Financial Resource Management Report: BSBFIM801 - All Assessments

VerifiedAdded on 2022/12/27

|54

|9231

|84

Report

AI Summary

This report, addressing BSBFIM801 Manage financial resources, comprehensively examines various aspects of financial management. It begins with an introduction to financial resources and their importance. The report is structured around six assessments, each delving into specific areas. Assessment 1 explores accounting principles, financial statements, cash flow principles, communication processes, compliance requirements, and the costs associated with capital, capital structure, and working capital. The subsequent assessments likely build upon these foundational concepts, providing in-depth analysis and practical applications related to managing financial resources effectively within an organizational context. The report integrates theoretical knowledge with practical insights, offering a well-rounded understanding of financial resource management.

BSBFIM801 Manage financial resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.....................................................................................................................................4

ASSESSMENT 1........................................................................................................................................4

ASSESSMENT 2......................................................................................................................................13

ASSESSMENT 3......................................................................................................................................18

ASSESSMENT 4......................................................................................................................................39

ASSESSMENT 5......................................................................................................................................45

ASSESSMENT 6......................................................................................................................................47

APPENDIX 1............................................................................................................................................51

APPENDIX 2............................................................................................................................................51

APPENDIX 3............................................................................................................................................52

INTRODUCTION.....................................................................................................................................4

ASSESSMENT 1........................................................................................................................................4

ASSESSMENT 2......................................................................................................................................13

ASSESSMENT 3......................................................................................................................................18

ASSESSMENT 4......................................................................................................................................39

ASSESSMENT 5......................................................................................................................................45

ASSESSMENT 6......................................................................................................................................47

APPENDIX 1............................................................................................................................................51

APPENDIX 2............................................................................................................................................51

APPENDIX 3............................................................................................................................................52

INTRODUCTION

Financial resources are a term in which consist of all the financial funds of a business

entity. These resources are essential part of business that help to conduct all the operational

activities in effective manner (Rodriguez-Fernandez, 2016). Various kinds of funding are utilized

by an entity such as, cash in the bank, venture capital and assets of company can convert cash

easily. These resources are required to manage in business in proper manner in which consist of

money they want to invest to start new venture. An essential source of income is the public

investment because people can purchase shares and presents an effective term of enhancing

capital. This report based on the managing financial resources of different organizations. In this

report consist of various assessment that based on the different financial activities.

ASSESSMENT 1

QUESTION 1 Explain the principles of:

Accounting- The term accounting can be known as a process of recording all financial

transactions in a systematic manner. The aim of accounting to get useful information during

preparation of financial statements. There are some principles of accounting which are as

follows:

Accrual principle- This is the principle which states that financial records must be

documented when they take place in the financial period, instead of in the cycles when

capital expenditures are correlated with each other. This really is the basis of accounting's

accrual basis. Instead of being arbitrarily put on hold or sped up by the related cash flows,

it is crucial for the development of cash receipts and payments what truly occurred in an

accounting cycle.

Conservatism principle- This is the principle in which companies can report costs and

obligations as rapidly as feasible, but only if they are confident they will exist, to record

sales and assets (Keehn, 2016). This gives the financial results a cautious slant that could

produce lower reported earnings, as sales and acknowledgment of assets could be

postponed for some time. Conversely, this theory appears to facilitate early, rather than

later, the recording of losses. This description may be pushed too far, where an

Financial resources are a term in which consist of all the financial funds of a business

entity. These resources are essential part of business that help to conduct all the operational

activities in effective manner (Rodriguez-Fernandez, 2016). Various kinds of funding are utilized

by an entity such as, cash in the bank, venture capital and assets of company can convert cash

easily. These resources are required to manage in business in proper manner in which consist of

money they want to invest to start new venture. An essential source of income is the public

investment because people can purchase shares and presents an effective term of enhancing

capital. This report based on the managing financial resources of different organizations. In this

report consist of various assessment that based on the different financial activities.

ASSESSMENT 1

QUESTION 1 Explain the principles of:

Accounting- The term accounting can be known as a process of recording all financial

transactions in a systematic manner. The aim of accounting to get useful information during

preparation of financial statements. There are some principles of accounting which are as

follows:

Accrual principle- This is the principle which states that financial records must be

documented when they take place in the financial period, instead of in the cycles when

capital expenditures are correlated with each other. This really is the basis of accounting's

accrual basis. Instead of being arbitrarily put on hold or sped up by the related cash flows,

it is crucial for the development of cash receipts and payments what truly occurred in an

accounting cycle.

