Financial Management Project Report, Analysis, and Valuation

VerifiedAdded on 2021/09/10

|13

|3807

|38

Project

AI Summary

This project report delves into critical aspects of financial management, encompassing a comprehensive analysis of capital budgeting techniques, valuation models, and market efficiency. The report begins by evaluating investment proposals using payback period and net present value (NPV) calculations for two machinery options, comparing their profitability and payback timelines. It then explores the implications of financial leasing versus purchasing, recalculating NPV and payback periods to determine the optimal financial strategy. The report further examines operating and financial leases, differentiating between their characteristics and applications. A comparative analysis of P/E ratios and dividend yields for two companies is conducted, considering the impact of financial gearing and shareholder considerations. Task B involves valuation analysis, applying dividend discount, P/E, and net asset valuation models to estimate a company's stock price, followed by a discussion of the strengths, weaknesses, and suitability of each model. Finally, the report addresses the efficient market hypothesis (EMH), outlining its weak, semi-strong, and strong forms and their implications for investment decisions.

Running Head: Financial Management

1

Project Report: Financial Management

1

Project Report: Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management

2

Contents

Task A...............................................................................................................................3

Question 1.....................................................................................................................3

Question 2.....................................................................................................................3

Question 3.....................................................................................................................4

Question 4.....................................................................................................................4

Task B...............................................................................................................................6

Question 1.....................................................................................................................6

Question 2.....................................................................................................................6

Question 3.....................................................................................................................7

Question 4.....................................................................................................................8

References.........................................................................................................................9

Appendix.........................................................................................................................10

2

Contents

Task A...............................................................................................................................3

Question 1.....................................................................................................................3

Question 2.....................................................................................................................3

Question 3.....................................................................................................................4

Question 4.....................................................................................................................4

Task B...............................................................................................................................6

Question 1.....................................................................................................................6

Question 2.....................................................................................................................6

Question 3.....................................................................................................................7

Question 4.....................................................................................................................8

References.........................................................................................................................9

Appendix.........................................................................................................................10

Financial Management

3

Task A:

Question 1:

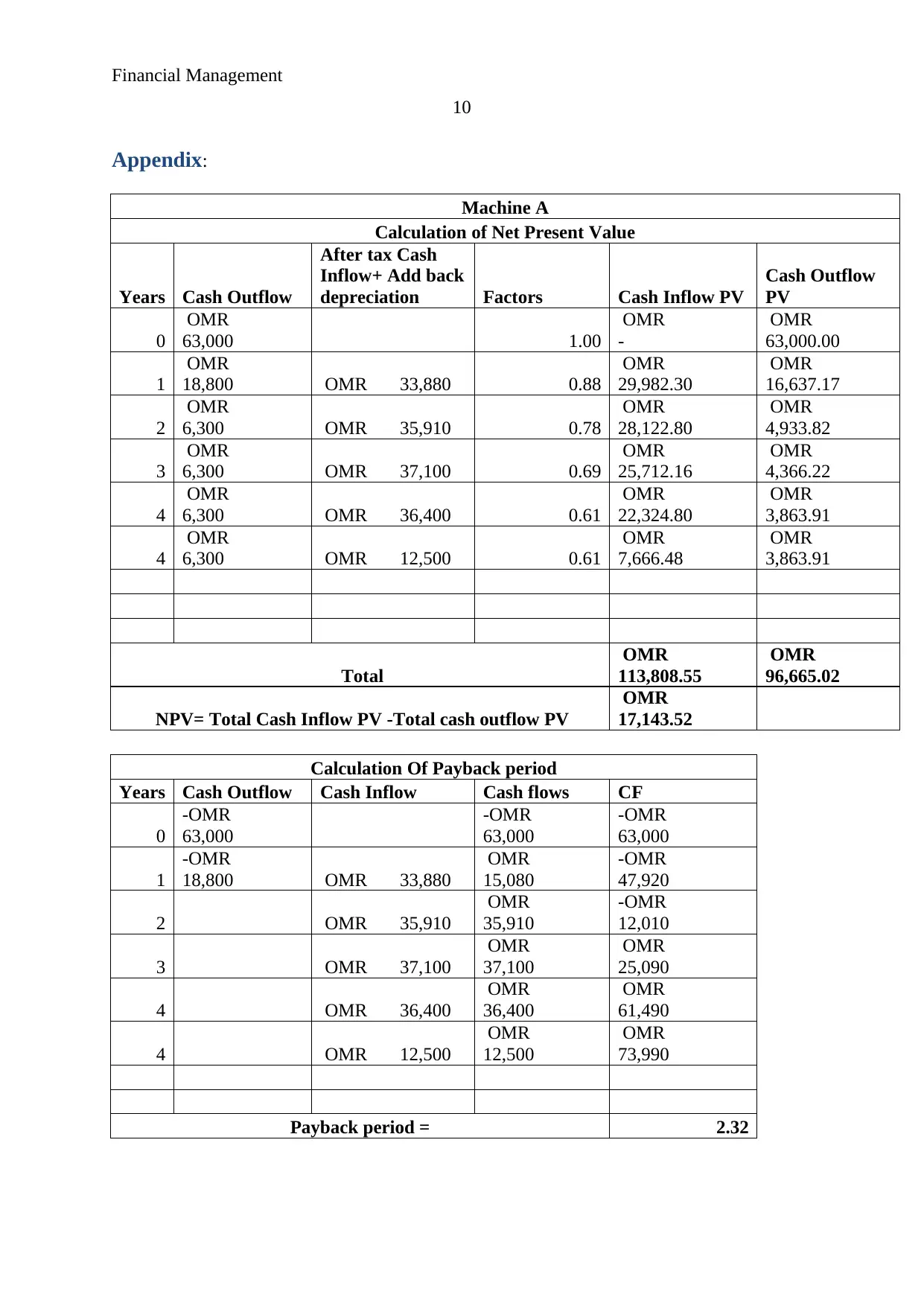

Calculation of payback period and net present values:

On the basis of the given case, the capital budgeting techniques have been applied on

both the companies in order to evaluate the best option for company’s growth and

profitability position. Payback period and net present value of the company has been

calculated to measure the best investment proposal for the company. On the basis of

calculation on machine A, it has been found that the NPV of machine A is OMR 17,143.52. It

depicts that the net present value of machinery is positive and explains that it would offer

better return to the company. As well as, the payback period of machinery A is 2.32 years

which depicts that the invested amount would be got back by the company in 2.23 years. Rest

the period, company would be able to make new profits (Higgins, 2012).

