment appraisal techniques...........................................................................................8

CONCLUSION........................................................................................................................................15

REFERENCES........................................................................................................................................16

INTRODUCTION.....................................................................................................................................3

MAIN BODY.............................................................................................................................................3

Question 2 – Mergers and Takeovers......................................................................................................3

Question 3: Investment appraisal techniques...........................................................................................8

CONCLUSION........................................................................................................................................15

REFERENCES........................................................................................................................................16

INTRODUCTION

In general, the financial management can be understood as a form of function which is

connected to effectively management of financial aspect of a company (Chandra, 2020). Under

financial management various kinds of activities are managed such as profitability, return, cost

and many more. This is the duty of financial managers to make effective use of all available

financial resources by making appropriate allocation. The objective of this project report is to

understand about different kinds of financial terms as valuation of companies for acquisition,

analysis of projects under investment appraisal methods. The report contains two questions

which are based on theoretical and practical application of merger & acquisition as well as on

different investment appraisal techniques.

MAIN BODY

In the project brief, there are three questions and out of these two questions have been selected

which are question two and three. Underneath, detailed solution of these questions has been done

in such manner:

Question 2 – Mergers and Takeovers

Overview: This question is based on valuation of company with an aim of acquiring. As per the

given information, it can be find out that Aztec plc is going to take over Trojan plc in upcoming

time period. For this purpose, detailed valuation of Trojan plc has been done so that managing

director of Aztec plc can determine that whether they should acquire or not this company.

(a) Price earnings ratio- Share price / Earnings per share

In order find out value of price earnings ratio, there should be availability of information

about share price and earnings per share. In accordance of brief, following information

are available such as:

Price of each share £2.05

Number of share outstanding 147 Million

Net income £40.4 Million

In general, the financial management can be understood as a form of function which is

connected to effectively management of financial aspect of a company (Chandra, 2020). Under

financial management various kinds of activities are managed such as profitability, return, cost

and many more. This is the duty of financial managers to make effective use of all available

financial resources by making appropriate allocation. The objective of this project report is to

understand about different kinds of financial terms as valuation of companies for acquisition,

analysis of projects under investment appraisal methods. The report contains two questions

which are based on theoretical and practical application of merger & acquisition as well as on

different investment appraisal techniques.

MAIN BODY

In the project brief, there are three questions and out of these two questions have been selected

which are question two and three. Underneath, detailed solution of these questions has been done

in such manner:

Question 2 – Mergers and Takeovers

Overview: This question is based on valuation of company with an aim of acquiring. As per the

given information, it can be find out that Aztec plc is going to take over Trojan plc in upcoming

time period. For this purpose, detailed valuation of Trojan plc has been done so that managing

director of Aztec plc can determine that whether they should acquire or not this company.

(a) Price earnings ratio- Share price / Earnings per share

In order find out value of price earnings ratio, there should be availability of information

about share price and earnings per share. In accordance of brief, following information

are available such as:

Price of each share £2.05

Number of share outstanding 147 Million

Net income £40.4 Million

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Computation of value of earnings per share:

EPS= Net income / Number of share outstanding

= £40.4 Million / 147 Million

= £0.27

From above part, value of both EPS and share price have been found, therefore price

earnings ratio will be as:

Price earnings ratio= £2.05 / £0.27

= 7.59

Interpretation: As per the above calculated value of price earnings ratio this can be find

out that Trojan plc is generating effective earnings from each share. Their earnings on

each share is around 0.27 pounds while value of each share is 2.05 pounds. Therefore,

price earnings ratio at 7.59 seems good to acquire Trojan plc by Aztec plc.

(b) Dividend valuation model:

Under this method, valuation is done in accordance of paid dividend during financial

year. There is a formula to apply this model that is as follows:

D1 / (1 + k) + D2 / (1 + k) 2 + D3 / (1 + k) 3 + D4 / (1 + k) 4………….

In this formula:

D1 refers to amount of dividend paid in 1st year.

D2 refers to amount of dividend paid in 2nd year.

D3 refers to amount of dividend paid in 3rd year.

D4 refers to amount of dividend paid in 4th year.

K refers to predicted rate of return

EPS= Net income / Number of share outstanding

= £40.4 Million / 147 Million

= £0.27

From above part, value of both EPS and share price have been found, therefore price

earnings ratio will be as:

Price earnings ratio= £2.05 / £0.27

= 7.59

Interpretation: As per the above calculated value of price earnings ratio this can be find

out that Trojan plc is generating effective earnings from each share. Their earnings on

each share is around 0.27 pounds while value of each share is 2.05 pounds. Therefore,

price earnings ratio at 7.59 seems good to acquire Trojan plc by Aztec plc.

(b) Dividend valuation model:

Under this method, valuation is done in accordance of paid dividend during financial

year. There is a formula to apply this model that is as follows:

D1 / (1 + k) + D2 / (1 + k) 2 + D3 / (1 + k) 3 + D4 / (1 + k) 4………….

In this formula:

D1 refers to amount of dividend paid in 1st year.

D2 refers to amount of dividend paid in 2nd year.

D3 refers to amount of dividend paid in 3rd year.

D4 refers to amount of dividend paid in 4th year.

