Financial Management: Decision Making and Sustainability Report

VerifiedAdded on 2023/01/12

|10

|2380

|36

Report

AI Summary

This report delves into the core principles of financial management, examining the critical role of decision-making in ensuring a business's sustainability. The report begins by evaluating various approaches, techniques, and factors that contribute to effective organizational decision-making, followed by a discussion on stakeholder management and the resolution of conflicting interests. It then explores the application of management accounting techniques for cost control and maximizing shareholder value, along with methods for fraud detection and ethical decision-making. The second part of the report analyzes the data used for operational and strategic decisions, investment appraisal techniques, and their effectiveness in maximizing returns. It further examines the value of financial decision-making techniques and strategies that support long-term financial sustainability, including the role of management accounting in improving financial performance. The report utilizes financial ratios to assess liquidity, efficiency, profitability, and debt management, providing insights into a company's financial health and its ability to meet its short-term and long-term obligations. The analysis includes real-world examples and financial statements to illustrate key concepts and provide practical applications for financial management.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

SCENARIO 1..................................................................................................................................1

1. Evaluation of the range of approaches, techniques and factors contributing to effective

decision making in organisation..................................................................................................1

2. Stakeholder management and management of conflicting of the stakeholder groups............3

3. Management accounting techniques in cost control and maximising the shareholder value.. 3

4. Techniques for fraud detection and prevention and approach for ethical decision making....4

SCENARIO 2..................................................................................................................................5

1. Data obtained for making operational and strategic decisions................................................5

2. Investment appraisal techniques and their effectiveness for maximising the returns over

investments..................................................................................................................................6

3. Value of techniques used in financial decision making...........................................................7

4. Financial decision making to support the long term sustainability.........................................7

5. Management accounting for improving the financial sustainability.....................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

TABLE OF CONTENTS................................................................................................................2

INTRODUCTION...........................................................................................................................1

SCENARIO 1..................................................................................................................................1

1. Evaluation of the range of approaches, techniques and factors contributing to effective

decision making in organisation..................................................................................................1

2. Stakeholder management and management of conflicting of the stakeholder groups............3

3. Management accounting techniques in cost control and maximising the shareholder value.. 3

4. Techniques for fraud detection and prevention and approach for ethical decision making....4

SCENARIO 2..................................................................................................................................5

1. Data obtained for making operational and strategic decisions................................................5

2. Investment appraisal techniques and their effectiveness for maximising the returns over

investments..................................................................................................................................6

3. Value of techniques used in financial decision making...........................................................7

4. Financial decision making to support the long term sustainability.........................................7

5. Management accounting for improving the financial sustainability.....................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial management refers to managing th financial operation of the business. It is very

important for the business to have a well defined financial structured to be followed by the

organisation. Present report cover the role of business decision making in the financial

management. It will enhance the understanding about the financial management and

effectiveness of decision making for sustainability of business.

SCENARIO 1

1. Evaluation of the range of approaches, techniques and factors contributing to effective

(Covered in PPT)

2. Stakeholder management and management of conflicting of the stakeholder groups.

(Covered in PPT)

3. Management accounting techniques in cost control and maximising the shareholder value.

(Covered in PPT)

4. Techniques for fraud detection and prevention and approach for ethical decision making

(Covered in PPT)

.

SCENARIO 2

1. Data obtained for making operational and strategic decisions.

Data obtained by the company is used for the operational decision making. Analysis

provides about the internal operation of business. They state the financial position in market and

its wealth. The results of the prior decision of the management could be reflected in the financial

statements of the company. Its profitability, liquidity, efficiency and capital structure could be

assessed from the financial statements of company. After analysing the business operation

manages take strategic decisions for improving its performance. Company reframe its strategies

that do not give positive results and also take measures for increasing its operational efficiency.

Comparison of the performance of the business is done with its competitors which provides the

managers about their standing. Managers adopt strategies for increasing their revenues and take

1

Financial management refers to managing th financial operation of the business. It is very

important for the business to have a well defined financial structured to be followed by the

organisation. Present report cover the role of business decision making in the financial

management. It will enhance the understanding about the financial management and

effectiveness of decision making for sustainability of business.

SCENARIO 1

1. Evaluation of the range of approaches, techniques and factors contributing to effective

(Covered in PPT)

2. Stakeholder management and management of conflicting of the stakeholder groups.

(Covered in PPT)

3. Management accounting techniques in cost control and maximising the shareholder value.

(Covered in PPT)

4. Techniques for fraud detection and prevention and approach for ethical decision making

(Covered in PPT)

.

