Financial Management Report: Right Shares and Appraisal Techniques

VerifiedAdded on 2023/01/16

|15

|3725

|83

Report

AI Summary

This financial management report addresses key concepts through a detailed analysis of right shares, investment appraisal techniques, and scrip dividends. The report begins with an introduction to financial management, followed by calculations and analysis related to issuing right shares, including determination of theoretical ex-rights price, value of each right share, and fair value per right share under different scenarios. The report then provides a critical discussion of the advantages of scrip dividends for both the enterprise and shareholders. Furthermore, the report applies various investment appraisal techniques, such as payback period, NPV, ARR, and IRR, to evaluate a potential investment. It includes detailed calculations and a critical evaluation of the benefits and limitations of each technique. The analysis is supported by examples from Lexbel Plc and Lovewell Limited, providing practical insights into financial decision-making. The report concludes with a summary of the key findings and a list of references.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

OUESTION 2...................................................................................................................................1

a. & b. Issuing right share and Determination of different values...............................................1

c. Critical discussion of advantages of scrip dividend from the point of view of the enterprise

and shareholders...........................................................................................................................5

QUESTION 3...................................................................................................................................6

a. Use of different investment appraisal techniques for calculations...........................................6

b. Critical evaluation of all the investment appraisal techniques by discussing all their benefits

and limitations............................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

OUESTION 2...................................................................................................................................1

a. & b. Issuing right share and Determination of different values...............................................1

c. Critical discussion of advantages of scrip dividend from the point of view of the enterprise

and shareholders...........................................................................................................................5

QUESTION 3...................................................................................................................................6

a. Use of different investment appraisal techniques for calculations...........................................6

b. Critical evaluation of all the investment appraisal techniques by discussing all their benefits

and limitations............................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Financial management can be defined as the process of planning and controlling the

finance related operations so that performance of whole organisation could be improved. Main

purpose of it is to apply management principles on funds of the enterprise for proper execution of

operations (Antonopoulos and Hall, 2015). This report is based upon usage of different

investment appraisal techniques and issuance of right shares within the organisation. For the

completion of this project question 2 and 3 are selected. This assignment covers various topics

such as scrip dividend, right shares etc. Additionally, NPV, ARR, IRR and pay back period are

also covered in this report.

OUESTION 2

a. & b. Issuing right share and Determination of different values

Most of the business entities may have to face the problem of lack of capital for the

purpose of performing operational activities. Additionally, some times insufficient working

capital related challenges may also dealt by business enterprises. For the purpose of dealing with

all of them in systematic manner it is very important for top level executives of organisations to

arrange funding to carry out operations. They can introduce fresh capital for business and launch

new shares in the market. One of the technique which is used by most of the companies to

improve cash position and enhance shareholder's equity is allowing scrip dividend to the

shareholders (Banerjee, 2015). By selecting this option a company and the individuals having

share in it get benefited because the business can enhance retained earning and the external

parties can increase their ownership in the entity. The shares which are issued against dividend to

the existing shareholders are known as right shares.

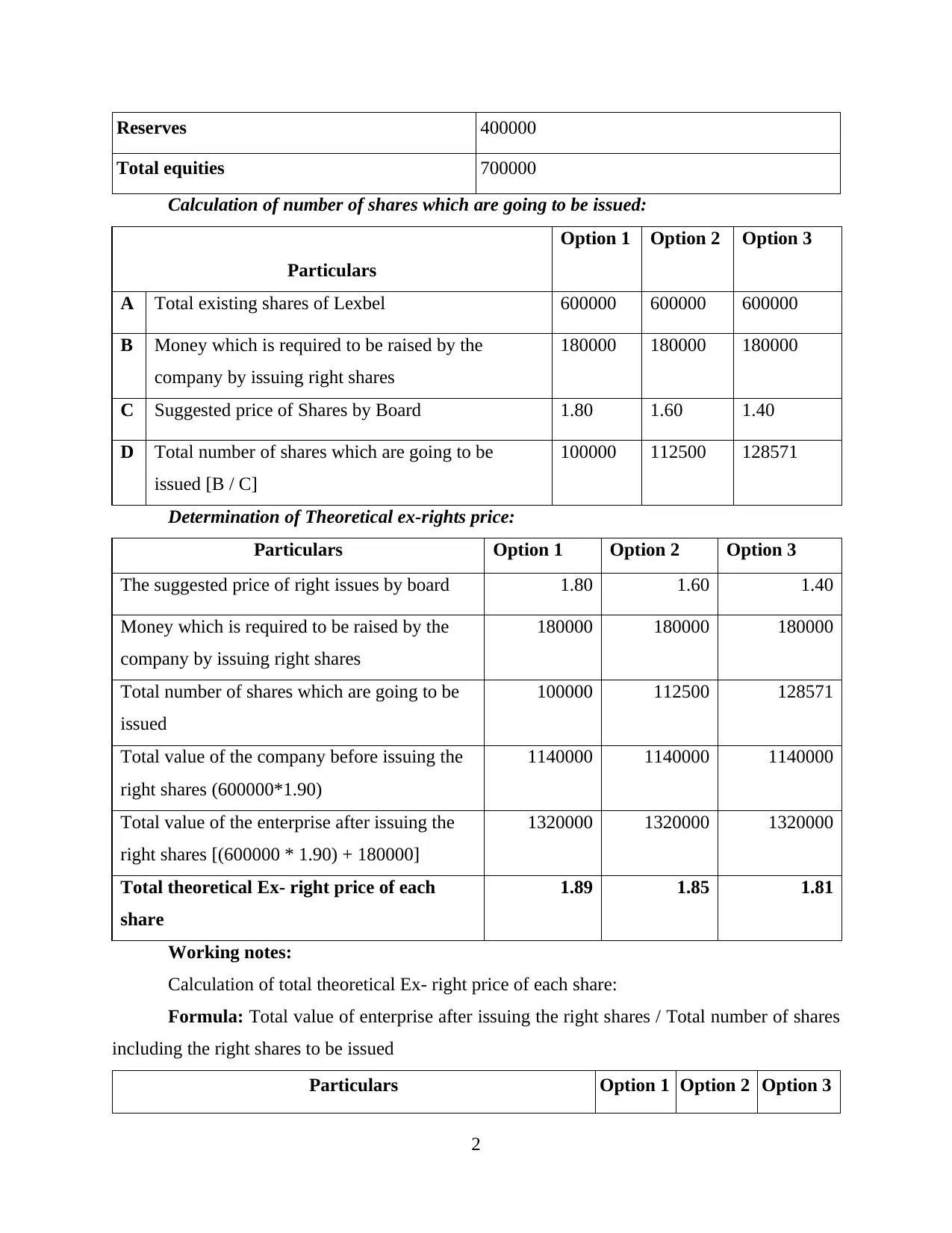

The Board members of Lexbel Plc have decided to raise 180000 pounds by issuing right

shares so that its operations could be expanded. The suggested price for them by the board are

1.80, 1.60 and 1.40. The market price for the existing shares is 1.90. Calculations for

identification of best options are as follows:

Provided information:

Particulars Details

Ordinary shares @ 50 300000

1

Financial management can be defined as the process of planning and controlling the

finance related operations so that performance of whole organisation could be improved. Main

purpose of it is to apply management principles on funds of the enterprise for proper execution of

operations (Antonopoulos and Hall, 2015). This report is based upon usage of different

investment appraisal techniques and issuance of right shares within the organisation. For the

completion of this project question 2 and 3 are selected. This assignment covers various topics

such as scrip dividend, right shares etc. Additionally, NPV, ARR, IRR and pay back period are

also covered in this report.

