Financial Decision-Making Report, BM414, Finance, Bucks University

VerifiedAdded on 2022/12/23

|12

|3760

|54

Report

AI Summary

This report provides a detailed analysis of financial decision-making within Skansa Plc, a construction company. It begins with an introduction to financial management and the company's background, including its strengths, weaknesses, opportunities, and threats. The report then delves into Task 1, which examines the roles and responsibilities of the accounting and finance departments. The accounting department's functions, including financial accounting, management accounting, tax functions, and auditing functions, are thoroughly discussed. The finance department's functions, such as investment, financing, dividend, and working capital management, are also analyzed. Task 2 focuses on ratio analysis, calculating and interpreting key financial ratios such as Return on Capital Employed (ROCE), Net Profit Margin, Current Ratio, Average Receivable Days, and Average Payable Days for 2018 and 2019. The analysis includes a comparative assessment of the company's financial performance based on these ratios, highlighting trends and potential areas for improvement. The report concludes with a summary of findings and recommendations for enhancing financial management practices within Skansa Plc.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION..........................................................................................................................3

Task 1..............................................................................................................................................3

Importance, duties and role of financial function.......................................................................3

Task 2..............................................................................................................................................7

Ratio analysis..............................................................................................................................7

CONCLUSION.............................................................................................................................11

REFERENCES.............................................................................................................................12

INTRODUCTION..........................................................................................................................3

Task 1..............................................................................................................................................3

Importance, duties and role of financial function.......................................................................3

Task 2..............................................................................................................................................7

Ratio analysis..............................................................................................................................7

CONCLUSION.............................................................................................................................11

REFERENCES.............................................................................................................................12

INTRODUCTION

Financial management is defined as managing financial resources associated with the

business entity. This report is based on the case study of Skansa Plc initiated business operations

in the year 1984. Company is associated with the construction sector. Currently the business

entity providing employment opportunities to approximately 33585 employees. Company is

owning an income of £ 6.054 billion. Company own a market share of approximately 2% that is

very impressive due to the presence of healthy market competition. Business entity contain

positive brand value, diversified resources, efficient employee base and well-structured

organisation hierarchy are the strengths associated with the business entity. Certain weaknesses

like less focus over innovation, technological advancement and inflation in economy is the

major weakness associated with the business entity. Opportunities such as global expansion,

product development, technical advancement and innovation is also associated with the business

idea hold by business entity. Competition is considered as the key threat associated with the

business operations company functioned in market. This project will discuss the financial

management related practices in respect to the business entity. Henceforth, report will emphasis

over different functional roles and responsibilities company channelise in order to manage its

finances in the best way possible. Furthermore, report will discuss the overall performance of

business entity for the two financial years based on comparative assessment.

Task 1

Importance, duties and role of financial function

Financial management practices are allocated to finance and accounts teams in the

organisation hierarchy of the Skansa Plc. Account and finance department both the areas allow

the business entity to establishes smooth control over the financial resources undertaken by the

business entity. Management has segregated different roles and responsibilities related to the

financial management in between account and finance department based on the skills and

abilities of the employees associated with individual department (Al Muhair and Nobanee,

2019). The basic segregation into the role both the departments play is that accounts deportment

is mainly focused towards the projection of the accounting transactions company has entertained

and on the other hand finance team is more involved in analysing the financial position of

company and make the best level of decision based on the needs and requirements of the

business entity.

Financial management is defined as managing financial resources associated with the

business entity. This report is based on the case study of Skansa Plc initiated business operations

in the year 1984. Company is associated with the construction sector. Currently the business

entity providing employment opportunities to approximately 33585 employees. Company is

owning an income of £ 6.054 billion. Company own a market share of approximately 2% that is

very impressive due to the presence of healthy market competition. Business entity contain

positive brand value, diversified resources, efficient employee base and well-structured

organisation hierarchy are the strengths associated with the business entity. Certain weaknesses

like less focus over innovation, technological advancement and inflation in economy is the

major weakness associated with the business entity. Opportunities such as global expansion,

product development, technical advancement and innovation is also associated with the business

idea hold by business entity. Competition is considered as the key threat associated with the

business operations company functioned in market. This project will discuss the financial

management related practices in respect to the business entity. Henceforth, report will emphasis

over different functional roles and responsibilities company channelise in order to manage its

finances in the best way possible. Furthermore, report will discuss the overall performance of

business entity for the two financial years based on comparative assessment.