SCENARIO 2

1. Data obtained for making operational and strategic decisions.

Data obtained by the company is used for the operational decision making. Analysis

provides about the internal operation of business. They state the financial position in market and

its wealth. The results of the prior decision of the management could be reflected in the financial

statements of the company. Its profitability, liquidity, efficiency and capital structure could be

assessed from the financial statements of company. After analysing the business operation

manages take strategic decisions for improving its performance. Company reframe its strategies

that do not give positive results and also take measures for increasing its operational efficiency.

Comparison of the performance of the business is done with its competitors which provides the

managers about their standing. Managers adopt strategies for increasing their revenues and take

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

corrective steps for keeping its costs under control. An appropriate mix of debts and equity

should be there for having minimum cost of capital.

2. Investment appraisal techniques and their effectiveness for maximising the returns over

investments.

Investment appraisal techniques refer to the techniques that help the manager in making

correct and accurate decisions. These investment appraisal techniques help the managers in

identifying the viability or feasibility of proposed investments to be made. It includes various

techniques such as NPV, ARR and payback period.

Net Present Value

Net present value is the investment appraisal techniques used by the experts and analysts

for identifying the viability of the propose investment. It identified whether the present value of

future cash flows generated are sufficient for recovering the cost of its project. Projectg is

considered to be profitable when the NPV is positive. This technique considers time value of

money which is not considered in other technique. However, it is difficult to determine the

discounting factor. After identifying the present values it could take decisions that maximises its

wealth.

Accounting Rate of Return.

Accounting rate is also the financial ratio used in identifying the profitability of

investments it is used for identifying the return from investments in terms of percentage.

Accounting rate of return focuses over the accounting profits of project. Profits are considered in

the cash flows generated by the project (Yermack 2017). If the return rate is not high project is

not accepted by the company and where with adequate returns is accepted. Unlike NPV this

approach do not consider time value of money. This helps in assessing the returns so that steps

and strategies for improving the cash flows could be taken for maximising the returns.

Payback period

It is an investment appraisal technique used by organisations to assess the feasibility of

investments. Payback period is concerned with identifying the time that will be taken by

investments to recover its cost of initial investments. It is the measure of breakeven point where

it will be meeting its costs. Project with shorter payback are considered profitable as after this it

will start to generate profit after recovering its costs. Using this investment techniques

2

should be there for having minimum cost of capital.

2. Investment appraisal techniques and their effectiveness for maximising the returns over

investments.

Investment appraisal techniques refer to the techniques that help the manager in making

correct and accurate decisions. These investment appraisal techniques help the managers in

identifying the viability or feasibility of proposed investments to be made. It includes various

techniques such as NPV, ARR and payback period.

Net Present Value

Net present value is the investment appraisal techniques used by the experts and analysts

for identifying the viability of the propose investment. It identified whether the present value of

future cash flows generated are sufficient for recovering the cost of its project. Projectg is

considered to be profitable when the NPV is positive. This technique considers time value of

money which is not considered in other technique. However, it is difficult to determine the

discounting factor. After identifying the present values it could take decisions that maximises its

wealth.

Accounting Rate of Return.

Accounting rate is also the financial ratio used in identifying the profitability of

investments it is used for identifying the return from investments in terms of percentage.

Accounting rate of return focuses over the accounting profits of project. Profits are considered in

the cash flows generated by the project (Yermack 2017). If the return rate is not high project is

not accepted by the company and where with adequate returns is accepted. Unlike NPV this

approach do not consider time value of money. This helps in assessing the returns so that steps

and strategies for improving the cash flows could be taken for maximising the returns.

Payback period

It is an investment appraisal technique used by organisations to assess the feasibility of

investments. Payback period is concerned with identifying the time that will be taken by

investments to recover its cost of initial investments. It is the measure of breakeven point where

it will be meeting its costs. Project with shorter payback are considered profitable as after this it

will start to generate profit after recovering its costs. Using this investment techniques

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management of the company aims at reducing the payback period so that profits could be earned

as early as possible.

