Financial Management Report: Long Term Finance and Appraisal

VerifiedAdded on 2023/01/13

|14

|3819

|99

Report

AI Summary

This report delves into financial management, focusing on long-term finance and equity finance. It analyzes a rights issue, determining the number of shares to be issued, theoretical ex-rights prices, and expected earnings per share under different scenarios. The report also calculates and evaluates investment appraisal techniques such as the payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR). Furthermore, it explores the concept of scrip dividends, outlining their advantages and disadvantages for both shareholders and the company. The analysis includes detailed calculations and recommendations based on the financial data provided, offering insights into investment decisions and financial planning strategies.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

Question 2. Long term finance: Equity finance:....................................................................1

Number of shares to be issued...........................................................................................2

Theoretical ex-rights price.................................................................................................2

Expected earnings per share..............................................................................................3

Question 3. Calculation as accordance of investment appraisal techniques:.........................5

1.The Payback Period........................................................................................................5

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK...............................................................................................................................................1

Question 2. Long term finance: Equity finance:....................................................................1

Number of shares to be issued...........................................................................................2

Theoretical ex-rights price.................................................................................................2

Expected earnings per share..............................................................................................3

Question 3. Calculation as accordance of investment appraisal techniques:.........................5

1.The Payback Period........................................................................................................5

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial management is defined as a procedure which consists of crucial operations like

planning, organizing, controlling and monitoring financial resources with a view to acquire all

the organizational goals and objectives. To control financial activities require to focus on

different aspects such as procurement of funds, utilization of funds, payments, risk analysis and

many other related things. The application of financial management is conducting with and

examining money and investments for an individual or an organisation to support and make

business decisions in appropriate manner. It is categorised into three manner such as capital

structure, working capital management and capital budgeting (Akgün and et.al., 2014). Through

management analysis the requirement of financial activities in any business entity and leads to

take financial planning as per the concern. It is essential part which promote an organisation in

order to acquisition of funds. In this report consist of long term finance, equity finance where

analysis of different task of that linked with numerical task. This study involves impact of

evaluation of different advantages and key limitations of multiple differing investments

appraisals techniques.

TASK

Question 2. Long term finance: Equity finance:

(a) Earnings after tax (PATA) – 20% on shareholders funds

Capital structure:

£

Ordinary shares of 50 p each 300,000

Reserves 400,000

700,000

Raise £180,000 from a right issue

The current ex-dividend market price - £1.90

When the shares were issued the price per share was £0.50

Three rights issue price suggested: £1.80, £1.60 and £1.40

The shares of Lexbel plc have a nominal value of 50 p per share and a book value of £300,000.

Therefore there are 600,000 shares. Calculations: 300,000/0.50 = 600,000.

Current market value = 600,000 × £1.90 = £1,140,000

1

Financial management is defined as a procedure which consists of crucial operations like

planning, organizing, controlling and monitoring financial resources with a view to acquire all

the organizational goals and objectives. To control financial activities require to focus on

different aspects such as procurement of funds, utilization of funds, payments, risk analysis and

many other related things. The application of financial management is conducting with and

examining money and investments for an individual or an organisation to support and make

business decisions in appropriate manner. It is categorised into three manner such as capital

structure, working capital management and capital budgeting (Akgün and et.al., 2014). Through

management analysis the requirement of financial activities in any business entity and leads to

take financial planning as per the concern. It is essential part which promote an organisation in

order to acquisition of funds. In this report consist of long term finance, equity finance where

analysis of different task of that linked with numerical task. This study involves impact of

evaluation of different advantages and key limitations of multiple differing investments

appraisals techniques.

TASK

Question 2. Long term finance: Equity finance:

(a) Earnings after tax (PATA) – 20% on shareholders funds

Capital structure:

£

Ordinary shares of 50 p each 300,000

Reserves 400,000

700,000

Raise £180,000 from a right issue

The current ex-dividend market price - £1.90

When the shares were issued the price per share was £0.50

Three rights issue price suggested: £1.80, £1.60 and £1.40

The shares of Lexbel plc have a nominal value of 50 p per share and a book value of £300,000.

Therefore there are 600,000 shares. Calculations: 300,000/0.50 = 600,000.

Current market value = 600,000 × £1.90 = £1,140,000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

