Financial Management Report: Hillside Industries Expansion Analysis

VerifiedAdded on 2022/08/13

|12

|2630

|11

Report

AI Summary

This report provides a comprehensive financial analysis for Hillside Industries, focusing on capital budgeting techniques to evaluate an expansion project. It examines working capital requirements, calculating the cash conversion cycle and its impact on liquidity. The report also conducts a break-even analysis, comparing accounting and cash break-even points to determine the minimum production levels needed for profitability under existing and proposed scenarios. Furthermore, the report calculates the Net Present Value (NPV), Internal Rate of Return (IRR), and Payback Period to assess the project's financial viability, concluding that the investment is profitable. The report also explores different sources of funding, recommending debt financing due to its tax benefits and lower risk profile compared to equity. Finally, the report recommends endorsing the expansion plan to the Board of Directors, supported by the positive financial metrics and strategic advantages identified.

Running head: FINANCIAL MANAGEMENT 1

FINANCIAL MANAGEMENT

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: FINANCIAL MANAGEMENT

Executive summary

Financial management is a wider term and the capital budgeting is an important process

and it is helpful in deciding the worth of the investments for which the funds are used. In this

current report a detailed understanding has been carried out for Board of Directors to understand

the net present value, payback period and the internal rate of return and their benefits. Further, an

understanding between the cash and the accounting break-even is bifurcated with tables and it is

clearly evident the project is acceptable with debt component being used as the source of finance.

Executive summary

Financial management is a wider term and the capital budgeting is an important process

and it is helpful in deciding the worth of the investments for which the funds are used. In this

current report a detailed understanding has been carried out for Board of Directors to understand

the net present value, payback period and the internal rate of return and their benefits. Further, an

understanding between the cash and the accounting break-even is bifurcated with tables and it is

clearly evident the project is acceptable with debt component being used as the source of finance.

Running head: FINANCIAL MANAGEMENT

Table of Contents

Introduction.................................................................................................................................................4

Question 1: Working capital requirements..................................................................................................4

Question 2: Breakeven Point.......................................................................................................................6

Question 3: Net present value......................................................................................................................8

Question 4: Sources of funds.......................................................................................................................9

Question 5: Recommendation’s endorsement............................................................................................10

References.................................................................................................................................................11

Table of Contents

Introduction.................................................................................................................................................4

Question 1: Working capital requirements..................................................................................................4

Question 2: Breakeven Point.......................................................................................................................6

Question 3: Net present value......................................................................................................................8

Question 4: Sources of funds.......................................................................................................................9

Question 5: Recommendation’s endorsement............................................................................................10

References.................................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running head: FINANCIAL MANAGEMENT

Introduction

Capital budgeting technique is the technique which is used by the company to analyze

the worth of the funds invested for the projects. The term capital budgeting is one of the crucial

terms of the finance subject and is widely used by the company. It also depicts the quantitative

view of each proposal in which the company has invested so that the management can take a

rational decision. In this report a detailed analysis is undertaken with respect of the treatment of

the working capital, net present value, cash conversion cycle and which source is useful for

expansion (Benamraoui, Jory, Boojihawon & Madichie, 2017).

Question 1: Working capital requirements

The working capital management is the strategy designed by companies to make sure

that the operations of the companies are running efficiently. The working capital is analyzed on

the basis of current assets and current liabilities and its impact on the financial statements. In this

section, Hillside Industries have implemented the working capital procedure to gather an

understanding of its implications over the increase in the payment and receivable period (.

(Source: Wang, 2019).

Introduction

Capital budgeting technique is the technique which is used by the company to analyze

the worth of the funds invested for the projects. The term capital budgeting is one of the crucial

terms of the finance subject and is widely used by the company. It also depicts the quantitative

view of each proposal in which the company has invested so that the management can take a

rational decision. In this report a detailed analysis is undertaken with respect of the treatment of

the working capital, net present value, cash conversion cycle and which source is useful for

expansion (Benamraoui, Jory, Boojihawon & Madichie, 2017).

Question 1: Working capital requirements

The working capital management is the strategy designed by companies to make sure

that the operations of the companies are running efficiently. The working capital is analyzed on

the basis of current assets and current liabilities and its impact on the financial statements. In this

section, Hillside Industries have implemented the working capital procedure to gather an

understanding of its implications over the increase in the payment and receivable period (.