OUESTION 2

a. & b. Issuing right share and Determination of different values

Most of the business entities may have to face the problem of lack of capital for the

purpose of performing operational activities. Additionally, some times insufficient working

capital related challenges may also dealt by business enterprises. For the purpose of dealing with

all of them in systematic manner it is very important for top level executives of organisations to

arrange funding to carry out operations. They can introduce fresh capital for business and launch

new shares in the market. One of the technique which is used by most of the companies to

improve cash position and enhance shareholder's equity is allowing scrip dividend to the

shareholders (Banerjee, 2015). By selecting this option a company and the individuals having

share in it get benefited because the business can enhance retained earning and the external

parties can increase their ownership in the entity. The shares which are issued against dividend to

the existing shareholders are known as right shares.

The Board members of Lexbel Plc have decided to raise 180000 pounds by issuing right

shares so that its operations could be expanded. The suggested price for them by the board are

1.80, 1.60 and 1.40. The market price for the existing shares is 1.90. Calculations for

identification of best options are as follows:

Provided information:

Particulars Details

Ordinary shares @ 50 300000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reserves 400000

Total equities 700000

Calculation of number of shares which are going to be issued:

Particulars

Option 1 Option 2 Option 3

A Total existing shares of Lexbel 600000 600000 600000

B Money which is required to be raised by the

company by issuing right shares

180000 180000 180000

C Suggested price of Shares by Board 1.80 1.60 1.40

D Total number of shares which are going to be

issued [B / C]

100000 112500 128571

Determination of Theoretical ex-rights price:

Particulars Option 1 Option 2 Option 3

The suggested price of right issues by board 1.80 1.60 1.40

Money which is required to be raised by the

company by issuing right shares

180000 180000 180000

Total number of shares which are going to be

issued

100000 112500 128571

Total value of the company before issuing the

right shares (600000*1.90)

1140000 1140000 1140000

Total value of the enterprise after issuing the

right shares [(600000 * 1.90) + 180000]

1320000 1320000 1320000

Total theoretical Ex- right price of each

share

1.89 1.85 1.81

Working notes:

Calculation of total theoretical Ex- right price of each share:

Formula: Total value of enterprise after issuing the right shares / Total number of shares

including the right shares to be issued

Particulars Option 1 Option 2 Option 3

2

Total equities 700000

Calculation of number of shares which are going to be issued:

Particulars

Option 1 Option 2 Option 3

A Total existing shares of Lexbel 600000 600000 600000

B Money which is required to be raised by the

company by issuing right shares

180000 180000 180000

C Suggested price of Shares by Board 1.80 1.60 1.40

D Total number of shares which are going to be

issued [B / C]

100000 112500 128571

Determination of Theoretical ex-rights price:

Particulars Option 1 Option 2 Option 3

The suggested price of right issues by board 1.80 1.60 1.40

Money which is required to be raised by the

company by issuing right shares

180000 180000 180000

Total number of shares which are going to be

issued

100000 112500 128571

Total value of the company before issuing the

right shares (600000*1.90)

1140000 1140000 1140000

Total value of the enterprise after issuing the

right shares [(600000 * 1.90) + 180000]

1320000 1320000 1320000

Total theoretical Ex- right price of each

share

1.89 1.85 1.81

Working notes:

Calculation of total theoretical Ex- right price of each share:

Formula: Total value of enterprise after issuing the right shares / Total number of shares

including the right shares to be issued

Particulars Option 1 Option 2 Option 3

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

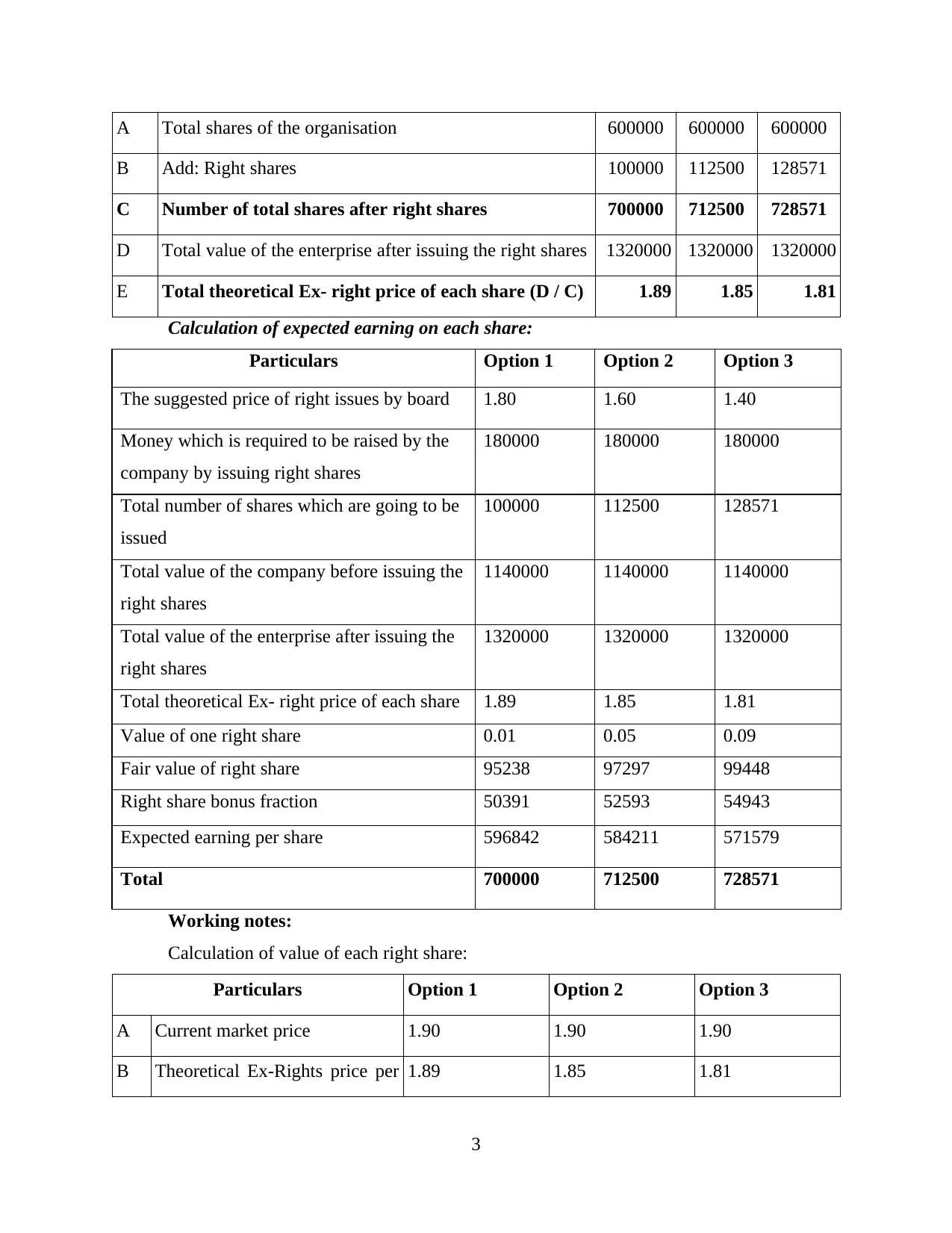

A Total shares of the organisation 600000 600000 600000

B Add: Right shares 100000 112500 128571

C Number of total shares after right shares 700000 712500 728571

D Total value of the enterprise after issuing the right shares 1320000 1320000 1320000

