Financial Management Report: Investment Appraisal for Austrochemicals

VerifiedAdded on 2020/04/07

|11

|1462

|44

Report

AI Summary

This financial management report presents an analysis of an investment proposal by Austrochemicals Limited to develop a new medicine for constipation. The report focuses on investment appraisal techniques, specifically Net Present Value (NPV) and Internal Rate of Return (IRR), to evaluate the financial viability of the project. The analysis includes calculations considering both scenarios: with and without contract manufacturing. The report provides a detailed breakdown of NPV and IRR, comparing the outcomes under different assumptions. The author concludes with recommendations on whether the company should invest in the new project, considering the initial investment, potential revenue from contract manufacturing, and the company's existing research and development costs. The report uses financial literature to support its analysis and conclusions, providing a clear framework for making investment decisions.

Running Head: FINANCIAL MANAGEMENT

Financial Management

Name of the Student:

Name of the University:

Authors Note:

Financial Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL MANAGEMENT

Table of Contents

Requirement 1:.................................................................................................................................2

Requirement 2:.................................................................................................................................3

Requirement 3:.................................................................................................................................4

Reference.........................................................................................................................................9

Table of Contents

Requirement 1:.................................................................................................................................2

Requirement 2:.................................................................................................................................3

Requirement 3:.................................................................................................................................4

Reference.........................................................................................................................................9

2FINANCIAL MANAGEMENT

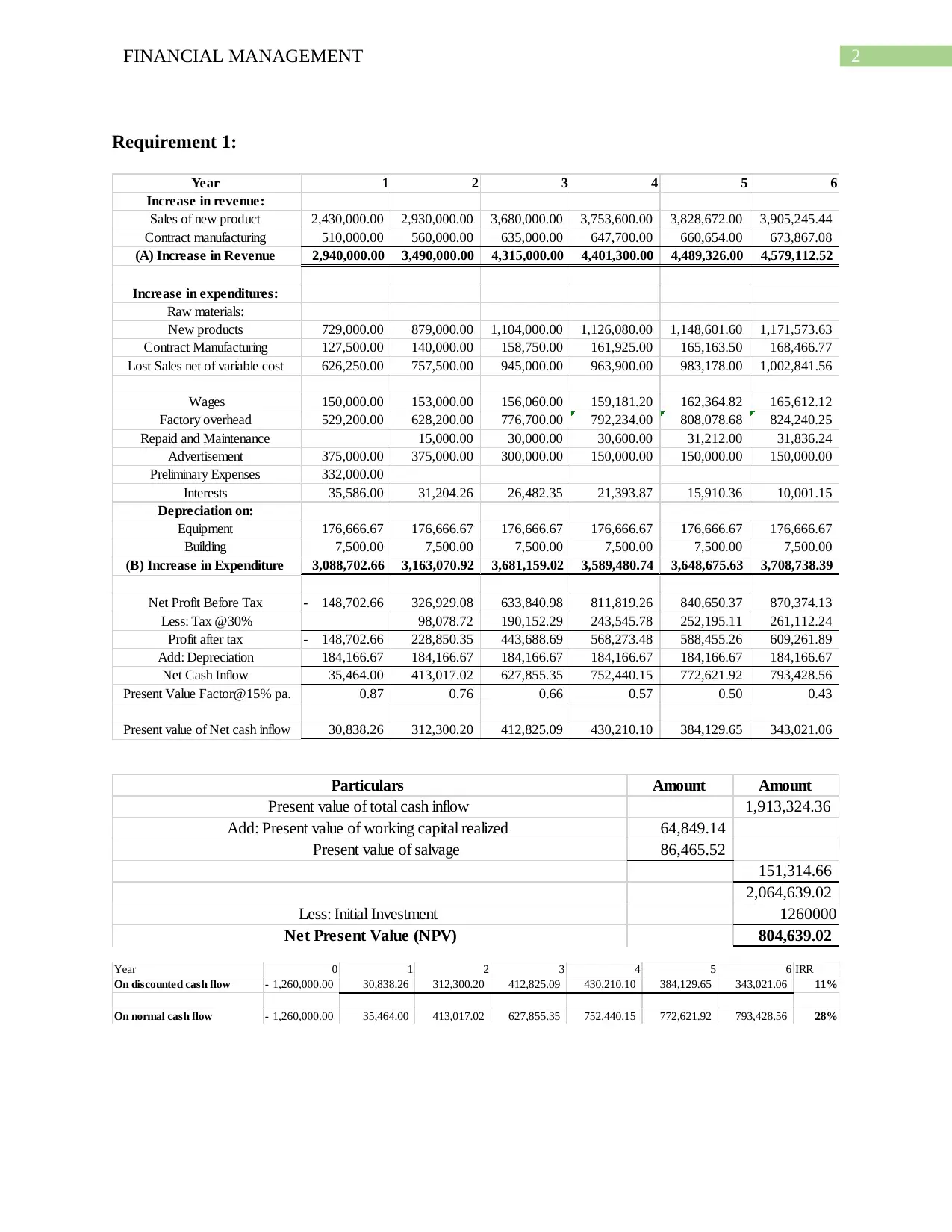

Requirement 1:

Year 1 2 3 4 5 6

Increase in revenue:

Sales of new product 2,430,000.00 2,930,000.00 3,680,000.00 3,753,600.00 3,828,672.00 3,905,245.44

Contract manufacturing 510,000.00 560,000.00 635,000.00 647,700.00 660,654.00 673,867.08

(A) Increase in Revenue 2,940,000.00 3,490,000.00 4,315,000.00 4,401,300.00 4,489,326.00 4,579,112.52

Increase in expenditures:

Raw materials:

New products 729,000.00 879,000.00 1,104,000.00 1,126,080.00 1,148,601.60 1,171,573.63

Contract Manufacturing 127,500.00 140,000.00 158,750.00 161,925.00 165,163.50 168,466.77

Lost Sales net of variable cost 626,250.00 757,500.00 945,000.00 963,900.00 983,178.00 1,002,841.56

Wages 150,000.00 153,000.00 156,060.00 159,181.20 162,364.82 165,612.12

Factory overhead 529,200.00 628,200.00 776,700.00 792,234.00 808,078.68 824,240.25