3. Value of techniques used in financial decision making.

Balance sheet –

It is one of the financial statements that provides information about the financial position

of company. A balances sheet consists of all the details about the assets and liabilities of the

company. It provides about the capital structure of company and financial risks associated with

the business (Martin, 2016). Using the information provided by balance sheet decisions related

the investments could be taken and for improving the financial structures. Important operational

decisions to increase the efficiency and liquidity are taken by the company with appropriated

measures.

Cash flows-

It is a financial statement that represents the inflows and outflows of cash. This is

prepared by the organisation giving information about the liquidity position of company. it could

be identified using these statement where the cash is deployed and the sources from where the

cash is raised. Management take effective strategic decisions for improving the liquidity position

of the company using this statement (BarR and McClellan, 2018). It is s highly used in financial

decision making by the managements as decisions are to be taken analysing the liquidity position

of the company.

Break even analysis –

It is a tool used in decision making by the managers for deciding their production

activities and related financial decisions. It is a metrics used for analysing the point at which the

product will meet its costs (Atmadja and Saputra, 2018). An appropriate sales mix is determined

for determining th level of sales company is required to achieve for achieving the required rate of

returns. It is used by the business management for making decisions related to the strategies to

achieve the goals and objectives of business.

4. Financial decision making to support the long term sustainability.

Persimmon plc

2018 2017

Liquidity ratio

3

as early as possible.

3. Value of techniques used in financial decision making.

Balance sheet –

It is one of the financial statements that provides information about the financial position

of company. A balances sheet consists of all the details about the assets and liabilities of the

company. It provides about the capital structure of company and financial risks associated with

the business (Martin, 2016). Using the information provided by balance sheet decisions related

the investments could be taken and for improving the financial structures. Important operational

decisions to increase the efficiency and liquidity are taken by the company with appropriated

measures.

Cash flows-

It is a financial statement that represents the inflows and outflows of cash. This is

prepared by the organisation giving information about the liquidity position of company. it could

be identified using these statement where the cash is deployed and the sources from where the

cash is raised. Management take effective strategic decisions for improving the liquidity position

of the company using this statement (BarR and McClellan, 2018). It is s highly used in financial

decision making by the managements as decisions are to be taken analysing the liquidity position

of the company.

Break even analysis –

It is a tool used in decision making by the managers for deciding their production

activities and related financial decisions. It is a metrics used for analysing the point at which the

product will meet its costs (Atmadja and Saputra, 2018). An appropriate sales mix is determined

for determining th level of sales company is required to achieve for achieving the required rate of

returns. It is used by the business management for making decisions related to the strategies to

achieve the goals and objectives of business.

