University of Sunderland APC308 Financial Management Report 2019

VerifiedAdded on 2023/01/16

|16

|4320

|71

Report

AI Summary

This financial management report delves into key concepts and calculations relevant to corporate finance. It begins by exploring the weighted average cost of capital (WACC), comparing market and book value calculations, and analyzing the impact of proposed capital structure changes by Kadlex Plc. The report then discusses the implications of gearing on WACC. Furthermore, the report examines the effects of short-termism on agency problems and bankruptcy. The core of the report involves a detailed analysis of investment appraisal techniques, including payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR), along with their respective advantages and limitations. Calculations are provided for a new machine purchase, illustrating the application of each technique. The report concludes with a summary of the findings and insights into financial decision-making.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a. Computation of market and book value cost of capital............................................................1

b. Recalculation of cost of capital of company............................................................................4

c. Discussion on minimisation of weighted average cost of capital by integrating the sensible

level of gearing in to the capital structure....................................................................................5

d. Effects of short-termism on agency problem and bankruptcy.................................................5

QUESTION 3...................................................................................................................................6

a. Calculation of different investment appraisal techniques such as pay back period, ARR,

NPV and IRR...............................................................................................................................6

b. Limitations and benefits of different investment appraisal techniques.................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

a. Computation of market and book value cost of capital............................................................1

b. Recalculation of cost of capital of company............................................................................4

c. Discussion on minimisation of weighted average cost of capital by integrating the sensible

level of gearing in to the capital structure....................................................................................5

d. Effects of short-termism on agency problem and bankruptcy.................................................5

QUESTION 3...................................................................................................................................6

a. Calculation of different investment appraisal techniques such as pay back period, ARR,

NPV and IRR...............................................................................................................................6

b. Limitations and benefits of different investment appraisal techniques.................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Financial management is the process of taking control over all the finance related

activities which are performed by an organisations for the purpose of achieving predetermined

business objectives. It is mainly focused with application of management principles to all the

monetary sources of entity. With the help of it, future requirements of funds for operations could

be determined (Antonopoulos and Hall, 2018). In order to make sure that all the procedures

related to it performed systematically it is very important for managers to analyse final accounts

appropriately so that judgements for future could be passed. For the completion of this report

questions one and three are selected. This assignment will cover various topics such as

calculation of market and book value of WACC, proposed changes in capital structure of

organisation and effect of short termism on bankruptcy and agency problem. Apart from this,

calculations with the help of different investment appraisal techniques along with their

advantages and disadvantages are also done in this project.

QUESTION 1

a. Computation of market and book value cost of capital

In all the organisations all the debts and equities are kept in a systematic manner which is

known as capital structure. In order to achieve all the objectives such as higher profitability,

large number of investors etc. it is very important for companies to make sure that they are

managing their securities appropriately (Baños-Caballero, García-Teruel and Martínez-Solano,

2016). While analysing it cost of capital is used to determine cost of all the equities, bonds, debts

etc. By analysing the financial statements the finance director of Kadlex Plc have assessed that

weighted average cost of capital of company is low. It is very important for the company to

improve it for this purpose the director have planned to issue new bonds in the market. The

impact of issuing them could be analysed with the help of below calculations:

For year 1 to 5 the growth are 21, 23, 25, 27 and 28 individually.

Calculation of growth=

Formula= Sn=S0*(1+g)n

28=21*(1+g)4

28/21=(1+g)4

1.33=(1+g)4

1

Financial management is the process of taking control over all the finance related

activities which are performed by an organisations for the purpose of achieving predetermined

business objectives. It is mainly focused with application of management principles to all the

monetary sources of entity. With the help of it, future requirements of funds for operations could

be determined (Antonopoulos and Hall, 2018). In order to make sure that all the procedures

related to it performed systematically it is very important for managers to analyse final accounts

appropriately so that judgements for future could be passed. For the completion of this report

questions one and three are selected. This assignment will cover various topics such as

calculation of market and book value of WACC, proposed changes in capital structure of

organisation and effect of short termism on bankruptcy and agency problem. Apart from this,

calculations with the help of different investment appraisal techniques along with their

advantages and disadvantages are also done in this project.

QUESTION 1

a. Computation of market and book value cost of capital

In all the organisations all the debts and equities are kept in a systematic manner which is

known as capital structure. In order to achieve all the objectives such as higher profitability,

large number of investors etc. it is very important for companies to make sure that they are

managing their securities appropriately (Baños-Caballero, García-Teruel and Martínez-Solano,

2016). While analysing it cost of capital is used to determine cost of all the equities, bonds, debts

etc. By analysing the financial statements the finance director of Kadlex Plc have assessed that

weighted average cost of capital of company is low. It is very important for the company to

improve it for this purpose the director have planned to issue new bonds in the market. The

impact of issuing them could be analysed with the help of below calculations:

For year 1 to 5 the growth are 21, 23, 25, 27 and 28 individually.