E Total theoretical Ex- right price of each share (D / C) 1.89 1.85 1.81

Calculation of expected earning on each share:

Particulars Option 1 Option 2 Option 3

The suggested price of right issues by board 1.80 1.60 1.40

Money which is required to be raised by the

company by issuing right shares

180000 180000 180000

Total number of shares which are going to be

issued

100000 112500 128571

Total value of the company before issuing the

right shares

1140000 1140000 1140000

Total value of the enterprise after issuing the

right shares

1320000 1320000 1320000

Total theoretical Ex- right price of each share 1.89 1.85 1.81

Value of one right share 0.01 0.05 0.09

Fair value of right share 95238 97297 99448

Right share bonus fraction 50391 52593 54943

Expected earning per share 596842 584211 571579

Total 700000 712500 728571

Working notes:

Calculation of value of each right share:

Particulars Option 1 Option 2 Option 3

A Current market price 1.90 1.90 1.90

B Theoretical Ex-Rights price per 1.89 1.85 1.81

3

B Add: Right shares 100000 112500 128571

C Number of total shares after right shares 700000 712500 728571

D Total value of the enterprise after issuing the right shares 1320000 1320000 1320000

E Total theoretical Ex- right price of each share (D / C) 1.89 1.85 1.81

Calculation of expected earning on each share:

Particulars Option 1 Option 2 Option 3

The suggested price of right issues by board 1.80 1.60 1.40

Money which is required to be raised by the

company by issuing right shares

180000 180000 180000

Total number of shares which are going to be

issued

100000 112500 128571

Total value of the company before issuing the

right shares

1140000 1140000 1140000

Total value of the enterprise after issuing the

right shares

1320000 1320000 1320000

Total theoretical Ex- right price of each share 1.89 1.85 1.81

Value of one right share 0.01 0.05 0.09

Fair value of right share 95238 97297 99448

Right share bonus fraction 50391 52593 54943

Expected earning per share 596842 584211 571579

Total 700000 712500 728571

Working notes:

Calculation of value of each right share:

Particulars Option 1 Option 2 Option 3

A Current market price 1.90 1.90 1.90

B Theoretical Ex-Rights price per 1.89 1.85 1.81

3

share

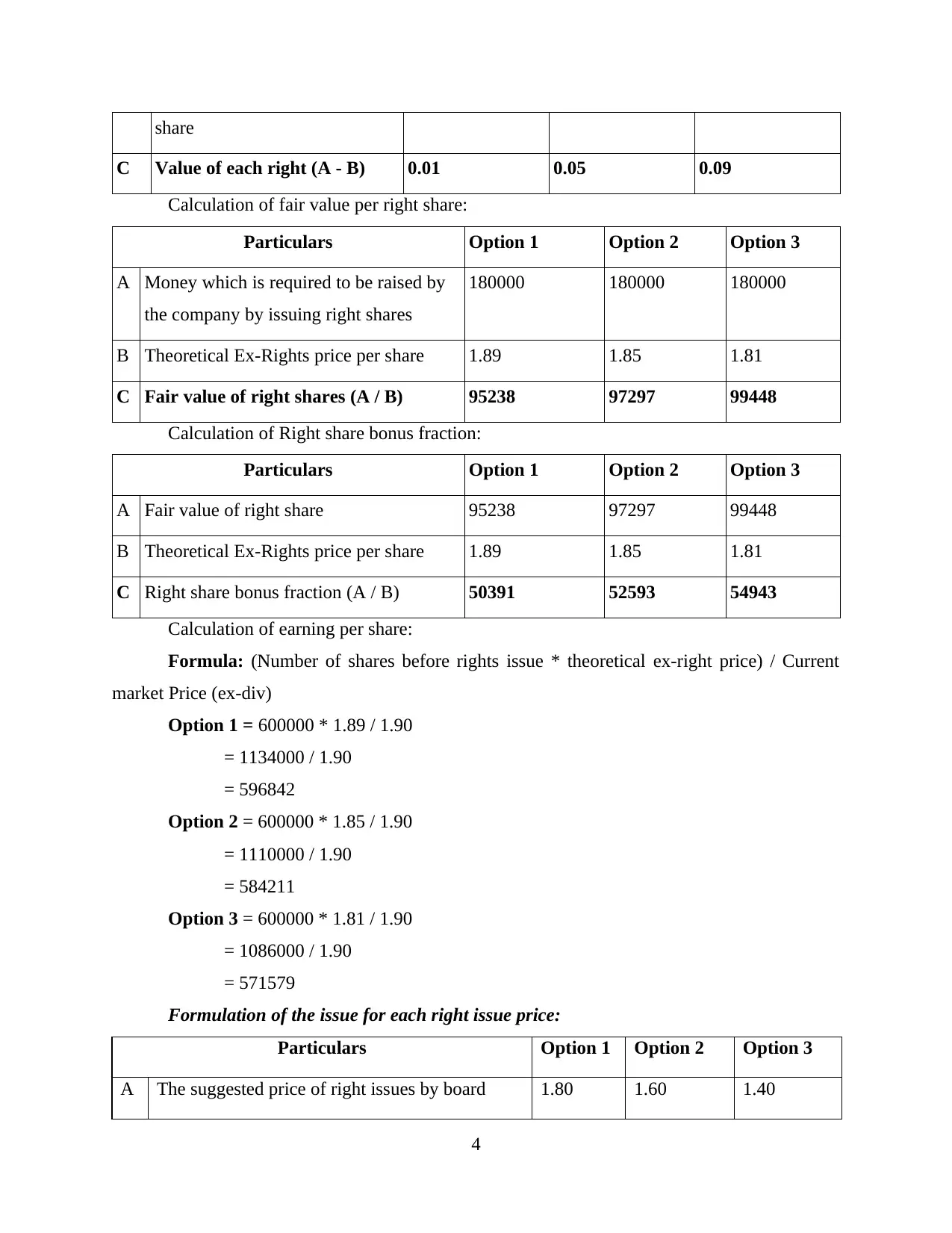

C Value of each right (A - B) 0.01 0.05 0.09

Calculation of fair value per right share:

Particulars Option 1 Option 2 Option 3

A Money which is required to be raised by

the company by issuing right shares

180000 180000 180000

B Theoretical Ex-Rights price per share 1.89 1.85 1.81

C Fair value of right shares (A / B) 95238 97297 99448

Calculation of Right share bonus fraction:

Particulars Option 1 Option 2 Option 3

A Fair value of right share 95238 97297 99448

B Theoretical Ex-Rights price per share 1.89 1.85 1.81

C Right share bonus fraction (A / B) 50391 52593 54943

Calculation of earning per share:

Formula: (Number of shares before rights issue * theoretical ex-right price) / Current

market Price (ex-div)

Option 1 = 600000 * 1.89 / 1.90

= 1134000 / 1.90

= 596842

Option 2 = 600000 * 1.85 / 1.90

= 1110000 / 1.90

= 584211

Option 3 = 600000 * 1.81 / 1.90

= 1086000 / 1.90

= 571579

Formulation of the issue for each right issue price:

Particulars Option 1 Option 2 Option 3

A The suggested price of right issues by board 1.80 1.60 1.40

4

C Value of each right (A - B) 0.01 0.05 0.09

Calculation of fair value per right share:

Particulars Option 1 Option 2 Option 3

A Money which is required to be raised by

the company by issuing right shares

180000 180000 180000

B Theoretical Ex-Rights price per share 1.89 1.85 1.81

C Fair value of right shares (A / B) 95238 97297 99448

Calculation of Right share bonus fraction:

Particulars Option 1 Option 2 Option 3

A Fair value of right share 95238 97297 99448

B Theoretical Ex-Rights price per share 1.89 1.85 1.81

C Right share bonus fraction (A / B) 50391 52593 54943

Calculation of earning per share:

Formula: (Number of shares before rights issue * theoretical ex-right price) / Current

market Price (ex-div)

Option 1 = 600000 * 1.89 / 1.90

= 1134000 / 1.90

= 596842

Option 2 = 600000 * 1.85 / 1.90

= 1110000 / 1.90

= 584211

Option 3 = 600000 * 1.81 / 1.90

= 1086000 / 1.90

= 571579

Formulation of the issue for each right issue price:

Particulars Option 1 Option 2 Option 3

A The suggested price of right issues by board 1.80 1.60 1.40

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

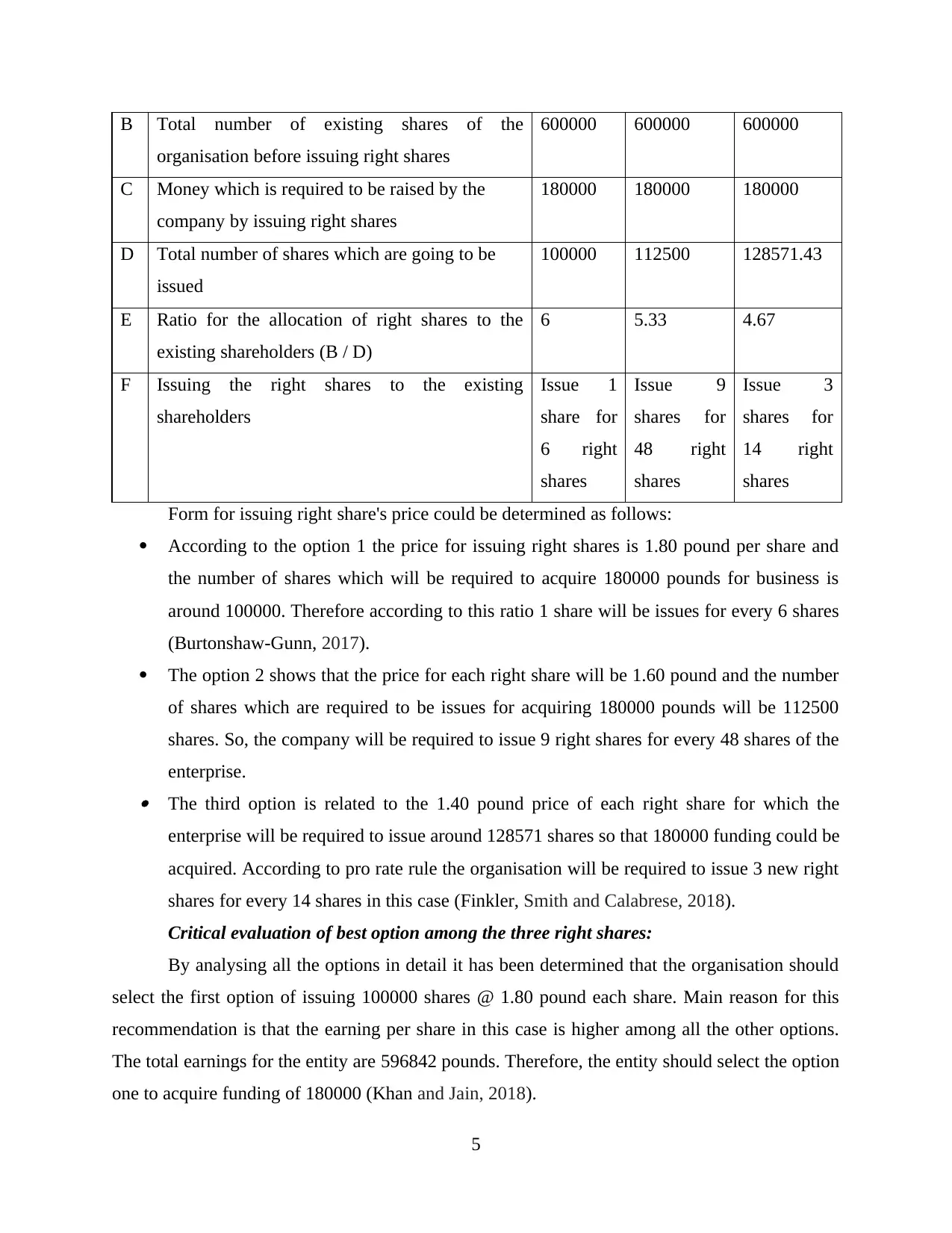

B Total number of existing shares of the

organisation before issuing right shares

600000 600000 600000

C Money which is required to be raised by the

company by issuing right shares

180000 180000 180000

D Total number of shares which are going to be

issued

100000 112500 128571.43

E Ratio for the allocation of right shares to the

existing shareholders (B / D)

6 5.33 4.67

F Issuing the right shares to the existing

shareholders

Issue 1

share for

6 right

shares

Issue 9

shares for

48 right

shares

Issue 3

shares for

14 right

shares

Form for issuing right share's price could be determined as follows:

According to the option 1 the price for issuing right shares is 1.80 pound per share and

the number of shares which will be required to acquire 180000 pounds for business is

around 100000. Therefore according to this ratio 1 share will be issues for every 6 shares

(Burtonshaw-Gunn, 2017).

The option 2 shows that the price for each right share will be 1.60 pound and the number

of shares which are required to be issues for acquiring 180000 pounds will be 112500

shares. So, the company will be required to issue 9 right shares for every 48 shares of the

enterprise. The third option is related to the 1.40 pound price of each right share for which the

enterprise will be required to issue around 128571 shares so that 180000 funding could be

acquired. According to pro rate rule the organisation will be required to issue 3 new right

shares for every 14 shares in this case (Finkler, Smith and Calabrese, 2018).

Critical evaluation of best option among the three right shares:

By analysing all the options in detail it has been determined that the organisation should

select the first option of issuing 100000 shares @ 1.80 pound each share. Main reason for this

recommendation is that the earning per share in this case is higher among all the other options.

