Financial Management Report: Analysis of Hillside Industries Expansion

VerifiedAdded on 2022/08/11

|12

|2919

|19

Report

AI Summary

This financial management report analyzes the proposed plant expansion of Hillside Industries, a public listed company. It examines the impact on working capital, including the cash conversion cycle and the need for additional working capital due to an increased average collection period. The report further evaluates the expansion's effect on productivity by comparing accounting and cash break-even points before and after the expansion. Finally, the report employs the Net Present Value (NPV) method to assess the project's feasibility, calculating the Weighted Average Cost of Capital (WACC) and determining a positive NPV, supporting the project's acceptance. The analysis highlights the multi-dimensional approach required in financial decision-making, considering various business areas simultaneously.

FINANCIAL MANAGEMENT

REPORT

TO THE BOARD OF

DIRECTORS OF

HILLSIDE

INDUSTRIES

REPORT

TO THE BOARD OF

DIRECTORS OF

HILLSIDE

INDUSTRIES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Financial management in an organisation involves various decisions and evaluations that are

focussed on the various business areas. The following report highlights the financial

management aspects at the Hillside Industries. As the company is considering the expansion

of the business operations, with the investments in the plant extensions, the related areas such

as the working capital, capital structure are evaluated. Further, the capital budgeting

technique of Net Present Value is employed to assess the feasibility of the project proposal,

based on the forecast of the future cash flows, arising out of expansion. Thus, it has been

concluded that a single financial decision involves multi-dimensional financial management

approach on the part of the top management because of the simultaneous impact on the varied

business areas.

Financial management in an organisation involves various decisions and evaluations that are

focussed on the various business areas. The following report highlights the financial

management aspects at the Hillside Industries. As the company is considering the expansion

of the business operations, with the investments in the plant extensions, the related areas such

as the working capital, capital structure are evaluated. Further, the capital budgeting

technique of Net Present Value is employed to assess the feasibility of the project proposal,

based on the forecast of the future cash flows, arising out of expansion. Thus, it has been

concluded that a single financial decision involves multi-dimensional financial management

approach on the part of the top management because of the simultaneous impact on the varied

business areas.

Contents

Introduction...........................................................................................................................................3

Impact on the working capital...............................................................................................................3

Impact on the productivity.....................................................................................................................5

Project proposal evaluation....................................................................................................................7

Financing decisions...............................................................................................................................9

Conclusion...........................................................................................................................................10

Introduction...........................................................................................................................................3

Impact on the working capital...............................................................................................................3

Impact on the productivity.....................................................................................................................5

Project proposal evaluation....................................................................................................................7

Financing decisions...............................................................................................................................9

Conclusion...........................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Financial management deals with the multi-dimensional coverage of the business operations

and involves various aspects. These range from the decisions regarding the financing,

working capital, project evaluation or the investing and others. It is significant to evaluate

these areas at length as the finds involved in the expansion are not only significant, but the

decisions once taken would not be reversed in the real future (Goyat and Nain, 2016). Hence,

it is important to evaluate the varied financial management aspects to ensure the efficiency of

the funds and the consideration of the stakeholder interests.

The following report is prepared with an objective to guide the senior executives and

management of the Hillside Industries as they contemplate the plant expansion. The varied

business areas that have been discussed in the report are the feasibility of plant expansion

using the capital budgeting tools, impact on the working capital because of the plant

expansion, the computation of the weighted average cost of capital and the comparison of the

accounting and the cash breakeven points before and after expansion.

Impact on the working capital

One of the key business areas that would be impacted because of the plant expansion is that

of the management of the working capital. One of the policies that have been considered by

the board of the directors is to increase the average collection period from existing 15 days to

30 days. This it to ensure the demand of the additional produced 5000 units that would be

produced due to the adoption of the new technology. However, the said move would lead to

the considerable impacts on the working capital of the enterprise, as discussed below.