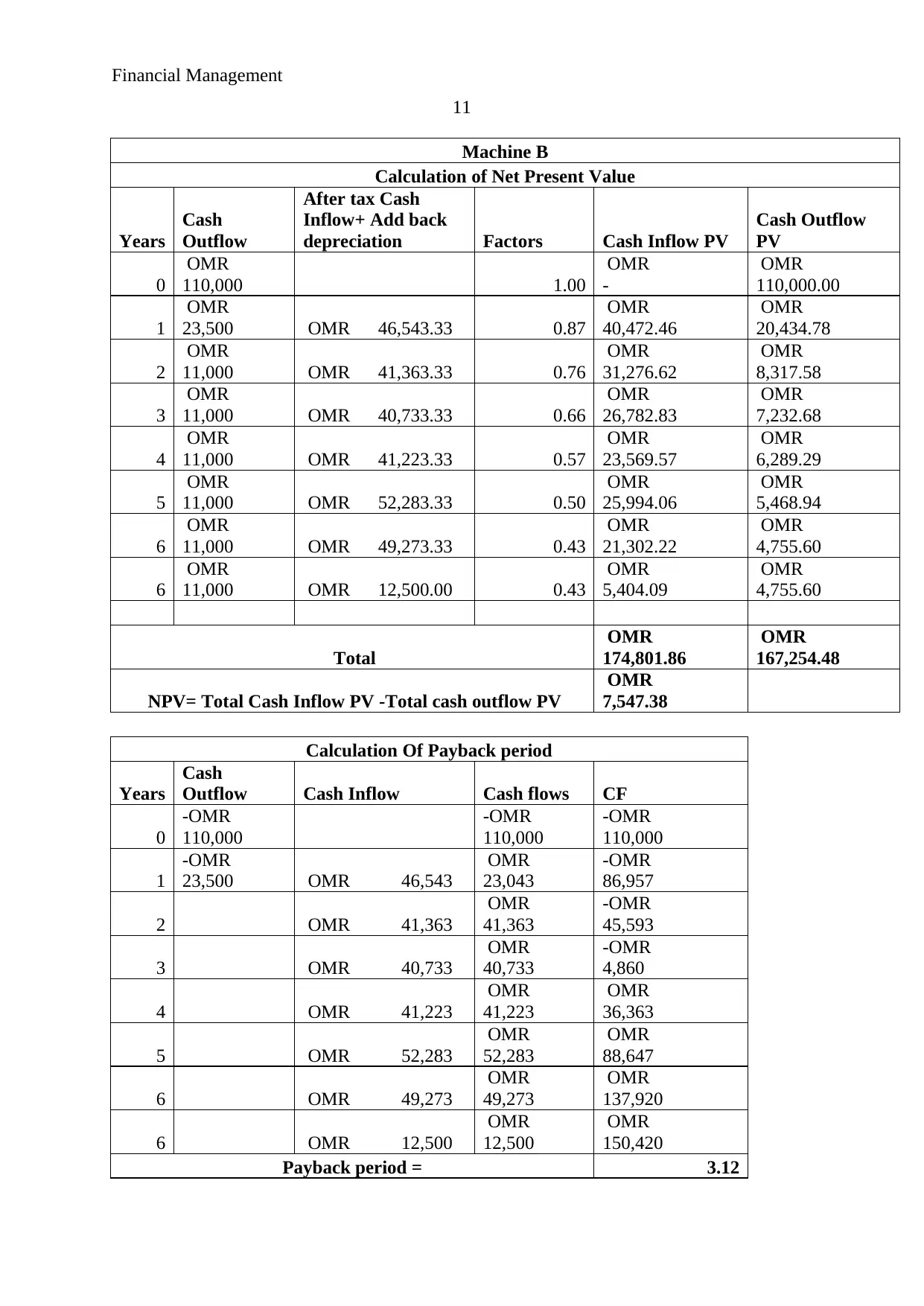

Further, the same calculations have been done on Machinery B in order to identify the

performance of Machinery B and compare it with Machinery A. On the basis of calculation

on machine B, it has been found that the NPV of machine B is OMR 7,547.38. It depicts that

the net present value of machinery is positive and explains that it would offer better return to

the company. As well as, the payback period of machinery B is 3.12 years which depicts that

the invested amount would be got back by the company in 3.12 years. Rest the period,

company would be able to make new profits (Kelly, 2012).

On the basis of the comparison study, it has been recognized that the machinery A is

better than Machinery B in terms of the net profit as well as the total time period in which, it

would be easier for the management of the company to get back the total invested amount

through the cash inflows. The calculations of both the machineries have been given in the

appendix.

Question 2:

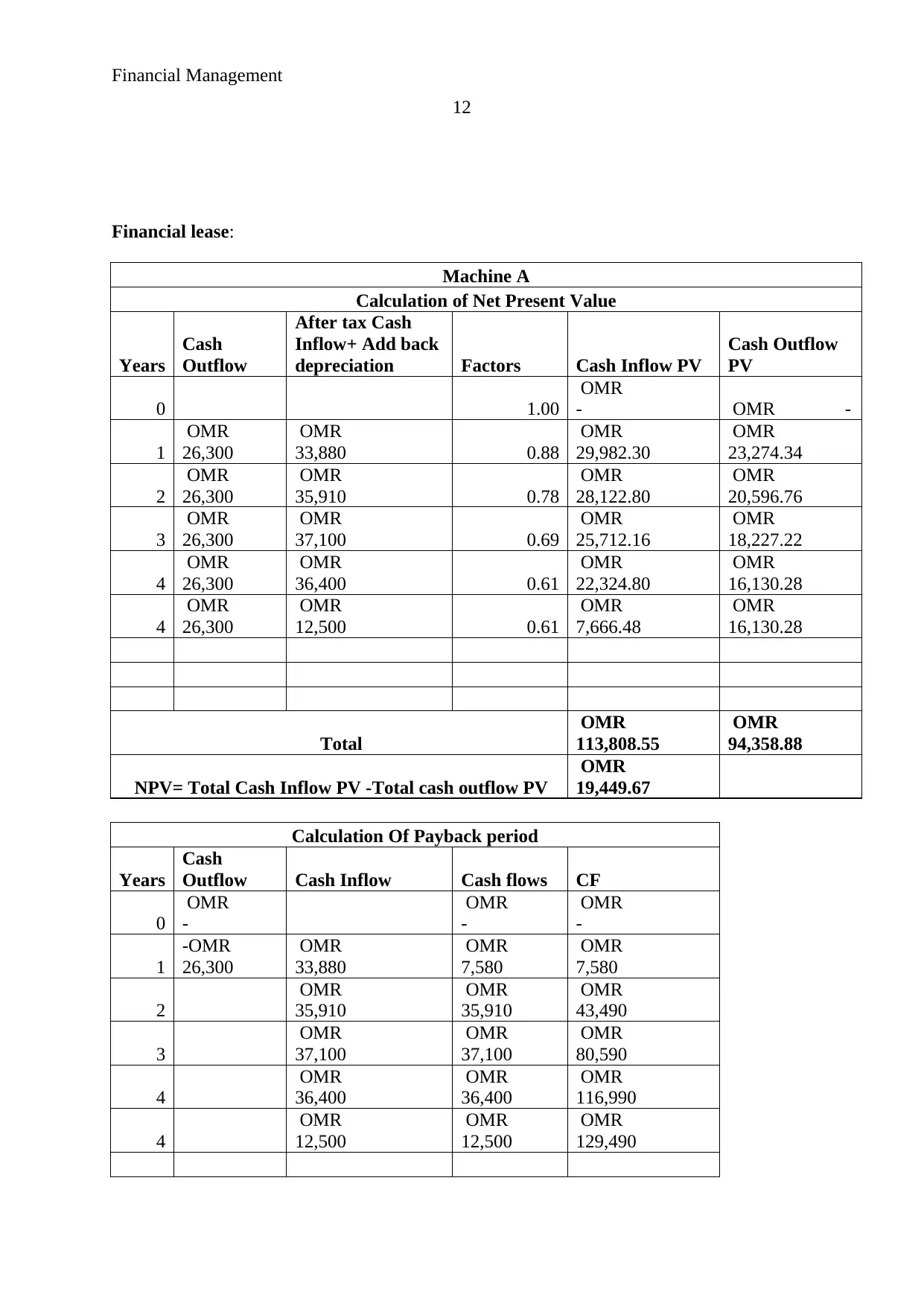

If according to the case, the machinery A is taken on finance lease than the outflow of

the company will be changed and it would affect on the capital budgeting decisions of the

company. On the basis of the calculations, it has been measured that whether the business

should take the machinery on lease or should but it. The capital budgeting techniques have

3

Task A:

Question 1:

Calculation of payback period and net present values:

On the basis of the given case, the capital budgeting techniques have been applied on

both the companies in order to evaluate the best option for company’s growth and

profitability position. Payback period and net present value of the company has been

calculated to measure the best investment proposal for the company. On the basis of

calculation on machine A, it has been found that the NPV of machine A is OMR 17,143.52. It

depicts that the net present value of machinery is positive and explains that it would offer

better return to the company. As well as, the payback period of machinery A is 2.32 years

which depicts that the invested amount would be got back by the company in 2.23 years. Rest

the period, company would be able to make new profits (Higgins, 2012).

Further, the same calculations have been done on Machinery B in order to identify the

performance of Machinery B and compare it with Machinery A. On the basis of calculation

on machine B, it has been found that the NPV of machine B is OMR 7,547.38. It depicts that

the net present value of machinery is positive and explains that it would offer better return to

the company. As well as, the payback period of machinery B is 3.12 years which depicts that

the invested amount would be got back by the company in 3.12 years. Rest the period,

company would be able to make new profits (Kelly, 2012).

On the basis of the comparison study, it has been recognized that the machinery A is

better than Machinery B in terms of the net profit as well as the total time period in which, it

would be easier for the management of the company to get back the total invested amount

through the cash inflows. The calculations of both the machineries have been given in the

appendix.

Question 2:

If according to the case, the machinery A is taken on finance lease than the outflow of

the company will be changed and it would affect on the capital budgeting decisions of the

company. On the basis of the calculations, it has been measured that whether the business

should take the machinery on lease or should but it. The capital budgeting techniques have

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management

4

been applied again on both the choices and it has been recognized that the overall outcome of

the machinery would be changed.

On the basis of calculation on machine a (financial lease), it has been found that the

NPV of machine A would be OMR 19,449.67. It depicts that the net present value of

machinery is positive and explains that it would offer better return to the company. As well

as, the payback period of machinery A is 0.83 years which depicts that the invested amount

would be got back by the company in 0.83 years. Rest the period, company would be able to

make new profits.

On the basis of the comparison study, it has been recognized that the machinery A on

lease is better option than buy of machinery A in terms of the net profit as well as the total

time period in which, it would be easier for the management of the company to get back the

total invested amount through the cash inflows (Krantz, 2016). The calculations of both the

machineries have been given in the appendix.

Question 3:

Operating and financial lease as a source of finance:

Operating lease and financial lease are the part of lease which is chosen by the

company on the basis of their requirement. In case of operating lease, when a company needs

any equipment for short time period than it is a better option. The leasing company give the

equipment for short term period in consideration with lease rent and then they wish to sell it

out as second hand after leasing period to other party. On operating lease, equipment is leased

by the company for 2-3 periods which is lesser than the actual time period of the machinery.

