Financial Management Report: NPV Analysis for Hamilton Ltd Project

VerifiedAdded on 2020/11/23

|19

|6516

|203

Report

AI Summary

This report presents a comprehensive financial management analysis for Hamilton Plc, focusing on investment appraisal techniques, particularly Net Present Value (NPV). The report evaluates the proposal to replace existing machinery (MA02) with a new model (MA05), providing detailed calculations of NPV for both scenarios. It examines the sales, raw materials, and production costs associated with each machine over a three-year period, considering inflation and corporate tax. The report analyzes the financial implications of each machine, comparing net cash inflows and discounted cash flows to determine which project is financially viable. Furthermore, it critically evaluates the use of NPV as an investment appraisal technique and explores alternative methods, such as Internal Rate of Return (IRR), payback period, and discounted payback period, to provide a more comprehensive assessment. The report concludes with recommendations for Hamilton Plc, guiding the company in making informed investment decisions to maximize returns and improve productivity. The assignment includes detailed calculations, explanations, and critical evaluations to support the financial recommendations.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Calculation of NPV (Net Present Value) for the proposal to replace MA02 with MA05......1

Question 2........................................................................................................................................4

Explaining which project should be accepted with supportive calculations..........................4

Question 3........................................................................................................................................7

Analysing proposal and making recommendation to the company........................................7

Question 4........................................................................................................................................9

Critical evaluation of use of NPV as a technique of investment appraisal............................9

Question 5......................................................................................................................................11

Identifying and critically evaluating use of alternative approaches to investment appraisal

techniques on reflecting circumstances of Hamilton Ltd.....................................................11

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Calculation of NPV (Net Present Value) for the proposal to replace MA02 with MA05......1

Question 2........................................................................................................................................4

Explaining which project should be accepted with supportive calculations..........................4

Question 3........................................................................................................................................7

Analysing proposal and making recommendation to the company........................................7

Question 4........................................................................................................................................9

Critical evaluation of use of NPV as a technique of investment appraisal............................9

Question 5......................................................................................................................................11

Identifying and critically evaluating use of alternative approaches to investment appraisal

techniques on reflecting circumstances of Hamilton Ltd.....................................................11

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Financial management is required so that finance can be used in an appropriate way and

it can be managed in a better manner. Investment appraisal methods are quite useful in this

context as funds should be applied only in high return yielding project. Present report deals with

Hamilton Plc. which is planning to replace existing machinery with MA05. The existing

machinery has only two years of estimated life and sales are estimated and are given. Future cash

flows are calculated by using NPV and critical analysis is explained in a better way. The

limitations of NPV are provided as management of firm thinks that it is not an appropriate

technique to rely upon and make decisions.

In context to this, alternative approaches are discussed such as IRR, payback period, IRR

and discounted payback period. Hence, company can evaluate the cash flows of two machineries

and decisions can be made with regard to investment appraisal methods and take enhance

decision for yielding better returns. Furthermore, organisation will be able to make a good

judgement as it cannot rely solely on one method for the purpose of making investment whether

organisation should invest in it or not. This is essentially required to evaluate project on payback

period to know that when will the project recover initial amount of investment made so that

appropriate decisions can be made in the best possible manner. Thus, other alternatives are

explained along with advantages and disadvantages to provide good overview to Hamilton Inc.

to make firm able to invest in machinery and garner higher productivity.

QUESTION 1

Calculation of NPV (Net Present Value) for the proposal to replace MA02 with MA05

For taking decisions regarding purchase of machinery by replacing with older one has

been calculated below:

MA02 MA05 MA02 MA05 MA02 MA05

Particulars 2019 2020 2021

Sales 620000 1150000 600000 1450000 0 1320000

Raw 62000 138000 60000 174000 0 158400

1

Financial management is required so that finance can be used in an appropriate way and

it can be managed in a better manner. Investment appraisal methods are quite useful in this

context as funds should be applied only in high return yielding project. Present report deals with

Hamilton Plc. which is planning to replace existing machinery with MA05. The existing

machinery has only two years of estimated life and sales are estimated and are given. Future cash

flows are calculated by using NPV and critical analysis is explained in a better way. The

limitations of NPV are provided as management of firm thinks that it is not an appropriate

technique to rely upon and make decisions.

In context to this, alternative approaches are discussed such as IRR, payback period, IRR

and discounted payback period. Hence, company can evaluate the cash flows of two machineries

and decisions can be made with regard to investment appraisal methods and take enhance

decision for yielding better returns. Furthermore, organisation will be able to make a good

judgement as it cannot rely solely on one method for the purpose of making investment whether

organisation should invest in it or not. This is essentially required to evaluate project on payback

period to know that when will the project recover initial amount of investment made so that

appropriate decisions can be made in the best possible manner. Thus, other alternatives are

explained along with advantages and disadvantages to provide good overview to Hamilton Inc.

to make firm able to invest in machinery and garner higher productivity.