One of the prime matrices to measure the efficiency of the working capital is the cash

conversion cycle. It is important to note that an efficient working capital management ensures

the sufficiency of the cash and the other short term or the liquid assets within an entity to

ensure the liquidity needed for the payment of the short term obligations. The computation of

the cash conversion cycle enables an entity to assess the number of days in the conversion of

the resources into cash (Ebben and Johnson, 2011). The formula for the cash conversion

cycle is-

Cash Conversion cycle = Operating Cycle - Daily Payments Outstanding

Financial management deals with the multi-dimensional coverage of the business operations

and involves various aspects. These range from the decisions regarding the financing,

working capital, project evaluation or the investing and others. It is significant to evaluate

these areas at length as the finds involved in the expansion are not only significant, but the

decisions once taken would not be reversed in the real future (Goyat and Nain, 2016). Hence,

it is important to evaluate the varied financial management aspects to ensure the efficiency of

the funds and the consideration of the stakeholder interests.

The following report is prepared with an objective to guide the senior executives and

management of the Hillside Industries as they contemplate the plant expansion. The varied

business areas that have been discussed in the report are the feasibility of plant expansion

using the capital budgeting tools, impact on the working capital because of the plant

expansion, the computation of the weighted average cost of capital and the comparison of the

accounting and the cash breakeven points before and after expansion.

Impact on the working capital

One of the key business areas that would be impacted because of the plant expansion is that

of the management of the working capital. One of the policies that have been considered by

the board of the directors is to increase the average collection period from existing 15 days to

30 days. This it to ensure the demand of the additional produced 5000 units that would be

produced due to the adoption of the new technology. However, the said move would lead to

the considerable impacts on the working capital of the enterprise, as discussed below.

One of the prime matrices to measure the efficiency of the working capital is the cash

conversion cycle. It is important to note that an efficient working capital management ensures

the sufficiency of the cash and the other short term or the liquid assets within an entity to

ensure the liquidity needed for the payment of the short term obligations. The computation of

the cash conversion cycle enables an entity to assess the number of days in the conversion of

the resources into cash (Ebben and Johnson, 2011). The formula for the cash conversion

cycle is-

Cash Conversion cycle = Operating Cycle - Daily Payments Outstanding

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Where,

Operating cycle = Daily Sales Outstanding + Daily Inventory Outstanding

The Daily Sales Outstanding or the Average Collection Period refers to the time taken by the

debtors to be converted into cash (Pogue, 2010). The Daily Payments Outstanding or the

Average Payment Period refers to the time taken by the entity to release the payments to the

creditors.

Thus, it is desired by the entities to keep the cash conversion cycle low, so as to ensure the

availability of the cash within the organisation (Attari and Raza, 2012). In addition, as per the

concept of the time value of money, the money in hand today is of more value than the one to

be received later on. The comparison of the existing and the proposed cash conversion cycles

is presented as follows.

Existing cash conversion cycle

Description Number of days

DSO (Average Collection Period) = 15

DIO (Inventory Conversion Period) = 15

DSO (Average Payment Period) = 12

Cash conversion cycle = 18

Proposed cash conversion cycle

Description Number of days

DSO (Average Collection Period) = 30

DIO (Inventory Conversion Period) = 15

DSO (Average Payment Period) = 12

Cash conversion cycle = 33

Thus, as computed above, it can be seen that the cash conversion cycle has increased from 18

days to 33 days in the proposed cash conversion cycle. This is because the average collection

period would be increased from 15 to 30 days. Further, the impact of the same on the

working capital has been highlighted below.

Impact on working capital

Description Number

Increment in the cash conversion cycle (days) = 15

Number of extra units produced (units) = 900

Cost of extra units payable to suppliers = $ 27,000.00

Operating cycle = Daily Sales Outstanding + Daily Inventory Outstanding

The Daily Sales Outstanding or the Average Collection Period refers to the time taken by the

debtors to be converted into cash (Pogue, 2010). The Daily Payments Outstanding or the

Average Payment Period refers to the time taken by the entity to release the payments to the

creditors.

Thus, it is desired by the entities to keep the cash conversion cycle low, so as to ensure the

availability of the cash within the organisation (Attari and Raza, 2012). In addition, as per the

concept of the time value of money, the money in hand today is of more value than the one to

be received later on. The comparison of the existing and the proposed cash conversion cycles

is presented as follows.

