Financial Management Report: Financial Analysis and Valuation Methods

VerifiedAdded on 2023/01/07

|14

|3955

|48

Report

AI Summary

This report delves into the realm of financial management, examining critical concepts like business valuation, mergers and acquisitions, and investment appraisal techniques. It begins with an introduction to financial management, emphasizing its role in controlling a firm's financial dimensions and ensuring efficient allocation of capital. The report then analyzes two key questions: firstly, it assesses the valuation of Trojan PLC, considering the price-earnings ratio, dividend valuation model, and discounted cash flow method, and it explores the merits and demerits of each approach. Secondly, it evaluates investment appraisal techniques, including the payback period, accounting rate of return, and net present value, providing recommendations for Love-well plc's equipment purchase. The report concludes by synthesizing the findings and offering strategic recommendations based on the analysis.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

QUESTIONS...................................................................................................................................3

Question 2 (Mergers and Takeovers).....................................................................................3

Question 3: Investment appraisal techniques.........................................................................7

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

QUESTIONS...................................................................................................................................3

Question 2 (Mergers and Takeovers).....................................................................................3

Question 3: Investment appraisal techniques.........................................................................7

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial management can usually be interpreted as a type of operation related to a firm’s

financial dimension being effectively controlled (Chandra, 2020). Numerous types of operations

are handled within financial control like productivity, revenue, expense and review of decision

making on unproductive operation. This really is the financial managers' responsibility to make

good use of entire financial capital accessible by making sufficient allocations that help to reach

the results. In present time, company focuses to have effective financial management so that

losses can be removed and business operation can be expanded.

The goal of this project is to understand various types of financial terminology and

concepts such as business valuation for sale, project review under methodology of investment

evaluation. The study includes two issues focused on theoretical and realistic implementation of

merger & acquisition and also various approaches for evaluating investment.

QUESTIONS

There are 3 sections in the design proposal and only 2 are picked out of these questions

(numbered two and three). Underneath, these problems were answered in depth in such ways as:

Question 2 (Mergers and Takeovers)

Overview: This reasoning is based on financial analysis of respective company with

acquisition goal. According to the details provided, Aztec plc will assume over Trojan plc with

in forthcoming span of time. Comprehensive explanation of Trojan plc was already performed

for this reason such that Aztec plc general manager can decide to either buy this business or not.

(a). Price earnings ratio- Share price / Earnings per share

In try to determine out the significance of the proportion of stock profits, data regarding

stock market as well as EPS should be available. According to the summary, following data is

available, for example:

Price of each share £2.05

Number of share outstanding 147 Million

Net income £40.4 Million

Calculation of EPS:

EPS = Net income / Number of share outstanding

= £40.4 Million / 147 Million

Financial management can usually be interpreted as a type of operation related to a firm’s

financial dimension being effectively controlled (Chandra, 2020). Numerous types of operations

are handled within financial control like productivity, revenue, expense and review of decision

making on unproductive operation. This really is the financial managers' responsibility to make

good use of entire financial capital accessible by making sufficient allocations that help to reach

the results. In present time, company focuses to have effective financial management so that

losses can be removed and business operation can be expanded.

The goal of this project is to understand various types of financial terminology and

concepts such as business valuation for sale, project review under methodology of investment

evaluation. The study includes two issues focused on theoretical and realistic implementation of

merger & acquisition and also various approaches for evaluating investment.

QUESTIONS

There are 3 sections in the design proposal and only 2 are picked out of these questions

(numbered two and three). Underneath, these problems were answered in depth in such ways as:

Question 2 (Mergers and Takeovers)

Overview: This reasoning is based on financial analysis of respective company with

acquisition goal. According to the details provided, Aztec plc will assume over Trojan plc with

in forthcoming span of time. Comprehensive explanation of Trojan plc was already performed

for this reason such that Aztec plc general manager can decide to either buy this business or not.

(a). Price earnings ratio- Share price / Earnings per share

In try to determine out the significance of the proportion of stock profits, data regarding

stock market as well as EPS should be available. According to the summary, following data is

available, for example:

Price of each share £2.05

Number of share outstanding 147 Million

Net income £40.4 Million

Calculation of EPS:

EPS = Net income / Number of share outstanding

= £40.4 Million / 147 Million

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= £0.27

Valuation from both EPS and shares cost has been derived according to the above

section, hence the stock earnings ratio would be as follows:

Price earnings ratio= £2.05 / £0.27

= 7.59

Description: According to the price earnings ratio estimated above, Trojan plc can be seen to

produce suitable earnings through every share. The profits on each stock are roughly 0.27 pounds

whereas the worth of every other share is 2.05 pounds. Thus, it seems appropriate to buy Trojan

plc from Aztec plc at such a stock earnings ratio of 7.59.

(b) Dividend valuation model:

Under this process, appraisal is performed during the financial year in conjunction with

paying dividend. To implement this pattern there is an equation which is as follows:

D1 / (1 + k) + D2 / (1 + k) 2 + D3 / (1 + k) 3 + D4 / (1 + k) 4………….

