Financial Management Report: Valuation, Capital Budgeting Analysis

VerifiedAdded on 2023/01/10

|15

|3687

|92

Report

AI Summary

This report provides a comprehensive analysis of financial management concepts. It begins with an introduction to financial management, emphasizing its role in decision-making. The report then delves into valuation methods, including the price/earnings ratio, dividend valuation, and discounted cash flow, with detailed calculations and critical reviews of each method. The report further explores capital budgeting tools, calculating and evaluating the merits and demerits of various techniques such as Net Present Value (NPV), Internal Rate of Return (IRR), payback period, and accounting rate of return (ARR). The analysis includes detailed calculations, tables, and critical evaluations, providing a thorough understanding of financial management principles and their application in investment decisions. The report concludes with a critical review of each method and tool, highlighting their strengths and weaknesses.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Question 2 – Mergers and Takeovers..............................................................................................3

a) Price/earnings ratio.................................................................................................................3

b) Dividend valuation method.....................................................................................................4

c) Discounted cash flow method.................................................................................................5

d. Critical review.........................................................................................................................6

Question 3........................................................................................................................................7

a. Calculating capital budgeting tool ..........................................................................................7

b. Critically evaluating merits & demerits of different capital budgeting tools .........................9

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

Question 2 – Mergers and Takeovers..............................................................................................3

a) Price/earnings ratio.................................................................................................................3

b) Dividend valuation method.....................................................................................................4

c) Discounted cash flow method.................................................................................................5

d. Critical review.........................................................................................................................6

Question 3........................................................................................................................................7

a. Calculating capital budgeting tool ..........................................................................................7

b. Critically evaluating merits & demerits of different capital budgeting tools .........................9

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

FM refers to planning, directing, organizing & controlling financial activities like

acquisition and use of funds of an entity. It means as application of the general principles of

management to the financial resources of company. It acts as the most important part of an

organization as all the important decisions are based on FM such as investment, dividend and

financing decision. The present report is based on different aspects of FM which include

computation of P/E ratio and valuation of dividend and asset. Furthermore, the report highlights

different methods of capital budgeting which helps in analysing the suitability of project.

Moreover, benefits and limitation of investment appraisal tools is also been presented in the

study.

Question 2 – Mergers and Takeovers

a) Price/earnings ratio

The price earnings ratio is the most common and popular method for the purpose of

valuation of the business. Under this approach, the price is identified using PER of the other

similar quoted business in the industry. The PER is evaluated by dividing the present MP per

share of the entity with its earnings per share (EPS). It helps in determining how much money

the investor is willing to pay for the company’s earnings (Ivanovski, Narasanov and Ivanovska,

2018). The companies with the higher earnings growth prospects mainly carry higher price

earnings ratio, this is because of the reason that these business entities are in the position to offer

return to its investors very quickly and higher percentage return in respect to the investment

which will be through offering dividend, rise in the share price or both. For instance, a company

having the price earnings ratio of 15 means it is selling for 15 times of its income and in simple

and easy terms, the investors are in the position to pay £15 for every £1 of present or the coming

years income (JUŠKEVIČIŪTĖ, 2017). In case of mergers and acquisition, using the price

earnings ratio for valuation, it is considered to be very useful as it can be used in comparing the

ratio with the various different business entity in the same industry or even against the historical

values of the company. But this ratio can be easily manipulated by the company as per the

requirement suing the accounting practices.

FM refers to planning, directing, organizing & controlling financial activities like

acquisition and use of funds of an entity. It means as application of the general principles of

management to the financial resources of company. It acts as the most important part of an

organization as all the important decisions are based on FM such as investment, dividend and

financing decision. The present report is based on different aspects of FM which include

computation of P/E ratio and valuation of dividend and asset. Furthermore, the report highlights

different methods of capital budgeting which helps in analysing the suitability of project.

Moreover, benefits and limitation of investment appraisal tools is also been presented in the

study.

Question 2 – Mergers and Takeovers

a) Price/earnings ratio

The price earnings ratio is the most common and popular method for the purpose of

valuation of the business. Under this approach, the price is identified using PER of the other

similar quoted business in the industry. The PER is evaluated by dividing the present MP per

share of the entity with its earnings per share (EPS). It helps in determining how much money

the investor is willing to pay for the company’s earnings (Ivanovski, Narasanov and Ivanovska,

2018). The companies with the higher earnings growth prospects mainly carry higher price

earnings ratio, this is because of the reason that these business entities are in the position to offer

return to its investors very quickly and higher percentage return in respect to the investment

which will be through offering dividend, rise in the share price or both. For instance, a company

having the price earnings ratio of 15 means it is selling for 15 times of its income and in simple

and easy terms, the investors are in the position to pay £15 for every £1 of present or the coming

years income (JUŠKEVIČIŪTĖ, 2017). In case of mergers and acquisition, using the price

earnings ratio for valuation, it is considered to be very useful as it can be used in comparing the

ratio with the various different business entity in the same industry or even against the historical

values of the company. But this ratio can be easily manipulated by the company as per the

requirement suing the accounting practices.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