Existing cash conversion cycle

Description Number of days

DSO (Average Collection Period) = 15

DIO (Inventory Conversion Period) = 15

DSO (Average Payment Period) = 12

Cash conversion cycle = 18

Proposed cash conversion cycle

Description Number of days

DSO (Average Collection Period) = 30

DIO (Inventory Conversion Period) = 15

DSO (Average Payment Period) = 12

Cash conversion cycle = 33

Thus, as computed above, it can be seen that the cash conversion cycle has increased from 18

days to 33 days in the proposed cash conversion cycle. This is because the average collection

period would be increased from 15 to 30 days. Further, the impact of the same on the

working capital has been highlighted below.

Impact on working capital

Description Number

Increment in the cash conversion cycle (days) = 15

Number of extra units produced (units) = 900

Cost of extra units payable to suppliers = $ 27,000.00

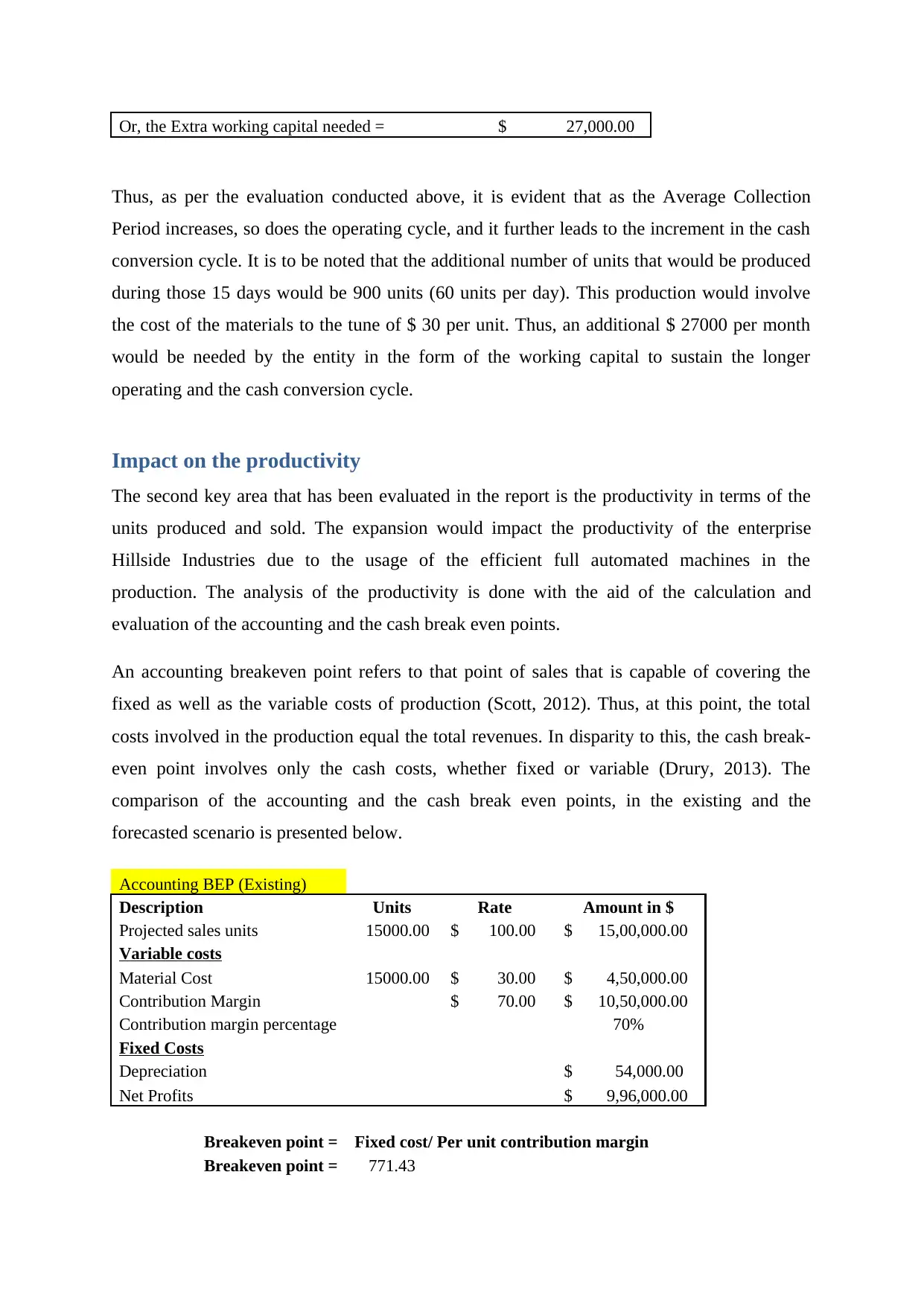

Or, the Extra working capital needed = $ 27,000.00

Thus, as per the evaluation conducted above, it is evident that as the Average Collection