The total earnings for the entity are 596842 pounds. Therefore, the entity should select the option

one to acquire funding of 180000 (Khan and Jain, 2018).

5

organisation before issuing right shares

600000 600000 600000

C Money which is required to be raised by the

company by issuing right shares

180000 180000 180000

D Total number of shares which are going to be

issued

100000 112500 128571.43

E Ratio for the allocation of right shares to the

existing shareholders (B / D)

6 5.33 4.67

F Issuing the right shares to the existing

shareholders

Issue 1

share for

6 right

shares

Issue 9

shares for

48 right

shares

Issue 3

shares for

14 right

shares

Form for issuing right share's price could be determined as follows:

According to the option 1 the price for issuing right shares is 1.80 pound per share and

the number of shares which will be required to acquire 180000 pounds for business is

around 100000. Therefore according to this ratio 1 share will be issues for every 6 shares

(Burtonshaw-Gunn, 2017).

The option 2 shows that the price for each right share will be 1.60 pound and the number

of shares which are required to be issues for acquiring 180000 pounds will be 112500

shares. So, the company will be required to issue 9 right shares for every 48 shares of the

enterprise. The third option is related to the 1.40 pound price of each right share for which the

enterprise will be required to issue around 128571 shares so that 180000 funding could be

acquired. According to pro rate rule the organisation will be required to issue 3 new right

shares for every 14 shares in this case (Finkler, Smith and Calabrese, 2018).

Critical evaluation of best option among the three right shares:

By analysing all the options in detail it has been determined that the organisation should

select the first option of issuing 100000 shares @ 1.80 pound each share. Main reason for this

recommendation is that the earning per share in this case is higher among all the other options.

The total earnings for the entity are 596842 pounds. Therefore, the entity should select the option

one to acquire funding of 180000 (Khan and Jain, 2018).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

c. Critical discussion of advantages of scrip dividend from the point of view of the enterprise and

shareholders

For all the organisations it is very important to maintain interest of shareholders in the

company as it is required for proper execution of all the operational activities. On the other hand,

one more thing which is also needed to be focused by top level executives of business entities

which is providing option to the shareholders to take a cash or scrip dividend. It can be defined

as a bonus or capitalisation issue in which the amount which is paid to the shareholders in cash is

converted in to securities and issued to them (Karadag, 2015). These are mainly provided to the

existing individuals who are holding shares within the company. By using it companies can save

money for future and also allow dividend to the shareholders so that their interest could be

maintain. The board of Lexbel Plc have also decided to issue right shares against the existing

stocks of the company so that monetary resources of 180000 pounds could be saved as retained

earnings. Scrip dividend is very beneficial for the business entities and some of the main

advantages of it are discussed below:

For company:

Scrip dividend is a way of saving monetary resources and paying dividend to the existing

shareholders. With the help of it business entities can enhance their retained earning as

well as number of shares. It also results in increased equities of the enterprise because by

using pro rata concept right shares are allocated to the shareholders (Mien and Thao,

2015).

It is a type of option which is provided to the shareholders to maintain their interest and

retain their ownership within the company. By giving choice to them the enterprise will

be able to fulfil their needs according to their requirements. By offering scrip dividend

the enterprise can enhance the gearing and improve the cash position in the market if

higher number of shareholders select the scrip option.

For shareholders:

If an organisation is allowing the shareholders to select from the options of scrip or cash

dividend then it can help them to find the best suitable alternative which will be

beneficial for them. One of the major benefit of for the shareholder is that it can facilitate

them to increase their ownership within the organisation.

6

shareholders

For all the organisations it is very important to maintain interest of shareholders in the

company as it is required for proper execution of all the operational activities. On the other hand,

one more thing which is also needed to be focused by top level executives of business entities

which is providing option to the shareholders to take a cash or scrip dividend. It can be defined

as a bonus or capitalisation issue in which the amount which is paid to the shareholders in cash is

converted in to securities and issued to them (Karadag, 2015). These are mainly provided to the

existing individuals who are holding shares within the company. By using it companies can save

money for future and also allow dividend to the shareholders so that their interest could be

maintain. The board of Lexbel Plc have also decided to issue right shares against the existing

stocks of the company so that monetary resources of 180000 pounds could be saved as retained

earnings. Scrip dividend is very beneficial for the business entities and some of the main

advantages of it are discussed below:

For company:

Scrip dividend is a way of saving monetary resources and paying dividend to the existing

shareholders. With the help of it business entities can enhance their retained earning as

well as number of shares. It also results in increased equities of the enterprise because by

using pro rata concept right shares are allocated to the shareholders (Mien and Thao,

2015).

It is a type of option which is provided to the shareholders to maintain their interest and

retain their ownership within the company. By giving choice to them the enterprise will

be able to fulfil their needs according to their requirements. By offering scrip dividend

the enterprise can enhance the gearing and improve the cash position in the market if

higher number of shareholders select the scrip option.

For shareholders:

If an organisation is allowing the shareholders to select from the options of scrip or cash

dividend then it can help them to find the best suitable alternative which will be

beneficial for them. One of the major benefit of for the shareholder is that it can facilitate

them to increase their ownership within the organisation.

6

If the shareholders get scrip dividend then it will be beneficial for them to attain a tax

advantage because they will get profits in the form of shares (Renz and Herman, 2016).

