Financial Management Report: Sources, Stakeholders, and Budgeting

VerifiedAdded on 2023/01/12

|15

|3312

|83

Report

AI Summary

This report offers a comprehensive overview of financial management within an organization. It begins by exploring the various sources of finance, including debt and equity, and then delves into the analysis of financial stakeholders, detailing their expectations and the impact of organizational decisions on them. The report emphasizes the importance of cash flow forecasting and cash flow management, outlining best practices and their significance. Furthermore, it discusses the assessment of business performance using financial measures such as liquidity, efficiency, profitability, and leverage ratios. The report also explains the role of financial performance indicators in monitoring the achievement of objectives and the purpose of key financial documents. Finally, it examines budgetary techniques, including the process of budget setting and the use of budgets to control costs within an organization's operations. Overall, the report provides a thorough understanding of financial management principles and their practical application.

B10821

Understanding financial

management

Understanding financial

management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

1. Understand finance within the context of an organization.......................................................4

1.1 Describe the organization’s sources of finance.................................................................4

1.2 Analyze the range of financial stakeholders and explain their various expectations of the

organization.................................................................................................................................6

1.3 Explain the importance of cash flow forecasting and cash flow management to the

organization.................................................................................................................................8

1.4 Provide a general assessment of business/organizational performance using appropriate

financial measures.....................................................................................................................10

2. Understand the value of recording financial management information.................................11

2.1 Explain the role of financial performance indicators in monitoring the achievement of

objectives...................................................................................................................................11

2.2 Explain the purpose of main financial documents used within the organization............11

3. Understand budgets for the management of own area of operation.......................................12

3.1 Explain the process of budget setting used in the organization......................................12

3.2 Explain how to use budgetary techniques to contribute to controlling cost in own area of

operation....................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

1. Understand finance within the context of an organization.......................................................4

1.1 Describe the organization’s sources of finance.................................................................4

1.2 Analyze the range of financial stakeholders and explain their various expectations of the

organization.................................................................................................................................6

1.3 Explain the importance of cash flow forecasting and cash flow management to the

organization.................................................................................................................................8

1.4 Provide a general assessment of business/organizational performance using appropriate

financial measures.....................................................................................................................10

2. Understand the value of recording financial management information.................................11

2.1 Explain the role of financial performance indicators in monitoring the achievement of

objectives...................................................................................................................................11

2.2 Explain the purpose of main financial documents used within the organization............11

3. Understand budgets for the management of own area of operation.......................................12

3.1 Explain the process of budget setting used in the organization......................................12

3.2 Explain how to use budgetary techniques to contribute to controlling cost in own area of

operation....................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

The purpose of this report is to have better understanding of finance within the context of

organization. There are basically two types of resources debt and equity to raise fund for any

company. Financial stakeholders are those internal and external parties which have stake in the

business like managers, investors, banks and various others. Cash flow management is the part of

forecasting of future cash to be coming to the organization and can be measured by measuring

actual result with forecasted expectations. The project also discusses about budgetary techniques

and process of setting budget for an organization. Today finance is becoming the core activity for

every business besides statistics; as this accounting tools help business in making set up plan

through trend analyses, forecasting, demand forecasting and capital budgeting.

The purpose of this report is to have better understanding of finance within the context of

organization. There are basically two types of resources debt and equity to raise fund for any

company. Financial stakeholders are those internal and external parties which have stake in the

business like managers, investors, banks and various others. Cash flow management is the part of

forecasting of future cash to be coming to the organization and can be measured by measuring

actual result with forecasted expectations. The project also discusses about budgetary techniques

and process of setting budget for an organization. Today finance is becoming the core activity for

every business besides statistics; as this accounting tools help business in making set up plan

through trend analyses, forecasting, demand forecasting and capital budgeting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Understand finance within the context of an organization