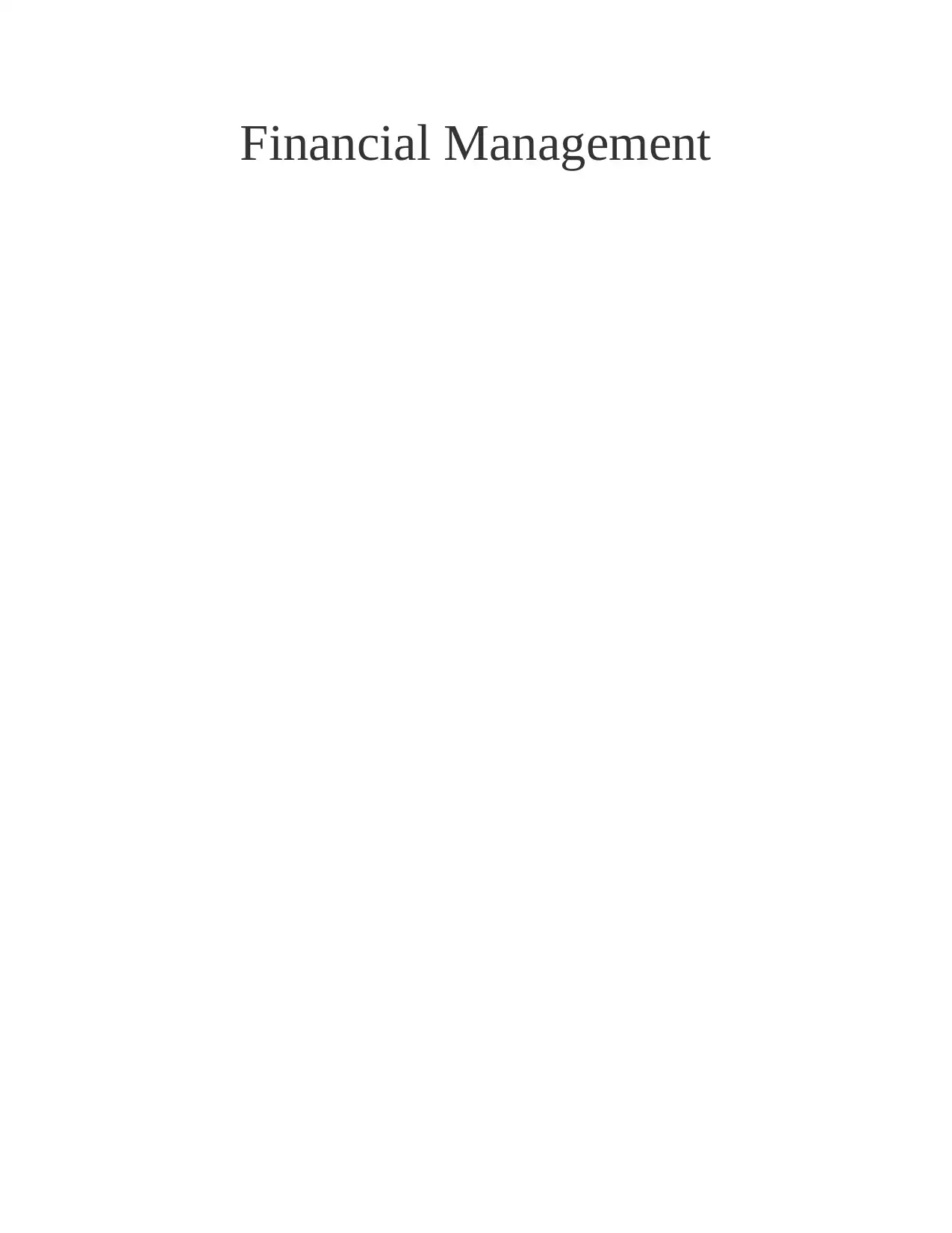

MPS £3.89

EPS £0.21

P/E ratio of Aztec (A) 18.52

Distributable earnings £40.4

number of shares 147

EPS of trojan (B) £0.27

Value per share of Trojan (A * B) £5.0004

Total market value £735.06

Statement showing valuation using price earnings ratio

As per the given case, the value of Trojan plc is £735.06 which is derived using the price

earning ratio. The market value is calculated by multiplying the number of shares with the per

share value of the Trojan plc.

b) Dividend valuation method

Under this valuation method, the dividend amount and the value of the stock is assumed

to be growing at the constant rate or in simple words, the dividend paid by the company will

grow at the constant percentage. This valuation method is mainly appropriate for the businesses

which increases their dividend by a fixed percentage every year. This method is very simple to

apply and is mainly suitable for the businesses with the stable growth along with the established

dividend pay-out ratios (Blanken, 2019). Investors can compare the businesses against the other

industries with the help of this model. Using this model, requires current dividend paid, the

expected rate of return and the growth rate. It actually establishes the relationship with these

three. Other than the above stated assumption, there are other assumptions as well, that is,

company’s growth is constant, financial leverage remains the same and the company’s free cash

flow is paid as the dividend.

EPS £0.21

P/E ratio of Aztec (A) 18.52

Distributable earnings £40.4

number of shares 147

EPS of trojan (B) £0.27

Value per share of Trojan (A * B) £5.0004

Total market value £735.06

Statement showing valuation using price earnings ratio

As per the given case, the value of Trojan plc is £735.06 which is derived using the price

earning ratio. The market value is calculated by multiplying the number of shares with the per

share value of the Trojan plc.

b) Dividend valuation method

Under this valuation method, the dividend amount and the value of the stock is assumed

to be growing at the constant rate or in simple words, the dividend paid by the company will

grow at the constant percentage. This valuation method is mainly appropriate for the businesses

which increases their dividend by a fixed percentage every year. This method is very simple to

apply and is mainly suitable for the businesses with the stable growth along with the established

dividend pay-out ratios (Blanken, 2019). Investors can compare the businesses against the other

industries with the help of this model. Using this model, requires current dividend paid, the

expected rate of return and the growth rate. It actually establishes the relationship with these

three. Other than the above stated assumption, there are other assumptions as well, that is,

company’s growth is constant, financial leverage remains the same and the company’s free cash

flow is paid as the dividend.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