Repaid and Maintenance 15,000.00 30,000.00 30,600.00 31,212.00 31,836.24

Advertisement 375,000.00 375,000.00 300,000.00 150,000.00 150,000.00 150,000.00

Preliminary Expenses 332,000.00

Interests 35,586.00 31,204.26 26,482.35 21,393.87 15,910.36 10,001.15

Depreciation on:

Equipment 176,666.67 176,666.67 176,666.67 176,666.67 176,666.67 176,666.67

Building 7,500.00 7,500.00 7,500.00 7,500.00 7,500.00 7,500.00

(B) Increase in Expenditure 3,088,702.66 3,163,070.92 3,681,159.02 3,589,480.74 3,648,675.63 3,708,738.39

Net Profit Before Tax 148,702.66- 326,929.08 633,840.98 811,819.26 840,650.37 870,374.13

Less: Tax @30% 98,078.72 190,152.29 243,545.78 252,195.11 261,112.24

Profit after tax 148,702.66- 228,850.35 443,688.69 568,273.48 588,455.26 609,261.89

Add: Depreciation 184,166.67 184,166.67 184,166.67 184,166.67 184,166.67 184,166.67

Net Cash Inflow 35,464.00 413,017.02 627,855.35 752,440.15 772,621.92 793,428.56

Present Value Factor@15% pa. 0.87 0.76 0.66 0.57 0.50 0.43

Present value of Net cash inflow 30,838.26 312,300.20 412,825.09 430,210.10 384,129.65 343,021.06

Particulars Amount Amount

Present value of total cash inflow 1,913,324.36

Add: Present value of working capital realized 64,849.14

Present value of salvage 86,465.52

151,314.66

2,064,639.02

Less: Initial Investment 1260000

Net Present Value (NPV) 804,639.02

Year 0 1 2 3 4 5 6 IRR

On discounted cash flow 1,260,000.00- 30,838.26 312,300.20 412,825.09 430,210.10 384,129.65 343,021.06 11%

On normal cash flow 1,260,000.00- 35,464.00 413,017.02 627,855.35 752,440.15 772,621.92 793,428.56 28%

Requirement 1:

Year 1 2 3 4 5 6

Increase in revenue:

Sales of new product 2,430,000.00 2,930,000.00 3,680,000.00 3,753,600.00 3,828,672.00 3,905,245.44

Contract manufacturing 510,000.00 560,000.00 635,000.00 647,700.00 660,654.00 673,867.08

(A) Increase in Revenue 2,940,000.00 3,490,000.00 4,315,000.00 4,401,300.00 4,489,326.00 4,579,112.52

Increase in expenditures:

Raw materials:

New products 729,000.00 879,000.00 1,104,000.00 1,126,080.00 1,148,601.60 1,171,573.63

Contract Manufacturing 127,500.00 140,000.00 158,750.00 161,925.00 165,163.50 168,466.77

Lost Sales net of variable cost 626,250.00 757,500.00 945,000.00 963,900.00 983,178.00 1,002,841.56

Wages 150,000.00 153,000.00 156,060.00 159,181.20 162,364.82 165,612.12

Factory overhead 529,200.00 628,200.00 776,700.00 792,234.00 808,078.68 824,240.25

Repaid and Maintenance 15,000.00 30,000.00 30,600.00 31,212.00 31,836.24

Advertisement 375,000.00 375,000.00 300,000.00 150,000.00 150,000.00 150,000.00

Preliminary Expenses 332,000.00

Interests 35,586.00 31,204.26 26,482.35 21,393.87 15,910.36 10,001.15

Depreciation on:

Equipment 176,666.67 176,666.67 176,666.67 176,666.67 176,666.67 176,666.67

Building 7,500.00 7,500.00 7,500.00 7,500.00 7,500.00 7,500.00

(B) Increase in Expenditure 3,088,702.66 3,163,070.92 3,681,159.02 3,589,480.74 3,648,675.63 3,708,738.39

Net Profit Before Tax 148,702.66- 326,929.08 633,840.98 811,819.26 840,650.37 870,374.13

Less: Tax @30% 98,078.72 190,152.29 243,545.78 252,195.11 261,112.24

Profit after tax 148,702.66- 228,850.35 443,688.69 568,273.48 588,455.26 609,261.89

Add: Depreciation 184,166.67 184,166.67 184,166.67 184,166.67 184,166.67 184,166.67

Net Cash Inflow 35,464.00 413,017.02 627,855.35 752,440.15 772,621.92 793,428.56

Present Value Factor@15% pa. 0.87 0.76 0.66 0.57 0.50 0.43

Present value of Net cash inflow 30,838.26 312,300.20 412,825.09 430,210.10 384,129.65 343,021.06

Particulars Amount Amount

Present value of total cash inflow 1,913,324.36

Add: Present value of working capital realized 64,849.14

Present value of salvage 86,465.52

151,314.66

2,064,639.02

Less: Initial Investment 1260000

Net Present Value (NPV) 804,639.02

Year 0 1 2 3 4 5 6 IRR

On discounted cash flow 1,260,000.00- 30,838.26 312,300.20 412,825.09 430,210.10 384,129.65 343,021.06 11%

On normal cash flow 1,260,000.00- 35,464.00 413,017.02 627,855.35 752,440.15 772,621.92 793,428.56 28%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL MANAGEMENT