Conservatism principle- This is the principle in which companies can report costs and

obligations as rapidly as feasible, but only if they are confident they will exist, to record

sales and assets (Keehn, 2016). This gives the financial results a cautious slant that could

produce lower reported earnings, as sales and acknowledgment of assets could be

postponed for some time. Conversely, this theory appears to facilitate early, rather than

later, the recording of losses. This description may be pushed too far, where an

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organsiation routinely misrepresents its consequences to be less than is actually the

situation.

Cost principle- This is the principle that a corporation should report its cash, liabilities,

and equity contributions only at their initial cost of acquisition. When a host of

accounting principles are going the way of changing revenues and expenses to their equal

values, this concept is becoming less true.

Principles of Financial statements: Financial statements are formal reports of a

company, individual, or other entity's financial transactions and role. Specific financial data is

delivered in a standardized and simple way. Below some key principles are mentioned in such

manner:

Income statement: As per the principle there should be calculation of gross and net gains

and losses on the basis of accounting rules and accept, for a given duration, that the rise

(or decrease) of total income over that time is profit margin (or loss).

Balance sheet- As per the principle there should be recognize that statements of asset and

responsibility balances on a defined date are non-current assets (fixed assets), capital

resources, total revenues, interest expense (creditors: sums due within 12 months),

lengthy obligations (borrowers: amounts due for more than one year), capital

expenditures, hired capital and owned capital are recognized and described.

Rules to prepare financial statements for different entities:

Sole trader-

Explain the distinction between a trading firm and a service company planning income

reports.

Allow allowances for accumulated and prepaid costs and changes for poor loans and

provisions for uncertain obligations for accrued and prepaid profits.

Making changes to products bought for us by the holder.

Limited liability companies:

Understand the value of the word restrictive liability.

situation.

Cost principle- This is the principle that a corporation should report its cash, liabilities,

and equity contributions only at their initial cost of acquisition. When a host of

accounting principles are going the way of changing revenues and expenses to their equal

values, this concept is becoming less true.

Principles of Financial statements: Financial statements are formal reports of a

company, individual, or other entity's financial transactions and role. Specific financial data is

delivered in a standardized and simple way. Below some key principles are mentioned in such

manner:

Income statement: As per the principle there should be calculation of gross and net gains

and losses on the basis of accounting rules and accept, for a given duration, that the rise

(or decrease) of total income over that time is profit margin (or loss).

Balance sheet- As per the principle there should be recognize that statements of asset and

responsibility balances on a defined date are non-current assets (fixed assets), capital

resources, total revenues, interest expense (creditors: sums due within 12 months),

lengthy obligations (borrowers: amounts due for more than one year), capital

expenditures, hired capital and owned capital are recognized and described.

Rules to prepare financial statements for different entities:

Sole trader-

Explain the distinction between a trading firm and a service company planning income

reports.

Allow allowances for accumulated and prepaid costs and changes for poor loans and

provisions for uncertain obligations for accrued and prepaid profits.

Making changes to products bought for us by the holder.

Limited liability companies:

Understand the value of the word restrictive liability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Prepare clear horizontally or vertically allocation accounts to grasp and differentiate

between approved, called-up, paid-up share capital.

Recognize and discern between share capital and loan resources (preferred stock and

common equity).

Principle of cash flow: The cash flow statement outlines the impact of a company's

running, spending and borrowing operations on cash mostly during accounting cycle. It reflects

on previous business decisions on topics including the issuing of shares or the selling of lengthy

securities. This detail is only accessible from the other financial reports in bits and pieces. While

cash flows are essential to the financial stability of a business, the cash flow statement

executives, analysts, lenders, and other stakeholders with critical data. Below principles of cash

flow statement are mentioned in such manner:

The cash flow statement assumes an action structure which is broken into three sections:

activities of business, acquisition and funding. Operating events are generally listed first,

followed by acquisition activities and, ultimately, funding activities. The cash flow theory

implies that the cumulative cash flows arising from that are only net income applicable to the

value of a project (Usman and Vanhaverbeke, 2017). The concept of discounted cash flow (DCF)

is built on the presumption that the value of a portfolio is approximately equal to the current

value of its potential expected cash flows. By either the direct method or the indirect method,

the operational component of the statement of cash flows can be seen. The investing and

supporting areas are the same for each method; the only distinction is in the operational portion.

between approved, called-up, paid-up share capital.

Recognize and discern between share capital and loan resources (preferred stock and

common equity).