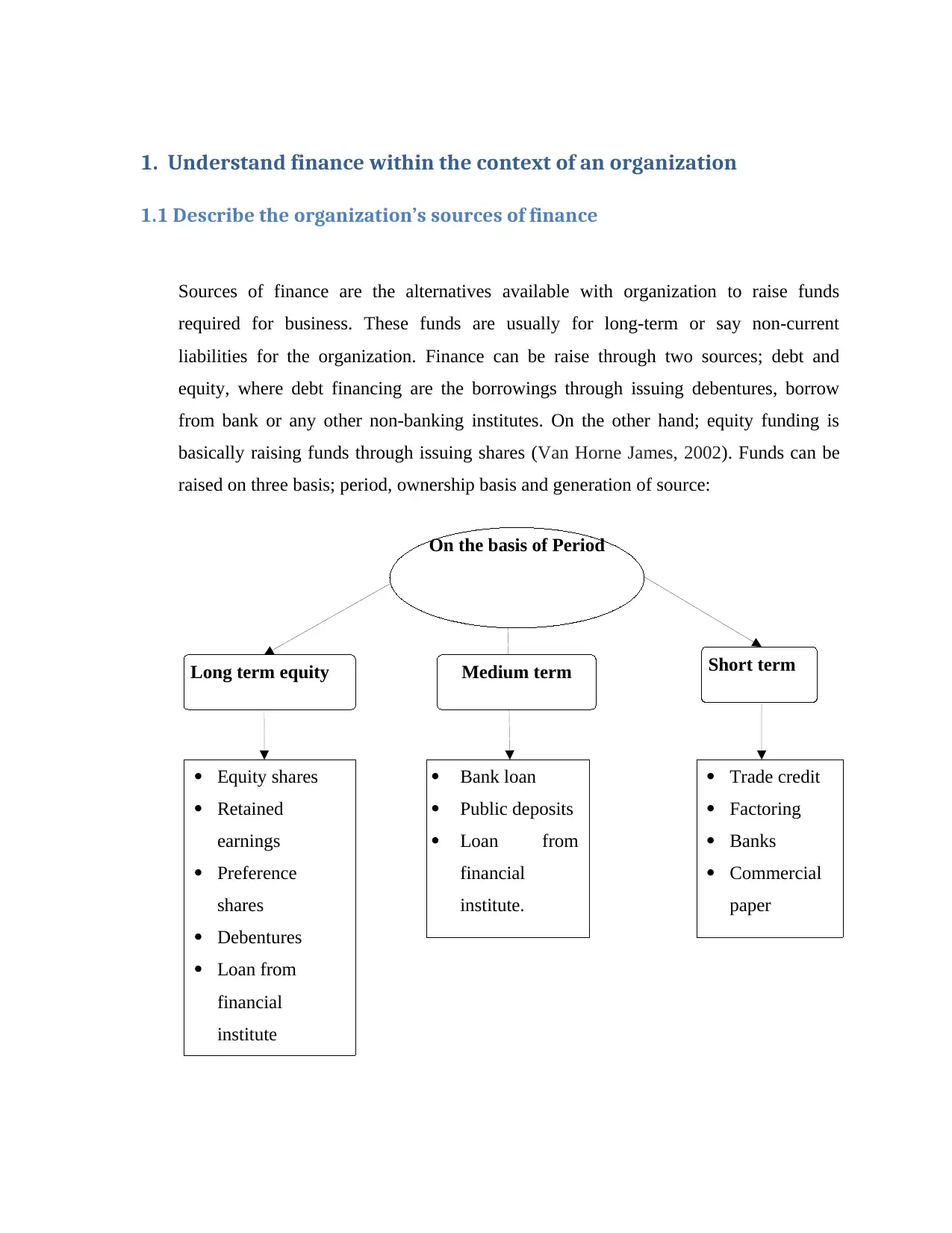

1.1 Describe the organization’s sources of finance

Sources of finance are the alternatives available with organization to raise funds

required for business. These funds are usually for long-term or say non-current

liabilities for the organization. Finance can be raise through two sources; debt and

equity, where debt financing are the borrowings through issuing debentures, borrow

from bank or any other non-banking institutes. On the other hand; equity funding is

basically raising funds through issuing shares (Van Horne James, 2002). Funds can be

raised on three basis; period, ownership basis and generation of source:

Long term equity Medium term Short term

Equity shares

Retained

earnings

Preference

shares

Debentures

Loan from

financial

institute

Bank loan

Public deposits

Loan from

financial

institute.