QUESTION 3

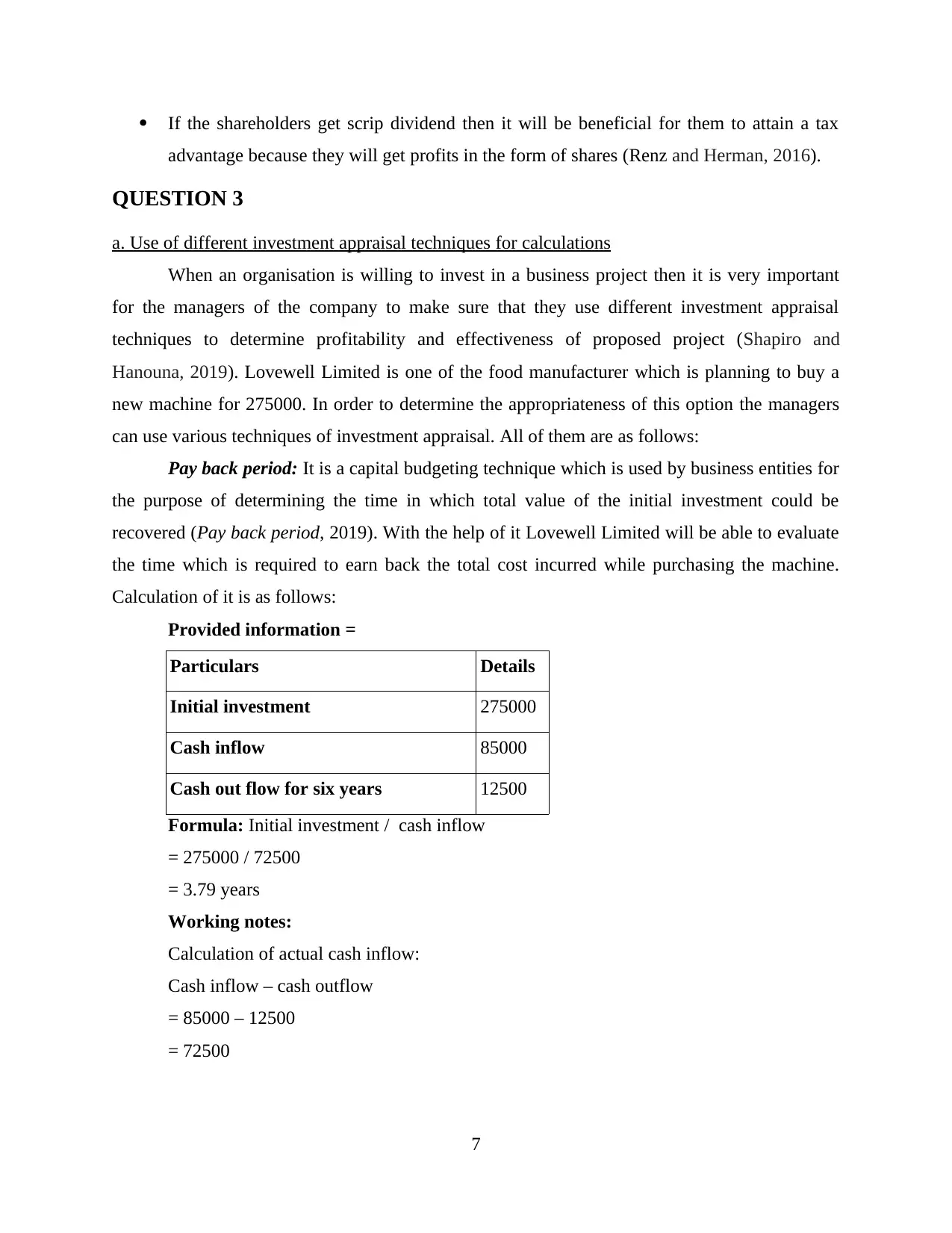

a. Use of different investment appraisal techniques for calculations

When an organisation is willing to invest in a business project then it is very important

for the managers of the company to make sure that they use different investment appraisal

techniques to determine profitability and effectiveness of proposed project (Shapiro and

Hanouna, 2019). Lovewell Limited is one of the food manufacturer which is planning to buy a

new machine for 275000. In order to determine the appropriateness of this option the managers

can use various techniques of investment appraisal. All of them are as follows:

Pay back period: It is a capital budgeting technique which is used by business entities for

the purpose of determining the time in which total value of the initial investment could be

recovered (Pay back period, 2019). With the help of it Lovewell Limited will be able to evaluate

the time which is required to earn back the total cost incurred while purchasing the machine.

Calculation of it is as follows:

Provided information =

Particulars Details

Initial investment 275000

Cash inflow 85000

Cash out flow for six years 12500

Formula: Initial investment / cash inflow

= 275000 / 72500

= 3.79 years

Working notes:

Calculation of actual cash inflow:

Cash inflow – cash outflow

= 85000 – 12500

= 72500

7

advantage because they will get profits in the form of shares (Renz and Herman, 2016).

QUESTION 3

a. Use of different investment appraisal techniques for calculations

When an organisation is willing to invest in a business project then it is very important

for the managers of the company to make sure that they use different investment appraisal

techniques to determine profitability and effectiveness of proposed project (Shapiro and

Hanouna, 2019). Lovewell Limited is one of the food manufacturer which is planning to buy a

new machine for 275000. In order to determine the appropriateness of this option the managers

can use various techniques of investment appraisal. All of them are as follows:

Pay back period: It is a capital budgeting technique which is used by business entities for

the purpose of determining the time in which total value of the initial investment could be

recovered (Pay back period, 2019). With the help of it Lovewell Limited will be able to evaluate

the time which is required to earn back the total cost incurred while purchasing the machine.

Calculation of it is as follows:

Provided information =

Particulars Details

Initial investment 275000

Cash inflow 85000

Cash out flow for six years 12500

Formula: Initial investment / cash inflow

= 275000 / 72500

= 3.79 years

Working notes:

Calculation of actual cash inflow:

Cash inflow – cash outflow

= 85000 – 12500

= 72500

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

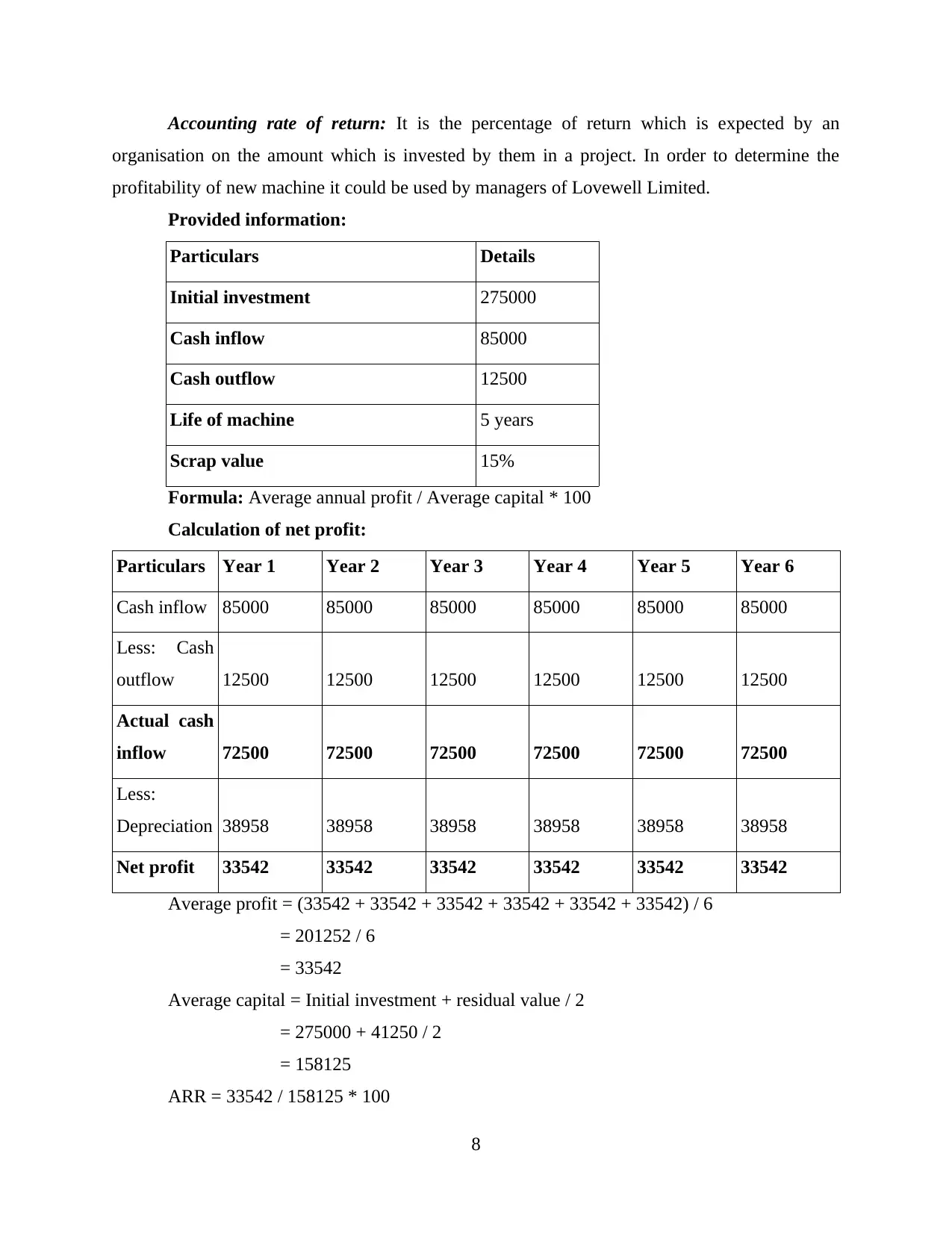

Accounting rate of return: It is the percentage of return which is expected by an

organisation on the amount which is invested by them in a project. In order to determine the

profitability of new machine it could be used by managers of Lovewell Limited.

