University of Sunderland: APC308 Financial Management Report, 2019

VerifiedAdded on 2023/01/17

|18

|4396

|80

Report

AI Summary

This report analyzes key aspects of financial management, focusing on right issues, project evaluation methods, and scrip dividends. It begins by examining the computation of the number of shares issued by Lexbel Plc and determining the most suitable right issue option for the company and shareholders, considering factors such as the theoretical ex-right price and new earnings per share. The report then critically evaluates the advantages of scrip dividends for both the company and shareholders, highlighting how they can preserve cash, enhance borrowing capacity, and provide flexibility in investment choices. Furthermore, the report delves into project evaluation methods, including payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR), to assess the viability of a project. The analysis includes detailed calculations and interpretations of each method, providing a comprehensive overview of the project's financial performance and recommendations for investment decisions. The report concludes with a discussion of the advantages and disadvantages of each project evaluation method.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 2........................................................................................................................................4

Number of the shares issued and ex-right price...........................................................................4

Question 3........................................................................................................................................8

(a)Project evaluation methods......................................................................................................8

b. Advantages and disadvantages of the project evaluation method.........................................12

CONCLUSION..............................................................................................................................15

REFERENCES .............................................................................................................................1

Question 2........................................................................................................................................4

Number of the shares issued and ex-right price...........................................................................4

Question 3........................................................................................................................................8

(a)Project evaluation methods......................................................................................................8

b. Advantages and disadvantages of the project evaluation method.........................................12

CONCLUSION..............................................................................................................................15

REFERENCES .............................................................................................................................1

Introduction

Financial management refers to the planning, directing, controlling and organizing

financial activities like procurement and use of the funds of an entity. In other words, it means

the application of principles of general management to the financial resources of the company.

The present report is based on various aspects of financial management that reveals the most

appropriate right issue for the company and the shareholders along with the benefits of the scrip

dividends to the company and the shareholders. The study highlights the computation of the

number of shares that had been issued by Lexbel Plc and the earning per share for reflecting the

most suitable option in relation to the right issues. In second part of the research study project

evaluation methods are used to evaluate viability of the project. Results of the ARR, NPV, IRR

and payback period are analysed and it is identified that project is viable for the firm.

Financial management refers to the planning, directing, controlling and organizing

financial activities like procurement and use of the funds of an entity. In other words, it means

the application of principles of general management to the financial resources of the company.

The present report is based on various aspects of financial management that reveals the most

appropriate right issue for the company and the shareholders along with the benefits of the scrip

dividends to the company and the shareholders. The study highlights the computation of the

number of shares that had been issued by Lexbel Plc and the earning per share for reflecting the

most suitable option in relation to the right issues. In second part of the research study project

evaluation methods are used to evaluate viability of the project. Results of the ARR, NPV, IRR

and payback period are analysed and it is identified that project is viable for the firm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