Task 1

Importance, duties and role of financial function

Financial management practices are allocated to finance and accounts teams in the

organisation hierarchy of the Skansa Plc. Account and finance department both the areas allow

the business entity to establishes smooth control over the financial resources undertaken by the

business entity. Management has segregated different roles and responsibilities related to the

financial management in between account and finance department based on the skills and

abilities of the employees associated with individual department (Al Muhair and Nobanee,

2019). The basic segregation into the role both the departments play is that accounts deportment

is mainly focused towards the projection of the accounting transactions company has entertained

and on the other hand finance team is more involved in analysing the financial position of

company and make the best level of decision based on the needs and requirements of the

business entity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accounts department

Management of Skansa Plc has allotted certain responsibilities such as financial

accounting, management accounting, tax functions and auditing functions to the accounts

departments. All these are the four primarily functions related to the accounting.

Finance accounting: Finance accounting is among the primary role and responsibility that

accounts department play in Skansa Plc. Financial accounting is more like utilising the series of

accounting principles and practices in order to represent the financial position of business entity

in the best way possible. Skansa Plc follow accrual basis when it comes to reporting the

financial position of the organisation. Accounts department classified financial data in certain

ways such as revenue, expenses, assets, liability and equity (Alkaraan, 2018). Revenue and

expenses are accounted and reported in the income statement of the respective financial year.

Assets, liability and equity accounts are projected under the balance sheet section of the

financial accounting. The basic aim behind the finance accounting is that to present or reflect the

accounting records associated with the respective financial year. Profitability is the main

element that accounting team try to identify against reporting transactions under finance

accounting.

Management accounting: Management accounting is all about taking financial decisions or

related to business operations undertaken by organisation. Management accounting techniques

further include ratio analysis, investment decision-making and other types of the assessment that

can empower the organisation to improve growth of company. Management accounting also

include cost accounting under which different costing methods such as job costing, batch costing

and other such techniques used by the Skansa Plc to take the best and profitable business

decision-making (Asandimitra and Kautsar, 2019). In context to the business growth and

development decision-making is a key tool that is used by organisation to maximise its growth

possibility. This part of operations include different roles and responsibilities such as forecasting

future growth, make or buy decisions, forecasting cash flows, understanding performance

variance and also to analysis the rate of return against a certain investment. This part of

accounting put a direct influence over the growth and development possibility of business

organisation. Skansa Plc also try to take competitive advantage with support of this technique

and accounting practice.

Management of Skansa Plc has allotted certain responsibilities such as financial

accounting, management accounting, tax functions and auditing functions to the accounts

departments. All these are the four primarily functions related to the accounting.

Finance accounting: Finance accounting is among the primary role and responsibility that

accounts department play in Skansa Plc. Financial accounting is more like utilising the series of

accounting principles and practices in order to represent the financial position of business entity

in the best way possible. Skansa Plc follow accrual basis when it comes to reporting the

financial position of the organisation. Accounts department classified financial data in certain

ways such as revenue, expenses, assets, liability and equity (Alkaraan, 2018). Revenue and

expenses are accounted and reported in the income statement of the respective financial year.

Assets, liability and equity accounts are projected under the balance sheet section of the

financial accounting. The basic aim behind the finance accounting is that to present or reflect the

accounting records associated with the respective financial year. Profitability is the main

element that accounting team try to identify against reporting transactions under finance

accounting.

Management accounting: Management accounting is all about taking financial decisions or

related to business operations undertaken by organisation. Management accounting techniques

further include ratio analysis, investment decision-making and other types of the assessment that

can empower the organisation to improve growth of company. Management accounting also

include cost accounting under which different costing methods such as job costing, batch costing

and other such techniques used by the Skansa Plc to take the best and profitable business

decision-making (Asandimitra and Kautsar, 2019). In context to the business growth and

development decision-making is a key tool that is used by organisation to maximise its growth

possibility. This part of operations include different roles and responsibilities such as forecasting

future growth, make or buy decisions, forecasting cash flows, understanding performance

variance and also to analysis the rate of return against a certain investment. This part of

accounting put a direct influence over the growth and development possibility of business

organisation. Skansa Plc also try to take competitive advantage with support of this technique

and accounting practice.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Tax functions: Tax functions are also coordinated by the accounts department of Skansa Plc.

This includes on the basis of the net income reflected under the profit and loss account of

company for the respective financial year evaluating the tax liability business entity need to

meet. Tax is the liability which business entity mitigate against earning profits from business

operations (BAKAR and BAKAR, 2020). This is also a ethical responsibility attached with the

businesses to pay back to the society whatever society has given to business house against

channelising business operations. Role of accounts teams is only not restricted to assessing the

tax liability buyt also to pay the same to meet up the responsibility.

Auditing functions: Audit is all about authorising the authenticity of the financial records such

as trading accounting, profit and loss statement and the balance sheet of company. This is about

to authenticate that the accounting treatment company has done is fair and as per the accounting

principles and requirements attached with accounting standards applicable over company

(Bawole and Adjei-Bamfo, 2020). Skansa Plc needs to conduct audit every year as this is the

mandatory requirements associated with the company act. Audit report also present by the board

of director of company in the annual general meeting held every year. Accounts department look

all the responsibilities associated with auditing the financial statements of business entity.

