Financial Resource Management Report: Contract Analysis and Planning

VerifiedAdded on 2020/02/03

|18

|4521

|47

Report

AI Summary

This report analyzes the financial resources required for a 'Specialty Fine Food and Drink' contract in the UK. It explores both internal and external sources of finance, including retained earnings, sale of assets, owners' contributions, and loans. The report assesses the implications of each financial source, recommending a combination of owner investment, long-term loans, and bank overdrafts. It then delves into cost analysis, financial planning requirements, and the information needed by decision-makers. A cash budget is created, and investment appraisal techniques are used to assess the viability of the contract. Finally, the report examines financial statements, comparing different types of businesses and performing ratio analysis to evaluate financial performance, using J Sainsbury Plc as a case study. The report covers various aspects of financial management, including cost analysis, financial planning, cash flow management, and investment appraisal techniques.

MANAGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Financial sources...................................................................................................................1

1.2 Implications of financial sources..........................................................................................2

1.3 Appropriate financial source for Specialty Fine Food and Drink........................................3

TASK 2............................................................................................................................................3

2.1 Analysis of cost and identifying financial sources................................................................3

2.2 Requirements of financial planning......................................................................................4

2.3 Required information for decision makers............................................................................4

2.4 Justification of impact of finance on financial statements....................................................5

TASK 3............................................................................................................................................5

3.1 Cash budget and decision making.........................................................................................5

3.2 Unit cost and pricing decisions based on relevant information............................................7

3.3 Viability of contract through investment appraisal techniques.............................................7

TASK 4............................................................................................................................................8

4.1 Financial statements..............................................................................................................8

4.2 Comparison of financial statements in respect to different types of businesses...................9

4.3 Ratio analysis (Financial position's analysis)........................................................................9

CONCLUSION..............................................................................................................................12

REFERENCE.................................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Financial sources...................................................................................................................1

1.2 Implications of financial sources..........................................................................................2

1.3 Appropriate financial source for Specialty Fine Food and Drink........................................3

TASK 2............................................................................................................................................3

2.1 Analysis of cost and identifying financial sources................................................................3

2.2 Requirements of financial planning......................................................................................4

2.3 Required information for decision makers............................................................................4

2.4 Justification of impact of finance on financial statements....................................................5

TASK 3............................................................................................................................................5

3.1 Cash budget and decision making.........................................................................................5

3.2 Unit cost and pricing decisions based on relevant information............................................7

3.3 Viability of contract through investment appraisal techniques.............................................7

TASK 4............................................................................................................................................8

4.1 Financial statements..............................................................................................................8

4.2 Comparison of financial statements in respect to different types of businesses...................9

4.3 Ratio analysis (Financial position's analysis)........................................................................9

CONCLUSION..............................................................................................................................12

REFERENCE.................................................................................................................................13

INDEX OF TABLES

Table 1: Cash budget.......................................................................................................................5

Table 2: Projected Sales Budget......................................................................................................6

Table 3: Unit cost.............................................................................................................................7

Table 4: NPV for organisation.........................................................................................................7

Table 5: Ratio analysis.....................................................................................................................9

Table 1: Cash budget.......................................................................................................................5

Table 2: Projected Sales Budget......................................................................................................6

Table 3: Unit cost.............................................................................................................................7

Table 4: NPV for organisation.........................................................................................................7

Table 5: Ratio analysis.....................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Illustration Index

Illustration 1: Ratio analysis..........................................................................................................11

Illustration 1: Ratio analysis..........................................................................................................11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Management of the financial resources has been one of the most significant tasks over the

ages for entities for undertaking business activities successfully. The government of the United

Kingdom has put forward an arena of opportunities for the small business firms to work on the

contracts of the central government in the country. For the purpose of the given assignment, a

contract on ‘Specialty Fine Food and Drink’ has been chosen from the contract finder for

establishing entity. Further, analysis of the financial sources and implications and costs involved

in accessing the chosen financial sources have been presented in the assignment in order to

assess the overall impact on the financial statements. Financial budgets and investments

appraisal techniques are implemented to assess the viability of the chosen contract. In the last

section, an analysis of the financial statements of J Sainsbury Plc has been presented to evaluate

the financial performance of the company.

TASK 1

1.1 Financial sources

In order to undertake the contract of ‘Specialty Fine Food and Drink’ in the UK, it is

essential to assess availability of financial resources of the business. Initial investment will of £

200000. Therefore, the bid will not exceed £ 300000 for the chosen contract. With respect to the

financing context, the entrepreneur has £ 20000 to invest in the business. For the purpose of the

entrepreneurship business the different financial sources available are internal and external

sources of finance.

