Financial Management Report: Budgeting, Variance and Recommendations

VerifiedAdded on 2021/02/20

|10

|1430

|325

Report

AI Summary

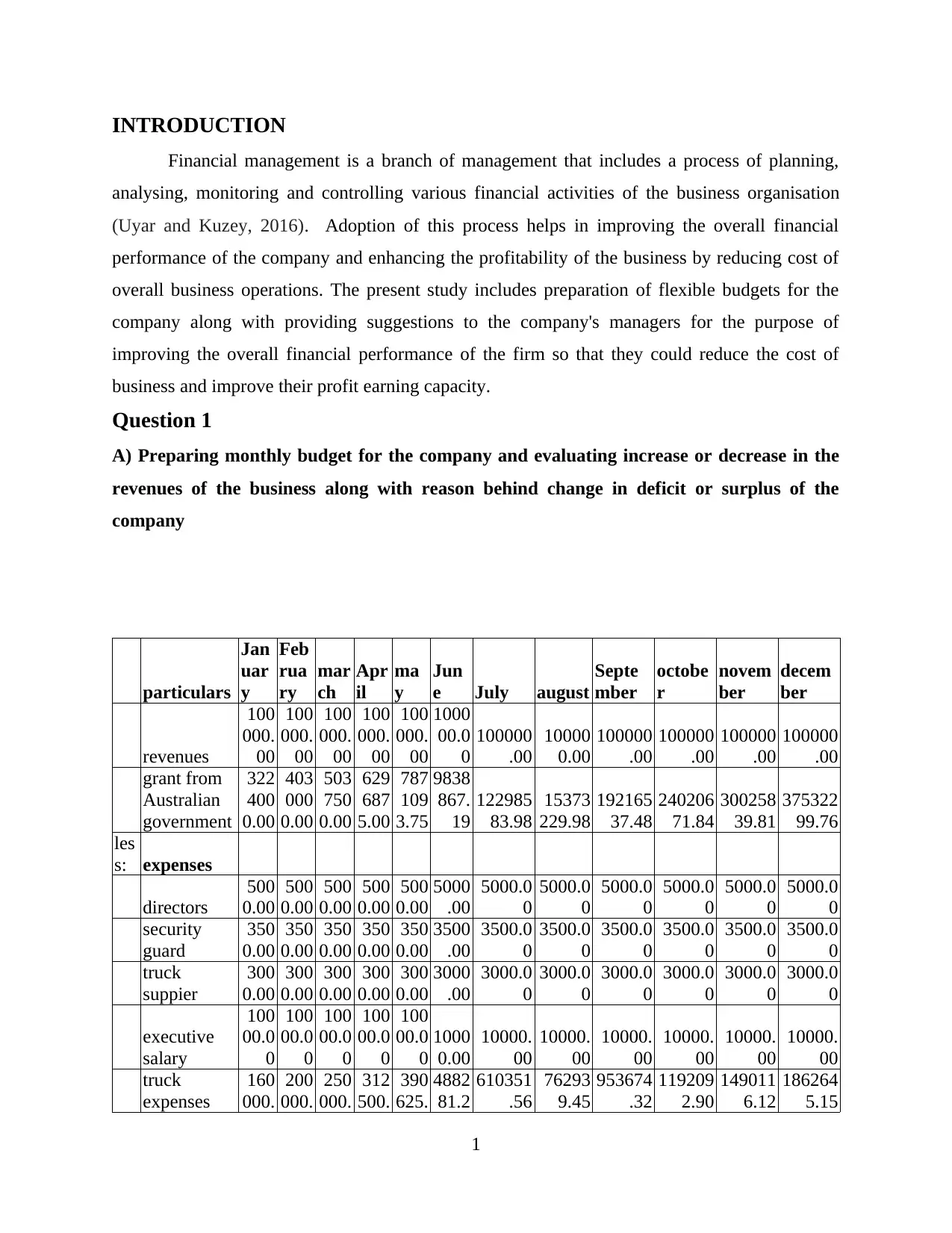

This financial management report provides an in-depth analysis of a company's financial performance, focusing on budgeting and variance analysis. The report begins with the preparation of a monthly budget, comparing revenues and expenses to determine the company's financial position. It then moves on to creating flexible budgets for different consultant scenarios, recommending appropriate fees to maximize profit. A key component of the report is the variance analysis, which compares budgeted and actual financial results, identifying favorable and unfavorable variances and providing insights into the underlying causes. The analysis covers revenues, variable expenses, and other expenses, offering recommendations for improving financial efficiency and profitability. The report concludes by emphasizing the importance of flexible budgeting in financial decision-making and performance evaluation, supporting the overall goal of enhancing the company's financial health.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.