Finance department

Finance department is also associated with the organisation hierarchy in Skansa Plc.

Finance department in Skansa Plc play roles and responsibilities like inveterate functions,

funding functions, dividend functions and working capital functions. All the four different

functions allow the business entity to achieve high growth possibility in respective market.

Investment function: Finance department of the Skansa Plc play role in taking investment

decisions that can empower the business entity to achieve all business objectives. Investment

decision is made by the company with support of different techniques like net present value

method, payback period method, investment rate of return technique and such other techniques

and methods. Capital and financial resources are minimum which further imposed the balanced

between risk and reward when it comes to making investment decision (Boisjoly and et.al.,

2020). Investment functions can be stated as the core function and responsibility associated with

the finance department. This is a huge challenge to select a particular investment among

multiple options with support of different methods. As every method of investment decision-

making contain certain level of limitation that restrict the management taking best level of

This includes on the basis of the net income reflected under the profit and loss account of

company for the respective financial year evaluating the tax liability business entity need to

meet. Tax is the liability which business entity mitigate against earning profits from business

operations (BAKAR and BAKAR, 2020). This is also a ethical responsibility attached with the

businesses to pay back to the society whatever society has given to business house against

channelising business operations. Role of accounts teams is only not restricted to assessing the

tax liability buyt also to pay the same to meet up the responsibility.

Auditing functions: Audit is all about authorising the authenticity of the financial records such

as trading accounting, profit and loss statement and the balance sheet of company. This is about

to authenticate that the accounting treatment company has done is fair and as per the accounting

principles and requirements attached with accounting standards applicable over company

(Bawole and Adjei-Bamfo, 2020). Skansa Plc needs to conduct audit every year as this is the

mandatory requirements associated with the company act. Audit report also present by the board

of director of company in the annual general meeting held every year. Accounts department look

all the responsibilities associated with auditing the financial statements of business entity.

Finance department

Finance department is also associated with the organisation hierarchy in Skansa Plc.

Finance department in Skansa Plc play roles and responsibilities like inveterate functions,

funding functions, dividend functions and working capital functions. All the four different

functions allow the business entity to achieve high growth possibility in respective market.

Investment function: Finance department of the Skansa Plc play role in taking investment

decisions that can empower the business entity to achieve all business objectives. Investment

decision is made by the company with support of different techniques like net present value

method, payback period method, investment rate of return technique and such other techniques

and methods. Capital and financial resources are minimum which further imposed the balanced

between risk and reward when it comes to making investment decision (Boisjoly and et.al.,

2020). Investment functions can be stated as the core function and responsibility associated with

the finance department. This is a huge challenge to select a particular investment among

multiple options with support of different methods. As every method of investment decision-

making contain certain level of limitation that restrict the management taking best level of

decision. Finance team choose a particular technique or method to choose the investment

decision-making.

Financing function: Financing function involve formulating budget so that proper funding

could have been allotted for every single functional area associated with the business entity.

Budget is all about projecting the expected financial needs and requirements of business entity

that can empower every single department of Skansa Plc meeting all responsibilities and sustain

a good flow of operations (Herranz and et.al., 2017). Financial resources are prominent and

empower the entity to achieve smooth control over operations. Financing function is stated as

the primary role and responsibility finance department play in company.

Dividend function: Dividend function is denoted as finalising how much dividend company

needed to pay to its shareholders and investors. This is another crucial function that finance

department play ion company. Shareholders also contain expectations against the capital;

resources they allocate to the Skansa Plc. Dividend is the return shareholders earn against the

investment decision they made in business functions of company. Under this responsibility

finance professionals require taking decision over the level of dividend needed to pay to

shareholders and investors so that more investment could have been attracted towards the

business entity.

Working capital function: Working capital is defined as the financial resources required to

mitigate day to day responsibility. Working capital is the balance between current nature asserts

of company and current liability associated with respective financial year of business entity. In

clear term it can reflect that working capital is the liquidity that in any situation Skansa Plc

required to sustain to achieve smooth control over functional responsibilities. There are certain

responsibilities which Skansa Plc maintain with support of working capital management such as

it allow company to hold strong liquidity position in business. It also evades the company

getting interruption in operations of company. It also enhances profitability of company against

operations (Marqués, García and Sánchez, 2020). This support the financial health of the

Skansa Plc. It can be projected that working capital play role of value addition in favour of the

business entity. Finance department play role in sustaining proper working capital and meet up

the needs and requirements associated with the business entity related to management of

company's working capital in business.

decision-making.

Financing function: Financing function involve formulating budget so that proper funding

could have been allotted for every single functional area associated with the business entity.