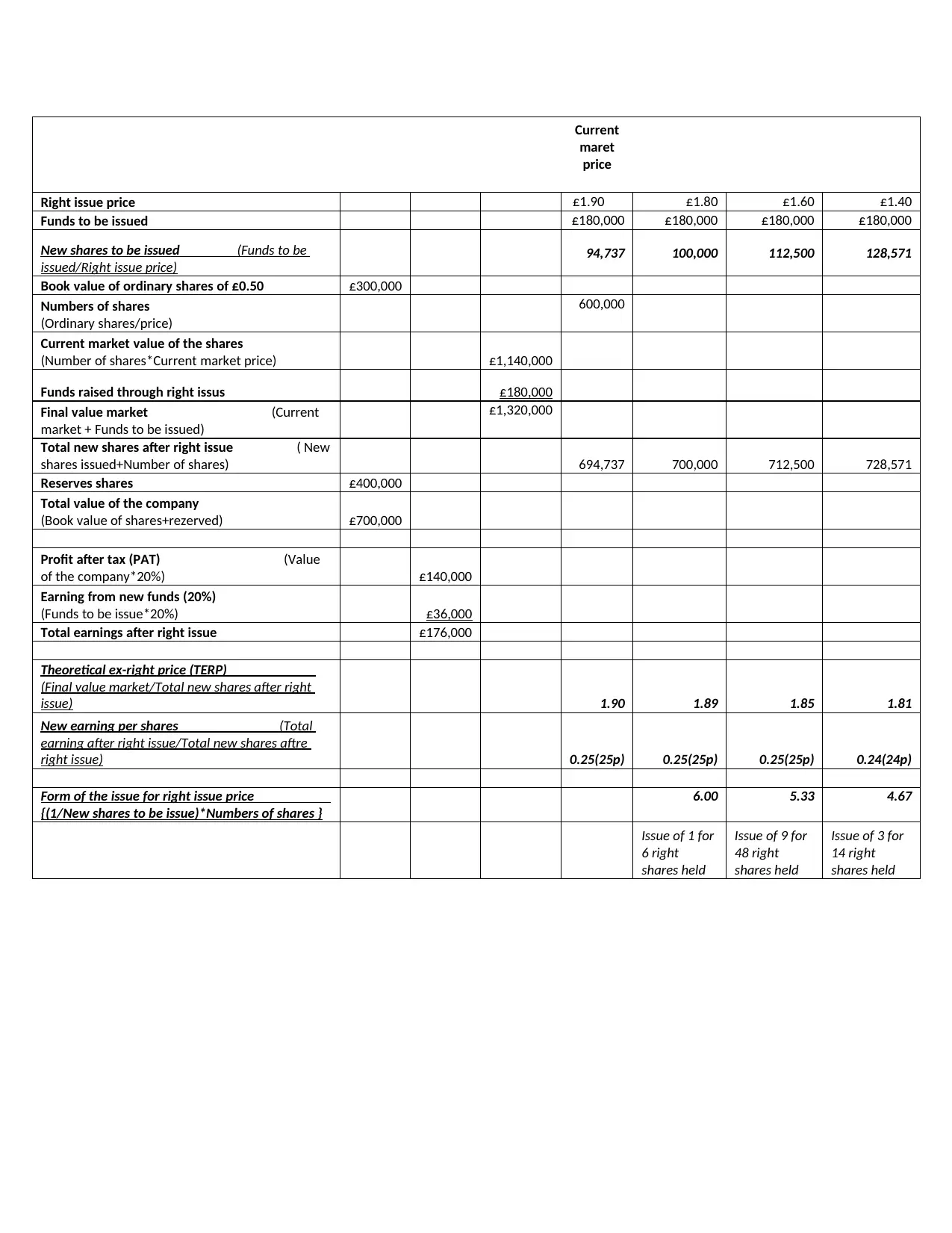

Question 2

Number of the shares issued and ex-right price

Ex-right price, it refers to the estimated share price of an enterprise that follows the right

issue. It has been estimated as the weighted average value of the price per share of the new and

existing shares. Right issue, it means an issue of the new shares in terms of cash to present

shareholders of an organization. Such shares have been issued at the price that is slightly lower

than the market price of the shares that is prevailing at a point of time (ElKelish, 2018). It has

been done for encouraging existing shareholders in taking up shares and in paying cash to the

company. The value of the theoretical ex-right price has been seen as usually low than share

price before the right issue.

Number of the shares issued and ex-right price

Ex-right price, it refers to the estimated share price of an enterprise that follows the right

issue. It has been estimated as the weighted average value of the price per share of the new and

existing shares. Right issue, it means an issue of the new shares in terms of cash to present

shareholders of an organization. Such shares have been issued at the price that is slightly lower

than the market price of the shares that is prevailing at a point of time (ElKelish, 2018). It has

been done for encouraging existing shareholders in taking up shares and in paying cash to the

company. The value of the theoretical ex-right price has been seen as usually low than share

price before the right issue.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current

maret

price

Right issue price £1.90 £1.80 £1.60 £1.40

Funds to be issued £180,000 £180,000 £180,000 £180,000

New shares to be issued (Funds to be

issued/Right issue price)

94,737 100,000 112,500 128,571

Book value of ordinary shares of £0.50 £300,000

Numbers of shares

(Ordinary shares/price)

600,000

Current market value of the shares

(Number of shares*Current market price) £1,140,000

Funds raised through right issus £180,000

Final value market (Current

market + Funds to be issued)

£1,320,000

Total new shares after right issue ( New

shares issued+Number of shares) 694,737 700,000 712,500 728,571

Reserves shares £400,000

Total value of the company

(Book value of shares+rezerved) £700,000

Profit after tax (PAT) (Value

of the company*20%) £140,000

Earning from new funds (20%)

(Funds to be issue*20%) £36,000

Total earnings after right issue £176,000

Theoretical ex-right price (TERP)

(Final value market/Total new shares after right

issue) 1.90 1.89 1.85 1.81

New earning per shares (Total

earning after right issue/Total new shares aftre

right issue) 0.25(25p) 0.25(25p) 0.25(25p) 0.24(24p)

Form of the issue for right issue price

{(1/New shares to be issue)*Numbers of shares }

6.00 5.33 4.67

Issue of 1 for

6 right

shares held

Issue of 9 for

48 right

shares held

Issue of 3 for

14 right

shares held

maret

price

Right issue price £1.90 £1.80 £1.60 £1.40

Funds to be issued £180,000 £180,000 £180,000 £180,000

New shares to be issued (Funds to be

issued/Right issue price)

94,737 100,000 112,500 128,571

Book value of ordinary shares of £0.50 £300,000

Numbers of shares

(Ordinary shares/price)

600,000

Current market value of the shares

(Number of shares*Current market price) £1,140,000

Funds raised through right issus £180,000

Final value market (Current

market + Funds to be issued)

£1,320,000

Total new shares after right issue ( New

shares issued+Number of shares) 694,737 700,000 712,500 728,571

Reserves shares £400,000

Total value of the company

(Book value of shares+rezerved) £700,000

Profit after tax (PAT) (Value

of the company*20%) £140,000

Earning from new funds (20%)

(Funds to be issue*20%) £36,000

Total earnings after right issue £176,000

Theoretical ex-right price (TERP)

(Final value market/Total new shares after right

issue) 1.90 1.89 1.85 1.81

New earning per shares (Total

earning after right issue/Total new shares aftre

right issue) 0.25(25p) 0.25(25p) 0.25(25p) 0.24(24p)

Form of the issue for right issue price

{(1/New shares to be issue)*Numbers of shares }

6.00 5.33 4.67

Issue of 1 for

6 right

shares held

Issue of 9 for

48 right

shares held

Issue of 3 for

14 right

shares held

From the above results, it has been observed that the third option is seen as the best for

the shareholders as well as for the company.

Shareholders could increase their exposure at a discounted value and could have a large

proportion of the shares on which they can earn returns in the future. On the other hand, the

company could make more expansion by creating larger share of the existing shareholders only

which in turn does not involve any cost and outsiders, or external parties cannot have stake over

it. Company should choose for the third option where the price of issuing the right shares

equates to 1.40. This the suitable option because employees get more shares at lower price and

the company will gain more and more employees in exercising the option of right issue.

Critically evaluating advantages of the scrip dividends with respect to shareholders and the

company

Scrip dividend refers to the new share of the company's or issuers' stock, which is being issued

to the shareholders rather than providing them with a dividend. Scrip dividends might be used

when an issue is having a very little amount of cash available in issuing the cash dividend but

still desire for paying the return to the shareholders in any manner (David and Ginglinger,

2016). Such dividends are also being availed to the shareholders as the alternative to the cash

dividend, which in turn rolled their dividend payments into a large number of the shares.