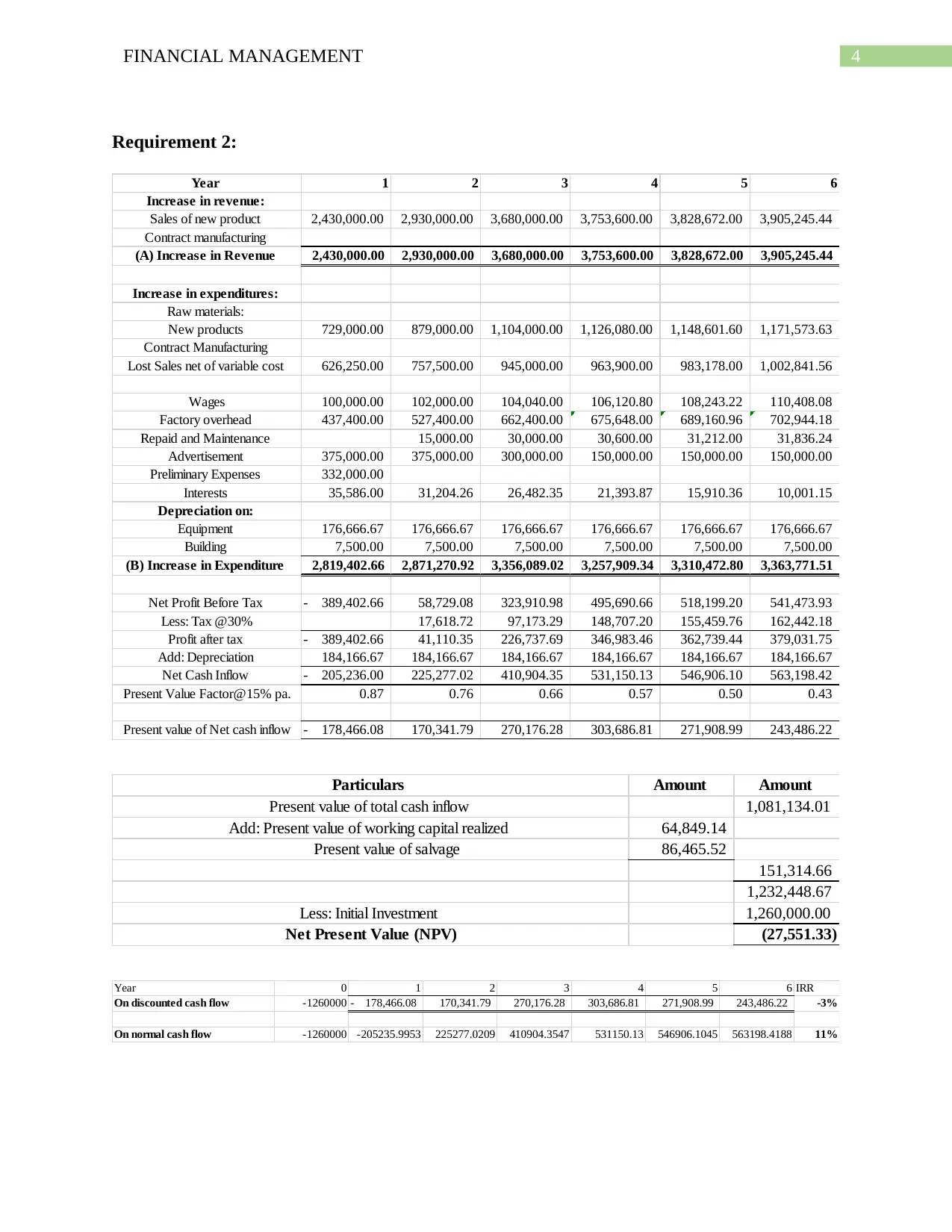

Requirement 2:

Year 1 2 3 4 5 6

Increase in revenue:

Sales of new product 2,430,000.00 2,930,000.00 3,680,000.00 3,753,600.00 3,828,672.00 3,905,245.44

Contract manufacturing

(A) Increase in Revenue 2,430,000.00 2,930,000.00 3,680,000.00 3,753,600.00 3,828,672.00 3,905,245.44

Increase in expenditures:

Raw materials:

New products 729,000.00 879,000.00 1,104,000.00 1,126,080.00 1,148,601.60 1,171,573.63

Contract Manufacturing

Lost Sales net of variable cost 626,250.00 757,500.00 945,000.00 963,900.00 983,178.00 1,002,841.56

Wages 100,000.00 102,000.00 104,040.00 106,120.80 108,243.22 110,408.08

Factory overhead 437,400.00 527,400.00 662,400.00 675,648.00 689,160.96 702,944.18

Repaid and Maintenance 15,000.00 30,000.00 30,600.00 31,212.00 31,836.24

Advertisement 375,000.00 375,000.00 300,000.00 150,000.00 150,000.00 150,000.00

Preliminary Expenses 332,000.00

Interests 35,586.00 31,204.26 26,482.35 21,393.87 15,910.36 10,001.15

Depreciation on:

Equipment 176,666.67 176,666.67 176,666.67 176,666.67 176,666.67 176,666.67

Building 7,500.00 7,500.00 7,500.00 7,500.00 7,500.00 7,500.00

(B) Increase in Expenditure 2,819,402.66 2,871,270.92 3,356,089.02 3,257,909.34 3,310,472.80 3,363,771.51

Net Profit Before Tax 389,402.66- 58,729.08 323,910.98 495,690.66 518,199.20 541,473.93

Less: Tax @30% 17,618.72 97,173.29 148,707.20 155,459.76 162,442.18

Profit after tax 389,402.66- 41,110.35 226,737.69 346,983.46 362,739.44 379,031.75

Add: Depreciation 184,166.67 184,166.67 184,166.67 184,166.67 184,166.67 184,166.67

Net Cash Inflow 205,236.00- 225,277.02 410,904.35 531,150.13 546,906.10 563,198.42

Present Value Factor@15% pa. 0.87 0.76 0.66 0.57 0.50 0.43

Present value of Net cash inflow 178,466.08- 170,341.79 270,176.28 303,686.81 271,908.99 243,486.22

Particulars Amount Amount

Present value of total cash inflow 1,081,134.01

Add: Present value of working capital realized 64,849.14

Present value of salvage 86,465.52

151,314.66

1,232,448.67

Less: Initial Investment 1,260,000.00

Net Present Value (NPV) (27,551.33)

Year 0 1 2 3 4 5 6 IRR

On discounted cash flow -1260000 178,466.08- 170,341.79 270,176.28 303,686.81 271,908.99 243,486.22 -3%

On normal cash flow -1260000 -205235.9953 225277.0209 410904.3547 531150.13 546906.1045 563198.4188 11%

Requirement 2:

Year 1 2 3 4 5 6

Increase in revenue:

Sales of new product 2,430,000.00 2,930,000.00 3,680,000.00 3,753,600.00 3,828,672.00 3,905,245.44

Contract manufacturing

(A) Increase in Revenue 2,430,000.00 2,930,000.00 3,680,000.00 3,753,600.00 3,828,672.00 3,905,245.44

Increase in expenditures:

Raw materials:

New products 729,000.00 879,000.00 1,104,000.00 1,126,080.00 1,148,601.60 1,171,573.63

Contract Manufacturing

Lost Sales net of variable cost 626,250.00 757,500.00 945,000.00 963,900.00 983,178.00 1,002,841.56

