IFM Report: Calculating NPV, IRR, and Investment Decisions Analysis

VerifiedAdded on 2022/12/14

|15

|3357

|158

Report

AI Summary

This report delves into the realm of international financial management, offering a comprehensive analysis of key concepts such as Net Present Value (NPV), Internal Rate of Return (IRR), and their application in investment appraisal. The report begins by calculating the expected NPV and standard deviation of NPV for Toughnut plc, followed by an analysis of RJW's estimated NPV, determining its feasibility. The report also explores the calculation of NPV, IRR, fund allocation, and cash flow for Alder plc, alongside a comparative analysis of different projects based on their NPV rankings. Furthermore, the report examines cash flow calculations, emphasizing the importance of positive NPV in investment decisions. The analysis incorporates financial formulas, tabular representations, and statistical techniques to evaluate the viability of various investment opportunities. Overall, the report aims to provide a practical understanding of financial management principles within an international context, offering insights into making informed investment decisions.

INTERNATIONAL FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1. Calculation of expected NPV and standard deviation of NPV of Toughnut plc.....................1

2. RJW's estimated Net present value..........................................................................................3

3. Calculation of the following for Alder plc...............................................................................4

A. Calculation of net present value..............................................................................................4

B. Internal rate of return for calculating appraisal of project......................................................5

C. Allocation of funds for achieving optimum return for getting high NPV...............................6

D. Calculation of cash flow.........................................................................................................6

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

1. Calculation of expected NPV and standard deviation of NPV of Toughnut plc.....................1

2. RJW's estimated Net present value..........................................................................................3

3. Calculation of the following for Alder plc...............................................................................4

A. Calculation of net present value..............................................................................................4

B. Internal rate of return for calculating appraisal of project......................................................5

C. Allocation of funds for achieving optimum return for getting high NPV...............................6

D. Calculation of cash flow.........................................................................................................6

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

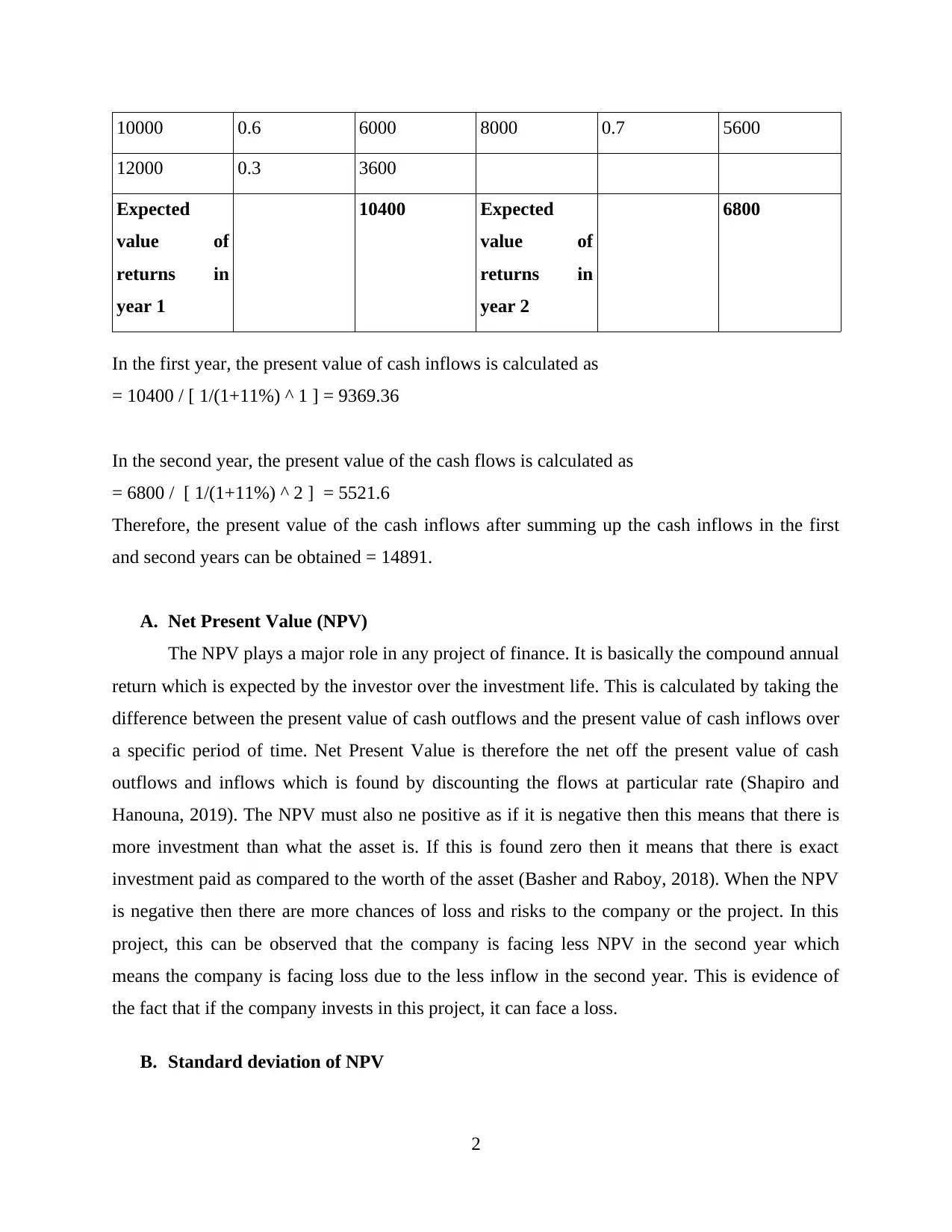

INTRODUCTION

International financial management is also referred as international finance deals in the

management of finance in the business environment which is international. This means making

money by trading through foreign currency exchange. This differs from financial management in

various aspects because as the IFM deals in finance of different countries various aspects are

covered in this such as political situations, diversified opportunity sets, currency and imperfect

markets (Knoke, Gosling and Paul, 2020). These factors are different in all the countries which

must be considered.

The report will shed light on the major areas of finance management such as NPV,

standard deviation of NPV of the companies such as Toughnut plc., RJW plc. etc. Net Present

Value (NPV) deals in the financial metric which helps in capturing the total value of the potential

investment opportunity. This also deals in projecting the future cash flows and the outflows

which are associated with the investment. The calculation of NPV takes into consideration many

factors such as opportunity cost; cost of capital of investor and risk tolerance through the rate of

discount. This is why, NPV or the Net Present Value is the approach which is used for financial

analysis to determine the feasibility of investment in the business or the project (Gaspars-

Wieloch, 2019).

NPV is basically the current value of the future cash flows which are then compared with

the initial investments. This report will also focus on calculating the standard deviation of NPV

which is basically a statistical technique for capital budgeting decisions for determining the

deviation from the means of project cash flows (Madura, 2020). The report will therefore shed

more light on calculation of the NPV and the standard deviation of NPV by using specific

formulas and tables.

1. Calculation of expected NPV and standard deviation of NPV of Toughnut plc

Investment at the initial level = 15000

Year 1

Returns Probability Expected

value

Returns Probability Expected

value

8000 0.1 800 4000 0.3 1200

1

International financial management is also referred as international finance deals in the

management of finance in the business environment which is international. This means making

money by trading through foreign currency exchange. This differs from financial management in

various aspects because as the IFM deals in finance of different countries various aspects are

covered in this such as political situations, diversified opportunity sets, currency and imperfect

markets (Knoke, Gosling and Paul, 2020). These factors are different in all the countries which

must be considered.