In other words, scrip dividends mean the process of facilitating the shareholders with a choice of

receiving the cash dividends or the dividend at the future period of time or the common stock

(Bernhart and Mai, 2016). At the time when the corporation issues the scrip dividends, it means

that the company is allowing the shareholders for increasing their holding size without incurring

any amount of the fees. Scrip dividends that are tied up with the common stock allow for issuing

the company in retaining and the facilitating and investors with an ability for increasing their

respective holdings within the corporation.

Advantages to the company

the shareholders as well as for the company.

Shareholders could increase their exposure at a discounted value and could have a large

proportion of the shares on which they can earn returns in the future. On the other hand, the

company could make more expansion by creating larger share of the existing shareholders only

which in turn does not involve any cost and outsiders, or external parties cannot have stake over

it. Company should choose for the third option where the price of issuing the right shares

equates to 1.40. This the suitable option because employees get more shares at lower price and

the company will gain more and more employees in exercising the option of right issue.

Critically evaluating advantages of the scrip dividends with respect to shareholders and the

company

Scrip dividend refers to the new share of the company's or issuers' stock, which is being issued

to the shareholders rather than providing them with a dividend. Scrip dividends might be used

when an issue is having a very little amount of cash available in issuing the cash dividend but

still desire for paying the return to the shareholders in any manner (David and Ginglinger,

2016). Such dividends are also being availed to the shareholders as the alternative to the cash

dividend, which in turn rolled their dividend payments into a large number of the shares.

In other words, scrip dividends mean the process of facilitating the shareholders with a choice of

receiving the cash dividends or the dividend at the future period of time or the common stock

(Bernhart and Mai, 2016). At the time when the corporation issues the scrip dividends, it means

that the company is allowing the shareholders for increasing their holding size without incurring

any amount of the fees. Scrip dividends that are tied up with the common stock allow for issuing

the company in retaining and the facilitating and investors with an ability for increasing their

respective holdings within the corporation.

Advantages to the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Scrip dividends help the company in preserving their cash position in case substantial, or a

majority of the shareholders takes up an option of the share. The share price of the company will

not be diluted if a small portion of the scrip dividend has been issued (Westhuizen, 2016). Scrip

dividends help an enterprise in enhancing its borrowing capacity as it results to decrease in the

gearing of the company by with issuance of the shares. It helps an entity in saving the cash as for

each and every shareholder which elects the shares, so it results in saving the money. Then they

could make use of the extra or additional cash for its operations or in paying down debt and

shoring up its balance sheet. In fact, it provides the companies in minimizing the risk regarding

increasing a liquidity position. This helps in raising market capitalization of corporate on stock

exchange by increasing the investors.

Advantages to shareholders

They have been given an option to choose for dividend or shares and deciding for the best

suitable option (French, 2015). Specifically, one of the investor might be a retiree who highly

depends on the cash dividends in paying off their living expenses. In such case, they would be

selecting the option of cash dividend, and on the other side, younger investors might desire for

owing more shares for the purpose of keeping it as the assets in order to get the future

appreciation in the prices or in earning higher returns. In case the shares are seen as undervalued,

they would liking or opting for the scrip dividends and would be electing in receiving the shares

(ElKelish, 2018). In such scenario, shareholders are benefited as they don't need to pay for the

transaction cost that they would be incurring when they had bought for the same number of the

shares through the brokerage account. Scrip dividends assist an investors with far more returns

and the financial gain opposing to cash dividends with passage of time.

majority of the shareholders takes up an option of the share. The share price of the company will

not be diluted if a small portion of the scrip dividend has been issued (Westhuizen, 2016). Scrip

dividends help an enterprise in enhancing its borrowing capacity as it results to decrease in the

gearing of the company by with issuance of the shares. It helps an entity in saving the cash as for

each and every shareholder which elects the shares, so it results in saving the money. Then they

could make use of the extra or additional cash for its operations or in paying down debt and

shoring up its balance sheet. In fact, it provides the companies in minimizing the risk regarding

increasing a liquidity position. This helps in raising market capitalization of corporate on stock

exchange by increasing the investors.

Advantages to shareholders

They have been given an option to choose for dividend or shares and deciding for the best

suitable option (French, 2015). Specifically, one of the investor might be a retiree who highly

depends on the cash dividends in paying off their living expenses. In such case, they would be

selecting the option of cash dividend, and on the other side, younger investors might desire for

owing more shares for the purpose of keeping it as the assets in order to get the future

appreciation in the prices or in earning higher returns. In case the shares are seen as undervalued,

they would liking or opting for the scrip dividends and would be electing in receiving the shares

(ElKelish, 2018). In such scenario, shareholders are benefited as they don't need to pay for the

transaction cost that they would be incurring when they had bought for the same number of the

shares through the brokerage account. Scrip dividends assist an investors with far more returns

and the financial gain opposing to cash dividends with passage of time.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 3