QUESTION 1

Calculation of NPV (Net Present Value) for the proposal to replace MA02 with MA05

For taking decisions regarding purchase of machinery by replacing with older one has

been calculated below:

MA02 MA05 MA02 MA05 MA02 MA05

Particulars 2019 2020 2021

Sales 620000 1150000 600000 1450000 0 1320000

Raw 62000 138000 60000 174000 0 158400

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

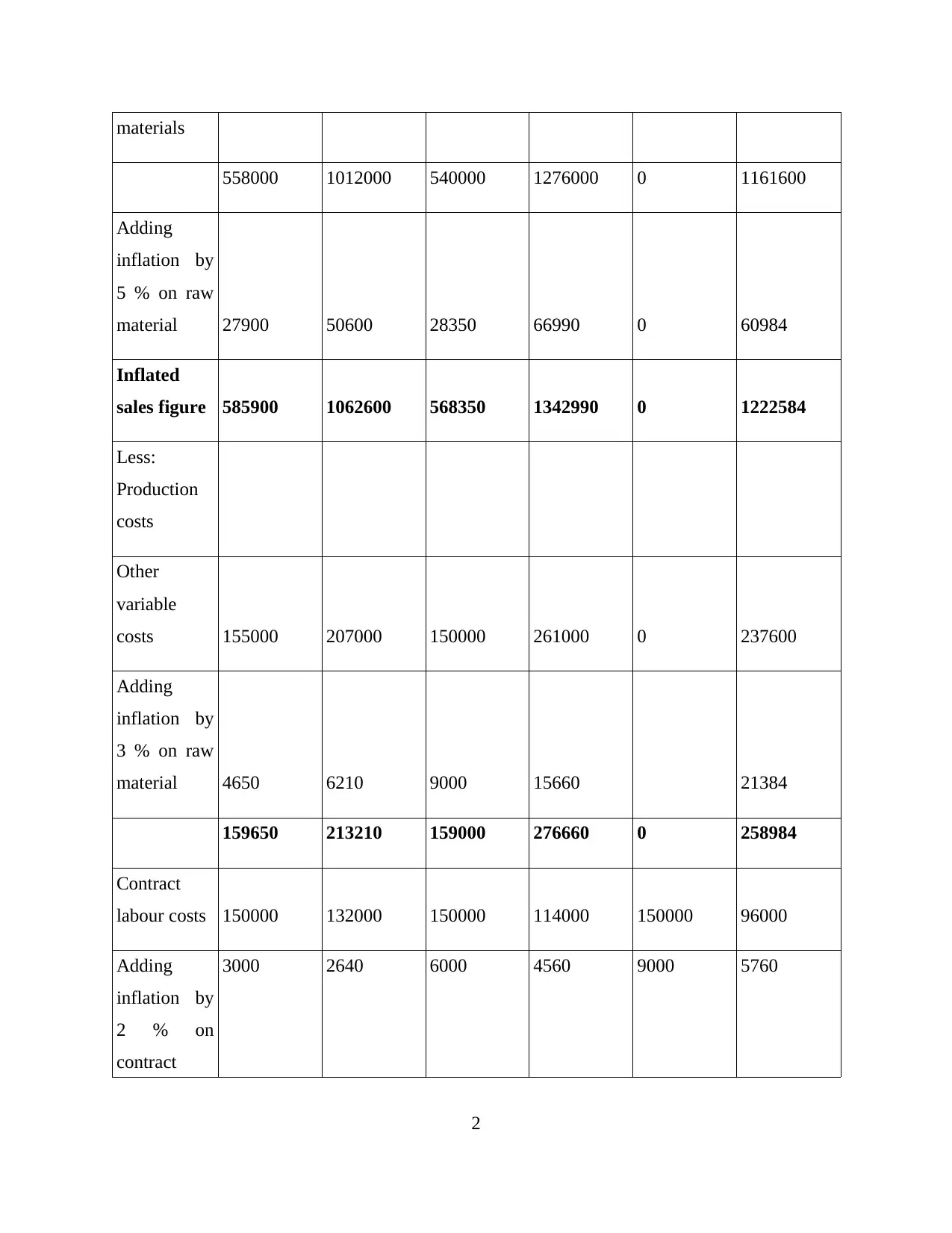

materials

558000 1012000 540000 1276000 0 1161600

Adding

inflation by

5 % on raw

material 27900 50600 28350 66990 0 60984

Inflated

sales figure 585900 1062600 568350 1342990 0 1222584

Less:

Production

costs

Other

variable

costs 155000 207000 150000 261000 0 237600

Adding

inflation by

3 % on raw

material 4650 6210 9000 15660 21384

159650 213210 159000 276660 0 258984

Contract

labour costs 150000 132000 150000 114000 150000 96000

Adding

inflation by

2 % on

contract

3000 2640 6000 4560 9000 5760

2

558000 1012000 540000 1276000 0 1161600

Adding

inflation by

5 % on raw

material 27900 50600 28350 66990 0 60984

Inflated

sales figure 585900 1062600 568350 1342990 0 1222584

Less:

Production

costs

Other

variable

costs 155000 207000 150000 261000 0 237600

Adding

inflation by

3 % on raw

material 4650 6210 9000 15660 21384

159650 213210 159000 276660 0 258984

Contract

labour costs 150000 132000 150000 114000 150000 96000

Adding

inflation by

2 % on

contract

3000 2640 6000 4560 9000 5760

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

labour costs

153000 134640 156000 118560 159000 101760

Total costs 312650 347850 315000 395220 159000 360744

Profit

Before Tax 273250 714750 253350 947770 -159000 861840

Less:

Corporate

tax @ 17% 46452.5 121507.5 43069.5 161120.9 -27030 146512.8

Net Profit

After Tax 226797.5 593242.5 210280.5 786649.1 -131970 715327.2

Adding

salvage

value 80000 200000

Net cash

inflows 226797.5 593242.5 290280.5 786649.1 -131970 915327.2

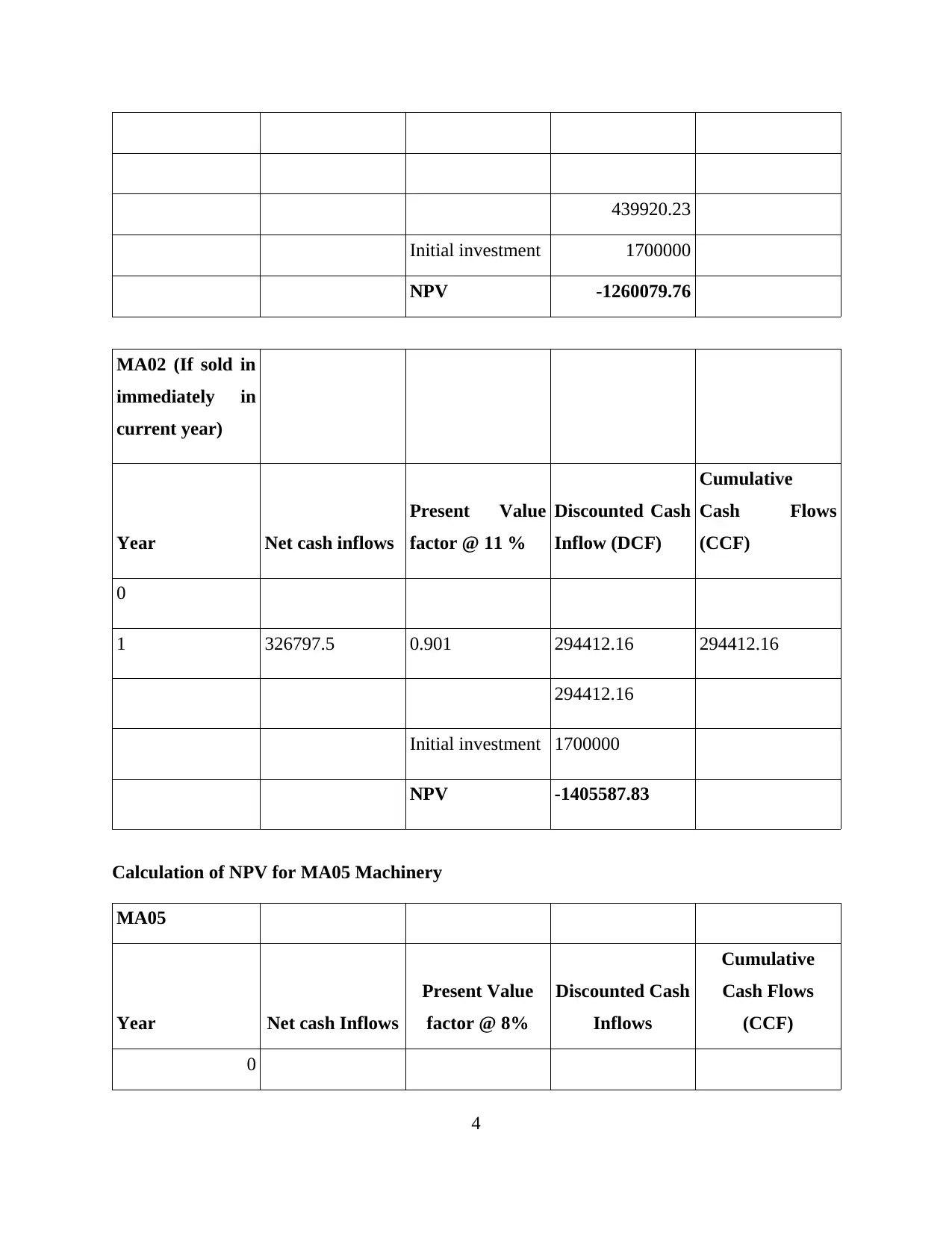

Calculation of NPV for MA02 Machinery

MA02 (If sold in

2020)

Year Net cash inflows

Present Value

factor @ 11 %

Discounted Cash

Inflow (DCF)

Cumulative

Cash Flows

(CCF)

0

1 226797.5 0.901 204322.07 204322.07

2 290280.5 0.812 235598.16 439920.23

3

153000 134640 156000 118560 159000 101760

Total costs 312650 347850 315000 395220 159000 360744

Profit

Before Tax 273250 714750 253350 947770 -159000 861840

Less:

Corporate

tax @ 17% 46452.5 121507.5 43069.5 161120.9 -27030 146512.8

Net Profit

After Tax 226797.5 593242.5 210280.5 786649.1 -131970 715327.2

Adding

salvage

value 80000 200000

Net cash

inflows 226797.5 593242.5 290280.5 786649.1 -131970 915327.2

Calculation of NPV for MA02 Machinery

MA02 (If sold in

2020)

Year Net cash inflows

Present Value

factor @ 11 %

Discounted Cash

Inflow (DCF)

Cumulative

Cash Flows

(CCF)

0

1 226797.5 0.901 204322.07 204322.07

2 290280.5 0.812 235598.16 439920.23

3

439920.23

Initial investment 1700000

NPV -1260079.76

MA02 (If sold in

immediately in

current year)

Year Net cash inflows

Present Value

factor @ 11 %

Discounted Cash

Inflow (DCF)

Cumulative

Cash Flows

(CCF)

0

1 326797.5 0.901 294412.16 294412.16

294412.16

Initial investment 1700000

NPV -1405587.83

Calculation of NPV for MA05 Machinery

MA05

Year Net cash Inflows

Present Value

factor @ 8%

Discounted Cash

Inflows

Cumulative

Cash Flows

(CCF)

0

4

Initial investment 1700000

NPV -1260079.76

MA02 (If sold in

immediately in

current year)

Year Net cash inflows

Present Value

factor @ 11 %

Discounted Cash

Inflow (DCF)