K refers to predicted rate of return

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

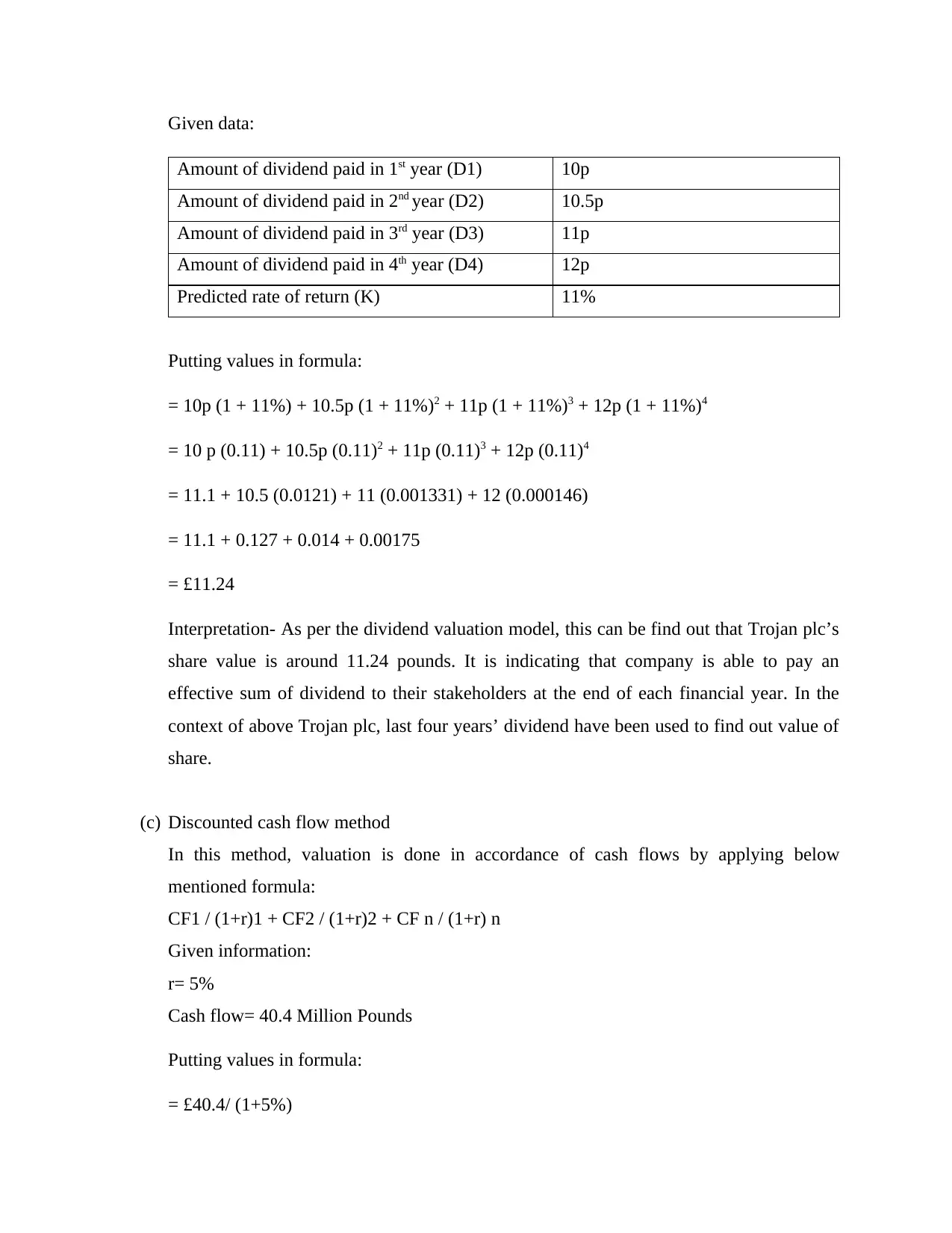

Given data:

Amount of dividend paid in 1st year (D1) 10p

Amount of dividend paid in 2nd year (D2) 10.5p

Amount of dividend paid in 3rd year (D3) 11p

Amount of dividend paid in 4th year (D4) 12p

Predicted rate of return (K) 11%

Putting values in formula:

= 10p (1 + 11%) + 10.5p (1 + 11%)2 + 11p (1 + 11%)3 + 12p (1 + 11%)4

= 10 p (0.11) + 10.5p (0.11)2 + 11p (0.11)3 + 12p (0.11)4

= 11.1 + 10.5 (0.0121) + 11 (0.001331) + 12 (0.000146)

= 11.1 + 0.127 + 0.014 + 0.00175

= £11.24

Interpretation- As per the dividend valuation model, this can be find out that Trojan plc’s

share value is around 11.24 pounds. It is indicating that company is able to pay an

effective sum of dividend to their stakeholders at the end of each financial year. In the

context of above Trojan plc, last four years’ dividend have been used to find out value of

share.

(c) Discounted cash flow method

In this method, valuation is done in accordance of cash flows by applying below

mentioned formula:

CF1 / (1+r)1 + CF2 / (1+r)2 + CF n / (1+r) n

Given information:

r= 5%

Cash flow= 40.4 Million Pounds

Putting values in formula:

= £40.4/ (1+5%)

Amount of dividend paid in 1st year (D1) 10p

Amount of dividend paid in 2nd year (D2) 10.5p

Amount of dividend paid in 3rd year (D3) 11p

Amount of dividend paid in 4th year (D4) 12p

Predicted rate of return (K) 11%

Putting values in formula:

= 10p (1 + 11%) + 10.5p (1 + 11%)2 + 11p (1 + 11%)3 + 12p (1 + 11%)4

= 10 p (0.11) + 10.5p (0.11)2 + 11p (0.11)3 + 12p (0.11)4

= 11.1 + 10.5 (0.0121) + 11 (0.001331) + 12 (0.000146)

= 11.1 + 0.127 + 0.014 + 0.00175

= £11.24

Interpretation- As per the dividend valuation model, this can be find out that Trojan plc’s

share value is around 11.24 pounds. It is indicating that company is able to pay an

effective sum of dividend to their stakeholders at the end of each financial year. In the

context of above Trojan plc, last four years’ dividend have been used to find out value of

share.

(c) Discounted cash flow method

In this method, valuation is done in accordance of cash flows by applying below

mentioned formula:

CF1 / (1+r)1 + CF2 / (1+r)2 + CF n / (1+r) n

Given information:

r= 5%

Cash flow= 40.4 Million Pounds

Putting values in formula:

= £40.4/ (1+5%)