4. Financial decision making to support the long term sustainability.

Persimmon plc

2018 2017

Liquidity ratio

3

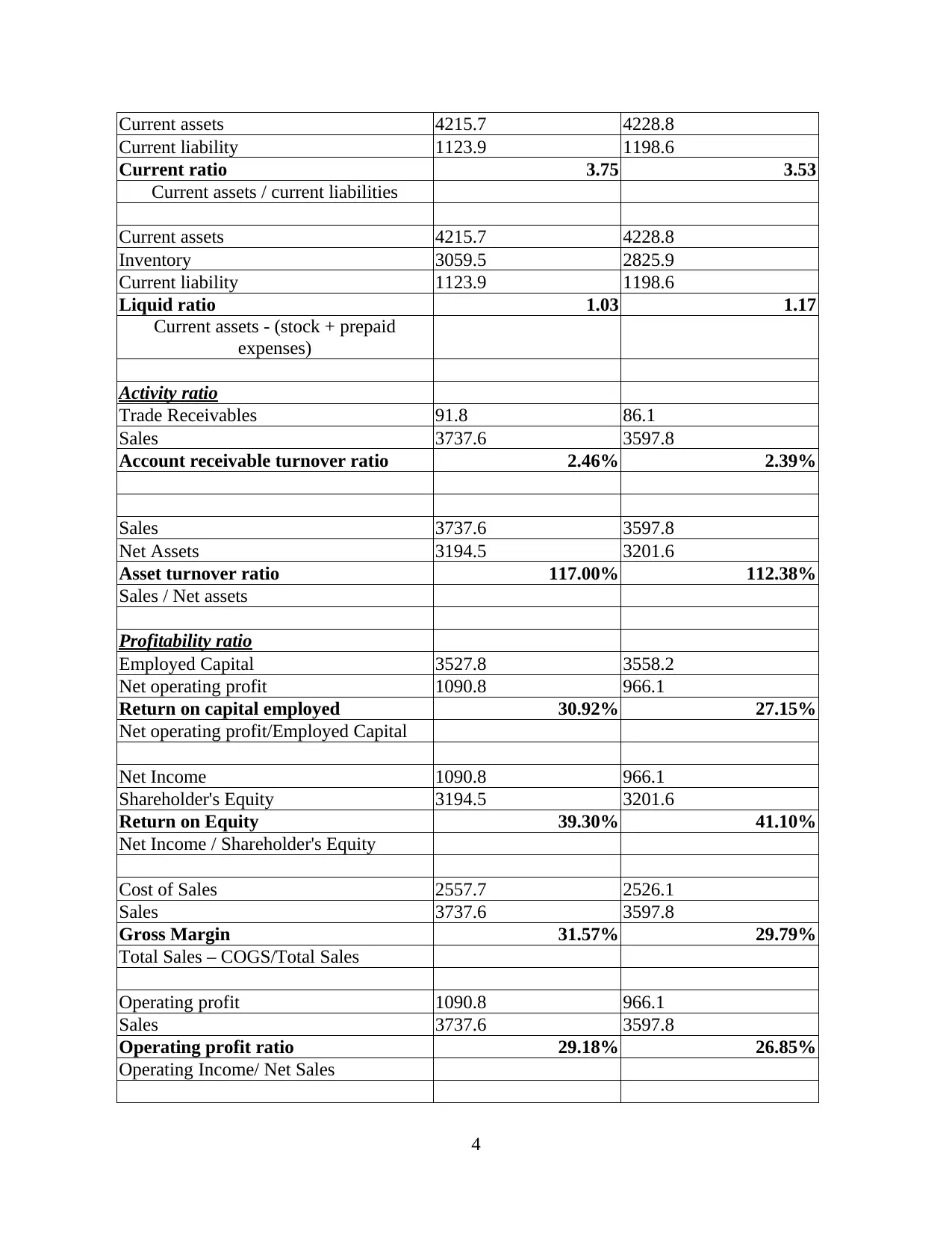

Current assets 4215.7 4228.8

Current liability 1123.9 1198.6

Current ratio 3.75 3.53

Current assets / current liabilities

Current assets 4215.7 4228.8

Inventory 3059.5 2825.9

Current liability 1123.9 1198.6

Liquid ratio 1.03 1.17

Current assets - (stock + prepaid

expenses)

Activity ratio

Trade Receivables 91.8 86.1

Sales 3737.6 3597.8

Account receivable turnover ratio 2.46% 2.39%

Sales 3737.6 3597.8

Net Assets 3194.5 3201.6

Asset turnover ratio 117.00% 112.38%

Sales / Net assets

Profitability ratio

Employed Capital 3527.8 3558.2

Net operating profit 1090.8 966.1

Return on capital employed 30.92% 27.15%

Net operating profit/Employed Capital

Net Income 1090.8 966.1

Shareholder's Equity 3194.5 3201.6

Return on Equity 39.30% 41.10%

Net Income / Shareholder's Equity

Cost of Sales 2557.7 2526.1

Sales 3737.6 3597.8

Gross Margin 31.57% 29.79%

Total Sales – COGS/Total Sales

Operating profit 1090.8 966.1

Sales 3737.6 3597.8

Operating profit ratio 29.18% 26.85%

Operating Income/ Net Sales

4

Current liability 1123.9 1198.6

Current ratio 3.75 3.53

Current assets / current liabilities

Current assets 4215.7 4228.8

Inventory 3059.5 2825.9

Current liability 1123.9 1198.6

Liquid ratio 1.03 1.17

Current assets - (stock + prepaid

expenses)