Period increases, so does the operating cycle, and it further leads to the increment in the cash

conversion cycle. It is to be noted that the additional number of units that would be produced

during those 15 days would be 900 units (60 units per day). This production would involve

the cost of the materials to the tune of $ 30 per unit. Thus, an additional $ 27000 per month

would be needed by the entity in the form of the working capital to sustain the longer

operating and the cash conversion cycle.

Impact on the productivity

The second key area that has been evaluated in the report is the productivity in terms of the

units produced and sold. The expansion would impact the productivity of the enterprise

Hillside Industries due to the usage of the efficient full automated machines in the

production. The analysis of the productivity is done with the aid of the calculation and

evaluation of the accounting and the cash break even points.

An accounting breakeven point refers to that point of sales that is capable of covering the

fixed as well as the variable costs of production (Scott, 2012). Thus, at this point, the total

costs involved in the production equal the total revenues. In disparity to this, the cash break-

even point involves only the cash costs, whether fixed or variable (Drury, 2013). The

comparison of the accounting and the cash break even points, in the existing and the

forecasted scenario is presented below.

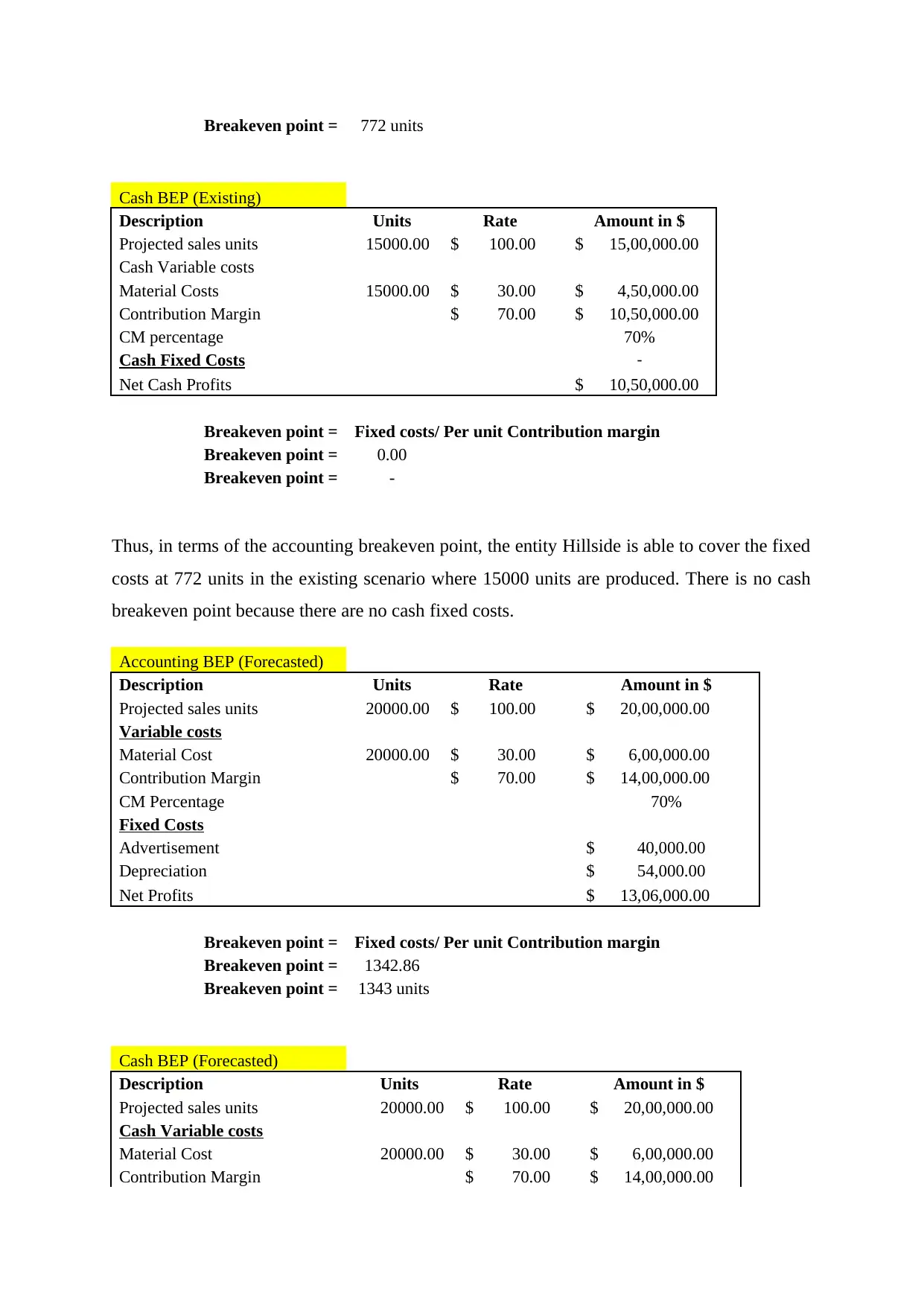

Accounting BEP (Existing)

Description Units Rate Amount in $

Projected sales units 15000.00 $ 100.00 $ 15,00,000.00

Variable costs

Material Cost 15000.00 $ 30.00 $ 4,50,000.00

Contribution Margin $ 70.00 $ 10,50,000.00

Contribution margin percentage 70%

Fixed Costs

Depreciation $ 54,000.00

Net Profits $ 9,96,000.00

Breakeven point = Fixed cost/ Per unit contribution margin

Breakeven point = 771.43

Thus, as per the evaluation conducted above, it is evident that as the Average Collection

Period increases, so does the operating cycle, and it further leads to the increment in the cash

conversion cycle. It is to be noted that the additional number of units that would be produced

during those 15 days would be 900 units (60 units per day). This production would involve

