Financial Management Report: Lexbel Plc and Investment Appraisal

VerifiedAdded on 2023/01/13

|14

|3759

|42

Report

AI Summary

This report provides a comprehensive analysis of financial management, focusing on two key areas: long-term finance and investment appraisal techniques. The first section delves into the concept of issuing right shares, specifically examining the case of Lexbel Plc, and includes calculations for Profit After Tax (PAT), the number of shares to be issued, theoretical ex-rights price, and expected earnings per share under various scenarios. It further evaluates different right issue options and the benefits of scrip dividends for both shareholders and companies. The second section explores various investment appraisal techniques, including the payback period, Accounting Rate of Return (ARR), Net Present Value (NPV), and Internal Rate of Return (IRR), to evaluate the attractiveness of an investment in new machinery for Lovewell Limited. The report provides detailed calculations for each method and critically evaluates the benefits and limitations of these techniques, offering valuable insights into financial decision-making.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 2. Long Terms Finance.....................................................................................................3

(a). Calculate PAT of 20% on shareholders funds of Lexbel Plc................................................3

(b). Determine various aspects which mentioned below.............................................................4

1. Number of shared to be issued.................................................................................................4

2. Theoretical ex rights price.......................................................................................................4

3. Expected earning per share......................................................................................................4

4. Form of issue of right issue price............................................................................................5

5. Evaluation of best option among these above mention options..............................................6

(c). Evaluate the benefits of scrip divided in context of shareholders or companies...................6

Question 3. Investment Appraisal Techniques................................................................................7

(a). By using investment appraisal techniques, calculate below mention following methods....7

1. Payback period.........................................................................................................................7

2. Accounting Rate of Reruns......................................................................................................8

3. Net Present Value....................................................................................................................9

4. Internal Rate of Return...........................................................................................................10

(b). Critically evaluate benefits or limitations of different investment appraisal techniques

....................................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES .............................................................................................................................14

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 2. Long Terms Finance.....................................................................................................3

(a). Calculate PAT of 20% on shareholders funds of Lexbel Plc................................................3

(b). Determine various aspects which mentioned below.............................................................4

1. Number of shared to be issued.................................................................................................4

2. Theoretical ex rights price.......................................................................................................4

3. Expected earning per share......................................................................................................4

4. Form of issue of right issue price............................................................................................5

5. Evaluation of best option among these above mention options..............................................6

(c). Evaluate the benefits of scrip divided in context of shareholders or companies...................6

Question 3. Investment Appraisal Techniques................................................................................7

(a). By using investment appraisal techniques, calculate below mention following methods....7

1. Payback period.........................................................................................................................7

2. Accounting Rate of Reruns......................................................................................................8

3. Net Present Value....................................................................................................................9

4. Internal Rate of Return...........................................................................................................10

(b). Critically evaluate benefits or limitations of different investment appraisal techniques

....................................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES .............................................................................................................................14

INTRODUCTION

Financial management is essential for every organizations because management will used

to analyse, measure and interpret financial results. With the help of various techniques or

method, managers able to evaluate actual performance or financial helps of company (Amanah,

Rahadian and Iradianty, 2016). Management should ensure that, they manage financial resources

which helps in achieving their desired goals & objectives. Main aim of this assessment is to

make people aware about importance of financial management in organizations. This assignment

based on two questions which are about long term finance and different investment appraisal

techniques.

MAIN BODY

Question 2. Long Terms Finance

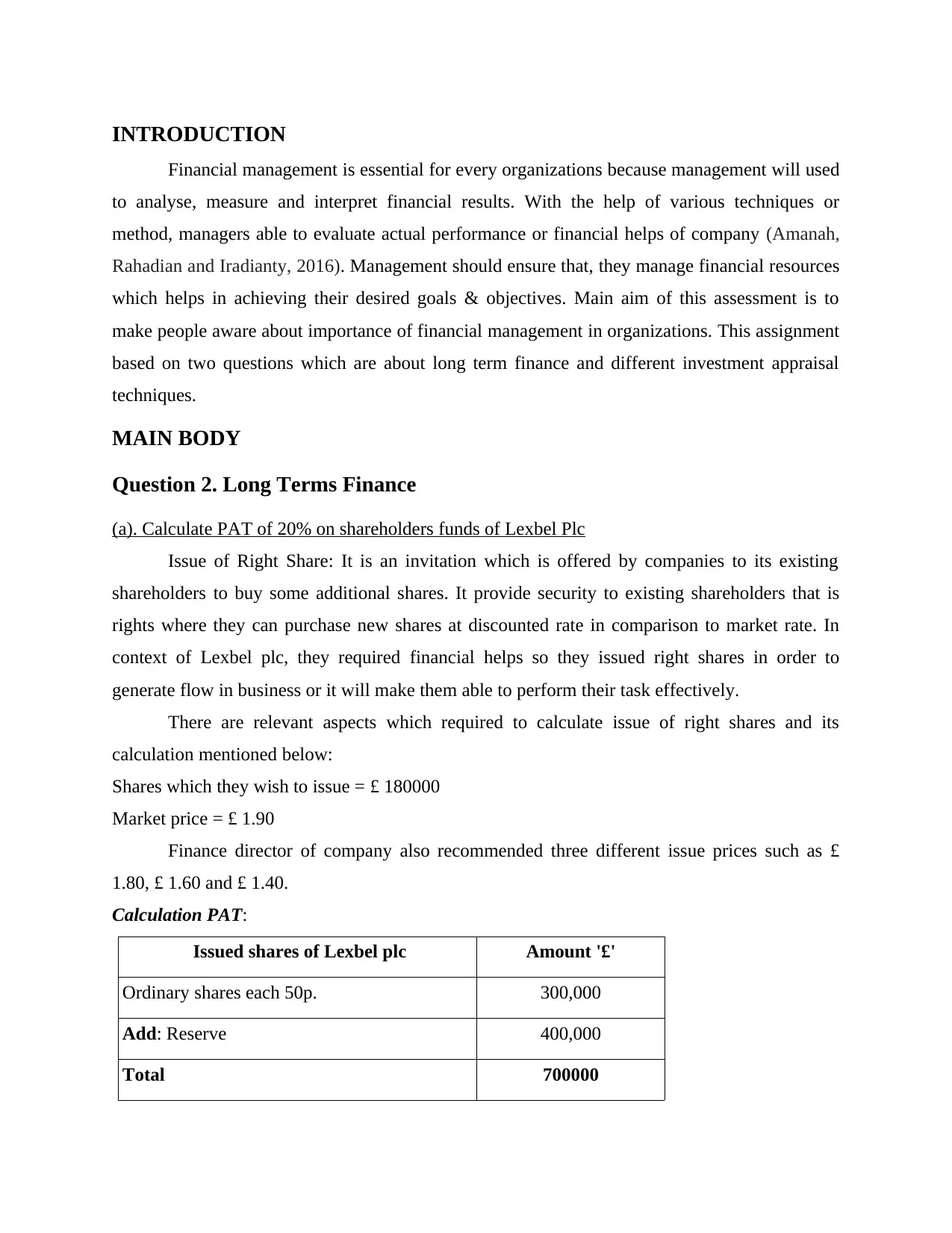

(a). Calculate PAT of 20% on shareholders funds of Lexbel Plc

Issue of Right Share: It is an invitation which is offered by companies to its existing