Calculation of growth=

Formula= Sn=S0*(1+g)n

28=21*(1+g)4

28/21=(1+g)4

1.33=(1+g)4

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

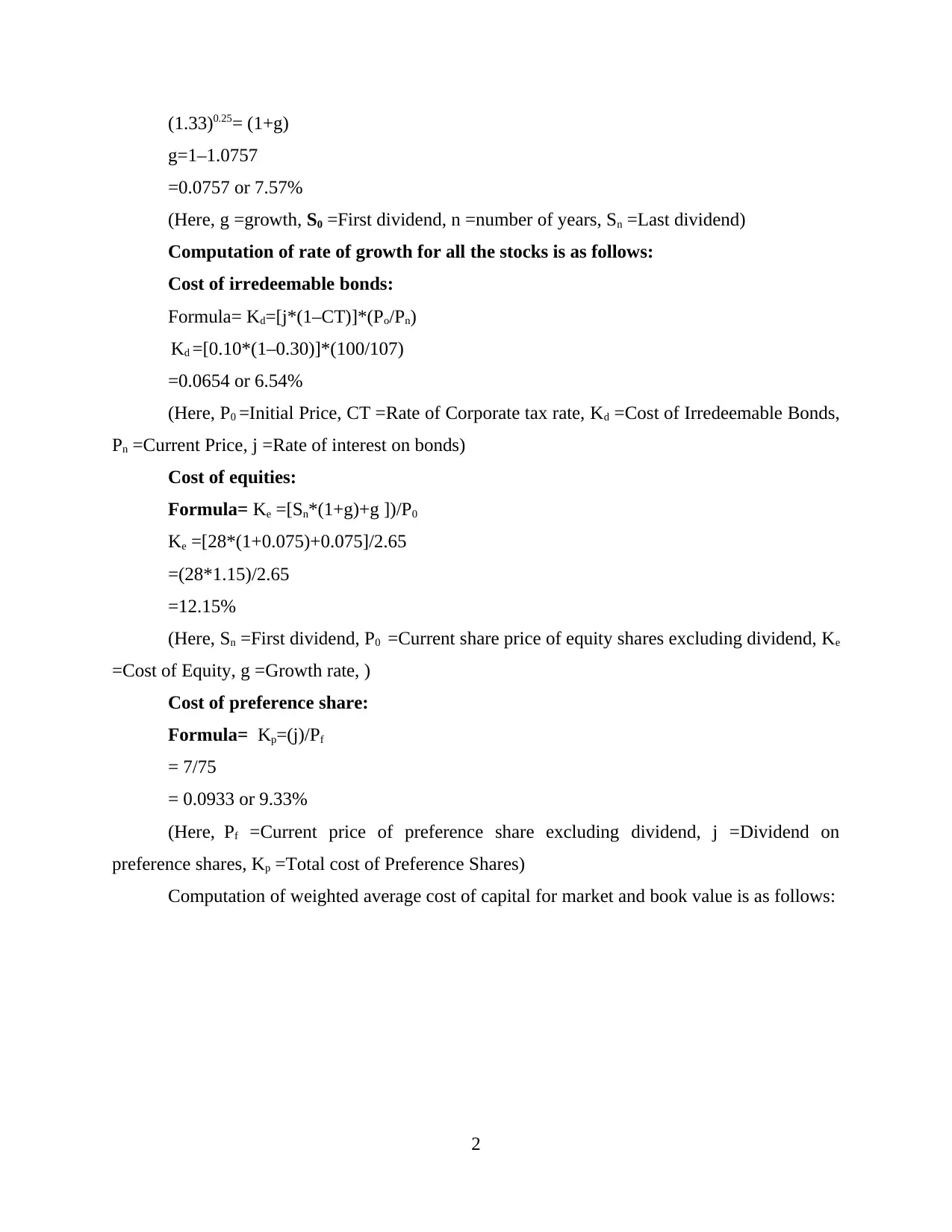

(1.33)0.25= (1+g)

g=1–1.0757

=0.0757 or 7.57%

(Here, g =growth, S0 =First dividend, n =number of years, Sn =Last dividend)

Computation of rate of growth for all the stocks is as follows:

Cost of irredeemable bonds:

Formula= Kd=[j*(1–CT)]*(Po/Pn)

Kd =[0.10*(1–0.30)]*(100/107)

=0.0654 or 6.54%

(Here, P0 =Initial Price, CT =Rate of Corporate tax rate, Kd =Cost of Irredeemable Bonds,

Pn =Current Price, j =Rate of interest on bonds)

Cost of equities:

Formula= Ke =[Sn*(1+g)+g ])/P0

Ke =[28*(1+0.075)+0.075]/2.65

=(28*1.15)/2.65

=12.15%

(Here, Sn =First dividend, P0 =Current share price of equity shares excluding dividend, Ke

=Cost of Equity, g =Growth rate, )

Cost of preference share:

Formula= Kp=(j)/Pf

= 7/75

= 0.0933 or 9.33%

(Here, Pf =Current price of preference share excluding dividend, j =Dividend on

preference shares, Kp =Total cost of Preference Shares)

Computation of weighted average cost of capital for market and book value is as follows:

2

g=1–1.0757

=0.0757 or 7.57%

(Here, g =growth, S0 =First dividend, n =number of years, Sn =Last dividend)

Computation of rate of growth for all the stocks is as follows:

Cost of irredeemable bonds:

Formula= Kd=[j*(1–CT)]*(Po/Pn)

Kd =[0.10*(1–0.30)]*(100/107)

=0.0654 or 6.54%

(Here, P0 =Initial Price, CT =Rate of Corporate tax rate, Kd =Cost of Irredeemable Bonds,

Pn =Current Price, j =Rate of interest on bonds)

Cost of equities:

Formula= Ke =[Sn*(1+g)+g ])/P0

Ke =[28*(1+0.075)+0.075]/2.65

=(28*1.15)/2.65

=12.15%

(Here, Sn =First dividend, P0 =Current share price of equity shares excluding dividend, Ke

=Cost of Equity, g =Growth rate, )

Cost of preference share:

Formula= Kp=(j)/Pf

= 7/75

= 0.0933 or 9.33%

(Here, Pf =Current price of preference share excluding dividend, j =Dividend on

preference shares, Kp =Total cost of Preference Shares)

Computation of weighted average cost of capital for market and book value is as follows:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

WACC calculations at market and book value are as follows:

WACC (Weighted average cost of capital) at market value:

Formula= [(Ke*MVe)+(Kp*MVp)+(Kd*MVd)]/Total Capital

=[(0.12*53000)+(0.09*7500)+(0.07*16050)]/76550

=[6360+675+1124]/76550

=8159/76550

= 0.1066 or 10.66%]

WACC (Weighted average cost of capital) at book value:

Formula= [(Ke*BVe)+(Kp*BVp)+(Kd*BVd)]/Total capital

=[(0.12*25000)+(0.09*10000)+(0.07*15000)]/50000

=[3000+900+1050]/50000

=4950/50000

=0.099 or 9.9%

(Here, MVp =Market value of all the preference shares, Mvd =Market value of debts of

organisation, MVe =Market value of total equities, Kp =Total cost of preference shares before

making changes, Ke =Total cost of equity before making changes, Kd =Total cost of debts before

3

WACC (Weighted average cost of capital) at market value:

Formula= [(Ke*MVe)+(Kp*MVp)+(Kd*MVd)]/Total Capital

=[(0.12*53000)+(0.09*7500)+(0.07*16050)]/76550

=[6360+675+1124]/76550

=8159/76550

= 0.1066 or 10.66%]

WACC (Weighted average cost of capital) at book value:

Formula= [(Ke*BVe)+(Kp*BVp)+(Kd*BVd)]/Total capital

=[(0.12*25000)+(0.09*10000)+(0.07*15000)]/50000

=[3000+900+1050]/50000

=4950/50000

=0.099 or 9.9%

(Here, MVp =Market value of all the preference shares, Mvd =Market value of debts of

organisation, MVe =Market value of total equities, Kp =Total cost of preference shares before

making changes, Ke =Total cost of equity before making changes, Kd =Total cost of debts before

3

applying changes, BVp =Actual book values of preference shares, Bve =Actual book value of

equities, BVd =Actual book value of debts for the organisation, Total capital =book + market

value of all the securities)