Budget is all about projecting the expected financial needs and requirements of business entity

that can empower every single department of Skansa Plc meeting all responsibilities and sustain

a good flow of operations (Herranz and et.al., 2017). Financial resources are prominent and

empower the entity to achieve smooth control over operations. Financing function is stated as

the primary role and responsibility finance department play in company.

Dividend function: Dividend function is denoted as finalising how much dividend company

needed to pay to its shareholders and investors. This is another crucial function that finance

department play ion company. Shareholders also contain expectations against the capital;

resources they allocate to the Skansa Plc. Dividend is the return shareholders earn against the

investment decision they made in business functions of company. Under this responsibility

finance professionals require taking decision over the level of dividend needed to pay to

shareholders and investors so that more investment could have been attracted towards the

business entity.

Working capital function: Working capital is defined as the financial resources required to

mitigate day to day responsibility. Working capital is the balance between current nature asserts

of company and current liability associated with respective financial year of business entity. In

clear term it can reflect that working capital is the liquidity that in any situation Skansa Plc

required to sustain to achieve smooth control over functional responsibilities. There are certain

responsibilities which Skansa Plc maintain with support of working capital management such as

it allow company to hold strong liquidity position in business. It also evades the company

getting interruption in operations of company. It also enhances profitability of company against

operations (Marqués, García and Sánchez, 2020). This support the financial health of the

Skansa Plc. It can be projected that working capital play role of value addition in favour of the

business entity. Finance department play role in sustaining proper working capital and meet up

the needs and requirements associated with the business entity related to management of

company's working capital in business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above mentioned roles and responsibilities are associated with the finance and

account department associated with the organisation hierarchy of Skansa Plc. It becomes

essential that both the department effectively sustain healthy control in between the functional

responsibilities attached with the accounts and finance department of company. In order to

manage the effective financial health both the departments requires to deal with the associated

responsibilities effectively.

Task 2

Ratio analysis

Ratio is the statistical representation of the performance of business entity. Ratio supports the

business entity to monitor the performance of entity in respective market. Performance

evaluation is the process where based on certain ratios overall performance of business entity is

monitored and measured. This involves ratios such as return on capital employed, net profit

margins, current ratio, average receivable days and average payable days.

Return on capital employed:

Earning before interest and tax / Capital employed (Total asset – current liability) * 100

2019

1650 / 5850 (8070 – 2220) * 100

= 28.21%

2018

1350 / 3830 (4470 – 645) * 100

= 35.25%

Return on capital employed is a term denoted the total revenue company could era

against the capital employed or the liquidity it has sustained in business. Revenue under this

ratio is about the earning Skansa Plc has earned before the interest and tax. This can be stated as

the revenue business entity could get against the operation and functions it has performed in

trading. Financial records reflect that Skansa Plc could face downfall in its return on capital

employed ratio. This clearly state that it has faced a downfall in sales for the year 2019 as

compare to the year 2018 that is further reflecting under this ratio. The down fall is

approximately 7.04% which is huge in one year (Mishra, 2018). There might be certain reason

such as product quality, marketing glitches, customer satisfaction related issues and many other

issues that could effect the level of consumer satisfaction business entity could gain against

account department associated with the organisation hierarchy of Skansa Plc. It becomes

essential that both the department effectively sustain healthy control in between the functional

responsibilities attached with the accounts and finance department of company. In order to

manage the effective financial health both the departments requires to deal with the associated

responsibilities effectively.

Task 2

Ratio analysis

Ratio is the statistical representation of the performance of business entity. Ratio supports the

business entity to monitor the performance of entity in respective market. Performance

evaluation is the process where based on certain ratios overall performance of business entity is

monitored and measured. This involves ratios such as return on capital employed, net profit

margins, current ratio, average receivable days and average payable days.

Return on capital employed:

Earning before interest and tax / Capital employed (Total asset – current liability) * 100

2019

1650 / 5850 (8070 – 2220) * 100

= 28.21%

2018

1350 / 3830 (4470 – 645) * 100

= 35.25%

Return on capital employed is a term denoted the total revenue company could era

against the capital employed or the liquidity it has sustained in business. Revenue under this

ratio is about the earning Skansa Plc has earned before the interest and tax. This can be stated as

the revenue business entity could get against the operation and functions it has performed in

trading. Financial records reflect that Skansa Plc could face downfall in its return on capital

employed ratio. This clearly state that it has faced a downfall in sales for the year 2019 as

compare to the year 2018 that is further reflecting under this ratio. The down fall is

approximately 7.04% which is huge in one year (Mishra, 2018). There might be certain reason

such as product quality, marketing glitches, customer satisfaction related issues and many other

issues that could effect the level of consumer satisfaction business entity could gain against

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

channelising business operations. 2019 was further a challenging year for many companies as

pandemic has also arises in the respective financial year. In order to improve the return on

capital employed Skansa Plc can focus over increasing its sales in the future. Further this is

important that the organisation can take decision reading control the operational cost so that

more earning can be addressed before interest and tax liabilities. This will make earning before

interest and tax stronger. Company can also take better decision to improve the working capital

management so that more effective numbers can demonstrate in future related to this particular

ratio.