shareholders to buy some additional shares. It provide security to existing shareholders that is

rights where they can purchase new shares at discounted rate in comparison to market rate. In

context of Lexbel plc, they required financial helps so they issued right shares in order to

generate flow in business or it will make them able to perform their task effectively.

There are relevant aspects which required to calculate issue of right shares and its

calculation mentioned below:

Shares which they wish to issue = £ 180000

Market price = £ 1.90

Finance director of company also recommended three different issue prices such as £

1.80, £ 1.60 and £ 1.40.

Calculation PAT:

Issued shares of Lexbel plc Amount '£'

Ordinary shares each 50p. 300,000

Add: Reserve 400,000

Total 700000

Financial management is essential for every organizations because management will used

to analyse, measure and interpret financial results. With the help of various techniques or

method, managers able to evaluate actual performance or financial helps of company (Amanah,

Rahadian and Iradianty, 2016). Management should ensure that, they manage financial resources

which helps in achieving their desired goals & objectives. Main aim of this assessment is to

make people aware about importance of financial management in organizations. This assignment

based on two questions which are about long term finance and different investment appraisal

techniques.

MAIN BODY

Question 2. Long Terms Finance

(a). Calculate PAT of 20% on shareholders funds of Lexbel Plc

Issue of Right Share: It is an invitation which is offered by companies to its existing

shareholders to buy some additional shares. It provide security to existing shareholders that is

rights where they can purchase new shares at discounted rate in comparison to market rate. In

context of Lexbel plc, they required financial helps so they issued right shares in order to

generate flow in business or it will make them able to perform their task effectively.

There are relevant aspects which required to calculate issue of right shares and its

calculation mentioned below:

Shares which they wish to issue = £ 180000

Market price = £ 1.90

Finance director of company also recommended three different issue prices such as £

1.80, £ 1.60 and £ 1.40.

Calculation PAT:

Issued shares of Lexbel plc Amount '£'

Ordinary shares each 50p. 300,000

Add: Reserve 400,000

Total 700000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit After Tax (PAT) { 700000 * 20 % } 140,000

(b). Determine various aspects which mentioned below

1. Number of shared to be issued

Formula:

Number of Share Issued = Aggregate Funds to be elevated / right issue prices

Calculation:

Issue Prices Condition 1 Condition 2 Condition 3

Existing shares in numbers 600,000 600,000 600,000

Fund to be raised (A) 180,000 180,000 180,000

Suggested right issue prices (B) 1.80 1.60 1.40

Number of shares to be issued (A/B) £ 100,000 £ 112,500

128,571.43 or £

128,571

2. Theoretical ex rights price

Theoretical ex rights price (TERP) is the process of estimating price of shares which

company follow at the time of rights issues. Usually companies estimated weighted average price

per share or new as well as existing shares (Arifin, 2017). It will be done, in order to generate

more finance in the business in terms of capital and give preference to existing shareholders.

Director of Lexbel plc wanted to issue shares at three different prices, so calculation is based on

it and it mentioned below:

Calculation of theoretical ex rights price:

Particulars Condition 1 Condition 2 Condition 3

Recommended prices to issue shares £ 1.80 £ 1.60 £ 1.40

Fund to be increased £ 180,000 £ 180,000 £ 180,000

Number of shares required to issue £ 100,000 £ 112,500 £ 128,571

(b). Determine various aspects which mentioned below

1. Number of shared to be issued

Formula:

Number of Share Issued = Aggregate Funds to be elevated / right issue prices

Calculation:

Issue Prices Condition 1 Condition 2 Condition 3

Existing shares in numbers 600,000 600,000 600,000

Fund to be raised (A) 180,000 180,000 180,000

Suggested right issue prices (B) 1.80 1.60 1.40

Number of shares to be issued (A/B) £ 100,000 £ 112,500

128,571.43 or £

128,571

2. Theoretical ex rights price

Theoretical ex rights price (TERP) is the process of estimating price of shares which

company follow at the time of rights issues. Usually companies estimated weighted average price

per share or new as well as existing shares (Arifin, 2017). It will be done, in order to generate

more finance in the business in terms of capital and give preference to existing shareholders.

Director of Lexbel plc wanted to issue shares at three different prices, so calculation is based on

it and it mentioned below:

Calculation of theoretical ex rights price:

Particulars Condition 1 Condition 2 Condition 3

Recommended prices to issue shares £ 1.80 £ 1.60 £ 1.40

Fund to be increased £ 180,000 £ 180,000 £ 180,000

Number of shares required to issue £ 100,000 £ 112,500 £ 128,571

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

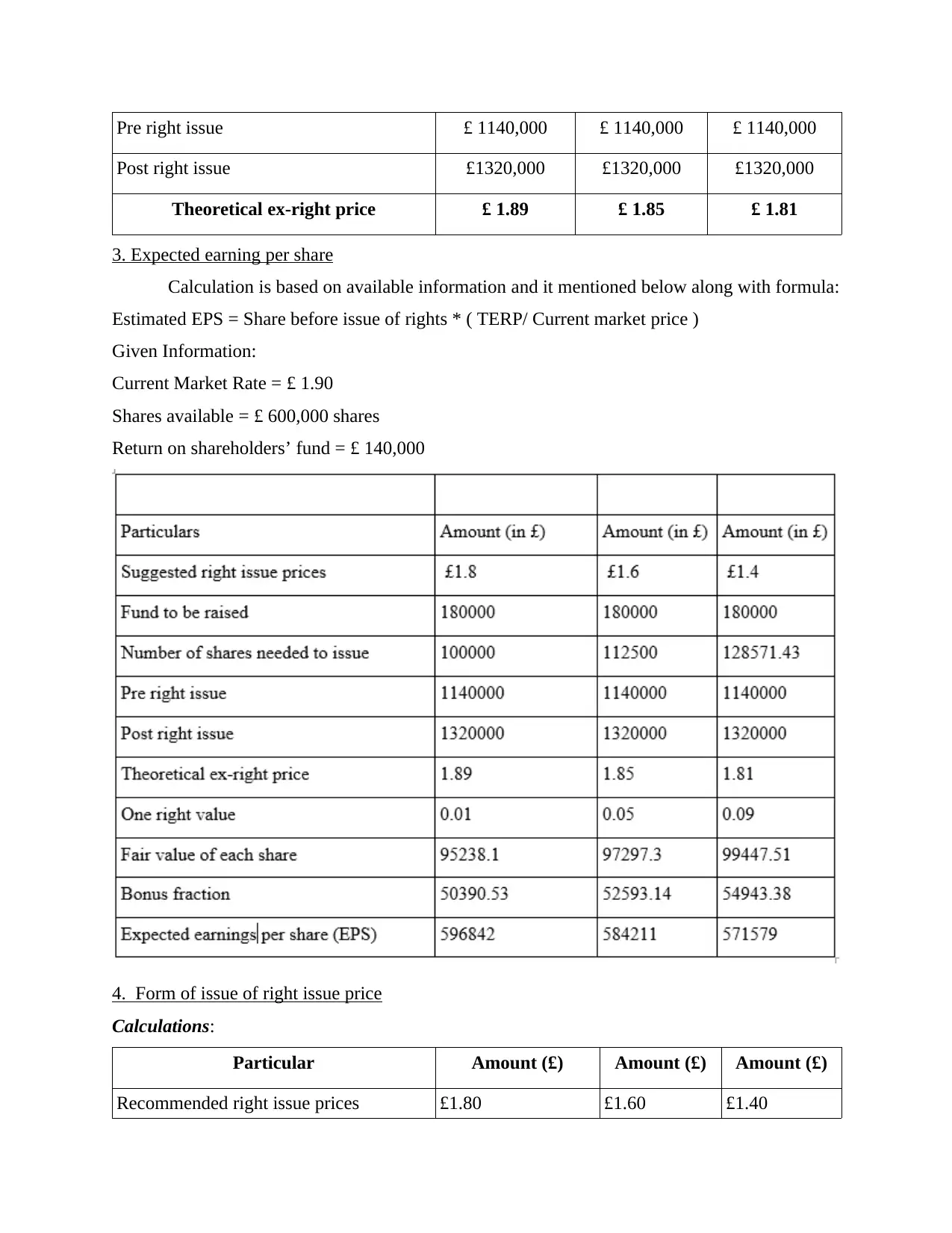

Pre right issue £ 1140,000 £ 1140,000 £ 1140,000

Post right issue £1320,000 £1320,000 £1320,000

Theoretical ex-right price £ 1.89 £ 1.85 £ 1.81

3. Expected earning per share

Calculation is based on available information and it mentioned below along with formula:

Estimated EPS = Share before issue of rights * ( TERP/ Current market price )

Given Information:

Current Market Rate = £ 1.90

Shares available = £ 600,000 shares

Return on shareholders’ fund = £ 140,000

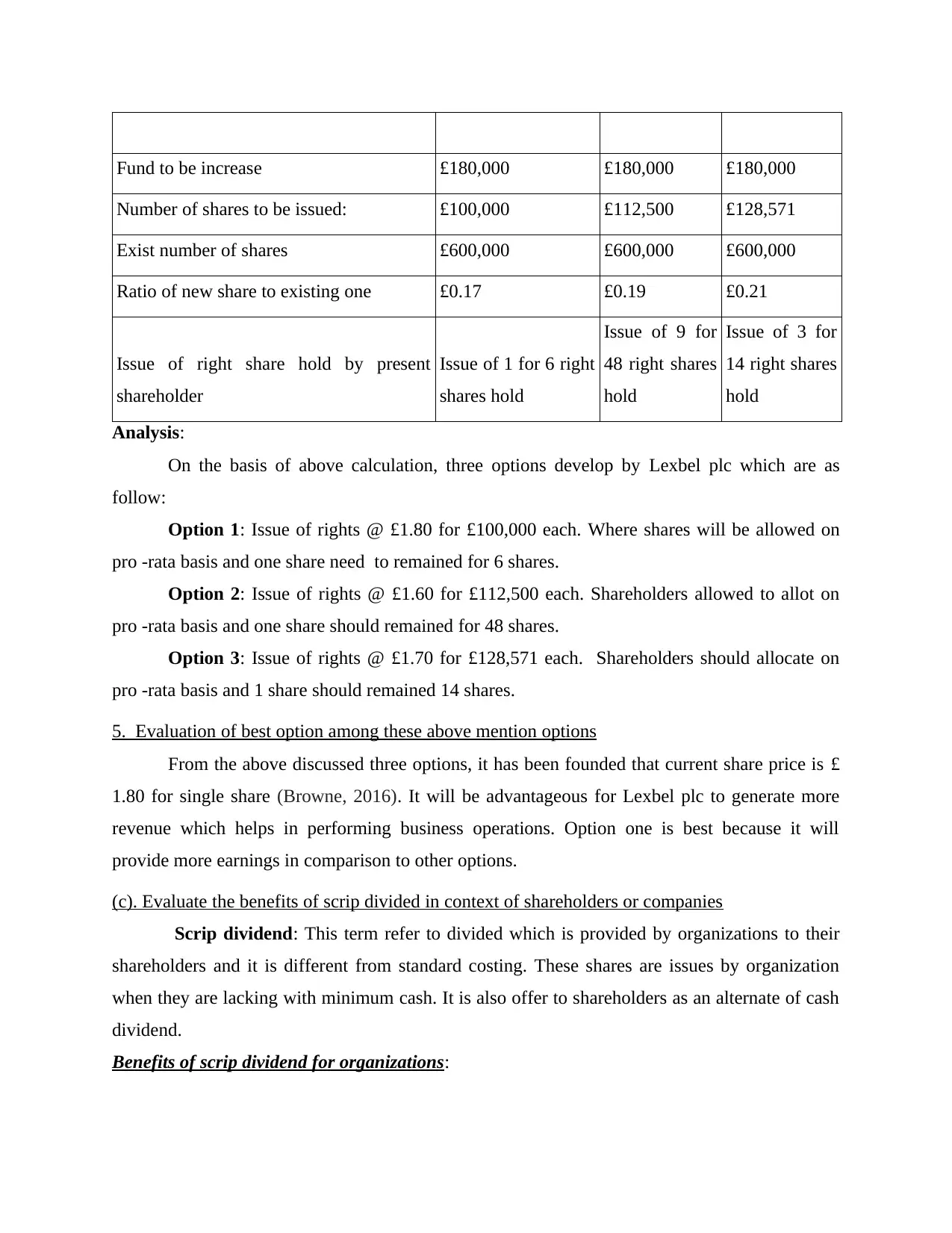

4. Form of issue of right issue price

Calculations:

Particular Amount (£) Amount (£) Amount (£)

Recommended right issue prices £1.80 £1.60 £1.40

Post right issue £1320,000 £1320,000 £1320,000

Theoretical ex-right price £ 1.89 £ 1.85 £ 1.81

3. Expected earning per share

Calculation is based on available information and it mentioned below along with formula:

Estimated EPS = Share before issue of rights * ( TERP/ Current market price )

Given Information:

Current Market Rate = £ 1.90

Shares available = £ 600,000 shares

Return on shareholders’ fund = £ 140,000

4. Form of issue of right issue price

Calculations:

Particular Amount (£) Amount (£) Amount (£)

Recommended right issue prices £1.80 £1.60 £1.40

Fund to be increase £180,000 £180,000 £180,000

Number of shares to be issued: £100,000 £112,500 £128,571

Exist number of shares £600,000 £600,000 £600,000

Ratio of new share to existing one £0.17 £0.19 £0.21

Issue of right share hold by present

shareholder

Issue of 1 for 6 right

shares hold

Issue of 9 for

48 right shares

hold

Issue of 3 for

14 right shares

hold

Analysis:

On the basis of above calculation, three options develop by Lexbel plc which are as

follow:

Option 1: Issue of rights @ £1.80 for £100,000 each. Where shares will be allowed on

pro -rata basis and one share need to remained for 6 shares.

Option 2: Issue of rights @ £1.60 for £112,500 each. Shareholders allowed to allot on

pro -rata basis and one share should remained for 48 shares.

Option 3: Issue of rights @ £1.70 for £128,571 each. Shareholders should allocate on

pro -rata basis and 1 share should remained 14 shares.

5. Evaluation of best option among these above mention options

From the above discussed three options, it has been founded that current share price is £

1.80 for single share (Browne, 2016). It will be advantageous for Lexbel plc to generate more

revenue which helps in performing business operations. Option one is best because it will

provide more earnings in comparison to other options.

(c). Evaluate the benefits of scrip divided in context of shareholders or companies

Scrip dividend: This term refer to divided which is provided by organizations to their

shareholders and it is different from standard costing. These shares are issues by organization

when they are lacking with minimum cash. It is also offer to shareholders as an alternate of cash

dividend.

Benefits of scrip dividend for organizations:

Number of shares to be issued: £100,000 £112,500 £128,571

Exist number of shares £600,000 £600,000 £600,000

Ratio of new share to existing one £0.17 £0.19 £0.21

Issue of right share hold by present

shareholder

Issue of 1 for 6 right

shares hold

Issue of 9 for

48 right shares

hold

Issue of 3 for

14 right shares

hold

Analysis:

On the basis of above calculation, three options develop by Lexbel plc which are as

follow:

Option 1: Issue of rights @ £1.80 for £100,000 each. Where shares will be allowed on

pro -rata basis and one share need to remained for 6 shares.

Option 2: Issue of rights @ £1.60 for £112,500 each. Shareholders allowed to allot on

pro -rata basis and one share should remained for 48 shares.

Option 3: Issue of rights @ £1.70 for £128,571 each. Shareholders should allocate on

pro -rata basis and 1 share should remained 14 shares.

5. Evaluation of best option among these above mention options

From the above discussed three options, it has been founded that current share price is £

1.80 for single share (Browne, 2016). It will be advantageous for Lexbel plc to generate more

revenue which helps in performing business operations. Option one is best because it will

provide more earnings in comparison to other options.

(c). Evaluate the benefits of scrip divided in context of shareholders or companies

Scrip dividend: This term refer to divided which is provided by organizations to their

shareholders and it is different from standard costing. These shares are issues by organization

when they are lacking with minimum cash. It is also offer to shareholders as an alternate of cash

dividend.

Benefits of scrip dividend for organizations:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is beneficial for organizations to maintain their cash balance to perform their

operational activities.

These shares issued by those companies which have strong brand value or creditability so

they introduce shares because they are unable to pay cash to their stakeholders.

It is one of the essential source of finance which help business to generate money except

of cash dividend.

At the time of issuing scrip dividends, it will lead to maximise equity and gearing

conditions of entities. Company pay scrip dividend at low rate of interest which will not impact share price of

companies.

Advantages of scrip dividend for shareholders:

One of the essential advantage of scrip dividend is that, shareholders can save their

money from tax.

It helps those shareholders who wanted to maximise their ownership in the organization.

Stakeholders can buy these shares or make their position more stronger.

Scrip dividend is beneficial for shareholders to save their transactions cost.

It also provide benefits in financial aspects because of time interval among cash dividend.

With the help of it, shareholders can maximise number of equity shares without paying

any additional charges for fix ownership. Such as buying charges, commission etc.

Question 3. Investment Appraisal Techniques

In this project report, different types of calculations required to done in order to measure

attractiveness of any investment (Collum, Menachemi and Sen, 2016). With the help of

investment appraisal techniques, selected company that is Lovewell Limited evaluate that, they

should invest in new machinery or not. Below mention calculation are as follow:

(a). By using investment appraisal techniques, calculate below mention following methods

1. Payback period

Payback Period refers to the duration absorbed by a firm to recover the initial cost of an

investment. The project completed in least years will be given more importance. It is the time

consumed to reach the Break-Even-Point (demand equivalent to supply). It is usually used in

operational activities.

These shares issued by those companies which have strong brand value or creditability so

they introduce shares because they are unable to pay cash to their stakeholders.

It is one of the essential source of finance which help business to generate money except

of cash dividend.

At the time of issuing scrip dividends, it will lead to maximise equity and gearing

conditions of entities. Company pay scrip dividend at low rate of interest which will not impact share price of

companies.

Advantages of scrip dividend for shareholders:

One of the essential advantage of scrip dividend is that, shareholders can save their

money from tax.

It helps those shareholders who wanted to maximise their ownership in the organization.

Stakeholders can buy these shares or make their position more stronger.

Scrip dividend is beneficial for shareholders to save their transactions cost.

It also provide benefits in financial aspects because of time interval among cash dividend.