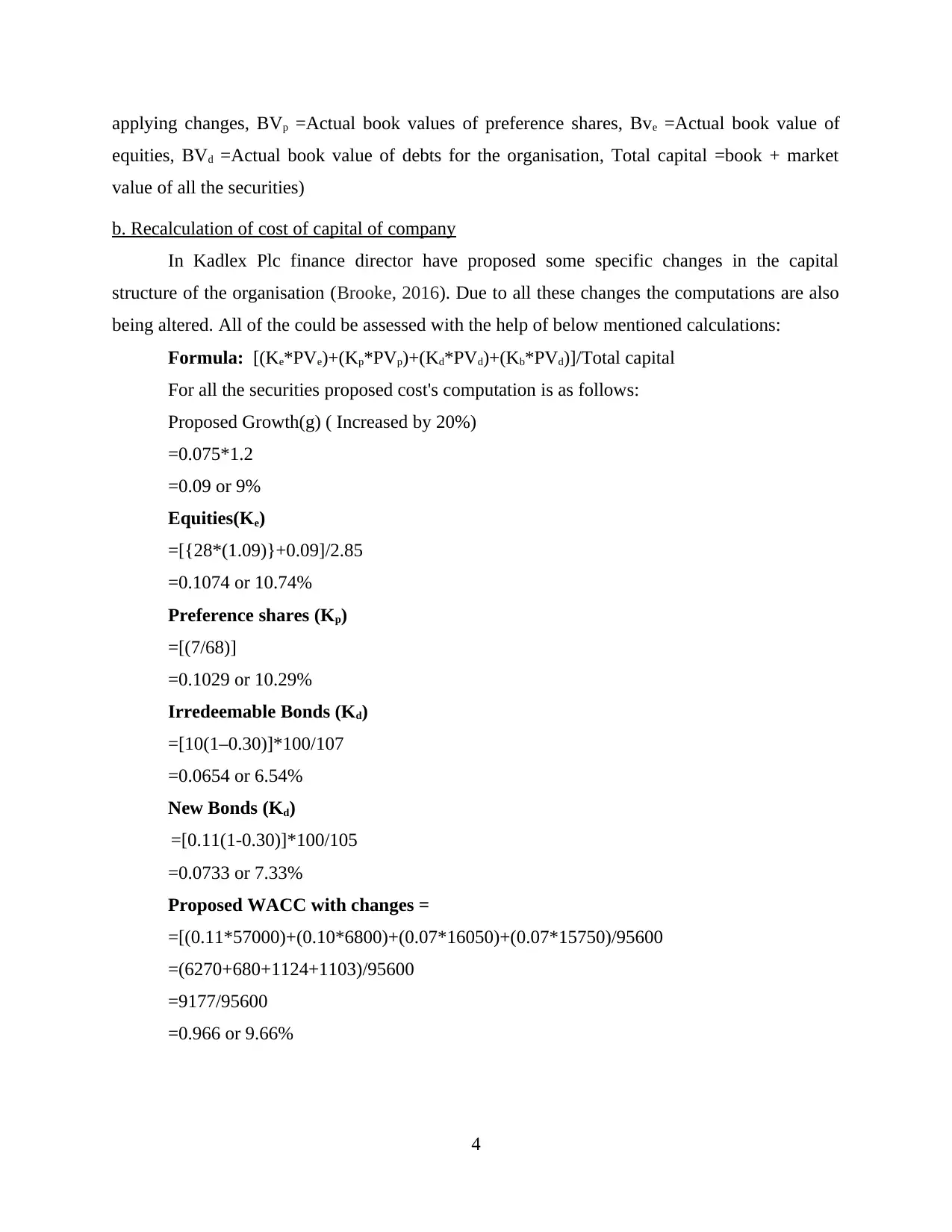

b. Recalculation of cost of capital of company

In Kadlex Plc finance director have proposed some specific changes in the capital

structure of the organisation (Brooke, 2016). Due to all these changes the computations are also

being altered. All of the could be assessed with the help of below mentioned calculations:

Formula: [(Ke*PVe)+(Kp*PVp)+(Kd*PVd)+(Kb*PVd)]/Total capital

For all the securities proposed cost's computation is as follows:

Proposed Growth(g) ( Increased by 20%)

=0.075*1.2

=0.09 or 9%

Equities(Ke)

=[{28*(1.09)}+0.09]/2.85

=0.1074 or 10.74%

Preference shares (Kp)

=[(7/68)]

=0.1029 or 10.29%

Irredeemable Bonds (Kd)

=[10(1–0.30)]*100/107

=0.0654 or 6.54%

New Bonds (Kd)

=[0.11(1-0.30)]*100/105

=0.0733 or 7.33%

Proposed WACC with changes =

=[(0.11*57000)+(0.10*6800)+(0.07*16050)+(0.07*15750)/95600

=(6270+680+1124+1103)/95600

=9177/95600

=0.966 or 9.66%

4

equities, BVd =Actual book value of debts for the organisation, Total capital =book + market

value of all the securities)

b. Recalculation of cost of capital of company

In Kadlex Plc finance director have proposed some specific changes in the capital

structure of the organisation (Brooke, 2016). Due to all these changes the computations are also

being altered. All of the could be assessed with the help of below mentioned calculations:

Formula: [(Ke*PVe)+(Kp*PVp)+(Kd*PVd)+(Kb*PVd)]/Total capital

For all the securities proposed cost's computation is as follows:

Proposed Growth(g) ( Increased by 20%)

=0.075*1.2

=0.09 or 9%

Equities(Ke)

=[{28*(1.09)}+0.09]/2.85

=0.1074 or 10.74%

Preference shares (Kp)

=[(7/68)]

=0.1029 or 10.29%

Irredeemable Bonds (Kd)

=[10(1–0.30)]*100/107

=0.0654 or 6.54%

New Bonds (Kd)