Trade credit

Factoring

Banks

Commercial

paper

On the basis of Period

1.1 Describe the organization’s sources of finance

Sources of finance are the alternatives available with organization to raise funds

required for business. These funds are usually for long-term or say non-current

liabilities for the organization. Finance can be raise through two sources; debt and

equity, where debt financing are the borrowings through issuing debentures, borrow

from bank or any other non-banking institutes. On the other hand; equity funding is

basically raising funds through issuing shares (Van Horne James, 2002). Funds can be

raised on three basis; period, ownership basis and generation of source:

Long term equity Medium term Short term

Equity shares

Retained

earnings

Preference

shares

Debentures

Loan from

financial

institute

Bank loan

Public deposits

Loan from

financial

institute.

Trade credit

Factoring

Banks

Commercial

paper

On the basis of Period

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

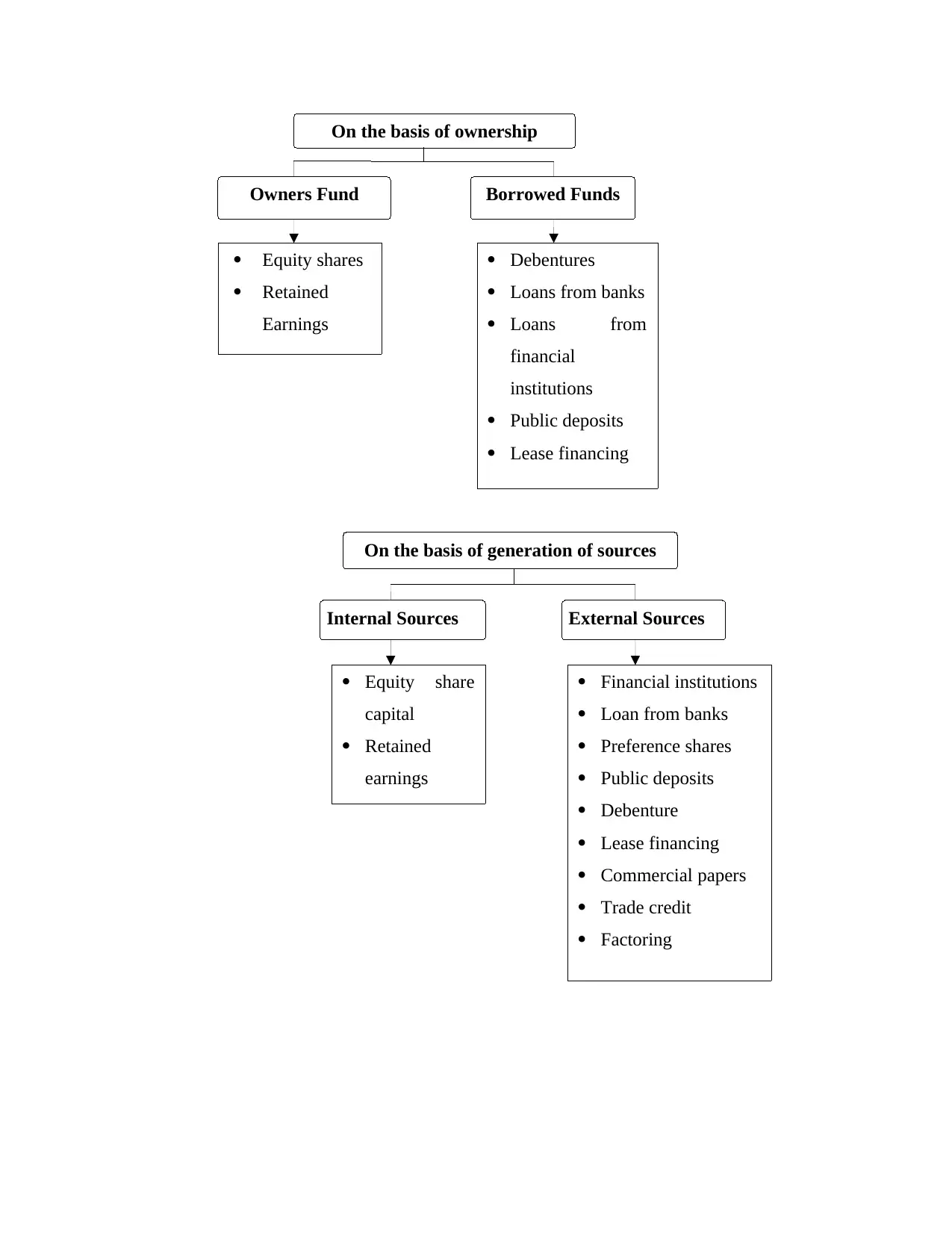

On the basis of ownership

Owners Fund Borrowed Funds

Equity shares

Retained

Earnings

Debentures

Loans from banks

Loans from

financial

institutions

Public deposits

Lease financing

On the basis of generation of sources

Internal Sources External Sources

Equity share

capital

Retained

earnings

Financial institutions

Loan from banks

Preference shares

Public deposits

Debenture

Lease financing

Commercial papers

Trade credit

Factoring

Owners Fund Borrowed Funds

Equity shares

Retained

Earnings

Debentures

Loans from banks

Loans from

financial

institutions

Public deposits

Lease financing

On the basis of generation of sources

Internal Sources External Sources

Equity share

capital

Retained

earnings

Financial institutions

Loan from banks

Preference shares

Public deposits

Debenture

Lease financing

Commercial papers

Trade credit

Factoring

1.2 Analyze the range of financial stakeholders and explain their various

expectations of the organization

Stakeholders: They are the person having personal or business interest in company

because any change in organization has direct impact on them. The common thing in all

stakeholders is they are well-wisher of organizations and always want growth of

company and business.

Stakeholder analysis: It is a process of determining those people having interest in

organization before the project begins and grouping them according to various levels of

their participation (Higgins and Reimers, 1995).