Cumulative

Cash Flows

(CCF)

0

1 326797.5 0.901 294412.16 294412.16

294412.16

Initial investment 1700000

NPV -1405587.83

Calculation of NPV for MA05 Machinery

MA05

Year Net cash Inflows

Present Value

factor @ 8%

Discounted Cash

Inflows

Cumulative

Cash Flows

(CCF)

0

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

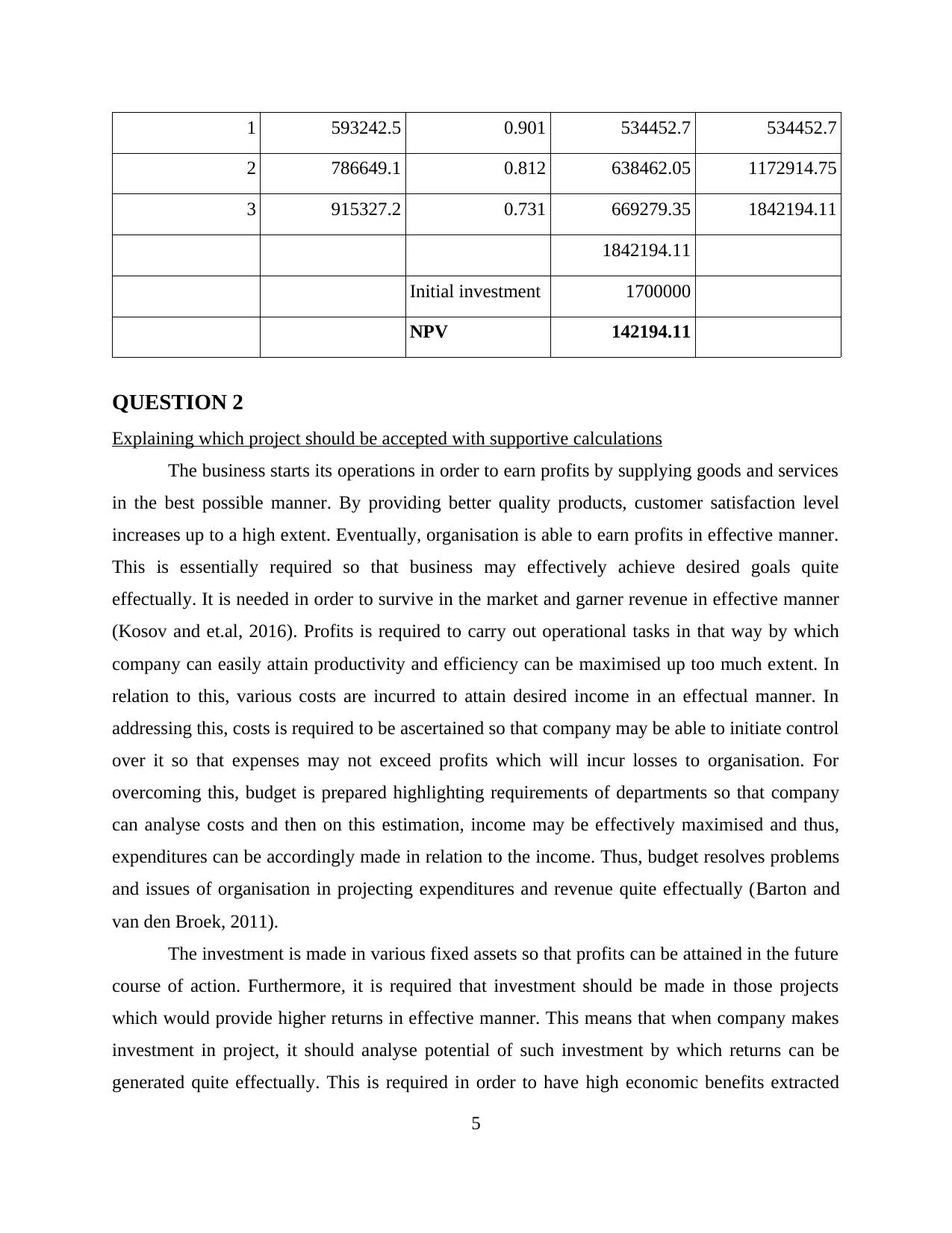

1 593242.5 0.901 534452.7 534452.7

2 786649.1 0.812 638462.05 1172914.75

3 915327.2 0.731 669279.35 1842194.11

1842194.11

Initial investment 1700000

NPV 142194.11

QUESTION 2

Explaining which project should be accepted with supportive calculations

The business starts its operations in order to earn profits by supplying goods and services

in the best possible manner. By providing better quality products, customer satisfaction level

increases up to a high extent. Eventually, organisation is able to earn profits in effective manner.

This is essentially required so that business may effectively achieve desired goals quite

effectually. It is needed in order to survive in the market and garner revenue in effective manner

(Kosov and et.al, 2016). Profits is required to carry out operational tasks in that way by which

company can easily attain productivity and efficiency can be maximised up too much extent. In

relation to this, various costs are incurred to attain desired income in an effectual manner. In

addressing this, costs is required to be ascertained so that company may be able to initiate control

over it so that expenses may not exceed profits which will incur losses to organisation. For

overcoming this, budget is prepared highlighting requirements of departments so that company

can analyse costs and then on this estimation, income may be effectively maximised and thus,

expenditures can be accordingly made in relation to the income. Thus, budget resolves problems

and issues of organisation in projecting expenditures and revenue quite effectually (Barton and

van den Broek, 2011).