This formula reads:

D1 corresponds to the dividend number earned in 1st year.

D2 applies to dividend number earned in the 2nd year.

D3 applies to dividend number earned in 3rd year.

D4 applies to dividend sums earned in 4th year.

K refers to the expected rate of return

Given data:

Amount of dividend paid in 1st year (D1) 10p

Amount of dividend paid in 2nd year (D2) 10.5p

Amount of dividend paid in 3rd year (D3) 11p

Amount of dividend paid in 4th year (D4) 12p

Predicted rate of return (K) 11%

Putting values in formula:

= 10p (1 + 11%) + 10.5p (1 + 11%)2 + 11p (1 + 11%)3 + 12p (1 + 11%)4

= 10 p (0.11) + 10.5p (0.11)2 + 11p (0.11)3 + 12p (0.11)4

= 11.1 + 10.5 (0.0121) + 11 (0.001331) + 12 (0.000146)

= 11.1 + 0.127 + 0.014 + 0.00175

= £11.24

Valuation from both EPS and shares cost has been derived according to the above

section, hence the stock earnings ratio would be as follows:

Price earnings ratio= £2.05 / £0.27

= 7.59

Description: According to the price earnings ratio estimated above, Trojan plc can be seen to

produce suitable earnings through every share. The profits on each stock are roughly 0.27 pounds

whereas the worth of every other share is 2.05 pounds. Thus, it seems appropriate to buy Trojan

plc from Aztec plc at such a stock earnings ratio of 7.59.

(b) Dividend valuation model:

Under this process, appraisal is performed during the financial year in conjunction with

paying dividend. To implement this pattern there is an equation which is as follows:

D1 / (1 + k) + D2 / (1 + k) 2 + D3 / (1 + k) 3 + D4 / (1 + k) 4………….

This formula reads:

D1 corresponds to the dividend number earned in 1st year.

D2 applies to dividend number earned in the 2nd year.

D3 applies to dividend number earned in 3rd year.

D4 applies to dividend sums earned in 4th year.

K refers to the expected rate of return

Given data:

Amount of dividend paid in 1st year (D1) 10p

Amount of dividend paid in 2nd year (D2) 10.5p

Amount of dividend paid in 3rd year (D3) 11p

Amount of dividend paid in 4th year (D4) 12p

Predicted rate of return (K) 11%

Putting values in formula:

= 10p (1 + 11%) + 10.5p (1 + 11%)2 + 11p (1 + 11%)3 + 12p (1 + 11%)4

= 10 p (0.11) + 10.5p (0.11)2 + 11p (0.11)3 + 12p (0.11)4

= 11.1 + 10.5 (0.0121) + 11 (0.001331) + 12 (0.000146)

= 11.1 + 0.127 + 0.014 + 0.00175

= £11.24

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: According to the dividend capitalization formula it can be observed that the

equity value of Trojan plc is about 11.24 pounds. It means that the results of each fiscal year, the

organization is willing to pay its creditors an appropriate amount of dividend. In the sense of

Trojan plc earlier, the distribution of last 4 years was used to figure out share interest.

(c) Discounted cash flow method

In this process the analysis is carried out in conjunction with the cash flows by calculating

average below:

CF1 / (1+r) 1 + CF2 / (1+r) 2 + CF n / (1+r) n

Given information:

r= 5%

Cash flow = 40.4 Million Pounds

Putting values in formula:

= £40.4/ (1+5%)

= £808

Interpretation: In accordance of above calculated value of share price under DCF method this

can be stated that Trojan plc is generating effective earnings. This value of share is computed in

accordance of cash flow for year one and cost of capital at 5%.

(d) Analysis of problems associated with above mentioned valuation methods.

Price earnings ratio: This can be interpreted as a process of ratio correlated with deciding the

relationship between the stock market as well as current share earnings (Itemgenova and

Sikveland, 2020). This form of ratio is critical for companies to accurately valuate a company in

terms of stock price. Basically, market analysis is conducted to determine the company's shares

price calculation. This measure is helpful in the sense of stakeholders and creditors, because they

can equate firm's existing market valuation with earnings. Using this proportion will lead to

problems or disadvantages that are discussed in this way below.

Demerits:

The key problem of using this formula would be that the loans/finance arrangement,

which contributes to inadequate valuation, is totally ignored.

equity value of Trojan plc is about 11.24 pounds. It means that the results of each fiscal year, the

organization is willing to pay its creditors an appropriate amount of dividend. In the sense of

Trojan plc earlier, the distribution of last 4 years was used to figure out share interest.

(c) Discounted cash flow method

In this process the analysis is carried out in conjunction with the cash flows by calculating

average below:

CF1 / (1+r) 1 + CF2 / (1+r) 2 + CF n / (1+r) n

Given information:

r= 5%

Cash flow = 40.4 Million Pounds

Putting values in formula:

= £40.4/ (1+5%)

= £808

Interpretation: In accordance of above calculated value of share price under DCF method this

can be stated that Trojan plc is generating effective earnings. This value of share is computed in

accordance of cash flow for year one and cost of capital at 5%.