Financial stakeholders: These are the persons or parties having direct impact on their

profit with the firm’s decisions and earnings. In other word; their profit and loss

occurrence is dependent on organizations performance. Financial stakeholders show

their presence in the form of Internal and External stakeholders. Some of the financial

stakeholders are discussed below:

Here the organization taken for stakeholder analysis is based on financial institutions

Internal Stakeholders:

1. Directors: They are responsible for taking sensitive decisions for the company and

have direct impact; as poor performance could result in cutting in salary or

sometimes loss of job.

Expectations: They expect a good structure of commission from company and also

decision power; and more ownership within organization.

2. Business owner: Also called first stakeholder of any company. Major impact on

owner is seen of any organization.

Expectations: They have expectation that organization will grow at constant rate

and become number one service provider and get large exposure among customers.

expectations of the organization

Stakeholders: They are the person having personal or business interest in company

because any change in organization has direct impact on them. The common thing in all

stakeholders is they are well-wisher of organizations and always want growth of

company and business.

Stakeholder analysis: It is a process of determining those people having interest in

organization before the project begins and grouping them according to various levels of

their participation (Higgins and Reimers, 1995).

Financial stakeholders: These are the persons or parties having direct impact on their

profit with the firm’s decisions and earnings. In other word; their profit and loss

occurrence is dependent on organizations performance. Financial stakeholders show

their presence in the form of Internal and External stakeholders. Some of the financial

stakeholders are discussed below:

Here the organization taken for stakeholder analysis is based on financial institutions

Internal Stakeholders:

1. Directors: They are responsible for taking sensitive decisions for the company and

have direct impact; as poor performance could result in cutting in salary or

sometimes loss of job.

Expectations: They expect a good structure of commission from company and also

decision power; and more ownership within organization.

2. Business owner: Also called first stakeholder of any company. Major impact on

owner is seen of any organization.