Wages 100,000.00 102,000.00 104,040.00 106,120.80 108,243.22 110,408.08

Factory overhead 437,400.00 527,400.00 662,400.00 675,648.00 689,160.96 702,944.18

Repaid and Maintenance 15,000.00 30,000.00 30,600.00 31,212.00 31,836.24

Advertisement 375,000.00 375,000.00 300,000.00 150,000.00 150,000.00 150,000.00

Preliminary Expenses 332,000.00

Interests 35,586.00 31,204.26 26,482.35 21,393.87 15,910.36 10,001.15

Depreciation on:

Equipment 176,666.67 176,666.67 176,666.67 176,666.67 176,666.67 176,666.67

Building 7,500.00 7,500.00 7,500.00 7,500.00 7,500.00 7,500.00

(B) Increase in Expenditure 2,819,402.66 2,871,270.92 3,356,089.02 3,257,909.34 3,310,472.80 3,363,771.51

Net Profit Before Tax 389,402.66- 58,729.08 323,910.98 495,690.66 518,199.20 541,473.93

Less: Tax @30% 17,618.72 97,173.29 148,707.20 155,459.76 162,442.18

Profit after tax 389,402.66- 41,110.35 226,737.69 346,983.46 362,739.44 379,031.75

Add: Depreciation 184,166.67 184,166.67 184,166.67 184,166.67 184,166.67 184,166.67

Net Cash Inflow 205,236.00- 225,277.02 410,904.35 531,150.13 546,906.10 563,198.42

Present Value Factor@15% pa. 0.87 0.76 0.66 0.57 0.50 0.43

Present value of Net cash inflow 178,466.08- 170,341.79 270,176.28 303,686.81 271,908.99 243,486.22

Particulars Amount Amount

Present value of total cash inflow 1,081,134.01

Add: Present value of working capital realized 64,849.14

Present value of salvage 86,465.52

151,314.66

1,232,448.67

Less: Initial Investment 1,260,000.00

Net Present Value (NPV) (27,551.33)

Year 0 1 2 3 4 5 6 IRR

On discounted cash flow -1260000 178,466.08- 170,341.79 270,176.28 303,686.81 271,908.99 243,486.22 -3%

On normal cash flow -1260000 -205235.9953 225277.0209 410904.3547 531150.13 546906.1045 563198.4188 11%

5FINANCIAL MANAGEMENT

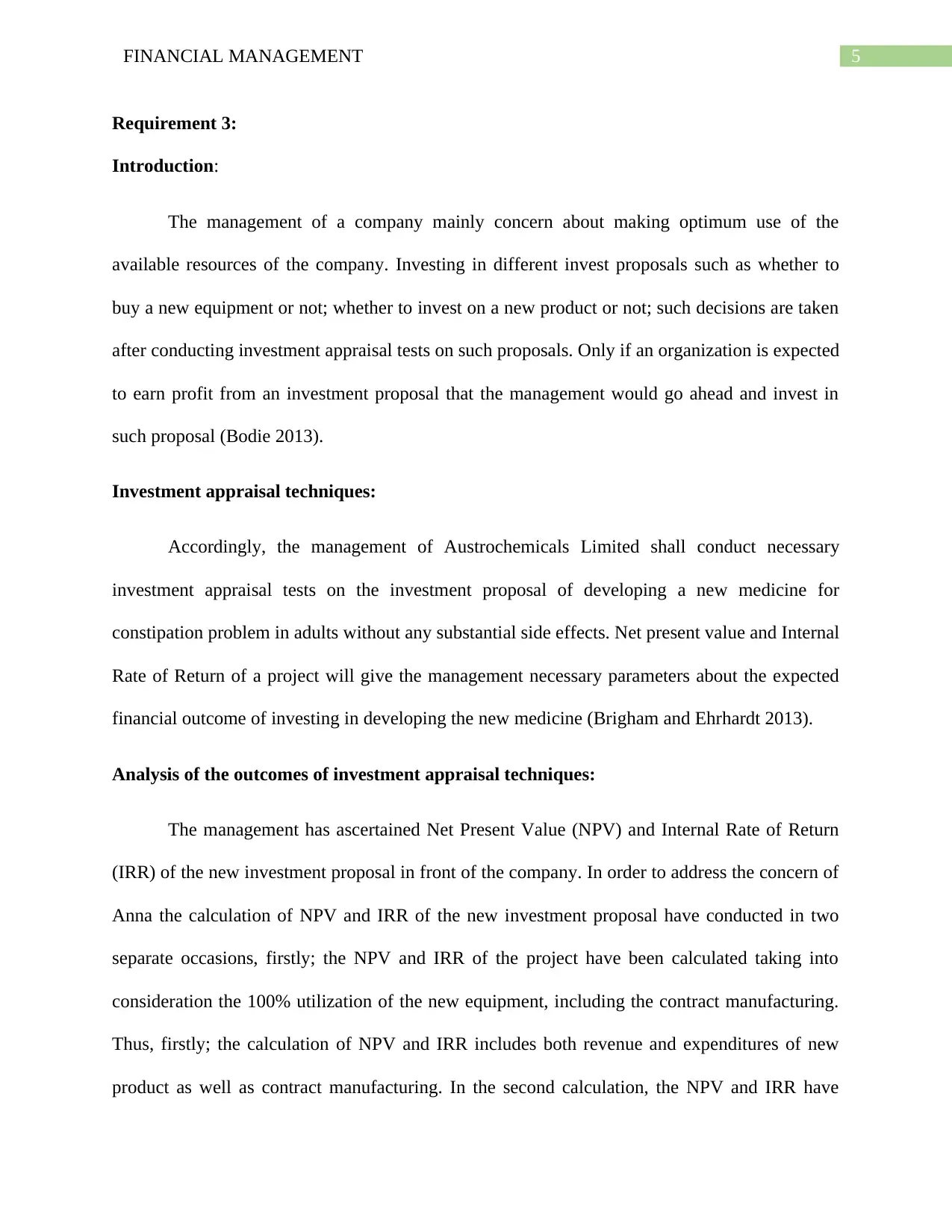

Requirement 3:

Introduction:

The management of a company mainly concern about making optimum use of the

available resources of the company. Investing in different invest proposals such as whether to

buy a new equipment or not; whether to invest on a new product or not; such decisions are taken

after conducting investment appraisal tests on such proposals. Only if an organization is expected

to earn profit from an investment proposal that the management would go ahead and invest in

such proposal (Bodie 2013).