the cost of the materials to the tune of $ 30 per unit. Thus, an additional $ 27000 per month

would be needed by the entity in the form of the working capital to sustain the longer

operating and the cash conversion cycle.

Impact on the productivity

The second key area that has been evaluated in the report is the productivity in terms of the

units produced and sold. The expansion would impact the productivity of the enterprise

Hillside Industries due to the usage of the efficient full automated machines in the

production. The analysis of the productivity is done with the aid of the calculation and

evaluation of the accounting and the cash break even points.

An accounting breakeven point refers to that point of sales that is capable of covering the

fixed as well as the variable costs of production (Scott, 2012). Thus, at this point, the total

costs involved in the production equal the total revenues. In disparity to this, the cash break-

even point involves only the cash costs, whether fixed or variable (Drury, 2013). The

comparison of the accounting and the cash break even points, in the existing and the

forecasted scenario is presented below.

Accounting BEP (Existing)

Description Units Rate Amount in $

Projected sales units 15000.00 $ 100.00 $ 15,00,000.00

Variable costs

Material Cost 15000.00 $ 30.00 $ 4,50,000.00

Contribution Margin $ 70.00 $ 10,50,000.00

Contribution margin percentage 70%

Fixed Costs

Depreciation $ 54,000.00

Net Profits $ 9,96,000.00

Breakeven point = Fixed cost/ Per unit contribution margin

Breakeven point = 771.43

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Breakeven point = 772 units

Cash BEP (Existing)

Description Units Rate Amount in $

Projected sales units 15000.00 $ 100.00 $ 15,00,000.00

Cash Variable costs

Material Costs 15000.00 $ 30.00 $ 4,50,000.00

Contribution Margin $ 70.00 $ 10,50,000.00

CM percentage 70%

Cash Fixed Costs -

Net Cash Profits $ 10,50,000.00

Breakeven point = Fixed costs/ Per unit Contribution margin

Breakeven point = 0.00

Breakeven point = -

Thus, in terms of the accounting breakeven point, the entity Hillside is able to cover the fixed

costs at 772 units in the existing scenario where 15000 units are produced. There is no cash

breakeven point because there are no cash fixed costs.