=[0.11(1-0.30)]*100/105

=0.0733 or 7.33%

Proposed WACC with changes =

=[(0.11*57000)+(0.10*6800)+(0.07*16050)+(0.07*15750)/95600

=(6270+680+1124+1103)/95600

=9177/95600

=0.966 or 9.66%

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

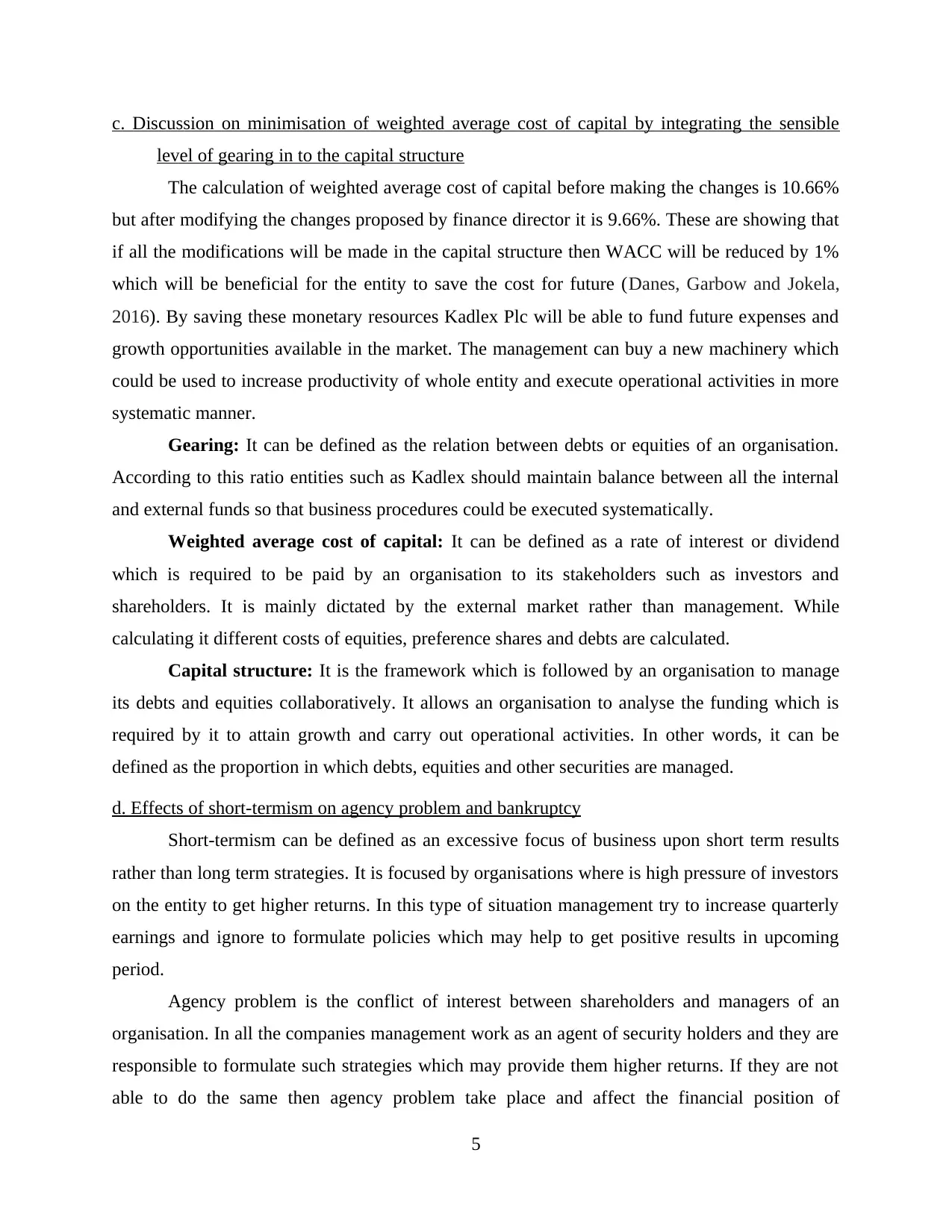

c. Discussion on minimisation of weighted average cost of capital by integrating the sensible

level of gearing in to the capital structure

The calculation of weighted average cost of capital before making the changes is 10.66%

but after modifying the changes proposed by finance director it is 9.66%. These are showing that

if all the modifications will be made in the capital structure then WACC will be reduced by 1%

which will be beneficial for the entity to save the cost for future (Danes, Garbow and Jokela,

2016). By saving these monetary resources Kadlex Plc will be able to fund future expenses and

growth opportunities available in the market. The management can buy a new machinery which

could be used to increase productivity of whole entity and execute operational activities in more

systematic manner.

Gearing: It can be defined as the relation between debts or equities of an organisation.

According to this ratio entities such as Kadlex should maintain balance between all the internal

and external funds so that business procedures could be executed systematically.

Weighted average cost of capital: It can be defined as a rate of interest or dividend

which is required to be paid by an organisation to its stakeholders such as investors and

shareholders. It is mainly dictated by the external market rather than management. While

calculating it different costs of equities, preference shares and debts are calculated.

Capital structure: It is the framework which is followed by an organisation to manage

its debts and equities collaboratively. It allows an organisation to analyse the funding which is

required by it to attain growth and carry out operational activities. In other words, it can be

defined as the proportion in which debts, equities and other securities are managed.

d. Effects of short-termism on agency problem and bankruptcy

Short-termism can be defined as an excessive focus of business upon short term results

rather than long term strategies. It is focused by organisations where is high pressure of investors

on the entity to get higher returns. In this type of situation management try to increase quarterly

earnings and ignore to formulate policies which may help to get positive results in upcoming

period.

Agency problem is the conflict of interest between shareholders and managers of an

organisation. In all the companies management work as an agent of security holders and they are

responsible to formulate such strategies which may provide them higher returns. If they are not

able to do the same then agency problem take place and affect the financial position of

5

level of gearing in to the capital structure

The calculation of weighted average cost of capital before making the changes is 10.66%

but after modifying the changes proposed by finance director it is 9.66%. These are showing that

if all the modifications will be made in the capital structure then WACC will be reduced by 1%

which will be beneficial for the entity to save the cost for future (Danes, Garbow and Jokela,

2016). By saving these monetary resources Kadlex Plc will be able to fund future expenses and

growth opportunities available in the market. The management can buy a new machinery which

could be used to increase productivity of whole entity and execute operational activities in more

systematic manner.

Gearing: It can be defined as the relation between debts or equities of an organisation.

According to this ratio entities such as Kadlex should maintain balance between all the internal

and external funds so that business procedures could be executed systematically.

Weighted average cost of capital: It can be defined as a rate of interest or dividend

which is required to be paid by an organisation to its stakeholders such as investors and

shareholders. It is mainly dictated by the external market rather than management. While

calculating it different costs of equities, preference shares and debts are calculated.

Capital structure: It is the framework which is followed by an organisation to manage

its debts and equities collaboratively. It allows an organisation to analyse the funding which is

required by it to attain growth and carry out operational activities. In other words, it can be

defined as the proportion in which debts, equities and other securities are managed.

d. Effects of short-termism on agency problem and bankruptcy

Short-termism can be defined as an excessive focus of business upon short term results

rather than long term strategies. It is focused by organisations where is high pressure of investors

on the entity to get higher returns. In this type of situation management try to increase quarterly

earnings and ignore to formulate policies which may help to get positive results in upcoming

period.

Agency problem is the conflict of interest between shareholders and managers of an

organisation. In all the companies management work as an agent of security holders and they are

responsible to formulate such strategies which may provide them higher returns. If they are not

able to do the same then agency problem take place and affect the financial position of

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

shareholders as they do not take interest in that business where they can't get higher returns

(Dwiastanti, 2017). On the other hand bankruptcy can be defined as legal process in which an

organisation became bankrupt due to lack of property and personal assets. If company is paying

attention towards short-termism then it may result in agency problem and bankruptcy because

due to this only short term benefits could be acquired. It will create the situation of lack of funds

for future which will result in no return to shareholders and no finance to carry out operations in

future. If situation of short-termism take place then it will become very difficult for the

companies to pay good returns to the security holders because long term profits cannot be

generated due to this.