Activity ratio

Trade Receivables 91.8 86.1

Sales 3737.6 3597.8

Account receivable turnover ratio 2.46% 2.39%

Sales 3737.6 3597.8

Net Assets 3194.5 3201.6

Asset turnover ratio 117.00% 112.38%

Sales / Net assets

Profitability ratio

Employed Capital 3527.8 3558.2

Net operating profit 1090.8 966.1

Return on capital employed 30.92% 27.15%

Net operating profit/Employed Capital

Net Income 1090.8 966.1

Shareholder's Equity 3194.5 3201.6

Return on Equity 39.30% 41.10%

Net Income / Shareholder's Equity

Cost of Sales 2557.7 2526.1

Sales 3737.6 3597.8

Gross Margin 31.57% 29.79%

Total Sales – COGS/Total Sales

Operating profit 1090.8 966.1

Sales 3737.6 3597.8

Operating profit ratio 29.18% 26.85%

Operating Income/ Net Sales

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

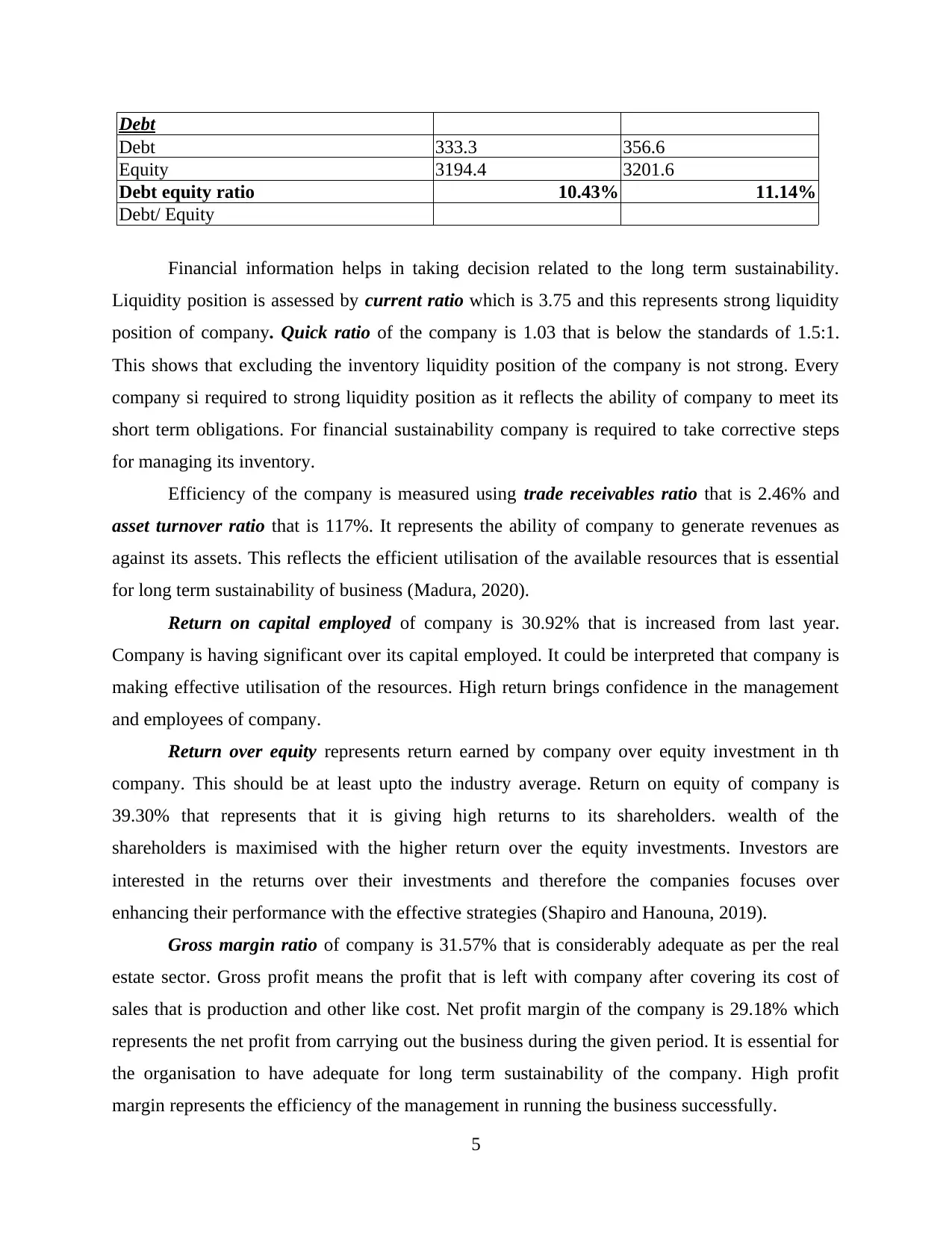

Debt

Debt 333.3 356.6

Equity 3194.4 3201.6

Debt equity ratio 10.43% 11.14%

Debt/ Equity

Financial information helps in taking decision related to the long term sustainability.

Liquidity position is assessed by current ratio which is 3.75 and this represents strong liquidity

position of company. Quick ratio of the company is 1.03 that is below the standards of 1.5:1.