(d) Analysis of problems associated with above mentioned valuation methods.

Price earnings ratio: This can be interpreted as a process of ratio correlated with deciding the

relationship between the stock market as well as current share earnings (Itemgenova and

Sikveland, 2020). This form of ratio is critical for companies to accurately valuate a company in

terms of stock price. Basically, market analysis is conducted to determine the company's shares

price calculation. This measure is helpful in the sense of stakeholders and creditors, because they

can equate firm's existing market valuation with earnings. Using this proportion will lead to

problems or disadvantages that are discussed in this way below.

Demerits:

The key problem of using this formula would be that the loans/finance arrangement,

which contributes to inadequate valuation, is totally ignored.

Consumers cannot gain statistics on EPS expansion of the industry by using this formula.

As a result, creditors do not consider it necessary to take investment decisions.

Moreover, it cannot be introduced in some companies that risk financial risks (Freihat

and Razaq, 2019). The explanation behind this problem would be that the price-earnings

ratio does not assess the risk of damages over the span of growth starting time.

Lastly, investor expectation can result in inflated share prices again for complete sector.

The explanation seems to be that stock prices can be under-estimated in comparison to

the Stock price only at time of contraction. Though earnings from firms may be measured

at the period of purchase according to the exchange rate of each given country. As a

result, the price-earnings ratio will be stronger.

Dividend valuation model: This valuation system is defined as a statistical concept that

specifies the stock is suitable for future payments of entire dividends. It is related to calculating

the market value of the company, irrespective of the current market situation that quantifies the

different dividend payment variables (Akben-Selçuk, 2020). If the valuation acquired by DVM is

greater than the foreign exchange rate then investment is considered under-priced and vice versa.

To calculate asset valuation under this formula, the dividend paid from past periods is

considered. As for the above estimation of the product, the dividend of the following four years

was used for appropriate consideration.

This system does have drawbacks that are discussed below:

The key disadvantage of the method is that it should be applied on the stocks of certain

businesses where they frequently pay dividends. Like small businesses, this concept

cannot be implemented as they don't allow dividend distributions. As a result, doing

proper valuation of micro businesses is impossible for big business.

Another downside to this approach is that it takes into account only one calculation

element which is dividend. Besides this, it disregards all other significant causes, like

consumer satisfaction, engagement and far more (Hendrawan and Rahayu, 2020). Thus

most businesses don't find full valuation and leads to massive loss.

In certain countries, businesses do not want to distribute dividends due to viewpoint of

tax gain. As a result, investors concentrate to invest money in figures of stock. In this

case the process above fails entirely.

As a result, creditors do not consider it necessary to take investment decisions.

Moreover, it cannot be introduced in some companies that risk financial risks (Freihat

and Razaq, 2019). The explanation behind this problem would be that the price-earnings

ratio does not assess the risk of damages over the span of growth starting time.

Lastly, investor expectation can result in inflated share prices again for complete sector.

The explanation seems to be that stock prices can be under-estimated in comparison to

the Stock price only at time of contraction. Though earnings from firms may be measured

at the period of purchase according to the exchange rate of each given country. As a

result, the price-earnings ratio will be stronger.

Dividend valuation model: This valuation system is defined as a statistical concept that

specifies the stock is suitable for future payments of entire dividends. It is related to calculating

the market value of the company, irrespective of the current market situation that quantifies the

different dividend payment variables (Akben-Selçuk, 2020). If the valuation acquired by DVM is

greater than the foreign exchange rate then investment is considered under-priced and vice versa.

To calculate asset valuation under this formula, the dividend paid from past periods is

considered. As for the above estimation of the product, the dividend of the following four years

was used for appropriate consideration.

This system does have drawbacks that are discussed below:

The key disadvantage of the method is that it should be applied on the stocks of certain

businesses where they frequently pay dividends. Like small businesses, this concept

cannot be implemented as they don't allow dividend distributions. As a result, doing

proper valuation of micro businesses is impossible for big business.

Another downside to this approach is that it takes into account only one calculation

element which is dividend. Besides this, it disregards all other significant causes, like

consumer satisfaction, engagement and far more (Hendrawan and Rahayu, 2020). Thus

most businesses don't find full valuation and leads to massive loss.

In certain countries, businesses do not want to distribute dividends due to viewpoint of

tax gain. As a result, investors concentrate to invest money in figures of stock. In this

case the process above fails entirely.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A selection of appropriate details will be required for the effective execution of this

template. Unless the evidence supplied is false, the effect may also be unreliable, that

may cause wrong business valuation.

Discounted method of cash flow: This is characterized as a type of approach in which a

company's value is dependent on the profitability of the given time period. Essentially, the main

purpose of this process is to assess the cash flow of the future time frame using details from

current fiscal years (Laitinen, 2019). One of the key advantages of this approach is in using by a

company's owners and creditors alike. It is because this approach is useful in supplying reliable

valuation-related information. Although, it does have other drawbacks such as:

The only downside of this approach is that with it a range of predictions is

rendered regarding capital expenses, the working capital including its upcoming weeks.