Investment appraisal techniques:

Accordingly, the management of Austrochemicals Limited shall conduct necessary

investment appraisal tests on the investment proposal of developing a new medicine for

constipation problem in adults without any substantial side effects. Net present value and Internal

Rate of Return of a project will give the management necessary parameters about the expected

financial outcome of investing in developing the new medicine (Brigham and Ehrhardt 2013).

Analysis of the outcomes of investment appraisal techniques:

The management has ascertained Net Present Value (NPV) and Internal Rate of Return

(IRR) of the new investment proposal in front of the company. In order to address the concern of

Anna the calculation of NPV and IRR of the new investment proposal have conducted in two

separate occasions, firstly; the NPV and IRR of the project have been calculated taking into

consideration the 100% utilization of the new equipment, including the contract manufacturing.

Thus, firstly; the calculation of NPV and IRR includes both revenue and expenditures of new

product as well as contract manufacturing. In the second calculation, the NPV and IRR have

Requirement 3:

Introduction:

The management of a company mainly concern about making optimum use of the

available resources of the company. Investing in different invest proposals such as whether to

buy a new equipment or not; whether to invest on a new product or not; such decisions are taken

after conducting investment appraisal tests on such proposals. Only if an organization is expected

to earn profit from an investment proposal that the management would go ahead and invest in

such proposal (Bodie 2013).

Investment appraisal techniques:

Accordingly, the management of Austrochemicals Limited shall conduct necessary

investment appraisal tests on the investment proposal of developing a new medicine for

constipation problem in adults without any substantial side effects. Net present value and Internal

Rate of Return of a project will give the management necessary parameters about the expected

financial outcome of investing in developing the new medicine (Brigham and Ehrhardt 2013).

Analysis of the outcomes of investment appraisal techniques:

The management has ascertained Net Present Value (NPV) and Internal Rate of Return

(IRR) of the new investment proposal in front of the company. In order to address the concern of

Anna the calculation of NPV and IRR of the new investment proposal have conducted in two

separate occasions, firstly; the NPV and IRR of the project have been calculated taking into

consideration the 100% utilization of the new equipment, including the contract manufacturing.

Thus, firstly; the calculation of NPV and IRR includes both revenue and expenditures of new

product as well as contract manufacturing. In the second calculation, the NPV and IRR have

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL MANAGEMENT

been calculated only assuming that the new equipment will only be used for development of new

medicine and thus, the expenditures and revenue from contract manufacturing were ignored

(Leary, M.T. and Roberts 2014).

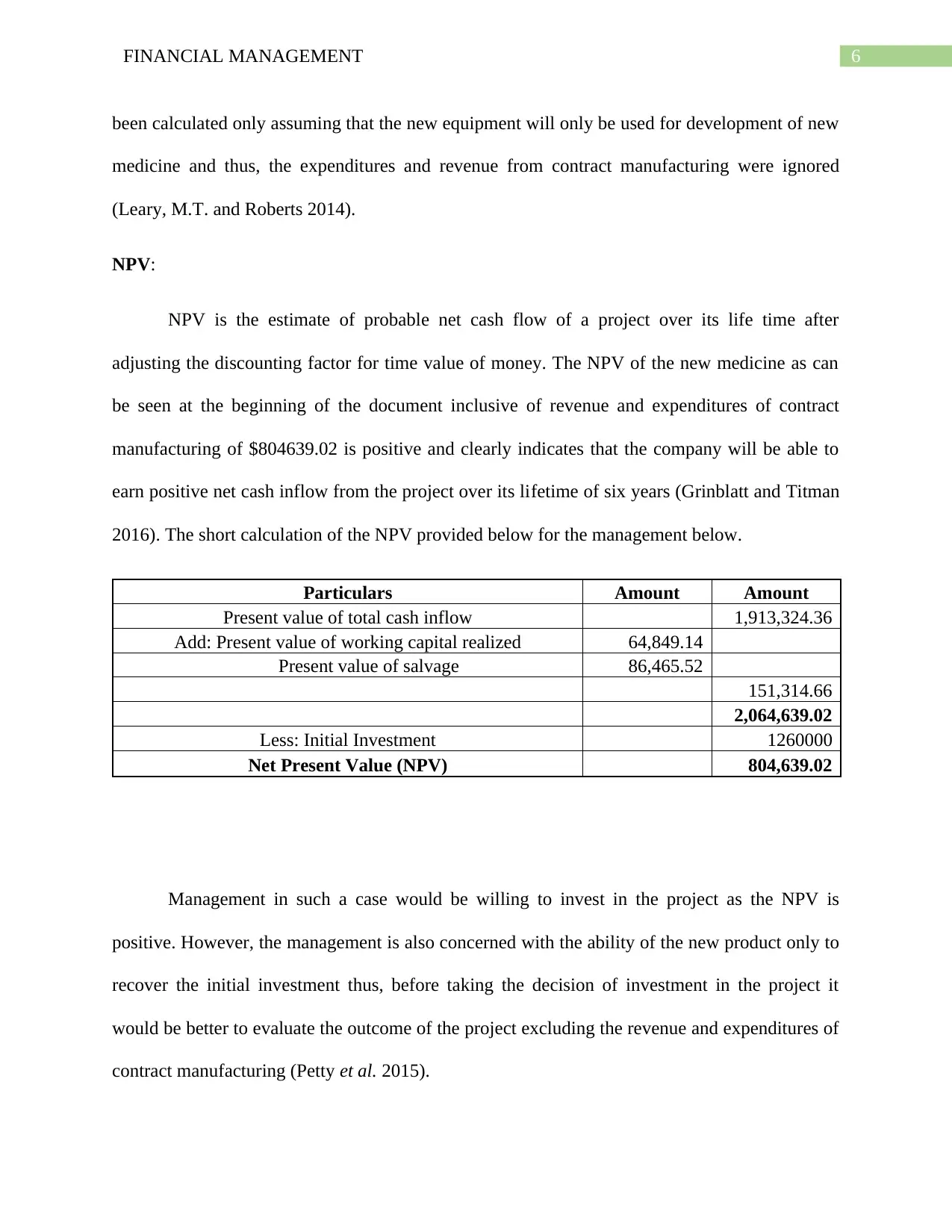

NPV:

NPV is the estimate of probable net cash flow of a project over its life time after

adjusting the discounting factor for time value of money. The NPV of the new medicine as can

be seen at the beginning of the document inclusive of revenue and expenditures of contract

manufacturing of $804639.02 is positive and clearly indicates that the company will be able to

earn positive net cash inflow from the project over its lifetime of six years (Grinblatt and Titman

2016). The short calculation of the NPV provided below for the management below.