With the help of it, shareholders can maximise number of equity shares without paying

any additional charges for fix ownership. Such as buying charges, commission etc.

Question 3. Investment Appraisal Techniques

In this project report, different types of calculations required to done in order to measure

attractiveness of any investment (Collum, Menachemi and Sen, 2016). With the help of

investment appraisal techniques, selected company that is Lovewell Limited evaluate that, they

should invest in new machinery or not. Below mention calculation are as follow:

(a). By using investment appraisal techniques, calculate below mention following methods

1. Payback period

Payback Period refers to the duration absorbed by a firm to recover the initial cost of an

investment. The project completed in least years will be given more importance. It is the time

consumed to reach the Break-Even-Point (demand equivalent to supply). It is usually used in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial and Capital Budgeting. It is the calculation for large number of years to convert the

investment into capital.

The formula to calculate the payback period depend either on an even cash inflow or an

uneven cash inflow.

Payback Period (Even Cash Inflow) : Initial Investment / Net Cash Flow per Period

Payback Period ( Uneven Cash Inflow) : A + B / C

Where ,

A = Previous year negative cumulation cash inflow number.

B = Absolute value (without negative sign) for cumulative net cash flow at end of period A.

C = Total cash inflow during the following period A.

Calculations:

Payback period = £ 275000 / £ 72500

= 3.79 years

It is observed that, company can recover their new machinery cost within 4 years because

payback period is 3.79 years. Low recovery period is beneficial for Lovewell limited and

machinery has six year life. Company should invest to purchase new machinery to boost their

production which further helps in increasing profit margin.

Working Notes*:

Actual inflow of cash = Cash inflow – Annual Outflow

= £ 85,000 – £ 12,500

= £ 72,500

Initial Investment = £ 275000

2. Accounting Rate of Reruns

The Accounting Rate of Return is also termed as Average Rate of Return (ARR). This

ratio does not use the concept of time value of money. The ARR is a formula used to make

Capital Budgeting decisions (Hall and Antonopoulos, 2017). ARR divides the average revenue

from company's initial investment to generate return that can be expected over the lifetime of

related projects. The ARR is helpful in determining the Annual Percentage Rate of Return of a

project. It can be used in multiple projects, as it provides the expected rate of return from each

project.

Formula:

investment into capital.

The formula to calculate the payback period depend either on an even cash inflow or an

uneven cash inflow.

Payback Period (Even Cash Inflow) : Initial Investment / Net Cash Flow per Period

Payback Period ( Uneven Cash Inflow) : A + B / C

Where ,

A = Previous year negative cumulation cash inflow number.

B = Absolute value (without negative sign) for cumulative net cash flow at end of period A.

C = Total cash inflow during the following period A.

Calculations:

Payback period = £ 275000 / £ 72500

= 3.79 years

It is observed that, company can recover their new machinery cost within 4 years because

payback period is 3.79 years. Low recovery period is beneficial for Lovewell limited and

machinery has six year life. Company should invest to purchase new machinery to boost their

production which further helps in increasing profit margin.

Working Notes*:

Actual inflow of cash = Cash inflow – Annual Outflow

= £ 85,000 – £ 12,500

= £ 72,500

Initial Investment = £ 275000

2. Accounting Rate of Reruns

The Accounting Rate of Return is also termed as Average Rate of Return (ARR). This

ratio does not use the concept of time value of money. The ARR is a formula used to make

Capital Budgeting decisions (Hall and Antonopoulos, 2017). ARR divides the average revenue

from company's initial investment to generate return that can be expected over the lifetime of

related projects. The ARR is helpful in determining the Annual Percentage Rate of Return of a

project. It can be used in multiple projects, as it provides the expected rate of return from each

project.

Formula:

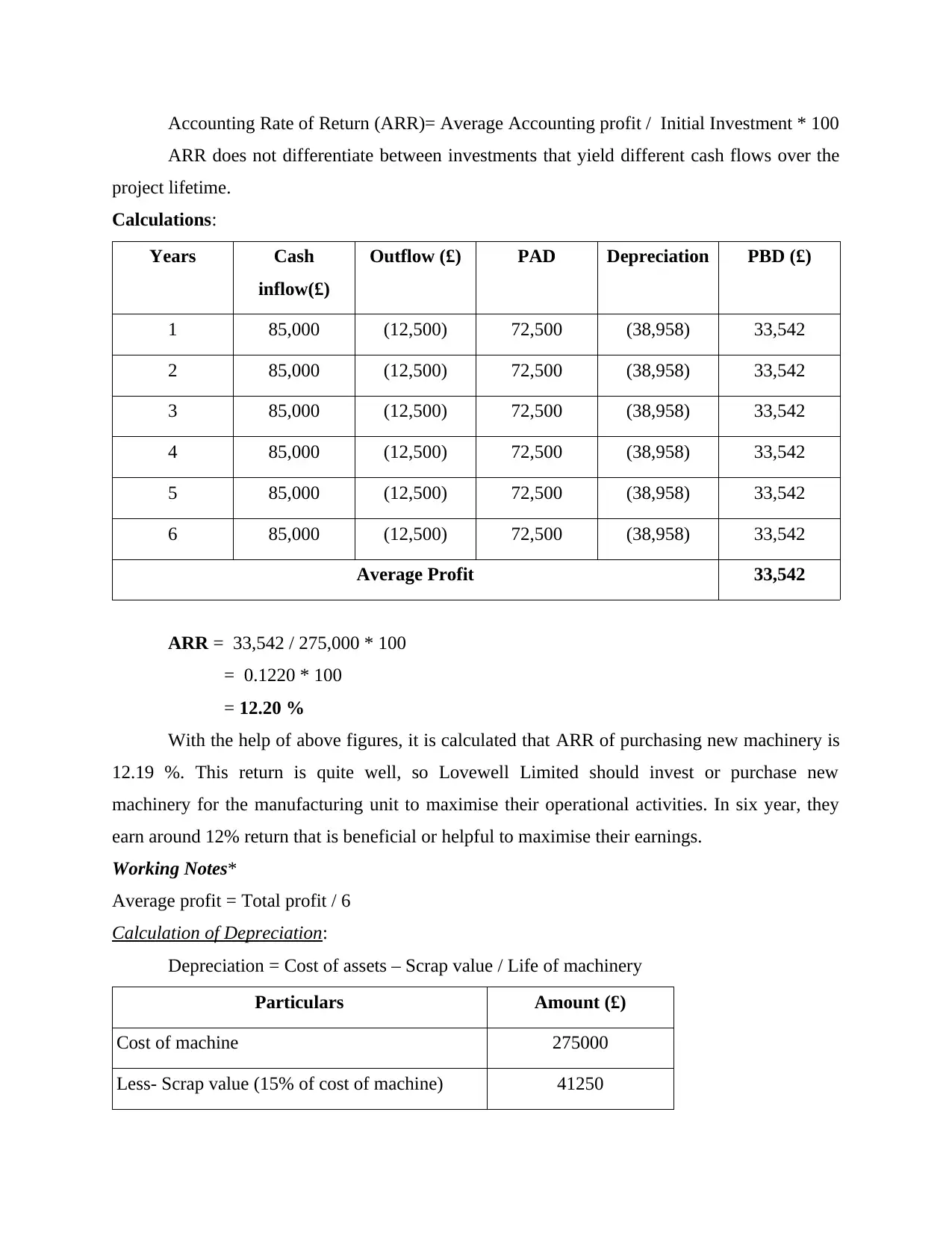

Accounting Rate of Return (ARR)= Average Accounting profit / Initial Investment * 100

ARR does not differentiate between investments that yield different cash flows over the

project lifetime.

Calculations:

Years Cash

inflow(£)

Outflow (£) PAD Depreciation PBD (£)

1 85,000 (12,500) 72,500 (38,958) 33,542

2 85,000 (12,500) 72,500 (38,958) 33,542

3 85,000 (12,500) 72,500 (38,958) 33,542

4 85,000 (12,500) 72,500 (38,958) 33,542

5 85,000 (12,500) 72,500 (38,958) 33,542

6 85,000 (12,500) 72,500 (38,958) 33,542

Average Profit 33,542

ARR = 33,542 / 275,000 * 100

= 0.1220 * 100

= 12.20 %

With the help of above figures, it is calculated that ARR of purchasing new machinery is

12.19 %. This return is quite well, so Lovewell Limited should invest or purchase new

machinery for the manufacturing unit to maximise their operational activities. In six year, they

earn around 12% return that is beneficial or helpful to maximise their earnings.

Working Notes*

Average profit = Total profit / 6

Calculation of Depreciation:

Depreciation = Cost of assets – Scrap value / Life of machinery

Particulars Amount (£)

Cost of machine 275000

Less- Scrap value (15% of cost of machine) 41250

ARR does not differentiate between investments that yield different cash flows over the

project lifetime.

Calculations:

Years Cash

inflow(£)

Outflow (£) PAD Depreciation PBD (£)

1 85,000 (12,500) 72,500 (38,958) 33,542

2 85,000 (12,500) 72,500 (38,958) 33,542

3 85,000 (12,500) 72,500 (38,958) 33,542

4 85,000 (12,500) 72,500 (38,958) 33,542

5 85,000 (12,500) 72,500 (38,958) 33,542

6 85,000 (12,500) 72,500 (38,958) 33,542

Average Profit 33,542

ARR = 33,542 / 275,000 * 100

= 0.1220 * 100

= 12.20 %

With the help of above figures, it is calculated that ARR of purchasing new machinery is

12.19 %. This return is quite well, so Lovewell Limited should invest or purchase new

machinery for the manufacturing unit to maximise their operational activities. In six year, they

earn around 12% return that is beneficial or helpful to maximise their earnings.

Working Notes*

Average profit = Total profit / 6

Calculation of Depreciation:

Depreciation = Cost of assets – Scrap value / Life of machinery

Particulars Amount (£)

Cost of machine 275000

Less- Scrap value (15% of cost of machine) 41250

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

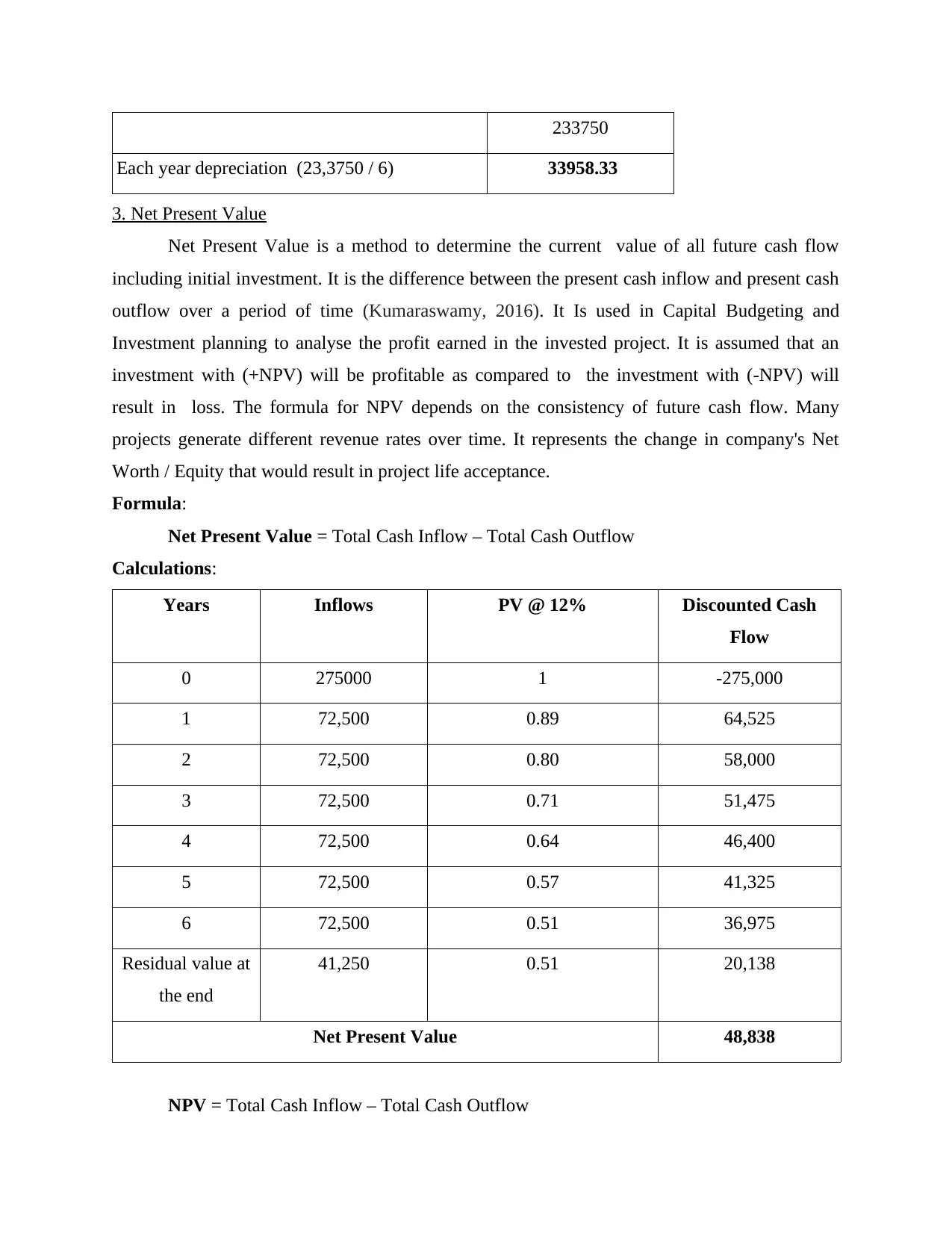

233750

Each year depreciation (23,3750 / 6) 33958.33

3. Net Present Value

Net Present Value is a method to determine the current value of all future cash flow