Therefore these expectations, relaying on this system is problematic for businesses.

On top of this, it is not appropriate for such construction ventures this are named for less

than a year. This should only be extended to initiatives that have been named for even

more than a year. This is just so since it can be costly and time-consuming for short-term

investment plans.

This technique's efficacy relies mostly on working capital supply for even more than

1 year. In the case of only about 2 years of working capital it cannot be considered for

valuation.

Recommendation to Aztec plc

On the basis of the above 3 valuation methods listed above, it could be proposed to the

management of Aztec plc must implement the Dividend income approach for Trojan plc market

value. The reasoning here seems to be that a thorough share valuation is conducted under DVM

which makes it easy for company owners to assess the financial a specific company. Although

there have been a number of pitfalls in the other of two approaches like price earnings ratio as

well as net present value (npv, making the valuation less successful. As well as these approaches,

they are only useful for evaluating profits and share value, rather than asset valuation.

Question 3: Investment appraisal techniques.

Overview: This issue is based on the use of different forms of investment assessment to

make the right decisions. According to the specified scenario, Love-well plc is preparing to

template. Unless the evidence supplied is false, the effect may also be unreliable, that

may cause wrong business valuation.

Discounted method of cash flow: This is characterized as a type of approach in which a

company's value is dependent on the profitability of the given time period. Essentially, the main

purpose of this process is to assess the cash flow of the future time frame using details from

current fiscal years (Laitinen, 2019). One of the key advantages of this approach is in using by a

company's owners and creditors alike. It is because this approach is useful in supplying reliable

valuation-related information. Although, it does have other drawbacks such as:

The only downside of this approach is that with it a range of predictions is

rendered regarding capital expenses, the working capital including its upcoming weeks.

Therefore these expectations, relaying on this system is problematic for businesses.

On top of this, it is not appropriate for such construction ventures this are named for less

than a year. This should only be extended to initiatives that have been named for even

more than a year. This is just so since it can be costly and time-consuming for short-term

investment plans.

This technique's efficacy relies mostly on working capital supply for even more than

1 year. In the case of only about 2 years of working capital it cannot be considered for

valuation.

Recommendation to Aztec plc

On the basis of the above 3 valuation methods listed above, it could be proposed to the

management of Aztec plc must implement the Dividend income approach for Trojan plc market

value. The reasoning here seems to be that a thorough share valuation is conducted under DVM

which makes it easy for company owners to assess the financial a specific company. Although

there have been a number of pitfalls in the other of two approaches like price earnings ratio as

well as net present value (npv, making the valuation less successful. As well as these approaches,

they are only useful for evaluating profits and share value, rather than asset valuation.

Question 3: Investment appraisal techniques.

Overview: This issue is based on the use of different forms of investment assessment to

make the right decisions. According to the specified scenario, Love-well plc is preparing to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

procure new equipment which will cost about 275,000 pounds. Without making investments in

this equipment, they need to use various approaches to better test the equipment.

Computation through different forms of risk appraisal approaches, alongside suggestions:

(A) Payback period: there have been 2 kinds of equations listed below under such a technique:

Payback period: Initial spending / working capital (whenever the cash flow is equal)

Payback period: Year since investment return + sum to be recovered / next month’s working

capital (so if cash flow is unbalanced)

Given data:

Investment £275000

Cash inflow (for six years) £85000

Cash outflow (for six years) £12500

The above data shows that the working capital is equal over all 6 years, so equation

should be:

Cash flow = Cash inflow - cash outflow

= £85000 - £12500

= £72500

Hence, payback period= £275000/£72500

= 3.79 years

Recommendation: According to the previous estimate, new equipment expenses should be

covered in about 3.79 years. The equipment which existence is about 6 years and whose expense

would be paid in nearly half decades of whole life. Love-well plc will then purchase this new

equipment under repayment term in compliance with the estimated result.