(Source: Wang, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: FINANCIAL MANAGEMENT

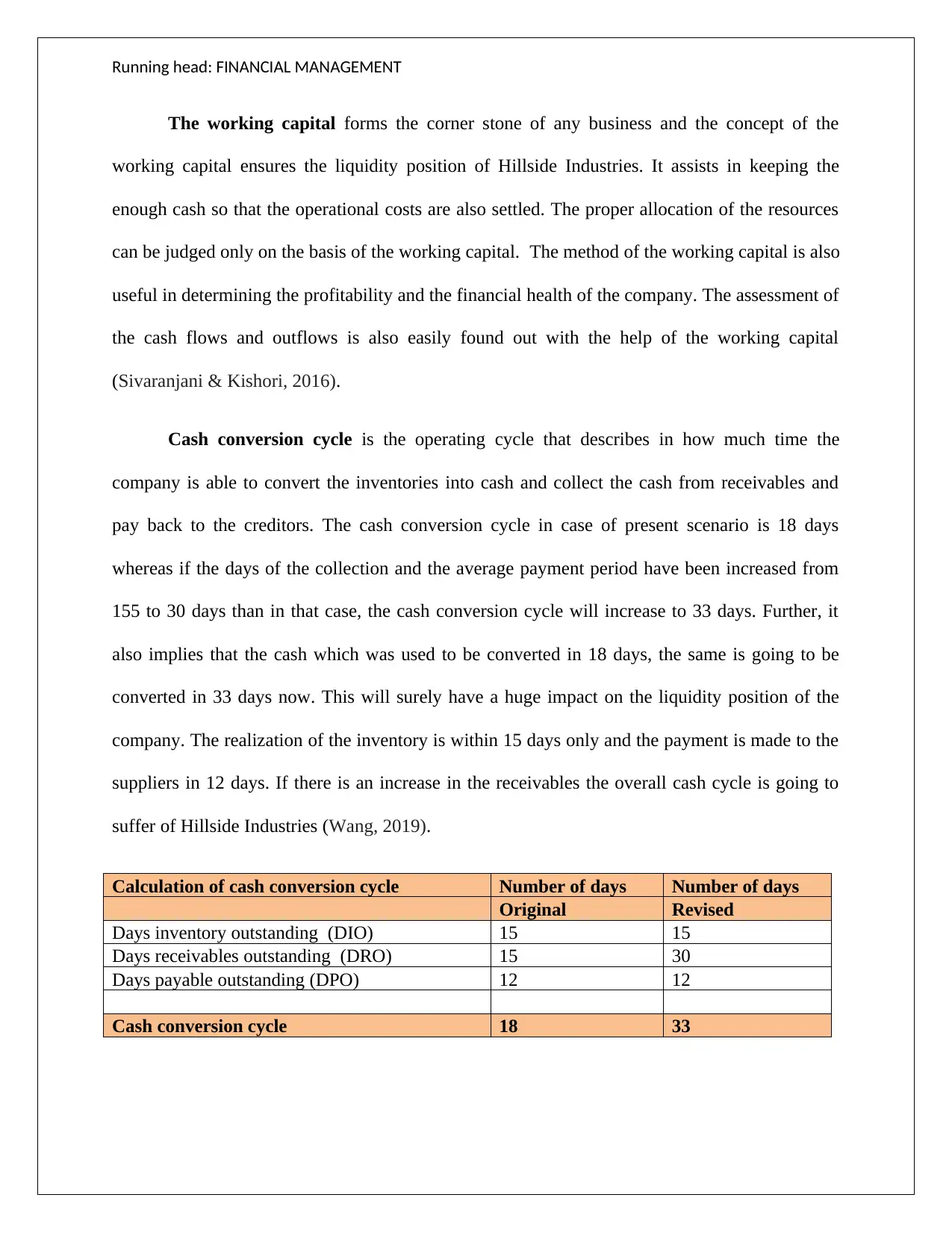

The working capital forms the corner stone of any business and the concept of the

working capital ensures the liquidity position of Hillside Industries. It assists in keeping the

enough cash so that the operational costs are also settled. The proper allocation of the resources

can be judged only on the basis of the working capital. The method of the working capital is also

useful in determining the profitability and the financial health of the company. The assessment of

the cash flows and outflows is also easily found out with the help of the working capital

(Sivaranjani & Kishori, 2016).

Cash conversion cycle is the operating cycle that describes in how much time the

company is able to convert the inventories into cash and collect the cash from receivables and

pay back to the creditors. The cash conversion cycle in case of present scenario is 18 days

whereas if the days of the collection and the average payment period have been increased from

155 to 30 days than in that case, the cash conversion cycle will increase to 33 days. Further, it

also implies that the cash which was used to be converted in 18 days, the same is going to be

converted in 33 days now. This will surely have a huge impact on the liquidity position of the

company. The realization of the inventory is within 15 days only and the payment is made to the

suppliers in 12 days. If there is an increase in the receivables the overall cash cycle is going to

suffer of Hillside Industries (Wang, 2019).