(a)Project evaluation methods

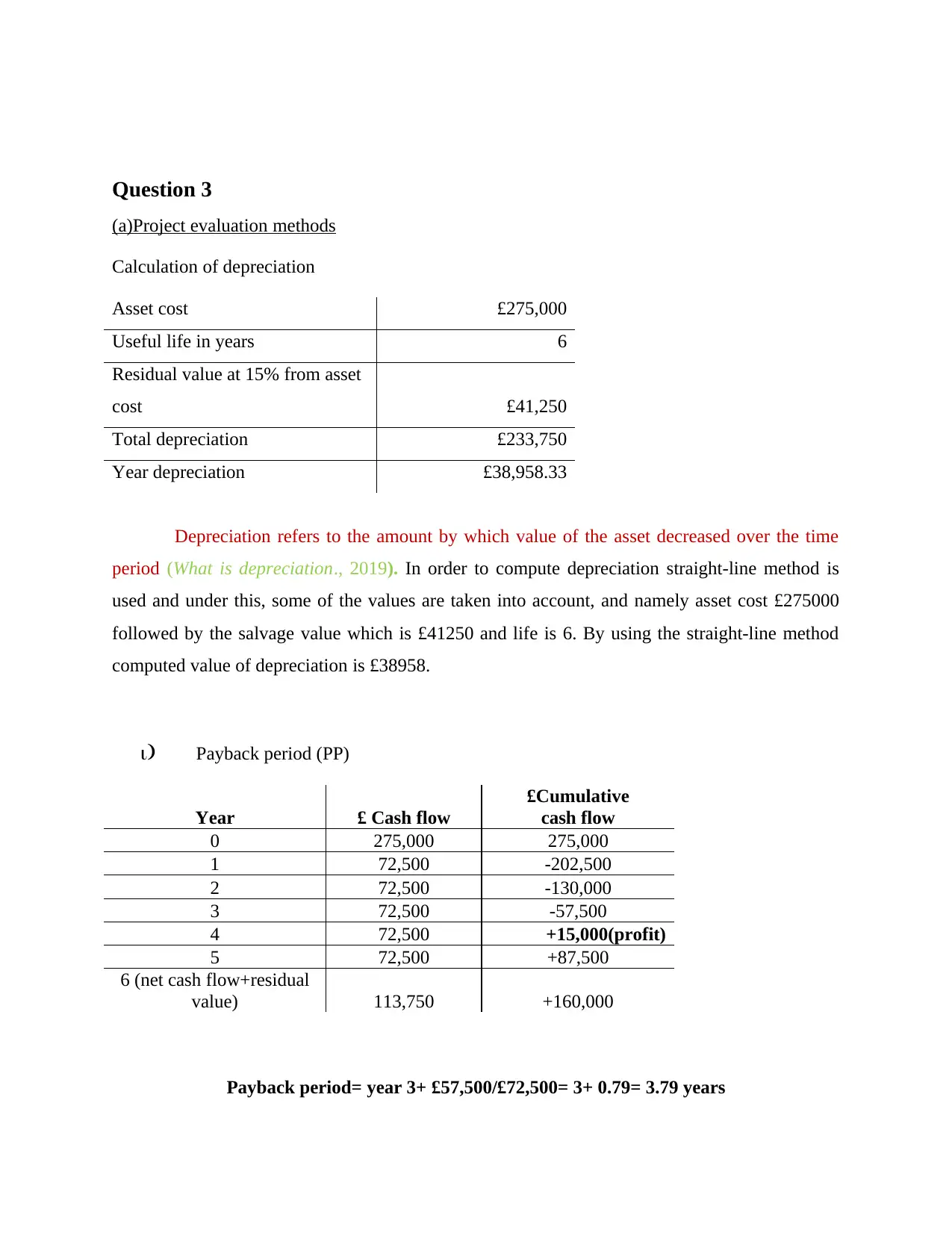

Calculation of depreciation

Asset cost £275,000

Useful life in years 6

Residual value at 15% from asset

cost £41,250

Total depreciation £233,750

Year depreciation £38,958.33

Depreciation refers to the amount by which value of the asset decreased over the time

period (What is depreciation., 2019). In order to compute depreciation straight-line method is

used and under this, some of the values are taken into account, and namely asset cost £275000

followed by the salvage value which is £41250 and life is 6. By using the straight-line method

computed value of depreciation is £38958.

i) Payback period (PP)

Year £ Cash flow

£Cumulative

cash flow

0 275,000 275,000

1 72,500 -202,500

2 72,500 -130,000

3 72,500 -57,500

4 72,500 +15,000(profit)

5 72,500 +87,500

6 (net cash flow+residual

value) 113,750 +160,000

Payback period= year 3+ £57,500/£72,500= 3+ 0.79= 3.79 years

(a)Project evaluation methods

Calculation of depreciation

Asset cost £275,000

Useful life in years 6

Residual value at 15% from asset

cost £41,250

Total depreciation £233,750

Year depreciation £38,958.33

Depreciation refers to the amount by which value of the asset decreased over the time

period (What is depreciation., 2019). In order to compute depreciation straight-line method is

used and under this, some of the values are taken into account, and namely asset cost £275000

followed by the salvage value which is £41250 and life is 6. By using the straight-line method

computed value of depreciation is £38958.

i) Payback period (PP)

Year £ Cash flow

£Cumulative

cash flow

0 275,000 275,000

1 72,500 -202,500

2 72,500 -130,000

3 72,500 -57,500

4 72,500 +15,000(profit)