Internal Sources: The internal sources of finance have been identified as retained earnings,

saleable value of the assets and working capital for the business. Retained earnings are identified as an available source of finance for the business as it is

the profit used in the business after distributing the dividend to the shareholders or the

providing a return to the owners. Sale of assets: Another important internal source of financing for the business is the ‘sale

of assets’. The proceeds from the ‘sale of assets’ are usually used for funding the capital

requirements of the business (Armstrong et al. 2010).

1

Management of the financial resources has been one of the most significant tasks over the

ages for entities for undertaking business activities successfully. The government of the United

Kingdom has put forward an arena of opportunities for the small business firms to work on the

contracts of the central government in the country. For the purpose of the given assignment, a

contract on ‘Specialty Fine Food and Drink’ has been chosen from the contract finder for

establishing entity. Further, analysis of the financial sources and implications and costs involved

in accessing the chosen financial sources have been presented in the assignment in order to

assess the overall impact on the financial statements. Financial budgets and investments

appraisal techniques are implemented to assess the viability of the chosen contract. In the last

section, an analysis of the financial statements of J Sainsbury Plc has been presented to evaluate

the financial performance of the company.

TASK 1

1.1 Financial sources

In order to undertake the contract of ‘Specialty Fine Food and Drink’ in the UK, it is

essential to assess availability of financial resources of the business. Initial investment will of £

200000. Therefore, the bid will not exceed £ 300000 for the chosen contract. With respect to the

financing context, the entrepreneur has £ 20000 to invest in the business. For the purpose of the

entrepreneurship business the different financial sources available are internal and external

sources of finance.

Internal Sources: The internal sources of finance have been identified as retained earnings,

saleable value of the assets and working capital for the business. Retained earnings are identified as an available source of finance for the business as it is

the profit used in the business after distributing the dividend to the shareholders or the

providing a return to the owners. Sale of assets: Another important internal source of financing for the business is the ‘sale

of assets’. The proceeds from the ‘sale of assets’ are usually used for funding the capital

requirements of the business (Armstrong et al. 2010).

1

Working capital: Reduction in the working capital requirement by the adjusting the

account payables or account receivables ensures reduction in working capital obligation

and therefore, the funds meant for working capital can be employed for other financing

obligations.

External Sources: The external sources of finance available to a business are owners’

contribution, bank overdrafts, trade creditors and long term loan. Owners’ contribution: It has been identified as the money invested by the owner or the

shareholders’ in order to commence and continue the business. Bank overdraft: It is a source of funding provided by the banks in order to fund the short

term obligations of a business (Beyer and et.al., 2010). The persons that provide business

materials on credit basis have been identified as trade creditors and are a source of

external business funding.

Long term loans: provided by the banks or the financial institutions are a source of

external funding requiring the business to payback the principal amount with interest on

maturity.

1.2 Implications of financial sources

The internal sources of finance have multiple insinuations in the form of advantages and

limitations. The benefits of accessing the internal sources of finance are immediate availability of

capital, absence of interest payments at regular intervals and controlling procedures with respect

to creditworthiness of the business. Other benefits are, third party influence is not present giving

the owners more flexibility and freedom to pursue the business (Brigham and Ehrhardt, 2013).

However, certain limitations of the internal sources of finance are absence of tax benefits and

limited capital expansion.

Implications of the external sources: Through the use of external sources of funding,

businesses are provided with the opportunity of investing the internal sources of finance in other

profitable business investments providing higher return. In addition, access to external financing

sources provides growth opportunities that the business would not be able to fund on its own.

However, the limitation of external funding is dilution of ownership and the fixed interest

payments to be provided to the investors.

2

account payables or account receivables ensures reduction in working capital obligation

and therefore, the funds meant for working capital can be employed for other financing

obligations.

External Sources: The external sources of finance available to a business are owners’

contribution, bank overdrafts, trade creditors and long term loan. Owners’ contribution: It has been identified as the money invested by the owner or the

shareholders’ in order to commence and continue the business. Bank overdraft: It is a source of funding provided by the banks in order to fund the short

term obligations of a business (Beyer and et.al., 2010). The persons that provide business

materials on credit basis have been identified as trade creditors and are a source of

external business funding.

Long term loans: provided by the banks or the financial institutions are a source of

external funding requiring the business to payback the principal amount with interest on

maturity.

1.2 Implications of financial sources

The internal sources of finance have multiple insinuations in the form of advantages and

limitations. The benefits of accessing the internal sources of finance are immediate availability of

capital, absence of interest payments at regular intervals and controlling procedures with respect

to creditworthiness of the business. Other benefits are, third party influence is not present giving

the owners more flexibility and freedom to pursue the business (Brigham and Ehrhardt, 2013).