Net profit margin:

Net profit / sales * 100

2019

675 / 6000 * 100

= 11.25%

2018

600 / 4800 * 100

= 12.5%

Net profit margin is the net advantage and financial benefits company is getting against

channelising business operations. This is the net profitability iof the business entity of the

respective financial year. Net profit is the revenue left in the bank of company after deducting

all possible expenditures for the respective financial year. Skansa Plc could earn the net profit

margin in the year 2018 was 12.5% whereas in the year 2019 the ratio is 11.25%. There is

significant downfall in the net profitability level of the business entity in the year 2019 as

compare to the financial year 2018. This clearly reflect that Skansa Plc could address reduced

level of profitability against the business operations entertained by company. The possible

reason behind the lower profit margin is probably company has addressed mow sales in the year

2019 as compare to the year 2018 (Setyawati and Suroso, 2017). Along with reduced sales

further the operational cost might also be more than the previous financial year that has also

created negative impact over the profit margin company has earned. In future for improving the

profitability business entity can take strong decisions to improve the sales of company. Further

the decision can also be taken against reducing the level of expenditures business entity has

pandemic has also arises in the respective financial year. In order to improve the return on

capital employed Skansa Plc can focus over increasing its sales in the future. Further this is

important that the organisation can take decision reading control the operational cost so that

more earning can be addressed before interest and tax liabilities. This will make earning before

interest and tax stronger. Company can also take better decision to improve the working capital

management so that more effective numbers can demonstrate in future related to this particular

ratio.

Net profit margin:

Net profit / sales * 100

2019

675 / 6000 * 100

= 11.25%

2018

600 / 4800 * 100

= 12.5%

Net profit margin is the net advantage and financial benefits company is getting against

channelising business operations. This is the net profitability iof the business entity of the

respective financial year. Net profit is the revenue left in the bank of company after deducting

all possible expenditures for the respective financial year. Skansa Plc could earn the net profit

margin in the year 2018 was 12.5% whereas in the year 2019 the ratio is 11.25%. There is

significant downfall in the net profitability level of the business entity in the year 2019 as

compare to the financial year 2018. This clearly reflect that Skansa Plc could address reduced

level of profitability against the business operations entertained by company. The possible

reason behind the lower profit margin is probably company has addressed mow sales in the year

2019 as compare to the year 2018 (Setyawati and Suroso, 2017). Along with reduced sales

further the operational cost might also be more than the previous financial year that has also

created negative impact over the profit margin company has earned. In future for improving the

profitability business entity can take strong decisions to improve the sales of company. Further

the decision can also be taken against reducing the level of expenditures business entity has

involved in against delivering business responsibilities. Net profit is the true indicator of the

performance of company and by enhancing the profit margin company can further strong the

portfolio of business.