5 72,500 +87,500

6 (net cash flow+residual

value) 113,750 +160,000

Payback period= year 3+ £57,500/£72,500= 3+ 0.79= 3.79 years

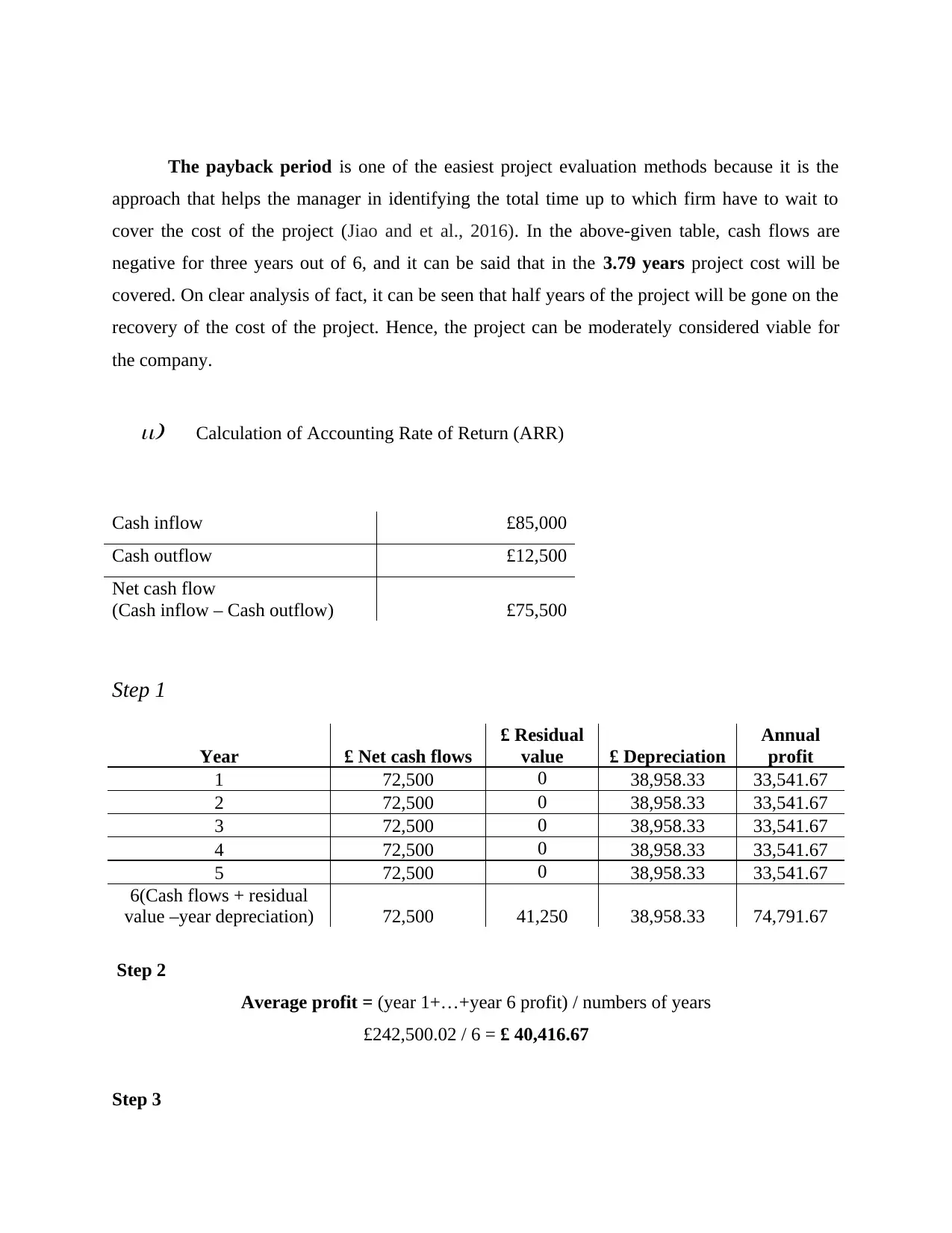

The payback period is one of the easiest project evaluation methods because it is the

approach that helps the manager in identifying the total time up to which firm have to wait to

cover the cost of the project (Jiao and et al., 2016). In the above-given table, cash flows are

negative for three years out of 6, and it can be said that in the 3.79 years project cost will be

covered. On clear analysis of fact, it can be seen that half years of the project will be gone on the

recovery of the cost of the project. Hence, the project can be moderately considered viable for

the company.

ii) Calculation of Accounting Rate of Return (ARR)

Cash inflow £85,000

Cash outflow £12,500

Net cash flow

(Cash inflow – Cash outflow) £75,500

Step 1

Year £ Net cash flows

£ Residual

value £ Depreciation

Annual

profit

1 72,500 0 38,958.33 33,541.67

2 72,500 0 38,958.33 33,541.67

3 72,500 0 38,958.33 33,541.67

4 72,500 0 38,958.33 33,541.67

5 72,500 0 38,958.33 33,541.67

6(Cash flows + residual

value –year depreciation) 72,500 41,250 38,958.33 74,791.67

Step 2

Average profit = (year 1+…+year 6 profit) / numbers of years

£242,500.02 / 6 = £ 40,416.67

Step 3

approach that helps the manager in identifying the total time up to which firm have to wait to

cover the cost of the project (Jiao and et al., 2016). In the above-given table, cash flows are

negative for three years out of 6, and it can be said that in the 3.79 years project cost will be

covered. On clear analysis of fact, it can be seen that half years of the project will be gone on the

recovery of the cost of the project. Hence, the project can be moderately considered viable for

the company.

ii) Calculation of Accounting Rate of Return (ARR)