However, certain limitations of the internal sources of finance are absence of tax benefits and

limited capital expansion.

Implications of the external sources: Through the use of external sources of funding,

businesses are provided with the opportunity of investing the internal sources of finance in other

profitable business investments providing higher return. In addition, access to external financing

sources provides growth opportunities that the business would not be able to fund on its own.

However, the limitation of external funding is dilution of ownership and the fixed interest

payments to be provided to the investors.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.3 Appropriate financial source for Specialty Fine Food and Drink

Regarding business project undertaken through the contract named, ‘Specialty Fine Food

and Drink’ it is observed that the suitable financial sources for the business project will be in the

form of external and internal sources. External sources in the form of Owners contribution, long

term loans, bank overdraft and trade creditors are recommended for the business. Owners

contribution to the extent of £ 20000 will be provided in the business. The remaining capital will

be financed through long term loans availed from the banks and financial institutions as the

business do not have a very high contribution from the entrepreneur (Gov.uk. 2017). For the

purpose of the long term loans the business the loan will be secured by the asset to be purchased

with the loan amount identified as ‘primary security’. The loan has been identified as a fixed

obligation for the business. ‘Bank overdraft’ facilities should be implemented as external sources

of finance in order to cater the short term funding requirements.

The internal sources of financing to be availed by the business should be in the form of

retained earnings, using personal savings and sale of assets. By using the earnings of the

company as a source of finance the business will be able to generate increased level of

operational flexibility and freedom (Broadbent and Cullen, 2012). In addition, various explicit

cost in the form of floatation cost, interest and dividend are not present. Through efficient

management of the working capital cycle the funds can be utilized for other business needs. In

order to cater certain long term finance needs the business may sell off certain assets or

equipments used in the business previously but not in use in the current scenario for the purpose

of undertaking investments in the business.

TASK 2

2.1 Analysis of cost and identifying financial sources

Through ages it has been observed that the lifeline of any business have been identified

as the ‘capital’ for the business. For obtaining the capital for the business it is important to

identify and assess the costs associated with the sources of financing. With respect to the internal

sources of financing it has been observed that in case of retained earnings certain amount of

opportunity costs are present. Financing through sale of assets involves the costs of repairing and

maintaining the assets and the cost of depreciation. In context to the external sources of finance,

the costs associated with the owners or shareholders contribution are in the form of dividend paid

3

Regarding business project undertaken through the contract named, ‘Specialty Fine Food

and Drink’ it is observed that the suitable financial sources for the business project will be in the

form of external and internal sources. External sources in the form of Owners contribution, long

term loans, bank overdraft and trade creditors are recommended for the business. Owners

contribution to the extent of £ 20000 will be provided in the business. The remaining capital will

be financed through long term loans availed from the banks and financial institutions as the

business do not have a very high contribution from the entrepreneur (Gov.uk. 2017). For the

purpose of the long term loans the business the loan will be secured by the asset to be purchased

with the loan amount identified as ‘primary security’. The loan has been identified as a fixed

obligation for the business. ‘Bank overdraft’ facilities should be implemented as external sources

of finance in order to cater the short term funding requirements.

The internal sources of financing to be availed by the business should be in the form of

retained earnings, using personal savings and sale of assets. By using the earnings of the

company as a source of finance the business will be able to generate increased level of

operational flexibility and freedom (Broadbent and Cullen, 2012). In addition, various explicit

cost in the form of floatation cost, interest and dividend are not present. Through efficient

management of the working capital cycle the funds can be utilized for other business needs. In

order to cater certain long term finance needs the business may sell off certain assets or

equipments used in the business previously but not in use in the current scenario for the purpose

of undertaking investments in the business.

TASK 2

2.1 Analysis of cost and identifying financial sources

Through ages it has been observed that the lifeline of any business have been identified

as the ‘capital’ for the business. For obtaining the capital for the business it is important to

identify and assess the costs associated with the sources of financing. With respect to the internal

sources of financing it has been observed that in case of retained earnings certain amount of

opportunity costs are present. Financing through sale of assets involves the costs of repairing and

maintaining the assets and the cost of depreciation. In context to the external sources of finance,

the costs associated with the owners or shareholders contribution are in the form of dividend paid

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to the shareholders (Katz and Green, 2009). The costs involved in the long term bank loans are in

the form of interest payments that is required to be paid through instalments along with the

principal amount. In addition, in order to avail the bank loan the business is required to provide a

guarantee or security to the bank so that in the event of any failure to repay the loan amount the

bank can exercises ownership on the property secured against the loan.