Calculation of cash conversion cycle Number of days Number of days

Original Revised

Days inventory outstanding (DIO) 15 15

Days receivables outstanding (DRO) 15 30

Days payable outstanding (DPO) 12 12

Cash conversion cycle 18 33

The working capital forms the corner stone of any business and the concept of the

working capital ensures the liquidity position of Hillside Industries. It assists in keeping the

enough cash so that the operational costs are also settled. The proper allocation of the resources

can be judged only on the basis of the working capital. The method of the working capital is also

useful in determining the profitability and the financial health of the company. The assessment of

the cash flows and outflows is also easily found out with the help of the working capital

(Sivaranjani & Kishori, 2016).

Cash conversion cycle is the operating cycle that describes in how much time the

company is able to convert the inventories into cash and collect the cash from receivables and

pay back to the creditors. The cash conversion cycle in case of present scenario is 18 days

whereas if the days of the collection and the average payment period have been increased from

155 to 30 days than in that case, the cash conversion cycle will increase to 33 days. Further, it

also implies that the cash which was used to be converted in 18 days, the same is going to be

converted in 33 days now. This will surely have a huge impact on the liquidity position of the

company. The realization of the inventory is within 15 days only and the payment is made to the

suppliers in 12 days. If there is an increase in the receivables the overall cash cycle is going to

suffer of Hillside Industries (Wang, 2019).