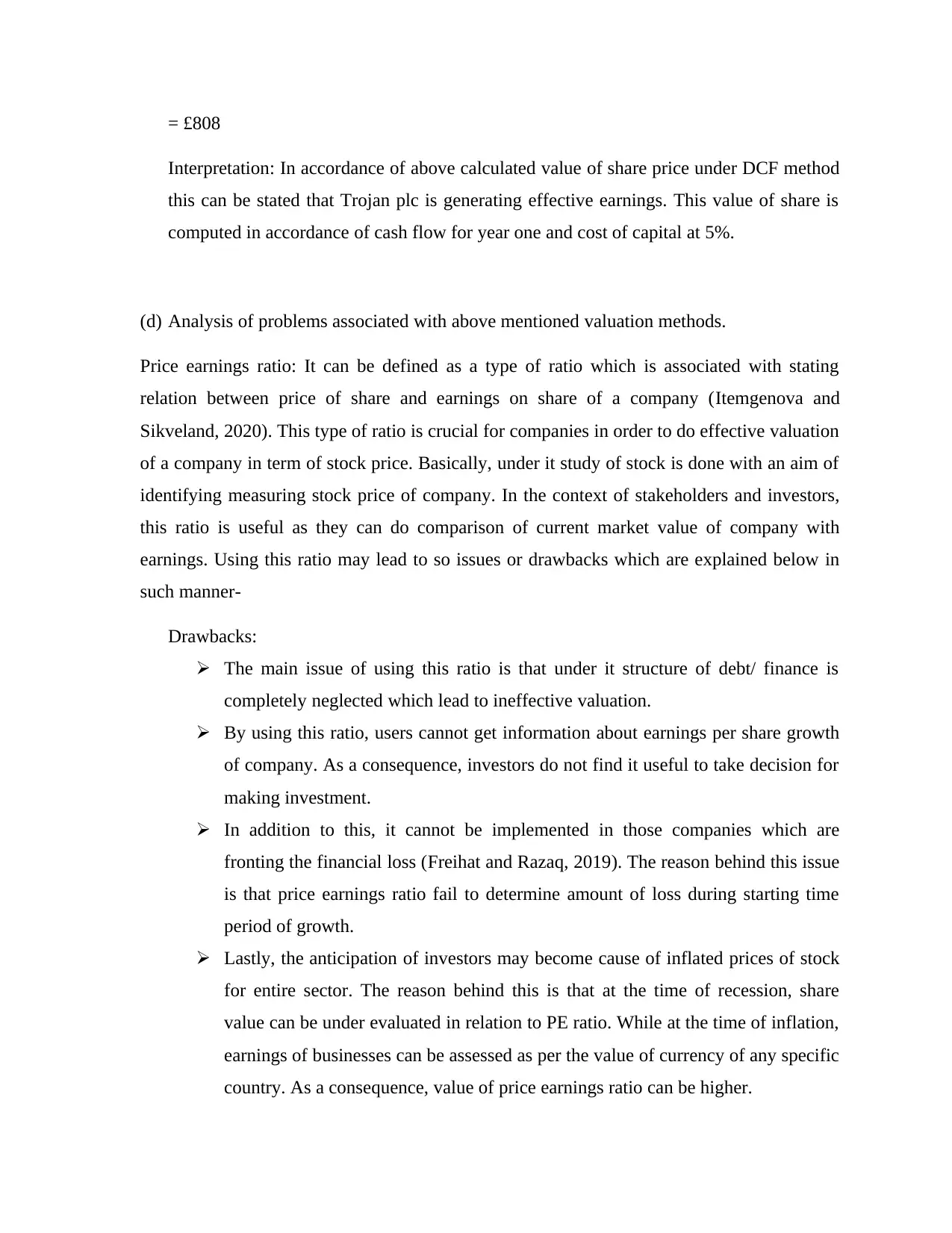

= £808

Interpretation: In accordance of above calculated value of share price under DCF method

this can be stated that Trojan plc is generating effective earnings. This value of share is

computed in accordance of cash flow for year one and cost of capital at 5%.

(d) Analysis of problems associated with above mentioned valuation methods.

Price earnings ratio: It can be defined as a type of ratio which is associated with stating

relation between price of share and earnings on share of a company (Itemgenova and

Sikveland, 2020). This type of ratio is crucial for companies in order to do effective valuation

of a company in term of stock price. Basically, under it study of stock is done with an aim of

identifying measuring stock price of company. In the context of stakeholders and investors,

this ratio is useful as they can do comparison of current market value of company with

earnings. Using this ratio may lead to so issues or drawbacks which are explained below in

such manner-

Drawbacks:

The main issue of using this ratio is that under it structure of debt/ finance is

completely neglected which lead to ineffective valuation.

By using this ratio, users cannot get information about earnings per share growth

of company. As a consequence, investors do not find it useful to take decision for

making investment.

In addition to this, it cannot be implemented in those companies which are

fronting the financial loss (Freihat and Razaq, 2019). The reason behind this issue

is that price earnings ratio fail to determine amount of loss during starting time

period of growth.

Lastly, the anticipation of investors may become cause of inflated prices of stock

for entire sector. The reason behind this is that at the time of recession, share

value can be under evaluated in relation to PE ratio. While at the time of inflation,

earnings of businesses can be assessed as per the value of currency of any specific

country. As a consequence, value of price earnings ratio can be higher.

Interpretation: In accordance of above calculated value of share price under DCF method

this can be stated that Trojan plc is generating effective earnings. This value of share is

computed in accordance of cash flow for year one and cost of capital at 5%.

(d) Analysis of problems associated with above mentioned valuation methods.

Price earnings ratio: It can be defined as a type of ratio which is associated with stating

relation between price of share and earnings on share of a company (Itemgenova and

Sikveland, 2020). This type of ratio is crucial for companies in order to do effective valuation

of a company in term of stock price. Basically, under it study of stock is done with an aim of

identifying measuring stock price of company. In the context of stakeholders and investors,

this ratio is useful as they can do comparison of current market value of company with

earnings. Using this ratio may lead to so issues or drawbacks which are explained below in

such manner-

Drawbacks:

The main issue of using this ratio is that under it structure of debt/ finance is

completely neglected which lead to ineffective valuation.

By using this ratio, users cannot get information about earnings per share growth

of company. As a consequence, investors do not find it useful to take decision for

making investment.

In addition to this, it cannot be implemented in those companies which are

fronting the financial loss (Freihat and Razaq, 2019). The reason behind this issue

is that price earnings ratio fail to determine amount of loss during starting time

period of growth.