2.2 Requirements of financial planning

Financial planning is identified as the process of analysing and setting up a detailed

course of action in order to undertake and perform the financial activities involved in a business.

Financial planning helps in managing the income and expenditure of the business effectively

thereby monitoring the cash outflows and inflows of the entity successfully. By increasing the

cash flow the business is able to generate higher amount of capital and investments for itself.

Thereby, resulting in overall improvement of the financial position of the business. Financial

planning helps in assessing the liabilities associated with a particular set of assets and improve

the liquidity position of the business (Siano and et.al., 2010). For the business project under

consideration, appropriate financial planning in the form of assessment of the available financial

resources, projected budgets, implementation of investment appraisal techniques and analysis of

the costs have been undertaken in order to formulate a suitable business plan for the project.

Through the analysis of the costs the expenditure to be incurred by the business are determined.

Formulation and analysis of the projected budget helps in determining the expected expenditure

and income of the business in the future (Sullivan, 2009). Through investment appraisal

techniques the viability of the contract undertaken is determined in order to assess the

investments options in the future.

2.3 Required information for decision makers

For the purpose of pursuing the business activities successfully, the internal and external

decision makers of the business require diverse form of financial information. The internal

decision makers in the form of the management, owners and the employees require financial

information in order to undertake the activities of the planning, scheming, controlling and

decision making process. The internal decision makers require financial information in the form

of accounting information and managerial information (Lusardi, 2012). The external decision

makers comprising creditors, customers, investors and regulatory authorities require information

for the purpose of investing in the company, availing the services of the company and protecting

4

the form of interest payments that is required to be paid through instalments along with the

principal amount. In addition, in order to avail the bank loan the business is required to provide a

guarantee or security to the bank so that in the event of any failure to repay the loan amount the

bank can exercises ownership on the property secured against the loan.

2.2 Requirements of financial planning

Financial planning is identified as the process of analysing and setting up a detailed

course of action in order to undertake and perform the financial activities involved in a business.

Financial planning helps in managing the income and expenditure of the business effectively

thereby monitoring the cash outflows and inflows of the entity successfully. By increasing the

cash flow the business is able to generate higher amount of capital and investments for itself.

Thereby, resulting in overall improvement of the financial position of the business. Financial

planning helps in assessing the liabilities associated with a particular set of assets and improve

the liquidity position of the business (Siano and et.al., 2010). For the business project under

consideration, appropriate financial planning in the form of assessment of the available financial

resources, projected budgets, implementation of investment appraisal techniques and analysis of

the costs have been undertaken in order to formulate a suitable business plan for the project.

Through the analysis of the costs the expenditure to be incurred by the business are determined.

Formulation and analysis of the projected budget helps in determining the expected expenditure

and income of the business in the future (Sullivan, 2009). Through investment appraisal

techniques the viability of the contract undertaken is determined in order to assess the

investments options in the future.

2.3 Required information for decision makers

For the purpose of pursuing the business activities successfully, the internal and external

decision makers of the business require diverse form of financial information. The internal

decision makers in the form of the management, owners and the employees require financial

information in order to undertake the activities of the planning, scheming, controlling and

decision making process. The internal decision makers require financial information in the form

of accounting information and managerial information (Lusardi, 2012). The external decision

makers comprising creditors, customers, investors and regulatory authorities require information

for the purpose of investing in the company, availing the services of the company and protecting

4

the interests of the stakeholders of the business. The creditors of the business need accounting

information in order to assess the credit worthiness of the entity.

2.4 Justification of impact of finance on financial statements

The main reason behind preparing and presenting the financial statements are the sources

and the activities related to financing. In order to identify, assess and analyse the performance of

the financing options undertaken the financial statements are prepared (Santos and Elliott, 2012).

Any form of increase or decrease in the finance availed in the business directly creates an impact

on the financial statements of the entity.

Influence on the financial statement by the various identified sources of

finance: Finance and financing activities have a significant or major amount of impact on the

financial statements of an entity. Different activities of financing have concurrent impact on the

financial statements of the enterprise as; income statement, profit and loss account, fund flow

and the cash flow statements etc. It has been observed that items or components such as sales,

capital of the owner, expenses, cost and borrowings creates an impact on the financial

statements. As and when companies undertake transactions simultaneously the items of the

financial statements are affected. Taking the items of the income statement and the balance sheet

an analysis is presented henceforth (Hoitash et al. 2009). When a business undertakes the

activities related to sales, the income statement is directly affected thereby increasing the revenue

and net profit of the entity. On the balance sheet the revenue generated in the income statement is

reflected through the accounts receivables. Financing activities in the form of capital generation

through issue of shares are reflected in the balance sheet while the dividend provided to the

investors from the profit generated creates an impact on the income statement by decreasing the

retained profits.