Expectations: They have expectation that organization will grow at constant rate

and become number one service provider and get large exposure among customers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Employees: These are the workers or live assets of the company. They get direct

impact of organization’s performance on their salary. For instance; in boom period

they get incentives, bonuses and hike in salary and in recession period their salaries

get halved.

Expectations: They expect job security, good incentives for their performance and

reward for their big achievement. Besides this; they also expect protection on site

and get medical benefit on time (Madura, 2020).

External Stakeholders:

1. Creditors: These are the suppliers who deliver raw material to company on

debt basis. If company has good performance than they will get more orders

and hence gets more revenue.

Expectations: They usually have expectation that company will place large

order for longer period of time and payback the amount on time.

2. Investors: These are the parties who have invested in company either through

purchasing some proportion of ownership or having partnership with business

owner of the organization. Any profit and loss occurrence can directly impact

the earnings of this stakeholder (Cornett and Saunders, 2003).

Expectations: They expect high growth more return on investments and

participation in decision making. Additional to this; they also expects mild risk

taken by the company not to compromise with solvency.

3. Financial institutions: These stakeholders are the money lenders to

organizations for startup of any new project. They receive monthly installment

from the company for the money owned.

Expectations: They expect more growth for lending more money for new

projects and timely payment. They don’t expect any insolvency from client

especially organization.

4. Shareholders: These stakeholders are the equity or preference holders of the

company and have direct impact on their earning through organizations better

performance.

Expectations: They expect more dividend or high market price for their shares.

impact of organization’s performance on their salary. For instance; in boom period

they get incentives, bonuses and hike in salary and in recession period their salaries

get halved.

Expectations: They expect job security, good incentives for their performance and

reward for their big achievement. Besides this; they also expect protection on site

and get medical benefit on time (Madura, 2020).

External Stakeholders:

1. Creditors: These are the suppliers who deliver raw material to company on

debt basis. If company has good performance than they will get more orders

and hence gets more revenue.

Expectations: They usually have expectation that company will place large

order for longer period of time and payback the amount on time.

2. Investors: These are the parties who have invested in company either through

purchasing some proportion of ownership or having partnership with business

owner of the organization. Any profit and loss occurrence can directly impact

the earnings of this stakeholder (Cornett and Saunders, 2003).

Expectations: They expect high growth more return on investments and

participation in decision making. Additional to this; they also expects mild risk

taken by the company not to compromise with solvency.

3. Financial institutions: These stakeholders are the money lenders to

organizations for startup of any new project. They receive monthly installment

from the company for the money owned.

Expectations: They expect more growth for lending more money for new

projects and timely payment. They don’t expect any insolvency from client

especially organization.

4. Shareholders: These stakeholders are the equity or preference holders of the

company and have direct impact on their earning through organizations better

performance.

Expectations: They expect more dividend or high market price for their shares.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Government bodies: These stakeholders are the regulatory authority who

regulates rules and regulations for all industries.

Expectations: They expect proper following of rules from company and also

expect for growth rate to increase employment rate and better economy.

1.3 Explain the importance of cash flow forecasting and cash flow

management to the organization

Best practice for cash flow forecasting:

Focusing on both short and medium term forecasting: Short term forecasting is

done mainly to cover 30 days, daily and weekly analysis, on the other hand;

medium term forecasting is done for the period of monthly to annually (Brigham,

1996).

Automation tool installation: Some automation tool such as trend analysis, linear

regression method, moving average method and SAP tools helps organizations in

automatically calculate future cash flows on the basis of current data.

Reviewing cash flow forecasting variances on regular basis: This is the best

practice; and should be done on regular basis to identify any big variances between

actual result and projected cash inflows and outflows to timely execute solutions

and improve the quality of forecasts.

Creation of various scenarios: Scenarios are good to analyze future outcomes and

also to find independent variables which can directly impact the dependent

variables which is cash inflows and outflows.

Best practices for cash flow management:

Selection of banking partners: Banks are now doing multiple functions like

automated process of payroll, accounts payable, electronic data interchange (EDI),

affordable outsourcing and data protection.

regulates rules and regulations for all industries.