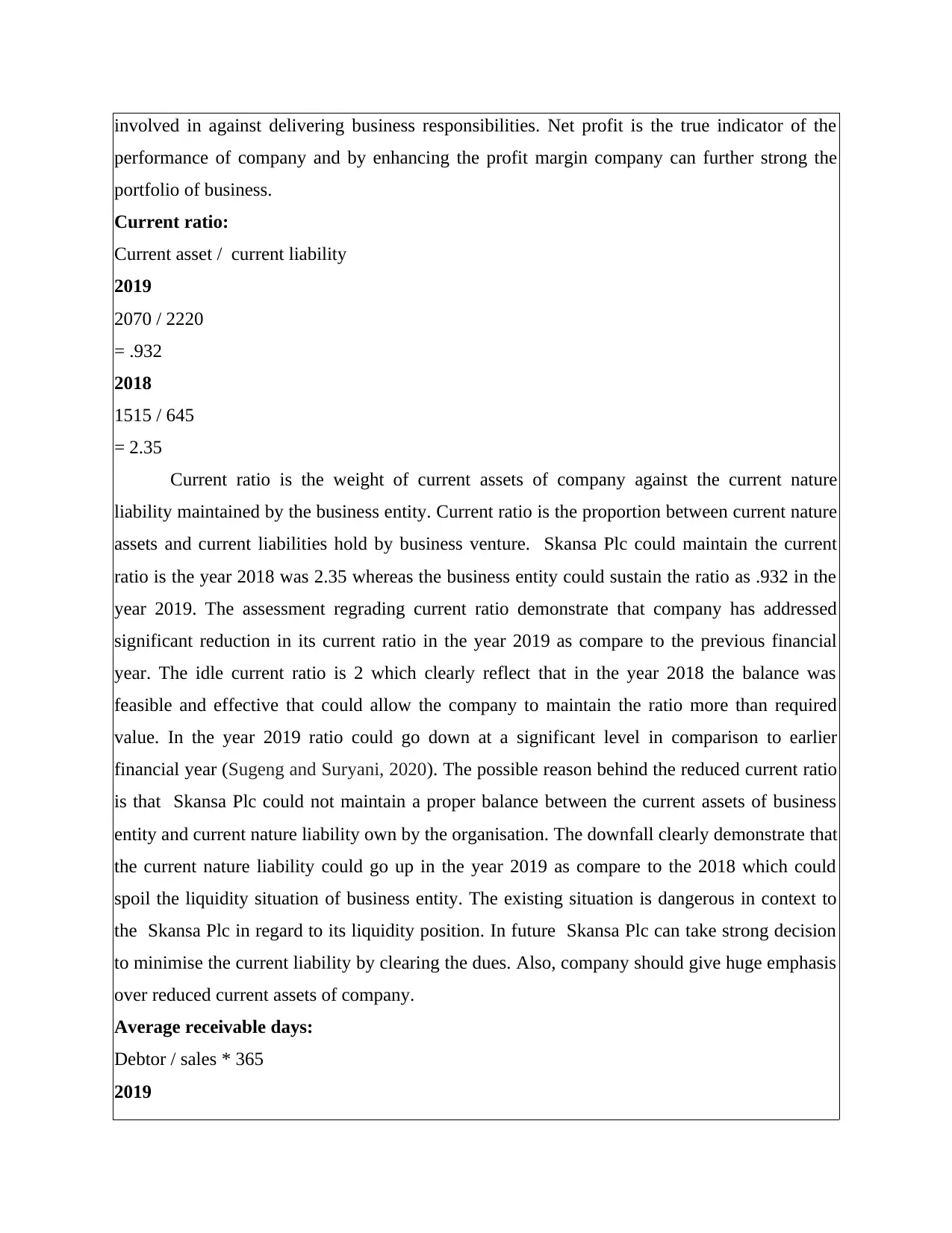

Current ratio:

Current asset / current liability

2019

2070 / 2220

= .932

2018

1515 / 645

= 2.35

Current ratio is the weight of current assets of company against the current nature

liability maintained by the business entity. Current ratio is the proportion between current nature

assets and current liabilities hold by business venture. Skansa Plc could maintain the current

ratio is the year 2018 was 2.35 whereas the business entity could sustain the ratio as .932 in the

year 2019. The assessment regrading current ratio demonstrate that company has addressed

significant reduction in its current ratio in the year 2019 as compare to the previous financial

year. The idle current ratio is 2 which clearly reflect that in the year 2018 the balance was

feasible and effective that could allow the company to maintain the ratio more than required

value. In the year 2019 ratio could go down at a significant level in comparison to earlier

financial year (Sugeng and Suryani, 2020). The possible reason behind the reduced current ratio

is that Skansa Plc could not maintain a proper balance between the current assets of business

entity and current nature liability own by the organisation. The downfall clearly demonstrate that

the current nature liability could go up in the year 2019 as compare to the 2018 which could

spoil the liquidity situation of business entity. The existing situation is dangerous in context to

the Skansa Plc in regard to its liquidity position. In future Skansa Plc can take strong decision

to minimise the current liability by clearing the dues. Also, company should give huge emphasis

over reduced current assets of company.

Average receivable days:

Debtor / sales * 365

2019

performance of company and by enhancing the profit margin company can further strong the

portfolio of business.

Current ratio:

Current asset / current liability

2019

2070 / 2220

= .932

2018

1515 / 645

= 2.35

Current ratio is the weight of current assets of company against the current nature

liability maintained by the business entity. Current ratio is the proportion between current nature

assets and current liabilities hold by business venture. Skansa Plc could maintain the current

ratio is the year 2018 was 2.35 whereas the business entity could sustain the ratio as .932 in the

year 2019. The assessment regrading current ratio demonstrate that company has addressed

significant reduction in its current ratio in the year 2019 as compare to the previous financial

year. The idle current ratio is 2 which clearly reflect that in the year 2018 the balance was

feasible and effective that could allow the company to maintain the ratio more than required

value. In the year 2019 ratio could go down at a significant level in comparison to earlier

financial year (Sugeng and Suryani, 2020). The possible reason behind the reduced current ratio

is that Skansa Plc could not maintain a proper balance between the current assets of business

entity and current nature liability own by the organisation. The downfall clearly demonstrate that

the current nature liability could go up in the year 2019 as compare to the 2018 which could

spoil the liquidity situation of business entity. The existing situation is dangerous in context to

the Skansa Plc in regard to its liquidity position. In future Skansa Plc can take strong decision

to minimise the current liability by clearing the dues. Also, company should give huge emphasis

over reduced current assets of company.