The report will shed light on the major areas of finance management such as NPV,

standard deviation of NPV of the companies such as Toughnut plc., RJW plc. etc. Net Present

Value (NPV) deals in the financial metric which helps in capturing the total value of the potential

investment opportunity. This also deals in projecting the future cash flows and the outflows

which are associated with the investment. The calculation of NPV takes into consideration many

factors such as opportunity cost; cost of capital of investor and risk tolerance through the rate of

discount. This is why, NPV or the Net Present Value is the approach which is used for financial

analysis to determine the feasibility of investment in the business or the project (Gaspars-

Wieloch, 2019).

NPV is basically the current value of the future cash flows which are then compared with

the initial investments. This report will also focus on calculating the standard deviation of NPV

which is basically a statistical technique for capital budgeting decisions for determining the

deviation from the means of project cash flows (Madura, 2020). The report will therefore shed

more light on calculation of the NPV and the standard deviation of NPV by using specific

formulas and tables.

1. Calculation of expected NPV and standard deviation of NPV of Toughnut plc

Investment at the initial level = 15000

Year 1

Returns Probability Expected

value

Returns Probability Expected

value

8000 0.1 800 4000 0.3 1200

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10000 0.6 6000 8000 0.7 5600

12000 0.3 3600

Expected

value of

returns in

year 1

10400 Expected

value of

returns in

year 2

6800

In the first year, the present value of cash inflows is calculated as

= 10400 / [ 1/(1+11%) ^ 1 ] = 9369.36

In the second year, the present value of the cash flows is calculated as

= 6800 / [ 1/(1+11%) ^ 2 ] = 5521.6

Therefore, the present value of the cash inflows after summing up the cash inflows in the first

and second years can be obtained = 14891.

A. Net Present Value (NPV)

The NPV plays a major role in any project of finance. It is basically the compound annual

return which is expected by the investor over the investment life. This is calculated by taking the

difference between the present value of cash outflows and the present value of cash inflows over

a specific period of time. Net Present Value is therefore the net off the present value of cash

outflows and inflows which is found by discounting the flows at particular rate (Shapiro and

Hanouna, 2019). The NPV must also ne positive as if it is negative then this means that there is

more investment than what the asset is. If this is found zero then it means that there is exact

investment paid as compared to the worth of the asset (Basher and Raboy, 2018). When the NPV

is negative then there are more chances of loss and risks to the company or the project. In this

project, this can be observed that the company is facing less NPV in the second year which

means the company is facing loss due to the less inflow in the second year. This is evidence of

the fact that if the company invests in this project, it can face a loss.

B. Standard deviation of NPV

2

12000 0.3 3600

Expected

value of

returns in

year 1

10400 Expected

value of

returns in

year 2

6800

In the first year, the present value of cash inflows is calculated as

= 10400 / [ 1/(1+11%) ^ 1 ] = 9369.36

In the second year, the present value of the cash flows is calculated as

= 6800 / [ 1/(1+11%) ^ 2 ] = 5521.6

Therefore, the present value of the cash inflows after summing up the cash inflows in the first

and second years can be obtained = 14891.

A. Net Present Value (NPV)

The NPV plays a major role in any project of finance. It is basically the compound annual

return which is expected by the investor over the investment life. This is calculated by taking the

difference between the present value of cash outflows and the present value of cash inflows over

a specific period of time. Net Present Value is therefore the net off the present value of cash

outflows and inflows which is found by discounting the flows at particular rate (Shapiro and

Hanouna, 2019). The NPV must also ne positive as if it is negative then this means that there is

more investment than what the asset is. If this is found zero then it means that there is exact

investment paid as compared to the worth of the asset (Basher and Raboy, 2018). When the NPV

is negative then there are more chances of loss and risks to the company or the project. In this

project, this can be observed that the company is facing less NPV in the second year which

means the company is facing loss due to the less inflow in the second year. This is evidence of

the fact that if the company invests in this project, it can face a loss.

B. Standard deviation of NPV

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

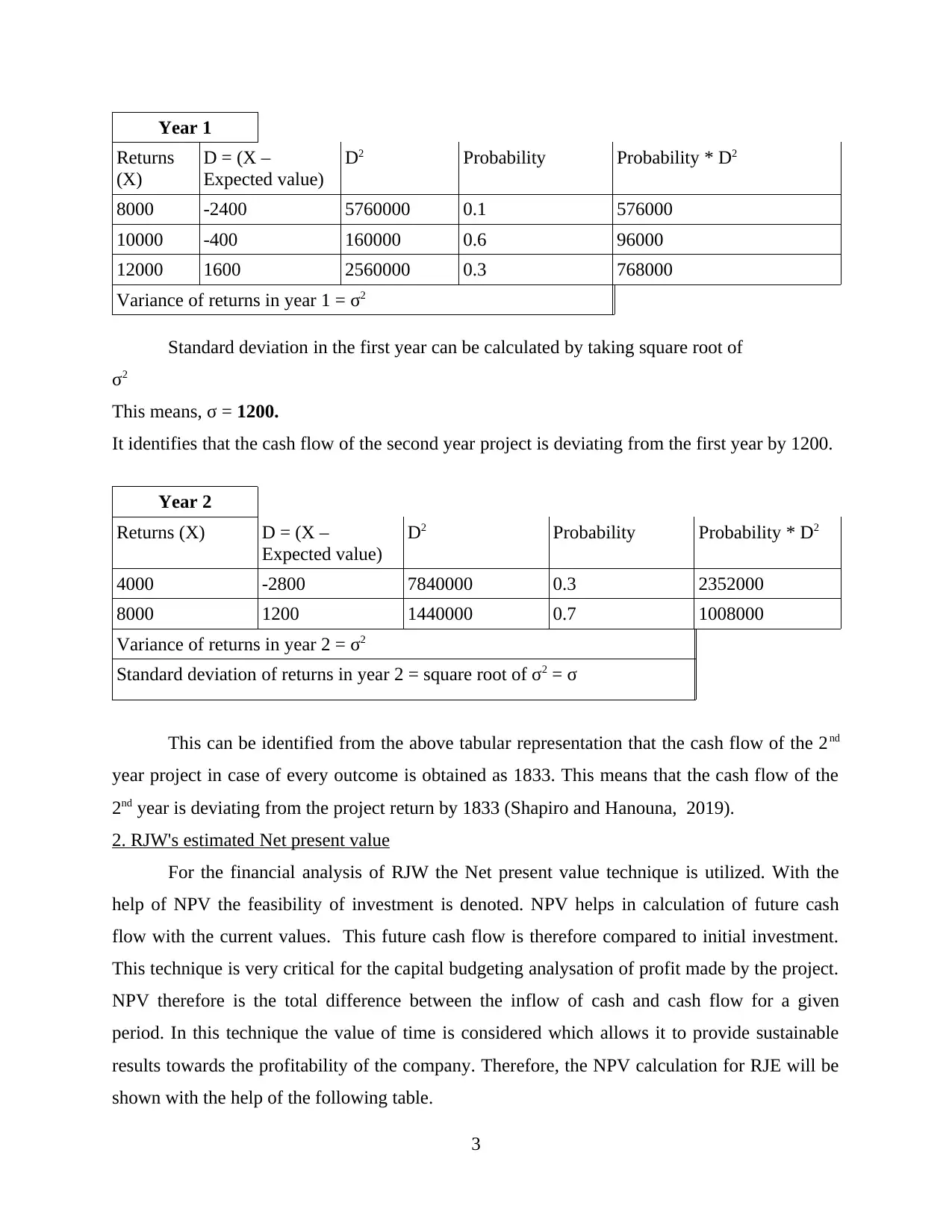

Year 1

Returns

(X)

D = (X –

Expected value)

D2 Probability Probability * D2

8000 -2400 5760000 0.1 576000

10000 -400 160000 0.6 96000

12000 1600 2560000 0.3 768000

Variance of returns in year 1 = σ2

Standard deviation in the first year can be calculated by taking square root of

σ2

This means, σ = 1200.

