International Financial Management Report and Financial Analysis

VerifiedAdded on 2023/01/07

|10

|2232

|56

Report

AI Summary

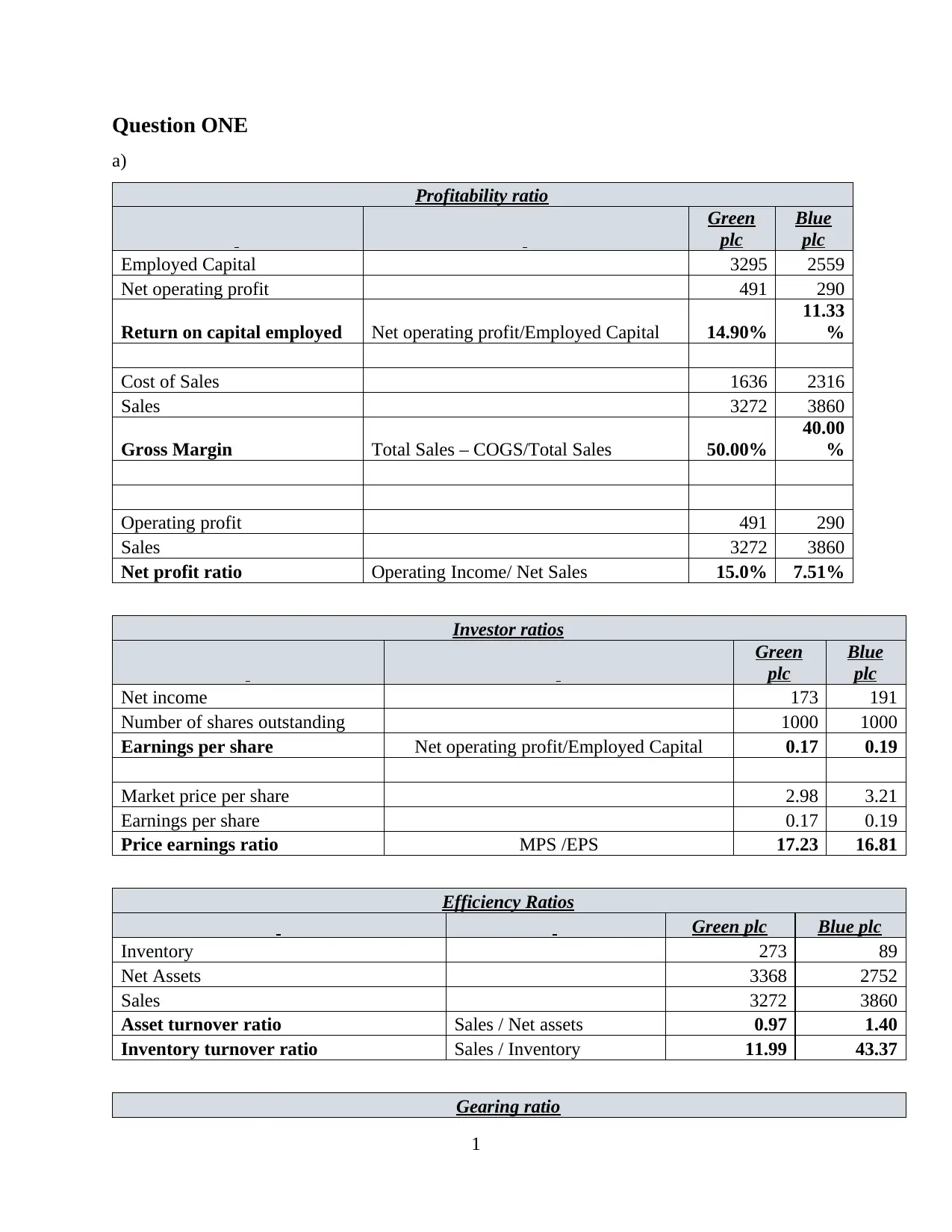

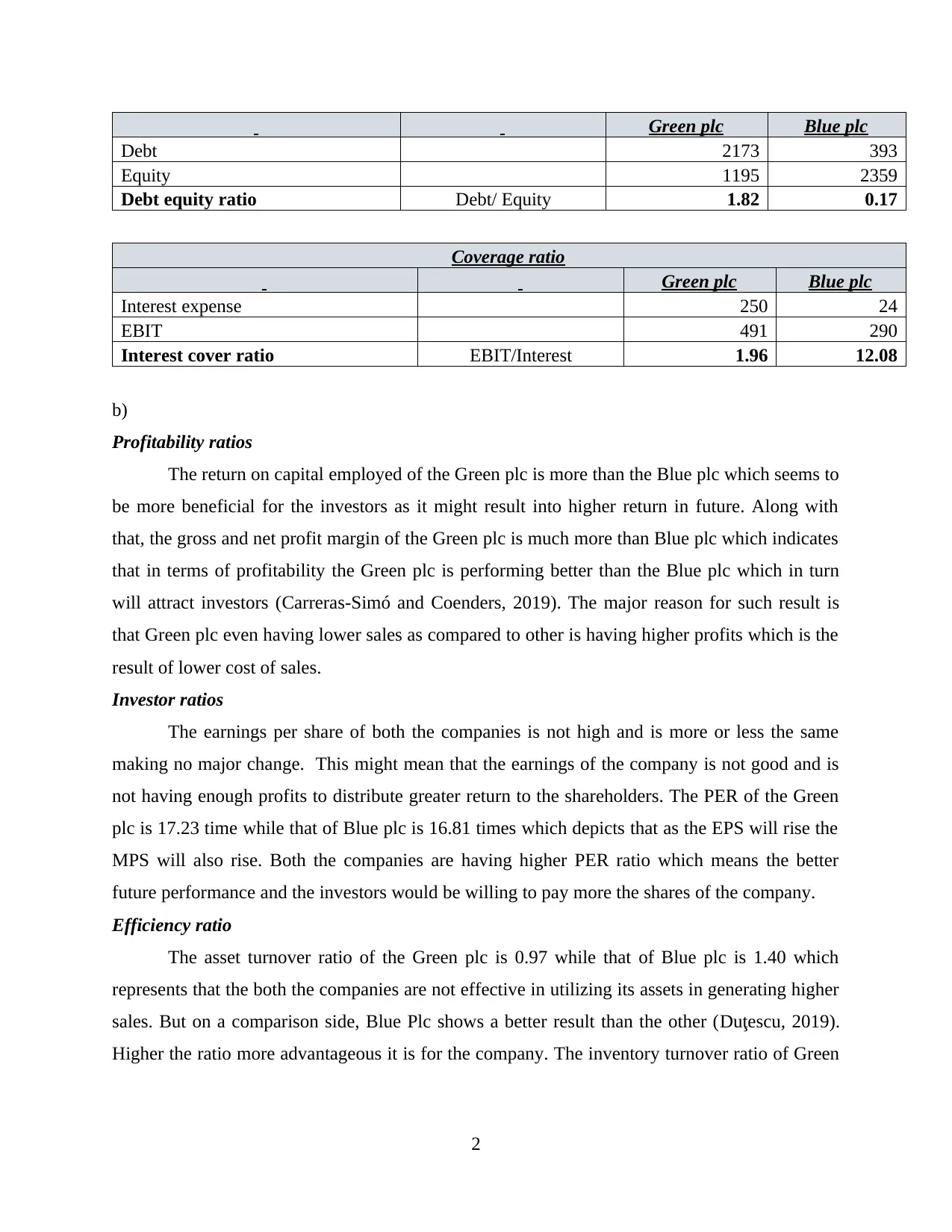

This report provides a comprehensive analysis of international financial management, encompassing three key questions. Question one delves into the profitability, investor, efficiency, and gearing ratios of two hypothetical companies, Green plc and Blue plc, comparing their financial performance. The analysis includes an assessment of the limitations of ratio analysis, such as its reliance on historical data and the potential impact of accounting practices. Question two focuses on calculating the Weighted Average Cost of Capital (WACC) for Art Co., using both book value and market value methods. The report explains the differences in WACC calculation based on these two methods and discusses the implications of WACC in investment decisions. Question three addresses the objectives of working capital management, emphasizing the trade-off between profitability and liquidity. It explores the conservative and aggressive approaches to working capital management and highlights the importance of effective working capital management for financial stability and investor returns. The report concludes with a list of cited references.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.