Financial Management Report: CHI SWOT, Ratio Analysis, and CCA

VerifiedAdded on 2023/01/10

|15

|2037

|26

Report

AI Summary

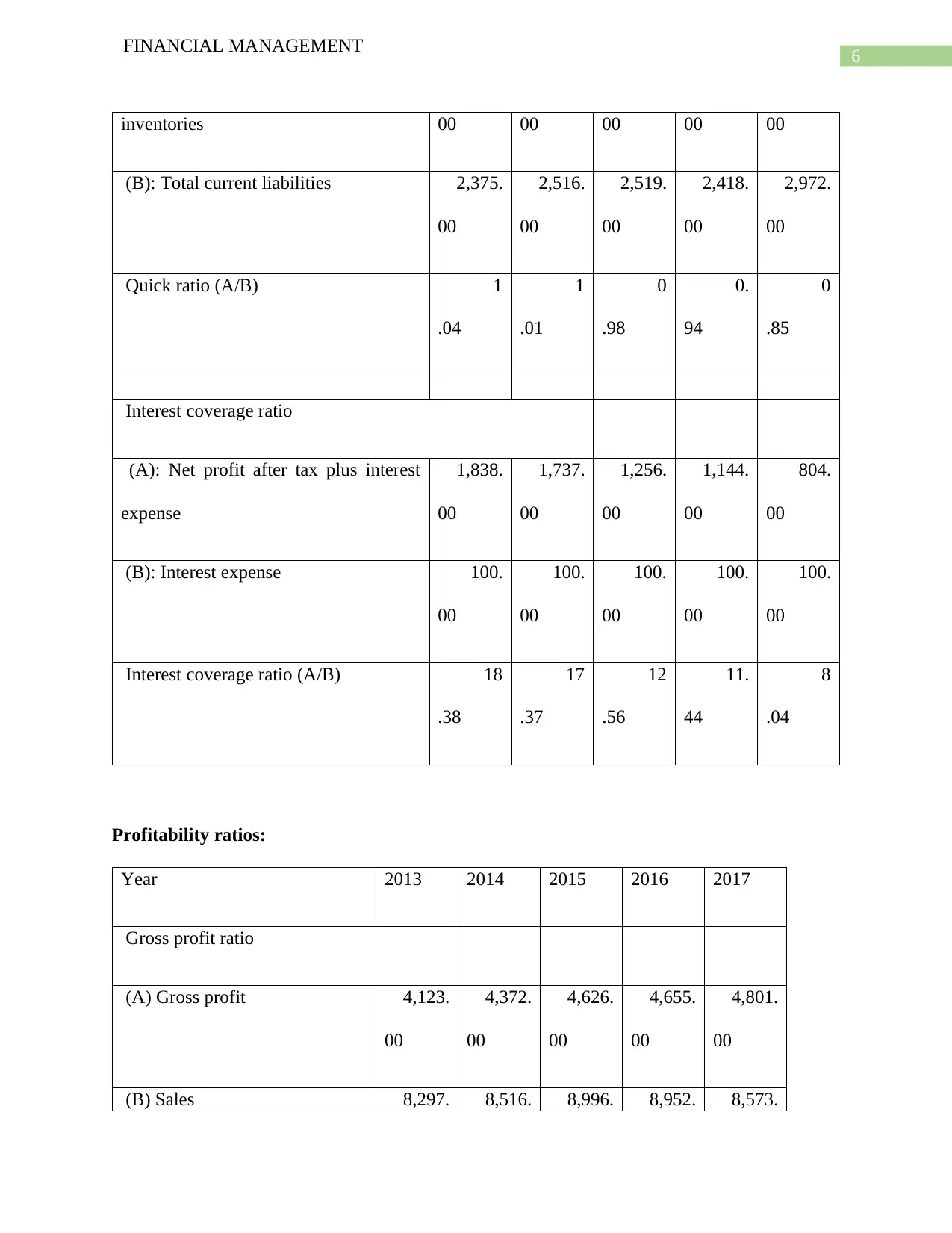

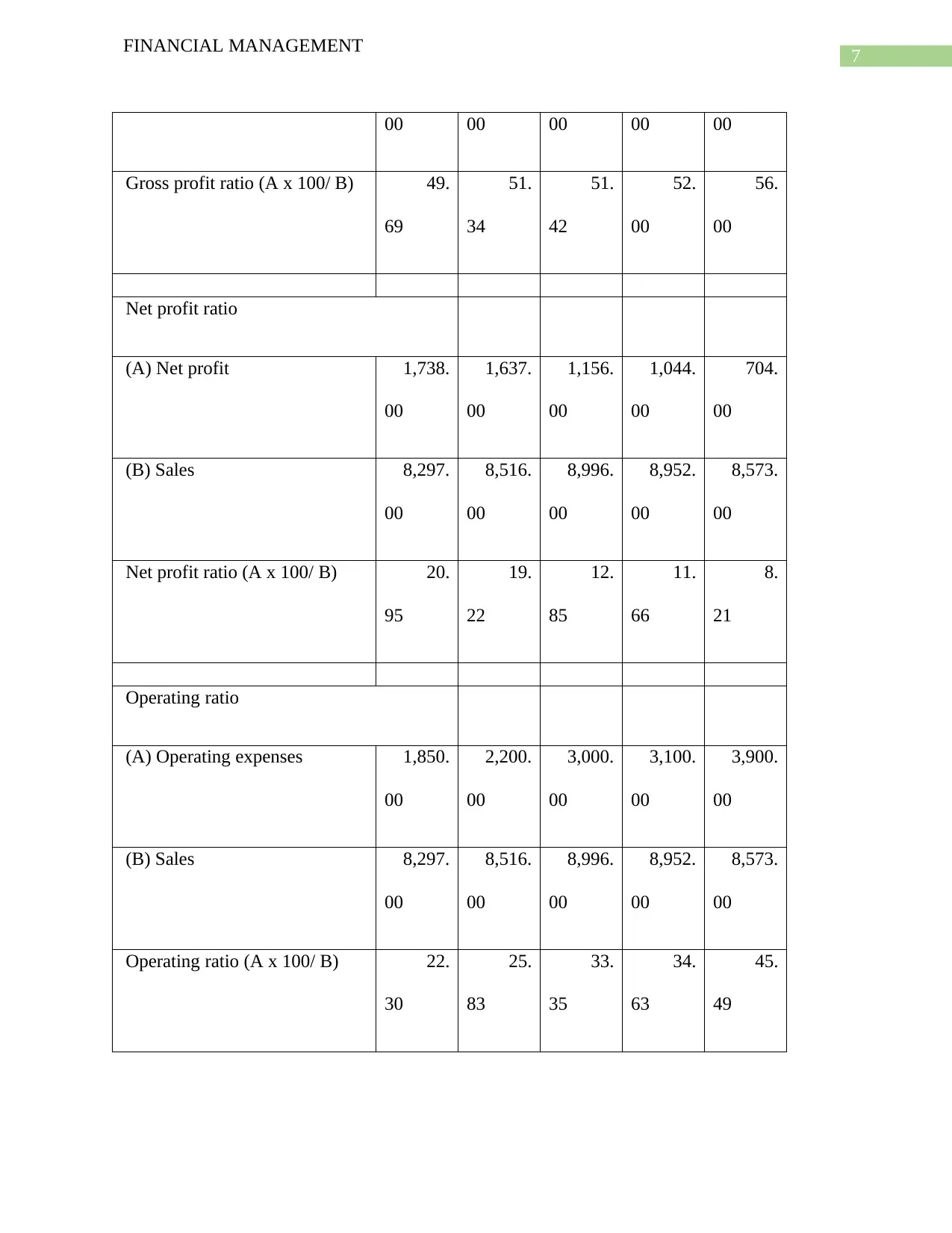

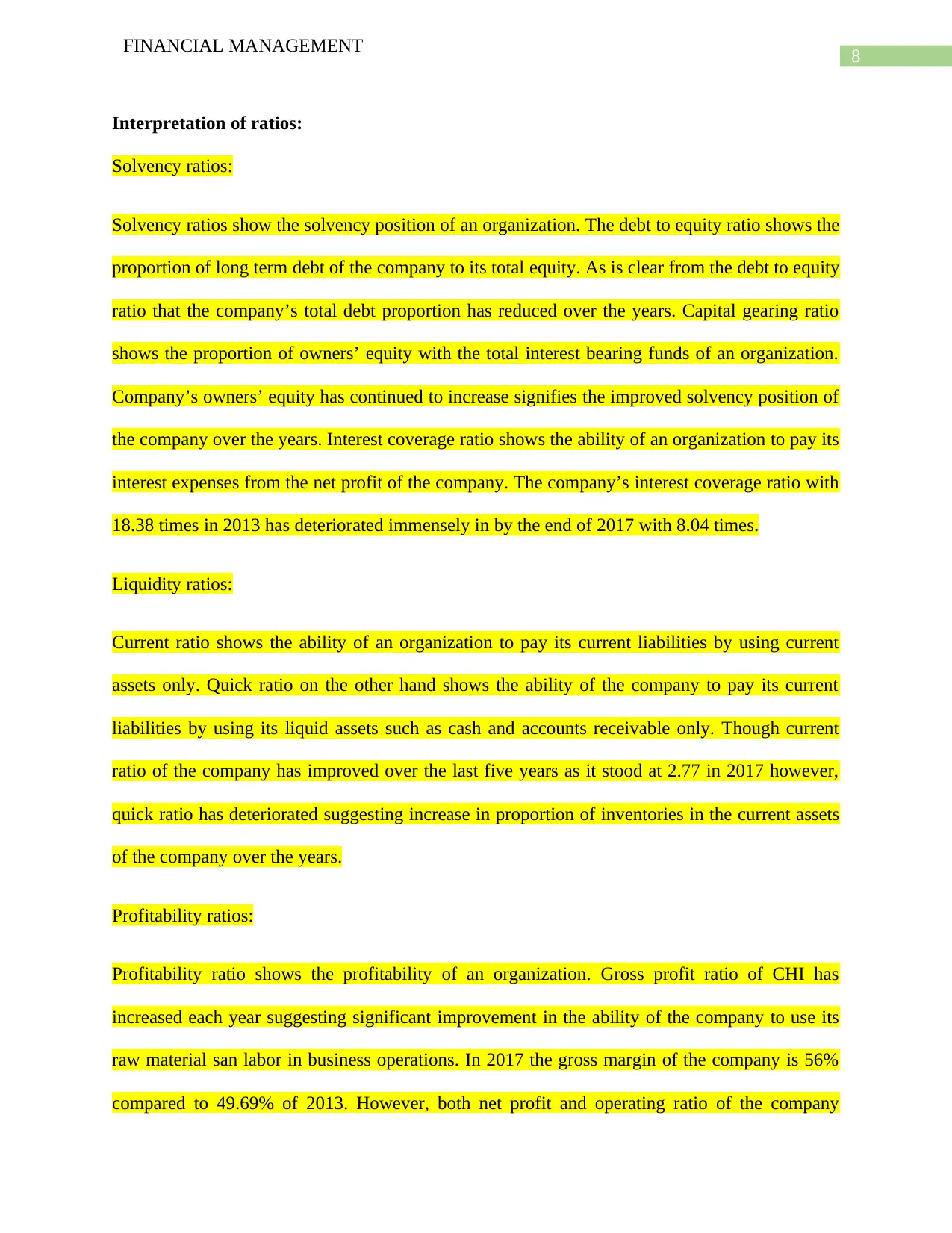