Particulars Amount Amount

Present value of total cash inflow 1,913,324.36

Add: Present value of working capital realized 64,849.14

Present value of salvage 86,465.52

151,314.66

2,064,639.02

Less: Initial Investment 1260000

Net Present Value (NPV) 804,639.02

Management in such a case would be willing to invest in the project as the NPV is

positive. However, the management is also concerned with the ability of the new product only to

recover the initial investment thus, before taking the decision of investment in the project it

would be better to evaluate the outcome of the project excluding the revenue and expenditures of

contract manufacturing (Petty et al. 2015).

been calculated only assuming that the new equipment will only be used for development of new

medicine and thus, the expenditures and revenue from contract manufacturing were ignored

(Leary, M.T. and Roberts 2014).

NPV:

NPV is the estimate of probable net cash flow of a project over its life time after

adjusting the discounting factor for time value of money. The NPV of the new medicine as can

be seen at the beginning of the document inclusive of revenue and expenditures of contract

manufacturing of $804639.02 is positive and clearly indicates that the company will be able to

earn positive net cash inflow from the project over its lifetime of six years (Grinblatt and Titman

2016). The short calculation of the NPV provided below for the management below.

Particulars Amount Amount

Present value of total cash inflow 1,913,324.36

Add: Present value of working capital realized 64,849.14

Present value of salvage 86,465.52

151,314.66

2,064,639.02

Less: Initial Investment 1260000

Net Present Value (NPV) 804,639.02

Management in such a case would be willing to invest in the project as the NPV is

positive. However, the management is also concerned with the ability of the new product only to

recover the initial investment thus, before taking the decision of investment in the project it

would be better to evaluate the outcome of the project excluding the revenue and expenditures of

contract manufacturing (Petty et al. 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL MANAGEMENT

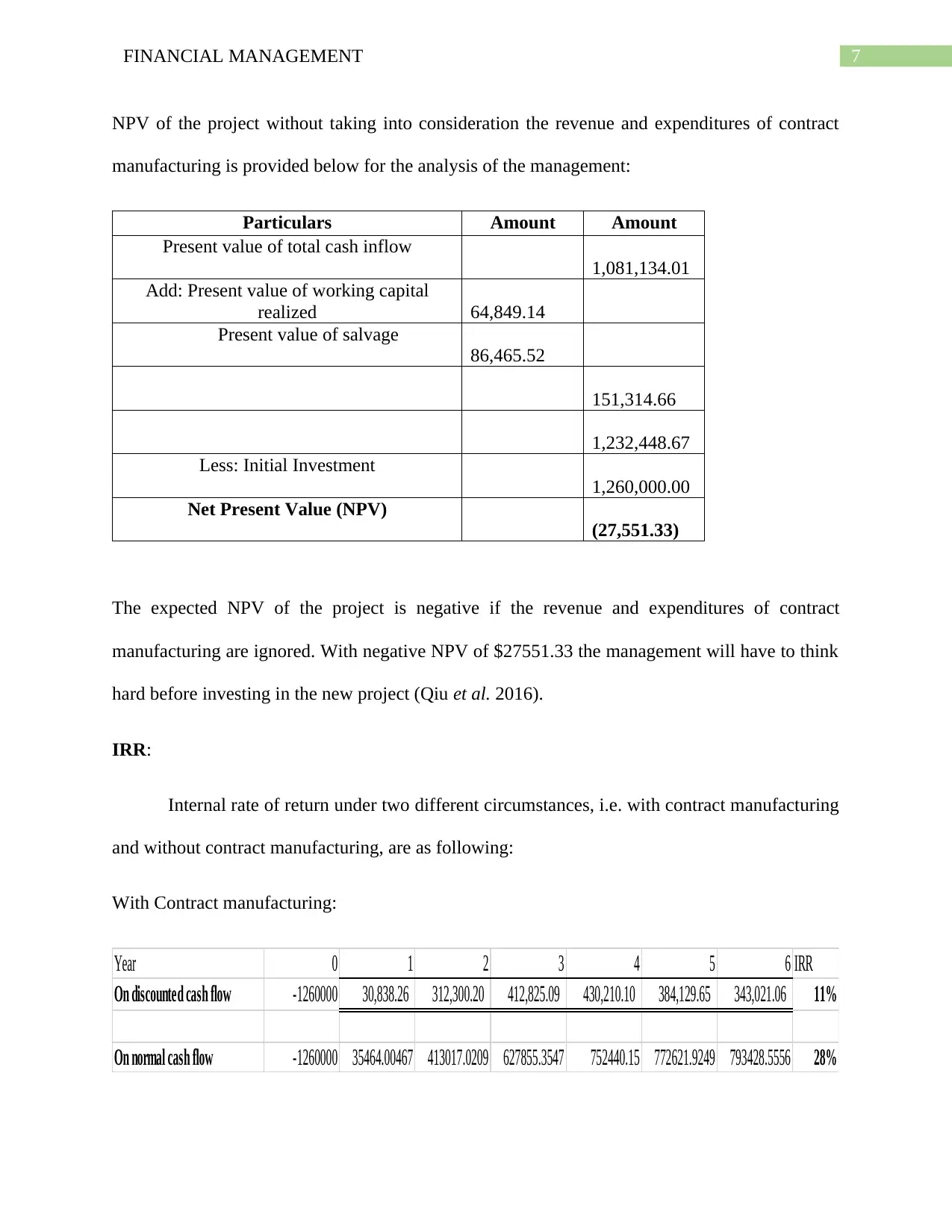

NPV of the project without taking into consideration the revenue and expenditures of contract

manufacturing is provided below for the analysis of the management:

Particulars Amount Amount

Present value of total cash inflow

1,081,134.01

Add: Present value of working capital

realized 64,849.14

Present value of salvage

86,465.52

151,314.66

1,232,448.67

Less: Initial Investment

1,260,000.00

Net Present Value (NPV)

(27,551.33)

The expected NPV of the project is negative if the revenue and expenditures of contract

manufacturing are ignored. With negative NPV of $27551.33 the management will have to think

hard before investing in the new project (Qiu et al. 2016).

