Financial Management Report: Risk, Portfolio, and VAR Analysis

VerifiedAdded on 2021/06/14

|7

|1216

|23

Report

AI Summary

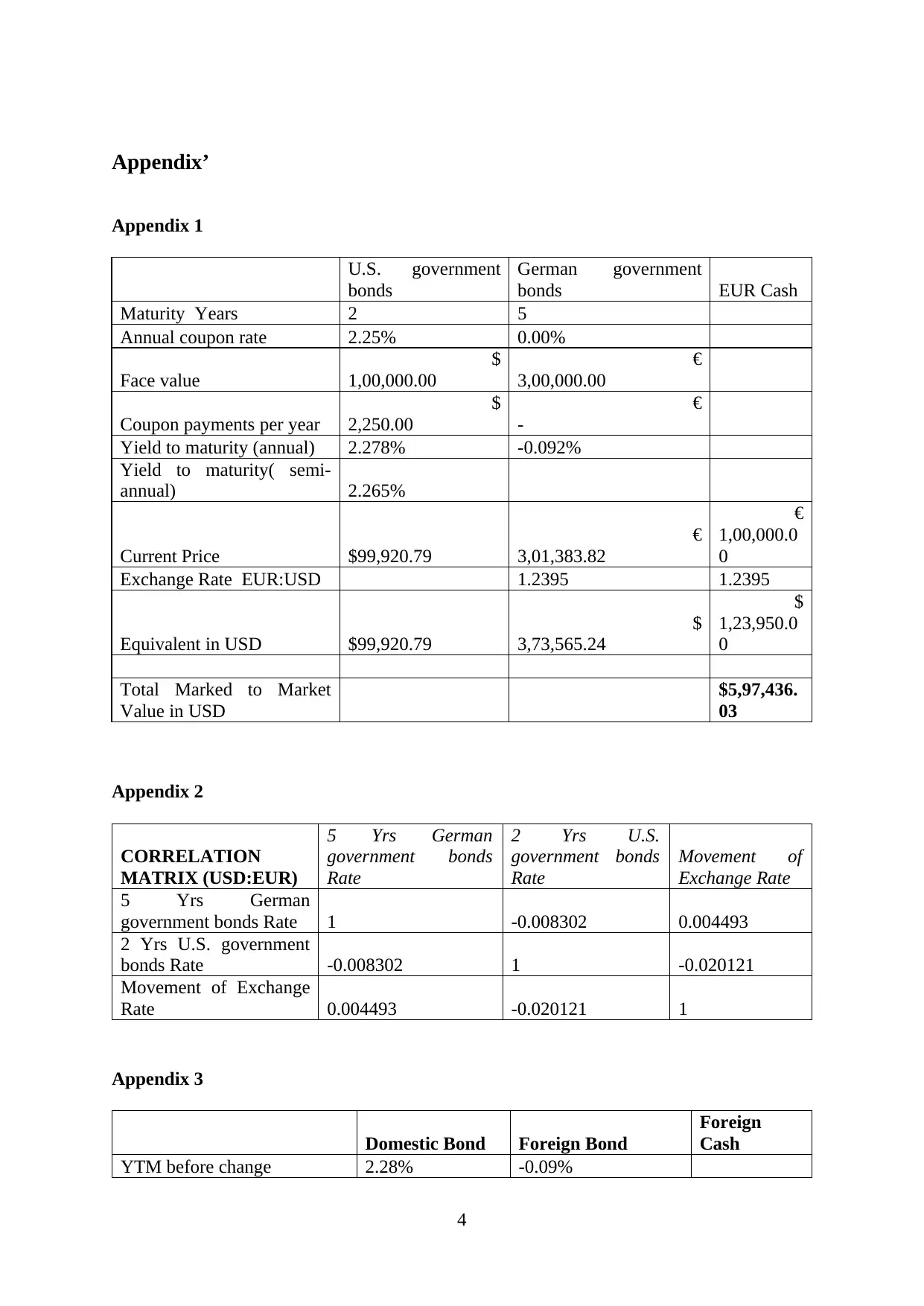

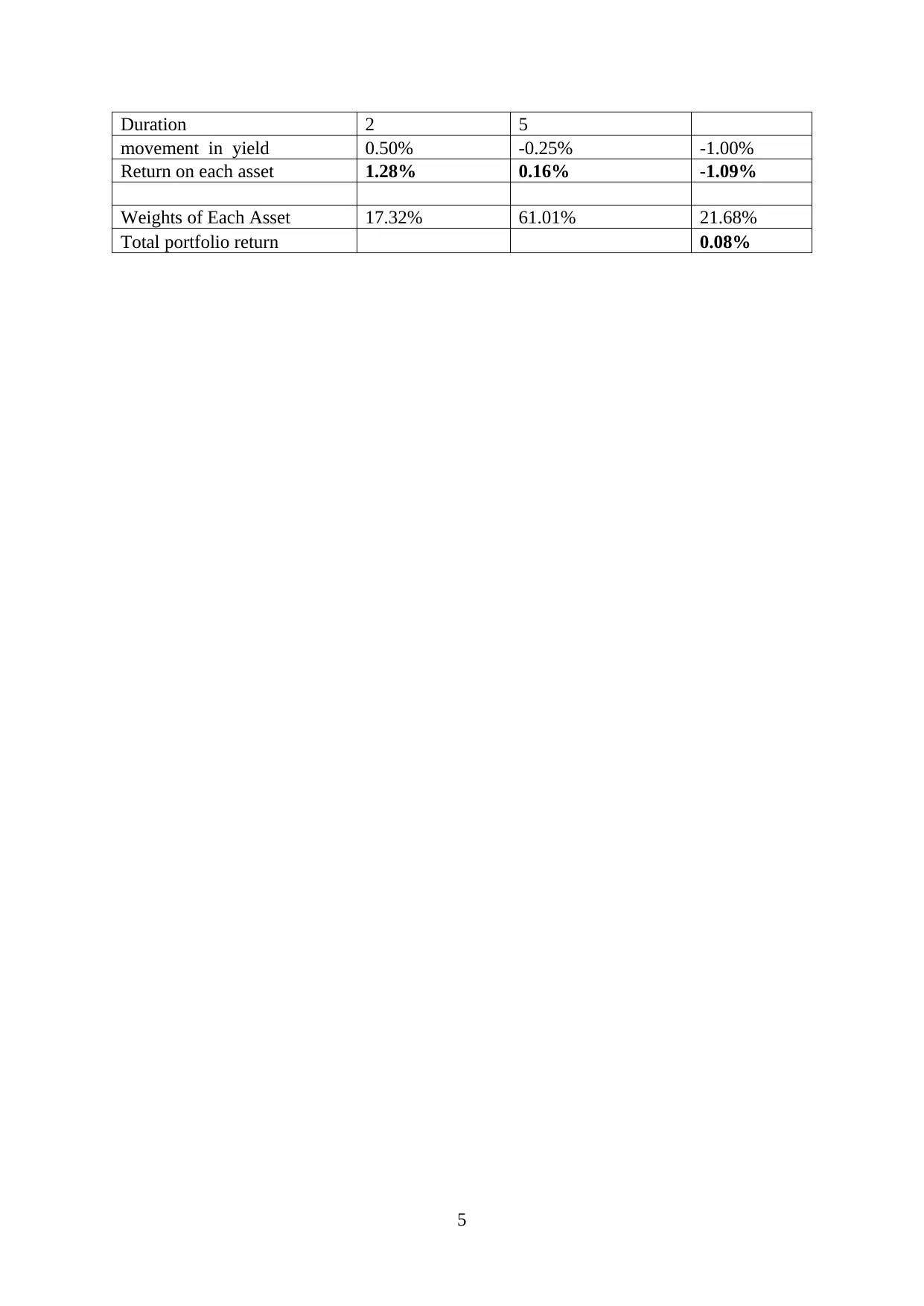

This financial management report analyzes a bank's portfolio, focusing on risk assessment, value-at-risk (VAR) calculations, and the impact of interest rate and exchange rate fluctuations. The report includes calculations of marked-to-market value for US and German government bonds, considering factors like yield to maturity, coupon rates, and exchange rates. It assesses various risks, including exchange rate, interest rate, and default risks, and uses correlation analysis to understand relationships between different financial instruments. The report also examines the impact of yield changes on portfolio returns and calculates portfolio returns under different scenarios. Furthermore, it explains VAR as a probabilistic measure of potential investment losses, outlining methods like correlation, Monte Carlo simulation, and historical simulation for its calculation.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.