The investment is made in various fixed assets so that profits can be attained in the future

course of action. Furthermore, it is required that investment should be made in those projects

which would provide higher returns in effective manner. This means that when company makes

investment in project, it should analyse potential of such investment by which returns can be

generated quite effectually. This is required in order to have high economic benefits extracted

5

2 786649.1 0.812 638462.05 1172914.75

3 915327.2 0.731 669279.35 1842194.11

1842194.11

Initial investment 1700000

NPV 142194.11

QUESTION 2

Explaining which project should be accepted with supportive calculations

The business starts its operations in order to earn profits by supplying goods and services

in the best possible manner. By providing better quality products, customer satisfaction level

increases up to a high extent. Eventually, organisation is able to earn profits in effective manner.

This is essentially required so that business may effectively achieve desired goals quite

effectually. It is needed in order to survive in the market and garner revenue in effective manner

(Kosov and et.al, 2016). Profits is required to carry out operational tasks in that way by which

company can easily attain productivity and efficiency can be maximised up too much extent. In

relation to this, various costs are incurred to attain desired income in an effectual manner. In

addressing this, costs is required to be ascertained so that company may be able to initiate control

over it so that expenses may not exceed profits which will incur losses to organisation. For

overcoming this, budget is prepared highlighting requirements of departments so that company

can analyse costs and then on this estimation, income may be effectively maximised and thus,

expenditures can be accordingly made in relation to the income. Thus, budget resolves problems

and issues of organisation in projecting expenditures and revenue quite effectually (Barton and

van den Broek, 2011).

The investment is made in various fixed assets so that profits can be attained in the future

course of action. Furthermore, it is required that investment should be made in those projects

which would provide higher returns in effective manner. This means that when company makes

investment in project, it should analyse potential of such investment by which returns can be

generated quite effectually. This is required in order to have high economic benefits extracted

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

out of the same. In relation to the case study, Hamilton Inc. which is engaged in the business of

manufacturing sports equipment and satisfies customers up to a high extent. It means that firm

produces good quantum of revenue in the market by selling quality products. Board of Directors

are planning to replace one of its machines used in production process and then purchasing

another machinery for accelerating production in the best possible manner. It means that if

equipment is replaced with that of new machinery, then level of production will be maximised

which is the ultimate goal of the firm. It will be able to provide sports equipment to customers

and earn desired level of revenue quite effectively.

The machinery which organisation is planning to replace is MA02 used in producing

basketballs. It is estimated that due to its normal passage of time, two years of life remains after

which machinery will of no use. It is required so that company may be able to achieve desired

production in effective manner. The proposal is made to purchase new machinery named as

MA05 which will inject production up to high level because it has improved specification. It will

help in increasing productivity and better quality basketballs can be produced quite effectually.

Eventually, increment in sales of such products will be achieved in the best possible manner.

Hence, it will provide good amount of profits in effective way. The cost of capital given is 11 %

to carry out cash flows (Hansen, 2018).

Two machines are at its disposal and so, decision is to be made to take into account that

machinery which could produce desired production of basketballs quite effectually. For taking

enhanced decision, NPV is calculated highlighting positive net cash inflows of machinery in next

three years. The sales figure are estimated for upcoming three years. In 2019, estimated sales are

620000, in next year 600000 and further is not given of MA02 as it will be disposed as estimated

useful life is of two years. On the other hand, sales predicted at the end of 2019 will be 1150000,

in 2020 figure will be 1450000 and in 2021, 1320000 will be produced. The raw materials,

labour are needed in order to achieve production in the best possible manner. In relation to this,

percentage of sales is expressed on raw materials, labour and related costs in effective way. It

can be said that different percentages are taken on sales figure. Moreover, contract labour costs

are amounting to 150000 which will be incurred on two machineries. If MA05 machine is

purchased, annual savings will be made on 12 % yearly which will reduced overall labour costs

and as such, savings can be accomplished in a better way. This would lead to increment in

production level and thus, sales will be increased up to a high extent of organisation.

6

manufacturing sports equipment and satisfies customers up to a high extent. It means that firm

produces good quantum of revenue in the market by selling quality products. Board of Directors

are planning to replace one of its machines used in production process and then purchasing

another machinery for accelerating production in the best possible manner. It means that if

equipment is replaced with that of new machinery, then level of production will be maximised

which is the ultimate goal of the firm. It will be able to provide sports equipment to customers

and earn desired level of revenue quite effectively.

The machinery which organisation is planning to replace is MA02 used in producing

basketballs. It is estimated that due to its normal passage of time, two years of life remains after

which machinery will of no use. It is required so that company may be able to achieve desired

production in effective manner. The proposal is made to purchase new machinery named as

MA05 which will inject production up to high level because it has improved specification. It will

help in increasing productivity and better quality basketballs can be produced quite effectually.

Eventually, increment in sales of such products will be achieved in the best possible manner.

Hence, it will provide good amount of profits in effective way. The cost of capital given is 11 %

to carry out cash flows (Hansen, 2018).

Two machines are at its disposal and so, decision is to be made to take into account that

machinery which could produce desired production of basketballs quite effectually. For taking

enhanced decision, NPV is calculated highlighting positive net cash inflows of machinery in next

three years. The sales figure are estimated for upcoming three years. In 2019, estimated sales are

620000, in next year 600000 and further is not given of MA02 as it will be disposed as estimated

useful life is of two years. On the other hand, sales predicted at the end of 2019 will be 1150000,

in 2020 figure will be 1450000 and in 2021, 1320000 will be produced. The raw materials,

labour are needed in order to achieve production in the best possible manner. In relation to this,

percentage of sales is expressed on raw materials, labour and related costs in effective way. It

can be said that different percentages are taken on sales figure. Moreover, contract labour costs

are amounting to 150000 which will be incurred on two machineries. If MA05 machine is

purchased, annual savings will be made on 12 % yearly which will reduced overall labour costs

and as such, savings can be accomplished in a better way. This would lead to increment in

production level and thus, sales will be increased up to a high extent of organisation.