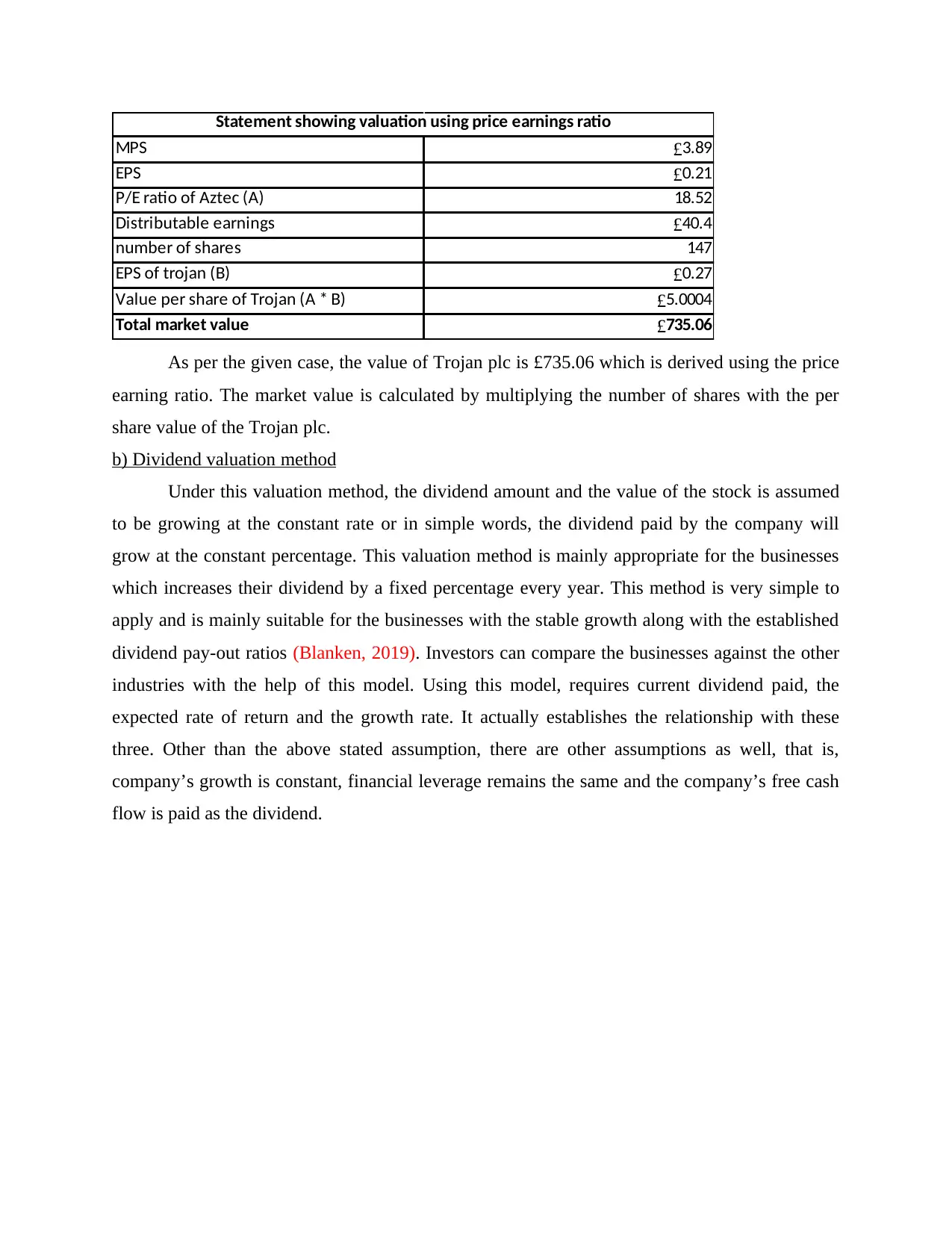

Current dividend (D) £0.13

Risk free rate of return (Rf) 5%

Return on the market (Rm) 11%

Beta (ß) 1.10%

As per CAPM, the required rate of return = Rf + (Rm-Rf) *ß

= 5% + (11% -5%) * 1.10%

Required rate of return (K) 5.07%

Growth rate 2%

Market price per share = D*(1+g) / (K-g)

= 0.13 * (1+2%) / (5.07% - 2%)

MPS £4.32

Total market value £635.04

Statement showing valuation using Dividend valuation method

The above statement depicts the valuation of the Trojan plc using dividend valuation

approach. Under this, the expected rate of return is determined using the CAPM formula and

then the dividend growth rate formula is implemented. The value of company under this is less

than the price earnings ratio valuation method.

c) Discounted cash flow method

This method is used for estimating the value of the company which is based in the cash

flows. This technique assists in evaluating the worth of the investment today and based on which

the projections are made in respect to the how much cash the company will generate in the

future. The companies mainly use WACC as the discounting rate. The DCF analysis is suitable

for any situation as the purpose remains the same that is the money invested today with the

expectation of receiving higher amount in the future (DRĂPGOI and et.al, 2016). The main

purpose of using this method is based on the ability of the business in generating and growing its

cash flow for its investors. Under mergers and acquisition, this approach is mainly useful for the

drive of determining the company’s worth by estimating the future cash flows over a certain

period of time. If it is carried out correctly, it is the most valuable method because it is forward

looking and depends less over the past data and is also less influenced by the external factors.

But it is very complex and requires deep understanding.

Risk free rate of return (Rf) 5%

Return on the market (Rm) 11%

Beta (ß) 1.10%

As per CAPM, the required rate of return = Rf + (Rm-Rf) *ß

= 5% + (11% -5%) * 1.10%

Required rate of return (K) 5.07%

Growth rate 2%

Market price per share = D*(1+g) / (K-g)

= 0.13 * (1+2%) / (5.07% - 2%)

MPS £4.32

Total market value £635.04

Statement showing valuation using Dividend valuation method

The above statement depicts the valuation of the Trojan plc using dividend valuation

approach. Under this, the expected rate of return is determined using the CAPM formula and

then the dividend growth rate formula is implemented. The value of company under this is less

than the price earnings ratio valuation method.

c) Discounted cash flow method

This method is used for estimating the value of the company which is based in the cash

flows. This technique assists in evaluating the worth of the investment today and based on which

the projections are made in respect to the how much cash the company will generate in the

future. The companies mainly use WACC as the discounting rate. The DCF analysis is suitable

for any situation as the purpose remains the same that is the money invested today with the

expectation of receiving higher amount in the future (DRĂPGOI and et.al, 2016). The main

purpose of using this method is based on the ability of the business in generating and growing its

cash flow for its investors. Under mergers and acquisition, this approach is mainly useful for the

drive of determining the company’s worth by estimating the future cash flows over a certain

period of time. If it is carried out correctly, it is the most valuable method because it is forward

looking and depends less over the past data and is also less influenced by the external factors.

But it is very complex and requires deep understanding.