It identifies that the cash flow of the second year project is deviating from the first year by 1200.

Year 2

Returns (X) D = (X –

Expected value)

D2 Probability Probability * D2

4000 -2800 7840000 0.3 2352000

8000 1200 1440000 0.7 1008000

Variance of returns in year 2 = σ2

Standard deviation of returns in year 2 = square root of σ2 = σ

This can be identified from the above tabular representation that the cash flow of the 2nd

year project in case of every outcome is obtained as 1833. This means that the cash flow of the

2nd year is deviating from the project return by 1833 (Shapiro and Hanouna, 2019).

2. RJW's estimated Net present value

For the financial analysis of RJW the Net present value technique is utilized. With the

help of NPV the feasibility of investment is denoted. NPV helps in calculation of future cash

flow with the current values. This future cash flow is therefore compared to initial investment.

This technique is very critical for the capital budgeting analysation of profit made by the project.

NPV therefore is the total difference between the inflow of cash and cash flow for a given

period. In this technique the value of time is considered which allows it to provide sustainable

results towards the profitability of the company. Therefore, the NPV calculation for RJE will be

shown with the help of the following table.

3

Returns

(X)

D = (X –

Expected value)

D2 Probability Probability * D2

8000 -2400 5760000 0.1 576000

10000 -400 160000 0.6 96000

12000 1600 2560000 0.3 768000

Variance of returns in year 1 = σ2

Standard deviation in the first year can be calculated by taking square root of

σ2

This means, σ = 1200.

It identifies that the cash flow of the second year project is deviating from the first year by 1200.

Year 2

Returns (X) D = (X –

Expected value)

D2 Probability Probability * D2

4000 -2800 7840000 0.3 2352000

8000 1200 1440000 0.7 1008000

Variance of returns in year 2 = σ2

Standard deviation of returns in year 2 = square root of σ2 = σ

This can be identified from the above tabular representation that the cash flow of the 2nd

year project in case of every outcome is obtained as 1833. This means that the cash flow of the

2nd year is deviating from the project return by 1833 (Shapiro and Hanouna, 2019).

2. RJW's estimated Net present value

For the financial analysis of RJW the Net present value technique is utilized. With the

help of NPV the feasibility of investment is denoted. NPV helps in calculation of future cash

flow with the current values. This future cash flow is therefore compared to initial investment.

This technique is very critical for the capital budgeting analysation of profit made by the project.

NPV therefore is the total difference between the inflow of cash and cash flow for a given

period. In this technique the value of time is considered which allows it to provide sustainable

results towards the profitability of the company. Therefore, the NPV calculation for RJE will be

shown with the help of the following table.

3

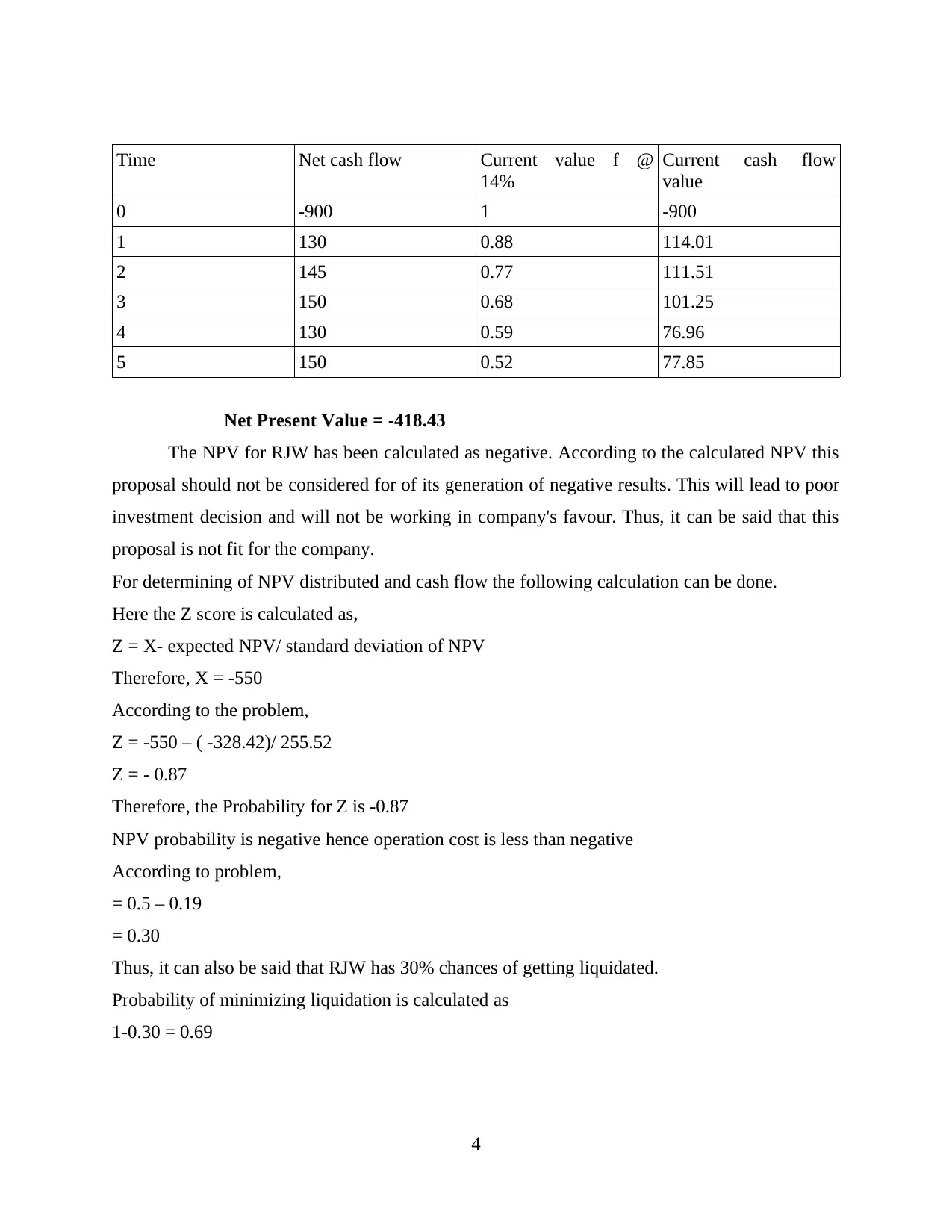

Time Net cash flow Current value f @

14%

Current cash flow

value

0 -900 1 -900

1 130 0.88 114.01

2 145 0.77 111.51

3 150 0.68 101.25

4 130 0.59 76.96

5 150 0.52 77.85

Net Present Value = -418.43

The NPV for RJW has been calculated as negative. According to the calculated NPV this

proposal should not be considered for of its generation of negative results. This will lead to poor

investment decision and will not be working in company's favour. Thus, it can be said that this

proposal is not fit for the company.

For determining of NPV distributed and cash flow the following calculation can be done.

Here the Z score is calculated as,

Z = X- expected NPV/ standard deviation of NPV

Therefore, X = -550

According to the problem,

Z = -550 – ( -328.42)/ 255.52

Z = - 0.87

Therefore, the Probability for Z is -0.87

NPV probability is negative hence operation cost is less than negative

According to problem,

= 0.5 – 0.19

= 0.30

Thus, it can also be said that RJW has 30% chances of getting liquidated.