Principle of cash flow: The cash flow statement outlines the impact of a company's

running, spending and borrowing operations on cash mostly during accounting cycle. It reflects

on previous business decisions on topics including the issuing of shares or the selling of lengthy

securities. This detail is only accessible from the other financial reports in bits and pieces. While

cash flows are essential to the financial stability of a business, the cash flow statement

executives, analysts, lenders, and other stakeholders with critical data. Below principles of cash

flow statement are mentioned in such manner:

The cash flow statement assumes an action structure which is broken into three sections:

activities of business, acquisition and funding. Operating events are generally listed first,

followed by acquisition activities and, ultimately, funding activities. The cash flow theory

implies that the cumulative cash flows arising from that are only net income applicable to the

value of a project (Usman and Vanhaverbeke, 2017). The concept of discounted cash flow (DCF)

is built on the presumption that the value of a portfolio is approximately equal to the current

value of its potential expected cash flows. By either the direct method or the indirect method,

the operational component of the statement of cash flows can be seen. The investing and

supporting areas are the same for each method; the only distinction is in the operational portion.

The key types of gross sales invoices and gross cash transfers are illustrated by the direct

process. In the other hand, the indirect approach continues with net profits and changes the

results of the sales on profit/loss. Cash flows from the operational segment will eventually

deliver the same outcome, whether underneath a direct or indirect approach, but the

representation will vary.

QUESTION 2: Briefly describe best-practice communication processes and methods.

The only way people can do amazing challenges is by a linked team and a linked

enterprise in modern environment. With the sharing of thoughts and knowledge, interactions and

relationships are created. In building these relations and interaction between individuals,

communication serves as a powerful method. A very important talent and craft is collaboration.

It is essential to have the correct purpose to communicate with the other person, no care what

way of communicating we use. Below some methods of communication are explained:

Written communication: This applies to handwritten or registered papers, such as

schedules, agreements, memos, meeting notes, paper review of specifications, risk

registers for design documentation and other associated written materials. It is used to

have well-thought-out and also well information, so it is easier to check than verbal

contact because it is not possible to change anything written instantly.

Oral communication: It requires the sharing of information or signals through orally

using phrases through face-to-face or mobile interactions (Shah, Sahai and Mishra, 2017).

It is the most popular mode of conversation, since it paves the way for suggestions right

after the message has been sent. It is understood that it is also random. The capacity to

listen and consider deeply before communicating is important in verbal contact.

Nonverbal communication: Without the use of language, non-verbal contact is

transmitting information. It is mostly via the language of one's body, movements, eye-

contacts, posture, pitch and sound of one's speech, etc. One can express immense

thoughts and emotions.

Visual communication: A image is a thousand words worth a picture. Written

correspondence is significantly enhanced by visual aids including such animation,

graphics, animation, graphs & maps, painting, signs and badges. In order to make

process. In the other hand, the indirect approach continues with net profits and changes the

results of the sales on profit/loss. Cash flows from the operational segment will eventually

deliver the same outcome, whether underneath a direct or indirect approach, but the

representation will vary.

QUESTION 2: Briefly describe best-practice communication processes and methods.

The only way people can do amazing challenges is by a linked team and a linked

enterprise in modern environment. With the sharing of thoughts and knowledge, interactions and

relationships are created. In building these relations and interaction between individuals,

communication serves as a powerful method. A very important talent and craft is collaboration.

It is essential to have the correct purpose to communicate with the other person, no care what

way of communicating we use. Below some methods of communication are explained:

Written communication: This applies to handwritten or registered papers, such as

schedules, agreements, memos, meeting notes, paper review of specifications, risk

registers for design documentation and other associated written materials. It is used to

have well-thought-out and also well information, so it is easier to check than verbal

contact because it is not possible to change anything written instantly.

Oral communication: It requires the sharing of information or signals through orally

using phrases through face-to-face or mobile interactions (Shah, Sahai and Mishra, 2017).

It is the most popular mode of conversation, since it paves the way for suggestions right

after the message has been sent. It is understood that it is also random. The capacity to

listen and consider deeply before communicating is important in verbal contact.

Nonverbal communication: Without the use of language, non-verbal contact is

transmitting information. It is mostly via the language of one's body, movements, eye-

contacts, posture, pitch and sound of one's speech, etc. One can express immense

thoughts and emotions.

Visual communication: A image is a thousand words worth a picture. Written

correspondence is significantly enhanced by visual aids including such animation,

graphics, animation, graphs & maps, painting, signs and badges. In order to make

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

knowledge sharing more accessible and successful, visual contact is often used in the

correct mix.

So these are methods of communication which are best in practice and need to be applied

in the context of companies for better outcome.