This kind of assets are not shown in the balance sheet of the company instead of it, the entire

lease cost of the machineries is shown in the income statement of the company on

expenditure side (Kinsky, 2011).

Whereas, in case of financial lease, it has been found that this lease is the alternative

of hire purchase in which the leasing company recovers the total cost of the machinery from

the company who has taken the equipment on lease. In this case, the company does not own

the machinery but most of the risk and rewards are hold by the leased company. The

company is holding responsible for insuring the assets, maintaining the assets etc. After the

end of the lease time period, business can sold it as second hand property (Madura, 2014).

4

been applied again on both the choices and it has been recognized that the overall outcome of

the machinery would be changed.

On the basis of calculation on machine a (financial lease), it has been found that the

NPV of machine A would be OMR 19,449.67. It depicts that the net present value of

machinery is positive and explains that it would offer better return to the company. As well

as, the payback period of machinery A is 0.83 years which depicts that the invested amount

would be got back by the company in 0.83 years. Rest the period, company would be able to

make new profits.

On the basis of the comparison study, it has been recognized that the machinery A on

lease is better option than buy of machinery A in terms of the net profit as well as the total

time period in which, it would be easier for the management of the company to get back the

total invested amount through the cash inflows (Krantz, 2016). The calculations of both the

machineries have been given in the appendix.

Question 3:

Operating and financial lease as a source of finance:

Operating lease and financial lease are the part of lease which is chosen by the

company on the basis of their requirement. In case of operating lease, when a company needs

any equipment for short time period than it is a better option. The leasing company give the

equipment for short term period in consideration with lease rent and then they wish to sell it

out as second hand after leasing period to other party. On operating lease, equipment is leased

by the company for 2-3 periods which is lesser than the actual time period of the machinery.

This kind of assets are not shown in the balance sheet of the company instead of it, the entire

lease cost of the machineries is shown in the income statement of the company on

expenditure side (Kinsky, 2011).

Whereas, in case of financial lease, it has been found that this lease is the alternative

of hire purchase in which the leasing company recovers the total cost of the machinery from

the company who has taken the equipment on lease. In this case, the company does not own

the machinery but most of the risk and rewards are hold by the leased company. The

company is holding responsible for insuring the assets, maintaining the assets etc. After the

end of the lease time period, business can sold it as second hand property (Madura, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management

5

These assets are shown in the statement of financial position of the company on assets side

and all the other expenses are shown in the income statement of the company.

Question 4:

a) P/E ratio:

P/E ratio of Mustafa and Anika limited has been studied and it has been recognized that

the P/E ratio of both the companies are 15% and 25% continuously which explains that the

price earnings performance of Mustafa was lower than the Anika and it indicates that the

investors are anticipating lower growth of the company. Instead of a bad year performance,

the P/E ratio of Anika limited has been better than the Mustafa because of the higher stock

price in the market.

b) Financial gearing impact:

The above study depicts that even after having a bad year; Anika had been able to

manage the better P/E in market than Mustafa. A huge reason behind this is share price and

the higher financial gearing position. It indicates that the price earnings ratio depicts about

the proportion of stock price against the earnings of the company. If the debt position of the

company would be higher than the earnings level of the company would be lower and as the

stock price of the company is already higher, thus, it has lead to the P/E ratio of the company

to better level than Mustafa limited (Lord, 2007).

c) comparison among P/e ratio and dividend yield:

The study has been done on the P/E ratio and dividend yield of both the companies and

it has been recognized that there is huge difference among both the company’s position. But

it has also been argued that the nominal value and the share price of both the companies are

also different that is the main factor to identify the P/E level and dividend yield of both the

companies. But as the result is always shown in the % and thus the result could be compare to

evaluate and compare the performance of both the companies. It will always lead to the

company towards a state where the comparison could be done and better strategies are made

for the betterment of the company (Rossi, 2014).

d) Shareholder impact:

The concern of company towards the shareholder is quite correct. Shareholders always

look for the P/E ratio, dividend yield, market position of the company etc to measure the

5

These assets are shown in the statement of financial position of the company on assets side

and all the other expenses are shown in the income statement of the company.

Question 4:

a) P/E ratio:

P/E ratio of Mustafa and Anika limited has been studied and it has been recognized that

the P/E ratio of both the companies are 15% and 25% continuously which explains that the

price earnings performance of Mustafa was lower than the Anika and it indicates that the

investors are anticipating lower growth of the company. Instead of a bad year performance,

the P/E ratio of Anika limited has been better than the Mustafa because of the higher stock

price in the market.

b) Financial gearing impact:

The above study depicts that even after having a bad year; Anika had been able to

manage the better P/E in market than Mustafa. A huge reason behind this is share price and

the higher financial gearing position. It indicates that the price earnings ratio depicts about

the proportion of stock price against the earnings of the company. If the debt position of the

company would be higher than the earnings level of the company would be lower and as the

stock price of the company is already higher, thus, it has lead to the P/E ratio of the company

to better level than Mustafa limited (Lord, 2007).

c) comparison among P/e ratio and dividend yield:

The study has been done on the P/E ratio and dividend yield of both the companies and

it has been recognized that there is huge difference among both the company’s position. But

it has also been argued that the nominal value and the share price of both the companies are

also different that is the main factor to identify the P/E level and dividend yield of both the

companies. But as the result is always shown in the % and thus the result could be compare to

evaluate and compare the performance of both the companies. It will always lead to the

company towards a state where the comparison could be done and better strategies are made

for the betterment of the company (Rossi, 2014).

d) Shareholder impact:

The concern of company towards the shareholder is quite correct. Shareholders always

look for the P/E ratio, dividend yield, market position of the company etc to measure the

Financial Management

6

performance of the company and make decision that whether the investment must be done in

the company or not (Gapenski, 2008). If the return from the company is even lower than the

risk free government bonds than it is quite big issue for the company and company should

focus on these points to improve the overall performance of the company.