IRR:

Internal rate of return under two different circumstances, i.e. with contract manufacturing

and without contract manufacturing, are as following:

With Contract manufacturing:

Year 0 1 2 3 4 5 6 IRR

On discounted cash flow -1260000 30,838.26 312,300.20 412,825.09 430,210.10 384,129.65 343,021.06 11%

On normal cash flow -1260000 35464.00467 413017.0209 627855.3547 752440.15 772621.9249 793428.5556 28%

NPV of the project without taking into consideration the revenue and expenditures of contract

manufacturing is provided below for the analysis of the management:

Particulars Amount Amount

Present value of total cash inflow

1,081,134.01

Add: Present value of working capital

realized 64,849.14

Present value of salvage

86,465.52

151,314.66

1,232,448.67

Less: Initial Investment

1,260,000.00

Net Present Value (NPV)

(27,551.33)

The expected NPV of the project is negative if the revenue and expenditures of contract

manufacturing are ignored. With negative NPV of $27551.33 the management will have to think

hard before investing in the new project (Qiu et al. 2016).

IRR:

Internal rate of return under two different circumstances, i.e. with contract manufacturing

and without contract manufacturing, are as following:

With Contract manufacturing:

Year 0 1 2 3 4 5 6 IRR

On discounted cash flow -1260000 30,838.26 312,300.20 412,825.09 430,210.10 384,129.65 343,021.06 11%

On normal cash flow -1260000 35464.00467 413017.0209 627855.3547 752440.15 772621.9249 793428.5556 28%

8FINANCIAL MANAGEMENT

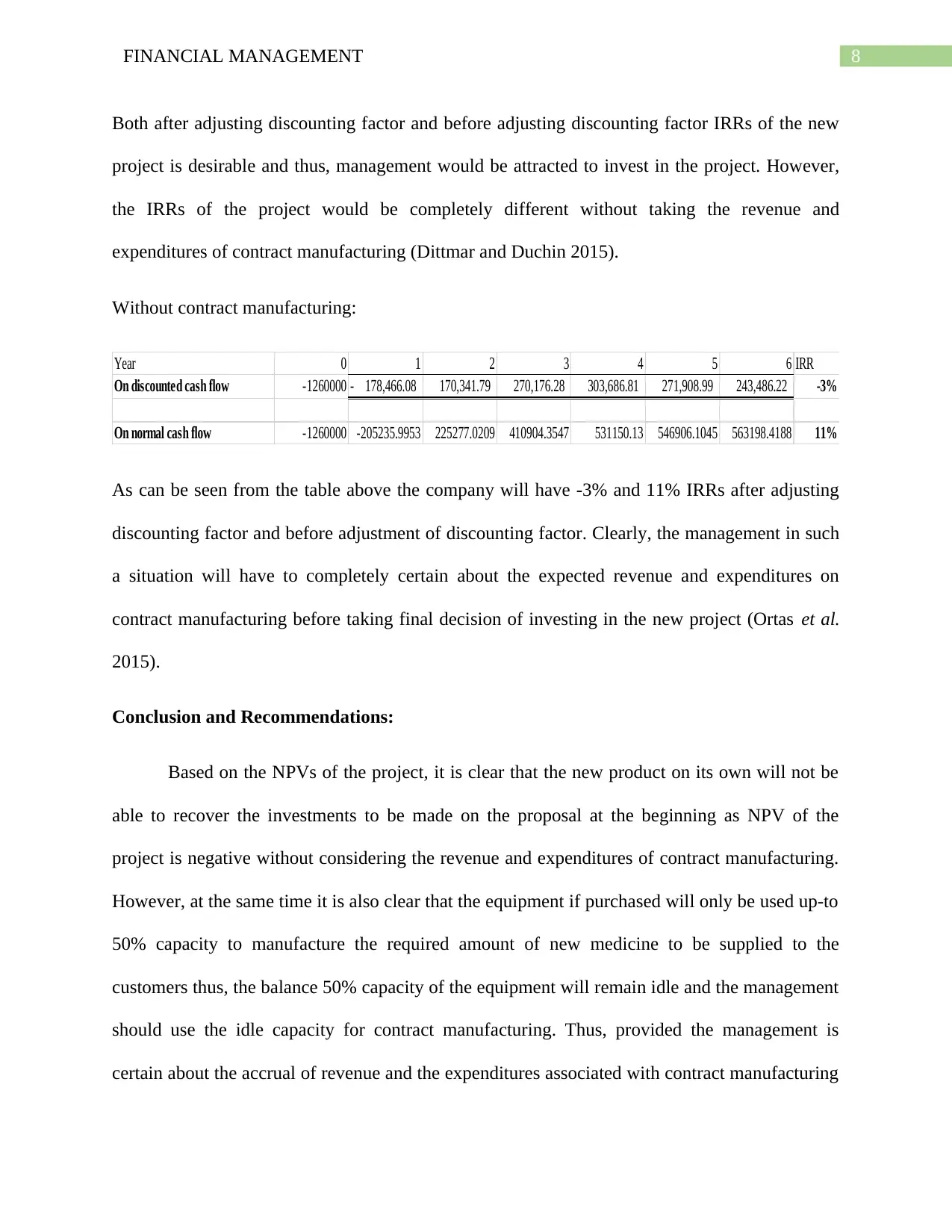

Both after adjusting discounting factor and before adjusting discounting factor IRRs of the new

project is desirable and thus, management would be attracted to invest in the project. However,

the IRRs of the project would be completely different without taking the revenue and

expenditures of contract manufacturing (Dittmar and Duchin 2015).

Without contract manufacturing:

Year 0 1 2 3 4 5 6 IRR

On discounted cash flow -1260000 178,466.08- 170,341.79 270,176.28 303,686.81 271,908.99 243,486.22 -3%

On normal cash flow -1260000 -205235.9953 225277.0209 410904.3547 531150.13 546906.1045 563198.4188 11%

As can be seen from the table above the company will have -3% and 11% IRRs after adjusting

discounting factor and before adjustment of discounting factor. Clearly, the management in such

a situation will have to completely certain about the expected revenue and expenditures on

contract manufacturing before taking final decision of investing in the new project (Ortas et al.