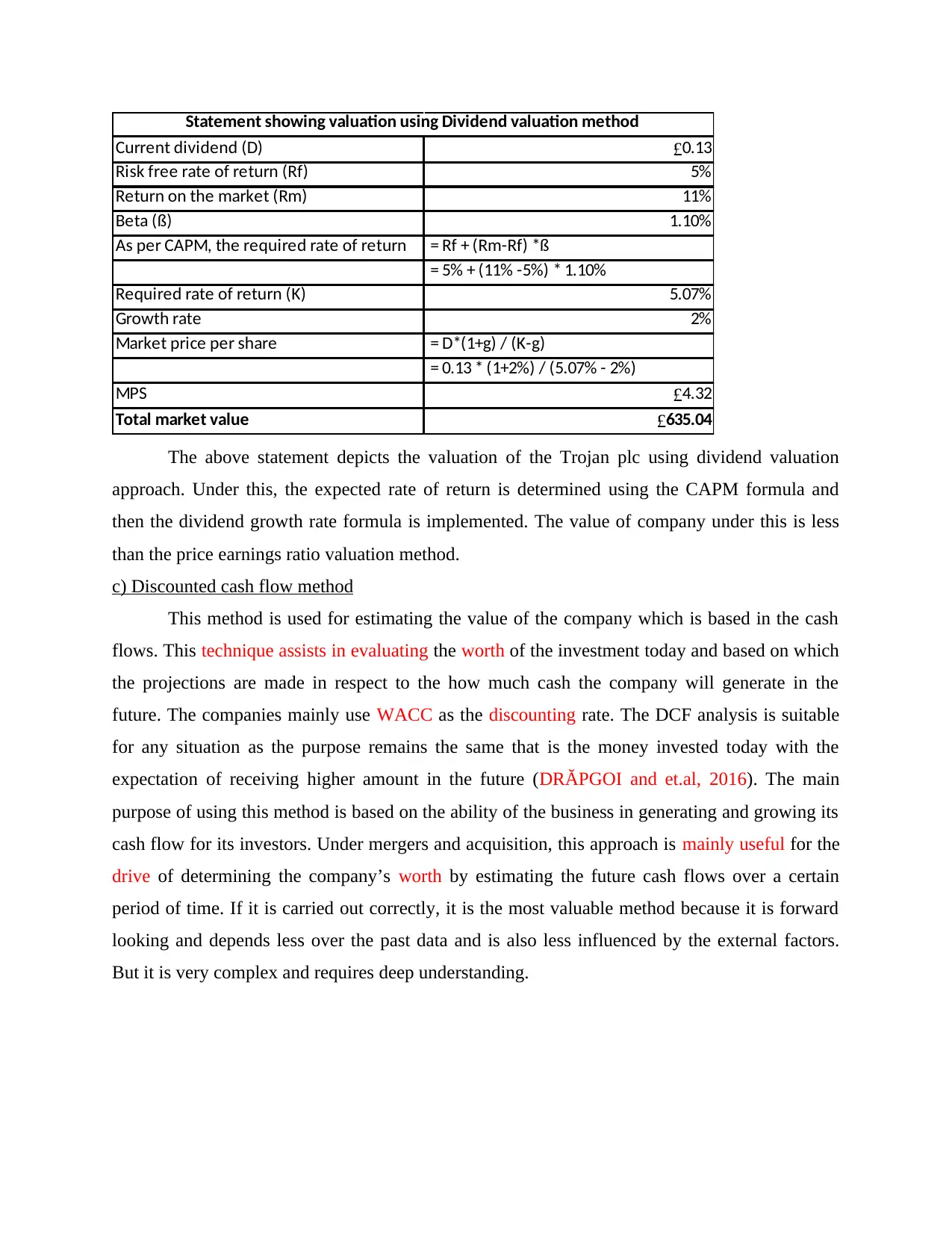

Discounted cash flow

Net operating profit £40.4

Add: depreciation 0

Add: change in working capital 0

Less: change in capital expenditure 0

Free cash flow £40.4

Discounting rate = WACC = 9%

PV of cash flow = Annual cash flow/discounting rate

Cash flow growth rate 2%

Market value per share = 40.4 / 9%

£448.89

Total market value £65986.67

Statement showing valuation using Discounted cash flow method

The above table, provides the calculation of the company’s value with the help of

discounted cash flow method. The value comes out to be £65986.83.

d. Critical review

Sivarajah and et.al. (2017) reviewed that price earning ratio represented as market price

of an entity's shares divided with that of its earnings value per share and is found as the widely

used multiple of earnings. It facilitates indication of the manner in which investors show

willingness in paying for company's earnings. As it has been reflected that earnings of firm

influenced towards varying extent through which an organization is been financed and in which

it pays for income tax, some analysts had turned towards different P/E ratio which removes an

effect of the firm's capital structure & income taxes on their earnings. However, this method

poses distortion impact on the returns of accounting guidelines and policy in context to

depreciation on intangible assets & amortization of the intangible assets, prefer for using price

earnings generated before charging interest, depreciation, amortization and taxes. This ratio

found as popular due to close relationship between EBITDA of corporation and its cash flow. It

requires positive value of accounting earnings, however, for the firms that operates at loss,

analyst need to find alternatives to the accounting earnings. The popular alternative is counted as

sales that results to determination of price to the sales ratio.

Moreover, Jacobs and et.al. (2018) stated that DDM is considered as the quantitative

method that is been used for forecasting price of an entity's stock on the basis of theory that its

current day price worth as sum of all the future payments of dividend when the discounted back

Net operating profit £40.4

Add: depreciation 0

Add: change in working capital 0

Less: change in capital expenditure 0

Free cash flow £40.4

Discounting rate = WACC = 9%

PV of cash flow = Annual cash flow/discounting rate

Cash flow growth rate 2%

Market value per share = 40.4 / 9%

£448.89

Total market value £65986.67

Statement showing valuation using Discounted cash flow method

The above table, provides the calculation of the company’s value with the help of

discounted cash flow method. The value comes out to be £65986.83.

d. Critical review

Sivarajah and et.al. (2017) reviewed that price earning ratio represented as market price

of an entity's shares divided with that of its earnings value per share and is found as the widely

used multiple of earnings. It facilitates indication of the manner in which investors show

willingness in paying for company's earnings. As it has been reflected that earnings of firm

influenced towards varying extent through which an organization is been financed and in which

it pays for income tax, some analysts had turned towards different P/E ratio which removes an

effect of the firm's capital structure & income taxes on their earnings. However, this method

poses distortion impact on the returns of accounting guidelines and policy in context to

depreciation on intangible assets & amortization of the intangible assets, prefer for using price

earnings generated before charging interest, depreciation, amortization and taxes. This ratio

found as popular due to close relationship between EBITDA of corporation and its cash flow. It

requires positive value of accounting earnings, however, for the firms that operates at loss,

analyst need to find alternatives to the accounting earnings. The popular alternative is counted as

sales that results to determination of price to the sales ratio.