This shows that excluding the inventory liquidity position of the company is not strong. Every

company si required to strong liquidity position as it reflects the ability of company to meet its

short term obligations. For financial sustainability company is required to take corrective steps

for managing its inventory.

Efficiency of the company is measured using trade receivables ratio that is 2.46% and

asset turnover ratio that is 117%. It represents the ability of company to generate revenues as

against its assets. This reflects the efficient utilisation of the available resources that is essential

for long term sustainability of business (Madura, 2020).

Return on capital employed of company is 30.92% that is increased from last year.

Company is having significant over its capital employed. It could be interpreted that company is

making effective utilisation of the resources. High return brings confidence in the management

and employees of company.

Return over equity represents return earned by company over equity investment in th

company. This should be at least upto the industry average. Return on equity of company is

39.30% that represents that it is giving high returns to its shareholders. wealth of the

shareholders is maximised with the higher return over the equity investments. Investors are

interested in the returns over their investments and therefore the companies focuses over

enhancing their performance with the effective strategies (Shapiro and Hanouna, 2019).

Gross margin ratio of company is 31.57% that is considerably adequate as per the real

estate sector. Gross profit means the profit that is left with company after covering its cost of

sales that is production and other like cost. Net profit margin of the company is 29.18% which

represents the net profit from carrying out the business during the given period. It is essential for

the organisation to have adequate for long term sustainability of the company. High profit

margin represents the efficiency of the management in running the business successfully.

5

Debt 333.3 356.6

Equity 3194.4 3201.6

Debt equity ratio 10.43% 11.14%

Debt/ Equity

Financial information helps in taking decision related to the long term sustainability.

Liquidity position is assessed by current ratio which is 3.75 and this represents strong liquidity

position of company. Quick ratio of the company is 1.03 that is below the standards of 1.5:1.

This shows that excluding the inventory liquidity position of the company is not strong. Every

company si required to strong liquidity position as it reflects the ability of company to meet its

short term obligations. For financial sustainability company is required to take corrective steps

for managing its inventory.

Efficiency of the company is measured using trade receivables ratio that is 2.46% and

asset turnover ratio that is 117%. It represents the ability of company to generate revenues as

against its assets. This reflects the efficient utilisation of the available resources that is essential

for long term sustainability of business (Madura, 2020).

Return on capital employed of company is 30.92% that is increased from last year.

Company is having significant over its capital employed. It could be interpreted that company is

making effective utilisation of the resources. High return brings confidence in the management

and employees of company.

Return over equity represents return earned by company over equity investment in th

company. This should be at least upto the industry average. Return on equity of company is

39.30% that represents that it is giving high returns to its shareholders. wealth of the

shareholders is maximised with the higher return over the equity investments. Investors are

interested in the returns over their investments and therefore the companies focuses over

enhancing their performance with the effective strategies (Shapiro and Hanouna, 2019).

Gross margin ratio of company is 31.57% that is considerably adequate as per the real

estate sector. Gross profit means the profit that is left with company after covering its cost of

sales that is production and other like cost. Net profit margin of the company is 29.18% which

represents the net profit from carrying out the business during the given period. It is essential for

the organisation to have adequate for long term sustainability of the company. High profit

margin represents the efficiency of the management in running the business successfully.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Debt Equity ratio is 10.43% that against the equity company is having 10 percent of debt.

Capital structure of the company is adequate with proper mix of debt and equity. It shows the

financial risks associated with the business (Atmadja and Saputra, 2018). High financial risks

affect the sustainability of company therefore it should strive for reducing the financial risks.

5. Management accounting for improving the financial sustainability.

Management accounting is quite necessary for the financial sustainability because it

helps a business to take better decision for the company which incorporates with the economic,

environmental and social components. Also, many government and regulatory bodies are also

tightening the relevant rules and regulations in order to become a socially responsible. Also, if

the organization have effective management accounting system then it will definitely assist to

enhance the overall performance of the company and also develop further growth options as well

(Căpușneanu and et.al., 2020). On the other side, globalization and technological development

and rapid population growth are sometimes cause fundamental change in the business world.