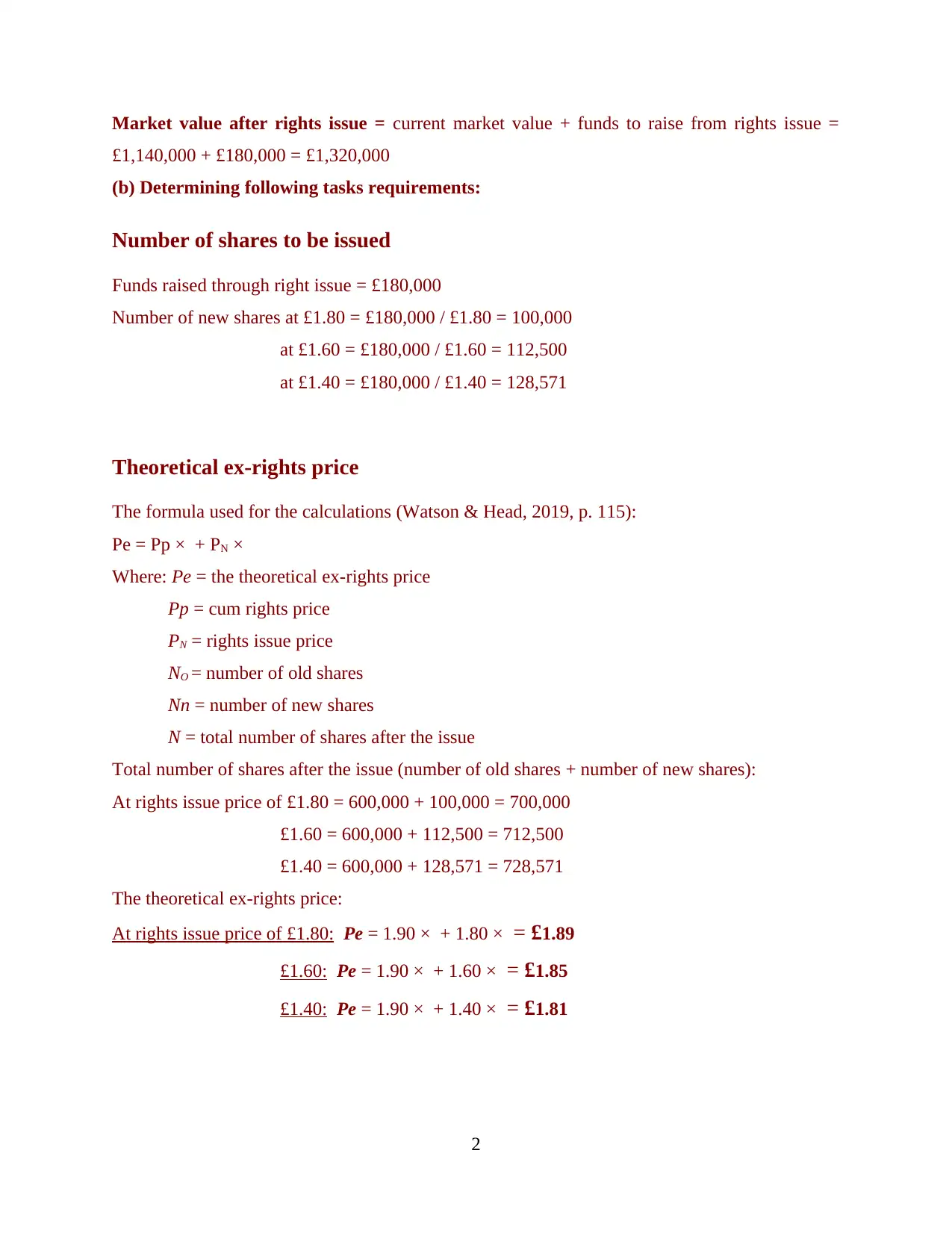

Market value after rights issue = current market value + funds to raise from rights issue =

£1,140,000 + £180,000 = £1,320,000

(b) Determining following tasks requirements:

Number of shares to be issued

Funds raised through right issue = £180,000

Number of new shares at £1.80 = £180,000 / £1.80 = 100,000

at £1.60 = £180,000 / £1.60 = 112,500

at £1.40 = £180,000 / £1.40 = 128,571

Theoretical ex-rights price

The formula used for the calculations (Watson & Head, 2019, p. 115):

Pe = Pp × + PN ×

Where: Pe = the theoretical ex-rights price

Pp = cum rights price

PN = rights issue price

NO = number of old shares

Nn = number of new shares

N = total number of shares after the issue

Total number of shares after the issue (number of old shares + number of new shares):

At rights issue price of £1.80 = 600,000 + 100,000 = 700,000

£1.60 = 600,000 + 112,500 = 712,500

£1.40 = 600,000 + 128,571 = 728,571

The theoretical ex-rights price:

At rights issue price of £1.80: Pe = 1.90 × + 1.80 × = £1.89

£1.60: Pe = 1.90 × + 1.60 × = £1.85

£1.40: Pe = 1.90 × + 1.40 × = £1.81

2

£1,140,000 + £180,000 = £1,320,000

(b) Determining following tasks requirements:

Number of shares to be issued

Funds raised through right issue = £180,000

Number of new shares at £1.80 = £180,000 / £1.80 = 100,000

at £1.60 = £180,000 / £1.60 = 112,500

at £1.40 = £180,000 / £1.40 = 128,571

Theoretical ex-rights price

The formula used for the calculations (Watson & Head, 2019, p. 115):

Pe = Pp × + PN ×

Where: Pe = the theoretical ex-rights price

Pp = cum rights price

PN = rights issue price

NO = number of old shares

Nn = number of new shares

N = total number of shares after the issue

Total number of shares after the issue (number of old shares + number of new shares):

At rights issue price of £1.80 = 600,000 + 100,000 = 700,000

£1.60 = 600,000 + 112,500 = 712,500

£1.40 = 600,000 + 128,571 = 728,571

The theoretical ex-rights price:

At rights issue price of £1.80: Pe = 1.90 × + 1.80 × = £1.89

£1.60: Pe = 1.90 × + 1.60 × = £1.85

£1.40: Pe = 1.90 × + 1.40 × = £1.81

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Expected earnings per share

Formula: Total earnings after rights issue / Total number of shares after the issue × 100%

Earnings before rights issue = £700,000 × 20% = £140,000

Earnings from new funds = £180,000 × 20% = £36,000

Total earnings after rights issue = £140,000 + £36,000 = £176,000

Expected earnings per share:

At rights issue price of £1.80: £176,000 / 700,000 = 0.251 × 100% = 25.1 p

£1.60: £176,000 / 712,500 = 0.247 × 100% = 24.7 p

£1.40: £176,000 / 728,571 = 0.242 × 100% = 24.2 p

i. Form of the issue for each rights issue price

Formula: 1 = 1 / number of new shares × number of old shares

At rights issue price of £1.80: 1 = 1/ 100,000 × 600,000 = 6

£1.60: 1 = 1/ 112,500 × 600,000 = 5.3

£1.40: 1 = 1/ 128,571 × 600,000 = 4.7

Therefore: At rights issue price of £1.80 per 6 shares will be offered 1 new share.

At rights issue price of £1.60 per 5.3 shares will be offered 1 new share.

At rights issue price of £1.60 per 4.7 shares will be offered 1 new share.

Below listed are various forms related to respective issues regarding each of the right-

issue price scenario, as follow:

In case of suggested right issue GBP 1.8 per share, issue proportion(on pro-rata basis)

should be 1 share against 6 existing shares to issue additional required 100000 shares.