6

Hamilton Inc. has to make decision which is essentially required so that business may be

able to achieve revenue quite effectively by increased sales. The NPV is calculated on the basis

of inflated figures and net cash inflows are being arrived by adding salvage value in effective

manner. The NPV of MA02 machinery is computed on two situations as given in the case study.

The first argument is that if equipment is sold immediately in current year, then salvage of

100000 is taken and as such, net inflows amounts to 326797.5 and then applying discounting

factor at 11 % rate, 294412.16 is arrived. The initial investment outlay is 17, 00,000 and by

deducting it, NPV is -1405587.83 which is negative. On the other hand, another situation is

given which is that Hamilton Inc. will sell in 2020 after two years, then resale value will be

80000 added to inflows to arrive at net cash flows. Furthermore, total CCF (Cumulative Cash

Flows) calculated are 439920.23 which is not desirable. Thus, by assuming both the situations, it

is clarified that company should replace machinery and sale it.

Furthermore, MA05 machinery is taken into account and NPV is calculated to analyse

whether it is worthwhile to accomplish desired production level of items or not. It can be

highlighted that by considering initial investment of 17,00,000, total cash flows arrived amounts

to 1842194.11 which is positive and it clarifies that investment in this project should be made so

that higher returns can be yield by the company. NPV is quite useful technique to arrive at

decision regarding the investment in project should be made or not. It is clarified from the fact

that Hamilton Inc. should invest in MA05 and replace existing machinery to initiate production

up too much extent. This will be helpful in achieving desired quantum of sales and hence,

company will be able to accomplish desired objectives in the best possible manner. Furthermore,

it should invest in new machinery in order to arrive at healthy level and thus, provide customer

satisfaction up to a higher extent (Profilet and Bacon, 2013).

QUESTION 3

Analysing proposal and making recommendations to company

The company is required to make investment in higher yielding project so that it may be

able to carry out production in desired quantum and satisfy customers to higher extent. The

organisation has made proposal to replace the existing machinery with that of new one to

effectively achieve higher quantum of production in the best possible manner. Hamilton Inc. has

planned that existing equipment will have a useful life of 2 years and then it will be disposed-off

7

able to achieve revenue quite effectively by increased sales. The NPV is calculated on the basis

of inflated figures and net cash inflows are being arrived by adding salvage value in effective

manner. The NPV of MA02 machinery is computed on two situations as given in the case study.

The first argument is that if equipment is sold immediately in current year, then salvage of

100000 is taken and as such, net inflows amounts to 326797.5 and then applying discounting

factor at 11 % rate, 294412.16 is arrived. The initial investment outlay is 17, 00,000 and by

deducting it, NPV is -1405587.83 which is negative. On the other hand, another situation is

given which is that Hamilton Inc. will sell in 2020 after two years, then resale value will be

80000 added to inflows to arrive at net cash flows. Furthermore, total CCF (Cumulative Cash

Flows) calculated are 439920.23 which is not desirable. Thus, by assuming both the situations, it

is clarified that company should replace machinery and sale it.

Furthermore, MA05 machinery is taken into account and NPV is calculated to analyse

whether it is worthwhile to accomplish desired production level of items or not. It can be

highlighted that by considering initial investment of 17,00,000, total cash flows arrived amounts

to 1842194.11 which is positive and it clarifies that investment in this project should be made so

that higher returns can be yield by the company. NPV is quite useful technique to arrive at

decision regarding the investment in project should be made or not. It is clarified from the fact

that Hamilton Inc. should invest in MA05 and replace existing machinery to initiate production

up too much extent. This will be helpful in achieving desired quantum of sales and hence,

company will be able to accomplish desired objectives in the best possible manner. Furthermore,

it should invest in new machinery in order to arrive at healthy level and thus, provide customer

satisfaction up to a higher extent (Profilet and Bacon, 2013).

QUESTION 3

Analysing proposal and making recommendations to company

The company is required to make investment in higher yielding project so that it may be

able to carry out production in desired quantum and satisfy customers to higher extent. The

organisation has made proposal to replace the existing machinery with that of new one to

effectively achieve higher quantum of production in the best possible manner. Hamilton Inc. has

planned that existing equipment will have a useful life of 2 years and then it will be disposed-off

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

because it can't be used further. The fixed assets lose its value due to normal wear and tear,

passage of time or obsolescence and related factors which is the loss to organisation as

depreciation is charged on it. Depreciation is charged and it is treated as cost to company as

organisation's income get reduced. However, depreciation has to be made so that correct

ascertainment of profits can be made and as such, financial health may be effectively assessed.

Firm is planning to discontinue MA02 machinery in which useful life is remaining of 2 years and

thus, production level has to be increased by implementing new equipment for accomplishing

adequate amount of production so that customer can be satisfied quite easily (Ries, 2018).