Probability of minimizing liquidation is calculated as

1-0.30 = 0.69

4

14%

Current cash flow

value

0 -900 1 -900

1 130 0.88 114.01

2 145 0.77 111.51

3 150 0.68 101.25

4 130 0.59 76.96

5 150 0.52 77.85

Net Present Value = -418.43

The NPV for RJW has been calculated as negative. According to the calculated NPV this

proposal should not be considered for of its generation of negative results. This will lead to poor

investment decision and will not be working in company's favour. Thus, it can be said that this

proposal is not fit for the company.

For determining of NPV distributed and cash flow the following calculation can be done.

Here the Z score is calculated as,

Z = X- expected NPV/ standard deviation of NPV

Therefore, X = -550

According to the problem,

Z = -550 – ( -328.42)/ 255.52

Z = - 0.87

Therefore, the Probability for Z is -0.87

NPV probability is negative hence operation cost is less than negative

According to problem,

= 0.5 – 0.19

= 0.30

Thus, it can also be said that RJW has 30% chances of getting liquidated.

Probability of minimizing liquidation is calculated as

1-0.30 = 0.69

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

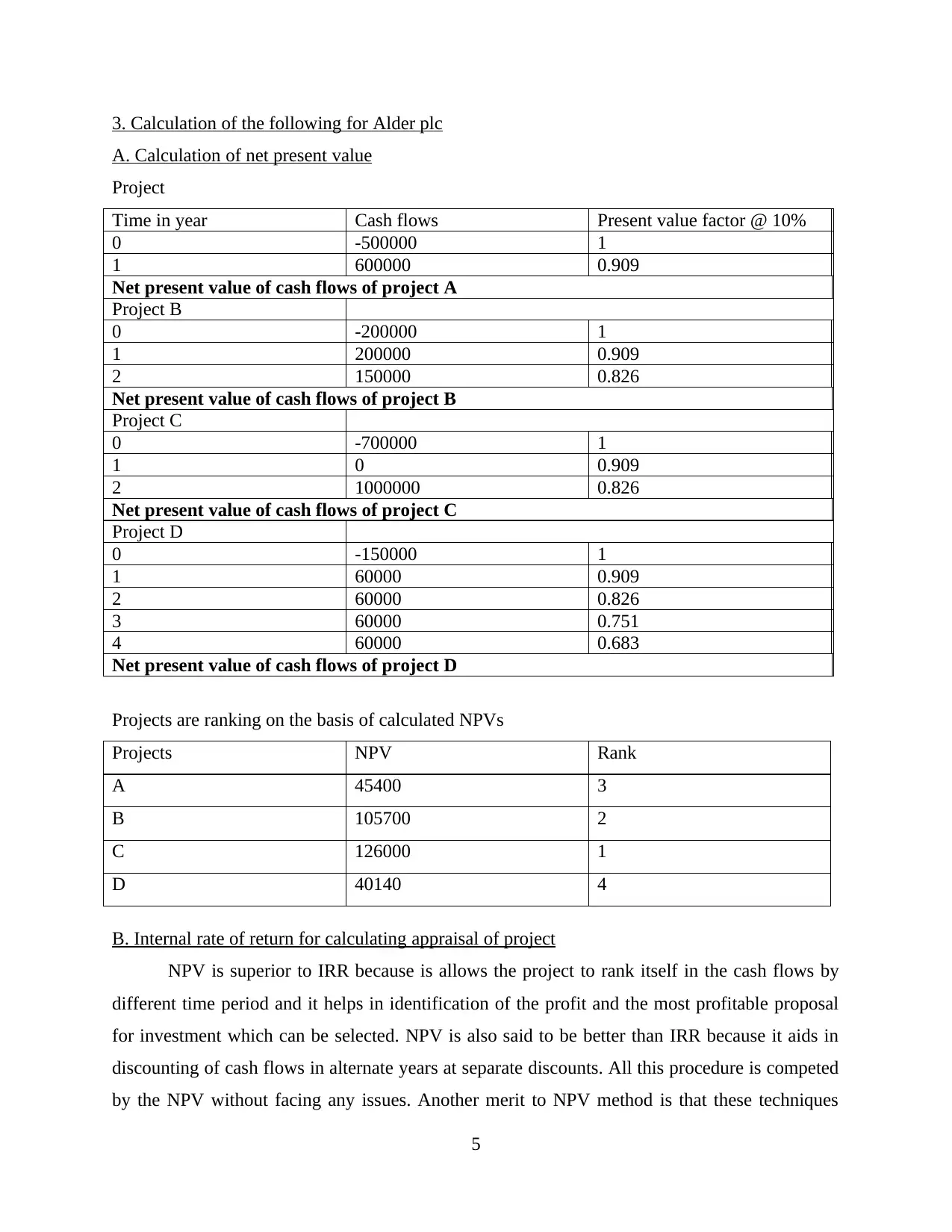

3. Calculation of the following for Alder plc

A. Calculation of net present value

Project

Time in year Cash flows Present value factor @ 10%

0 -500000 1

1 600000 0.909

Net present value of cash flows of project A

Project B

0 -200000 1

1 200000 0.909

2 150000 0.826

Net present value of cash flows of project B

Project C

0 -700000 1

1 0 0.909

2 1000000 0.826

Net present value of cash flows of project C

Project D

0 -150000 1

1 60000 0.909

2 60000 0.826

3 60000 0.751

4 60000 0.683

Net present value of cash flows of project D

Projects are ranking on the basis of calculated NPVs

Projects NPV Rank

A 45400 3

B 105700 2

C 126000 1

D 40140 4

B. Internal rate of return for calculating appraisal of project

NPV is superior to IRR because is allows the project to rank itself in the cash flows by

different time period and it helps in identification of the profit and the most profitable proposal

for investment which can be selected. NPV is also said to be better than IRR because it aids in

discounting of cash flows in alternate years at separate discounts. All this procedure is competed

by the NPV without facing any issues. Another merit to NPV method is that these techniques

5

A. Calculation of net present value

Project

Time in year Cash flows Present value factor @ 10%

0 -500000 1

1 600000 0.909

Net present value of cash flows of project A

Project B

0 -200000 1

1 200000 0.909

2 150000 0.826

Net present value of cash flows of project B

Project C

0 -700000 1

1 0 0.909

2 1000000 0.826

Net present value of cash flows of project C

Project D

0 -150000 1

1 60000 0.909

2 60000 0.826

3 60000 0.751

4 60000 0.683

Net present value of cash flows of project D

Projects are ranking on the basis of calculated NPVs

Projects NPV Rank

A 45400 3

B 105700 2

C 126000 1

D 40140 4

B. Internal rate of return for calculating appraisal of project

NPV is superior to IRR because is allows the project to rank itself in the cash flows by

different time period and it helps in identification of the profit and the most profitable proposal

for investment which can be selected. NPV is also said to be better than IRR because it aids in

discounting of cash flows in alternate years at separate discounts. All this procedure is competed

by the NPV without facing any issues. Another merit to NPV method is that these techniques

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

allows the calculation of lots of discounted rates for making the business more flexible allowing

the company more options during selection of its investments. IRR tool do not have this system

present in it making it less flexible enough.

Another technique which is very useful when it comes to making investment decision is

the decision-making technique. With the help of NPV all the factors of inflow can be found

according to the life of the project. In IRR the discounting rate for return and reinvestment rates

both can be said as same as per NPV. Thus, it makes both the techniques quite different from

each other. All the factors of financial management influences the decision-making of context of

investment in the project.