Lastly, the anticipation of investors may become cause of inflated prices of stock

for entire sector. The reason behind this is that at the time of recession, share

value can be under evaluated in relation to PE ratio. While at the time of inflation,

earnings of businesses can be assessed as per the value of currency of any specific

country. As a consequence, value of price earnings ratio can be higher.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

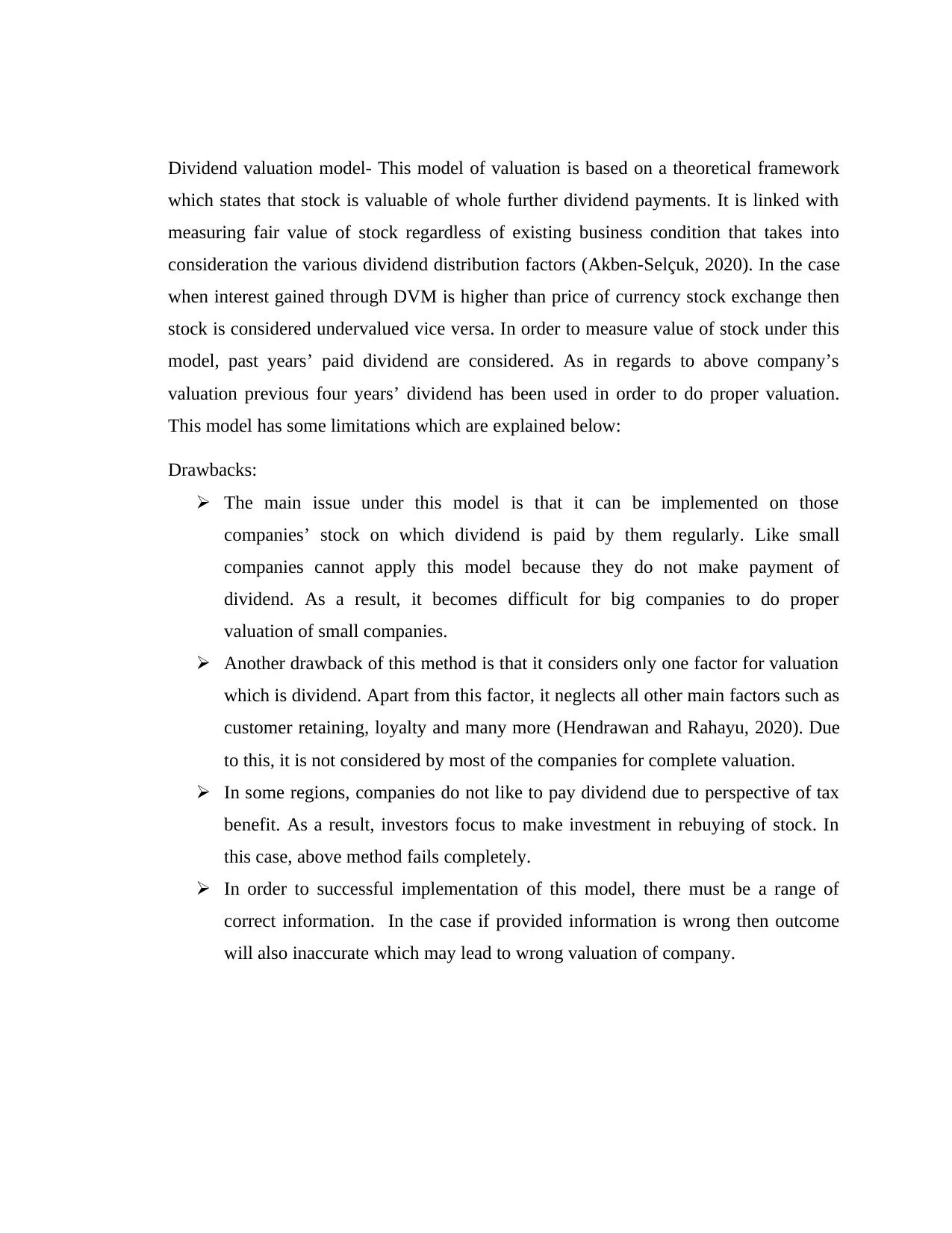

Dividend valuation model- This model of valuation is based on a theoretical framework

which states that stock is valuable of whole further dividend payments. It is linked with

measuring fair value of stock regardless of existing business condition that takes into

consideration the various dividend distribution factors (Akben-Selçuk, 2020). In the case

when interest gained through DVM is higher than price of currency stock exchange then

stock is considered undervalued vice versa. In order to measure value of stock under this

model, past years’ paid dividend are considered. As in regards to above company’s

valuation previous four years’ dividend has been used in order to do proper valuation.

This model has some limitations which are explained below:

Drawbacks:

The main issue under this model is that it can be implemented on those

companies’ stock on which dividend is paid by them regularly. Like small

companies cannot apply this model because they do not make payment of

dividend. As a result, it becomes difficult for big companies to do proper

valuation of small companies.

Another drawback of this method is that it considers only one factor for valuation

which is dividend. Apart from this factor, it neglects all other main factors such as

customer retaining, loyalty and many more (Hendrawan and Rahayu, 2020). Due

to this, it is not considered by most of the companies for complete valuation.

In some regions, companies do not like to pay dividend due to perspective of tax

benefit. As a result, investors focus to make investment in rebuying of stock. In

this case, above method fails completely.

In order to successful implementation of this model, there must be a range of

correct information. In the case if provided information is wrong then outcome

will also inaccurate which may lead to wrong valuation of company.

which states that stock is valuable of whole further dividend payments. It is linked with

measuring fair value of stock regardless of existing business condition that takes into

consideration the various dividend distribution factors (Akben-Selçuk, 2020). In the case

when interest gained through DVM is higher than price of currency stock exchange then

stock is considered undervalued vice versa. In order to measure value of stock under this

model, past years’ paid dividend are considered. As in regards to above company’s

valuation previous four years’ dividend has been used in order to do proper valuation.

This model has some limitations which are explained below:

Drawbacks:

The main issue under this model is that it can be implemented on those

companies’ stock on which dividend is paid by them regularly. Like small

companies cannot apply this model because they do not make payment of

dividend. As a result, it becomes difficult for big companies to do proper

valuation of small companies.

Another drawback of this method is that it considers only one factor for valuation

which is dividend. Apart from this factor, it neglects all other main factors such as

customer retaining, loyalty and many more (Hendrawan and Rahayu, 2020). Due

to this, it is not considered by most of the companies for complete valuation.

In some regions, companies do not like to pay dividend due to perspective of tax

benefit. As a result, investors focus to make investment in rebuying of stock. In

this case, above method fails completely.