The estimated sales in the future are made in which at the end of 2019, 620000 will be

achieved. Furthermore, in next year sales will be 600000 and after that no sales are analysed as

useful life would be over. On the other side, MA05 machinery will produce revenue amounting

to 1150000 in 2019, 1450000 in 2020 and then 1320000 in next year. The sales have been

estimated higher in second equipment as it will be able to inject production. Average production

costs are carried out which is expressed as percentage of revenue for the two proposals. The raw

materials are 10 % and 12 % of MA02 MA05 respectively. On the other hand, variable cost have

25 % and 18 % respectively on both machineries. Hence, these percentages are implemented in

correct ascertainment of raw materials. Contract labour costs are ascertained to be incurred for

carrying production. In addition to this, if organisation purchases new machinery then it will

easily save labour costs on annual basis up to 12 % which would be beneficial for Hamilton Inc

as it can alleviate expenditures and achieve more quantum of production at least possible cost

(McDougal, 2017).

Furthermore, inflation rate has been provided which will be applied and as such, all the

figures will be inflated. The criteria of inflation are that general cost includes sales and other

variable cost having 3 % on sales figure. Moreover, raw material is applied of 5 % rate, contract

labour is 2 %. These percentages will remain same in first year, however, it will be increased

with same rate year after year to find out correct inflated figures. In simple words, inflation rate

will be increased annually and calculated on compound basis quite effectually. This is essential

to be taken into account so that firm may be able to consider inflation factor which leads to hike

in prices and related factors. On the other hand, there are two arguments as per the situation as

Board of Directors will discontinue old machinery immediately in the current year if new one is

bought and salvage value will be 100000. If it is sold after using for production in next two

8

passage of time or obsolescence and related factors which is the loss to organisation as

depreciation is charged on it. Depreciation is charged and it is treated as cost to company as

organisation's income get reduced. However, depreciation has to be made so that correct

ascertainment of profits can be made and as such, financial health may be effectively assessed.

Firm is planning to discontinue MA02 machinery in which useful life is remaining of 2 years and

thus, production level has to be increased by implementing new equipment for accomplishing

adequate amount of production so that customer can be satisfied quite easily (Ries, 2018).

The estimated sales in the future are made in which at the end of 2019, 620000 will be

achieved. Furthermore, in next year sales will be 600000 and after that no sales are analysed as

useful life would be over. On the other side, MA05 machinery will produce revenue amounting

to 1150000 in 2019, 1450000 in 2020 and then 1320000 in next year. The sales have been

estimated higher in second equipment as it will be able to inject production. Average production

costs are carried out which is expressed as percentage of revenue for the two proposals. The raw

materials are 10 % and 12 % of MA02 MA05 respectively. On the other hand, variable cost have

25 % and 18 % respectively on both machineries. Hence, these percentages are implemented in

correct ascertainment of raw materials. Contract labour costs are ascertained to be incurred for

carrying production. In addition to this, if organisation purchases new machinery then it will

easily save labour costs on annual basis up to 12 % which would be beneficial for Hamilton Inc

as it can alleviate expenditures and achieve more quantum of production at least possible cost

(McDougal, 2017).

Furthermore, inflation rate has been provided which will be applied and as such, all the

figures will be inflated. The criteria of inflation are that general cost includes sales and other

variable cost having 3 % on sales figure. Moreover, raw material is applied of 5 % rate, contract

labour is 2 %. These percentages will remain same in first year, however, it will be increased

with same rate year after year to find out correct inflated figures. In simple words, inflation rate

will be increased annually and calculated on compound basis quite effectually. This is essential

to be taken into account so that firm may be able to consider inflation factor which leads to hike

in prices and related factors. On the other hand, there are two arguments as per the situation as

Board of Directors will discontinue old machinery immediately in the current year if new one is

bought and salvage value will be 100000. If it is sold after using for production in next two

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

years, then resale amount would be 80000 at the end of March 2020. The salvage value of

another machinery will be 200000 at end of 2021 financial year. The organisation will be able to

garner positive NPV with respect of newer project.

The firm should not choose for continuing existing machinery as it will be unprofitable to

invest in the same. Hereby it is recommended to Hamilton Inc that investment should be made in

new project as it has positive value in terms of revenue. Furthermore, NPV has several benefits

which suits best in taking investment decisions quite effectually. First and one of the main merit

of NPV is that time value of money concept is effectively considered in evaluating effectiveness

and attractiveness of project with much ease. Moreover, it is main pillar of capital budgeting

technique which is widely used to evaluate project. Another merit of using such technique is that

company should can analyse risk associated with the investment and as a result, effective and

better decisions can be easily taken (Berger and Hannan, 2013).

Furthermore, cost of capital is analysed and taken in order to assess cash flows up too

much extent. The projections made with the help of NPV are quite useful as they are calculated

by taking difference between cash inflows and outflows quite effectively. NPV has various

alternatives or possibilities such as zero, positive and negative. The value of cash inflows is

greater than that of present value, NPV is said to be positive. If both the values are positive, then

zero NPV is found. If cash flows are less than present value, then negative NPV prevails. Hence,

it can be said that NPV of new project is greater and positive and thus, it is recommended to

invest in the project for higher returns.

QUESTION 4

Critical evaluation of the use of NPV as a technique of investment appraisal

The NPV has several advantages of NPV technique as it helps organisation to analyse

investment in the best possible manner. This is essentially required so that business may be able

to take advantage of the investment appraisal approach in making effective decisions. It is

needed so that higher returns may be generated which can be used for accomplishing tasks quite

effectually and investment would be feasible. However, apart from several benefits, there are

several limitations which restrict the use of NPV as a sole technique for judging viability of

capital investment. Hamilton Inc. has utilised NPV method and it believes that such technique is

not beneficial for organisation as it has limitations. In relation to this, demerits are there which

9

another machinery will be 200000 at end of 2021 financial year. The organisation will be able to

garner positive NPV with respect of newer project.