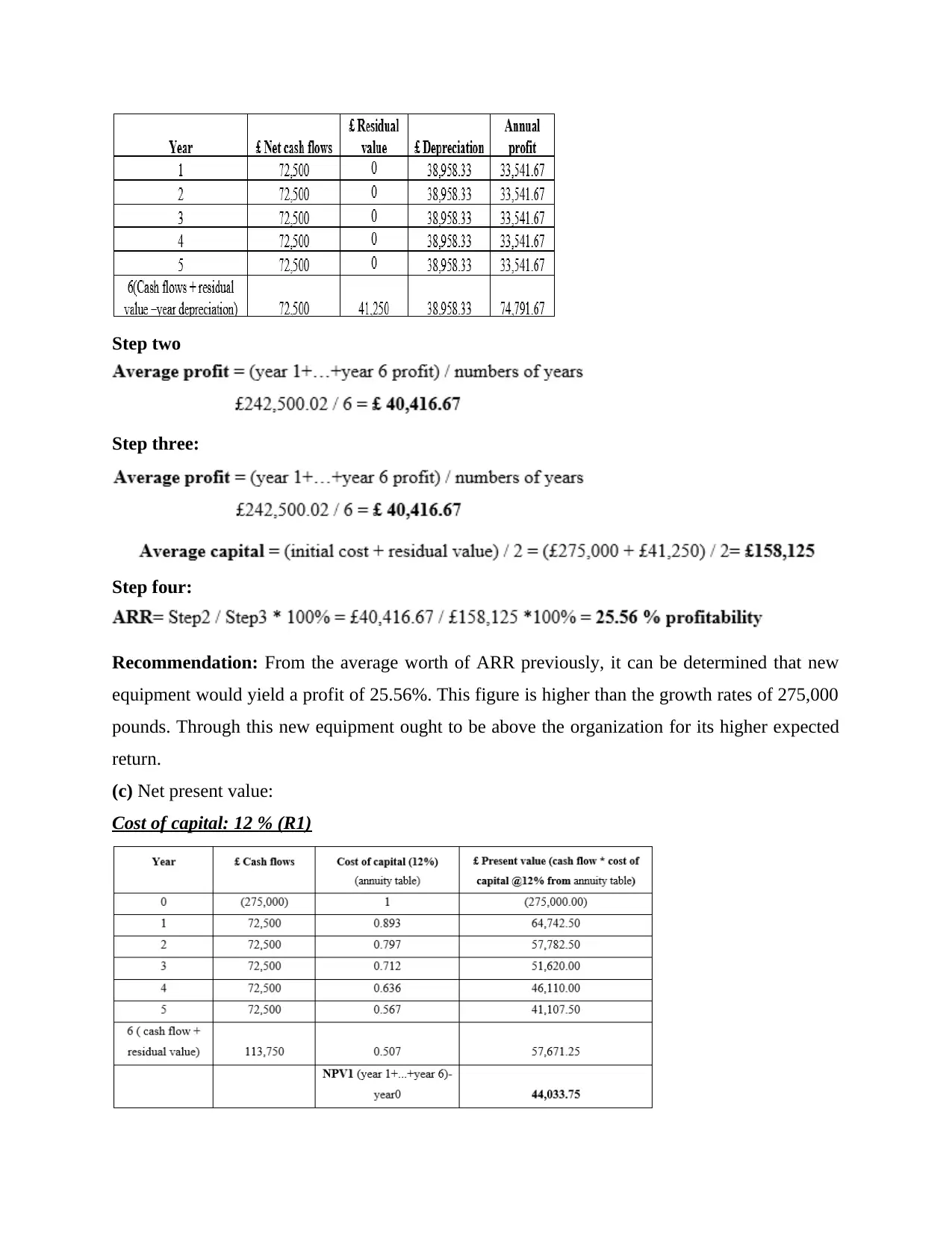

(b) Accounting rate of return:

Given information-

Step one:

this equipment, they need to use various approaches to better test the equipment.

Computation through different forms of risk appraisal approaches, alongside suggestions:

(A) Payback period: there have been 2 kinds of equations listed below under such a technique:

Payback period: Initial spending / working capital (whenever the cash flow is equal)

Payback period: Year since investment return + sum to be recovered / next month’s working

capital (so if cash flow is unbalanced)

Given data:

Investment £275000

Cash inflow (for six years) £85000

Cash outflow (for six years) £12500

The above data shows that the working capital is equal over all 6 years, so equation

should be:

Cash flow = Cash inflow - cash outflow

= £85000 - £12500

= £72500

Hence, payback period= £275000/£72500

= 3.79 years

Recommendation: According to the previous estimate, new equipment expenses should be

covered in about 3.79 years. The equipment which existence is about 6 years and whose expense

would be paid in nearly half decades of whole life. Love-well plc will then purchase this new

equipment under repayment term in compliance with the estimated result.

(b) Accounting rate of return:

Given information-

Step one:

Step two

Step three:

Step four:

Recommendation: From the average worth of ARR previously, it can be determined that new

equipment would yield a profit of 25.56%. This figure is higher than the growth rates of 275,000

pounds. Through this new equipment ought to be above the organization for its higher expected

return.