Task B:

Question 1:

Valuation analysis:

Valuation analysis is a process in which the stock price of the company is estimated

through evaluating the assets worth, dividend value, P/E ratio etc of the company. Valuation

analysis makes it easier for the business and the stakeholder to measure that whether the

intrinsic value of the company is undervalued or overvalued in the market.

In the given case, the dividend discount model, P/E valuation model and net asset

valuation model have been applied on the company to evaluate the intrinsic price of the

company. On the basis of the DDM model, the stock price of the company should be $

363.33 whereas the net asset valuation model and P/E model explains that the stock price of

the company must be $ 180 and $ 633.5 respectively. The calculations of each of the model

have been attached in the appendix.

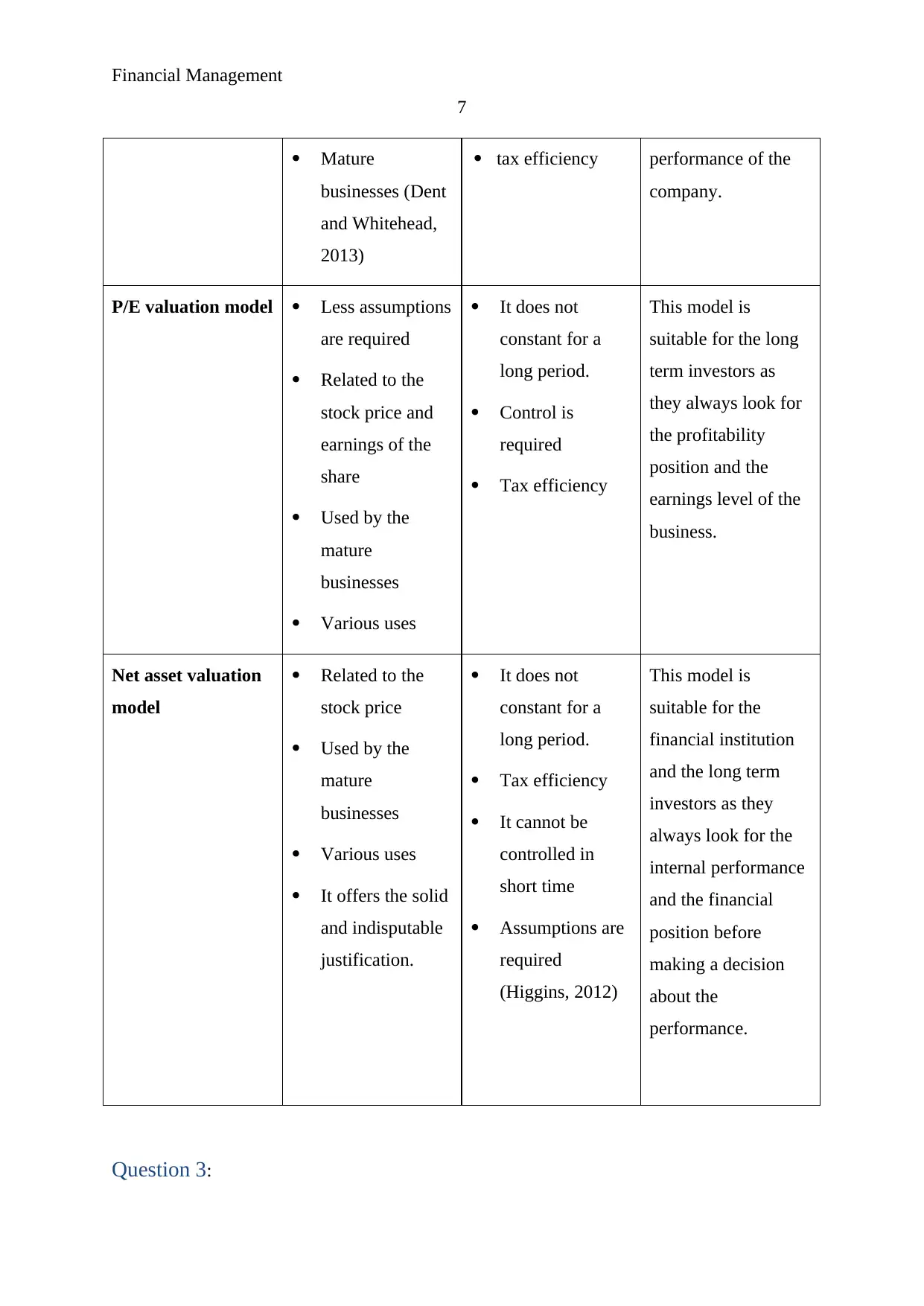

Question 2:

Strength, weakness and suitability of valuation model:

Valuation model Strength Weakness Suitability

Dividend Discount

model

It offers the solid

and indisputable

justification.

It stays constant

for a long period.

No requirement

of control

Limited use

Too many

assumptions

many not be

related to the

earnings of the

company

This model is

suitable for the

business as it offers

the fair value and the

investors always look

for the return they

will get rather than

the earnings and the

net assets

6

performance of the company and make decision that whether the investment must be done in

the company or not (Gapenski, 2008). If the return from the company is even lower than the

risk free government bonds than it is quite big issue for the company and company should

focus on these points to improve the overall performance of the company.

Task B:

Question 1:

Valuation analysis:

Valuation analysis is a process in which the stock price of the company is estimated

through evaluating the assets worth, dividend value, P/E ratio etc of the company. Valuation

analysis makes it easier for the business and the stakeholder to measure that whether the

intrinsic value of the company is undervalued or overvalued in the market.

In the given case, the dividend discount model, P/E valuation model and net asset

valuation model have been applied on the company to evaluate the intrinsic price of the

company. On the basis of the DDM model, the stock price of the company should be $

363.33 whereas the net asset valuation model and P/E model explains that the stock price of

the company must be $ 180 and $ 633.5 respectively. The calculations of each of the model

have been attached in the appendix.

Question 2:

Strength, weakness and suitability of valuation model:

Valuation model Strength Weakness Suitability

Dividend Discount

model

It offers the solid

and indisputable

justification.

It stays constant

for a long period.