Calculation of cash conversion cycle Number of days Number of days

Original Revised

Days inventory outstanding (DIO) 15 15

Days receivables outstanding (DRO) 15 30

Days payable outstanding (DPO) 12 12

Cash conversion cycle 18 33

Running head: FINANCIAL MANAGEMENT

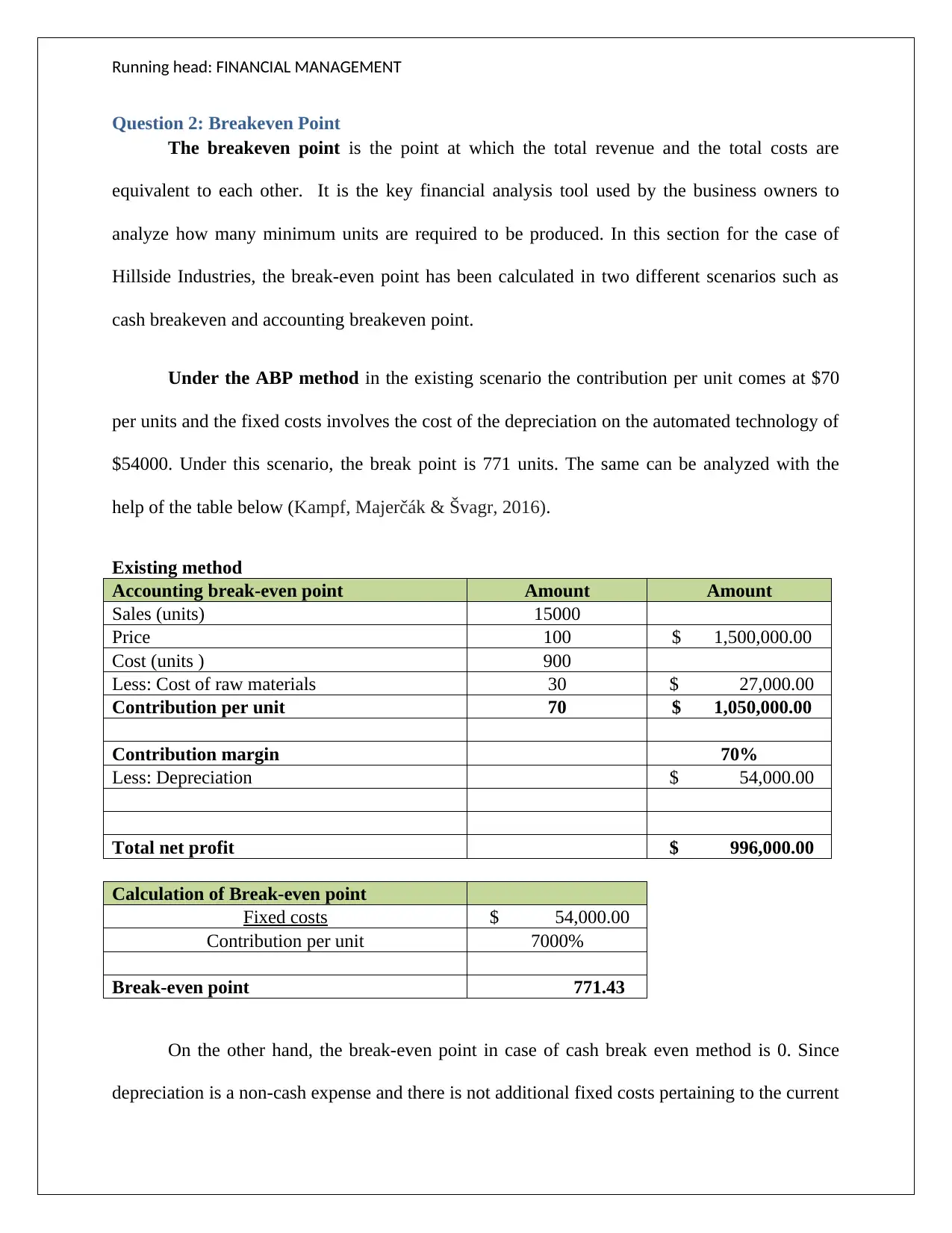

Question 2: Breakeven Point

The breakeven point is the point at which the total revenue and the total costs are

equivalent to each other. It is the key financial analysis tool used by the business owners to

analyze how many minimum units are required to be produced. In this section for the case of

Hillside Industries, the break-even point has been calculated in two different scenarios such as

cash breakeven and accounting breakeven point.

Under the ABP method in the existing scenario the contribution per unit comes at $70

per units and the fixed costs involves the cost of the depreciation on the automated technology of

$54000. Under this scenario, the break point is 771 units. The same can be analyzed with the

help of the table below (Kampf, Majerčák & Švagr, 2016).

Existing method

Accounting break-even point Amount Amount

Sales (units) 15000

Price 100 $ 1,500,000.00

Cost (units ) 900

Less: Cost of raw materials 30 $ 27,000.00

Contribution per unit 70 $ 1,050,000.00

Contribution margin 70%

Less: Depreciation $ 54,000.00

Total net profit $ 996,000.00

Calculation of Break-even point

Fixed costs $ 54,000.00

Contribution per unit 7000%

Break-even point 771.43

On the other hand, the break-even point in case of cash break even method is 0. Since

depreciation is a non-cash expense and there is not additional fixed costs pertaining to the current

Question 2: Breakeven Point

The breakeven point is the point at which the total revenue and the total costs are

equivalent to each other. It is the key financial analysis tool used by the business owners to

analyze how many minimum units are required to be produced. In this section for the case of

Hillside Industries, the break-even point has been calculated in two different scenarios such as

cash breakeven and accounting breakeven point.

Under the ABP method in the existing scenario the contribution per unit comes at $70

per units and the fixed costs involves the cost of the depreciation on the automated technology of

$54000. Under this scenario, the break point is 771 units. The same can be analyzed with the

help of the table below (Kampf, Majerčák & Švagr, 2016).

Existing method

Accounting break-even point Amount Amount

Sales (units) 15000

Price 100 $ 1,500,000.00

Cost (units ) 900

Less: Cost of raw materials 30 $ 27,000.00

Contribution per unit 70 $ 1,050,000.00

Contribution margin 70%

Less: Depreciation $ 54,000.00

Total net profit $ 996,000.00

Calculation of Break-even point

Fixed costs $ 54,000.00

Contribution per unit 7000%

Break-even point 771.43

On the other hand, the break-even point in case of cash break even method is 0. Since

depreciation is a non-cash expense and there is not additional fixed costs pertaining to the current

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running head: FINANCIAL MANAGEMENT

year, the cash breakeven is 0. It also implies that since there is no fixed cost the company has no

minimum unit’s criteria to fulfill.