QUESTION 3: Briefly describe compliance requirements, including relevant legislative

responsibilities.

Compliance usually involves agreeing with a regulation, such as a definition, procedure, norm or

statute. Regulatory enforcement defines the aim that companies strive to accomplish in their

attempts to ensure that they are mindful of the applicable rules, legislation, and legislation and

take action to conform with them (Eniola and Entebang, 2016). Due to the growing number of

laws and the need for organsiational accountability, the use of standardized and harmonized sets

of compliance controls is gradually being embraced by organizations. This strategy is used to

insure which, without any of the needless duplication of initiative and operation from capital, all

relevant governance criteria can be fulfilled. Regulatory enforcement varies not only by sector

but also by venue. The financial, science, and medicinal regulatory frameworks in one nation, for

example, could be identical but with significantly unique nuances in an another nation. This

similarities and variations are also the result of actions in different nations, markets and policy

environments to shifting priorities and specifications.

QUESTION 4: Explain the cost of-

Cost of capital: Capital expense is the interest earned needed to make an investment

appraisal initiative worthwhile, like constructing a new plant. Usually, as owners and statisticians

analyze the cost of capital, they mean the weighted average of the debt and equity costs of a

business combined together. The cost of the capital calculation is used collectively by businesses

to assess if the expense of resources is worthwhile a capital venture and by shareholders who use

it to evaluate if an expenditure is worth taking the risk as opposed to the gain. Capital costs

depend on the method of funding used. It applies to the equity cost if the corporation is funded

solely by assets, or to the debt expense if it is creating the actual by debt. Cost of capital, from

the viewpoint of a shareholder, is the return required by whoever is supplying the wealth for a

company. In other terms, it is an estimation of the vulnerability of a corporation. In doing so, to

correct mix.

So these are methods of communication which are best in practice and need to be applied

in the context of companies for better outcome.

QUESTION 3: Briefly describe compliance requirements, including relevant legislative

responsibilities.

Compliance usually involves agreeing with a regulation, such as a definition, procedure, norm or

statute. Regulatory enforcement defines the aim that companies strive to accomplish in their

attempts to ensure that they are mindful of the applicable rules, legislation, and legislation and

take action to conform with them (Eniola and Entebang, 2016). Due to the growing number of

laws and the need for organsiational accountability, the use of standardized and harmonized sets

of compliance controls is gradually being embraced by organizations. This strategy is used to

insure which, without any of the needless duplication of initiative and operation from capital, all

relevant governance criteria can be fulfilled. Regulatory enforcement varies not only by sector

but also by venue. The financial, science, and medicinal regulatory frameworks in one nation, for

example, could be identical but with significantly unique nuances in an another nation. This

similarities and variations are also the result of actions in different nations, markets and policy

environments to shifting priorities and specifications.

QUESTION 4: Explain the cost of-

Cost of capital: Capital expense is the interest earned needed to make an investment

appraisal initiative worthwhile, like constructing a new plant. Usually, as owners and statisticians

analyze the cost of capital, they mean the weighted average of the debt and equity costs of a

business combined together. The cost of the capital calculation is used collectively by businesses

to assess if the expense of resources is worthwhile a capital venture and by shareholders who use

it to evaluate if an expenditure is worth taking the risk as opposed to the gain. Capital costs

depend on the method of funding used. It applies to the equity cost if the corporation is funded

solely by assets, or to the debt expense if it is creating the actual by debt. Cost of capital, from

the viewpoint of a shareholder, is the return required by whoever is supplying the wealth for a

company. In other terms, it is an estimation of the vulnerability of a corporation. In doing so, to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

decide if a certain inventory is too risky but would create a decent investment, a shareholder can

look at the variability (beta) of the financial performance of a firm. The capital cost of a business

is usually estimated using the capital method's cost model that includes the cost of both debt and

equity financing. In necessary to come at a consolidated rate, each segment of the company’s

capital structure is weighted correspondingly, and the calculation includes any type of debt

financing on the profit and loss account, except stockholders, shares, and other types of debt.

Cost of capital structure: The structure of capital of business is way of financing overall

growth and operations with the help of different funding sources. The composition of capital

applies to the amount of debt and/or equity that a business uses to support its activities and fund

its resources (Picken, 2017). The financial structure of a company is usually expressed as a

percentage of debt-to-equity or debt-to-capital. Debt and capital ratio are used to support the

purchases, capital costs, investments, and other assets of a firm. When they determine which to

use leverage or equity to fund projects, there are compromises businesses have to make, and

management can combine the two to find the optimal cash position. A firm's optimum financial

performance is also described as the debt and equity which resulted in the company's lowest

value of the firm cost (WACC). In fact, this technical definition is not often utilized, because

companies also have a tactical or conceptual interpretation of what will be the optimal

framework. A company may issue either more debt and equity in order to optimize the

framework. As a method of recapitalization, the additional money that is acquired can be used to

invest in new investments or can be used to buy back debt/equity that is already unpaid.