In order to successful implementation of this model, there must be a range of

correct information. In the case if provided information is wrong then outcome

will also inaccurate which may lead to wrong valuation of company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

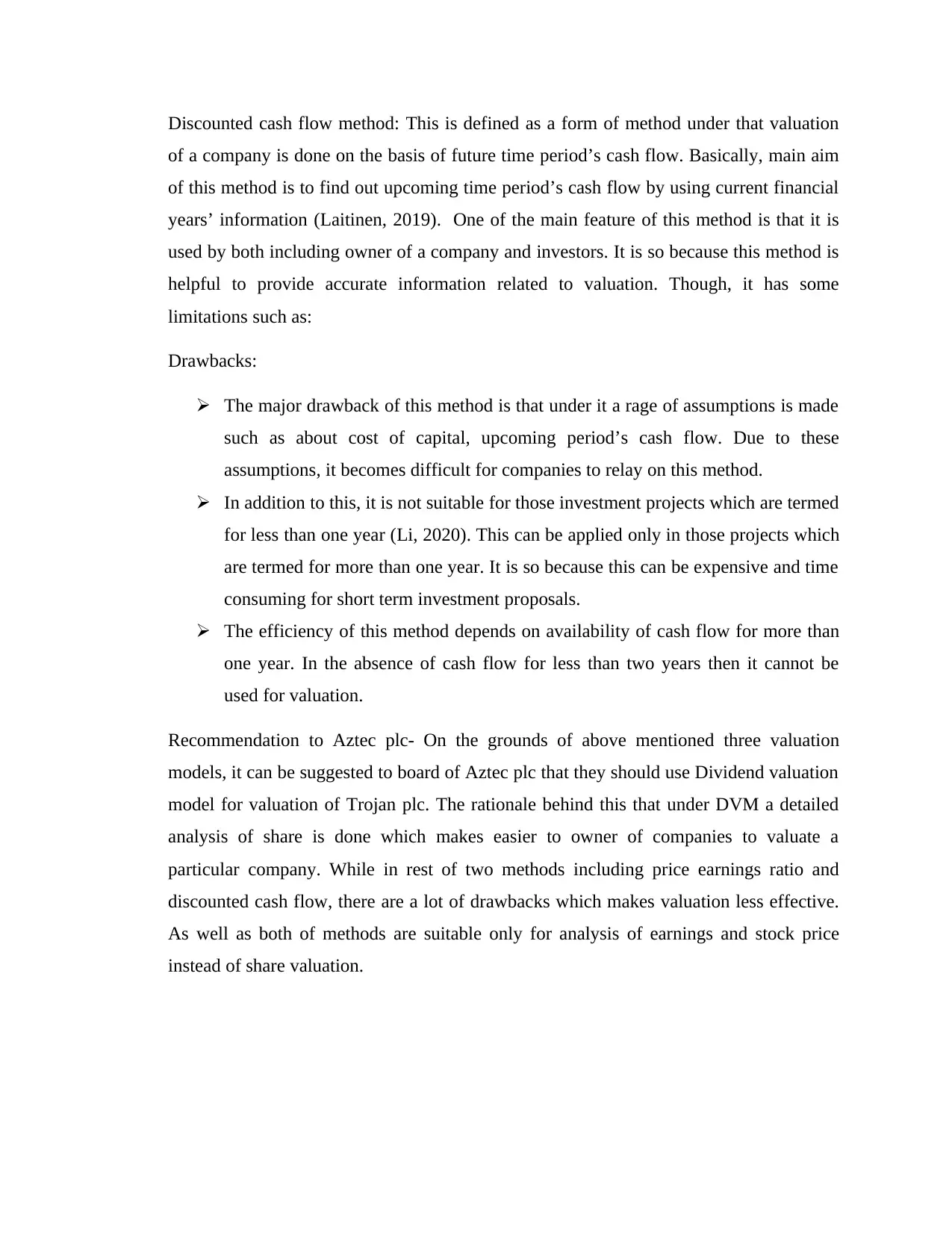

Discounted cash flow method: This is defined as a form of method under that valuation

of a company is done on the basis of future time period’s cash flow. Basically, main aim

of this method is to find out upcoming time period’s cash flow by using current financial

years’ information (Laitinen, 2019). One of the main feature of this method is that it is

used by both including owner of a company and investors. It is so because this method is

helpful to provide accurate information related to valuation. Though, it has some

limitations such as:

Drawbacks:

The major drawback of this method is that under it a rage of assumptions is made

such as about cost of capital, upcoming period’s cash flow. Due to these

assumptions, it becomes difficult for companies to relay on this method.

In addition to this, it is not suitable for those investment projects which are termed

for less than one year (Li, 2020). This can be applied only in those projects which

are termed for more than one year. It is so because this can be expensive and time

consuming for short term investment proposals.

The efficiency of this method depends on availability of cash flow for more than

one year. In the absence of cash flow for less than two years then it cannot be

used for valuation.

Recommendation to Aztec plc- On the grounds of above mentioned three valuation

models, it can be suggested to board of Aztec plc that they should use Dividend valuation

model for valuation of Trojan plc. The rationale behind this that under DVM a detailed

analysis of share is done which makes easier to owner of companies to valuate a

particular company. While in rest of two methods including price earnings ratio and

discounted cash flow, there are a lot of drawbacks which makes valuation less effective.

As well as both of methods are suitable only for analysis of earnings and stock price

instead of share valuation.

of a company is done on the basis of future time period’s cash flow. Basically, main aim

of this method is to find out upcoming time period’s cash flow by using current financial

years’ information (Laitinen, 2019). One of the main feature of this method is that it is

used by both including owner of a company and investors. It is so because this method is

helpful to provide accurate information related to valuation. Though, it has some

limitations such as:

Drawbacks:

The major drawback of this method is that under it a rage of assumptions is made

such as about cost of capital, upcoming period’s cash flow. Due to these

assumptions, it becomes difficult for companies to relay on this method.

In addition to this, it is not suitable for those investment projects which are termed

for less than one year (Li, 2020). This can be applied only in those projects which

are termed for more than one year. It is so because this can be expensive and time

consuming for short term investment proposals.

The efficiency of this method depends on availability of cash flow for more than

one year. In the absence of cash flow for less than two years then it cannot be

used for valuation.

Recommendation to Aztec plc- On the grounds of above mentioned three valuation

models, it can be suggested to board of Aztec plc that they should use Dividend valuation

model for valuation of Trojan plc. The rationale behind this that under DVM a detailed

analysis of share is done which makes easier to owner of companies to valuate a

particular company. While in rest of two methods including price earnings ratio and

discounted cash flow, there are a lot of drawbacks which makes valuation less effective.

As well as both of methods are suitable only for analysis of earnings and stock price

instead of share valuation.