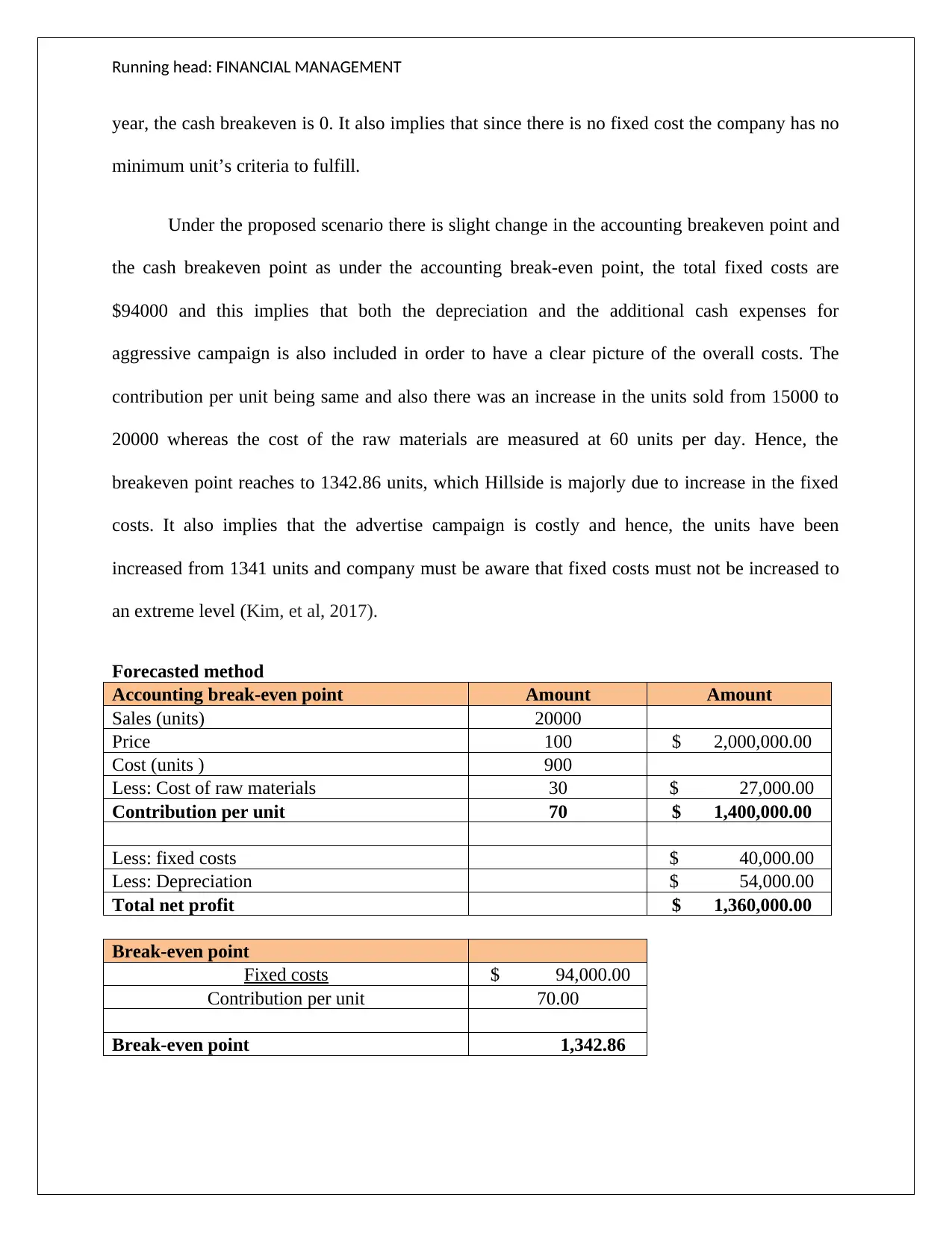

Under the proposed scenario there is slight change in the accounting breakeven point and

the cash breakeven point as under the accounting break-even point, the total fixed costs are

$94000 and this implies that both the depreciation and the additional cash expenses for

aggressive campaign is also included in order to have a clear picture of the overall costs. The

contribution per unit being same and also there was an increase in the units sold from 15000 to

20000 whereas the cost of the raw materials are measured at 60 units per day. Hence, the

breakeven point reaches to 1342.86 units, which Hillside is majorly due to increase in the fixed

costs. It also implies that the advertise campaign is costly and hence, the units have been

increased from 1341 units and company must be aware that fixed costs must not be increased to

an extreme level (Kim, et al, 2017).

Forecasted method

Accounting break-even point Amount Amount

Sales (units) 20000

Price 100 $ 2,000,000.00

Cost (units ) 900

Less: Cost of raw materials 30 $ 27,000.00

Contribution per unit 70 $ 1,400,000.00

Less: fixed costs $ 40,000.00

Less: Depreciation $ 54,000.00

Total net profit $ 1,360,000.00

Break-even point

Fixed costs $ 94,000.00

Contribution per unit 70.00

Break-even point 1,342.86

year, the cash breakeven is 0. It also implies that since there is no fixed cost the company has no

minimum unit’s criteria to fulfill.

Under the proposed scenario there is slight change in the accounting breakeven point and

the cash breakeven point as under the accounting break-even point, the total fixed costs are

$94000 and this implies that both the depreciation and the additional cash expenses for

aggressive campaign is also included in order to have a clear picture of the overall costs. The

contribution per unit being same and also there was an increase in the units sold from 15000 to

20000 whereas the cost of the raw materials are measured at 60 units per day. Hence, the

breakeven point reaches to 1342.86 units, which Hillside is majorly due to increase in the fixed

costs. It also implies that the advertise campaign is costly and hence, the units have been

increased from 1341 units and company must be aware that fixed costs must not be increased to

an extreme level (Kim, et al, 2017).