In second case of suggested issues of GBP 1.6 per share, issue proportion(on pro-rata

basis) should be 9 shares against 48 existing shares in order to issue additionally 112500

required.

While in thirst case of suggested issues of GBP 1.4 per share, issue proportion(on pro-

rata basis) should be 3 shares against 14 existing shares in order to issue additionally

required 128571 shares.

Scrip Dividend:

Scrip dividends or scripting issues are issue of shares usually performed as a manner to

reward shareholders rather than traditional dividends. When a corporation's directors chose to

3

Formula: Total earnings after rights issue / Total number of shares after the issue × 100%

Earnings before rights issue = £700,000 × 20% = £140,000

Earnings from new funds = £180,000 × 20% = £36,000

Total earnings after rights issue = £140,000 + £36,000 = £176,000

Expected earnings per share:

At rights issue price of £1.80: £176,000 / 700,000 = 0.251 × 100% = 25.1 p

£1.60: £176,000 / 712,500 = 0.247 × 100% = 24.7 p

£1.40: £176,000 / 728,571 = 0.242 × 100% = 24.2 p

i. Form of the issue for each rights issue price

Formula: 1 = 1 / number of new shares × number of old shares

At rights issue price of £1.80: 1 = 1/ 100,000 × 600,000 = 6

£1.60: 1 = 1/ 112,500 × 600,000 = 5.3

£1.40: 1 = 1/ 128,571 × 600,000 = 4.7

Therefore: At rights issue price of £1.80 per 6 shares will be offered 1 new share.

At rights issue price of £1.60 per 5.3 shares will be offered 1 new share.

At rights issue price of £1.60 per 4.7 shares will be offered 1 new share.

Below listed are various forms related to respective issues regarding each of the right-

issue price scenario, as follow:

In case of suggested right issue GBP 1.8 per share, issue proportion(on pro-rata basis)

should be 1 share against 6 existing shares to issue additional required 100000 shares.

In second case of suggested issues of GBP 1.6 per share, issue proportion(on pro-rata

basis) should be 9 shares against 48 existing shares in order to issue additionally 112500

required.

While in thirst case of suggested issues of GBP 1.4 per share, issue proportion(on pro-

rata basis) should be 3 shares against 14 existing shares in order to issue additionally

required 128571 shares.

Scrip Dividend:

Scrip dividends or scripting issues are issue of shares usually performed as a manner to

reward shareholders rather than traditional dividends. When a corporation's directors chose to

3

preserve funds inside the corporation but recognize that they need at least usually a certain sum

of dividend, company could provide equity shareholders choice of cash or scrip dividend. Scrip

dividend is dividend sum paid into certificates eligible to be given in future by holder on capital

stocks. This is certificate approved by a company to its shareholder that demonstrates that

holder's right to same extent of value in property and franchise as scrip dividend, with the

exception that the company has right to reimburse a scrip dividend on coming years earnings and

that no voting rights are accorded to scrip dividend. Scrip dividend shall contain scrip or

certificates subjecting stockholders who obtain them to rights and privileges stated therein, often

to the declaration of earnings at future date, often to right of the company's supplementary stock,

securities or other liabilities. This form of dividend typically indicates that cash flows of the

corporation is small. It is due as a scrip or attestation if company does not have enough money,

but has sufficient withholding income (Alsemgeest, 2015). A scrip issue involves transferring the

cash reserve of company to stocks and distribution to its current shareholders. For instance,

Barclays Bank is corporation paying scrip dividends. scrip issue may be a manner to make new

shares which are free of cost to shareholders. Every investor is permitted at all times to sell its

scrip on market. Moreover, when submitting the tax-return, they must record the amount of scrip

dividend as value of cash dividend. Here are some crucial benefits discussed separately in

context of shareholders and corporation, as follows:

Advantages of Scrip dividend:

For shareholders:

When there is a option of shares accessible towards dividend, shareholders may obtain

tax benefits. The advantage for every shareholder of scrip dividend is they can easily/smoothly

enhance their participation within the organization without paying broking fees or stamping

duties is to be pay on share purchase (Arianti, 2018). All the holders which are entitled to get

scrip dividend can do this in order to boost ownership without bearing any purchase costs of

buying more shares/securities.

For company:

The share prices will not diminish substantially by small issue of any scrip dividends.

However, empirical evidence demonstrates that the inventory / security price has fallen in event

cash is not presented as a choice. A share's issue made under scrip dividend leads to less cost of

issue and also controls the gearing position of organisation, which eventually assist in enhancing

4

of dividend, company could provide equity shareholders choice of cash or scrip dividend. Scrip

dividend is dividend sum paid into certificates eligible to be given in future by holder on capital

stocks. This is certificate approved by a company to its shareholder that demonstrates that

holder's right to same extent of value in property and franchise as scrip dividend, with the

exception that the company has right to reimburse a scrip dividend on coming years earnings and

that no voting rights are accorded to scrip dividend. Scrip dividend shall contain scrip or

certificates subjecting stockholders who obtain them to rights and privileges stated therein, often

to the declaration of earnings at future date, often to right of the company's supplementary stock,

securities or other liabilities. This form of dividend typically indicates that cash flows of the

corporation is small. It is due as a scrip or attestation if company does not have enough money,

but has sufficient withholding income (Alsemgeest, 2015). A scrip issue involves transferring the

cash reserve of company to stocks and distribution to its current shareholders. For instance,

Barclays Bank is corporation paying scrip dividends. scrip issue may be a manner to make new

shares which are free of cost to shareholders. Every investor is permitted at all times to sell its

scrip on market. Moreover, when submitting the tax-return, they must record the amount of scrip

dividend as value of cash dividend. Here are some crucial benefits discussed separately in

context of shareholders and corporation, as follows:

Advantages of Scrip dividend:

For shareholders:

When there is a option of shares accessible towards dividend, shareholders may obtain

tax benefits. The advantage for every shareholder of scrip dividend is they can easily/smoothly

enhance their participation within the organization without paying broking fees or stamping

duties is to be pay on share purchase (Arianti, 2018). All the holders which are entitled to get

scrip dividend can do this in order to boost ownership without bearing any purchase costs of

buying more shares/securities.