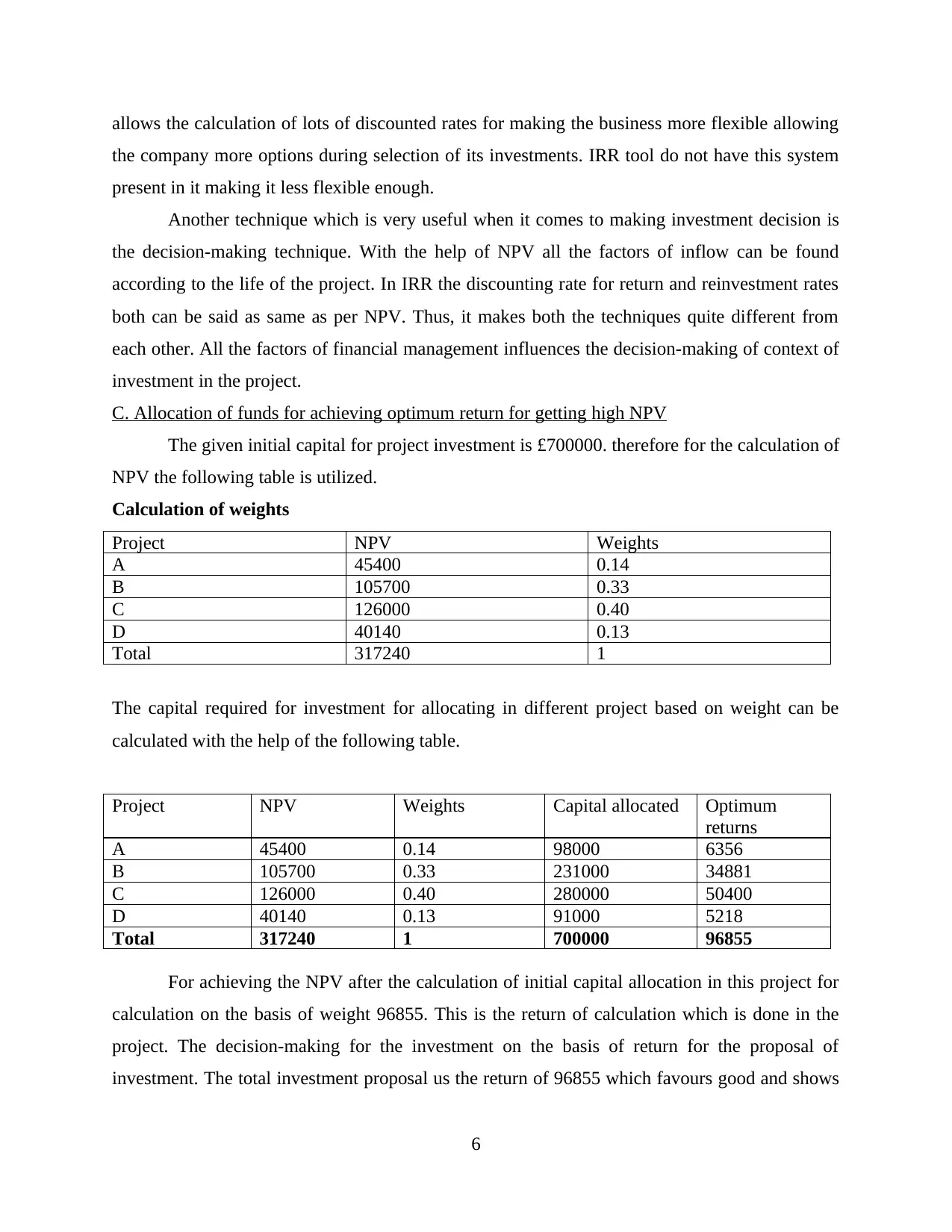

C. Allocation of funds for achieving optimum return for getting high NPV

The given initial capital for project investment is £700000. therefore for the calculation of

NPV the following table is utilized.

Calculation of weights

Project NPV Weights

A 45400 0.14

B 105700 0.33

C 126000 0.40

D 40140 0.13

Total 317240 1

The capital required for investment for allocating in different project based on weight can be

calculated with the help of the following table.

Project NPV Weights Capital allocated Optimum

returns

A 45400 0.14 98000 6356

B 105700 0.33 231000 34881

C 126000 0.40 280000 50400

D 40140 0.13 91000 5218

Total 317240 1 700000 96855

For achieving the NPV after the calculation of initial capital allocation in this project for

calculation on the basis of weight 96855. This is the return of calculation which is done in the

project. The decision-making for the investment on the basis of return for the proposal of

investment. The total investment proposal us the return of 96855 which favours good and shows

6

the company more options during selection of its investments. IRR tool do not have this system

present in it making it less flexible enough.

Another technique which is very useful when it comes to making investment decision is

the decision-making technique. With the help of NPV all the factors of inflow can be found

according to the life of the project. In IRR the discounting rate for return and reinvestment rates

both can be said as same as per NPV. Thus, it makes both the techniques quite different from

each other. All the factors of financial management influences the decision-making of context of

investment in the project.

C. Allocation of funds for achieving optimum return for getting high NPV

The given initial capital for project investment is £700000. therefore for the calculation of

NPV the following table is utilized.

Calculation of weights

Project NPV Weights

A 45400 0.14

B 105700 0.33

C 126000 0.40

D 40140 0.13

Total 317240 1

The capital required for investment for allocating in different project based on weight can be

calculated with the help of the following table.

Project NPV Weights Capital allocated Optimum

returns

A 45400 0.14 98000 6356

B 105700 0.33 231000 34881

C 126000 0.40 280000 50400

D 40140 0.13 91000 5218

Total 317240 1 700000 96855

For achieving the NPV after the calculation of initial capital allocation in this project for

calculation on the basis of weight 96855. This is the return of calculation which is done in the

project. The decision-making for the investment on the basis of return for the proposal of

investment. The total investment proposal us the return of 96855 which favours good and shows

6

the value of net present value and technique for selection of profitability in the project (Dikov,

2020).