Cost of working capital: The cost of working capital is related to those expense which

are related to managing day to day operations and activities for a company. These expenses are

considered on the basis of two distinct factors: firm’s short term expenses and current portion of

lengthy term debts which is usually the part of debt during the upcoming time period. All types

of expenses are can be identified on company’s balance sheet in current liability part. In the

current liabilities portion of their balance sheets, many businesses have at least two categories of

accounts: accrued liabilities and payroll payable. In addition, the particular items categorized as

current liabilities differ across industries and sectors and they're more focused on which day-to-

day operations are essential to the organsiation. In the industrial sector, for instance, the expenses

involved with the transformation of raw materials to finished goods are also defined as WCC.

look at the variability (beta) of the financial performance of a firm. The capital cost of a business

is usually estimated using the capital method's cost model that includes the cost of both debt and

equity financing. In necessary to come at a consolidated rate, each segment of the company’s

capital structure is weighted correspondingly, and the calculation includes any type of debt

financing on the profit and loss account, except stockholders, shares, and other types of debt.

Cost of capital structure: The structure of capital of business is way of financing overall

growth and operations with the help of different funding sources. The composition of capital

applies to the amount of debt and/or equity that a business uses to support its activities and fund

its resources (Picken, 2017). The financial structure of a company is usually expressed as a

percentage of debt-to-equity or debt-to-capital. Debt and capital ratio are used to support the

purchases, capital costs, investments, and other assets of a firm. When they determine which to

use leverage or equity to fund projects, there are compromises businesses have to make, and

management can combine the two to find the optimal cash position. A firm's optimum financial

performance is also described as the debt and equity which resulted in the company's lowest

value of the firm cost (WACC). In fact, this technical definition is not often utilized, because

companies also have a tactical or conceptual interpretation of what will be the optimal

framework. A company may issue either more debt and equity in order to optimize the

framework. As a method of recapitalization, the additional money that is acquired can be used to

invest in new investments or can be used to buy back debt/equity that is already unpaid.

Cost of working capital: The cost of working capital is related to those expense which

are related to managing day to day operations and activities for a company. These expenses are

considered on the basis of two distinct factors: firm’s short term expenses and current portion of

lengthy term debts which is usually the part of debt during the upcoming time period. All types

of expenses are can be identified on company’s balance sheet in current liability part. In the

current liabilities portion of their balance sheets, many businesses have at least two categories of

accounts: accrued liabilities and payroll payable. In addition, the particular items categorized as

current liabilities differ across industries and sectors and they're more focused on which day-to-

day operations are essential to the organsiation. In the industrial sector, for instance, the expenses

involved with the transformation of raw materials to finished goods are also defined as WCC.

The purchasing and handling of raw resources can be linked to huge parts of a company's overall

budget. In the other side, a tech corporation could see larger portions of its existing liabilities

controlled by the expense and sale of design and technology (R&D).

Question 5 Identify and describe finance and investment decision

The Investment Decision refers to decisions taken by investors or strategic planning at the

highest level in regards to the quantity of financial resources to be used in the context of business

opportunities.

Simply, it is considered an investing choice to choose the type of resources wherein the funds

will be spent by the corporation. Such properties fell into two classifications:

Capital Budgeting is defined as the decision to spend money in long-term investments.

Therefore, Capital Budgeting is the method of choosing an asset or project plan that will load

quickly returns (Caha, 2017). The first important step in Capital Budgeting is to pick a resource

on the grounds of the gains that will be extracted from it in the potential, either present or fresh.

The next step is the study of the complexity and risk inherent in the plan. Because the profits are

to be accumulated in the future, the ambiguity about the return is large. Lastly, it is important to

set the required rate of return on which the success of the long mission will be measured.

The amount invested in existing assets or brief resources is referred to as the maintenance of

working capital. The control of operating capital works with the management of available

budget. In the other side, a tech corporation could see larger portions of its existing liabilities

controlled by the expense and sale of design and technology (R&D).

Question 5 Identify and describe finance and investment decision

The Investment Decision refers to decisions taken by investors or strategic planning at the

highest level in regards to the quantity of financial resources to be used in the context of business

opportunities.