Cash inflow £85,000

Cash outflow £12,500

Net cash flow

(Cash inflow – Cash outflow) £75,500

Step 1

Year £ Net cash flows

£ Residual

value £ Depreciation

Annual

profit

1 72,500 0 38,958.33 33,541.67

2 72,500 0 38,958.33 33,541.67

3 72,500 0 38,958.33 33,541.67

4 72,500 0 38,958.33 33,541.67

5 72,500 0 38,958.33 33,541.67

6(Cash flows + residual

value –year depreciation) 72,500 41,250 38,958.33 74,791.67

Step 2

Average profit = (year 1+…+year 6 profit) / numbers of years

£242,500.02 / 6 = £ 40,416.67

Step 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

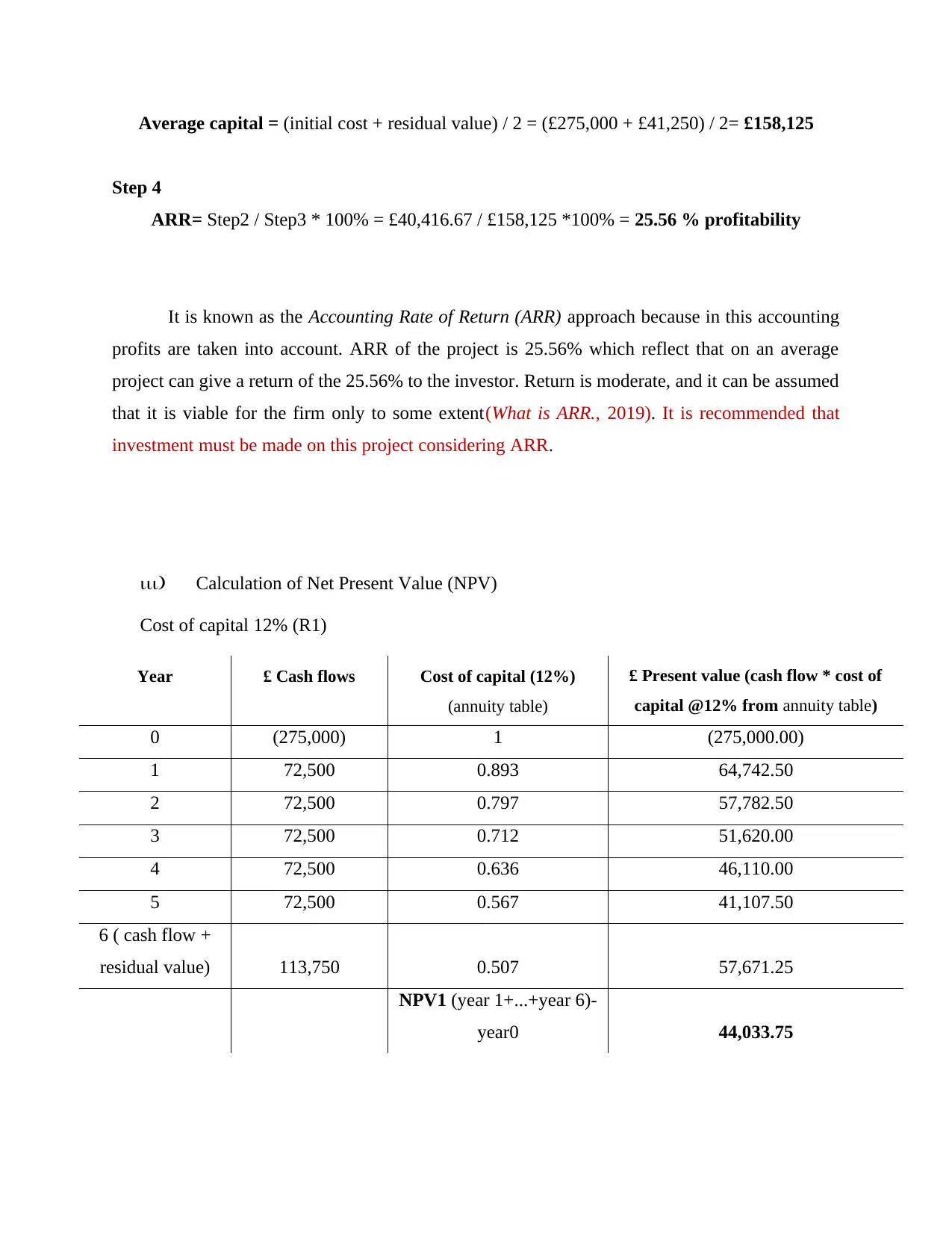

Average capital = (initial cost + residual value) / 2 = (£275,000 + £41,250) / 2= £158,125

Step 4

ARR= Step2 / Step3 * 100% = £40,416.67 / £158,125 *100% = 25.56 % profitability

It is known as the Accounting Rate of Return (ARR) approach because in this accounting

profits are taken into account. ARR of the project is 25.56% which reflect that on an average

project can give a return of the 25.56% to the investor. Return is moderate, and it can be assumed

that it is viable for the firm only to some extent(What is ARR., 2019). It is recommended that

investment must be made on this project considering ARR.

iii) Calculation of Net Present Value (NPV)

Cost of capital 12% (R1)

Year £ Cash flows Cost of capital (12%)

(annuity table)

£ Present value (cash flow * cost of

capital @12% from annuity table)

0 (275,000) 1 (275,000.00)

1 72,500 0.893 64,742.50

2 72,500 0.797 57,782.50

3 72,500 0.712 51,620.00

4 72,500 0.636 46,110.00

5 72,500 0.567 41,107.50

6 ( cash flow +

residual value) 113,750 0.507 57,671.25

NPV1 (year 1+...+year 6)-

year0 44,033.75

Step 4

ARR= Step2 / Step3 * 100% = £40,416.67 / £158,125 *100% = 25.56 % profitability

It is known as the Accounting Rate of Return (ARR) approach because in this accounting

profits are taken into account. ARR of the project is 25.56% which reflect that on an average

project can give a return of the 25.56% to the investor. Return is moderate, and it can be assumed

that it is viable for the firm only to some extent(What is ARR., 2019). It is recommended that

investment must be made on this project considering ARR.

iii) Calculation of Net Present Value (NPV)

Cost of capital 12% (R1)

Year £ Cash flows Cost of capital (12%)

(annuity table)

£ Present value (cash flow * cost of

capital @12% from annuity table)

0 (275,000) 1 (275,000.00)