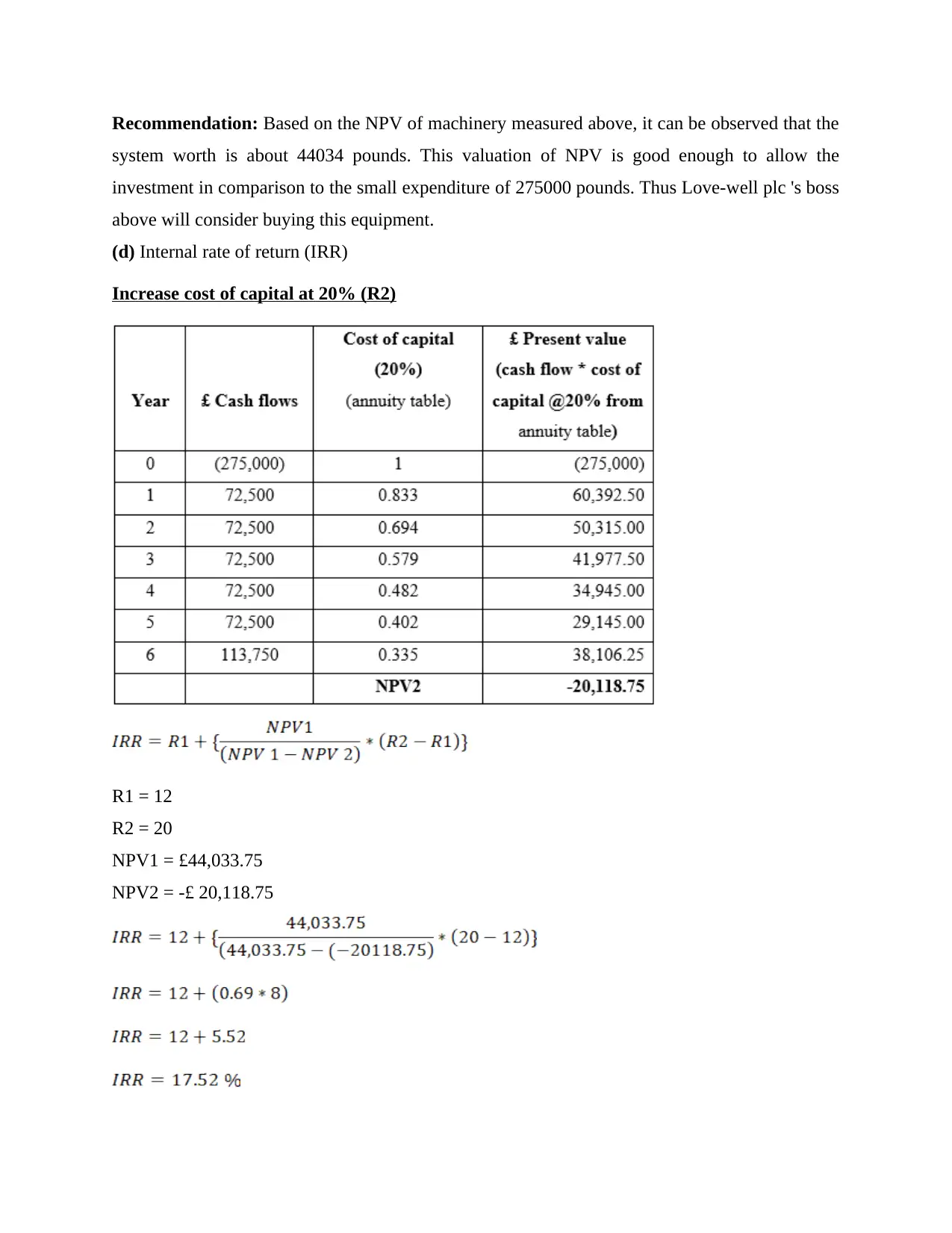

(c) Net present value:

Cost of capital: 12 % (R1)

Step three:

Step four:

Recommendation: From the average worth of ARR previously, it can be determined that new

equipment would yield a profit of 25.56%. This figure is higher than the growth rates of 275,000

pounds. Through this new equipment ought to be above the organization for its higher expected

return.

(c) Net present value:

Cost of capital: 12 % (R1)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Recommendation: Based on the NPV of machinery measured above, it can be observed that the

system worth is about 44034 pounds. This valuation of NPV is good enough to allow the

investment in comparison to the small expenditure of 275000 pounds. Thus Love-well plc 's boss

above will consider buying this equipment.