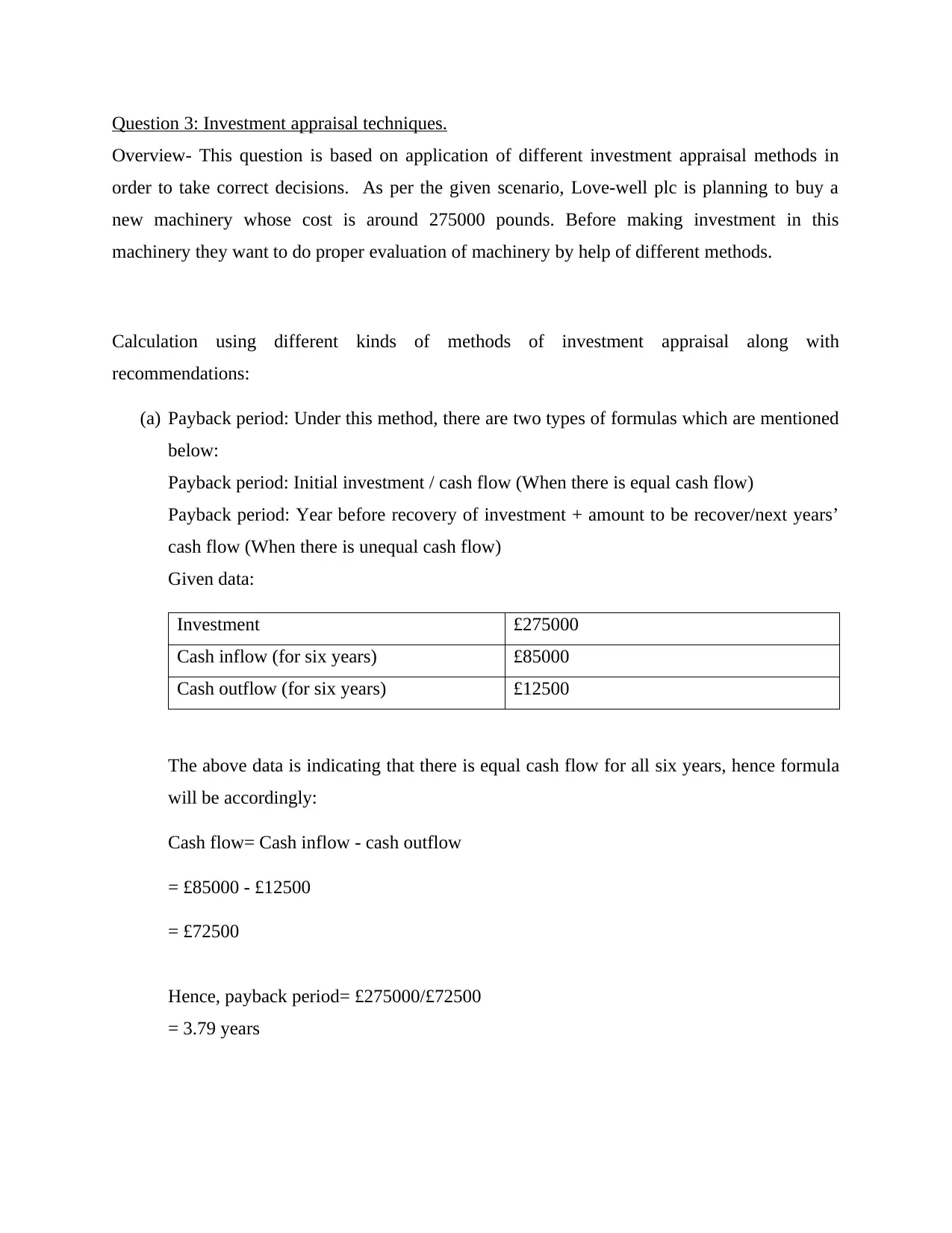

Question 3: Investment appraisal techniques.

Overview- This question is based on application of different investment appraisal methods in

order to take correct decisions. As per the given scenario, Love-well plc is planning to buy a

new machinery whose cost is around 275000 pounds. Before making investment in this

machinery they want to do proper evaluation of machinery by help of different methods.

Calculation using different kinds of methods of investment appraisal along with

recommendations:

(a) Payback period: Under this method, there are two types of formulas which are mentioned

below:

Payback period: Initial investment / cash flow (When there is equal cash flow)

Payback period: Year before recovery of investment + amount to be recover/next years’

cash flow (When there is unequal cash flow)

Given data:

Investment £275000

Cash inflow (for six years) £85000

Cash outflow (for six years) £12500

The above data is indicating that there is equal cash flow for all six years, hence formula

will be accordingly:

Cash flow= Cash inflow - cash outflow

= £85000 - £12500

= £72500

Hence, payback period= £275000/£72500

= 3.79 years

Overview- This question is based on application of different investment appraisal methods in

order to take correct decisions. As per the given scenario, Love-well plc is planning to buy a

new machinery whose cost is around 275000 pounds. Before making investment in this

machinery they want to do proper evaluation of machinery by help of different methods.

Calculation using different kinds of methods of investment appraisal along with

recommendations:

(a) Payback period: Under this method, there are two types of formulas which are mentioned

below:

Payback period: Initial investment / cash flow (When there is equal cash flow)

Payback period: Year before recovery of investment + amount to be recover/next years’

cash flow (When there is unequal cash flow)

Given data:

Investment £275000

Cash inflow (for six years) £85000

Cash outflow (for six years) £12500

The above data is indicating that there is equal cash flow for all six years, hence formula

will be accordingly:

Cash flow= Cash inflow - cash outflow

= £85000 - £12500

= £72500

Hence, payback period= £275000/£72500

= 3.79 years

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

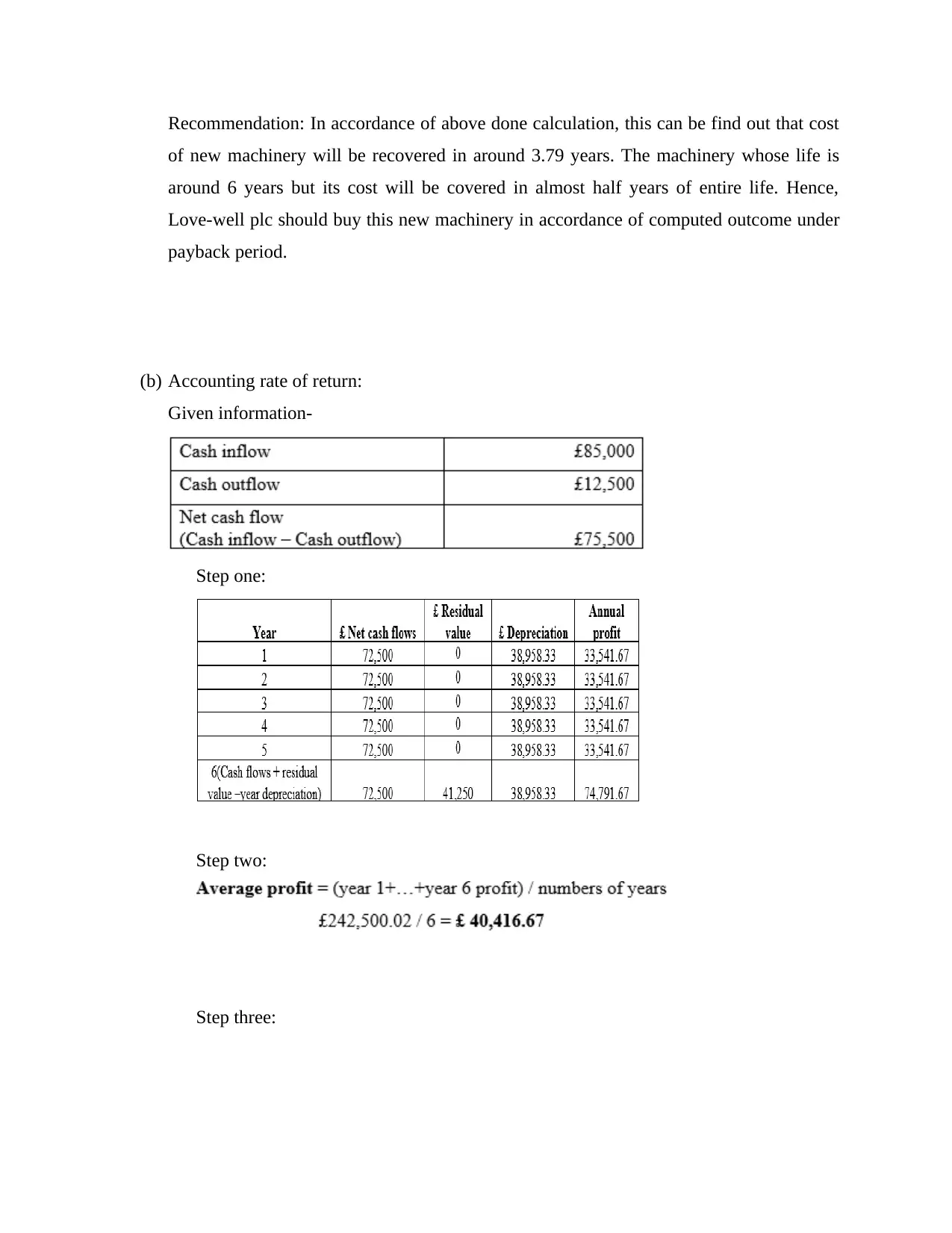

Recommendation: In accordance of above done calculation, this can be find out that cost

of new machinery will be recovered in around 3.79 years. The machinery whose life is

around 6 years but its cost will be covered in almost half years of entire life. Hence,

Love-well plc should buy this new machinery in accordance of computed outcome under

payback period.

(b) Accounting rate of return:

Given information-

Step one:

Step two:

Step three:

of new machinery will be recovered in around 3.79 years. The machinery whose life is

around 6 years but its cost will be covered in almost half years of entire life. Hence,

Love-well plc should buy this new machinery in accordance of computed outcome under

payback period.

(b) Accounting rate of return:

Given information-

Step one:

Step two:

Step three:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

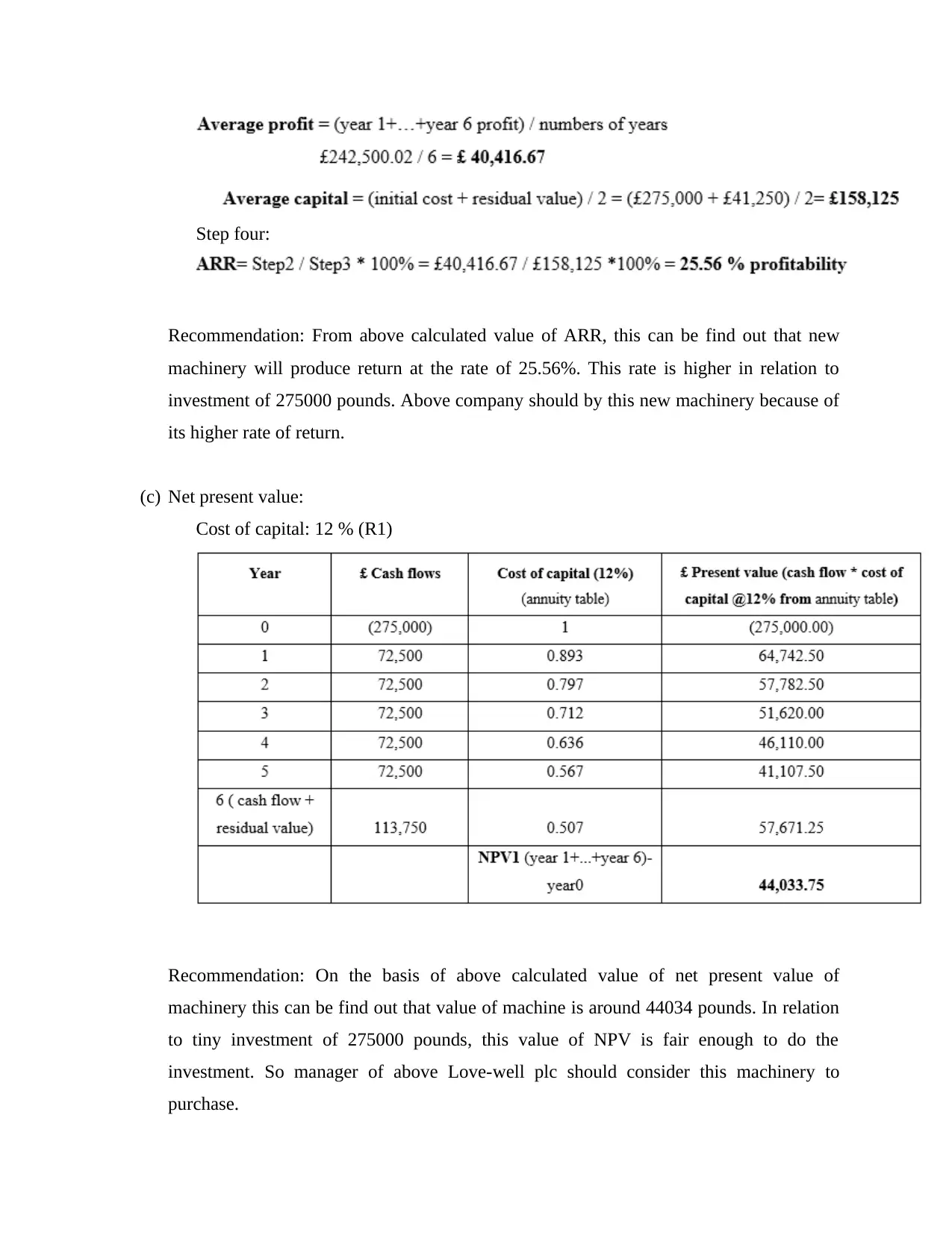

Step four:

Recommendation: From above calculated value of ARR, this can be find out that new

machinery will produce return at the rate of 25.56%. This rate is higher in relation to

investment of 275000 pounds. Above company should by this new machinery because of

its higher rate of return.

(c) Net present value:

Cost of capital: 12 % (R1)

Recommendation: On the basis of above calculated value of net present value of

machinery this can be find out that value of machine is around 44034 pounds. In relation

to tiny investment of 275000 pounds, this value of NPV is fair enough to do the

investment. So manager of above Love-well plc should consider this machinery to

purchase.

Recommendation: From above calculated value of ARR, this can be find out that new

machinery will produce return at the rate of 25.56%. This rate is higher in relation to

investment of 275000 pounds. Above company should by this new machinery because of

its higher rate of return.

(c) Net present value:

Cost of capital: 12 % (R1)

Recommendation: On the basis of above calculated value of net present value of

machinery this can be find out that value of machine is around 44034 pounds. In relation

to tiny investment of 275000 pounds, this value of NPV is fair enough to do the

investment. So manager of above Love-well plc should consider this machinery to

purchase.

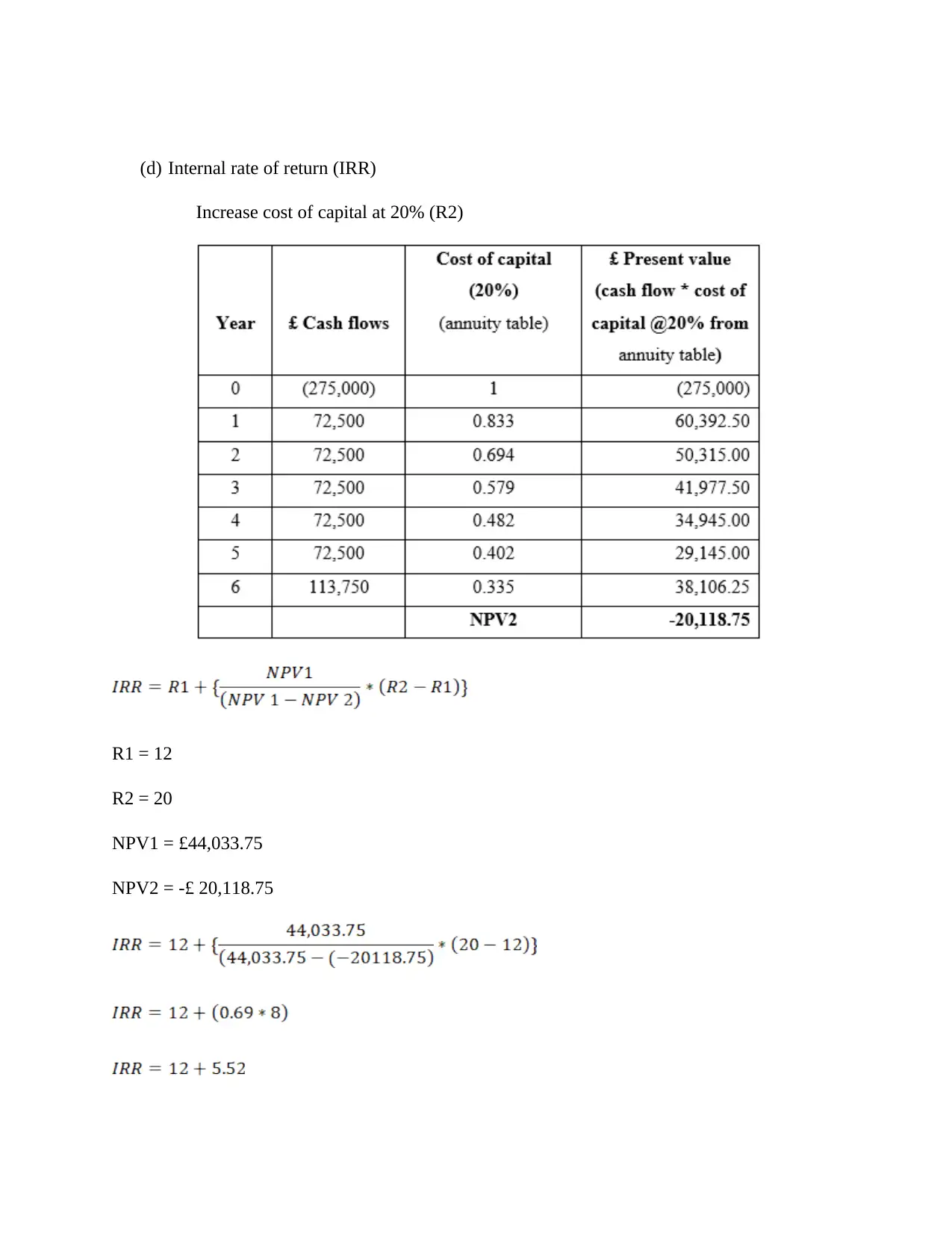

(d) Internal rate of return (IRR)

Increase cost of capital at 20% (R2)

R1 = 12

R2 = 20

NPV1 = £44,033.75

NPV2 = -£ 20,118.75

Increase cost of capital at 20% (R2)

R1 = 12

R2 = 20

NPV1 = £44,033.75

NPV2 = -£ 20,118.75

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.