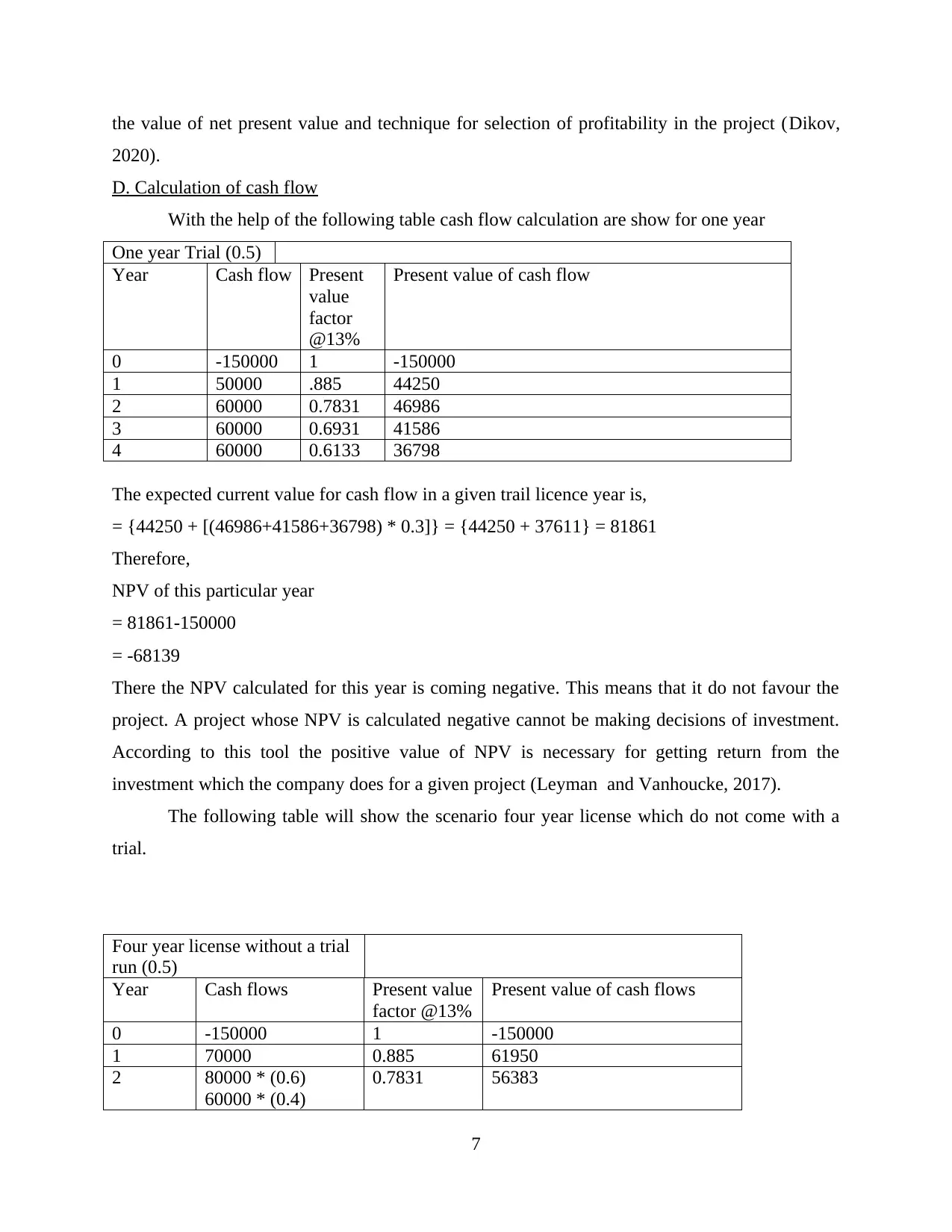

D. Calculation of cash flow

With the help of the following table cash flow calculation are show for one year

One year Trial (0.5)

Year Cash flow Present

value

factor

@13%

Present value of cash flow

0 -150000 1 -150000

1 50000 .885 44250

2 60000 0.7831 46986

3 60000 0.6931 41586

4 60000 0.6133 36798

The expected current value for cash flow in a given trail licence year is,

= {44250 + [(46986+41586+36798) * 0.3]} = {44250 + 37611} = 81861

Therefore,

NPV of this particular year

= 81861-150000

= -68139

There the NPV calculated for this year is coming negative. This means that it do not favour the

project. A project whose NPV is calculated negative cannot be making decisions of investment.

According to this tool the positive value of NPV is necessary for getting return from the

investment which the company does for a given project (Leyman and Vanhoucke, 2017).

The following table will show the scenario four year license which do not come with a

trial.

Four year license without a trial

run (0.5)

Year Cash flows Present value

factor @13%

Present value of cash flows

0 -150000 1 -150000

1 70000 0.885 61950

2 80000 * (0.6)

60000 * (0.4)

0.7831 56383

7

2020).

D. Calculation of cash flow

With the help of the following table cash flow calculation are show for one year

One year Trial (0.5)

Year Cash flow Present

value

factor

@13%

Present value of cash flow

0 -150000 1 -150000

1 50000 .885 44250

2 60000 0.7831 46986

3 60000 0.6931 41586

4 60000 0.6133 36798

The expected current value for cash flow in a given trail licence year is,

= {44250 + [(46986+41586+36798) * 0.3]} = {44250 + 37611} = 81861

Therefore,

NPV of this particular year

= 81861-150000

= -68139

There the NPV calculated for this year is coming negative. This means that it do not favour the

project. A project whose NPV is calculated negative cannot be making decisions of investment.

According to this tool the positive value of NPV is necessary for getting return from the

investment which the company does for a given project (Leyman and Vanhoucke, 2017).

The following table will show the scenario four year license which do not come with a

trial.

Four year license without a trial

run (0.5)

Year Cash flows Present value

factor @13%

Present value of cash flows

0 -150000 1 -150000

1 70000 0.885 61950

2 80000 * (0.6)

60000 * (0.4)

0.7831 56383

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3 80000 * (0.6)

60000 * (0.4)

0.6931 49903

4 80000 * (0.6)

60000 * (0.4)

0.6133 44158

The expected current value for last four years cash flow without a trial can be calculated as.

= [61950 + 56383 + 49903 + 44158] = 212394

NPV for 4 years of licence = 212394 – 150000 = 62394 (Dikov, 2020)

From the above calculation the generated value of NPV is determined positive. Therefore, it can

be said that this project can be done. This is because the positive NPV provides a business with

high returns and thus the company is eligible to take this decision for the project (Gabbi and

Levich, 2019).

