Financial Management Report: Cash Conversion Cycle and Equity

VerifiedAdded on 2022/09/28

|16

|2679

|19

Report

AI Summary

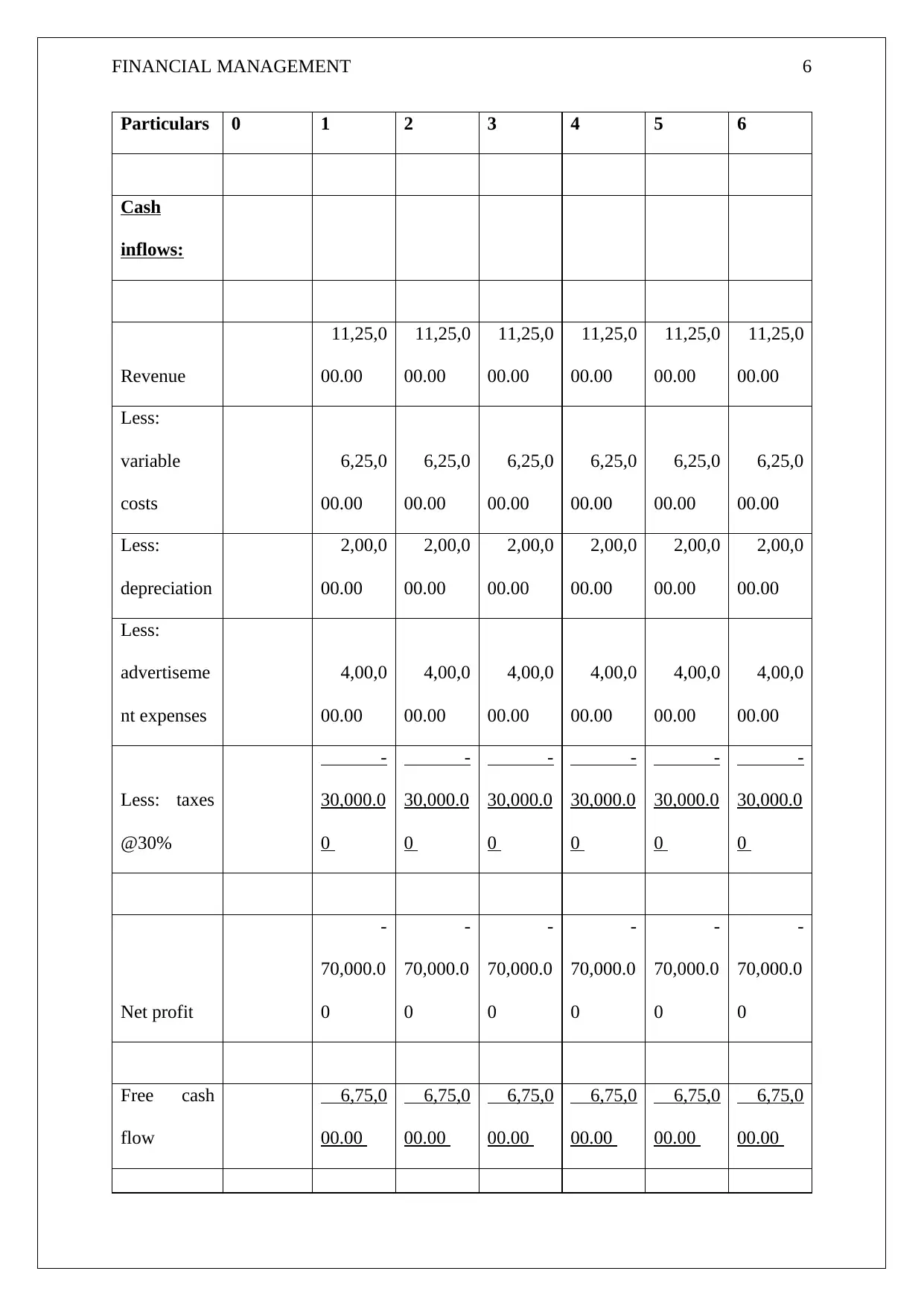

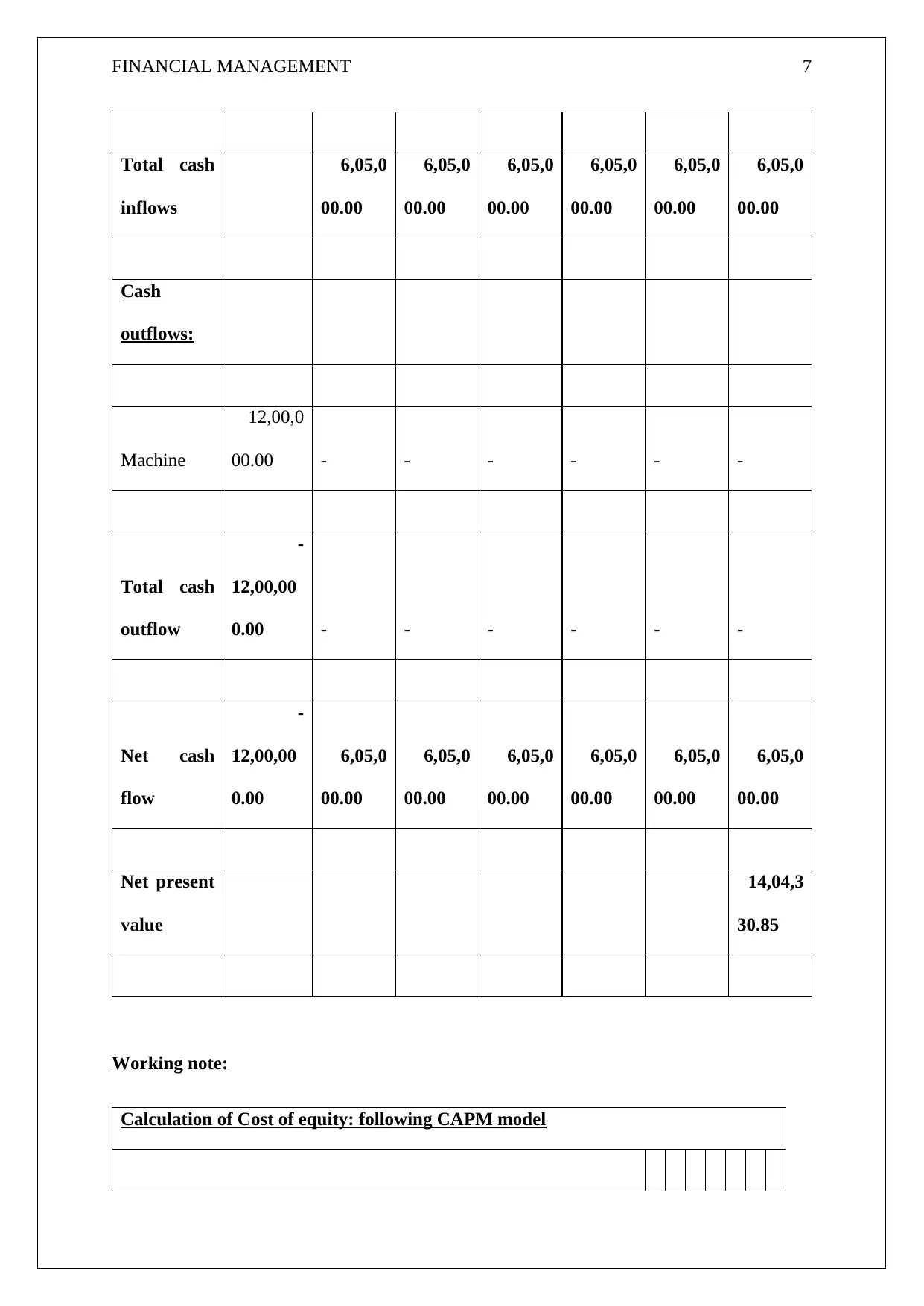

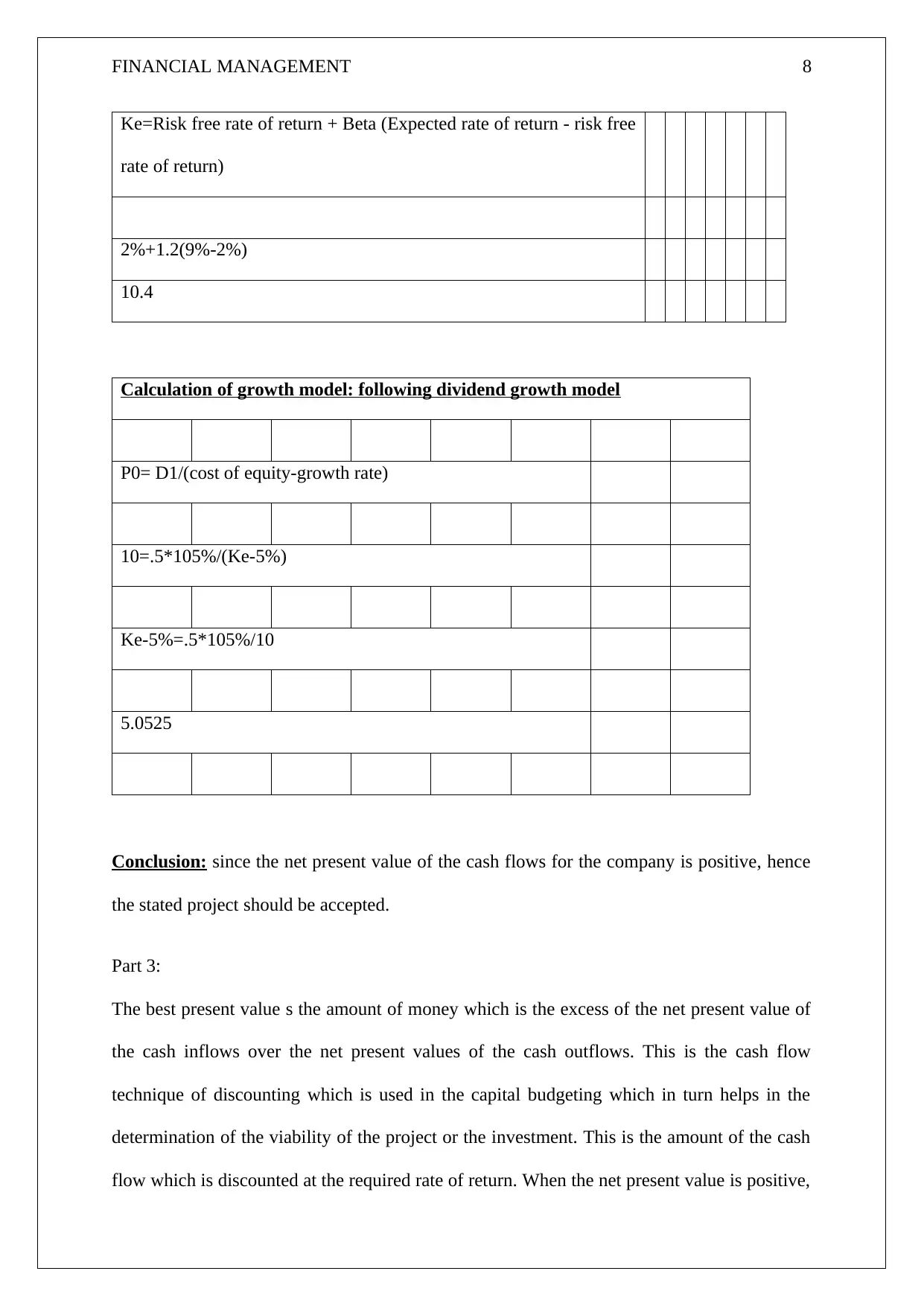