Forecasted method

Accounting break-even point Amount Amount

Sales (units) 20000

Price 100 $ 2,000,000.00

Cost (units ) 900

Less: Cost of raw materials 30 $ 27,000.00

Contribution per unit 70 $ 1,400,000.00

Less: fixed costs $ 40,000.00

Less: Depreciation $ 54,000.00

Total net profit $ 1,360,000.00

Break-even point

Fixed costs $ 94,000.00

Contribution per unit 70.00

Break-even point 1,342.86

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: FINANCIAL MANAGEMENT

The cash breakeven point in case of the proposed situation is 571.43 units as only cash

expenses that have been incurred for ruling the campaign will only be included as depreciation is

non-cash expense. Therefore, from the other overall analysis it can be stated that, the marketing

departmental proposal is feasible in terms of cash break even as only 571 units are required to be

produced rather than 771 units in case of existing method (Wisnubroto & Suyanto, 2019).

Question 3: Net present value

The net present value is one of the core terms of the techniques of the capital budgeting.

In this section the net present value for the investment made by Hillside Industries, wanting to

expand the business has been analyzed in detail. The NPV is the difference between the present

inflows and the outflows; it is the medium through which the feasibility of the project is analyzed

in detail. The net present value for the proposal of Hillside Industries is $91681. This indicates at

present the value of the automated technology is $91681 and if the company invests in the

project, the future feasibility and growth will increase accordingly. The positive NPV indicates

that the investment will be profitable (Willigers, Jones & Bratvold, 2017).

There are several benefits for choosing the net present value as one of the techniques as it has

several benefits. The net present value method readily accepts the cash flow pattern and in fact

considers all of the cash flows. Another benefit of NPV is it considers the approach of time value

of money and treats the present value worthy enough than future value.

Apart from NPV there are other techniques as well which are also calculated to get more

understanding while choosing the investment proposal. These techniques are internal rate of

return and payback period (Andreasen, Schindler & Valenzuela, 2019).

The cash breakeven point in case of the proposed situation is 571.43 units as only cash

expenses that have been incurred for ruling the campaign will only be included as depreciation is

non-cash expense. Therefore, from the other overall analysis it can be stated that, the marketing

departmental proposal is feasible in terms of cash break even as only 571 units are required to be

produced rather than 771 units in case of existing method (Wisnubroto & Suyanto, 2019).

Question 3: Net present value

The net present value is one of the core terms of the techniques of the capital budgeting.

In this section the net present value for the investment made by Hillside Industries, wanting to

expand the business has been analyzed in detail. The NPV is the difference between the present

inflows and the outflows; it is the medium through which the feasibility of the project is analyzed

in detail. The net present value for the proposal of Hillside Industries is $91681. This indicates at

present the value of the automated technology is $91681 and if the company invests in the

project, the future feasibility and growth will increase accordingly. The positive NPV indicates

that the investment will be profitable (Willigers, Jones & Bratvold, 2017).

There are several benefits for choosing the net present value as one of the techniques as it has

several benefits. The net present value method readily accepts the cash flow pattern and in fact

considers all of the cash flows. Another benefit of NPV is it considers the approach of time value

of money and treats the present value worthy enough than future value.

Apart from NPV there are other techniques as well which are also calculated to get more

understanding while choosing the investment proposal. These techniques are internal rate of

return and payback period (Andreasen, Schindler & Valenzuela, 2019).

Running head: FINANCIAL MANAGEMENT

The internal rate of return also known as IRR is the rate at which the NPV is equivalent

to zero whereas the payback period is a method that helps in defining the time period in which

the initial costs incurred for any proposal will be recovered. This method also helps in the

evaluation of the proposals in the quick manner. These two techniques are also beneficial as the

early payback enhances the overall liquidity position and it’s simpler to calculate and understand.

IRR is not dependent on the hurdle rate and timing of all cash flows is taken into consideration.

For better understanding, the calculations have been done and it has been realized that payback

period is 3.69 years and the internal rate of return in 16% which is higher than the cost of capital.

Hence, overall examination indicates the proposal is feasible and profitable as well (Frank &

Shen, 2016).