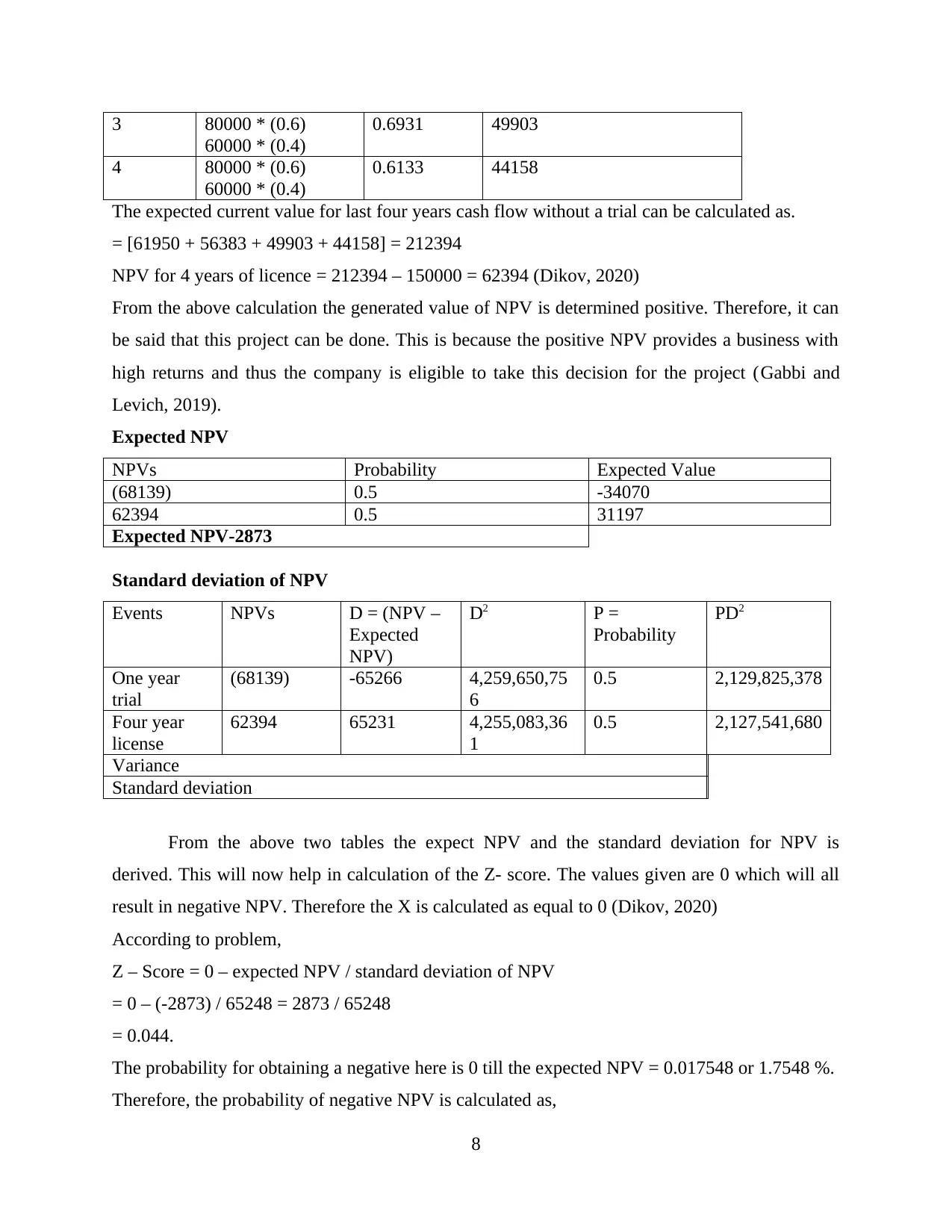

Expected NPV

NPVs Probability Expected Value

(68139) 0.5 -34070

62394 0.5 31197

Expected NPV-2873

Standard deviation of NPV

Events NPVs D = (NPV –

Expected

NPV)

D2 P =

Probability

PD2

One year

trial

(68139) -65266 4,259,650,75

6

0.5 2,129,825,378

Four year

license

62394 65231 4,255,083,36

1

0.5 2,127,541,680

Variance

Standard deviation

From the above two tables the expect NPV and the standard deviation for NPV is

derived. This will now help in calculation of the Z- score. The values given are 0 which will all

result in negative NPV. Therefore the X is calculated as equal to 0 (Dikov, 2020)

According to problem,

Z – Score = 0 – expected NPV / standard deviation of NPV

= 0 – (-2873) / 65248 = 2873 / 65248

= 0.044.

The probability for obtaining a negative here is 0 till the expected NPV = 0.017548 or 1.7548 %.

Therefore, the probability of negative NPV is calculated as,

8

60000 * (0.4)

0.6931 49903

4 80000 * (0.6)

60000 * (0.4)

0.6133 44158

The expected current value for last four years cash flow without a trial can be calculated as.

= [61950 + 56383 + 49903 + 44158] = 212394

NPV for 4 years of licence = 212394 – 150000 = 62394 (Dikov, 2020)

From the above calculation the generated value of NPV is determined positive. Therefore, it can

be said that this project can be done. This is because the positive NPV provides a business with

high returns and thus the company is eligible to take this decision for the project (Gabbi and

Levich, 2019).

Expected NPV

NPVs Probability Expected Value

(68139) 0.5 -34070

62394 0.5 31197

Expected NPV-2873

Standard deviation of NPV

Events NPVs D = (NPV –

Expected

NPV)

D2 P =

Probability

PD2

One year

trial

(68139) -65266 4,259,650,75

6

0.5 2,129,825,378

Four year

license

62394 65231 4,255,083,36

1

0.5 2,127,541,680

Variance

Standard deviation

From the above two tables the expect NPV and the standard deviation for NPV is

derived. This will now help in calculation of the Z- score. The values given are 0 which will all

result in negative NPV. Therefore the X is calculated as equal to 0 (Dikov, 2020)

According to problem,

Z – Score = 0 – expected NPV / standard deviation of NPV

= 0 – (-2873) / 65248 = 2873 / 65248

= 0.044.

The probability for obtaining a negative here is 0 till the expected NPV = 0.017548 or 1.7548 %.

Therefore, the probability of negative NPV is calculated as,

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 0.5 + 0.017548

= 0.5175 or 51.75%.

In all the analysed project there remains a factor of negative NPV which helps in not making

decisions of investment. In the scenario were the company has made an investment decision it

will be very difficult for the company to handle and the business will start facing losses. The

negative value of NPV shows that the business will not be successful in earning from investment

in there project. This it is required by the business to make careful evaluation for all the types of

investments. This shows the importance of NPV and also provides exact picture of the given

project based on the investment of the business (Yusrina and et.al 2017).

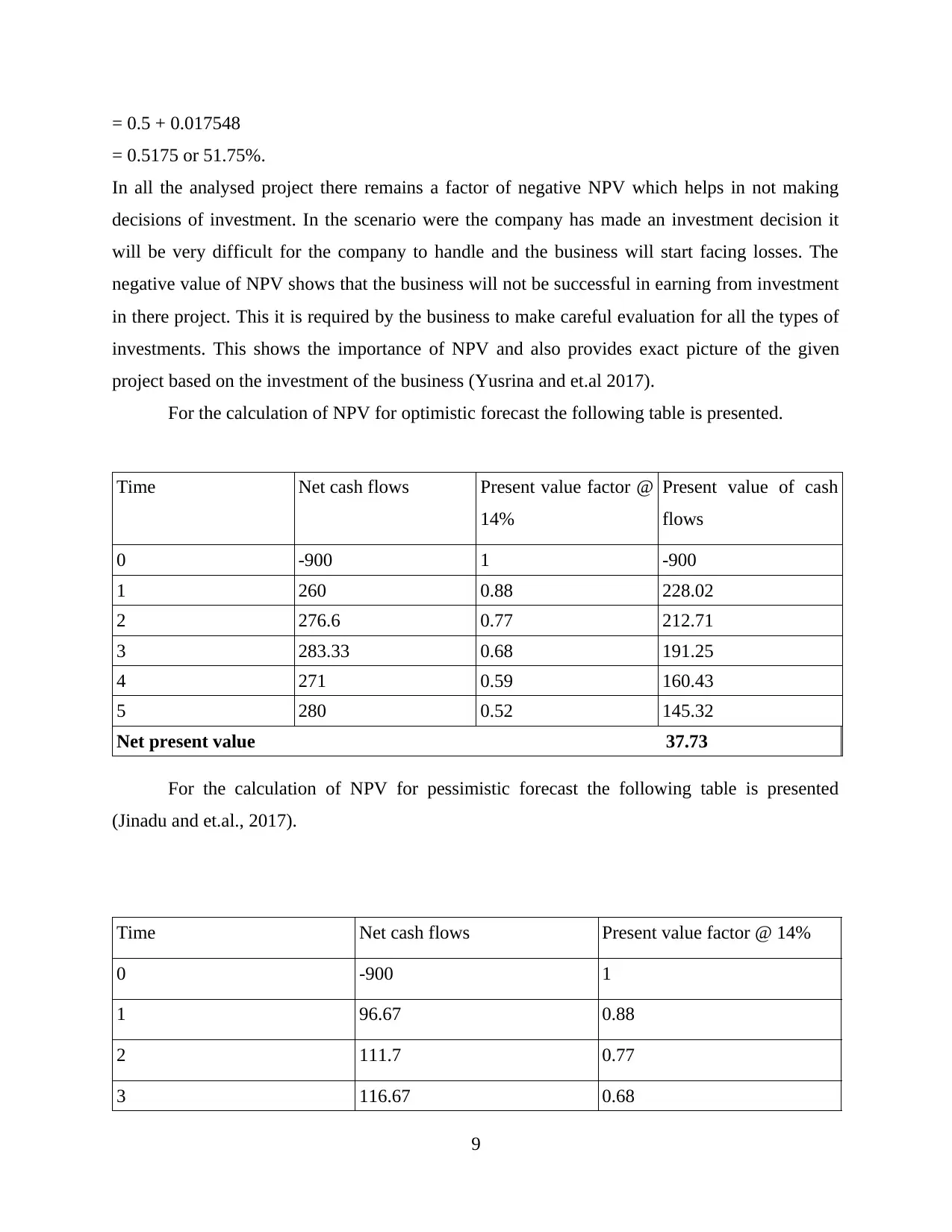

For the calculation of NPV for optimistic forecast the following table is presented.