1 72,500 0.893 64,742.50

2 72,500 0.797 57,782.50

3 72,500 0.712 51,620.00

4 72,500 0.636 46,110.00

5 72,500 0.567 41,107.50

6 ( cash flow +

residual value) 113,750 0.507 57,671.25

NPV1 (year 1+...+year 6)-

year0 44,033.75

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

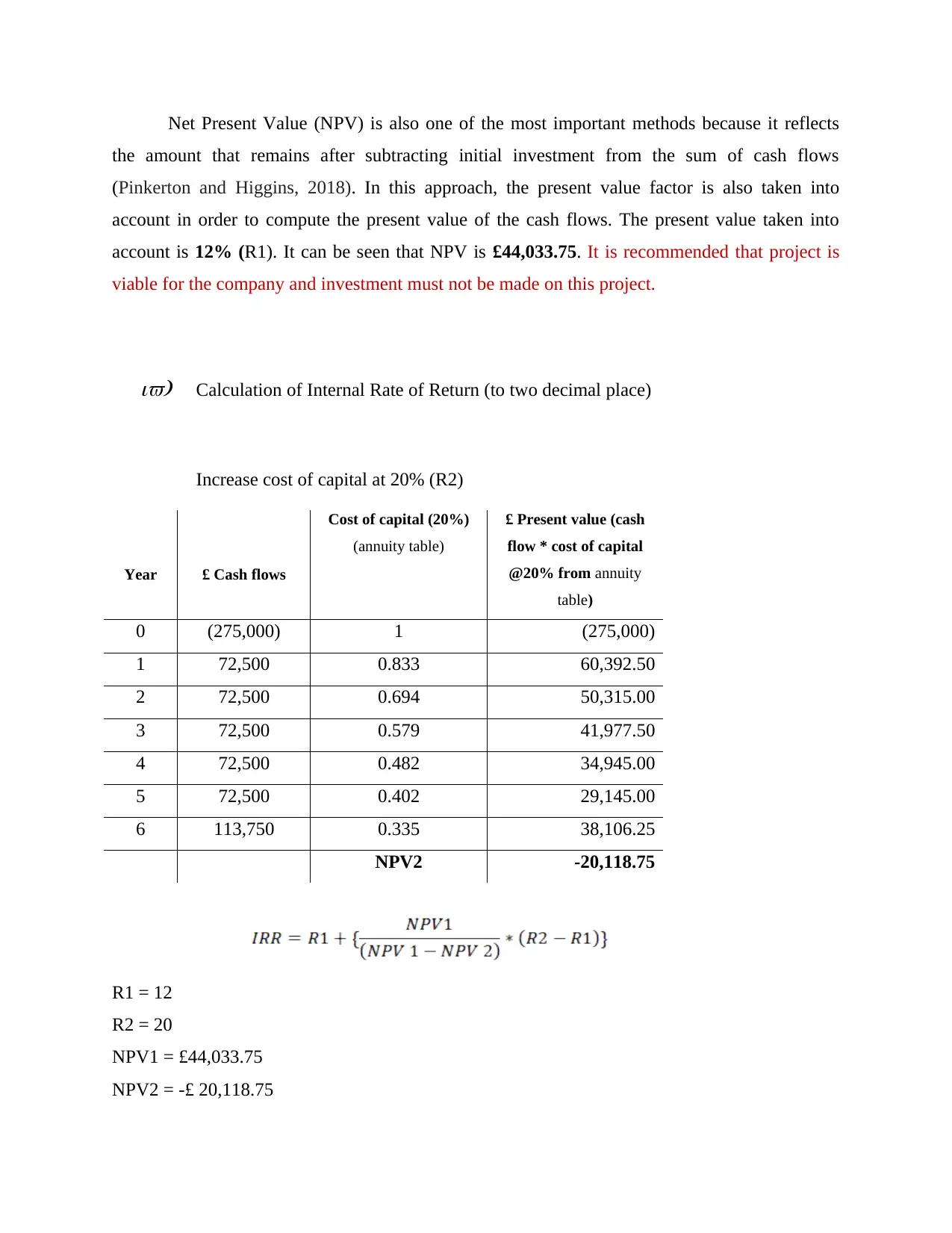

Net Present Value (NPV) is also one of the most important methods because it reflects

the amount that remains after subtracting initial investment from the sum of cash flows

(Pinkerton and Higgins, 2018). In this approach, the present value factor is also taken into

account in order to compute the present value of the cash flows. The present value taken into

account is 12% (R1). It can be seen that NPV is £44,033.75. It is recommended that project is

viable for the company and investment must not be made on this project.

iv) Calculation of Internal Rate of Return (to two decimal place)

Increase cost of capital at 20% (R2)

Year £ Cash flows

Cost of capital (20%)

(annuity table)

£ Present value (cash

flow * cost of capital

@20% from annuity

table)

0 (275,000) 1 (275,000)

1 72,500 0.833 60,392.50

2 72,500 0.694 50,315.00

3 72,500 0.579 41,977.50

4 72,500 0.482 34,945.00

5 72,500 0.402 29,145.00

6 113,750 0.335 38,106.25

NPV2 -20,118.75

R1 = 12

R2 = 20

NPV1 = £44,033.75

NPV2 = -£ 20,118.75

the amount that remains after subtracting initial investment from the sum of cash flows

(Pinkerton and Higgins, 2018). In this approach, the present value factor is also taken into

account in order to compute the present value of the cash flows. The present value taken into

account is 12% (R1). It can be seen that NPV is £44,033.75. It is recommended that project is

viable for the company and investment must not be made on this project.

iv) Calculation of Internal Rate of Return (to two decimal place)

Increase cost of capital at 20% (R2)

Year £ Cash flows

Cost of capital (20%)

(annuity table)

£ Present value (cash

flow * cost of capital

@20% from annuity

table)

0 (275,000) 1 (275,000)