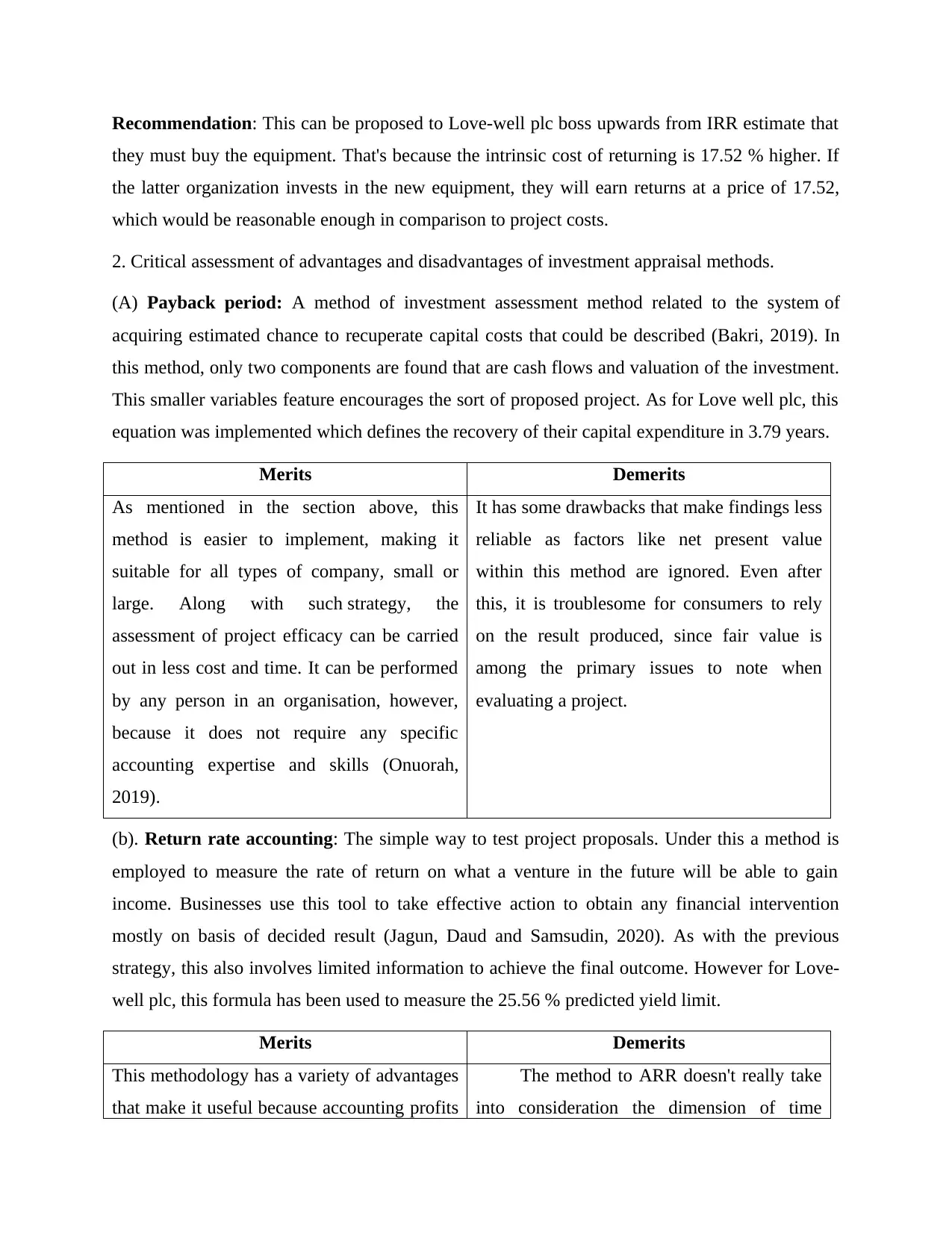

(d) Internal rate of return (IRR)

Increase cost of capital at 20% (R2)

R1 = 12

R2 = 20

NPV1 = £44,033.75

NPV2 = -£ 20,118.75

system worth is about 44034 pounds. This valuation of NPV is good enough to allow the

investment in comparison to the small expenditure of 275000 pounds. Thus Love-well plc 's boss

above will consider buying this equipment.

(d) Internal rate of return (IRR)

Increase cost of capital at 20% (R2)

R1 = 12

R2 = 20

NPV1 = £44,033.75

NPV2 = -£ 20,118.75

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Recommendation: This can be proposed to Love-well plc boss upwards from IRR estimate that

they must buy the equipment. That's because the intrinsic cost of returning is 17.52 % higher. If

the latter organization invests in the new equipment, they will earn returns at a price of 17.52,

which would be reasonable enough in comparison to project costs.

2. Critical assessment of advantages and disadvantages of investment appraisal methods.

(A) Payback period: A method of investment assessment method related to the system of

acquiring estimated chance to recuperate capital costs that could be described (Bakri, 2019). In

this method, only two components are found that are cash flows and valuation of the investment.

This smaller variables feature encourages the sort of proposed project. As for Love well plc, this

equation was implemented which defines the recovery of their capital expenditure in 3.79 years.

Merits Demerits

As mentioned in the section above, this

method is easier to implement, making it

suitable for all types of company, small or

large. Along with such strategy, the

assessment of project efficacy can be carried

out in less cost and time. It can be performed

by any person in an organisation, however,

because it does not require any specific

accounting expertise and skills (Onuorah,

2019).

It has some drawbacks that make findings less

reliable as factors like net present value

within this method are ignored. Even after

this, it is troublesome for consumers to rely

on the result produced, since fair value is

among the primary issues to note when

evaluating a project.

(b). Return rate accounting: The simple way to test project proposals. Under this a method is

employed to measure the rate of return on what a venture in the future will be able to gain

income. Businesses use this tool to take effective action to obtain any financial intervention

mostly on basis of decided result (Jagun, Daud and Samsudin, 2020). As with the previous

strategy, this also involves limited information to achieve the final outcome. However for Love-

well plc, this formula has been used to measure the 25.56 % predicted yield limit.

Merits Demerits

This methodology has a variety of advantages

that make it useful because accounting profits

The method to ARR doesn't really take

into consideration the dimension of time

they must buy the equipment. That's because the intrinsic cost of returning is 17.52 % higher. If

the latter organization invests in the new equipment, they will earn returns at a price of 17.52,

which would be reasonable enough in comparison to project costs.