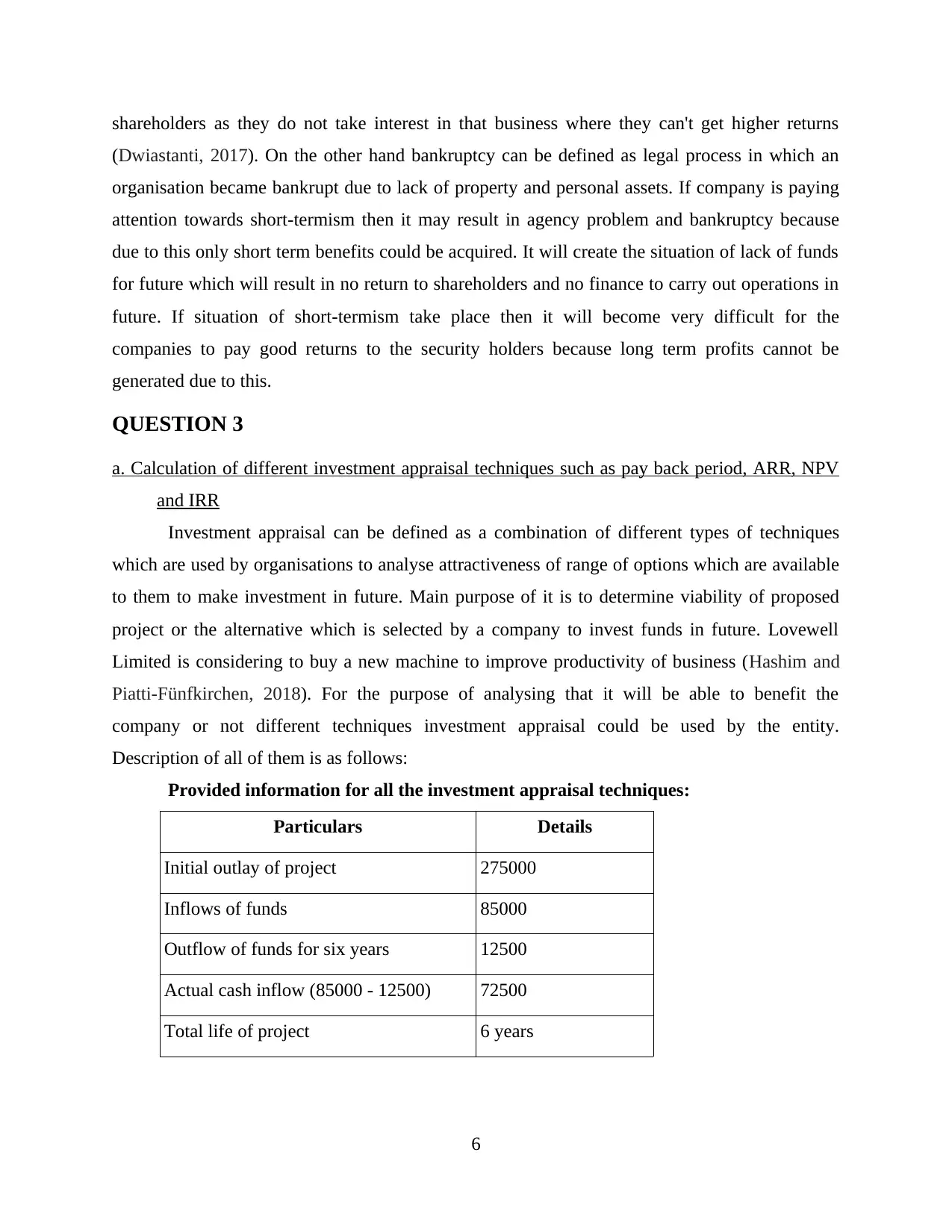

QUESTION 3

a. Calculation of different investment appraisal techniques such as pay back period, ARR, NPV

and IRR

Investment appraisal can be defined as a combination of different types of techniques

which are used by organisations to analyse attractiveness of range of options which are available

to them to make investment in future. Main purpose of it is to determine viability of proposed

project or the alternative which is selected by a company to invest funds in future. Lovewell

Limited is considering to buy a new machine to improve productivity of business (Hashim and

Piatti-Fünfkirchen, 2018). For the purpose of analysing that it will be able to benefit the

company or not different techniques investment appraisal could be used by the entity.

Description of all of them is as follows:

Provided information for all the investment appraisal techniques:

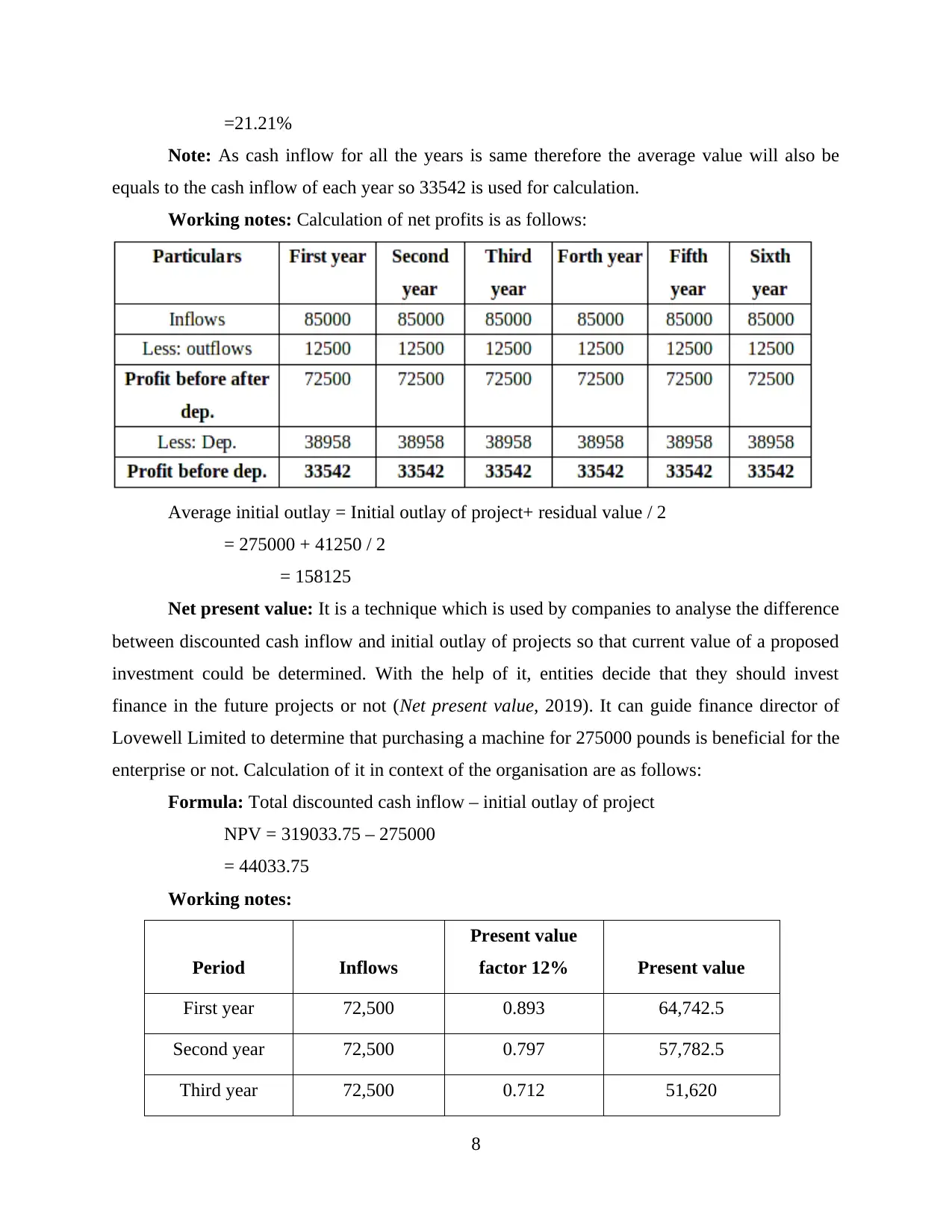

Particulars Details

Initial outlay of project 275000

Inflows of funds 85000

Outflow of funds for six years 12500

Actual cash inflow (85000 - 12500) 72500

Total life of project 6 years

6

(Dwiastanti, 2017). On the other hand bankruptcy can be defined as legal process in which an