1 72,500 0.833 60,392.50

2 72,500 0.694 50,315.00

3 72,500 0.579 41,977.50

4 72,500 0.482 34,945.00

5 72,500 0.402 29,145.00

6 113,750 0.335 38,106.25

NPV2 -20,118.75

R1 = 12

R2 = 20

NPV1 = £44,033.75

NPV2 = -£ 20,118.75

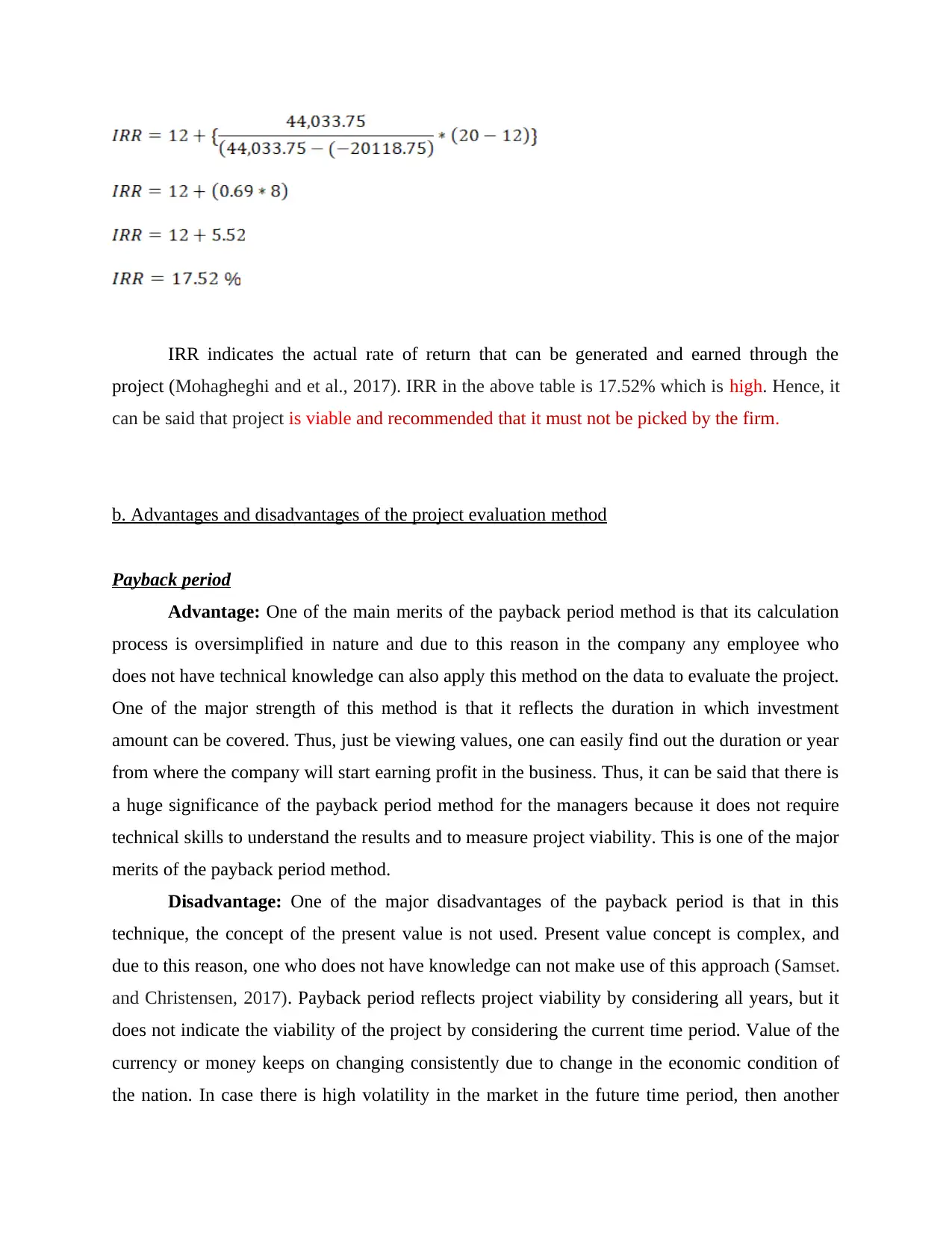

IRR indicates the actual rate of return that can be generated and earned through the

project (Mohagheghi and et al., 2017). IRR in the above table is 17.52% which is high. Hence, it

can be said that project is viable and recommended that it must not be picked by the firm.

b. Advantages and disadvantages of the project evaluation method

Payback period

Advantage: One of the main merits of the payback period method is that its calculation

process is oversimplified in nature and due to this reason in the company any employee who

does not have technical knowledge can also apply this method on the data to evaluate the project.

One of the major strength of this method is that it reflects the duration in which investment

amount can be covered. Thus, just be viewing values, one can easily find out the duration or year

from where the company will start earning profit in the business. Thus, it can be said that there is

a huge significance of the payback period method for the managers because it does not require

technical skills to understand the results and to measure project viability. This is one of the major

merits of the payback period method.

Disadvantage: One of the major disadvantages of the payback period is that in this

technique, the concept of the present value is not used. Present value concept is complex, and

due to this reason, one who does not have knowledge can not make use of this approach (Samset.

and Christensen, 2017). Payback period reflects project viability by considering all years, but it

does not indicate the viability of the project by considering the current time period. Value of the

currency or money keeps on changing consistently due to change in the economic condition of

the nation. In case there is high volatility in the market in the future time period, then another

project (Mohagheghi and et al., 2017). IRR in the above table is 17.52% which is high. Hence, it

can be said that project is viable and recommended that it must not be picked by the firm.

b. Advantages and disadvantages of the project evaluation method

Payback period

Advantage: One of the main merits of the payback period method is that its calculation

process is oversimplified in nature and due to this reason in the company any employee who

does not have technical knowledge can also apply this method on the data to evaluate the project.

One of the major strength of this method is that it reflects the duration in which investment

amount can be covered. Thus, just be viewing values, one can easily find out the duration or year

from where the company will start earning profit in the business. Thus, it can be said that there is

a huge significance of the payback period method for the managers because it does not require

technical skills to understand the results and to measure project viability. This is one of the major

merits of the payback period method.

Disadvantage: One of the major disadvantages of the payback period is that in this

technique, the concept of the present value is not used. Present value concept is complex, and

due to this reason, one who does not have knowledge can not make use of this approach (Samset.

and Christensen, 2017). Payback period reflects project viability by considering all years, but it

does not indicate the viability of the project by considering the current time period. Value of the

currency or money keeps on changing consistently due to change in the economic condition of

the nation. In case there is high volatility in the market in the future time period, then another

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.