Moreover, Jacobs and et.al. (2018) stated that DDM is considered as the quantitative

method that is been used for forecasting price of an entity's stock on the basis of theory that its

current day price worth as sum of all the future payments of dividend when the discounted back

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to its present value. This model is counted as very much conservative and does not need growth

assumptions for creating value. The growth rate of dividend for the stock being evaluated could

be higher that return rate. However, it only works on the stocks that pays dividends as some

small businesses does pay dividend which reflects that this model of valuation could not be used

for identifying their value. There are various factors which could influence stock valuation over

the time such as retention of customers, loyalty of brand and also intangible asset ownership has

potential for increasing company's value. Therefore, if growth rate of dividend is stable, such

type of non-dividend factors could change valuation of firm. This means valuation technique

when computed accurately, might not produce the desired results.

It has been reviewed by Kvassay, Rabcan and Rusnak (2017) that DCF models are been

premised on most of fundamental tenets under which value of firm equates to current value of

future related cash flows that is to be generated through an entity's operations, discounts at the

rate which depicts riskiness of such cash flows. This model facilitates an estimation of the firm's

total value on the basis of its free cash flows to firm discounting at WACC. On other state, DCF

valuation is seen as extremely sensitive towards the assumptions with regard to the perpetual

growth and discount rate (Qiao, Peng and Wang, 2017). This model works the best only in

those situations when there is high degree of the confidence regarding all the future cash flow,

but in case the firm's operations lacks its visibility, it became as difficult for predicting sales,

capital investment with the certainty and operating disbursements.

Thus, price to earning ratio is considered as most suitable technique for making valuation of the

shareholders funds and asset.

Question 3

a. Calculating capital budgeting tool

Particulars Amount

Asset cost £275,000

Useful life in years 6

Residual value at 15% from asset cost £41,250

Total depreciation £233,750

Year depreciation £38,958.33

assumptions for creating value. The growth rate of dividend for the stock being evaluated could

be higher that return rate. However, it only works on the stocks that pays dividends as some

small businesses does pay dividend which reflects that this model of valuation could not be used

for identifying their value. There are various factors which could influence stock valuation over

the time such as retention of customers, loyalty of brand and also intangible asset ownership has

potential for increasing company's value. Therefore, if growth rate of dividend is stable, such

type of non-dividend factors could change valuation of firm. This means valuation technique

when computed accurately, might not produce the desired results.

It has been reviewed by Kvassay, Rabcan and Rusnak (2017) that DCF models are been

premised on most of fundamental tenets under which value of firm equates to current value of

future related cash flows that is to be generated through an entity's operations, discounts at the

rate which depicts riskiness of such cash flows. This model facilitates an estimation of the firm's

total value on the basis of its free cash flows to firm discounting at WACC. On other state, DCF

valuation is seen as extremely sensitive towards the assumptions with regard to the perpetual

growth and discount rate (Qiao, Peng and Wang, 2017). This model works the best only in

those situations when there is high degree of the confidence regarding all the future cash flow,

but in case the firm's operations lacks its visibility, it became as difficult for predicting sales,

capital investment with the certainty and operating disbursements.

Thus, price to earning ratio is considered as most suitable technique for making valuation of the

shareholders funds and asset.

Question 3

a. Calculating capital budgeting tool

Particulars Amount

Asset cost £275,000

Useful life in years 6

Residual value at 15% from asset cost £41,250

Total depreciation £233,750

Year depreciation £38,958.33

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

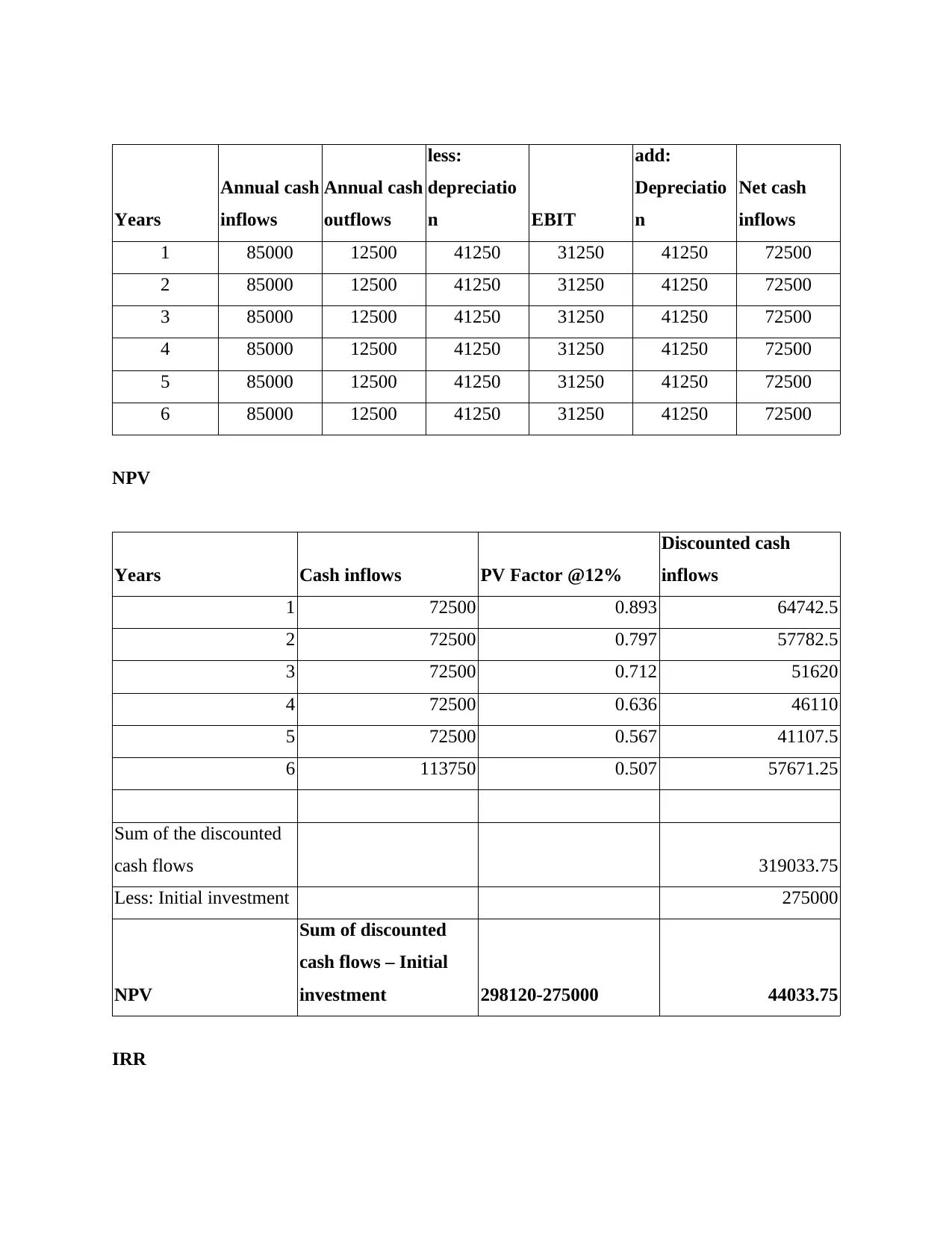

Years

Annual cash

inflows

Annual cash

outflows

less:

depreciatio

n EBIT

add:

Depreciatio

n

Net cash

inflows

1 85000 12500 41250 31250 41250 72500

2 85000 12500 41250 31250 41250 72500

3 85000 12500 41250 31250 41250 72500

4 85000 12500 41250 31250 41250 72500

5 85000 12500 41250 31250 41250 72500

6 85000 12500 41250 31250 41250 72500

NPV

Years Cash inflows PV Factor @12%

Discounted cash

inflows

1 72500 0.893 64742.5

2 72500 0.797 57782.5

3 72500 0.712 51620

4 72500 0.636 46110

5 72500 0.567 41107.5

6 113750 0.507 57671.25

Sum of the discounted

cash flows 319033.75

Less: Initial investment 275000

NPV

Sum of discounted

cash flows – Initial

investment 298120-275000 44033.75

IRR

Annual cash

inflows

Annual cash

outflows

less:

depreciatio

n EBIT

add:

Depreciatio

n

Net cash

inflows

1 85000 12500 41250 31250 41250 72500

2 85000 12500 41250 31250 41250 72500

3 85000 12500 41250 31250 41250 72500

4 85000 12500 41250 31250 41250 72500

5 85000 12500 41250 31250 41250 72500

6 85000 12500 41250 31250 41250 72500

NPV

Years Cash inflows PV Factor @12%

Discounted cash

inflows

1 72500 0.893 64742.5

2 72500 0.797 57782.5

3 72500 0.712 51620

4 72500 0.636 46110

5 72500 0.567 41107.5

6 113750 0.507 57671.25

Sum of the discounted

cash flows 319033.75

Less: Initial investment 275000

NPV

Sum of discounted

cash flows – Initial

investment 298120-275000 44033.75

IRR

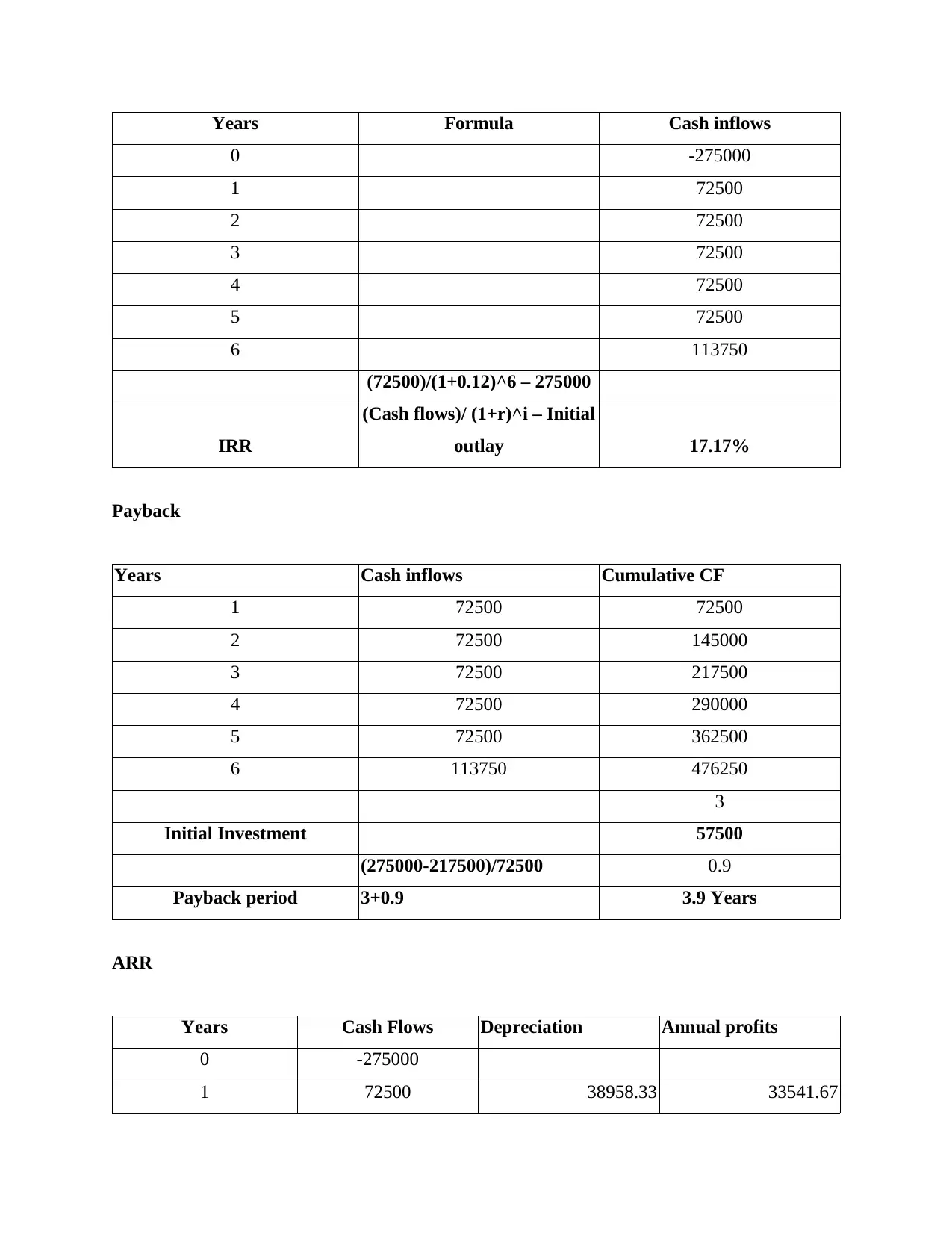

Years Formula Cash inflows

0 -275000

1 72500

2 72500

3 72500

4 72500

5 72500

6 113750

(72500)/(1+0.12)^6 – 275000

IRR

(Cash flows)/ (1+r)^i – Initial

outlay 17.17%

Payback

Years Cash inflows Cumulative CF

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 113750 476250

3

Initial Investment 57500

(275000-217500)/72500 0.9

Payback period 3+0.9 3.9 Years

ARR

Years Cash Flows Depreciation Annual profits

0 -275000

1 72500 38958.33 33541.67

0 -275000

1 72500

2 72500

3 72500

4 72500

5 72500

6 113750

(72500)/(1+0.12)^6 – 275000

IRR

(Cash flows)/ (1+r)^i – Initial

outlay 17.17%

Payback

Years Cash inflows Cumulative CF

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 113750 476250

3

Initial Investment 57500