including initial investment. It is the difference between the present cash inflow and present cash

outflow over a period of time (Kumaraswamy, 2016). It Is used in Capital Budgeting and

Investment planning to analyse the profit earned in the invested project. It is assumed that an

investment with (+NPV) will be profitable as compared to the investment with (-NPV) will

result in loss. The formula for NPV depends on the consistency of future cash flow. Many

projects generate different revenue rates over time. It represents the change in company's Net

Worth / Equity that would result in project life acceptance.

Formula:

Net Present Value = Total Cash Inflow – Total Cash Outflow

Calculations:

Years Inflows PV @ 12% Discounted Cash

Flow

0 275000 1 -275,000

1 72,500 0.89 64,525

2 72,500 0.80 58,000

3 72,500 0.71 51,475

4 72,500 0.64 46,400

5 72,500 0.57 41,325

6 72,500 0.51 36,975

Residual value at

the end

41,250 0.51 20,138

Net Present Value 48,838

NPV = Total Cash Inflow – Total Cash Outflow

Each year depreciation (23,3750 / 6) 33958.33

3. Net Present Value

Net Present Value is a method to determine the current value of all future cash flow

including initial investment. It is the difference between the present cash inflow and present cash

outflow over a period of time (Kumaraswamy, 2016). It Is used in Capital Budgeting and

Investment planning to analyse the profit earned in the invested project. It is assumed that an

investment with (+NPV) will be profitable as compared to the investment with (-NPV) will

result in loss. The formula for NPV depends on the consistency of future cash flow. Many

projects generate different revenue rates over time. It represents the change in company's Net

Worth / Equity that would result in project life acceptance.

Formula:

Net Present Value = Total Cash Inflow – Total Cash Outflow

Calculations:

Years Inflows PV @ 12% Discounted Cash

Flow

0 275000 1 -275,000

1 72,500 0.89 64,525

2 72,500 0.80 58,000

3 72,500 0.71 51,475

4 72,500 0.64 46,400

5 72,500 0.57 41,325

6 72,500 0.51 36,975

Residual value at

the end

41,250 0.51 20,138

Net Present Value 48,838

NPV = Total Cash Inflow – Total Cash Outflow

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 318,838- 275,000

= 43,838

Above calculation shows that, NPV of new machinery is £ 43,838 which indicate that,

investment will be beneficial as well as profitable for Lovewell Limited. It will further helps in

enhancing efficiency or effectiveness which improve overall production or profit margin.

Positive NPV selected to negative will rejected because in future, it will not advantageous.

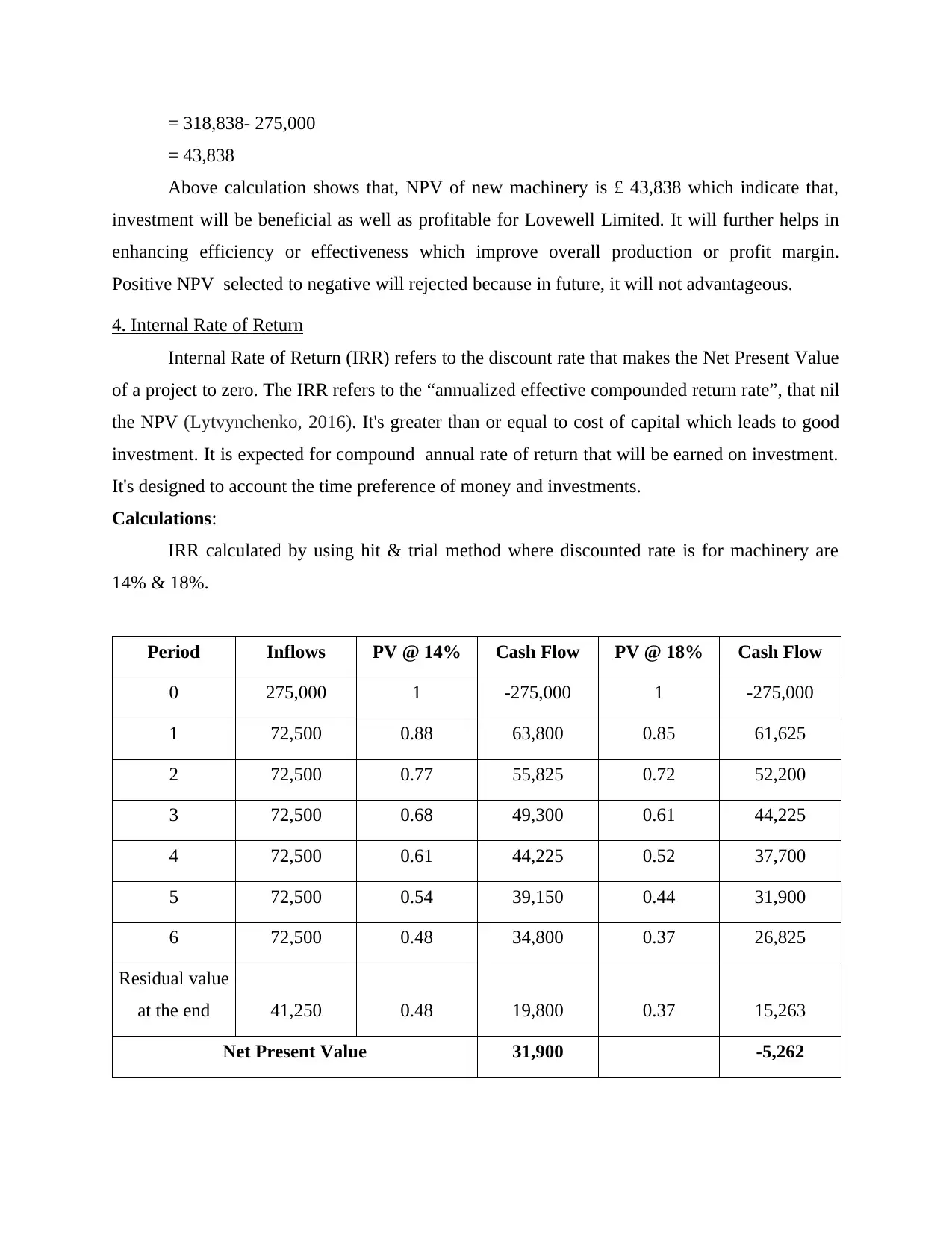

4. Internal Rate of Return

Internal Rate of Return (IRR) refers to the discount rate that makes the Net Present Value