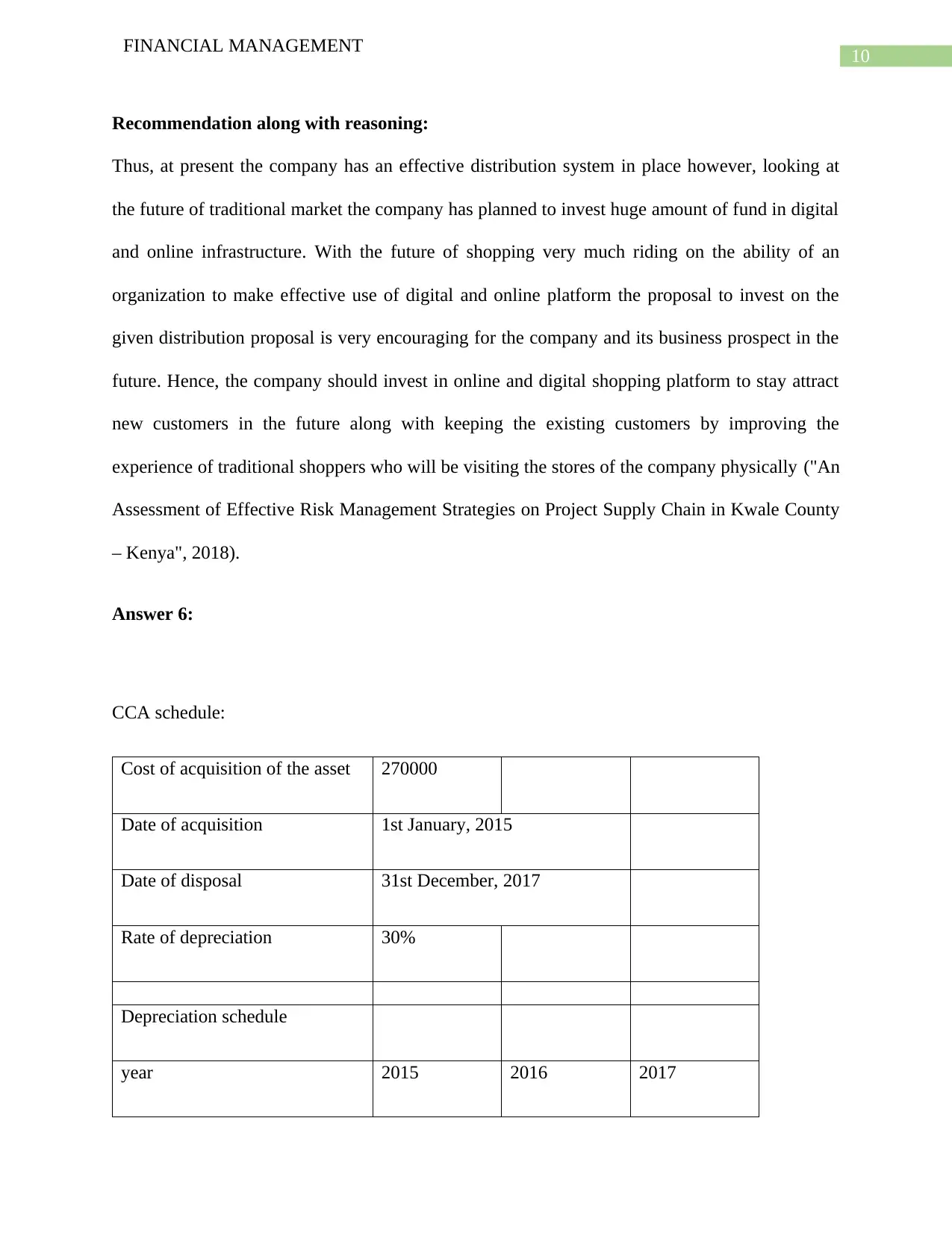

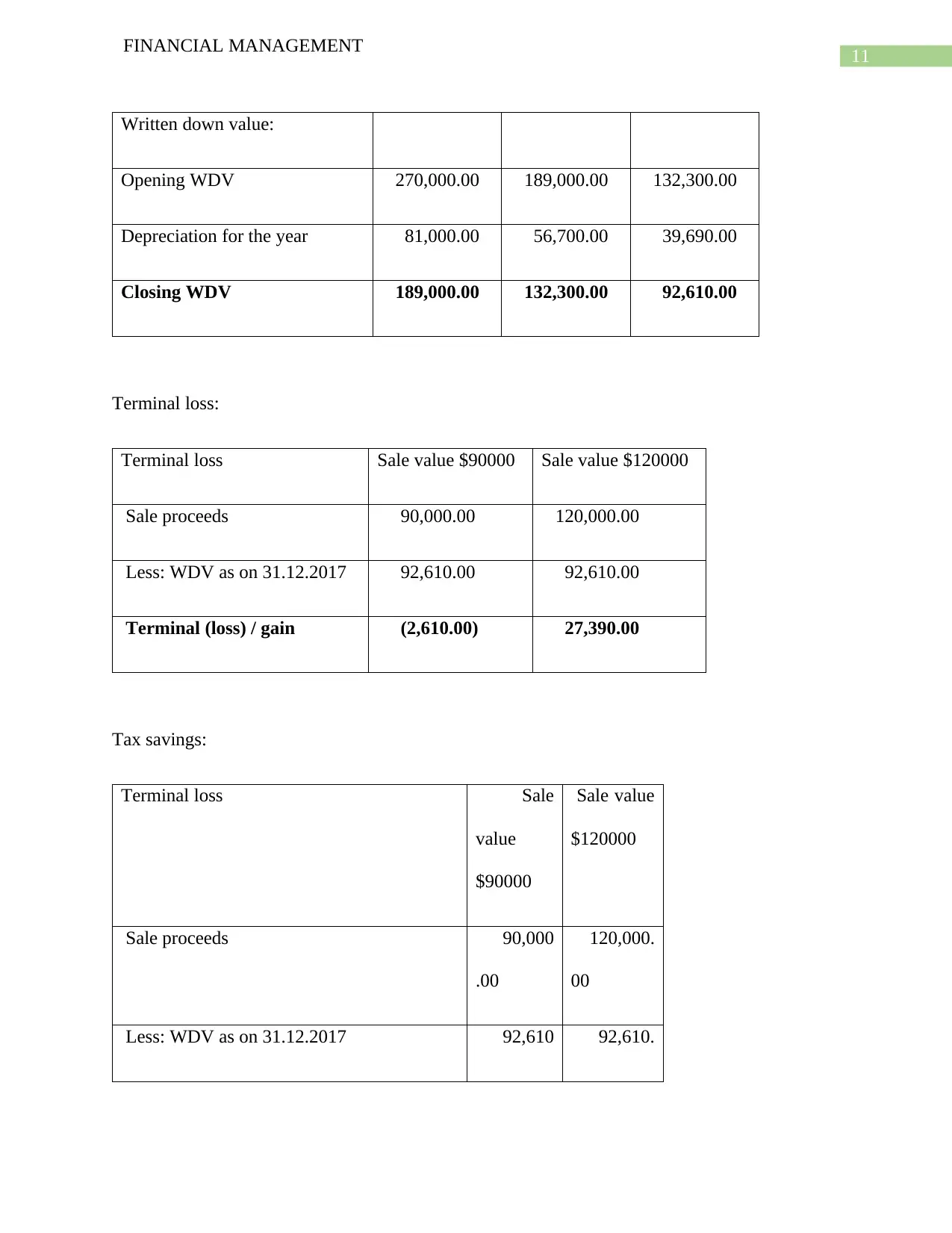

This report presents a comprehensive financial analysis of Canada Hardware (CHI). It begins with a SWOT analysis, evaluating the company's internal strengths and weaknesses, and external opportunities and threats. The report then delves into a detailed ratio analysis, covering solvency, liquidity, and profitability ratios from 2013 to 2017, with interpretations of each. The analysis assesses the company's debt-to-equity, capital gearing, interest coverage, current, quick, gross profit, net profit, and operating ratios. Furthermore, the report evaluates distribution and acquisition proposals, offering recommendations for future financial strategies, particularly focusing on online and digital platform investments. Finally, it includes a CCA (Capital Cost Allowance) schedule, analyzing depreciation, terminal loss, tax savings, and the calculation of the average tax rate, providing a complete overview of CHI's financial position and strategic recommendations.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.