TASK 3

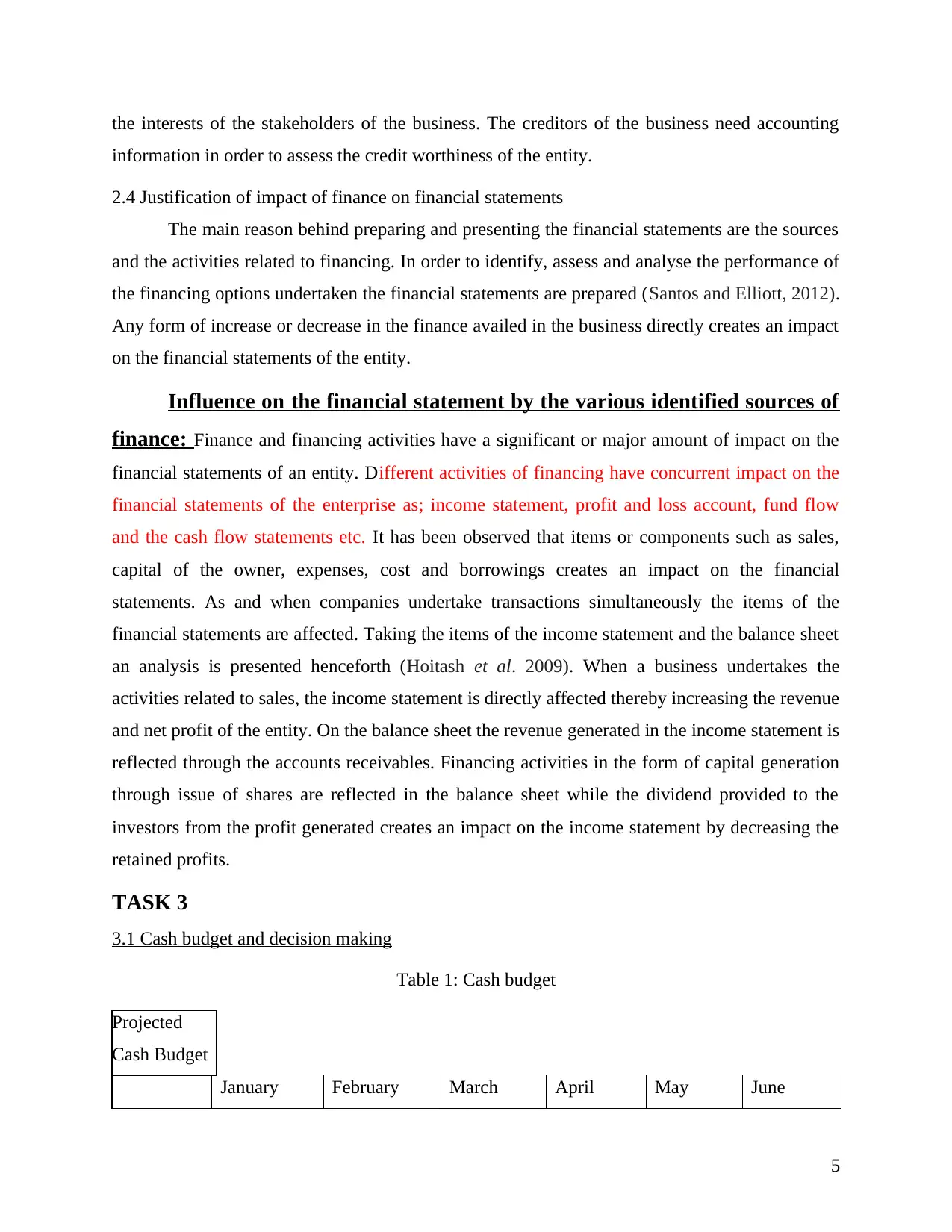

3.1 Cash budget and decision making

Table 1: Cash budget

Projected

Cash Budget

January February March April May June

5

information in order to assess the credit worthiness of the entity.

2.4 Justification of impact of finance on financial statements

The main reason behind preparing and presenting the financial statements are the sources

and the activities related to financing. In order to identify, assess and analyse the performance of

the financing options undertaken the financial statements are prepared (Santos and Elliott, 2012).

Any form of increase or decrease in the finance availed in the business directly creates an impact

on the financial statements of the entity.