Therefore, it is also analyzed that through management accounting tools and techniques,

the company will easily manage the work and improve its financial performance as well. It is so

because it is not easy to perform the work manually and keep in mind all the expenses, that is

why, it is quite necessary to use management accounting and its standard principles that will

assist to raise the brand image of company and improve its financial performance as well (Jones

And et.al., 2018). In addition to this, most of the top leaders and managers also uses the

management accounting in their companies so that they will easily determine the actual

performance of the company and also make decisions accordingly. So, to minimize the issue and

difficulties, it is quite necessary for the company to take decisions accordingly and implement

management accounting tool and techniques as well.

CONCLUSION

From the above report it is concluded that financial management is very essential for

business. Companies for making informed business decisions are required to have knowledge of

the various financial management concepts. Decision making is very important task to be

performed by the management therefore it should be taken after analysing all the facts and

figures.

6

Capital structure of the company is adequate with proper mix of debt and equity. It shows the

financial risks associated with the business (Atmadja and Saputra, 2018). High financial risks

affect the sustainability of company therefore it should strive for reducing the financial risks.

5. Management accounting for improving the financial sustainability.

Management accounting is quite necessary for the financial sustainability because it

helps a business to take better decision for the company which incorporates with the economic,

environmental and social components. Also, many government and regulatory bodies are also

tightening the relevant rules and regulations in order to become a socially responsible. Also, if

the organization have effective management accounting system then it will definitely assist to

enhance the overall performance of the company and also develop further growth options as well

(Căpușneanu and et.al., 2020). On the other side, globalization and technological development

and rapid population growth are sometimes cause fundamental change in the business world.

Therefore, it is also analyzed that through management accounting tools and techniques,

the company will easily manage the work and improve its financial performance as well. It is so

because it is not easy to perform the work manually and keep in mind all the expenses, that is

why, it is quite necessary to use management accounting and its standard principles that will

assist to raise the brand image of company and improve its financial performance as well (Jones

And et.al., 2018). In addition to this, most of the top leaders and managers also uses the

management accounting in their companies so that they will easily determine the actual

performance of the company and also make decisions accordingly. So, to minimize the issue and

difficulties, it is quite necessary for the company to take decisions accordingly and implement

management accounting tool and techniques as well.

CONCLUSION

From the above report it is concluded that financial management is very essential for

business. Companies for making informed business decisions are required to have knowledge of

the various financial management concepts. Decision making is very important task to be

performed by the management therefore it should be taken after analysing all the facts and

figures.

6

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Căpușneanu, S. and et.al.,2020. Management Accounting in the Digital Economy: Evolution and

Perspectives. In Improving Business Performance Through Innovation in the Digital

Economy (pp. 156-176).IGI Global.

Shapiro, A.C. and Hanouna, P., 2019. Multinational financial management. Wiley.

Madura, J., 2020. International financial management. Cengage Learning.

Jones, C. And et.al., 2018. Financial Management for Nurse Managers and Executives-E-Book.

Elsevier Health Sciences.

Barr, M.J. and McClellan, G.S., 2018. Budgets and financial management in higher education.

John Wiley & Sons.

Martin, L.L., 2016. Financial management for human service administrators. Waveland Press.

Yermack, D., 2017. Donor governance and financial management in prominent US art

museums. Journal of Cultural Economics.41(3). pp.215-235.

Matthew, B.T., 2016. Financial management in the sport industry. Taylor & Francis.

Atmadja, A.T. and Saputra, K.A.K., 2018. Determinant factors influencing the accountability of

village financial management. Academy of Strategic Management Journal.

8

Books and Journals

Căpușneanu, S. and et.al.,2020. Management Accounting in the Digital Economy: Evolution and

Perspectives. In Improving Business Performance Through Innovation in the Digital

Economy (pp. 156-176).IGI Global.

Shapiro, A.C. and Hanouna, P., 2019. Multinational financial management. Wiley.

Madura, J., 2020. International financial management. Cengage Learning.

Jones, C. And et.al., 2018. Financial Management for Nurse Managers and Executives-E-Book.

Elsevier Health Sciences.

Barr, M.J. and McClellan, G.S., 2018. Budgets and financial management in higher education.

John Wiley & Sons.

Martin, L.L., 2016. Financial management for human service administrators. Waveland Press.

Yermack, D., 2017. Donor governance and financial management in prominent US art

museums. Journal of Cultural Economics.41(3). pp.215-235.

Matthew, B.T., 2016. Financial management in the sport industry. Taylor & Francis.

Atmadja, A.T. and Saputra, K.A.K., 2018. Determinant factors influencing the accountability of

village financial management. Academy of Strategic Management Journal.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.