organisation became bankrupt due to lack of property and personal assets. If company is paying

attention towards short-termism then it may result in agency problem and bankruptcy because

due to this only short term benefits could be acquired. It will create the situation of lack of funds

for future which will result in no return to shareholders and no finance to carry out operations in

future. If situation of short-termism take place then it will become very difficult for the

companies to pay good returns to the security holders because long term profits cannot be

generated due to this.

QUESTION 3

a. Calculation of different investment appraisal techniques such as pay back period, ARR, NPV

and IRR

Investment appraisal can be defined as a combination of different types of techniques

which are used by organisations to analyse attractiveness of range of options which are available

to them to make investment in future. Main purpose of it is to determine viability of proposed

project or the alternative which is selected by a company to invest funds in future. Lovewell

Limited is considering to buy a new machine to improve productivity of business (Hashim and

Piatti-Fünfkirchen, 2018). For the purpose of analysing that it will be able to benefit the

company or not different techniques investment appraisal could be used by the entity.

Description of all of them is as follows:

Provided information for all the investment appraisal techniques:

Particulars Details

Initial outlay of project 275000

Inflows of funds 85000

Outflow of funds for six years 12500

Actual cash inflow (85000 - 12500) 72500

Total life of project 6 years

6

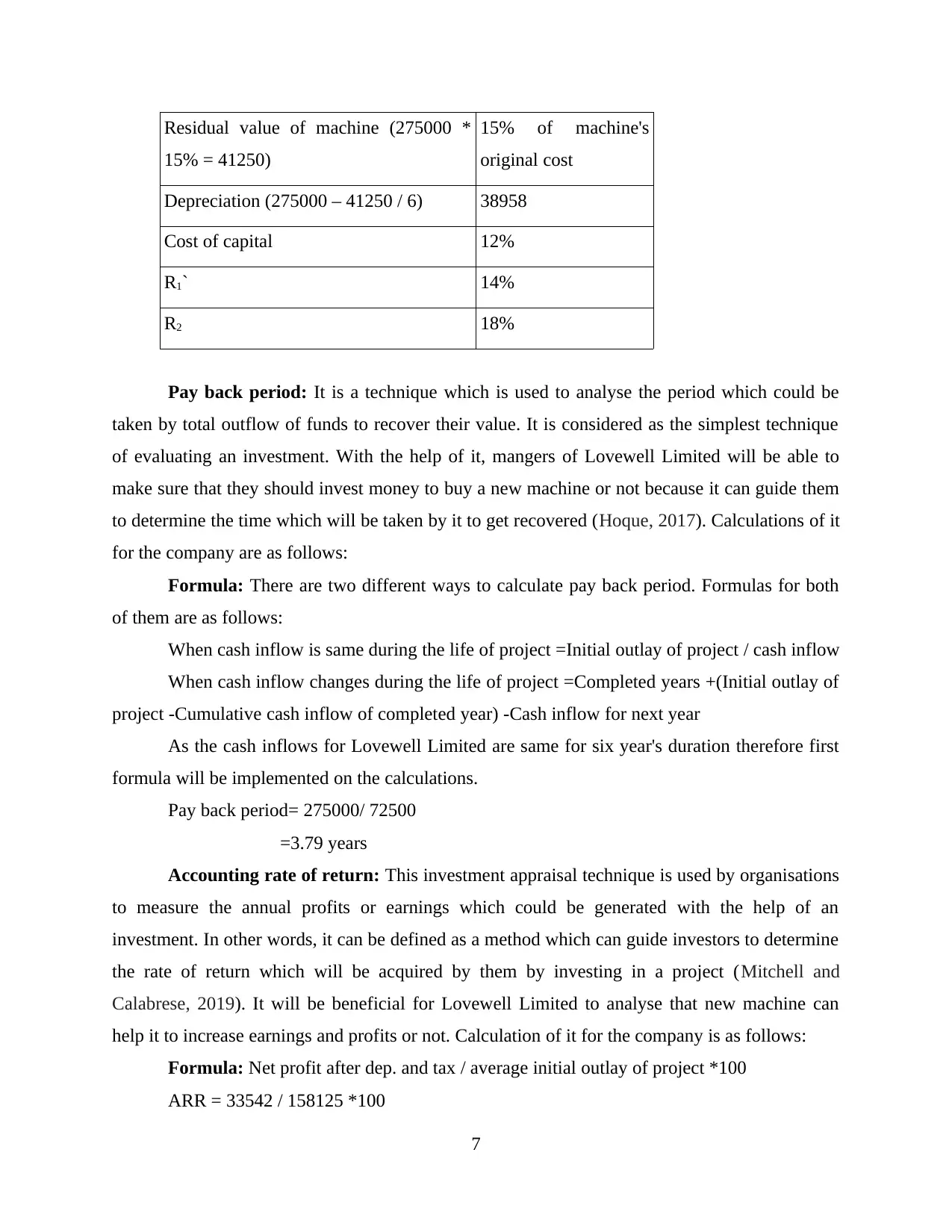

Residual value of machine (275000 *

15% = 41250)

15% of machine's

original cost

Depreciation (275000 – 41250 / 6) 38958

Cost of capital 12%

R1` 14%

R2 18%

Pay back period: It is a technique which is used to analyse the period which could be

taken by total outflow of funds to recover their value. It is considered as the simplest technique

of evaluating an investment. With the help of it, mangers of Lovewell Limited will be able to

make sure that they should invest money to buy a new machine or not because it can guide them

to determine the time which will be taken by it to get recovered (Hoque, 2017). Calculations of it

for the company are as follows:

Formula: There are two different ways to calculate pay back period. Formulas for both

of them are as follows:

When cash inflow is same during the life of project =Initial outlay of project / cash inflow

When cash inflow changes during the life of project =Completed years +(Initial outlay of

project -Cumulative cash inflow of completed year) -Cash inflow for next year

As the cash inflows for Lovewell Limited are same for six year's duration therefore first

formula will be implemented on the calculations.