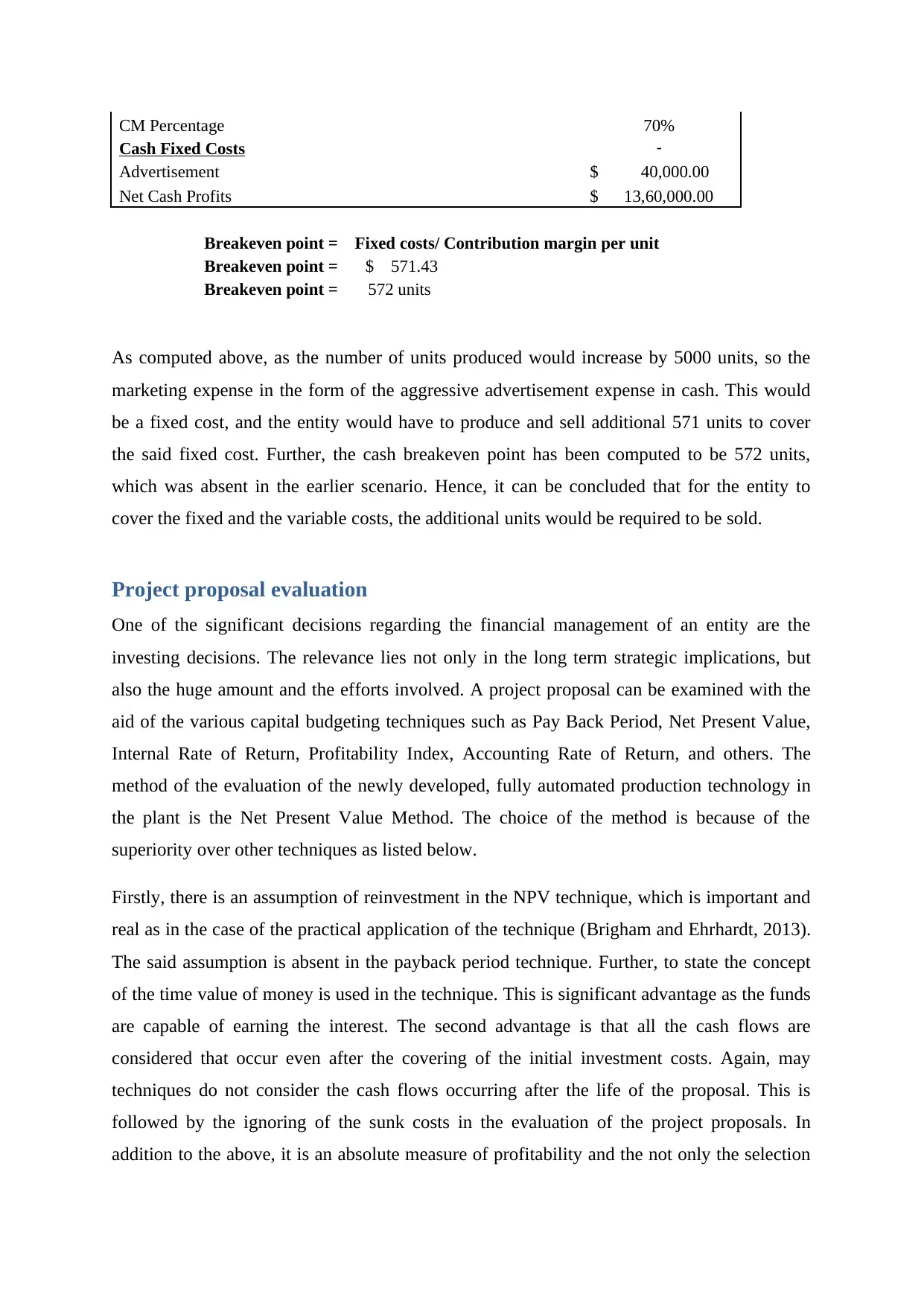

Accounting BEP (Forecasted)

Description Units Rate Amount in $

Projected sales units 20000.00 $ 100.00 $ 20,00,000.00

Variable costs

Material Cost 20000.00 $ 30.00 $ 6,00,000.00

Contribution Margin $ 70.00 $ 14,00,000.00

CM Percentage 70%

Fixed Costs

Advertisement $ 40,000.00

Depreciation $ 54,000.00

Net Profits $ 13,06,000.00

Breakeven point = Fixed costs/ Per unit Contribution margin

Breakeven point = 1342.86

Breakeven point = 1343 units

Cash BEP (Forecasted)