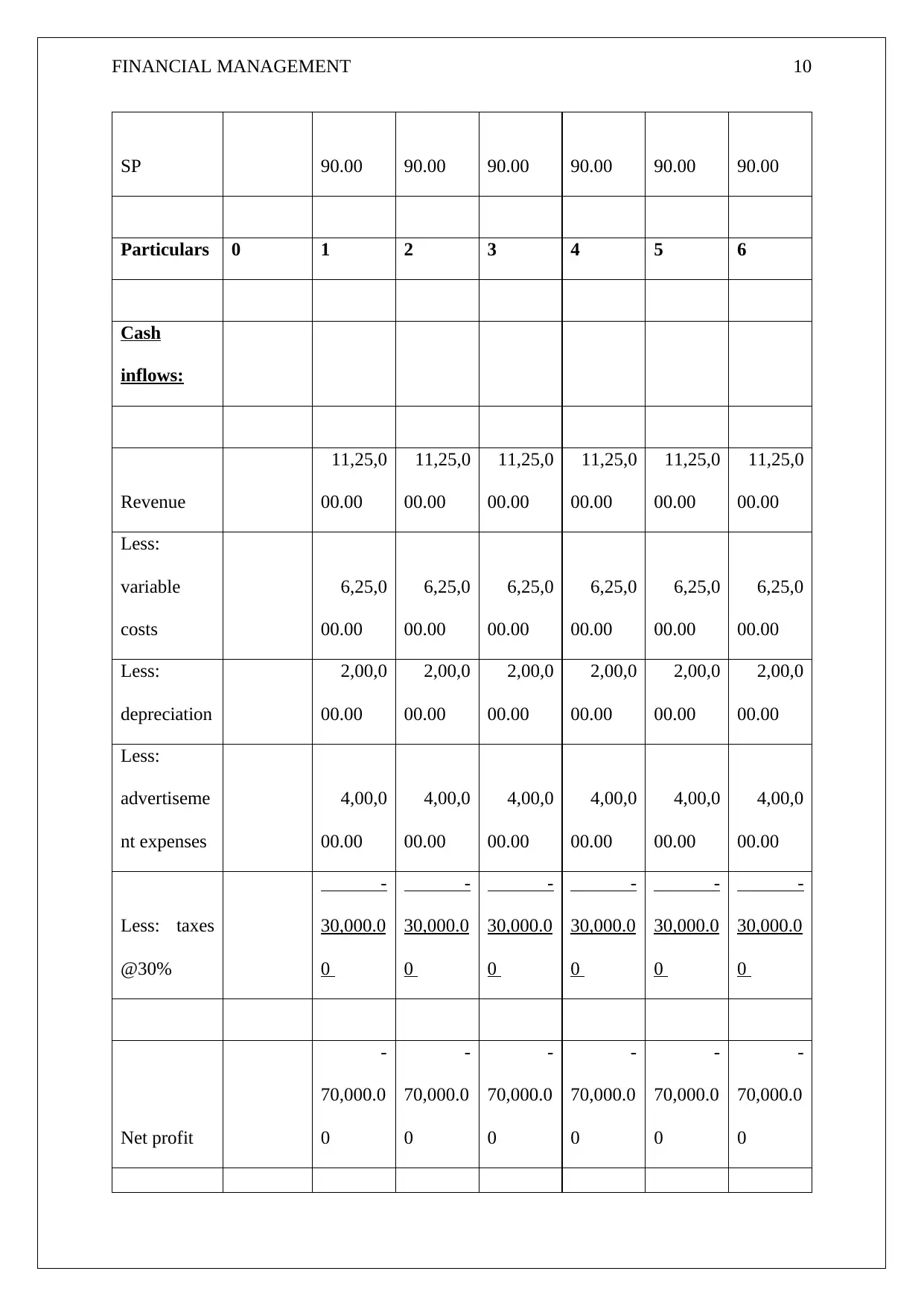

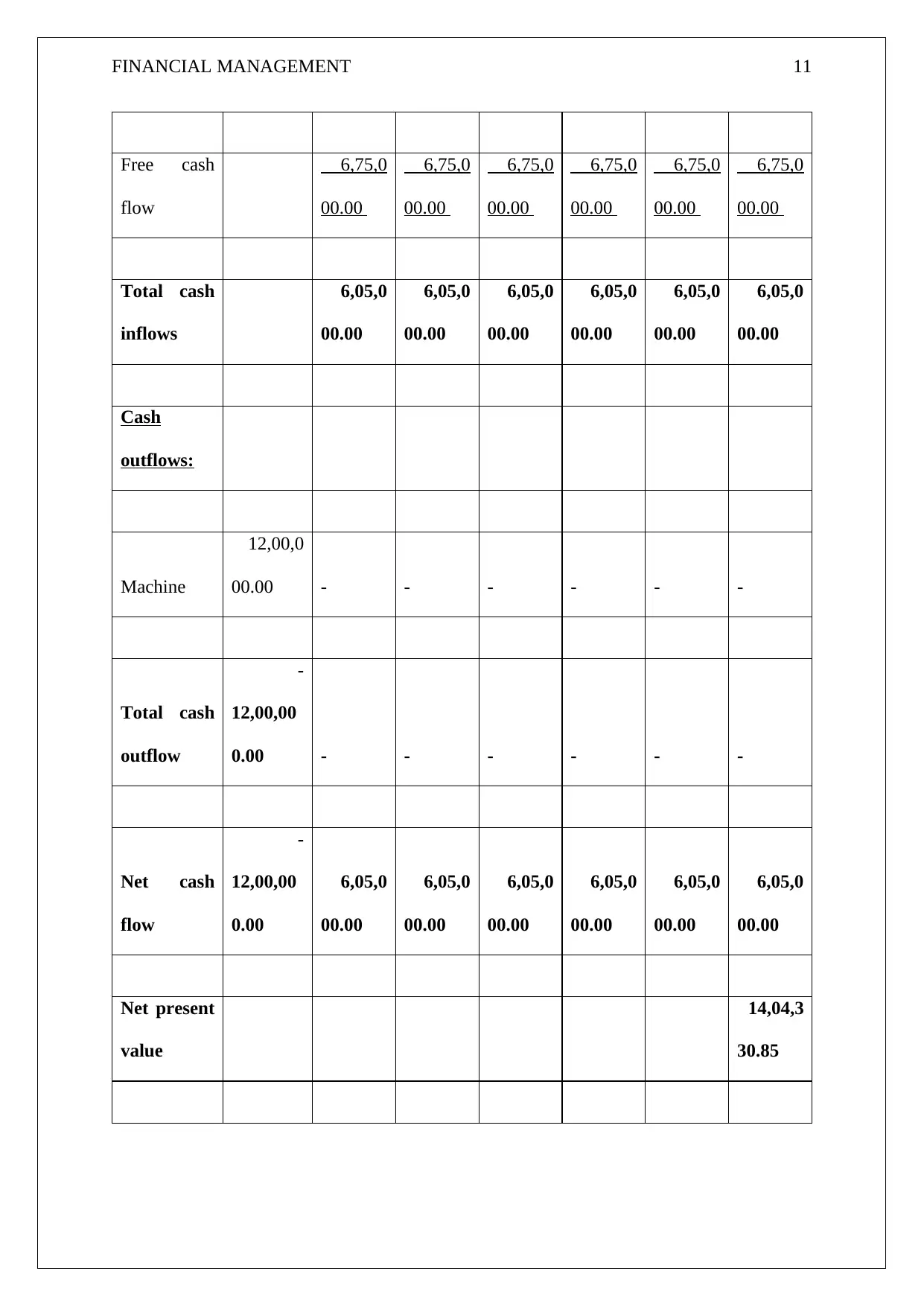

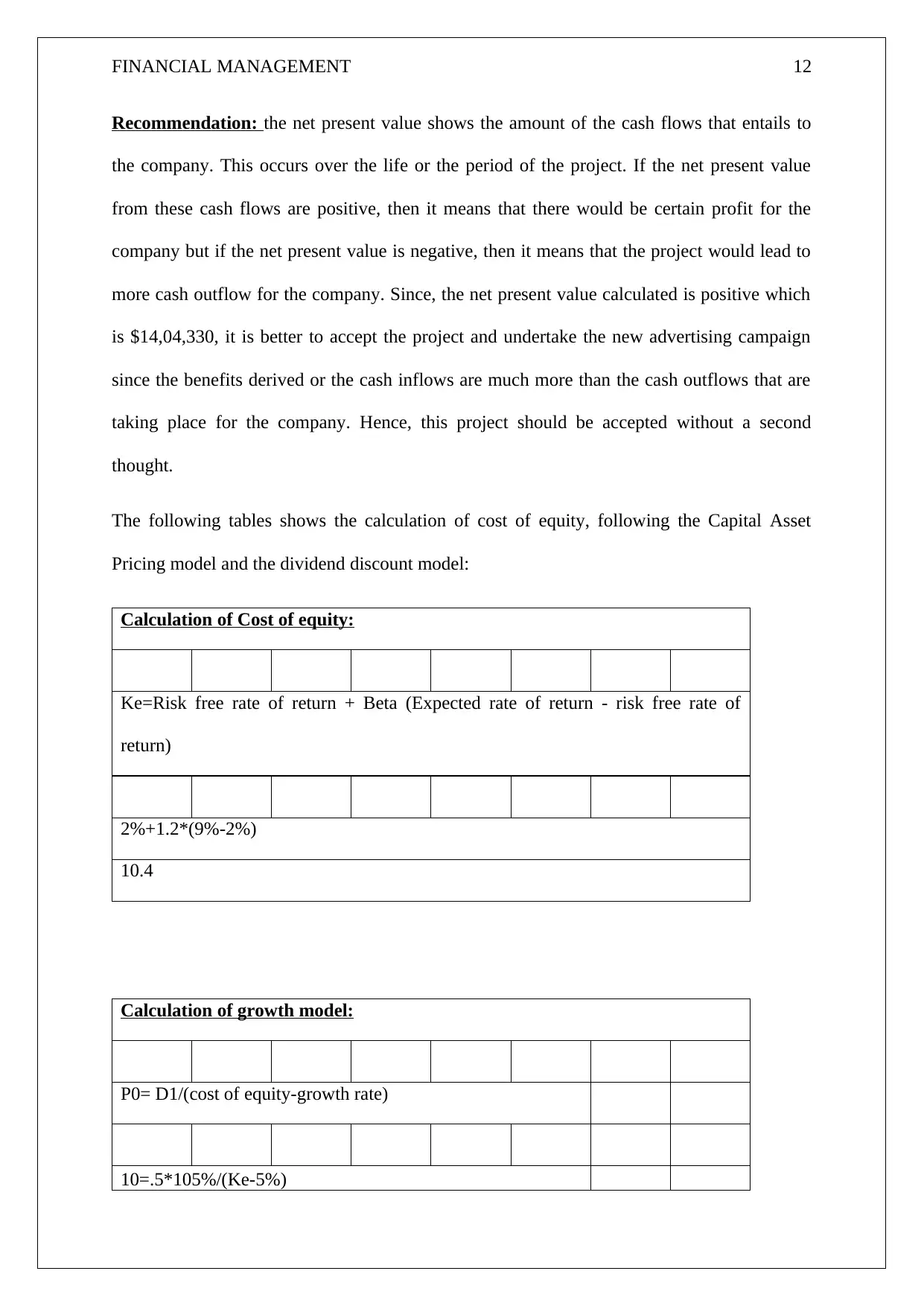

This financial management report delves into key concepts such as the cash conversion cycle, emphasizing its importance for small businesses in managing liquidity and short-term obligations. It explains the components of the cycle, including inventory days, accounts receivable days, and accounts payable days, and how they are calculated. The report then presents a cash flow analysis with detailed calculations of revenue, costs, and net profit over a six-year period, culminating in the determination of net present value (NPV). The NPV calculation incorporates the cost of equity using both the Capital Asset Pricing Model (CAPM) and the dividend growth model, leading to a recommendation to accept the project due to its positive NPV. The report also discusses the advantages of using NPV in capital budgeting, highlighting its consideration of the time value of money and its role in maximizing company value. The report concludes with a comparative analysis of financing options, evaluating the implications of issuing equity shares versus selling Australian bonds, to determine the optimal financing strategy.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.