Pay back period= 275000/ 72500

=3.79 years

Accounting rate of return: This investment appraisal technique is used by organisations

to measure the annual profits or earnings which could be generated with the help of an

investment. In other words, it can be defined as a method which can guide investors to determine

the rate of return which will be acquired by them by investing in a project (Mitchell and

Calabrese, 2019). It will be beneficial for Lovewell Limited to analyse that new machine can

help it to increase earnings and profits or not. Calculation of it for the company is as follows:

Formula: Net profit after dep. and tax / average initial outlay of project *100

ARR = 33542 / 158125 *100

7

15% = 41250)

15% of machine's

original cost

Depreciation (275000 – 41250 / 6) 38958

Cost of capital 12%

R1` 14%

R2 18%

Pay back period: It is a technique which is used to analyse the period which could be

taken by total outflow of funds to recover their value. It is considered as the simplest technique

of evaluating an investment. With the help of it, mangers of Lovewell Limited will be able to

make sure that they should invest money to buy a new machine or not because it can guide them

to determine the time which will be taken by it to get recovered (Hoque, 2017). Calculations of it

for the company are as follows:

Formula: There are two different ways to calculate pay back period. Formulas for both

of them are as follows:

When cash inflow is same during the life of project =Initial outlay of project / cash inflow

When cash inflow changes during the life of project =Completed years +(Initial outlay of

project -Cumulative cash inflow of completed year) -Cash inflow for next year

As the cash inflows for Lovewell Limited are same for six year's duration therefore first

formula will be implemented on the calculations.

Pay back period= 275000/ 72500

=3.79 years

Accounting rate of return: This investment appraisal technique is used by organisations

to measure the annual profits or earnings which could be generated with the help of an

investment. In other words, it can be defined as a method which can guide investors to determine

the rate of return which will be acquired by them by investing in a project (Mitchell and

Calabrese, 2019). It will be beneficial for Lovewell Limited to analyse that new machine can

help it to increase earnings and profits or not. Calculation of it for the company is as follows:

Formula: Net profit after dep. and tax / average initial outlay of project *100

ARR = 33542 / 158125 *100

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

=21.21%

Note: As cash inflow for all the years is same therefore the average value will also be

equals to the cash inflow of each year so 33542 is used for calculation.

Working notes: Calculation of net profits is as follows:

Average initial outlay = Initial outlay of project+ residual value / 2

= 275000 + 41250 / 2

= 158125

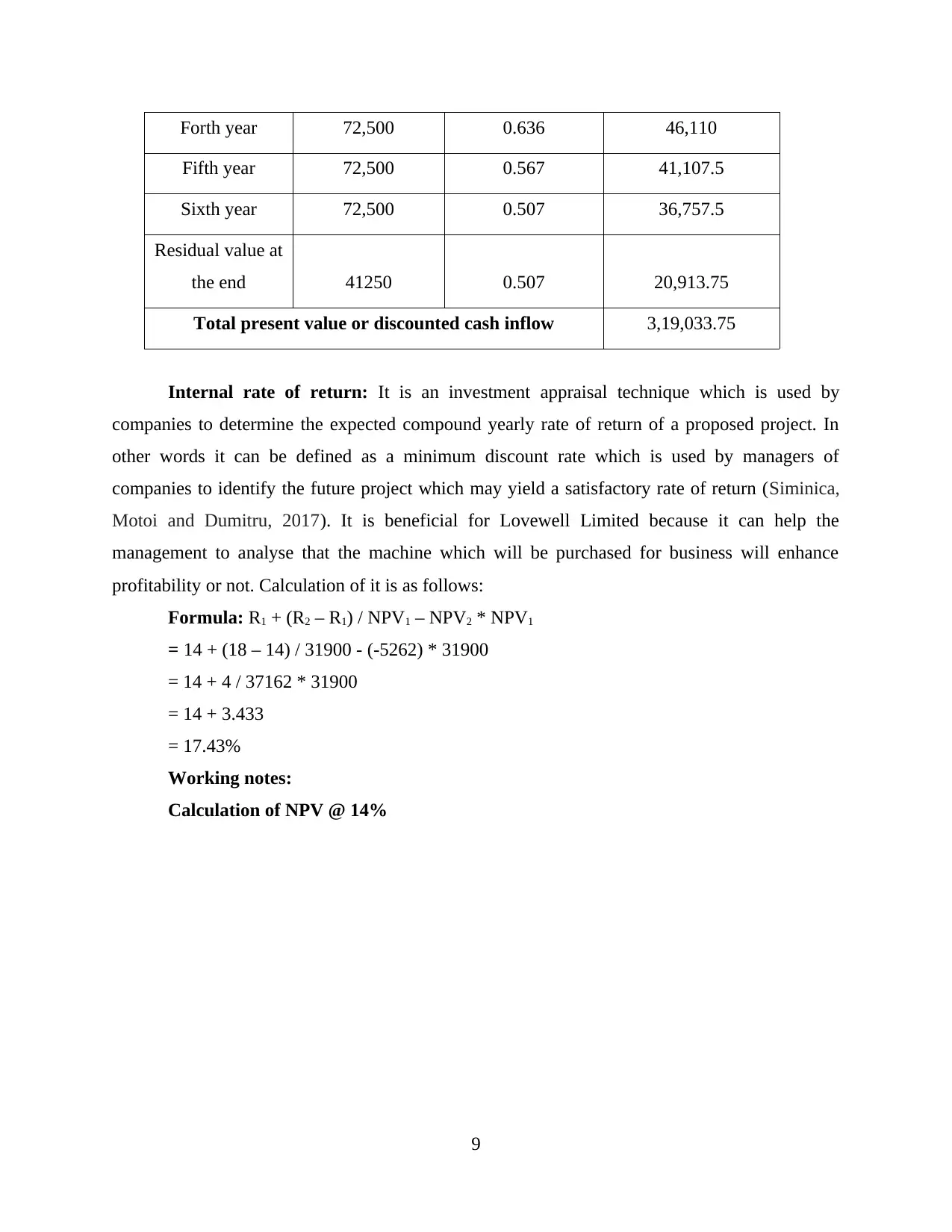

Net present value: It is a technique which is used by companies to analyse the difference

between discounted cash inflow and initial outlay of projects so that current value of a proposed

investment could be determined. With the help of it, entities decide that they should invest

finance in the future projects or not (Net present value, 2019). It can guide finance director of

Lovewell Limited to determine that purchasing a machine for 275000 pounds is beneficial for the

enterprise or not. Calculation of it in context of the organisation are as follows:

Formula: Total discounted cash inflow – initial outlay of project

NPV = 319033.75 – 275000

= 44033.75

Working notes:

Period Inflows

Present value

factor 12% Present value

First year 72,500 0.893 64,742.5

Second year 72,500 0.797 57,782.5

Third year 72,500 0.712 51,620

8

Note: As cash inflow for all the years is same therefore the average value will also be

equals to the cash inflow of each year so 33542 is used for calculation.

