Financial Management Report: Aztec plc and Trojan plc Analysis

VerifiedAdded on 2023/01/09

|17

|3860

|60

Report

AI Summary

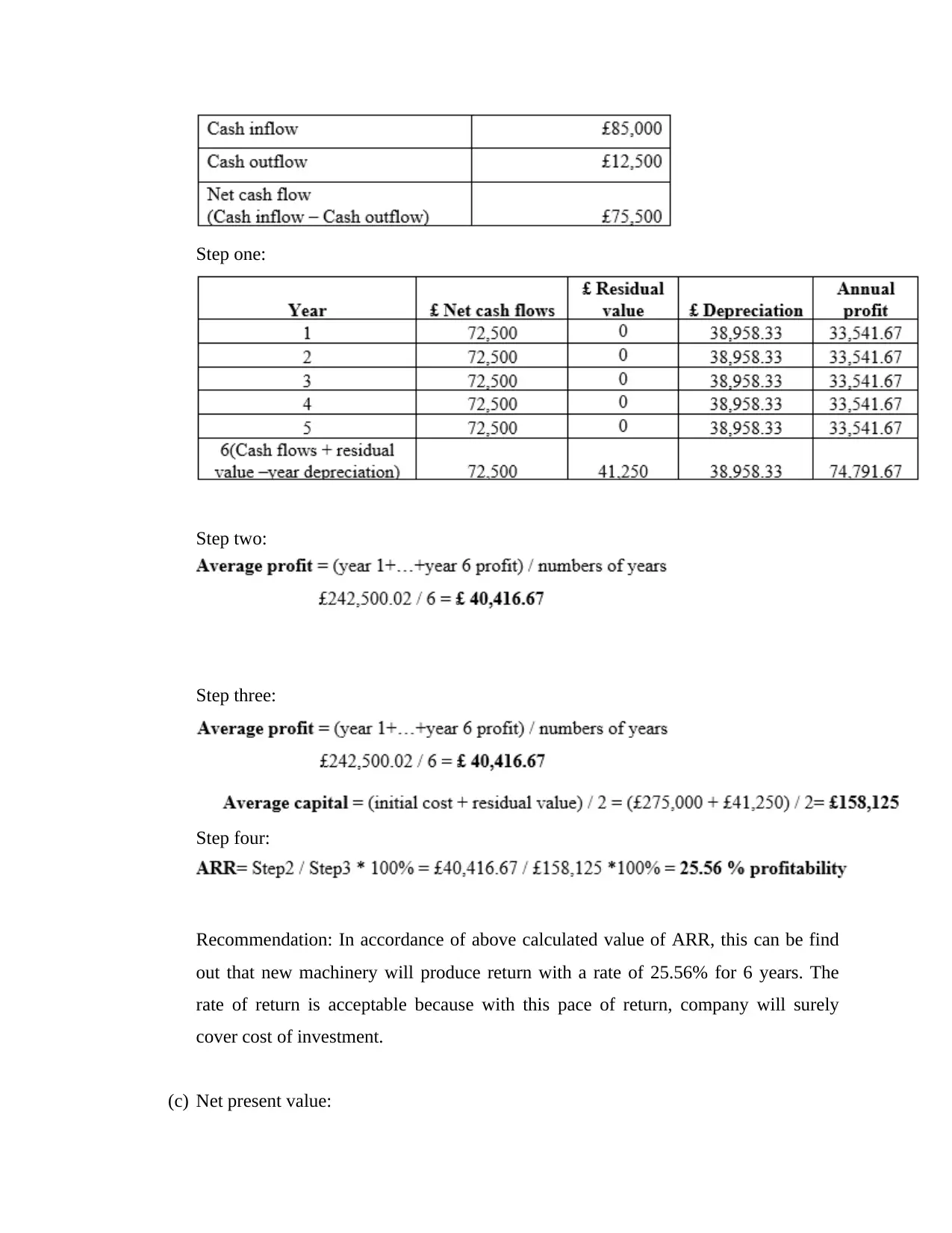

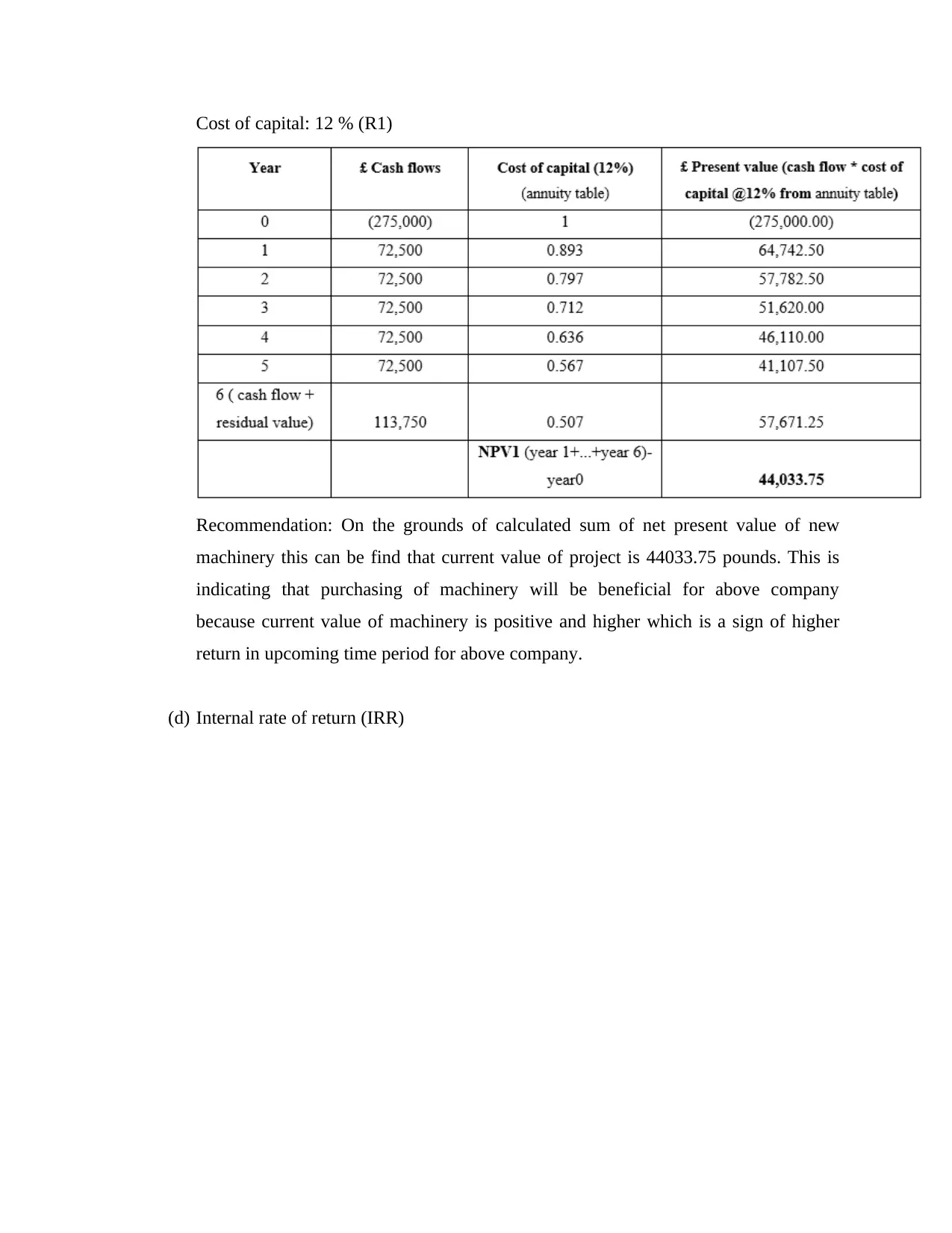

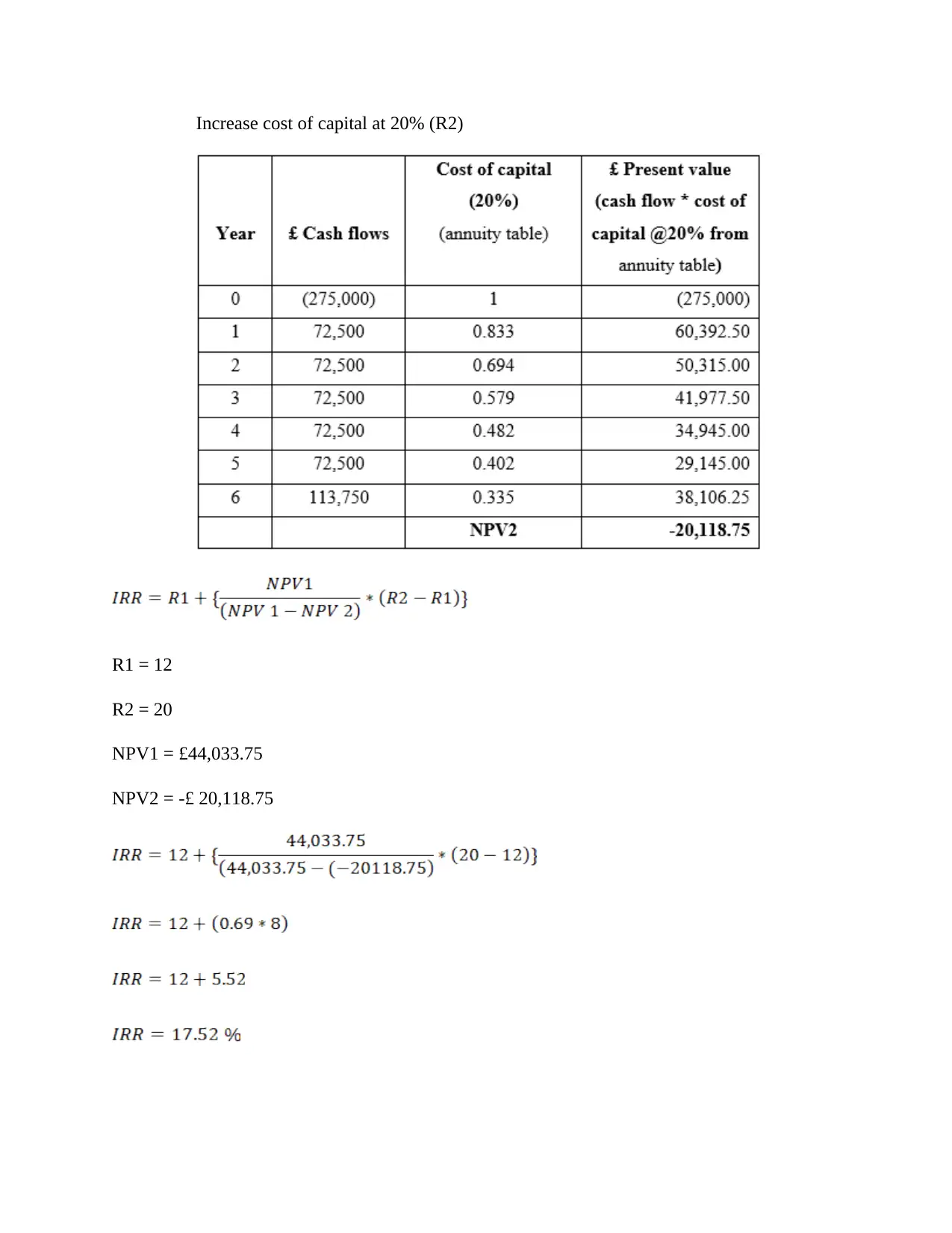

This report delves into the realm of financial management, focusing on mergers, takeovers, and investment appraisal techniques. It begins by defining financial management and its importance in companies, emphasizing the allocation of financial resources. The main body of the report addresses two key questions: mergers and acquisitions, specifically analyzing the potential acquisition of Trojan plc by Aztec plc using methods such as Price Earnings Ratio, Dividend Valuation Model, and Discounted Cash Flow. It also provides a critical analysis of the problems associated with each valuation method and offers recommendations. The second part of the report focuses on investment appraisal methods, calculating and evaluating the efficiency of new machinery for Love well limited using the payback period, accounting rate of return, net present value, and internal rate of return. The report concludes with a critical evaluation of the benefits and drawbacks of these investment appraisal methods, providing comprehensive insights into financial decision-making.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.