For company:

The share prices will not diminish substantially by small issue of any scrip dividends.

However, empirical evidence demonstrates that the inventory / security price has fallen in event

cash is not presented as a choice. A share's issue made under scrip dividend leads to less cost of

issue and also controls the gearing position of organisation, which eventually assist in enhancing

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

overall lending/borrowing capacity. This can support in sustaining an organization's aggregate

cash balance as when large no. of shareholders support the equity alternatives (Brigham and

Houston, 2012).

Disadvantages:

For Shareholders:

The fair value of such share is based on state of economy, which could cause losses if the

circumstances are not favourable for shareholders. Due to above discussed risk of diminishing

value of shares, instead of selecting the option of shares, most of the shareholders consider or opt

for cash under scrip dividend. Which lead to difficult for other investors who wants to get short

term benefit of share value increase on selecting scrip dividend (Goel, Chadha and Sharma,

2015).

For Company:

The aggregate sum amount paid by corporation as dividend payout may show increment

in case dividend per share is more than aggregate earning which can lead to distract potential

investors. As options are given under scrip dividend as compare to normal dividend which shows

that company is struggling with major cash-flows issues and impacts company's reputation in

eyes of investors (Karadag, 2015).

Question 3. Calculation as accordance of investment appraisal techniques:

(i) Payback period: Initial investment/ cash flow:

Investment = £275,000

Annual cash inflow = £85,000

Cash outflow = £12,500

Net cash flow = Cash inflow – cash outflow = £85,000 - £12,500 = £72,500

Residual value = 15% of the £275,000 = £41,250 added to year 6

Total depreciation = £275,000 - £41,250 = £233,750

Annual depreciation = £233,750/6 = £38,958.33

1. The Payback Period

Payback = (57,500/72,500) + 3 years = 3.79 years

5

cash balance as when large no. of shareholders support the equity alternatives (Brigham and

Houston, 2012).

Disadvantages:

For Shareholders:

The fair value of such share is based on state of economy, which could cause losses if the

circumstances are not favourable for shareholders. Due to above discussed risk of diminishing

value of shares, instead of selecting the option of shares, most of the shareholders consider or opt

for cash under scrip dividend. Which lead to difficult for other investors who wants to get short

term benefit of share value increase on selecting scrip dividend (Goel, Chadha and Sharma,

2015).

For Company:

The aggregate sum amount paid by corporation as dividend payout may show increment

in case dividend per share is more than aggregate earning which can lead to distract potential

investors. As options are given under scrip dividend as compare to normal dividend which shows

that company is struggling with major cash-flows issues and impacts company's reputation in

eyes of investors (Karadag, 2015).

Question 3. Calculation as accordance of investment appraisal techniques:

(i) Payback period: Initial investment/ cash flow:

Investment = £275,000

Annual cash inflow = £85,000

Cash outflow = £12,500

Net cash flow = Cash inflow – cash outflow = £85,000 - £12,500 = £72,500

Residual value = 15% of the £275,000 = £41,250 added to year 6

Total depreciation = £275,000 - £41,250 = £233,750

Annual depreciation = £233,750/6 = £38,958.33

1. The Payback Period

Payback = (57,500/72,500) + 3 years = 3.79 years

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

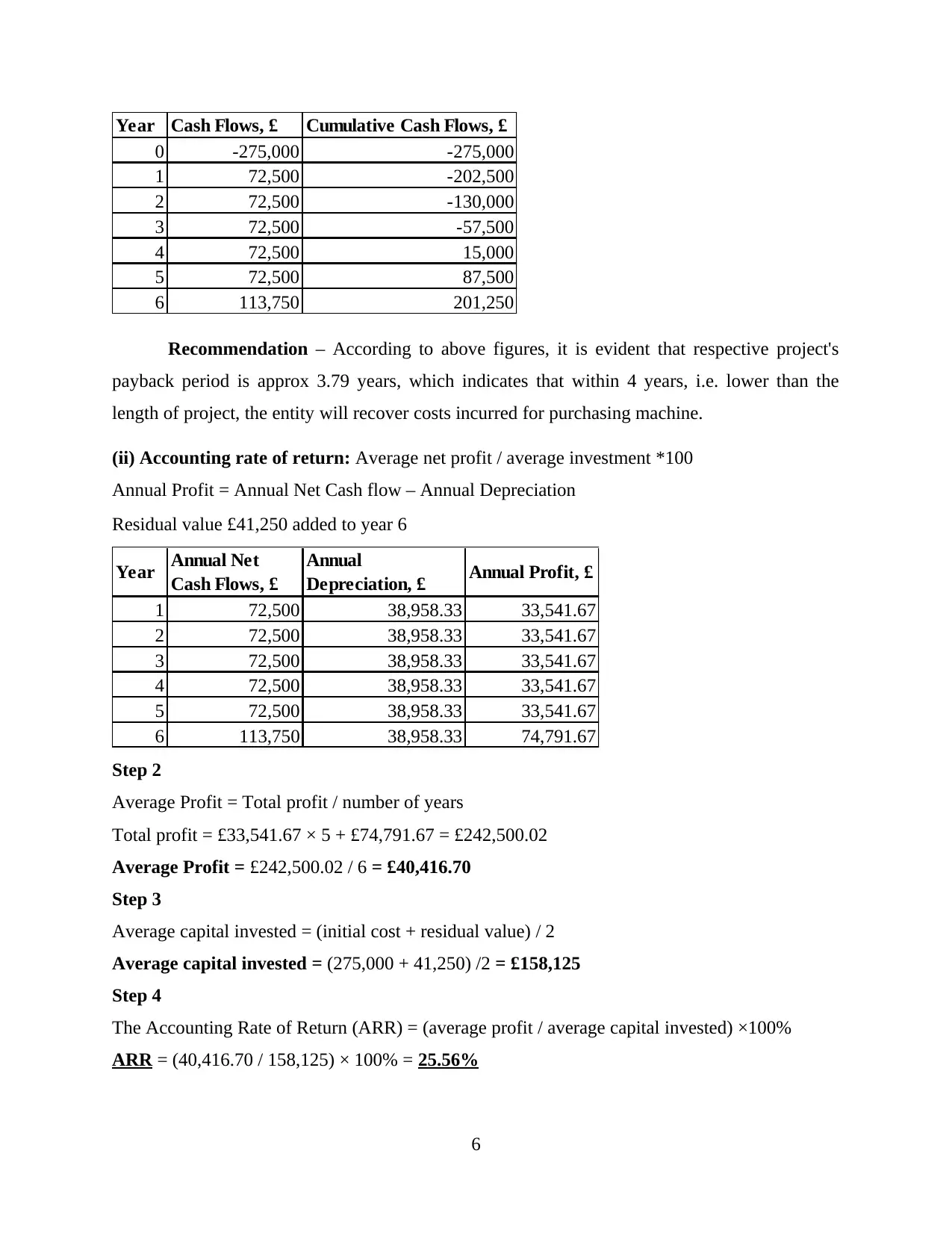

Year Cash Flows, £ Cumulative Cash Flows, £

0 -275,000 -275,000

1 72,500 -202,500

2 72,500 -130,000

3 72,500 -57,500

4 72,500 15,000

5 72,500 87,500

6 113,750 201,250

Recommendation – According to above figures, it is evident that respective project's

payback period is approx 3.79 years, which indicates that within 4 years, i.e. lower than the

length of project, the entity will recover costs incurred for purchasing machine.

(ii) Accounting rate of return: Average net profit / average investment *100

Annual Profit = Annual Net Cash flow – Annual Depreciation

Residual value £41,250 added to year 6

Year Annual Net

Cash Flows, £

Annual

Depreciation, £ Annual Profit, £

1 72,500 38,958.33 33,541.67

2 72,500 38,958.33 33,541.67

3 72,500 38,958.33 33,541.67

4 72,500 38,958.33 33,541.67

5 72,500 38,958.33 33,541.67

6 113,750 38,958.33 74,791.67

Step 2

Average Profit = Total profit / number of years

Total profit = £33,541.67 × 5 + £74,791.67 = £242,500.02

Average Profit = £242,500.02 / 6 = £40,416.70

Step 3

Average capital invested = (initial cost + residual value) / 2

Average capital invested = (275,000 + 41,250) /2 = £158,125

Step 4

The Accounting Rate of Return (ARR) = (average profit / average capital invested) ×100%

ARR = (40,416.70 / 158,125) × 100% = 25.56%

6

0 -275,000 -275,000

1 72,500 -202,500

2 72,500 -130,000

3 72,500 -57,500

4 72,500 15,000

5 72,500 87,500

6 113,750 201,250

Recommendation – According to above figures, it is evident that respective project's

payback period is approx 3.79 years, which indicates that within 4 years, i.e. lower than the

length of project, the entity will recover costs incurred for purchasing machine.

(ii) Accounting rate of return: Average net profit / average investment *100

Annual Profit = Annual Net Cash flow – Annual Depreciation

Residual value £41,250 added to year 6

Year Annual Net

Cash Flows, £

Annual

Depreciation, £ Annual Profit, £

1 72,500 38,958.33 33,541.67

2 72,500 38,958.33 33,541.67

3 72,500 38,958.33 33,541.67

4 72,500 38,958.33 33,541.67

5 72,500 38,958.33 33,541.67

6 113,750 38,958.33 74,791.67

Step 2

Average Profit = Total profit / number of years

Total profit = £33,541.67 × 5 + £74,791.67 = £242,500.02

Average Profit = £242,500.02 / 6 = £40,416.70

Step 3

Average capital invested = (initial cost + residual value) / 2

Average capital invested = (275,000 + 41,250) /2 = £158,125

Step 4

The Accounting Rate of Return (ARR) = (average profit / average capital invested) ×100%