Expectations: They expect proper following of rules from company and also

expect for growth rate to increase employment rate and better economy.

1.3 Explain the importance of cash flow forecasting and cash flow

management to the organization

Best practice for cash flow forecasting:

Focusing on both short and medium term forecasting: Short term forecasting is

done mainly to cover 30 days, daily and weekly analysis, on the other hand;

medium term forecasting is done for the period of monthly to annually (Brigham,

1996).

Automation tool installation: Some automation tool such as trend analysis, linear

regression method, moving average method and SAP tools helps organizations in

automatically calculate future cash flows on the basis of current data.

Reviewing cash flow forecasting variances on regular basis: This is the best

practice; and should be done on regular basis to identify any big variances between

actual result and projected cash inflows and outflows to timely execute solutions

and improve the quality of forecasts.

Creation of various scenarios: Scenarios are good to analyze future outcomes and

also to find independent variables which can directly impact the dependent

variables which is cash inflows and outflows.

Best practices for cash flow management:

Selection of banking partners: Banks are now doing multiple functions like

automated process of payroll, accounts payable, electronic data interchange (EDI),

affordable outsourcing and data protection.

Developing cash forecasting: With irregular cash inflows and higher association

of variance risks; it is preferred to do rolling budget forecasting; which involves

continuous evaluation of budgets to maintain accuracy of projected data.

Improving Investment yields: Through effectively management of portfolio

within organization; company can improve investment yield by avoiding non-

moving assets and making fund idle (Brigham and Ehrhardt, 2013).

Reviewing cash management: Making strategies and plans regarding cash

management is not enough; regular testing and removing bug and error can make it

more effective.

Centralize infrastructure: Organizations having branches in more than one

country should adopt centralize handling of data and information’s or it should built

centralized server which is integrated to other branch’s server to get timely data and

provide full control over their cash transactions.

Importance of cash flow forecasting:

Prepare in advance for any shortage of fund: Through cash flow forecasting any

company can meet funds required for new project or payment to creditors. Urgent

requirement of fund can only meet; when firm prepared for same and ready with

alternatives.

Tells about opportunities and threats: Projected cash flow shows opportunities

and threats related with adopting new project. It also tells about any hurdle in long

term growth of the business.

Shows projected growth of organization: How company will grow and at what

rate can only answer by cash flow forecasting.

Establish control over unnecessary utilization of cash: Through cost volume

analyses; organization can track where the funds come from and where it is utilized

and what impact it falls on productivity of operations.

Importance of cash flow management:

Better utilization of funds: By making proper portfolio; organization can better

utilize its idle funds for generating more cash inflows.

of variance risks; it is preferred to do rolling budget forecasting; which involves

continuous evaluation of budgets to maintain accuracy of projected data.

Improving Investment yields: Through effectively management of portfolio

within organization; company can improve investment yield by avoiding non-

moving assets and making fund idle (Brigham and Ehrhardt, 2013).

Reviewing cash management: Making strategies and plans regarding cash

management is not enough; regular testing and removing bug and error can make it

more effective.

Centralize infrastructure: Organizations having branches in more than one

country should adopt centralize handling of data and information’s or it should built

centralized server which is integrated to other branch’s server to get timely data and

provide full control over their cash transactions.

Importance of cash flow forecasting:

Prepare in advance for any shortage of fund: Through cash flow forecasting any

company can meet funds required for new project or payment to creditors. Urgent

requirement of fund can only meet; when firm prepared for same and ready with

alternatives.

Tells about opportunities and threats: Projected cash flow shows opportunities

and threats related with adopting new project. It also tells about any hurdle in long

term growth of the business.

Shows projected growth of organization: How company will grow and at what

rate can only answer by cash flow forecasting.

Establish control over unnecessary utilization of cash: Through cost volume

analyses; organization can track where the funds come from and where it is utilized

and what impact it falls on productivity of operations.

Importance of cash flow management:

Better utilization of funds: By making proper portfolio; organization can better

utilize its idle funds for generating more cash inflows.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Improves non-moving assets: Non-moving assets are those equipments and

prosperities which are not being utilized by business to convert into cash; through

proper management these assets can be minimized.