Simply, it is considered an investing choice to choose the type of resources wherein the funds

will be spent by the corporation. Such properties fell into two classifications:

Capital Budgeting is defined as the decision to spend money in long-term investments.

Therefore, Capital Budgeting is the method of choosing an asset or project plan that will load

quickly returns (Caha, 2017). The first important step in Capital Budgeting is to pick a resource

on the grounds of the gains that will be extracted from it in the potential, either present or fresh.

The next step is the study of the complexity and risk inherent in the plan. Because the profits are

to be accumulated in the future, the ambiguity about the return is large. Lastly, it is important to

set the required rate of return on which the success of the long mission will be measured.

The amount invested in existing assets or brief resources is referred to as the maintenance of

working capital. The control of operating capital works with the management of available

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

resources that are incredibly liquid. The decision to invest in short-term assets is critical for an

enterprise, when long-term sustainability requires short-term survival. A business seeks to

preserve a trade-off among financial performance through the cash management. If a corporation

has less operating capital, i.e. less funds invested in short-term investments, so the company will

not be able to cover off its existing liabilities and will collapse. Or if the company has more

existing assets than appropriate, it may have a detrimental impact on the company's profitability.

Question 6 Describe the goal of financial resource management

The goal of financial resource management is that organization is increasing profit which

can be reviewed by computing the gross margin and net profit margin ratios. The other goal of

arranging resources is to deduct the cost through company's expenditure. The meaning of

financial management that planning, managing and guiding and controlling different financial

activities like procurement and utilization of funds of an entity. There are mentioned different

financial goal of financial resource management such as:

Maximizing shareholder value: It is goal of finance resource management to increase shareholder

value that comes from interpretations the role of corporate governance (Huang and Knight,

2017). In large business entity manage financial resources in effective manner and invest into

securities properly that provide back good returns. On the basis of these return provide good

return to their shareholders. Thus, it will help to increase value of holders and increasing their

wealth by paying dividends due to increase market price.

Maximizing market value: The main goal of financial resource management that increasing the

market value which is connected to idea of increasing shareholder value as market value is the

price. There are various models of corporate governance all over the world that differ from

variety of capitalism which are embedded. Every organization want repudiated position in the

market to get growth and sustainability. For this require to increase market value properly and

take right decisions.

Question 7 Principles of financial relevant to the organization's operations

enterprise, when long-term sustainability requires short-term survival. A business seeks to

preserve a trade-off among financial performance through the cash management. If a corporation

has less operating capital, i.e. less funds invested in short-term investments, so the company will

not be able to cover off its existing liabilities and will collapse. Or if the company has more

existing assets than appropriate, it may have a detrimental impact on the company's profitability.

Question 6 Describe the goal of financial resource management

The goal of financial resource management is that organization is increasing profit which

can be reviewed by computing the gross margin and net profit margin ratios. The other goal of

arranging resources is to deduct the cost through company's expenditure. The meaning of

financial management that planning, managing and guiding and controlling different financial

activities like procurement and utilization of funds of an entity. There are mentioned different

financial goal of financial resource management such as:

Maximizing shareholder value: It is goal of finance resource management to increase shareholder

value that comes from interpretations the role of corporate governance (Huang and Knight,

2017). In large business entity manage financial resources in effective manner and invest into

securities properly that provide back good returns. On the basis of these return provide good

return to their shareholders. Thus, it will help to increase value of holders and increasing their

wealth by paying dividends due to increase market price.

Maximizing market value: The main goal of financial resource management that increasing the

market value which is connected to idea of increasing shareholder value as market value is the

price. There are various models of corporate governance all over the world that differ from

variety of capitalism which are embedded. Every organization want repudiated position in the

market to get growth and sustainability. For this require to increase market value properly and

take right decisions.

Question 7 Principles of financial relevant to the organization's operations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The first rule in financing is that the essence of capital is time. The dollar received now, in other

words, would be more important than the dollar received in the future. In order to make more

profits, money will then be spent. Inflation is a continuous rise in the overall cost of the cost of

goods and services.

The connection between risk and reward is clarified by the second principle of finance. The

bigger the incentive, the greater the risk. This theory implies that if the profit is minimal, having

a high-risk expenditure is a waste of money (Weber and Feltmate, 2016).

The Third Finance Theory notes that portfolio diversifying, or the allocation of investment and

liability over several different undertakings, will minimize the ultimate risk of the lender. This is

critical because the absence of portfolio diversity will raise market risk for the shareholder.