No requirement

of control

Limited use

Too many

assumptions

many not be

related to the

earnings of the

company

This model is

suitable for the

business as it offers

the fair value and the

investors always look

for the return they

will get rather than

the earnings and the

net assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management

7

Mature

businesses (Dent

and Whitehead,

2013)

tax efficiency performance of the

company.

P/E valuation model Less assumptions

are required

Related to the

stock price and

earnings of the

share

Used by the

mature

businesses

Various uses

It does not

constant for a

long period.

Control is

required

Tax efficiency

This model is

suitable for the long

term investors as

they always look for

the profitability

position and the

earnings level of the

business.

Net asset valuation

model

Related to the

stock price

Used by the

mature

businesses

Various uses

It offers the solid

and indisputable

justification.

It does not

constant for a

long period.

Tax efficiency

It cannot be

controlled in

short time

Assumptions are

required

(Higgins, 2012)

This model is

suitable for the

financial institution

and the long term

investors as they

always look for the

internal performance

and the financial

position before

making a decision

about the

performance.

Question 3:

7

Mature

businesses (Dent

and Whitehead,

2013)

tax efficiency performance of the

company.

P/E valuation model Less assumptions

are required

Related to the

stock price and

earnings of the

share

Used by the

mature

businesses

Various uses

It does not

constant for a

long period.

Control is

required

Tax efficiency

This model is

suitable for the long

term investors as

they always look for

the profitability

position and the

earnings level of the

business.

Net asset valuation

model

Related to the

stock price

Used by the

mature

businesses

Various uses

It offers the solid

and indisputable

justification.

It does not

constant for a

long period.

Tax efficiency

It cannot be

controlled in

short time

Assumptions are

required

(Higgins, 2012)

This model is

suitable for the

financial institution

and the long term

investors as they

always look for the

internal performance

and the financial

position before

making a decision

about the

performance.

Question 3:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management

8

Efficient market hypothesis is an investment theory where the stock price of an

organization reflects about the information of the business and explains that the consistent

alpha generation is not possible in the business. Mainly, there are three forms of efficient

market hypothesis which are weak form, semi strong and strong form of EMH.

Weak from of EMH explains that the market is efficient and it reflects about entire

market information. It is assumed in this form that the rate of return is an independent factor

in the market which must not be affected from the past rate of return of the company

(Narayan, Narayan, Popp and Ali Ahmed, 2015). Whereas, the semi strong EMH defines that

the market is efficient and only reflect about the publicly available information of the

company. It incorporates the EMH’s weak form as well. It indicates that the investors always

make decision about the investment through the available information in the market

(Marwala and Hurwitz, 2017).

Lastly, the strong form of EMH has been studied. The strong form implies that market

is efficient and depicts about all the public and private information about an organization. It

builds up and incorporates the semi strong and weak form of EMH (Khan and Khan, 2016). It

defines that the decision is made by the investors on the basis of the available public and

private information.

Question 4:

On the basis of the valuation techniques, strength, weakness and suitability of various

valuation models and the efficient market hypothesis, it has been recognized that the stock

market is quite variable in nature. With the changes of each of the information and factor, the

stock performance of the company get change and along with that, the decisions of the

investors about the company get also change. If the strong form of EMH is taken into the

concern than it depicts that the changes into the public and private information affect the

investment decision of the stockholder (Komariah, Mahbub and Sin, 2015). However, it has

also been mentioned that they do not take the concern on the previous data which is not true.

In order to invest for a long period, in a security, investors focuses on the previous data and

future forecasted performance of the company.

8

Efficient market hypothesis is an investment theory where the stock price of an

organization reflects about the information of the business and explains that the consistent

alpha generation is not possible in the business. Mainly, there are three forms of efficient

market hypothesis which are weak form, semi strong and strong form of EMH.

Weak from of EMH explains that the market is efficient and it reflects about entire

market information. It is assumed in this form that the rate of return is an independent factor

in the market which must not be affected from the past rate of return of the company

(Narayan, Narayan, Popp and Ali Ahmed, 2015). Whereas, the semi strong EMH defines that

the market is efficient and only reflect about the publicly available information of the

company. It incorporates the EMH’s weak form as well. It indicates that the investors always

make decision about the investment through the available information in the market

(Marwala and Hurwitz, 2017).

Lastly, the strong form of EMH has been studied. The strong form implies that market

is efficient and depicts about all the public and private information about an organization. It

builds up and incorporates the semi strong and weak form of EMH (Khan and Khan, 2016). It

defines that the decision is made by the investors on the basis of the available public and

private information.

Question 4:

On the basis of the valuation techniques, strength, weakness and suitability of various

valuation models and the efficient market hypothesis, it has been recognized that the stock

market is quite variable in nature. With the changes of each of the information and factor, the

stock performance of the company get change and along with that, the decisions of the

investors about the company get also change. If the strong form of EMH is taken into the

concern than it depicts that the changes into the public and private information affect the

investment decision of the stockholder (Komariah, Mahbub and Sin, 2015). However, it has

also been mentioned that they do not take the concern on the previous data which is not true.

In order to invest for a long period, in a security, investors focuses on the previous data and

future forecasted performance of the company.

Financial Management

9

References:

Dent, M. and Whitehead, S. 2013. Managing professional identities: Knowledge,

performativities and the'new'professional (Vol. 19). Routledge.

Gapenski, L.C., 2008. Healthcare finance: an introduction to accounting and financial

management. Health Administration Press.

Higgins, R. C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Kelly, K.S., 2012. Effective fund-raising management. Routledge.

Khan, N.U. and Khan, S., 2016. Weak Form of Efficient Market Hypothesis: Evidence from

Pakistan. Business & Economic Review, 8(SE), pp.1-18.

Kinsky, R. 2011. Charting Made Simple: A Beginner's Guide to Technical Analysis. John

Wiley & Sons.

Komariah, K.S., Mahbub, C. and Sin, B.K., 2015. Efficient Market Hypothesis Approach to

Predict USD/IDR Trends using Twitter Sentiment Analysis. Database, 6, p.12th.

Krantz, M. 2016. Fundamental Analysis for Dummies. London: John Wiley & Sons.