Average receivable days:

Debtor / sales * 365

2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1200 / 6000 * 365

= 73 Days

2018

900 / 4800 * 365

= 68.44 Days

Average receivable days is the average time required to recover the debtor amount. This

time is the average number of days company is allowing to its debtor to pay all the due value to

Skansa Plc. The average receivable days are 68.44 days in the year 2018 whereas the days could

go up in the year 2019 from 68.44 days to 73 days. This clearly reflect that the organisation is

allowing or taking more time to recover its debtor as compare to the previous financial year.

This also create a huge impact over the liquidity position of business entity. In order to maintain

strong liquidity position business entity required to ensure proper control over maintaining

debtor in such way that they do not take or consume much time to repay the due value

(Wahyuni, 2020). The possible reason behind the increased debtor collection period is that the

market could face a downfall which also influenced the sales of Skansa Plc. The downfall in

market could cause into low turnover like debtor, net profit margin and other such issues. The

existing situation is not positive and company should communicate with its debtor to recover the

due amount as soon as possible. Proper communication on a constant basis is the key way to

achieve the lower turnover ratio.

Average payable days:

Trade payable / cost of sale * 365

2019

2100 / 4350 * 365

= 176.21 Days

2018

570 / 3450 * 365

= 60.304 Days

Average payable period is the time company is taking to repay its creditor. This is the

average number of days business entity is getting to clear al the dues against the creditor of

business venture. IN the year 2018 the Skansa Plc could maintain its average payment period as

60.304 days on the other hand the days could go at 176.21 days in the year 2019. This is a huge

= 73 Days

2018

900 / 4800 * 365

= 68.44 Days

Average receivable days is the average time required to recover the debtor amount. This

time is the average number of days company is allowing to its debtor to pay all the due value to

Skansa Plc. The average receivable days are 68.44 days in the year 2018 whereas the days could

go up in the year 2019 from 68.44 days to 73 days. This clearly reflect that the organisation is

allowing or taking more time to recover its debtor as compare to the previous financial year.

This also create a huge impact over the liquidity position of business entity. In order to maintain

strong liquidity position business entity required to ensure proper control over maintaining

debtor in such way that they do not take or consume much time to repay the due value

(Wahyuni, 2020). The possible reason behind the increased debtor collection period is that the

market could face a downfall which also influenced the sales of Skansa Plc. The downfall in

market could cause into low turnover like debtor, net profit margin and other such issues. The

existing situation is not positive and company should communicate with its debtor to recover the

due amount as soon as possible. Proper communication on a constant basis is the key way to

achieve the lower turnover ratio.

Average payable days:

Trade payable / cost of sale * 365

2019

2100 / 4350 * 365

= 176.21 Days

2018

570 / 3450 * 365

= 60.304 Days

Average payable period is the time company is taking to repay its creditor. This is the

average number of days business entity is getting to clear al the dues against the creditor of

business venture. IN the year 2018 the Skansa Plc could maintain its average payment period as

60.304 days on the other hand the days could go at 176.21 days in the year 2019. This is a huge

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

change or difference business entity has addressed. This further influence the company's brand

image in respective market (White and et.al., 2019). The possible reason behind the increased

payable period is that the sacrificed liquidity position of the organisation. Company should take

decisions regarding improving the liquidity position so that it will get proper financial resources

to repay all its creditor. As the increased creditor payable period completely demolish the brand

value and goodwill in market.

CONCLUSION

Accounting and finance department pay role and responsibilities in company such as

financial accounting, management accounting, tax functions and auditing functions are the

primary role and responsibility attached with the account department. Finance department

further pay role and responsibilities like investment function, financing function, dividend

function and working capital function. All these are the primary role and responsibilities

associated with the accounting and finance department of company. Skansa Plc could not

perform much effectively in the year 2019 as compare to the year 2018. It is recommended that

in current time any investment made in company is not safe. More time can be taken to analysis

the performance of business entity before taking any investment decision in organisation.

image in respective market (White and et.al., 2019). The possible reason behind the increased

payable period is that the sacrificed liquidity position of the organisation. Company should take

decisions regarding improving the liquidity position so that it will get proper financial resources

to repay all its creditor. As the increased creditor payable period completely demolish the brand

value and goodwill in market.

CONCLUSION

Accounting and finance department pay role and responsibilities in company such as

financial accounting, management accounting, tax functions and auditing functions are the

primary role and responsibility attached with the account department. Finance department

further pay role and responsibilities like investment function, financing function, dividend

function and working capital function. All these are the primary role and responsibilities

associated with the accounting and finance department of company. Skansa Plc could not

perform much effectively in the year 2019 as compare to the year 2018. It is recommended that

in current time any investment made in company is not safe. More time can be taken to analysis

the performance of business entity before taking any investment decision in organisation.

REFERENCES

Books and Journals

Al Muhairi, M. and Nobanee, H., 2019. Sustainable financial management. Available at SSRN

3472417.