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 260 0.88 228.02

2 276.6 0.77 212.71

3 283.33 0.68 191.25

4 271 0.59 160.43

5 280 0.52 145.32

Net present value 37.73

For the calculation of NPV for pessimistic forecast the following table is presented

(Jinadu and et.al., 2017).

Time Net cash flows Present value factor @ 14%

0 -900 1

1 96.67 0.88

2 111.7 0.77

3 116.67 0.68

9

= 0.5175 or 51.75%.

In all the analysed project there remains a factor of negative NPV which helps in not making

decisions of investment. In the scenario were the company has made an investment decision it

will be very difficult for the company to handle and the business will start facing losses. The

negative value of NPV shows that the business will not be successful in earning from investment

in there project. This it is required by the business to make careful evaluation for all the types of

investments. This shows the importance of NPV and also provides exact picture of the given

project based on the investment of the business (Yusrina and et.al 2017).

For the calculation of NPV for optimistic forecast the following table is presented.

Time Net cash flows Present value factor @

14%

Present value of cash

flows

0 -900 1 -900

1 260 0.88 228.02

2 276.6 0.77 212.71

3 283.33 0.68 191.25

4 271 0.59 160.43

5 280 0.52 145.32

Net present value 37.73

For the calculation of NPV for pessimistic forecast the following table is presented

(Jinadu and et.al., 2017).

Time Net cash flows Present value factor @ 14%

0 -900 1

1 96.67 0.88

2 111.7 0.77

3 116.67 0.68

9

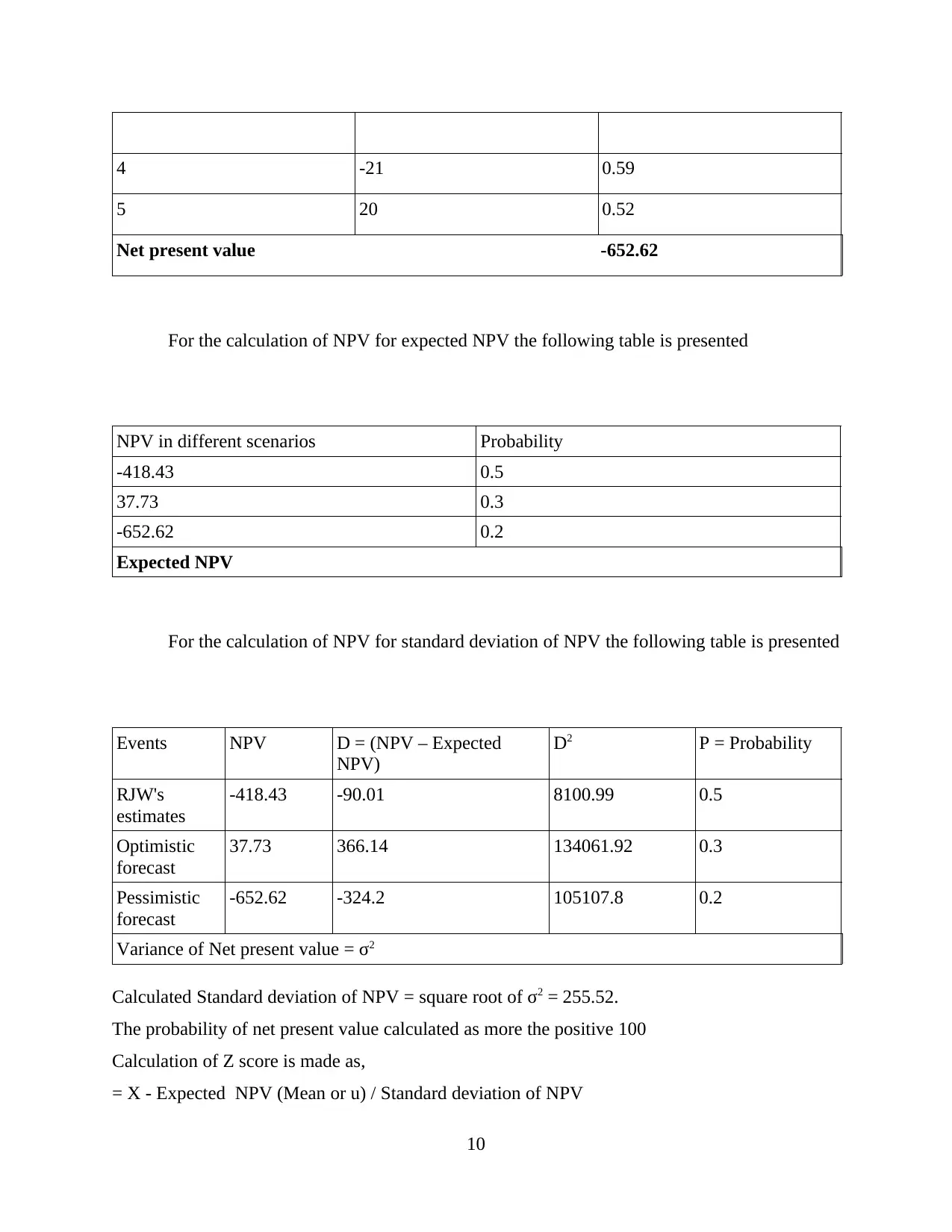

4 -21 0.59

5 20 0.52

Net present value -652.62

For the calculation of NPV for expected NPV the following table is presented

NPV in different scenarios Probability

-418.43 0.5

37.73 0.3

-652.62 0.2

Expected NPV

For the calculation of NPV for standard deviation of NPV the following table is presented

Events NPV D = (NPV – Expected

NPV)

D2 P = Probability

RJW's

estimates

-418.43 -90.01 8100.99 0.5

Optimistic

forecast

37.73 366.14 134061.92 0.3

Pessimistic

forecast

-652.62 -324.2 105107.8 0.2

Variance of Net present value = σ2

Calculated Standard deviation of NPV = square root of σ2 = 255.52.

The probability of net present value calculated as more the positive 100

Calculation of Z score is made as,

= X - Expected NPV (Mean or u) / Standard deviation of NPV

10

5 20 0.52

Net present value -652.62

For the calculation of NPV for expected NPV the following table is presented

NPV in different scenarios Probability

-418.43 0.5

37.73 0.3

-652.62 0.2

Expected NPV

For the calculation of NPV for standard deviation of NPV the following table is presented

Events NPV D = (NPV – Expected

NPV)

D2 P = Probability

RJW's

estimates

-418.43 -90.01 8100.99 0.5

Optimistic

forecast

37.73 366.14 134061.92 0.3

Pessimistic

forecast

-652.62 -324.2 105107.8 0.2

Variance of Net present value = σ2

Calculated Standard deviation of NPV = square root of σ2 = 255.52.

The probability of net present value calculated as more the positive 100

Calculation of Z score is made as,

= X - Expected NPV (Mean or u) / Standard deviation of NPV

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

![International Finance Management Assignment - Finance [Course Code]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Ffd%2F69271dad5c5f4f2c8ab93e7e6daf77ee.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.