(275000-217500)/72500 0.9

Payback period 3+0.9 3.9 Years

ARR

Years Cash Flows Depreciation Annual profits

0 -275000

1 72500 38958.33 33541.67

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

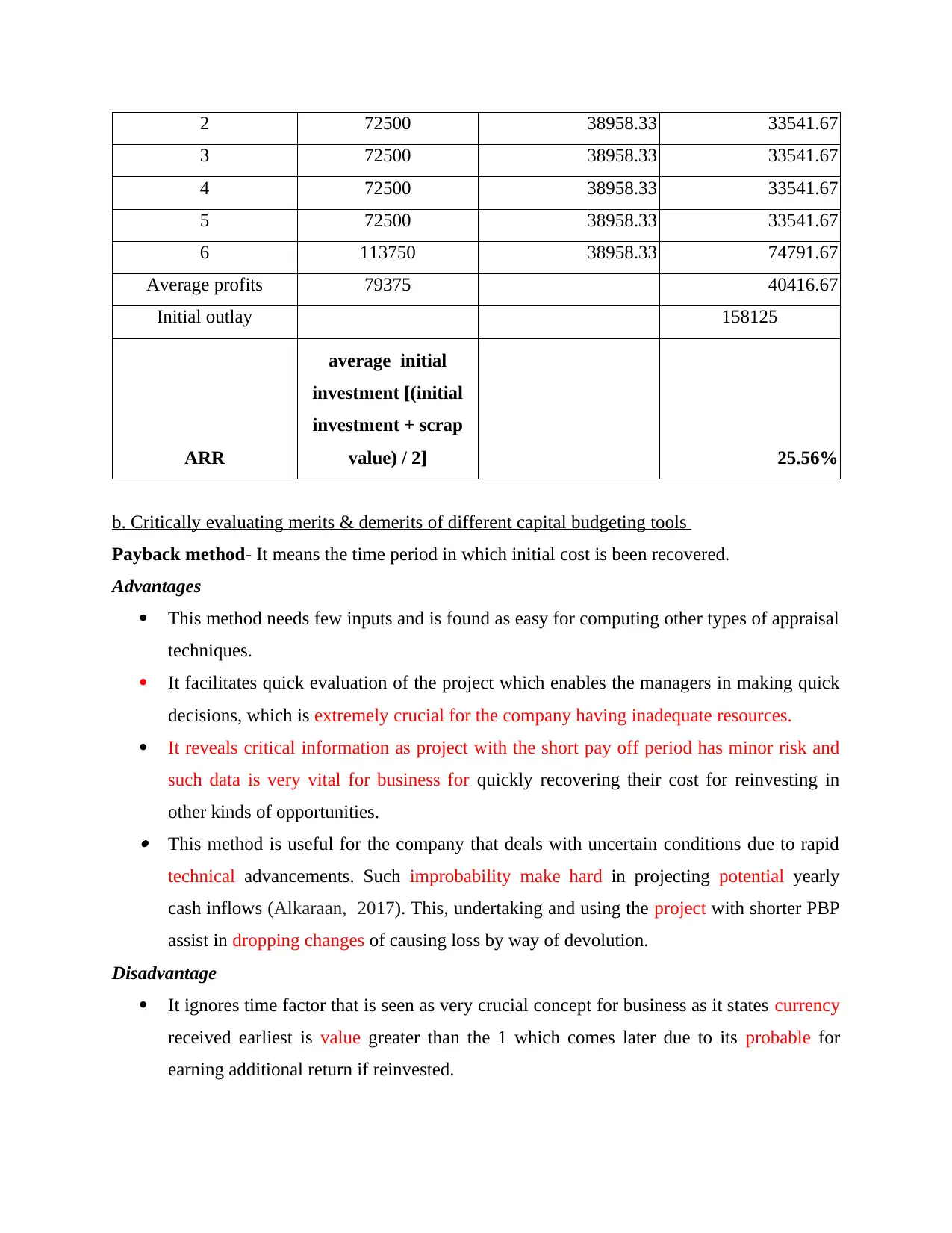

2 72500 38958.33 33541.67

3 72500 38958.33 33541.67

4 72500 38958.33 33541.67

5 72500 38958.33 33541.67

6 113750 38958.33 74791.67

Average profits 79375 40416.67

Initial outlay 158125

ARR

average initial

investment [(initial

investment + scrap

value) / 2] 25.56%

b. Critically evaluating merits & demerits of different capital budgeting tools

Payback method- It means the time period in which initial cost is been recovered.

Advantages

This method needs few inputs and is found as easy for computing other types of appraisal

techniques.

It facilitates quick evaluation of the project which enables the managers in making quick

decisions, which is extremely crucial for the company having inadequate resources.

It reveals critical information as project with the short pay off period has minor risk and

such data is very vital for business for quickly recovering their cost for reinvesting in

other kinds of opportunities. This method is useful for the company that deals with uncertain conditions due to rapid

technical advancements. Such improbability make hard in projecting potential yearly

cash inflows (Alkaraan, 2017). This, undertaking and using the project with shorter PBP

assist in dropping changes of causing loss by way of devolution.

Disadvantage

It ignores time factor that is seen as very crucial concept for business as it states currency

received earliest is value greater than the 1 which comes later due to its probable for

earning additional return if reinvested.

3 72500 38958.33 33541.67

4 72500 38958.33 33541.67

5 72500 38958.33 33541.67

6 113750 38958.33 74791.67

Average profits 79375 40416.67

Initial outlay 158125

ARR

average initial

investment [(initial

investment + scrap

value) / 2] 25.56%

b. Critically evaluating merits & demerits of different capital budgeting tools

Payback method- It means the time period in which initial cost is been recovered.