ARR = (40,416.70 / 158,125) × 100% = 25.56%

6

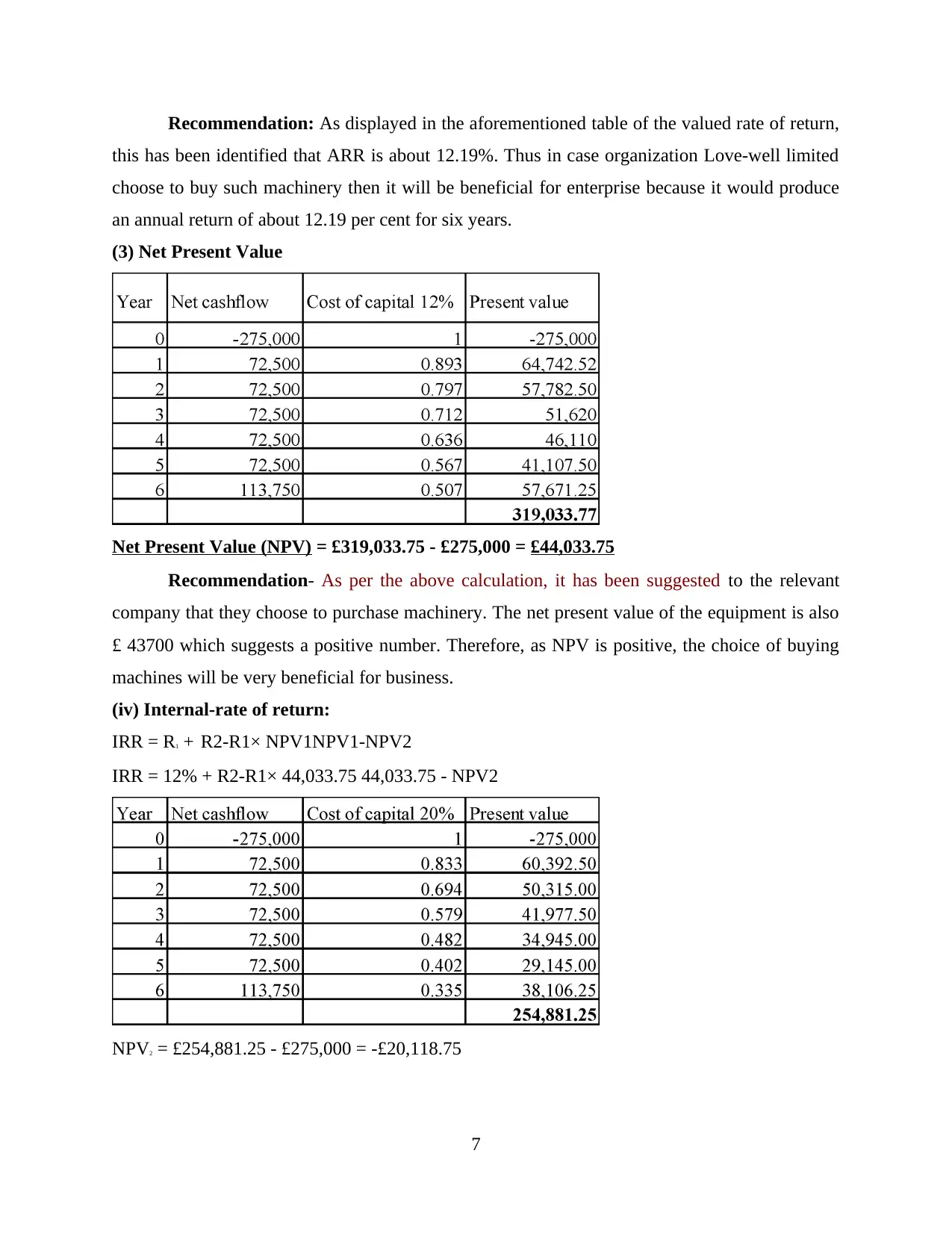

Recommendation: As displayed in the aforementioned table of the valued rate of return,

this has been identified that ARR is about 12.19%. Thus in case organization Love-well limited

choose to buy such machinery then it will be beneficial for enterprise because it would produce

an annual return of about 12.19 per cent for six years.

(3) Net Present Value

Net Present Value (NPV) = £319,033.75 - £275,000 = £44,033.75

Recommendation- As per the above calculation, it has been suggested to the relevant

company that they choose to purchase machinery. The net present value of the equipment is also

£ 43700 which suggests a positive number. Therefore, as NPV is positive, the choice of buying

machines will be very beneficial for business.