Improves liquidity and solvency: Through avoiding wastage of resources and

selecting proper funding alternatives; organization can improve liquidity and

solvency (Fabozzi and Peterson, 2003).

Minimize wastage of resources: Effective planning and controlling of resources

minimize the unnecessary consumption of funds.

1.4 Provide a general assessment of business/organizational performance

using appropriate financial measures

Business performance can be assess in three ways; by comparing actual results with

competitor having same industry and services, matching past data of company and by

measuring actual data with reference to budgeted one. Some of the useful assessment

tools helpful in determination of results are discussed below:

Liquidity ratios: These ratios show the liquidity of company; as liquidity means

how easily organization can cover its current liabilities with available funds. Some

of the liquidity ratios tools are current ratio and quick / acid test ratio

Efficiency ratios: These are effective tool to determine the performance of

collections, cash flow and operational results. Some of the tools of efficiency ratios

are inventory turnover ratio, average collection period and debtor’s turnover ratio.

Profitability ratios: These ratios show how much proportion of earning is gained

by business with comparison to investment. Examples; net profit margin, gross

profit margin, return on investment and return on equity.

Leverage ratios: It tells about long-term solvency of a company and tells about at

what extent long-term debt can be used to support organization. Examples of

leverage ratios are; Debt-to-equity and debt-to-asset (Block, Hirt and Danielsen,

1994).

prosperities which are not being utilized by business to convert into cash; through

proper management these assets can be minimized.

Improves liquidity and solvency: Through avoiding wastage of resources and

selecting proper funding alternatives; organization can improve liquidity and

solvency (Fabozzi and Peterson, 2003).

Minimize wastage of resources: Effective planning and controlling of resources

minimize the unnecessary consumption of funds.

1.4 Provide a general assessment of business/organizational performance

using appropriate financial measures

Business performance can be assess in three ways; by comparing actual results with

competitor having same industry and services, matching past data of company and by

measuring actual data with reference to budgeted one. Some of the useful assessment

tools helpful in determination of results are discussed below:

Liquidity ratios: These ratios show the liquidity of company; as liquidity means

how easily organization can cover its current liabilities with available funds. Some

of the liquidity ratios tools are current ratio and quick / acid test ratio

Efficiency ratios: These are effective tool to determine the performance of

collections, cash flow and operational results. Some of the tools of efficiency ratios

are inventory turnover ratio, average collection period and debtor’s turnover ratio.

Profitability ratios: These ratios show how much proportion of earning is gained

by business with comparison to investment. Examples; net profit margin, gross

profit margin, return on investment and return on equity.

Leverage ratios: It tells about long-term solvency of a company and tells about at

what extent long-term debt can be used to support organization. Examples of

leverage ratios are; Debt-to-equity and debt-to-asset (Block, Hirt and Danielsen,

1994).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Understand the value of recording financial management

information

2.1 Explain the role of financial performance indicators in monitoring the

achievement of objectives

1. Settlement of KPIs: Financial performance helps organization in setting key

performance indicators to match actual performance with objectives set by firm.

2. Setting up monitoring and measurement systems: Financial performance plays a

major role in setting monitoring and measurement systems through providing

effective tools of analyses of data.

3. Collecting and recording data: Financial indicators supports achieving objectives

through accurately collection of data and recording it without any error; which helps

company in setting proper objective.

4. Helps in data analysis: Through various tools such as profitability ratios,

comparative balance sheet, trend analysis, leverage ratios, etc. it helps organization

to properly interpret data with original results; to find any misleading factors and

observe it to further improvement of same (Rose and Hudgins, 2006).

5. Use of effective reporting: Financial performance indicators has a role to show

results with effective and simple to read reports; which helps management in

identifying reasons for growth and failure in achieving of goal.