The Fourth Finance Theory says that even in pricing shares, capital markets are successful. The

business tracks a company's reports, projected estimates, supply and demand, and other

variables. This theory could not be the right approach for stakeholders, based on historical

evidence, because the capital markets in itself are effective and the financial climate is still

evolving.

The fifth principle of financing is that the priorities of a shareholders and managers can vary.

The supervisor is doing what they think is profit maximization. The shareholder, on the other

side, needs the price of the inventory to rise so that the shareholder can buy the property to

maximize their capital at a better profit.

The sixth finance principle states that credibility makes a difference. Credibility has a major

impact on an investment's plans to spend in a financial asset or not. A financial product is a

written matter indicating the right to obtain a property that can be traded, including such money,

the contractual right to produce or take funds, or any other form of equity. Firms with similar

credibility will encourage more individuals to purchase their stocks. Companies with lower

credibility can have trouble persuading individuals to purchase securities.

Question 8 Explain risk and return

Risk: It is defined as a financial term that presents uncertainty in regard deviation

expected earnings. Risk measures the uncertainty of an investor that willingly take to realize a

words, would be more important than the dollar received in the future. In order to make more

profits, money will then be spent. Inflation is a continuous rise in the overall cost of the cost of

goods and services.

The connection between risk and reward is clarified by the second principle of finance. The

bigger the incentive, the greater the risk. This theory implies that if the profit is minimal, having

a high-risk expenditure is a waste of money (Weber and Feltmate, 2016).

The Third Finance Theory notes that portfolio diversifying, or the allocation of investment and

liability over several different undertakings, will minimize the ultimate risk of the lender. This is

critical because the absence of portfolio diversity will raise market risk for the shareholder.

The Fourth Finance Theory says that even in pricing shares, capital markets are successful. The

business tracks a company's reports, projected estimates, supply and demand, and other

variables. This theory could not be the right approach for stakeholders, based on historical

evidence, because the capital markets in itself are effective and the financial climate is still

evolving.

The fifth principle of financing is that the priorities of a shareholders and managers can vary.

The supervisor is doing what they think is profit maximization. The shareholder, on the other

side, needs the price of the inventory to rise so that the shareholder can buy the property to

maximize their capital at a better profit.

The sixth finance principle states that credibility makes a difference. Credibility has a major

impact on an investment's plans to spend in a financial asset or not. A financial product is a

written matter indicating the right to obtain a property that can be traded, including such money,

the contractual right to produce or take funds, or any other form of equity. Firms with similar

credibility will encourage more individuals to purchase their stocks. Companies with lower

credibility can have trouble persuading individuals to purchase securities.

Question 8 Explain risk and return

Risk: It is defined as a financial term that presents uncertainty in regard deviation

expected earnings. Risk measures the uncertainty of an investor that willingly take to realize a

gain from an investment. It can be deducted by using diversification and hedging strategies.

There are various types of risk that arise in the business because of losing some or all an

investment. These are, market, financial, business, liquidity, sovereign, insurance risk.

Return: It can be presented minimal as the change in dollar value of an investment over

time. It is presented in percentage manner that derived from the ratio of profit of investment

(Zenghelis and Stern, 2016). Return can also be presented as net outcomes in which deduct after

fees, taxes and inflation. Returns are mainly annualized in comparison way while holding for

period return and computes the gain or loss during the investment time was held. It is mainly

calculated in percentage manner from the original investment after that manager cam analysis

and compare how well their investment and efficient in market. The overall amount of

investment is mainly based on a lot of different things but it considers as main force is risky. It is

highly investments reap a greater rate of return than low risk investments.