Provided information:

Particulars Details

Initial investment 275000

Cash inflow 85000

Cash outflow 12500

Life of machine 5 years

Scrap value 15%

Formula: Average annual profit / Average capital * 100

Calculation of net profit:

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Cash inflow 85000 85000 85000 85000 85000 85000

Less: Cash

outflow 12500 12500 12500 12500 12500 12500

Actual cash

inflow 72500 72500 72500 72500 72500 72500

Less:

Depreciation 38958 38958 38958 38958 38958 38958

Net profit 33542 33542 33542 33542 33542 33542

Average profit = (33542 + 33542 + 33542 + 33542 + 33542 + 33542) / 6

= 201252 / 6

= 33542

Average capital = Initial investment + residual value / 2

= 275000 + 41250 / 2

= 158125

ARR = 33542 / 158125 * 100

8

organisation on the amount which is invested by them in a project. In order to determine the

profitability of new machine it could be used by managers of Lovewell Limited.

Provided information:

Particulars Details

Initial investment 275000

Cash inflow 85000

Cash outflow 12500

Life of machine 5 years

Scrap value 15%

Formula: Average annual profit / Average capital * 100

Calculation of net profit:

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Cash inflow 85000 85000 85000 85000 85000 85000

Less: Cash

outflow 12500 12500 12500 12500 12500 12500

Actual cash

inflow 72500 72500 72500 72500 72500 72500

Less:

Depreciation 38958 38958 38958 38958 38958 38958

Net profit 33542 33542 33542 33542 33542 33542

Average profit = (33542 + 33542 + 33542 + 33542 + 33542 + 33542) / 6

= 201252 / 6

= 33542

Average capital = Initial investment + residual value / 2

= 275000 + 41250 / 2

= 158125

ARR = 33542 / 158125 * 100

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 21.21%

Working notes:

Calculation of depreciation:

Formula: Initial investment – Scrap value / life on project

= 275000 – 41250 / 6

= 38958

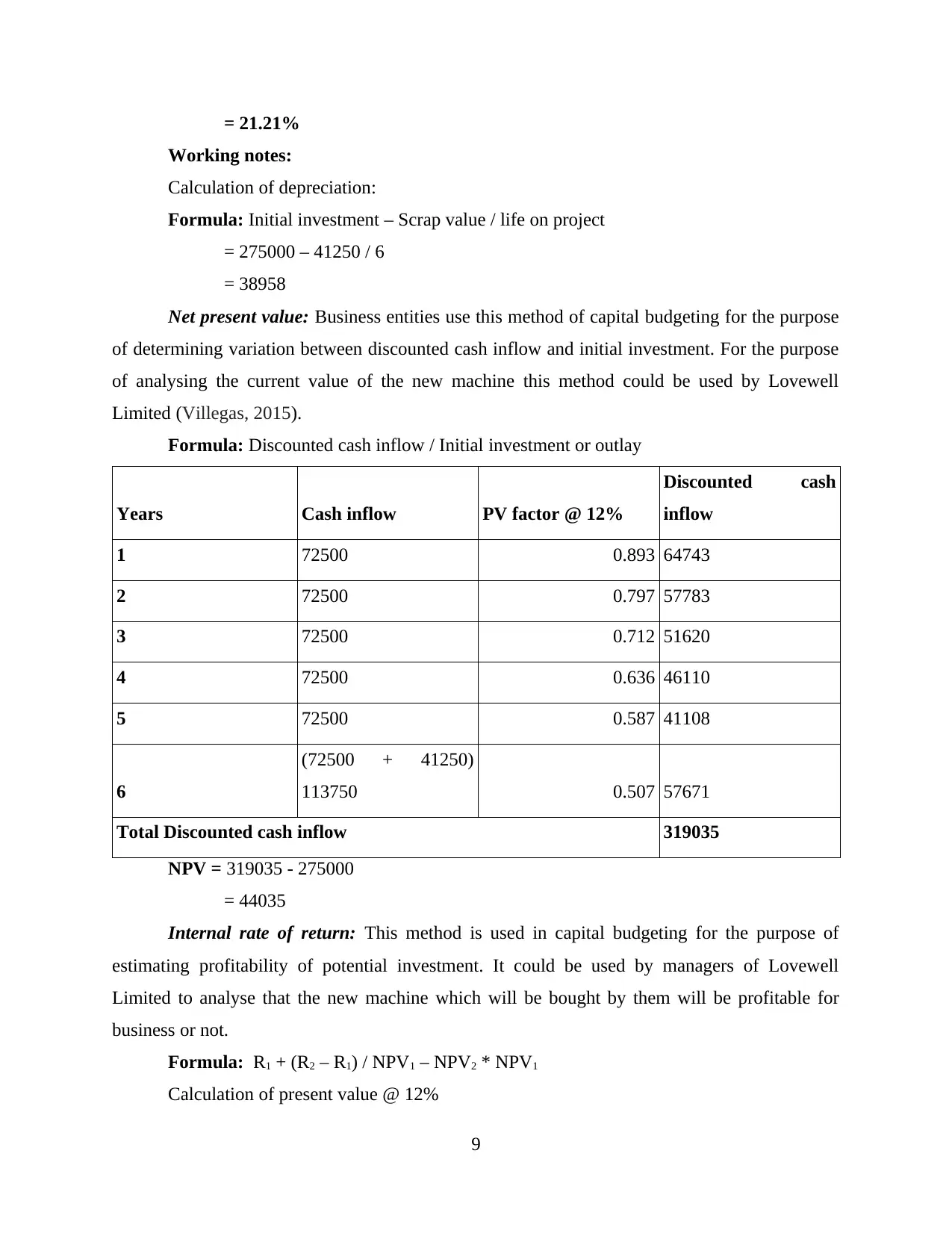

Net present value: Business entities use this method of capital budgeting for the purpose

of determining variation between discounted cash inflow and initial investment. For the purpose

of analysing the current value of the new machine this method could be used by Lovewell

Limited (Villegas, 2015).