Advantages

This method needs few inputs and is found as easy for computing other types of appraisal

techniques.

It facilitates quick evaluation of the project which enables the managers in making quick

decisions, which is extremely crucial for the company having inadequate resources.

It reveals critical information as project with the short pay off period has minor risk and

such data is very vital for business for quickly recovering their cost for reinvesting in

other kinds of opportunities. This method is useful for the company that deals with uncertain conditions due to rapid

technical advancements. Such improbability make hard in projecting potential yearly

cash inflows (Alkaraan, 2017). This, undertaking and using the project with shorter PBP

assist in dropping changes of causing loss by way of devolution.

Disadvantage

It ignores time factor that is seen as very crucial concept for business as it states currency

received earliest is value greater than the 1 which comes later due to its probable for

earning additional return if reinvested.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This technique takes into account only those cash flows until time an initial cost is been

covered (Ayodele, 2019). It fails for taking into account cash flows that comes in

successive years; such narrow view of cash flows might force the company in overlook

the proposal that can generate productive cash flows in coming years.

This technique is simple that it does not consider the normal situations of business.

Usually, the capital investments are not considered as investment for one-time rather such

type of projects requires further amount of investments in future periods as well.

It does not guarantee that the proposal with shorter period would generate profits. If cash

flows from project stops at payback period, the proposed project would be resulted as

unviable after an ending of payback period.

ARR- It referred as the average return ascertained on the annual profits by dividing it by average

capital.

Advantages

This tool assists in making comparison of the new project with the proposals which are

deemed as cost-efficient or with the other kinds of projects which are competitive in the

nature.

This technique makes easier for understanding and computing payback period. It takes

into account savings or profits that occur over a period of proposal's entire financial span.

It presents a clear picture relating to project's profitability by dividing average annual

profits to that of initial outlay.

This technique creates the perspective of net return or earnings, that is profits after the

depreciation & payments (Babatunde, 2016).

ARR shows much more interest in return of its investments, therefore, it helps in

satisfying owner’s interest relating to their investment returns.

It takes into account accounting profit concept under which profits could be determined

through computing return rates. In this accounting profits could be easily computed with

help of the accounting records.

ARR is seen as extremely useful for the company to measure its current performance as it

takes an average of past as well as current years cash inflows with that of initial cost

(Higham, Fortune and Boothman, 2016).

covered (Ayodele, 2019). It fails for taking into account cash flows that comes in

successive years; such narrow view of cash flows might force the company in overlook

the proposal that can generate productive cash flows in coming years.

This technique is simple that it does not consider the normal situations of business.

Usually, the capital investments are not considered as investment for one-time rather such

type of projects requires further amount of investments in future periods as well.

It does not guarantee that the proposal with shorter period would generate profits. If cash

flows from project stops at payback period, the proposed project would be resulted as

unviable after an ending of payback period.

ARR- It referred as the average return ascertained on the annual profits by dividing it by average

capital.

Advantages

This tool assists in making comparison of the new project with the proposals which are

deemed as cost-efficient or with the other kinds of projects which are competitive in the

nature.

This technique makes easier for understanding and computing payback period. It takes

into account savings or profits that occur over a period of proposal's entire financial span.

It presents a clear picture relating to project's profitability by dividing average annual

profits to that of initial outlay.

This technique creates the perspective of net return or earnings, that is profits after the

depreciation & payments (Babatunde, 2016).

ARR shows much more interest in return of its investments, therefore, it helps in

satisfying owner’s interest relating to their investment returns.

It takes into account accounting profit concept under which profits could be determined

through computing return rates. In this accounting profits could be easily computed with

help of the accounting records.

ARR is seen as extremely useful for the company to measure its current performance as it

takes an average of past as well as current years cash inflows with that of initial cost

(Higham, Fortune and Boothman, 2016).

Under this the investments that has large span, the technique helps in computing simple

rate of return with that of true rate of return.

Disadvantages

This technique is known for ignoring the time aspect at the time of choosing alternative

use of fund.

It ignores the external factors which hinders profit earning capability of project into

account (Kolawole, 2016). This causes a limitation in earning higher amount or value of

the profits for an enterprise.

This tool creates problems in managerial decisions taking as under this people would be

arriving at the diverse results in case of ROI & ARR are computed separately.

ARR does not consider cash inflows into the consideration and is interested only in the

accounting profits.

Under this the projects cannot be appraised where instalments of an investment had been

made greater than two times in separate parts so it found unhelpful sometimes.

The life of multiple investments does not consider by method, however, while calculating

average income, investment lifetime are taken into consideration.

This technique overlooks a period that investments take for generating profits or earning

return as it ignores the time frame.

NPV- It states the difference between future & current value of an investment.

Advantages

NPV method is seen as easy for applying real business proposals in case cash flows &

discount rate are known very well.

This technique takes into account an impact of inflation on future project's return, thus

estimates time value of the money.

In NPV, rate of price cut could be accustomed as per the risk existing in industry, along

several other factors for obtaining adequate output.

It helps in determining value of investment as under NPV, earnings throughout the life of

project could be acquired, that facilitates the firm in knowing future value of particular

investment.

rate of return with that of true rate of return.

Disadvantages

This technique is known for ignoring the time aspect at the time of choosing alternative

use of fund.

It ignores the external factors which hinders profit earning capability of project into

account (Kolawole, 2016). This causes a limitation in earning higher amount or value of

the profits for an enterprise.

This tool creates problems in managerial decisions taking as under this people would be

arriving at the diverse results in case of ROI & ARR are computed separately.

ARR does not consider cash inflows into the consideration and is interested only in the

accounting profits.

Under this the projects cannot be appraised where instalments of an investment had been

made greater than two times in separate parts so it found unhelpful sometimes.

The life of multiple investments does not consider by method, however, while calculating

average income, investment lifetime are taken into consideration.

This technique overlooks a period that investments take for generating profits or earning

return as it ignores the time frame.

NPV- It states the difference between future & current value of an investment.

Advantages

NPV method is seen as easy for applying real business proposals in case cash flows &

discount rate are known very well.

This technique takes into account an impact of inflation on future project's return, thus

estimates time value of the money.

In NPV, rate of price cut could be accustomed as per the risk existing in industry, along

several other factors for obtaining adequate output.

It helps in determining value of investment as under NPV, earnings throughout the life of

project could be acquired, that facilitates the firm in knowing future value of particular

investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.