2. Critical assessment of advantages and disadvantages of investment appraisal methods.

(A) Payback period: A method of investment assessment method related to the system of

acquiring estimated chance to recuperate capital costs that could be described (Bakri, 2019). In

this method, only two components are found that are cash flows and valuation of the investment.

This smaller variables feature encourages the sort of proposed project. As for Love well plc, this

equation was implemented which defines the recovery of their capital expenditure in 3.79 years.

Merits Demerits

As mentioned in the section above, this

method is easier to implement, making it

suitable for all types of company, small or

large. Along with such strategy, the

assessment of project efficacy can be carried

out in less cost and time. It can be performed

by any person in an organisation, however,

because it does not require any specific

accounting expertise and skills (Onuorah,

2019).

It has some drawbacks that make findings less

reliable as factors like net present value

within this method are ignored. Even after

this, it is troublesome for consumers to rely

on the result produced, since fair value is

among the primary issues to note when

evaluating a project.

(b). Return rate accounting: The simple way to test project proposals. Under this a method is

employed to measure the rate of return on what a venture in the future will be able to gain

income. Businesses use this tool to take effective action to obtain any financial intervention

mostly on basis of decided result (Jagun, Daud and Samsudin, 2020). As with the previous

strategy, this also involves limited information to achieve the final outcome. However for Love-

well plc, this formula has been used to measure the 25.56 % predicted yield limit.

Merits Demerits

This methodology has a variety of advantages

that make it useful because accounting profits

The method to ARR doesn't really take

into consideration the dimension of time

are used in it when cash flows are being used

in certain methods for project evaluation.

Along with another defining aspect of this

approach is that it is simple to use because it

is based on the execution of formulas that can

be implemented by anyone within the

organization.

value which is an essential feature. This

renders the test less precise and efficient

(Kabanda, 2019). Further than this, cash flows

underneath it are entirely ignored that is not

really that helpful in terms of the success

appraisal of a project.

(c) Net present value: That is defined as a tool used to calculate the current cost of a

company. Under it, the present value of the enterprise is determined by deducting

expenditure amounts from the cumulative cash flow of the years in question. The

discounted cash flow calculation is determined using the estimated Present Value (PV)

factor (Jagun, 2020) of it. Frequently, the mechanism is called NPV. This strategy has

been applied to determine the net enterprise value equipment in the Love-well plc

context.

Merits Demerits

The key benefit of using this method is that it

involves time amount of money dimension in

the process of calculating actual project value

(Boeri, 2019). It allows this method more

efficient and successful compared to other

techniques mentioned above, since time value

dimension has been ignored in the methods

discussed above. Another significant factor of

this method is that cumulative years, capital

expenditures are weighed of determining the

current investment potential.

The main drawback to this method is that,

despite the expense of capital-related

expectations, it is hard to complete. Along

with this belief, decisions are rendered less

reliable and counterproductive. On top of this,

it does not contain fixed costs for calculating

the present project performance.

(d) Internal rate of return: This can be described as a procedure of process and the

development of deciding the actual cost of gain for a venture. This style is called a type

of approach that is too hard to use because it requires strong accounting experience and

skills (Tariq and Khattak, 2019). This method can be extended and also only those

persons that have sufficient accounting knowledge. As for the above-mentioned sector,

in certain methods for project evaluation.

Along with another defining aspect of this

approach is that it is simple to use because it

is based on the execution of formulas that can

be implemented by anyone within the

organization.

value which is an essential feature. This

renders the test less precise and efficient

(Kabanda, 2019). Further than this, cash flows

underneath it are entirely ignored that is not

really that helpful in terms of the success

appraisal of a project.

(c) Net present value: That is defined as a tool used to calculate the current cost of a

company. Under it, the present value of the enterprise is determined by deducting

expenditure amounts from the cumulative cash flow of the years in question. The

discounted cash flow calculation is determined using the estimated Present Value (PV)

factor (Jagun, 2020) of it. Frequently, the mechanism is called NPV. This strategy has

been applied to determine the net enterprise value equipment in the Love-well plc

context.

Merits Demerits

The key benefit of using this method is that it

involves time amount of money dimension in

the process of calculating actual project value

(Boeri, 2019). It allows this method more

efficient and successful compared to other

techniques mentioned above, since time value

dimension has been ignored in the methods

discussed above. Another significant factor of

this method is that cumulative years, capital

expenditures are weighed of determining the

current investment potential.

The main drawback to this method is that,

despite the expense of capital-related

expectations, it is hard to complete. Along

with this belief, decisions are rendered less

reliable and counterproductive. On top of this,

it does not contain fixed costs for calculating

the present project performance.

(d) Internal rate of return: This can be described as a procedure of process and the

development of deciding the actual cost of gain for a venture. This style is called a type

of approach that is too hard to use because it requires strong accounting experience and

skills (Tariq and Khattak, 2019). This method can be extended and also only those

persons that have sufficient accounting knowledge. As for the above-mentioned sector,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.