Formula: Discounted cash inflow / Initial investment or outlay

Years Cash inflow PV factor @ 12%

Discounted cash

inflow

1 72500 0.893 64743

2 72500 0.797 57783

3 72500 0.712 51620

4 72500 0.636 46110

5 72500 0.587 41108

6

(72500 + 41250)

113750 0.507 57671

Total Discounted cash inflow 319035

NPV = 319035 - 275000

= 44035

Internal rate of return: This method is used in capital budgeting for the purpose of

estimating profitability of potential investment. It could be used by managers of Lovewell

Limited to analyse that the new machine which will be bought by them will be profitable for

business or not.

Formula: R1 + (R2 – R1) / NPV1 – NPV2 * NPV1

Calculation of present value @ 12%

9

Working notes:

Calculation of depreciation:

Formula: Initial investment – Scrap value / life on project

= 275000 – 41250 / 6

= 38958

Net present value: Business entities use this method of capital budgeting for the purpose

of determining variation between discounted cash inflow and initial investment. For the purpose

of analysing the current value of the new machine this method could be used by Lovewell

Limited (Villegas, 2015).

Formula: Discounted cash inflow / Initial investment or outlay

Years Cash inflow PV factor @ 12%

Discounted cash

inflow

1 72500 0.893 64743

2 72500 0.797 57783

3 72500 0.712 51620

4 72500 0.636 46110

5 72500 0.587 41108

6

(72500 + 41250)

113750 0.507 57671

Total Discounted cash inflow 319035

NPV = 319035 - 275000

= 44035

Internal rate of return: This method is used in capital budgeting for the purpose of

estimating profitability of potential investment. It could be used by managers of Lovewell

Limited to analyse that the new machine which will be bought by them will be profitable for

business or not.

Formula: R1 + (R2 – R1) / NPV1 – NPV2 * NPV1

Calculation of present value @ 12%

9

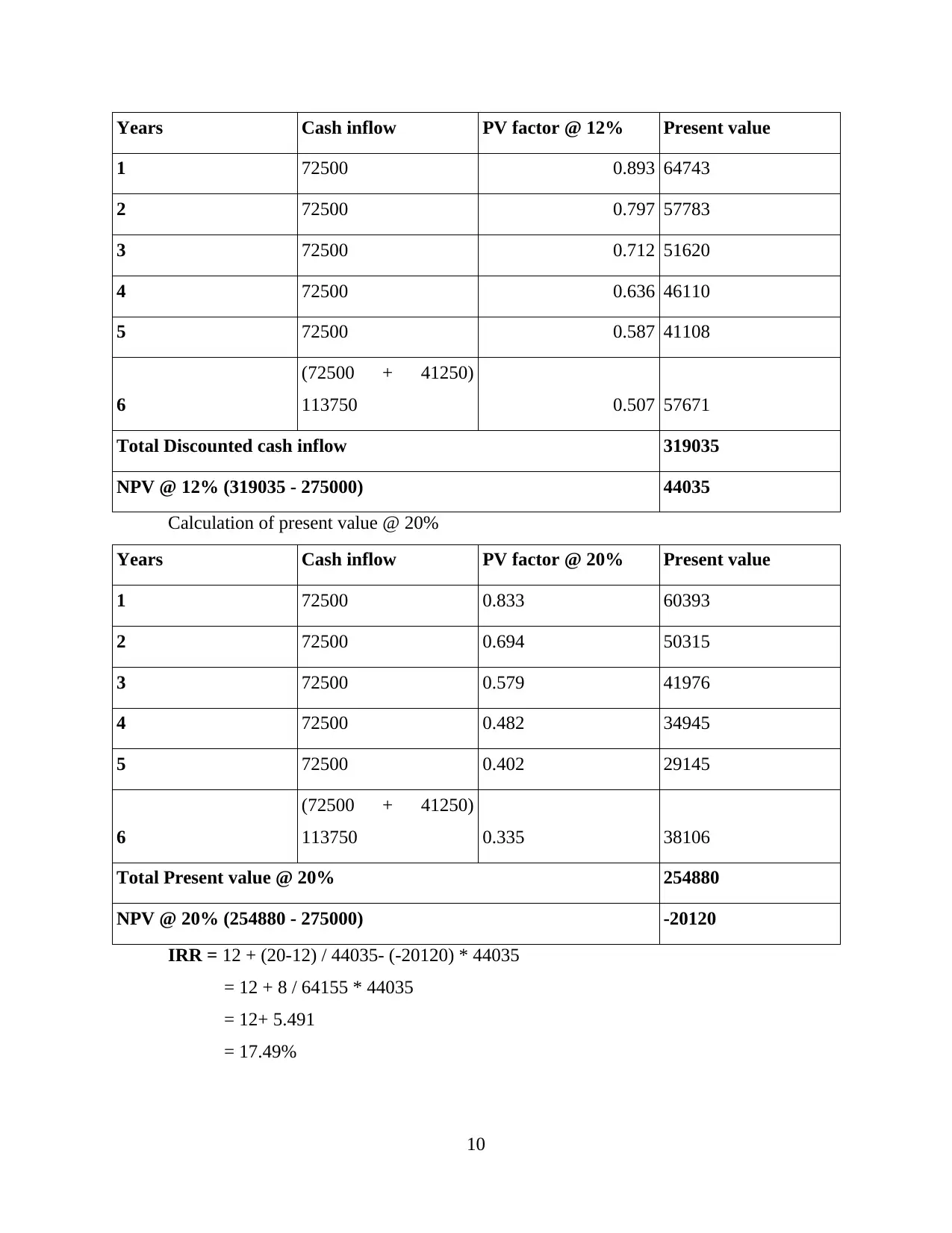

Years Cash inflow PV factor @ 12% Present value

1 72500 0.893 64743

2 72500 0.797 57783

3 72500 0.712 51620

4 72500 0.636 46110

5 72500 0.587 41108

6

(72500 + 41250)

113750 0.507 57671

Total Discounted cash inflow 319035

NPV @ 12% (319035 - 275000) 44035

Calculation of present value @ 20%

Years Cash inflow PV factor @ 20% Present value

1 72500 0.833 60393

2 72500 0.694 50315

3 72500 0.579 41976

4 72500 0.482 34945

5 72500 0.402 29145

6

(72500 + 41250)

113750 0.335 38106

Total Present value @ 20% 254880

NPV @ 20% (254880 - 275000) -20120

IRR = 12 + (20-12) / 44035- (-20120) * 44035

= 12 + 8 / 64155 * 44035

= 12+ 5.491

= 17.49%

10

1 72500 0.893 64743

2 72500 0.797 57783

3 72500 0.712 51620

4 72500 0.636 46110

5 72500 0.587 41108

6

(72500 + 41250)

113750 0.507 57671

Total Discounted cash inflow 319035

NPV @ 12% (319035 - 275000) 44035

Calculation of present value @ 20%

Years Cash inflow PV factor @ 20% Present value

1 72500 0.833 60393

2 72500 0.694 50315

3 72500 0.579 41976

4 72500 0.482 34945

5 72500 0.402 29145

6

(72500 + 41250)

113750 0.335 38106

Total Present value @ 20% 254880

NPV @ 20% (254880 - 275000) -20120

IRR = 12 + (20-12) / 44035- (-20120) * 44035

= 12 + 8 / 64155 * 44035

= 12+ 5.491

= 17.49%

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.