Alkaraan, F., 2018. Public financial management reform: an ongoing journey towards good

governance. Journal of Financial Reporting and Accounting.

Asandimitra, N. and Kautsar, A., 2019. The Influence of Financial Information, Financial Self

Efficacy, and Emotional Intelligence to Financial Management Behavior of Female

Lecturer. Humanities & Social Sciences Reviews. 7(6). pp.1112-1124.

BAKAR, M. Z. A. and BAKAR, S. A., 2020. Prudent financial management practices among

Malaysian youth: The moderating roles of financial education. The Journal of Asian

Finance, Economics, and Business. 7(6). pp.525-535.

Bawole, J. N. and Adjei-Bamfo, P., 2020. Public procurement and public financial management

in Africa: Dynamics and influences. Public Organization Review. 20(2). pp.301-318.

Boisjoly, R. P. and et.al., 2020. Working capital management: Financial and valuation

impacts. Journal of Business Research. 108. pp.1-8.

Herranz, R. E. and et.al., 2017. Leveraging financial management performance of the Spanish

aerospace manufacturing value chain. Journal of Business Economics and

Management. 18(5). pp.1005-1022.

Marqués, A. I., García, V. and Sánchez, J. S., 2020. Ranking-based MCDM models in financial

management applications: analysis and emerging challenges. Progress in Artificial

Intelligence. 9. pp.171-193.

Mishra, S., 2018. Financial management and forecasting using business intelligence and big

data analytic tools. International Journal of Financial Engineering. 5(02). p.1850011.

Setyawati, I. and Suroso, S., 2017. Does the Sharia Personal Financial Management Require?

Study of Sharia Financial Literacy Among Lecturers. International Journal of

Economics and Financial Issues. 7(4).

Sugeng, B. and Suryani, A. W., 2020. Enhancing the learning performance of passive learners

in a financial management class using problem-based learning. Journal of University

Teaching & Learning Practice. 17(1). p.5.

Wahyuni, R. A. E., 2020. Strategy Of Illegal Technology Financial Management In Form Of

Online Loans. Jurnal Hukum Prasada. 7(1). pp.27-33.

White, K. and et.al., 2019. The relationship between financial knowledge, financial

management, and financial self-efficacy among African-American students. Financial

Management, and Financial Self-Efficacy Among African-American Students (October

12, 2019).

Books and Journals

Al Muhairi, M. and Nobanee, H., 2019. Sustainable financial management. Available at SSRN

3472417.

Alkaraan, F., 2018. Public financial management reform: an ongoing journey towards good

governance. Journal of Financial Reporting and Accounting.

Asandimitra, N. and Kautsar, A., 2019. The Influence of Financial Information, Financial Self

Efficacy, and Emotional Intelligence to Financial Management Behavior of Female

Lecturer. Humanities & Social Sciences Reviews. 7(6). pp.1112-1124.

BAKAR, M. Z. A. and BAKAR, S. A., 2020. Prudent financial management practices among

Malaysian youth: The moderating roles of financial education. The Journal of Asian

Finance, Economics, and Business. 7(6). pp.525-535.

Bawole, J. N. and Adjei-Bamfo, P., 2020. Public procurement and public financial management

in Africa: Dynamics and influences. Public Organization Review. 20(2). pp.301-318.

Boisjoly, R. P. and et.al., 2020. Working capital management: Financial and valuation

impacts. Journal of Business Research. 108. pp.1-8.

Herranz, R. E. and et.al., 2017. Leveraging financial management performance of the Spanish

aerospace manufacturing value chain. Journal of Business Economics and

Management. 18(5). pp.1005-1022.

Marqués, A. I., García, V. and Sánchez, J. S., 2020. Ranking-based MCDM models in financial

management applications: analysis and emerging challenges. Progress in Artificial

Intelligence. 9. pp.171-193.

Mishra, S., 2018. Financial management and forecasting using business intelligence and big

data analytic tools. International Journal of Financial Engineering. 5(02). p.1850011.

Setyawati, I. and Suroso, S., 2017. Does the Sharia Personal Financial Management Require?

Study of Sharia Financial Literacy Among Lecturers. International Journal of

Economics and Financial Issues. 7(4).

Sugeng, B. and Suryani, A. W., 2020. Enhancing the learning performance of passive learners

in a financial management class using problem-based learning. Journal of University

Teaching & Learning Practice. 17(1). p.5.

Wahyuni, R. A. E., 2020. Strategy Of Illegal Technology Financial Management In Form Of

Online Loans. Jurnal Hukum Prasada. 7(1). pp.27-33.

White, K. and et.al., 2019. The relationship between financial knowledge, financial

management, and financial self-efficacy among African-American students. Financial

Management, and Financial Self-Efficacy Among African-American Students (October

12, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.