Influence on the financial statement by the various identified sources of

finance: Finance and financing activities have a significant or major amount of impact on the

financial statements of an entity. Different activities of financing have concurrent impact on the

financial statements of the enterprise as; income statement, profit and loss account, fund flow

and the cash flow statements etc. It has been observed that items or components such as sales,

capital of the owner, expenses, cost and borrowings creates an impact on the financial

statements. As and when companies undertake transactions simultaneously the items of the

financial statements are affected. Taking the items of the income statement and the balance sheet

an analysis is presented henceforth (Hoitash et al. 2009). When a business undertakes the

activities related to sales, the income statement is directly affected thereby increasing the revenue

and net profit of the entity. On the balance sheet the revenue generated in the income statement is

reflected through the accounts receivables. Financing activities in the form of capital generation

through issue of shares are reflected in the balance sheet while the dividend provided to the

investors from the profit generated creates an impact on the income statement by decreasing the

retained profits.

TASK 3

3.1 Cash budget and decision making

Table 1: Cash budget

Projected

Cash Budget

January February March April May June

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Amount £) (Amount £) (Amount £)

(Amount

£)

(Amount

£)

(Amount

£)

Opening

Balance 1000 -4680 -3160 -1540 180 1650

Income

Cash Sales 4000 4700 4900 4800 5000 5200

Credit

Sales nil 700 900 800 400 500

Loan 7000 nil nil nil nil nil

Total

Income 11000 5400 5800 5600 5400 5700

Expenditu

re

Rent 800 800 800 800 800 800

Electricity 80 80 80 80 30 30

Purchases 5600 1900 2000 1800 1900 1800

Wages 1200 1100 1300 1200 1200 1200

Equipment

s 9000 nil nil nil nil nil

Total

expenditur

e 16680 3880 4180 3880 3930 3830

Net Cash

flow -5680 1520 1620 1720 1470 1870

Closing

Balance -4680 -3160 -1540 180 1650 3520

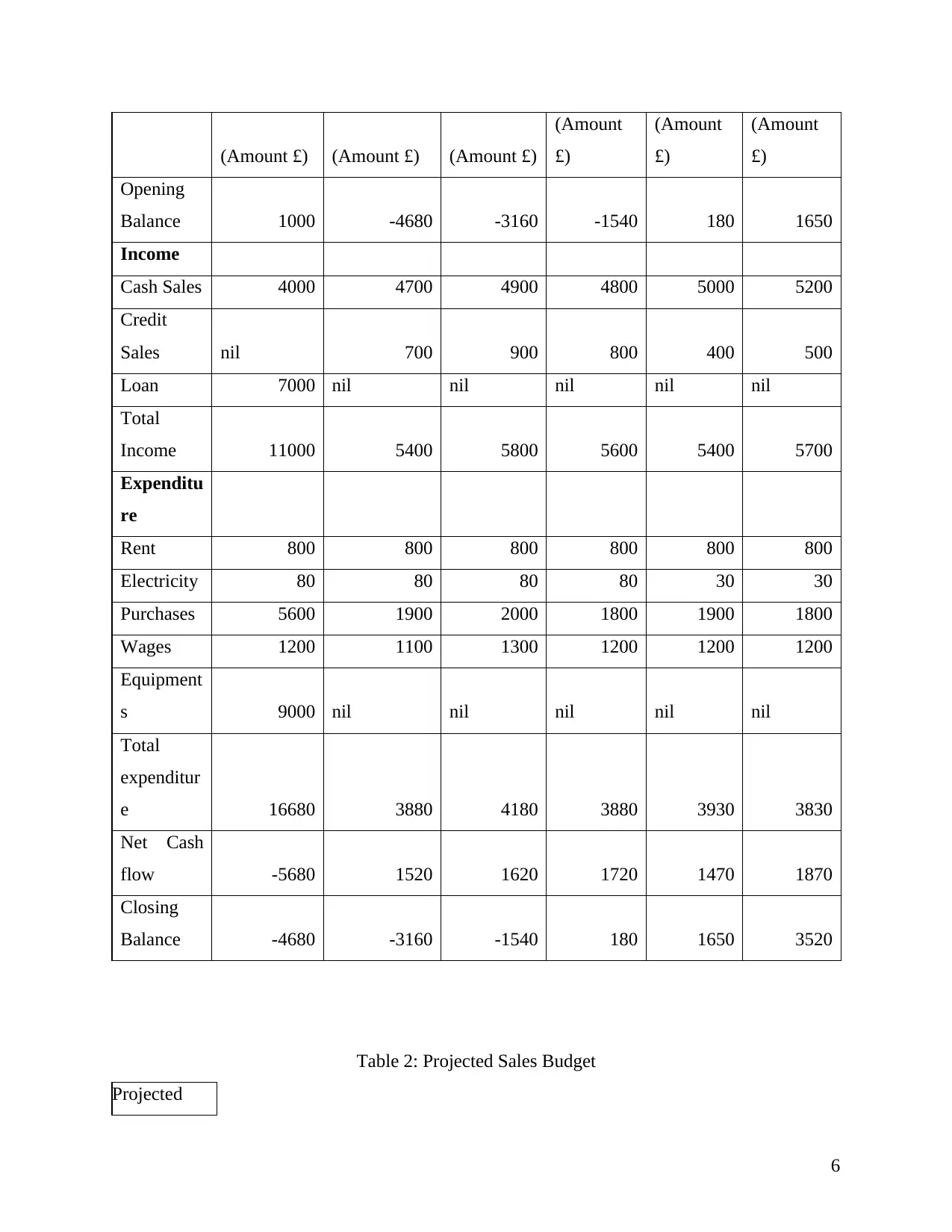

Table 2: Projected Sales Budget

Projected

6

(Amount

£)

(Amount

£)

(Amount

£)

Opening

Balance 1000 -4680 -3160 -1540 180 1650