2.2 Explain the purpose of main financial documents used within the

organization

Financial documents are also known as financial statements which are used for

reporting financial information like balance sheet, income statement and cash flow

statement. The purpose of main financial documents used within organization is

discussed below:

Income Statement: This financial document is helpful in showing total earnings of the

business at the end of the year. It also indicates various variables and non-variables

information

2.1 Explain the role of financial performance indicators in monitoring the

achievement of objectives

1. Settlement of KPIs: Financial performance helps organization in setting key

performance indicators to match actual performance with objectives set by firm.

2. Setting up monitoring and measurement systems: Financial performance plays a

major role in setting monitoring and measurement systems through providing

effective tools of analyses of data.

3. Collecting and recording data: Financial indicators supports achieving objectives

through accurately collection of data and recording it without any error; which helps

company in setting proper objective.

4. Helps in data analysis: Through various tools such as profitability ratios,

comparative balance sheet, trend analysis, leverage ratios, etc. it helps organization

to properly interpret data with original results; to find any misleading factors and

observe it to further improvement of same (Rose and Hudgins, 2006).

5. Use of effective reporting: Financial performance indicators has a role to show

results with effective and simple to read reports; which helps management in

identifying reasons for growth and failure in achieving of goal.

2.2 Explain the purpose of main financial documents used within the

organization

Financial documents are also known as financial statements which are used for

reporting financial information like balance sheet, income statement and cash flow

statement. The purpose of main financial documents used within organization is

discussed below:

Income Statement: This financial document is helpful in showing total earnings of the

business at the end of the year. It also indicates various variables and non-variables

expenses and plays important role in identifying earning per share, distributable profit

and retained earnings of organizations.

Balance Sheet: It well known for showing financial position of the company. It

grouped assets and liabilities separately to show where the various sources of fund are

utilized to acquire current and non-current assets. It indicates financial strength of

organization (Stern, Stewart III and Chew, 1995).

Cash flow statement: It shows liquidity of a company through tracking; from where

cash is coming and where it is utilized. This statement has importance for internal

stakeholders like managers and directors to know how much cash business required in

future meeting working capital requirements.

3. Understand budgets for the management of own area of operation

3.1 Explain the process of budget setting used in the organization

1. Communication within executive management: The first step in making budget

process is to communicate the plan for budget to CEO, COO and CFO regarding

requirement of budget plan for next fiscal year.

2. Establishing objectives and goals: After successfully communicating needs for

preparing budget forecasting; setting up of goals and objectives which can be met by

organization within a year has done.

3. Developing detailed budget: On the basis of various financial documents such as

income statement, balance sheet and cash flow statement; a detailed distribution of

various costs done and also sources for achieving estimated revenue mentioned.

4. Compilation and revision of budget model: After go through above three steps;

the fourth step is to revised and test for error in budget model (Rosen and Granbois,

1983).

5. Budget committee review: Final budget is reviewed by board of directors and

committee to check the feasibility of budget and changes in revenue if implemented.

and retained earnings of organizations.

Balance Sheet: It well known for showing financial position of the company. It

grouped assets and liabilities separately to show where the various sources of fund are

utilized to acquire current and non-current assets. It indicates financial strength of

organization (Stern, Stewart III and Chew, 1995).

Cash flow statement: It shows liquidity of a company through tracking; from where

cash is coming and where it is utilized. This statement has importance for internal

stakeholders like managers and directors to know how much cash business required in

future meeting working capital requirements.

3. Understand budgets for the management of own area of operation

3.1 Explain the process of budget setting used in the organization

1. Communication within executive management: The first step in making budget

process is to communicate the plan for budget to CEO, COO and CFO regarding

requirement of budget plan for next fiscal year.

2. Establishing objectives and goals: After successfully communicating needs for

preparing budget forecasting; setting up of goals and objectives which can be met by

organization within a year has done.

3. Developing detailed budget: On the basis of various financial documents such as

income statement, balance sheet and cash flow statement; a detailed distribution of

various costs done and also sources for achieving estimated revenue mentioned.

4. Compilation and revision of budget model: After go through above three steps;

the fourth step is to revised and test for error in budget model (Rosen and Granbois,

1983).

5. Budget committee review: Final budget is reviewed by board of directors and

committee to check the feasibility of budget and changes in revenue if implemented.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.