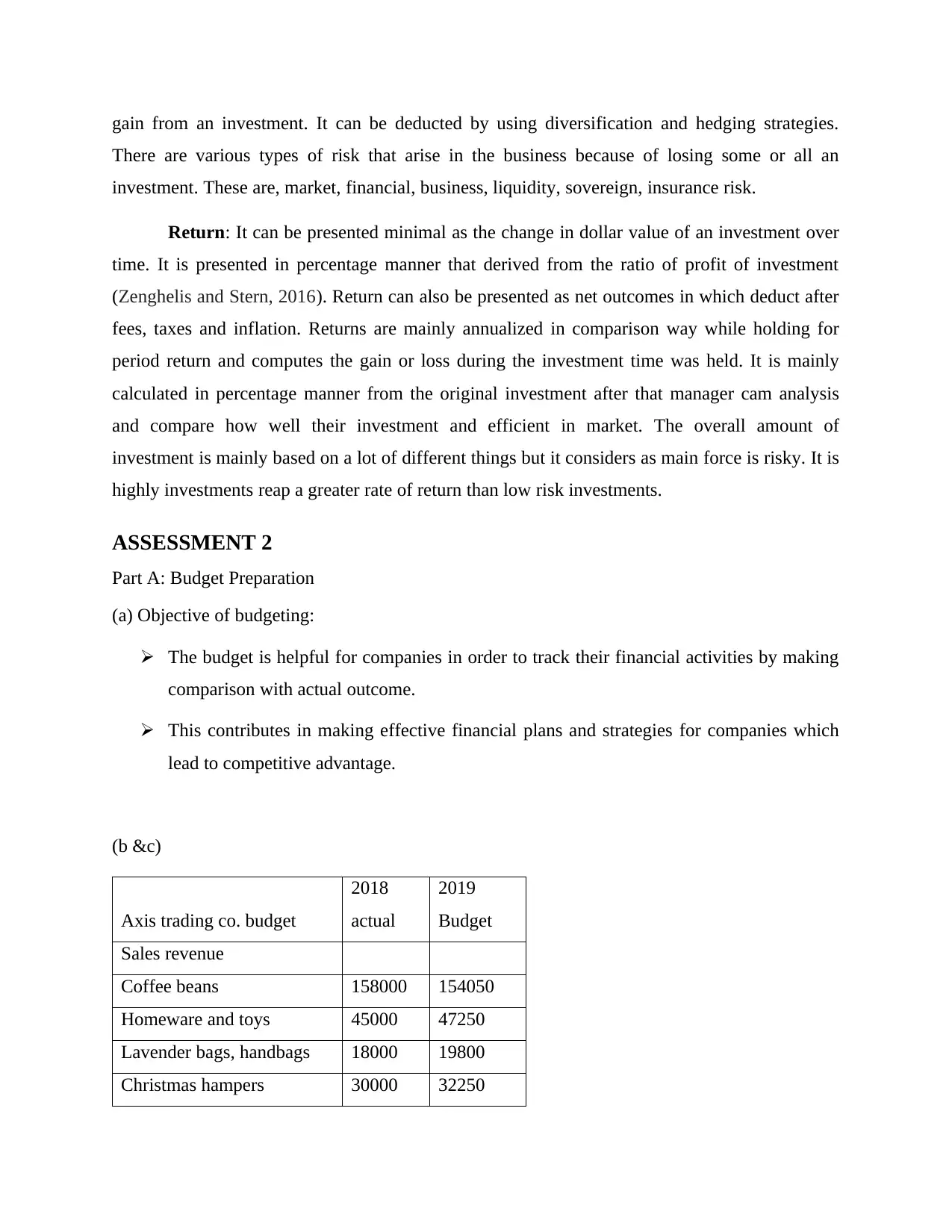

ASSESSMENT 2

Part A: Budget Preparation

(a) Objective of budgeting:

The budget is helpful for companies in order to track their financial activities by making

comparison with actual outcome.

This contributes in making effective financial plans and strategies for companies which

lead to competitive advantage.

(b &c)

Axis trading co. budget

2018

actual

2019

Budget

Sales revenue

Coffee beans 158000 154050

Homeware and toys 45000 47250

Lavender bags, handbags 18000 19800

Christmas hampers 30000 32250

There are various types of risk that arise in the business because of losing some or all an

investment. These are, market, financial, business, liquidity, sovereign, insurance risk.

Return: It can be presented minimal as the change in dollar value of an investment over

time. It is presented in percentage manner that derived from the ratio of profit of investment

(Zenghelis and Stern, 2016). Return can also be presented as net outcomes in which deduct after

fees, taxes and inflation. Returns are mainly annualized in comparison way while holding for

period return and computes the gain or loss during the investment time was held. It is mainly

calculated in percentage manner from the original investment after that manager cam analysis

and compare how well their investment and efficient in market. The overall amount of

investment is mainly based on a lot of different things but it considers as main force is risky. It is

highly investments reap a greater rate of return than low risk investments.

ASSESSMENT 2

Part A: Budget Preparation

(a) Objective of budgeting:

The budget is helpful for companies in order to track their financial activities by making

comparison with actual outcome.

This contributes in making effective financial plans and strategies for companies which

lead to competitive advantage.

(b &c)

Axis trading co. budget

2018

actual

2019

Budget

Sales revenue

Coffee beans 158000 154050

Homeware and toys 45000 47250

Lavender bags, handbags 18000 19800

Christmas hampers 30000 32250

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 54

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.