Question 4: Sources of funds

Generally the sources are funds are of different types such as debt and equity. The debt

being the fixed payment option and equity being the risk bearers the company must invest

according to their capacity and funds. On the basis of the cost of the equity and the cost of the

debt, the company must use the cost of equity as the choice for the expansion plan as the cost of

equity is already high at 11% with beta value of 2 whereas the debt cost is 6.48% (Roy, Rudra &

Prasad, 2017). Using debt helps in lowering down the risk as the debt is prone to the deductions

due to the tax factor associated. The tax savings help in reduction of the overall cost of capital.

Equity financing tends to be risky and this defines that debt shall be the right choice on account

of Hillside. Using debt also helps to retain the profits in the business itself as only the amount of

interest is paid out of profits. It also helps in maximizing the financial leverage by keeping the

extra profits for the equity investors. Hence, from the overall in-depth analysis it can be assured

The internal rate of return also known as IRR is the rate at which the NPV is equivalent

to zero whereas the payback period is a method that helps in defining the time period in which

the initial costs incurred for any proposal will be recovered. This method also helps in the

evaluation of the proposals in the quick manner. These two techniques are also beneficial as the

early payback enhances the overall liquidity position and it’s simpler to calculate and understand.

IRR is not dependent on the hurdle rate and timing of all cash flows is taken into consideration.

For better understanding, the calculations have been done and it has been realized that payback

period is 3.69 years and the internal rate of return in 16% which is higher than the cost of capital.

Hence, overall examination indicates the proposal is feasible and profitable as well (Frank &

Shen, 2016).

Question 4: Sources of funds

Generally the sources are funds are of different types such as debt and equity. The debt

being the fixed payment option and equity being the risk bearers the company must invest

according to their capacity and funds. On the basis of the cost of the equity and the cost of the

debt, the company must use the cost of equity as the choice for the expansion plan as the cost of

equity is already high at 11% with beta value of 2 whereas the debt cost is 6.48% (Roy, Rudra &

Prasad, 2017). Using debt helps in lowering down the risk as the debt is prone to the deductions

due to the tax factor associated. The tax savings help in reduction of the overall cost of capital.

Equity financing tends to be risky and this defines that debt shall be the right choice on account

of Hillside. Using debt also helps to retain the profits in the business itself as only the amount of

interest is paid out of profits. It also helps in maximizing the financial leverage by keeping the

extra profits for the equity investors. Hence, from the overall in-depth analysis it can be assured

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Running head: FINANCIAL MANAGEMENT

that for Hillside Industries, cost of debt is the useful component (Osma, Gomez-Conde & de las

Heras, 2018).

Question 5: Recommendation’s endorsement

From the overall analysis it is conclusive that the recommended plan shall be endorsed to

the Board of the directors. The reason behind such endorsement is that the entire analysis is in

favor of the selection of the proposal. Also the concept of the breakeven point has been divided

into four sections and the ultimate result states that the minimum units that are required are less

in case of the cash accounting breakeven point as it ignored the inclusion of depreciation. Due to

the positive net present value, higher internal rate of return and the payback period is less than

the term of the investment proposal; the company will have the higher growth and opportunities

in future. In the later half, the debt has been chosen as the method for expansion of the project

only because it is subjected to tax deductions as discussed above which will be helpful in

retaining the overall gain of the business. Since the boards of the directors were bewildered this

analysis will defiantly help them out. Henceforth, Hillside industries must accept the proposal

and shall invest the funds for greater returns in the business.

that for Hillside Industries, cost of debt is the useful component (Osma, Gomez-Conde & de las

Heras, 2018).

Question 5: Recommendation’s endorsement

From the overall analysis it is conclusive that the recommended plan shall be endorsed to

the Board of the directors. The reason behind such endorsement is that the entire analysis is in

favor of the selection of the proposal. Also the concept of the breakeven point has been divided

into four sections and the ultimate result states that the minimum units that are required are less

in case of the cash accounting breakeven point as it ignored the inclusion of depreciation. Due to

the positive net present value, higher internal rate of return and the payback period is less than

the term of the investment proposal; the company will have the higher growth and opportunities

in future. In the later half, the debt has been chosen as the method for expansion of the project

only because it is subjected to tax deductions as discussed above which will be helpful in

retaining the overall gain of the business. Since the boards of the directors were bewildered this

analysis will defiantly help them out. Henceforth, Hillside industries must accept the proposal

and shall invest the funds for greater returns in the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Running head: FINANCIAL MANAGEMENT

References

Andreasen, E., Schindler, M., & Valenzuela, P. (2019). Capital controls and the cost of

debt. IMF Economic Review, 67(2), 288-314.

Benamraoui, A., Jory, S. R., Boojihawon, D. R., & Madichie, N. O. (2017). Net Present Value

Analysis and the Wealth Creation Process: A Case Illustration. The Accounting

Educators' Journal, 26.