Lord, B.R., 2007. Strategic management accounting. Issues in Management Accounting, 3.

Madura, J. 2014. Financial Markets and Institutions. Cengage Learning.

Marwala, T. and Hurwitz, E., 2017. Efficient Market Hypothesis. In Artificial Intelligence

and Economic Theory: Skynet in the Market (pp. 101-110). Springer, Cham.

Narayan, P.K., Narayan, S., Popp, S. and Ali Ahmed, H., 2015. Is the efficient market

hypothesis day-of-the-week dependent? Evidence from the banking sector. Applied

Economics, 47(23), pp.2359-2378.

Rossi, M., 2014. Capital budgeting in Europe: confronting theory with practice. International

Journal of Managerial and Financial Accounting, 6(4), pp.341-356.

9

References:

Dent, M. and Whitehead, S. 2013. Managing professional identities: Knowledge,

performativities and the'new'professional (Vol. 19). Routledge.

Gapenski, L.C., 2008. Healthcare finance: an introduction to accounting and financial

management. Health Administration Press.

Higgins, R. C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Kelly, K.S., 2012. Effective fund-raising management. Routledge.

Khan, N.U. and Khan, S., 2016. Weak Form of Efficient Market Hypothesis: Evidence from

Pakistan. Business & Economic Review, 8(SE), pp.1-18.

Kinsky, R. 2011. Charting Made Simple: A Beginner's Guide to Technical Analysis. John

Wiley & Sons.

Komariah, K.S., Mahbub, C. and Sin, B.K., 2015. Efficient Market Hypothesis Approach to

Predict USD/IDR Trends using Twitter Sentiment Analysis. Database, 6, p.12th.

Krantz, M. 2016. Fundamental Analysis for Dummies. London: John Wiley & Sons.

Lord, B.R., 2007. Strategic management accounting. Issues in Management Accounting, 3.

Madura, J. 2014. Financial Markets and Institutions. Cengage Learning.

Marwala, T. and Hurwitz, E., 2017. Efficient Market Hypothesis. In Artificial Intelligence

and Economic Theory: Skynet in the Market (pp. 101-110). Springer, Cham.

Narayan, P.K., Narayan, S., Popp, S. and Ali Ahmed, H., 2015. Is the efficient market

hypothesis day-of-the-week dependent? Evidence from the banking sector. Applied

Economics, 47(23), pp.2359-2378.

Rossi, M., 2014. Capital budgeting in Europe: confronting theory with practice. International

Journal of Managerial and Financial Accounting, 6(4), pp.341-356.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management

10

Appendix:

Machine A

Calculation of Net Present Value

Years Cash Outflow

After tax Cash

Inflow+ Add back

depreciation Factors Cash Inflow PV

Cash Outflow

PV

0

OMR

63,000 1.00

OMR

-

OMR

63,000.00

1

OMR

18,800 OMR 33,880 0.88

OMR

29,982.30

OMR

16,637.17

2

OMR

6,300 OMR 35,910 0.78

OMR

28,122.80

OMR

4,933.82

3

OMR

6,300 OMR 37,100 0.69

OMR

25,712.16

OMR

4,366.22

4

OMR

6,300 OMR 36,400 0.61

OMR

22,324.80

OMR

3,863.91

4

OMR

6,300 OMR 12,500 0.61

OMR

7,666.48

OMR

3,863.91

Total

OMR

113,808.55

OMR

96,665.02

NPV= Total Cash Inflow PV -Total cash outflow PV

OMR

17,143.52

Calculation Of Payback period

Years Cash Outflow Cash Inflow Cash flows CF

0

-OMR

63,000

-OMR

63,000

-OMR

63,000

1

-OMR

18,800 OMR 33,880

OMR

15,080

-OMR

47,920

2 OMR 35,910

OMR

35,910

-OMR

12,010

3 OMR 37,100

OMR

37,100

OMR

25,090

4 OMR 36,400

OMR

36,400

OMR

61,490

4 OMR 12,500

OMR

12,500

OMR

73,990

Payback period = 2.32

10

Appendix:

Machine A

Calculation of Net Present Value

Years Cash Outflow

After tax Cash

Inflow+ Add back

depreciation Factors Cash Inflow PV

Cash Outflow

PV

0

OMR

63,000 1.00

OMR

-

OMR

63,000.00

1

OMR

18,800 OMR 33,880 0.88

OMR

29,982.30

OMR

16,637.17

2

OMR

6,300 OMR 35,910 0.78

OMR

28,122.80

OMR

4,933.82

3

OMR

6,300 OMR 37,100 0.69

OMR

25,712.16

OMR

4,366.22

4

OMR

6,300 OMR 36,400 0.61

OMR

22,324.80

OMR

3,863.91

4

OMR

6,300 OMR 12,500 0.61

OMR

7,666.48

OMR

3,863.91

Total

OMR

113,808.55

OMR

96,665.02

NPV= Total Cash Inflow PV -Total cash outflow PV

OMR

17,143.52

Calculation Of Payback period

Years Cash Outflow Cash Inflow Cash flows CF

0

-OMR

63,000

-OMR

63,000

-OMR

63,000

1

-OMR

18,800 OMR 33,880

OMR

15,080

-OMR

47,920

2 OMR 35,910

OMR

35,910

-OMR

12,010

3 OMR 37,100

OMR

37,100

OMR

25,090

4 OMR 36,400

OMR

36,400

OMR

61,490

4 OMR 12,500

OMR

12,500

OMR

73,990

Payback period = 2.32

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management

11

Machine B

Calculation of Net Present Value

Years

Cash

Outflow

After tax Cash

Inflow+ Add back

depreciation Factors Cash Inflow PV

Cash Outflow

PV

0

OMR

110,000 1.00

OMR

-

OMR

110,000.00

1

OMR

23,500 OMR 46,543.33 0.87

OMR

40,472.46

OMR

20,434.78

2

OMR

11,000 OMR 41,363.33 0.76

OMR

31,276.62

OMR

8,317.58

3

OMR

11,000 OMR 40,733.33 0.66

OMR

26,782.83

OMR

7,232.68

4

OMR

11,000 OMR 41,223.33 0.57

OMR

23,569.57

OMR

6,289.29

5

OMR

11,000 OMR 52,283.33 0.50

OMR

25,994.06

OMR

5,468.94

6

OMR

11,000 OMR 49,273.33 0.43

OMR

21,302.22

OMR

4,755.60

6

OMR

11,000 OMR 12,500.00 0.43

OMR

5,404.09

OMR

4,755.60

Total

OMR

174,801.86

OMR

167,254.48

NPV= Total Cash Inflow PV -Total cash outflow PV

OMR

7,547.38

Calculation Of Payback period

Years

Cash

Outflow Cash Inflow Cash flows CF

0

-OMR

110,000

-OMR

110,000

-OMR

110,000

1

-OMR

23,500 OMR 46,543

OMR

23,043

-OMR

86,957

2 OMR 41,363

OMR

41,363

-OMR

45,593

3 OMR 40,733

OMR

40,733

-OMR

4,860

4 OMR 41,223

OMR

41,223

OMR

36,363

5 OMR 52,283

OMR

52,283

OMR

88,647

6 OMR 49,273

OMR

49,273

OMR

137,920

6 OMR 12,500

OMR

12,500

OMR

150,420

Payback period = 3.12

11

Machine B

Calculation of Net Present Value

Years

Cash

Outflow

After tax Cash

Inflow+ Add back

depreciation Factors Cash Inflow PV

Cash Outflow

PV

0

OMR

110,000 1.00

OMR

-

OMR

110,000.00

1

OMR

23,500 OMR 46,543.33 0.87

OMR

40,472.46

OMR

20,434.78

2

OMR

11,000 OMR 41,363.33 0.76

OMR

31,276.62

OMR

8,317.58

3

OMR

11,000 OMR 40,733.33 0.66

OMR

26,782.83

OMR

7,232.68

4

OMR

11,000 OMR 41,223.33 0.57

OMR

23,569.57

OMR

6,289.29

5

OMR

11,000 OMR 52,283.33 0.50

OMR

25,994.06

OMR

5,468.94

6

OMR

11,000 OMR 49,273.33 0.43

OMR

21,302.22

OMR

4,755.60

6

OMR

11,000 OMR 12,500.00 0.43

OMR

5,404.09

OMR

4,755.60

Total

OMR

174,801.86

OMR

167,254.48

NPV= Total Cash Inflow PV -Total cash outflow PV

OMR

7,547.38

Calculation Of Payback period

Years

Cash

Outflow Cash Inflow Cash flows CF

0

-OMR

110,000

-OMR

110,000

-OMR

110,000

1

-OMR

23,500 OMR 46,543

OMR

23,043

-OMR

86,957

2 OMR 41,363

OMR

41,363

-OMR

45,593

3 OMR 40,733

OMR

40,733

-OMR

4,860

4 OMR 41,223

OMR

41,223

OMR

36,363

5 OMR 52,283

OMR

52,283

OMR

88,647

6 OMR 49,273

OMR

49,273

OMR

137,920

6 OMR 12,500

OMR

12,500

OMR

150,420

Payback period = 3.12

Financial Management

12

Financial lease:

Machine A

Calculation of Net Present Value

Years

Cash

Outflow

After tax Cash

Inflow+ Add back

depreciation Factors Cash Inflow PV

Cash Outflow

PV

0 1.00

OMR

- OMR -

1

OMR

26,300

OMR

33,880 0.88

OMR

29,982.30

OMR

23,274.34

2

OMR

26,300

OMR

35,910 0.78

OMR

28,122.80

OMR

20,596.76

3

OMR

26,300

OMR

37,100 0.69

OMR

25,712.16

OMR

18,227.22

4

OMR

26,300

OMR

36,400 0.61

OMR

22,324.80

OMR

16,130.28

4

OMR

26,300

OMR

12,500 0.61

OMR

7,666.48

OMR

16,130.28

Total

OMR

113,808.55

OMR

94,358.88

NPV= Total Cash Inflow PV -Total cash outflow PV

OMR

19,449.67

Calculation Of Payback period

Years

Cash

Outflow Cash Inflow Cash flows CF

0

OMR

-

OMR

-

OMR

-

1

-OMR

26,300

OMR

33,880

OMR

7,580

OMR

7,580

2

OMR

35,910

OMR

35,910

OMR

43,490

3

OMR

37,100

OMR

37,100

OMR

80,590

4

OMR

36,400

OMR

36,400

OMR

116,990

4

OMR

12,500

OMR

12,500

OMR

129,490

12

Financial lease:

Machine A

Calculation of Net Present Value

Years

Cash

Outflow

After tax Cash

Inflow+ Add back

depreciation Factors Cash Inflow PV

Cash Outflow

PV

0 1.00

OMR

- OMR -

1

OMR

26,300

OMR

33,880 0.88

OMR

29,982.30

OMR

23,274.34

2

OMR

26,300

OMR

35,910 0.78

OMR

28,122.80

OMR

20,596.76

3

OMR

26,300

OMR

37,100 0.69

OMR

25,712.16

OMR

18,227.22

4

OMR

26,300

OMR

36,400 0.61

OMR

22,324.80

OMR

16,130.28

4

OMR

26,300

OMR

12,500 0.61

OMR

7,666.48

OMR

16,130.28

Total

OMR

113,808.55

OMR

94,358.88

NPV= Total Cash Inflow PV -Total cash outflow PV

OMR

19,449.67

Calculation Of Payback period

Years

Cash

Outflow Cash Inflow Cash flows CF

0

OMR

-

OMR

-

OMR

-

1

-OMR

26,300

OMR

33,880

OMR

7,580

OMR

7,580

2

OMR

35,910

OMR

35,910

OMR

43,490

3

OMR

37,100

OMR

37,100

OMR

80,590

4

OMR

36,400

OMR

36,400

OMR

116,990

4

OMR

12,500

OMR

12,500

OMR

129,490

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.