2015).

Conclusion and Recommendations:

Based on the NPVs of the project, it is clear that the new product on its own will not be

able to recover the investments to be made on the proposal at the beginning as NPV of the

project is negative without considering the revenue and expenditures of contract manufacturing.

However, at the same time it is also clear that the equipment if purchased will only be used up-to

50% capacity to manufacture the required amount of new medicine to be supplied to the

customers thus, the balance 50% capacity of the equipment will remain idle and the management

should use the idle capacity for contract manufacturing. Thus, provided the management is

certain about the accrual of revenue and the expenditures associated with contract manufacturing

Both after adjusting discounting factor and before adjusting discounting factor IRRs of the new

project is desirable and thus, management would be attracted to invest in the project. However,

the IRRs of the project would be completely different without taking the revenue and

expenditures of contract manufacturing (Dittmar and Duchin 2015).

Without contract manufacturing:

Year 0 1 2 3 4 5 6 IRR

On discounted cash flow -1260000 178,466.08- 170,341.79 270,176.28 303,686.81 271,908.99 243,486.22 -3%

On normal cash flow -1260000 -205235.9953 225277.0209 410904.3547 531150.13 546906.1045 563198.4188 11%

As can be seen from the table above the company will have -3% and 11% IRRs after adjusting

discounting factor and before adjustment of discounting factor. Clearly, the management in such

a situation will have to completely certain about the expected revenue and expenditures on

contract manufacturing before taking final decision of investing in the new project (Ortas et al.

2015).

Conclusion and Recommendations:

Based on the NPVs of the project, it is clear that the new product on its own will not be

able to recover the investments to be made on the proposal at the beginning as NPV of the

project is negative without considering the revenue and expenditures of contract manufacturing.

However, at the same time it is also clear that the equipment if purchased will only be used up-to

50% capacity to manufacture the required amount of new medicine to be supplied to the

customers thus, the balance 50% capacity of the equipment will remain idle and the management

should use the idle capacity for contract manufacturing. Thus, provided the management is

certain about the accrual of revenue and the expenditures associated with contract manufacturing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL MANAGEMENT

then ,the management should invest in the new project to develop the medicine and shared the

balance 50% capacity of the of equipment for contract manufacturing. IRR of the project before

adjustment of discounting factor at 28% and after adjustment of discounting rate 15% per annum

at 11% are also desirable from the point of view of AL. Thus, the management should go ahead

and make investment to acquire the new equipment necessary for development of the medicine.

The NPV of the investment proposal even if negative without considering the revenue

and expenditures of contract manufacturing with - $27551.33 however, still the management

should invest in the project even if the contract manufacturing does not materialize. This is

despite that fact that the IRR of the project with discounted cash inflow is -3% because the

company has already incurred expenditure on research and development of the medicine of

$332000.00 and if the management decides not invest in the development of the new medicine

then the loss would be far greater than -$27551.33 with $332000.00. Hence, the company should

invest $1260000.00 to acquire the new equipment needed for the development of the

constipation medicine.

then ,the management should invest in the new project to develop the medicine and shared the

balance 50% capacity of the of equipment for contract manufacturing. IRR of the project before

adjustment of discounting factor at 28% and after adjustment of discounting rate 15% per annum

at 11% are also desirable from the point of view of AL. Thus, the management should go ahead

and make investment to acquire the new equipment necessary for development of the medicine.

The NPV of the investment proposal even if negative without considering the revenue

and expenditures of contract manufacturing with - $27551.33 however, still the management

should invest in the project even if the contract manufacturing does not materialize. This is

despite that fact that the IRR of the project with discounted cash inflow is -3% because the

company has already incurred expenditure on research and development of the medicine of

$332000.00 and if the management decides not invest in the development of the new medicine

then the loss would be far greater than -$27551.33 with $332000.00. Hence, the company should

invest $1260000.00 to acquire the new equipment needed for the development of the

constipation medicine.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL MANAGEMENT

Reference

Bodie, Z., 2013. Investments. McGraw-Hill.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Dittmar, A. and Duchin, R., 2015. Looking in the Rearview Mirror: The Effect of Managers'

Professional Experience on Corporate Financial Policy. The Review of Financial Studies, 29(3),

pp.565-602.

Grinblatt, M. and Titman, S., 2016. Financial markets & corporate strategy.

Leary, M.T. and Roberts, M.R., 2014. Do peer firms affect corporate financial policy?. The

Journal of Finance, 69(1), pp.139-178.

Ortas, E., Gallego‐Alvarez, I. and Álvarez Etxeberria, I., 2015. Financial factors influencing the

quality of corporate social responsibility and environmental management disclosure: A quantile

regression approach. Corporate Social Responsibility and Environmental Management, 22(6),

pp.362-380.

Petty, J.W., Titman, S., Keown, A.J., Martin, P., Martin, J.D. and Burrow, M., 2015. Financial

management: Principles and applications. Pearson Higher Education AU.

Qiu, Y., Shaukat, A. and Tharyan, R., 2016. Environmental and social disclosures: Link with

corporate financial performance. The British Accounting Review, 48(1), pp.102-116.

Reference

Bodie, Z., 2013. Investments. McGraw-Hill.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Dittmar, A. and Duchin, R., 2015. Looking in the Rearview Mirror: The Effect of Managers'

Professional Experience on Corporate Financial Policy. The Review of Financial Studies, 29(3),

pp.565-602.

Grinblatt, M. and Titman, S., 2016. Financial markets & corporate strategy.

Leary, M.T. and Roberts, M.R., 2014. Do peer firms affect corporate financial policy?. The

Journal of Finance, 69(1), pp.139-178.

Ortas, E., Gallego‐Alvarez, I. and Álvarez Etxeberria, I., 2015. Financial factors influencing the

quality of corporate social responsibility and environmental management disclosure: A quantile

regression approach. Corporate Social Responsibility and Environmental Management, 22(6),

pp.362-380.

Petty, J.W., Titman, S., Keown, A.J., Martin, P., Martin, J.D. and Burrow, M., 2015. Financial

management: Principles and applications. Pearson Higher Education AU.

Qiu, Y., Shaukat, A. and Tharyan, R., 2016. Environmental and social disclosures: Link with

corporate financial performance. The British Accounting Review, 48(1), pp.102-116.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.