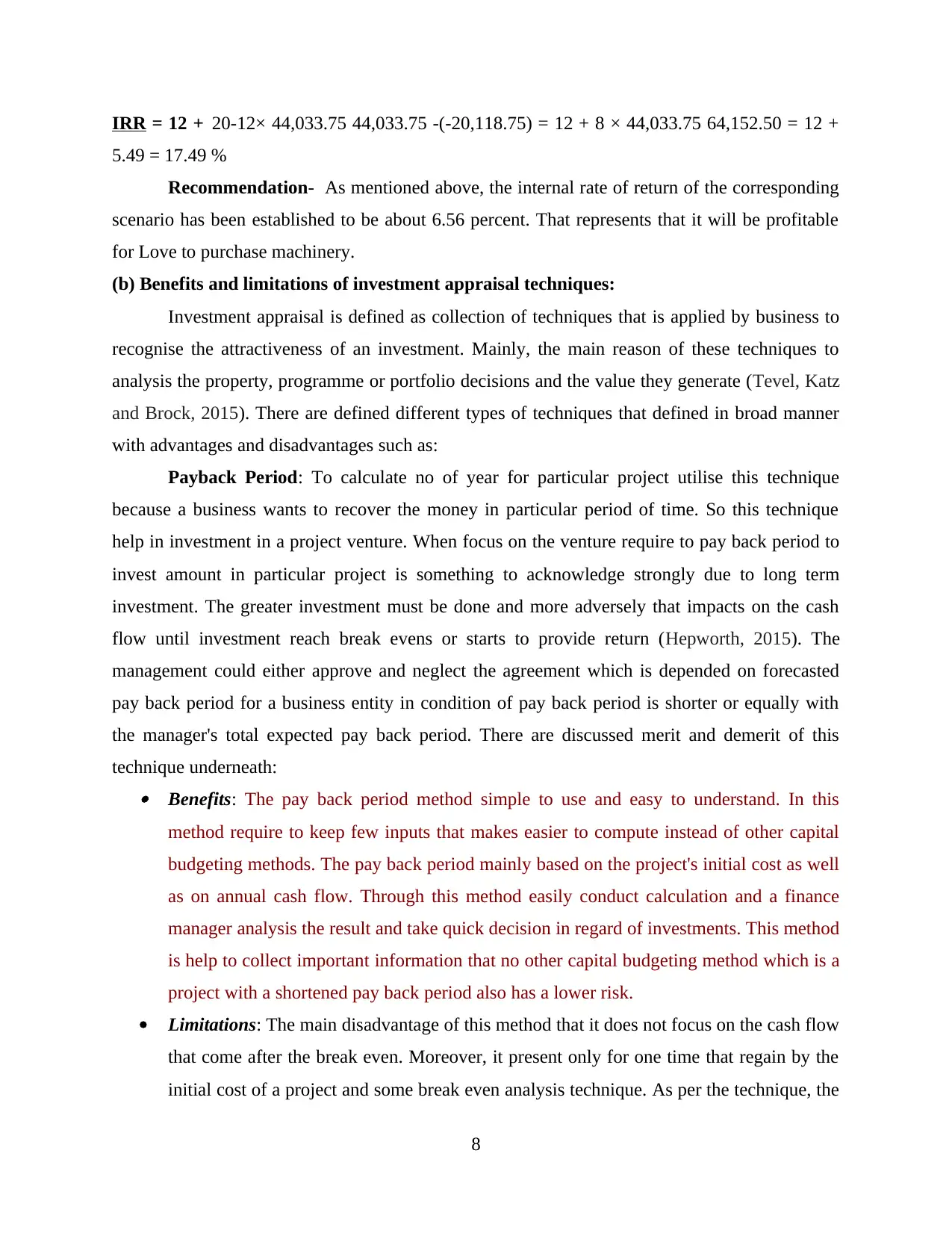

(iv) Internal-rate of return:

IRR = R1 + R2-R1× NPV1NPV1-NPV2

IRR = 12% + R2-R1× 44,033.75 44,033.75 - NPV2

NPV2 = £254,881.25 - £275,000 = -£20,118.75

7

this has been identified that ARR is about 12.19%. Thus in case organization Love-well limited

choose to buy such machinery then it will be beneficial for enterprise because it would produce

an annual return of about 12.19 per cent for six years.

(3) Net Present Value

Net Present Value (NPV) = £319,033.75 - £275,000 = £44,033.75

Recommendation- As per the above calculation, it has been suggested to the relevant

company that they choose to purchase machinery. The net present value of the equipment is also

£ 43700 which suggests a positive number. Therefore, as NPV is positive, the choice of buying

machines will be very beneficial for business.

(iv) Internal-rate of return:

IRR = R1 + R2-R1× NPV1NPV1-NPV2

IRR = 12% + R2-R1× 44,033.75 44,033.75 - NPV2

NPV2 = £254,881.25 - £275,000 = -£20,118.75

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

IRR = 12 + 20-12× 44,033.75 44,033.75 -(-20,118.75) = 12 + 8 × 44,033.75 64,152.50 = 12 +

5.49 = 17.49 %

Recommendation- As mentioned above, the internal rate of return of the corresponding

scenario has been established to be about 6.56 percent. That represents that it will be profitable

for Love to purchase machinery.

(b) Benefits and limitations of investment appraisal techniques:

Investment appraisal is defined as collection of techniques that is applied by business to

recognise the attractiveness of an investment. Mainly, the main reason of these techniques to

analysis the property, programme or portfolio decisions and the value they generate (Tevel, Katz

and Brock, 2015). There are defined different types of techniques that defined in broad manner

with advantages and disadvantages such as:

Payback Period: To calculate no of year for particular project utilise this technique

because a business wants to recover the money in particular period of time. So this technique

help in investment in a project venture. When focus on the venture require to pay back period to

invest amount in particular project is something to acknowledge strongly due to long term

investment. The greater investment must be done and more adversely that impacts on the cash

flow until investment reach break evens or starts to provide return (Hepworth, 2015). The

management could either approve and neglect the agreement which is depended on forecasted

pay back period for a business entity in condition of pay back period is shorter or equally with

the manager's total expected pay back period. There are discussed merit and demerit of this

technique underneath: Benefits: The pay back period method simple to use and easy to understand. In this

method require to keep few inputs that makes easier to compute instead of other capital

budgeting methods. The pay back period mainly based on the project's initial cost as well

as on annual cash flow. Through this method easily conduct calculation and a finance

manager analysis the result and take quick decision in regard of investments. This method

is help to collect important information that no other capital budgeting method which is a

project with a shortened pay back period also has a lower risk.

Limitations: The main disadvantage of this method that it does not focus on the cash flow

that come after the break even. Moreover, it present only for one time that regain by the

initial cost of a project and some break even analysis technique. As per the technique, the

8

5.49 = 17.49 %

Recommendation- As mentioned above, the internal rate of return of the corresponding

scenario has been established to be about 6.56 percent. That represents that it will be profitable

for Love to purchase machinery.

(b) Benefits and limitations of investment appraisal techniques:

Investment appraisal is defined as collection of techniques that is applied by business to

recognise the attractiveness of an investment. Mainly, the main reason of these techniques to

analysis the property, programme or portfolio decisions and the value they generate (Tevel, Katz

and Brock, 2015). There are defined different types of techniques that defined in broad manner

with advantages and disadvantages such as:

Payback Period: To calculate no of year for particular project utilise this technique

because a business wants to recover the money in particular period of time. So this technique

help in investment in a project venture. When focus on the venture require to pay back period to

invest amount in particular project is something to acknowledge strongly due to long term

investment. The greater investment must be done and more adversely that impacts on the cash

flow until investment reach break evens or starts to provide return (Hepworth, 2015). The

management could either approve and neglect the agreement which is depended on forecasted

pay back period for a business entity in condition of pay back period is shorter or equally with

the manager's total expected pay back period. There are discussed merit and demerit of this

technique underneath: Benefits: The pay back period method simple to use and easy to understand. In this

method require to keep few inputs that makes easier to compute instead of other capital

budgeting methods. The pay back period mainly based on the project's initial cost as well

as on annual cash flow. Through this method easily conduct calculation and a finance

manager analysis the result and take quick decision in regard of investments. This method

is help to collect important information that no other capital budgeting method which is a

project with a shortened pay back period also has a lower risk.

Limitations: The main disadvantage of this method that it does not focus on the cash flow

that come after the break even. Moreover, it present only for one time that regain by the

initial cost of a project and some break even analysis technique. As per the technique, the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

particular method can create conflict with net present value that will be wrong. It is not

particular way for analysis that how shorter the pay back period should be invest into

project (Morden, 2016).