The firm should not choose for continuing existing machinery as it will be unprofitable to

invest in the same. Hereby it is recommended to Hamilton Inc that investment should be made in

new project as it has positive value in terms of revenue. Furthermore, NPV has several benefits

which suits best in taking investment decisions quite effectually. First and one of the main merit

of NPV is that time value of money concept is effectively considered in evaluating effectiveness

and attractiveness of project with much ease. Moreover, it is main pillar of capital budgeting

technique which is widely used to evaluate project. Another merit of using such technique is that

company should can analyse risk associated with the investment and as a result, effective and

better decisions can be easily taken (Berger and Hannan, 2013).

Furthermore, cost of capital is analysed and taken in order to assess cash flows up too

much extent. The projections made with the help of NPV are quite useful as they are calculated

by taking difference between cash inflows and outflows quite effectively. NPV has various

alternatives or possibilities such as zero, positive and negative. The value of cash inflows is

greater than that of present value, NPV is said to be positive. If both the values are positive, then

zero NPV is found. If cash flows are less than present value, then negative NPV prevails. Hence,

it can be said that NPV of new project is greater and positive and thus, it is recommended to

invest in the project for higher returns.

QUESTION 4

Critical evaluation of the use of NPV as a technique of investment appraisal

The NPV has several advantages of NPV technique as it helps organisation to analyse

investment in the best possible manner. This is essentially required so that business may be able

to take advantage of the investment appraisal approach in making effective decisions. It is

needed so that higher returns may be generated which can be used for accomplishing tasks quite

effectually and investment would be feasible. However, apart from several benefits, there are

several limitations which restrict the use of NPV as a sole technique for judging viability of

capital investment. Hamilton Inc. has utilised NPV method and it believes that such technique is

not beneficial for organisation as it has limitations. In relation to this, demerits are there which

9

means that company should not rely on this method as it has disadvantages and so, it is advised

not to be reliant on NPV technique for making investment decisions. The main demerit of using

NPV is that it is much sensitive to discount rates (Charupat and Miu, 2013).

The main demerit of using NPV is that it is very much sensitive to discount rates.

Furthermore, risks associated with project cannot be analysed as it lay emphasis on profitability

aspect and do not take into account other important factors like when will project recover cost of

investment which is known as initial outlay. The discounting rate used are of bit guesswork and

are not worthwhile to rely on for taking decisions. If discounted rate is decreased or increases,

then results will be inappropriate and so, final conclusion will be hampered and conflicting

results may be attained leading to inaccurate decisions in relation to the investment. Furthermore,

NPV is not useful when there are two mutually exclusive projects and thus, results would be

inappropriate and wrong decisions will be taken. The critics are listed as below:

Though NPV method is useful for determining the present value of future cash flows but

it also has some limitations. These limitations are as follows:

Cash flow estimate: NPV method considers forecasted cash flows which are difficult to

determine in the present time. The forecasted cash flows never give a true value and the present

values ascertained are always ambiguous.

Sensitivity to discounted rates: Computation under this method is done on the basis of

summation of multiple discounted cash flows. Both positive and negative values are converted

into present value at same point of time. A small increase or decrease in the discounted rate will

have a considerable effect on final output.

Excludes the value of real option: This does not take into account value of real option

that may exist within the investment. It means that if a project is giving loss and is expected to

have an opportunity of expansion in the near future, this method will not provide an inclusion of

such projects.

Determination of discounted rates: It is also difficult to determine the discount rates

preciously for calculating present value of cash flows (Gill and Biger, 2013).

Mutually exclusive projects: Caution needed to applied while using net present value

method when alternative projects with uneven lives are there. Calculation by this method can

give ambiguous results in such situation.

10

not to be reliant on NPV technique for making investment decisions. The main demerit of using

NPV is that it is much sensitive to discount rates (Charupat and Miu, 2013).

The main demerit of using NPV is that it is very much sensitive to discount rates.

Furthermore, risks associated with project cannot be analysed as it lay emphasis on profitability

aspect and do not take into account other important factors like when will project recover cost of

investment which is known as initial outlay. The discounting rate used are of bit guesswork and

are not worthwhile to rely on for taking decisions. If discounted rate is decreased or increases,

then results will be inappropriate and so, final conclusion will be hampered and conflicting

results may be attained leading to inaccurate decisions in relation to the investment. Furthermore,

NPV is not useful when there are two mutually exclusive projects and thus, results would be

inappropriate and wrong decisions will be taken. The critics are listed as below:

Though NPV method is useful for determining the present value of future cash flows but

it also has some limitations. These limitations are as follows:

Cash flow estimate: NPV method considers forecasted cash flows which are difficult to

determine in the present time. The forecasted cash flows never give a true value and the present

values ascertained are always ambiguous.

Sensitivity to discounted rates: Computation under this method is done on the basis of

summation of multiple discounted cash flows. Both positive and negative values are converted

into present value at same point of time. A small increase or decrease in the discounted rate will

have a considerable effect on final output.

Excludes the value of real option: This does not take into account value of real option

that may exist within the investment. It means that if a project is giving loss and is expected to

have an opportunity of expansion in the near future, this method will not provide an inclusion of

such projects.

Determination of discounted rates: It is also difficult to determine the discount rates

preciously for calculating present value of cash flows (Gill and Biger, 2013).

Mutually exclusive projects: Caution needed to applied while using net present value

method when alternative projects with uneven lives are there. Calculation by this method can

give ambiguous results in such situation.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.