Working notes: Calculation of net profits is as follows:

Average initial outlay = Initial outlay of project+ residual value / 2

= 275000 + 41250 / 2

= 158125

Net present value: It is a technique which is used by companies to analyse the difference

between discounted cash inflow and initial outlay of projects so that current value of a proposed

investment could be determined. With the help of it, entities decide that they should invest

finance in the future projects or not (Net present value, 2019). It can guide finance director of

Lovewell Limited to determine that purchasing a machine for 275000 pounds is beneficial for the

enterprise or not. Calculation of it in context of the organisation are as follows:

Formula: Total discounted cash inflow – initial outlay of project

NPV = 319033.75 – 275000

= 44033.75

Working notes:

Period Inflows

Present value

factor 12% Present value

First year 72,500 0.893 64,742.5

Second year 72,500 0.797 57,782.5

Third year 72,500 0.712 51,620

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Forth year 72,500 0.636 46,110

Fifth year 72,500 0.567 41,107.5

Sixth year 72,500 0.507 36,757.5

Residual value at

the end 41250 0.507 20,913.75

Total present value or discounted cash inflow 3,19,033.75

Internal rate of return: It is an investment appraisal technique which is used by

companies to determine the expected compound yearly rate of return of a proposed project. In

other words it can be defined as a minimum discount rate which is used by managers of

companies to identify the future project which may yield a satisfactory rate of return (Siminica,

Motoi and Dumitru, 2017). It is beneficial for Lovewell Limited because it can help the

management to analyse that the machine which will be purchased for business will enhance

profitability or not. Calculation of it is as follows:

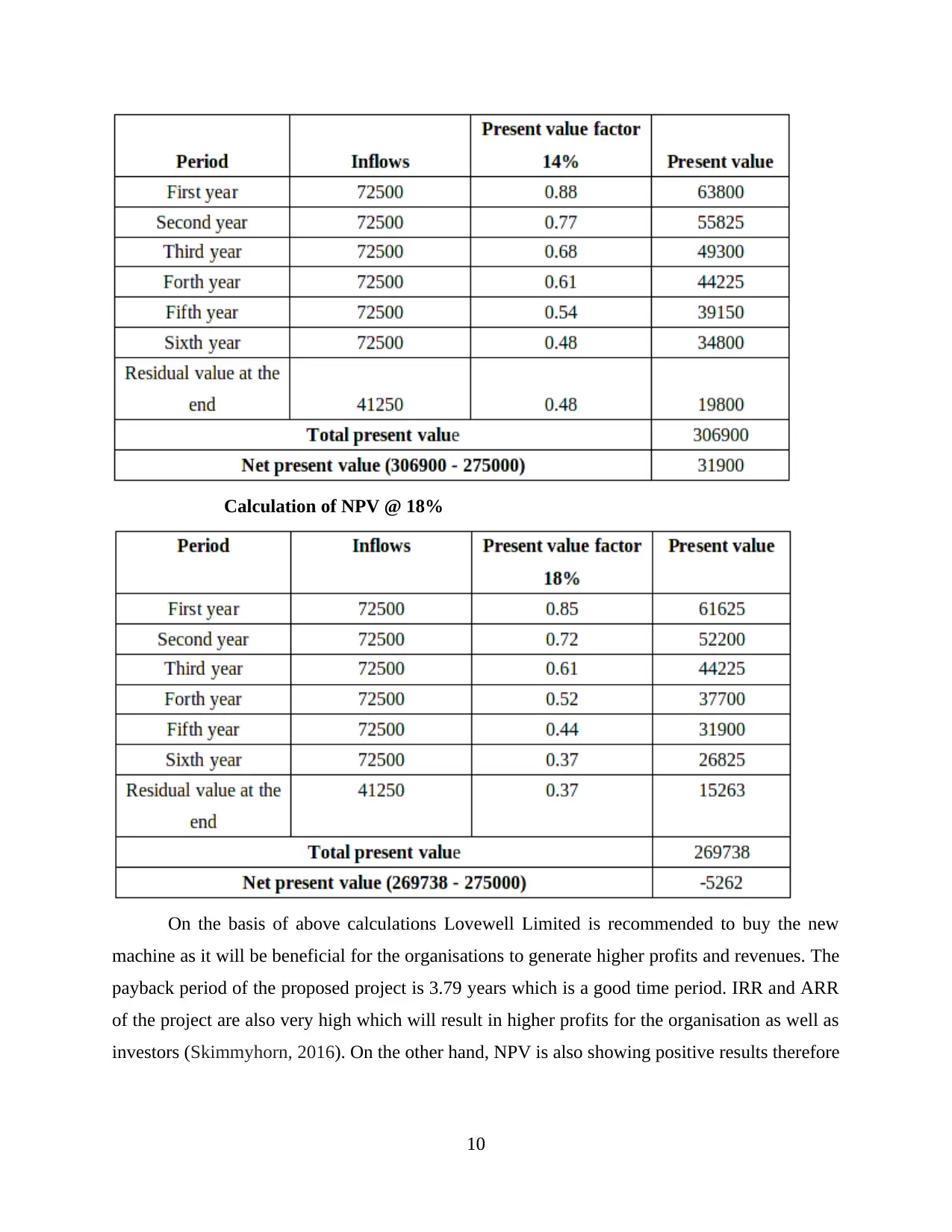

Formula: R1 + (R2 – R1) / NPV1 – NPV2 * NPV1

= 14 + (18 – 14) / 31900 - (-5262) * 31900

= 14 + 4 / 37162 * 31900

= 14 + 3.433

= 17.43%

Working notes:

Calculation of NPV @ 14%

9

Fifth year 72,500 0.567 41,107.5

Sixth year 72,500 0.507 36,757.5

Residual value at

the end 41250 0.507 20,913.75

Total present value or discounted cash inflow 3,19,033.75

Internal rate of return: It is an investment appraisal technique which is used by

companies to determine the expected compound yearly rate of return of a proposed project. In

other words it can be defined as a minimum discount rate which is used by managers of

companies to identify the future project which may yield a satisfactory rate of return (Siminica,

Motoi and Dumitru, 2017). It is beneficial for Lovewell Limited because it can help the

management to analyse that the machine which will be purchased for business will enhance

profitability or not. Calculation of it is as follows:

Formula: R1 + (R2 – R1) / NPV1 – NPV2 * NPV1

= 14 + (18 – 14) / 31900 - (-5262) * 31900

= 14 + 4 / 37162 * 31900

= 14 + 3.433

= 17.43%

Working notes:

Calculation of NPV @ 14%

9

Calculation of NPV @ 18%

On the basis of above calculations Lovewell Limited is recommended to buy the new

machine as it will be beneficial for the organisations to generate higher profits and revenues. The

payback period of the proposed project is 3.79 years which is a good time period. IRR and ARR

of the project are also very high which will result in higher profits for the organisation as well as

investors (Skimmyhorn, 2016). On the other hand, NPV is also showing positive results therefore

10

On the basis of above calculations Lovewell Limited is recommended to buy the new

machine as it will be beneficial for the organisations to generate higher profits and revenues. The

payback period of the proposed project is 3.79 years which is a good time period. IRR and ARR

of the project are also very high which will result in higher profits for the organisation as well as

investors (Skimmyhorn, 2016). On the other hand, NPV is also showing positive results therefore

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.