Income

Cash Sales 4000 4700 4900 4800 5000 5200

Credit

Sales nil 700 900 800 400 500

Loan 7000 nil nil nil nil nil

Total

Income 11000 5400 5800 5600 5400 5700

Expenditu

re

Rent 800 800 800 800 800 800

Electricity 80 80 80 80 30 30

Purchases 5600 1900 2000 1800 1900 1800

Wages 1200 1100 1300 1200 1200 1200

Equipment

s 9000 nil nil nil nil nil

Total

expenditur

e 16680 3880 4180 3880 3930 3830

Net Cash

flow -5680 1520 1620 1720 1470 1870

Closing

Balance -4680 -3160 -1540 180 1650 3520

Table 2: Projected Sales Budget

Projected

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales Budget

January

(Amount £)

February

(Amount £)

March

(Amount

£)

April

(Amount

£)

May

(Amount

£)

June

(Amount

£)

Units 500 510 520 530 550 550

Sales Price 8 10.59 11.15 10.57 9.82 10.36

Cash Sales 4000 4700 4900 4800 5000 5200

Credit Sales nil 700 900 800 400 500

Total

Estimated

Sales 4000 5400 5800 5600 5400 5700

3.2 Unit cost and pricing decisions based on relevant information

Table 3: Unit cost

Calculation of Unit cost

Item (Amount £)

Steak 2

Vegetables and other ingredients 1

Labour 2.5

Overheads 2

Cost of meal 7.5

Mark up cost (20%) 1.5

Vat (20%) 1.5

Price of meal 10.5

Depending on the cost determined the pricing decision has to be undertaken. In the

current context, ‘mark up pricing’ have been undertaken to determine the average price of the

meals to be provided by the ‘Specialty Fine Food and Drink’ business.

7

January

(Amount £)

February

(Amount £)

March

(Amount

£)

April

(Amount

£)

May

(Amount

£)

June

(Amount

£)

Units 500 510 520 530 550 550

Sales Price 8 10.59 11.15 10.57 9.82 10.36

Cash Sales 4000 4700 4900 4800 5000 5200

Credit Sales nil 700 900 800 400 500

Total

Estimated

Sales 4000 5400 5800 5600 5400 5700

3.2 Unit cost and pricing decisions based on relevant information

Table 3: Unit cost

Calculation of Unit cost

Item (Amount £)

Steak 2

Vegetables and other ingredients 1

Labour 2.5

Overheads 2

Cost of meal 7.5

Mark up cost (20%) 1.5

Vat (20%) 1.5

Price of meal 10.5

Depending on the cost determined the pricing decision has to be undertaken. In the

current context, ‘mark up pricing’ have been undertaken to determine the average price of the

meals to be provided by the ‘Specialty Fine Food and Drink’ business.