of a project to zero. The IRR refers to the “annualized effective compounded return rate”, that nil

the NPV (Lytvynchenko, 2016). It's greater than or equal to cost of capital which leads to good

investment. It is expected for compound annual rate of return that will be earned on investment.

It's designed to account the time preference of money and investments.

Calculations:

IRR calculated by using hit & trial method where discounted rate is for machinery are

14% & 18%.

Period Inflows PV @ 14% Cash Flow PV @ 18% Cash Flow

0 275,000 1 -275,000 1 -275,000

1 72,500 0.88 63,800 0.85 61,625

2 72,500 0.77 55,825 0.72 52,200

3 72,500 0.68 49,300 0.61 44,225

4 72,500 0.61 44,225 0.52 37,700

5 72,500 0.54 39,150 0.44 31,900

6 72,500 0.48 34,800 0.37 26,825

Residual value

at the end 41,250 0.48 19,800 0.37 15,263

Net Present Value 31,900 -5,262

= 43,838

Above calculation shows that, NPV of new machinery is £ 43,838 which indicate that,

investment will be beneficial as well as profitable for Lovewell Limited. It will further helps in

enhancing efficiency or effectiveness which improve overall production or profit margin.

Positive NPV selected to negative will rejected because in future, it will not advantageous.

4. Internal Rate of Return

Internal Rate of Return (IRR) refers to the discount rate that makes the Net Present Value

of a project to zero. The IRR refers to the “annualized effective compounded return rate”, that nil

the NPV (Lytvynchenko, 2016). It's greater than or equal to cost of capital which leads to good

investment. It is expected for compound annual rate of return that will be earned on investment.

It's designed to account the time preference of money and investments.

Calculations:

IRR calculated by using hit & trial method where discounted rate is for machinery are

14% & 18%.

Period Inflows PV @ 14% Cash Flow PV @ 18% Cash Flow

0 275,000 1 -275,000 1 -275,000

1 72,500 0.88 63,800 0.85 61,625

2 72,500 0.77 55,825 0.72 52,200

3 72,500 0.68 49,300 0.61 44,225

4 72,500 0.61 44,225 0.52 37,700

5 72,500 0.54 39,150 0.44 31,900

6 72,500 0.48 34,800 0.37 26,825

Residual value

at the end 41,250 0.48 19,800 0.37 15,263

Net Present Value 31,900 -5,262

IRR = 14 + { 31900 / 31900 - (−5262) } * ( 18-14 )

= 14 + { 31900 / 37162 } * 4

= 17.43 %.

From the above calculation it has been analysed that IRR of new machinery is 17.43 %

that is beneficial for Lovewell Limited. Because managers will select projects on the basis of

higher returns in comparison to other options.

(b). Critically evaluate benefits or limitations of different investment appraisal techniques

Payback period:

Benefits: Payback period is one of the simple method of investment appraisal to identify

that project is beneficial or profitable for company or not. With the help of this method,

managers can select best portfolio to invest. Such as low recovery period will be going to select

because it help company to recover initial investment more faster.

Limitations: At the time of making decisions, managers will reject negative NPV

because it will not profitable at all (Mwangi, Kiarie and Kiai, 2016). This method does not

consider time value of money and after that, if any project have same cash flow than further

decisions will be based on minimum recovery time.

Accounting rate of return:

Benefits: ARR help managers to make decisions regarding their investments. Higher

returns are beneficial as well as profitable for company. So before making any decisions,

management calculate ARR of projects select most suitable one. This method consider

accounting value which is often consider by managers in decision making process.

Limitations: Average rate of return ignore cash flow of portfolio that is based on

accounting profit and further they calculate by using average profit. It will further impact various

practices that required to manage. In this investment appraisal techniques, time value of money

ignore which influence as well as impact entire result or profitability of project.

Net present value:

Benefits: Most of organizations follow NPV to evaluate their investment and identify that

company should invest in this project or not. Positive value of NPV selected and negative will be

reject because invest in such project is not beneficial for company. This technique of investment

appraisal consider time value of money which generate more opportunities in front of

organizations. It is helpful for managers to make their decisions on the basis of NPV value.

= 14 + { 31900 / 37162 } * 4

= 17.43 %.

From the above calculation it has been analysed that IRR of new machinery is 17.43 %

that is beneficial for Lovewell Limited. Because managers will select projects on the basis of

higher returns in comparison to other options.

(b). Critically evaluate benefits or limitations of different investment appraisal techniques

Payback period:

Benefits: Payback period is one of the simple method of investment appraisal to identify

that project is beneficial or profitable for company or not. With the help of this method,

managers can select best portfolio to invest. Such as low recovery period will be going to select

because it help company to recover initial investment more faster.

Limitations: At the time of making decisions, managers will reject negative NPV

because it will not profitable at all (Mwangi, Kiarie and Kiai, 2016). This method does not

consider time value of money and after that, if any project have same cash flow than further

decisions will be based on minimum recovery time.

Accounting rate of return:

Benefits: ARR help managers to make decisions regarding their investments. Higher

returns are beneficial as well as profitable for company. So before making any decisions,

management calculate ARR of projects select most suitable one. This method consider

accounting value which is often consider by managers in decision making process.

Limitations: Average rate of return ignore cash flow of portfolio that is based on

accounting profit and further they calculate by using average profit. It will further impact various

practices that required to manage. In this investment appraisal techniques, time value of money

ignore which influence as well as impact entire result or profitability of project.

Net present value:

Benefits: Most of organizations follow NPV to evaluate their investment and identify that

company should invest in this project or not. Positive value of NPV selected and negative will be

reject because invest in such project is not beneficial for company. This technique of investment

appraisal consider time value of money which generate more opportunities in front of

organizations. It is helpful for managers to make their decisions on the basis of NPV value.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.