Accounting rate of return: It is one of the investment appraisal technique that known as

financial ratio and utilised in capital budgeting. This technique is not depended on the cash flows

that is applied in broad manner. It is a traditional method that use for measurement as well as

viability of project. This is a most popular technique which is assessed as a proportion of the

project that awaited average yearly net income to its total investment. The companies used this

method for feasibility measurement of a venture, mainly compare with other venture. Therefore,

the inability of ARR to make up for collected taxes, interest, inflation and cash flows that makes

it mistake fore longer time period planning (Osadchy and Akhmetshin, 2015). Advantages: Through this method get right point after then compute rather than cash

inflows. This method helps to compare particular project with other project and get

results for decision making. It is average investment method which is applied by the

online cheap accountants in east London to compute the return proportion on the amount

of average investment. This method easily applied by manager for analysis capital

projects that can be quickly by all. To calculate wise this method easy to apply and gain

result easily.

Disadvantages: This method more time on calculation due to selection in alternate.

Therefore, this is delusive method in order to compare two or more capital projects for

any business entity. ARR is mainly applied on basis of net profit that generate by capital

project and specially related with cash flow which is quite aspect for a business entity.

Net Present Value: It is defined as investment technique which is presenting a target

return of a given initial cost that has been achieved in certain period of time. NPV defines to

select initial investment expected to accomplish the target return when all else is the same. Net

present value is based on the discounted cash flow and initial investment proposal or venture

(Parker, 2012). Advantages: The main advantage of this method to consist of fact that focus on the time

value of money and supports to administration for effective decision making procedure. It

is not only supports in analysis of projects of same size but it also supports to recognising

a specific investment for generating profit.

9

particular way for analysis that how shorter the pay back period should be invest into

project (Morden, 2016).

Accounting rate of return: It is one of the investment appraisal technique that known as

financial ratio and utilised in capital budgeting. This technique is not depended on the cash flows

that is applied in broad manner. It is a traditional method that use for measurement as well as

viability of project. This is a most popular technique which is assessed as a proportion of the

project that awaited average yearly net income to its total investment. The companies used this

method for feasibility measurement of a venture, mainly compare with other venture. Therefore,

the inability of ARR to make up for collected taxes, interest, inflation and cash flows that makes

it mistake fore longer time period planning (Osadchy and Akhmetshin, 2015). Advantages: Through this method get right point after then compute rather than cash

inflows. This method helps to compare particular project with other project and get

results for decision making. It is average investment method which is applied by the

online cheap accountants in east London to compute the return proportion on the amount

of average investment. This method easily applied by manager for analysis capital

projects that can be quickly by all. To calculate wise this method easy to apply and gain

result easily.

Disadvantages: This method more time on calculation due to selection in alternate.

Therefore, this is delusive method in order to compare two or more capital projects for

any business entity. ARR is mainly applied on basis of net profit that generate by capital

project and specially related with cash flow which is quite aspect for a business entity.

Net Present Value: It is defined as investment technique which is presenting a target

return of a given initial cost that has been achieved in certain period of time. NPV defines to

select initial investment expected to accomplish the target return when all else is the same. Net

present value is based on the discounted cash flow and initial investment proposal or venture

(Parker, 2012). Advantages: The main advantage of this method to consist of fact that focus on the time

value of money and supports to administration for effective decision making procedure. It

is not only supports in analysis of projects of same size but it also supports to recognising

a specific investment for generating profit.

9

Disadvantages: The drawback that it does not focus on the hidden cost and can not be

utilised by business entity in order to compare various projects with each other. In this

method does not follow particular guideline so results may be right may be wrong. The

percentage of value is left to the discretion of organisations and it could be instances

wherein the NPV was inaccurate rate of returns (Prentice, 2016).

Internal rate of return: This method use by business concern to calculate specific

percentage where NPV value is Zero. The break even rate calculate through discounted cash

flows where identify that NPV always Zero. Through this method collect initial investment

which is minimum requirement of the business (Rampini, Viswanathan and Vuillemey, 2019). Advantages: It focus on the value of time that require for any business. In case of

analysing percentage of cost of capital and compare with IRR that could be implemented

then re-evaluated a particular capital project. It presents rank of different project so

according to that a manager take right decision in order to generate profitability.

Disadvantages: In this method ignore economies of scale which is required for any

organisation. When company set any rate of return and it is not match with internal rate

of return so company does not generate effective profitability and create problem for

business (Tang and Baker, 2016).

CONCLUSION

From above report study it has been articulated that entire mechanism of financial

management help managers in effectively managing resources and arrangement of required

funds. This is quite wider aspect which offer various techniques and tool to take decisions and

allocate funds in business's operations.

10

utilised by business entity in order to compare various projects with each other. In this

method does not follow particular guideline so results may be right may be wrong. The

percentage of value is left to the discretion of organisations and it could be instances

wherein the NPV was inaccurate rate of returns (Prentice, 2016).

Internal rate of return: This method use by business concern to calculate specific

percentage where NPV value is Zero. The break even rate calculate through discounted cash

flows where identify that NPV always Zero. Through this method collect initial investment

which is minimum requirement of the business (Rampini, Viswanathan and Vuillemey, 2019). Advantages: It focus on the value of time that require for any business. In case of

analysing percentage of cost of capital and compare with IRR that could be implemented

then re-evaluated a particular capital project. It presents rank of different project so

according to that a manager take right decision in order to generate profitability.

Disadvantages: In this method ignore economies of scale which is required for any

organisation. When company set any rate of return and it is not match with internal rate

of return so company does not generate effective profitability and create problem for

business (Tang and Baker, 2016).

CONCLUSION

From above report study it has been articulated that entire mechanism of financial

management help managers in effectively managing resources and arrangement of required

funds. This is quite wider aspect which offer various techniques and tool to take decisions and

allocate funds in business's operations.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.