7

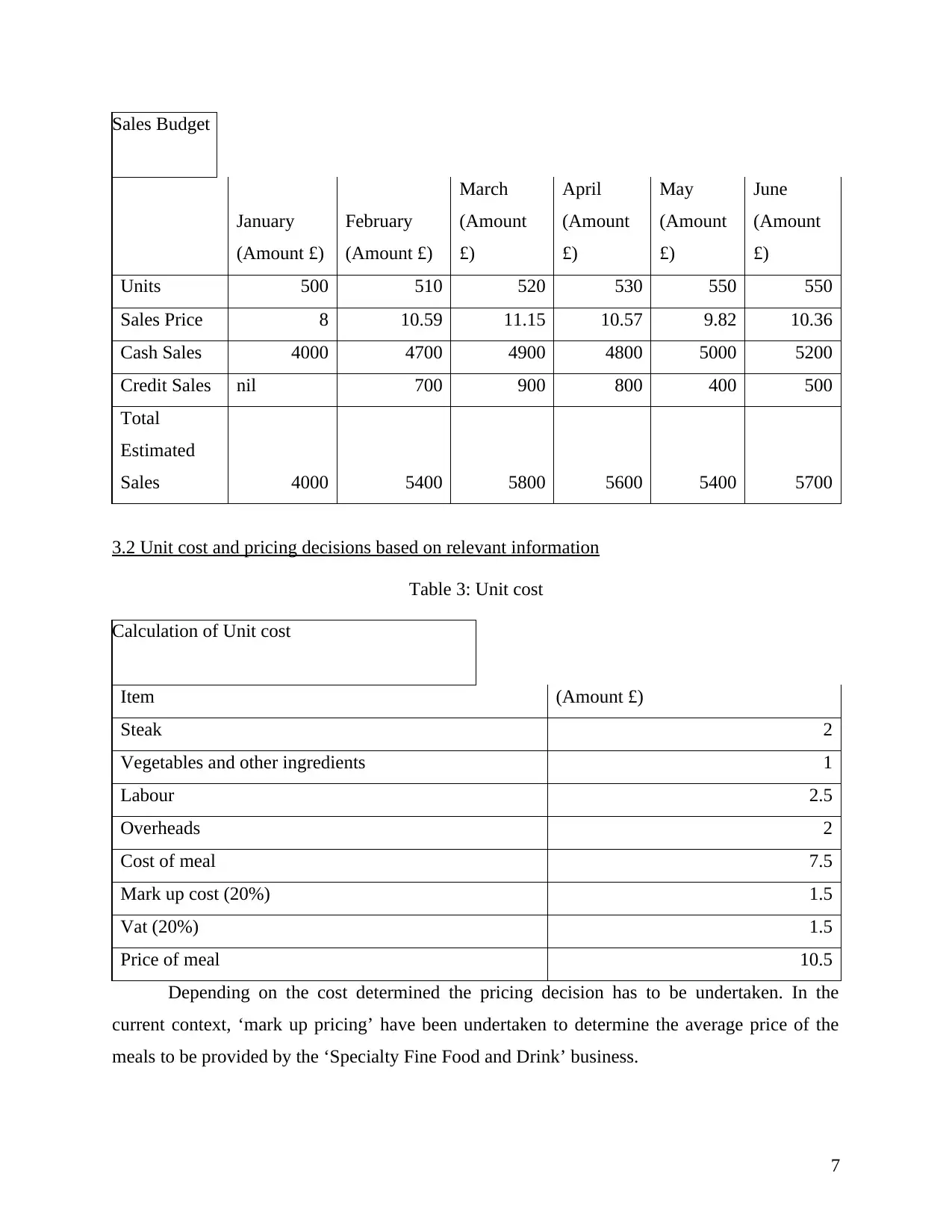

3.3 Viability of contract through investment appraisal techniques

Table 4: NPV for organisation

Year Cash inflows (In pound) Discounting factor @ 10% Present value of cash inflow

0 -2000000 1 -2000000

1 650000 0.909 590850

2 550000 0.826 454300

3 350000 0.751 262850

4 480000 0.683 327840

5 455000 0.621 282555

6 255000 0.564 143820

Total Present value from cash flows 2

0

6

2

2

1

5

Less: Initial Investment 2000000

Net Present Value 62215

Interpretation: As per the initial investment to be made in the project the cash inflows

of the 6 years have been presented along with the Net Present Value of the project which is £

62215.

TASK 4

4.1 Financial statements

Cash flow statement: In order to evaluate the liquidity position and leverage of an

organization, statement of cash flow should have to be prepared by the financial analyst

for interpreting the financial result appropriately. Main factors of this financial statement

8

Table 4: NPV for organisation

Year Cash inflows (In pound) Discounting factor @ 10% Present value of cash inflow

0 -2000000 1 -2000000

1 650000 0.909 590850

2 550000 0.826 454300

3 350000 0.751 262850

4 480000 0.683 327840

5 455000 0.621 282555

6 255000 0.564 143820

Total Present value from cash flows 2

0

6

2

2

1

5

Less: Initial Investment 2000000

Net Present Value 62215

Interpretation: As per the initial investment to be made in the project the cash inflows

of the 6 years have been presented along with the Net Present Value of the project which is £

62215.

TASK 4

4.1 Financial statements

Cash flow statement: In order to evaluate the liquidity position and leverage of an

organization, statement of cash flow should have to be prepared by the financial analyst

for interpreting the financial result appropriately. Main factors of this financial statement

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.