Frank, M. Z., & Shen, T. (2016). Investment and the weighted average cost of capital. Journal of

Financial Economics, 119(2), 300-315.

Kampf, R., Majerčák, P., & Švagr, P. (2016). Application of break-even point analysis. NAŠE

MORE: znanstveno-stručni časopis za more i pomorstvo, 63(3 Special Issue), 126-128.

Kim, S., Jang, H., Gao, R., Kim, C., Chung, Y., & Bang, S. (2017). Break-Even Point Analysis

of Sodium-Cooled Fast Reactor Capital Investment Cost Comparing the Direct Disposal

Option and Pyro-Sodium-Cooled Fast Reactor Nuclear Fuel Cycle Option in

Korea. Sustainability, 9(9), 1518.

Osma, B. G., Gomez-Conde, J., & de las Heras, E. (2018). Debt pressure and interactive use of

control systems: Effects on cost of debt. Management Accounting Research, 40, 27-46.

Roy, D., Rudra, D., & Prasad, P. (2017). Capital Structure and Capital Budgeting: An Empirical

and Analytical Study of the Relationship. Research Bulletin, 42(4), 50-60.

Singh, H. P., Kumar, S., & Colombage, S. (2017). Working capital management and firm

profitability: a meta-analysis. Qualitative Research in Financial Markets.

References

Andreasen, E., Schindler, M., & Valenzuela, P. (2019). Capital controls and the cost of

debt. IMF Economic Review, 67(2), 288-314.

Benamraoui, A., Jory, S. R., Boojihawon, D. R., & Madichie, N. O. (2017). Net Present Value

Analysis and the Wealth Creation Process: A Case Illustration. The Accounting

Educators' Journal, 26.

Frank, M. Z., & Shen, T. (2016). Investment and the weighted average cost of capital. Journal of

Financial Economics, 119(2), 300-315.

Kampf, R., Majerčák, P., & Švagr, P. (2016). Application of break-even point analysis. NAŠE

MORE: znanstveno-stručni časopis za more i pomorstvo, 63(3 Special Issue), 126-128.

Kim, S., Jang, H., Gao, R., Kim, C., Chung, Y., & Bang, S. (2017). Break-Even Point Analysis

of Sodium-Cooled Fast Reactor Capital Investment Cost Comparing the Direct Disposal

Option and Pyro-Sodium-Cooled Fast Reactor Nuclear Fuel Cycle Option in

Korea. Sustainability, 9(9), 1518.

Osma, B. G., Gomez-Conde, J., & de las Heras, E. (2018). Debt pressure and interactive use of

control systems: Effects on cost of debt. Management Accounting Research, 40, 27-46.

Roy, D., Rudra, D., & Prasad, P. (2017). Capital Structure and Capital Budgeting: An Empirical

and Analytical Study of the Relationship. Research Bulletin, 42(4), 50-60.

Singh, H. P., Kumar, S., & Colombage, S. (2017). Working capital management and firm

profitability: a meta-analysis. Qualitative Research in Financial Markets.

Running head: FINANCIAL MANAGEMENT

Sivaranjani, R., & Kishori, B. (2016). A Comparative Analysis of Working Capital Management

Among Top 5 NSE Listed Indian Steel Companies. International Journal for Innovative

Research in Science & Technology, 821-828.

Wang, B. (2019). The cash conversion cycle spread. Journal of Financial Economics, 133(2),

472-497.

Willigers, B. J., Jones, B., & Bratvold, R. B. (2017). The net-present-value paradox: Criticized

by many, applied by all. SPE Economics & Management, 9(04), 90-102.

Wisnubroto, P., & Suyanto, M. (2019). ANALISIS CAPITAL BUDGETING SEBAGAI

METODE MENILAI KELAYAKAN INVESTASI PERUSAHAAN. CIEHIS

Prosiding, 1(1), 48-58.

Sivaranjani, R., & Kishori, B. (2016). A Comparative Analysis of Working Capital Management

Among Top 5 NSE Listed Indian Steel Companies. International Journal for Innovative

Research in Science & Technology, 821-828.

Wang, B. (2019). The cash conversion cycle spread. Journal of Financial Economics, 133(2),

472-497.

Willigers, B. J., Jones, B., & Bratvold, R. B. (2017). The net-present-value paradox: Criticized

by many, applied by all. SPE Economics & Management, 9(04), 90-102.

Wisnubroto, P., & Suyanto, M. (2019). ANALISIS CAPITAL BUDGETING SEBAGAI

METODE MENILAI KELAYAKAN INVESTASI PERUSAHAAN. CIEHIS

Prosiding, 1(1), 48-58.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.