Description Units Rate Amount in $

Projected sales units 20000.00 $ 100.00 $ 20,00,000.00

Cash Variable costs

Material Cost 20000.00 $ 30.00 $ 6,00,000.00

Contribution Margin $ 70.00 $ 14,00,000.00

Cash BEP (Existing)

Description Units Rate Amount in $

Projected sales units 15000.00 $ 100.00 $ 15,00,000.00

Cash Variable costs

Material Costs 15000.00 $ 30.00 $ 4,50,000.00

Contribution Margin $ 70.00 $ 10,50,000.00

CM percentage 70%

Cash Fixed Costs -

Net Cash Profits $ 10,50,000.00

Breakeven point = Fixed costs/ Per unit Contribution margin

Breakeven point = 0.00

Breakeven point = -

Thus, in terms of the accounting breakeven point, the entity Hillside is able to cover the fixed

costs at 772 units in the existing scenario where 15000 units are produced. There is no cash

breakeven point because there are no cash fixed costs.

Accounting BEP (Forecasted)

Description Units Rate Amount in $

Projected sales units 20000.00 $ 100.00 $ 20,00,000.00

Variable costs

Material Cost 20000.00 $ 30.00 $ 6,00,000.00

Contribution Margin $ 70.00 $ 14,00,000.00

CM Percentage 70%

Fixed Costs

Advertisement $ 40,000.00

Depreciation $ 54,000.00

Net Profits $ 13,06,000.00

Breakeven point = Fixed costs/ Per unit Contribution margin

Breakeven point = 1342.86

Breakeven point = 1343 units

Cash BEP (Forecasted)

Description Units Rate Amount in $

Projected sales units 20000.00 $ 100.00 $ 20,00,000.00

Cash Variable costs

Material Cost 20000.00 $ 30.00 $ 6,00,000.00

Contribution Margin $ 70.00 $ 14,00,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CM Percentage 70%

Cash Fixed Costs -

Advertisement $ 40,000.00

Net Cash Profits $ 13,60,000.00

Breakeven point = Fixed costs/ Contribution margin per unit

Breakeven point = $ 571.43

Breakeven point = 572 units

As computed above, as the number of units produced would increase by 5000 units, so the

marketing expense in the form of the aggressive advertisement expense in cash. This would

be a fixed cost, and the entity would have to produce and sell additional 571 units to cover

the said fixed cost. Further, the cash breakeven point has been computed to be 572 units,

which was absent in the earlier scenario. Hence, it can be concluded that for the entity to

cover the fixed and the variable costs, the additional units would be required to be sold.

Project proposal evaluation

One of the significant decisions regarding the financial management of an entity are the

investing decisions. The relevance lies not only in the long term strategic implications, but

also the huge amount and the efforts involved. A project proposal can be examined with the

aid of the various capital budgeting techniques such as Pay Back Period, Net Present Value,

Internal Rate of Return, Profitability Index, Accounting Rate of Return, and others. The

method of the evaluation of the newly developed, fully automated production technology in

the plant is the Net Present Value Method. The choice of the method is because of the

superiority over other techniques as listed below.

Firstly, there is an assumption of reinvestment in the NPV technique, which is important and

real as in the case of the practical application of the technique (Brigham and Ehrhardt, 2013).

The said assumption is absent in the payback period technique. Further, to state the concept

of the time value of money is used in the technique. This is significant advantage as the funds

are capable of earning the interest. The second advantage is that all the cash flows are

considered that occur even after the covering of the initial investment costs. Again, may

techniques do not consider the cash flows occurring after the life of the proposal. This is

followed by the ignoring of the sunk costs in the evaluation of the project proposals. In

addition to the above, it is an absolute measure of profitability and the not only the selection

Cash Fixed Costs -

Advertisement $ 40,000.00

Net Cash Profits $ 13,60,000.00

Breakeven point = Fixed costs/ Contribution margin per unit

Breakeven point = $ 571.43

Breakeven point = 572 units

As computed above, as the number of units produced would increase by 5000 units, so the

marketing expense in the form of the aggressive advertisement expense in cash. This would

be a fixed cost, and the entity would have to produce and sell additional 571 units to cover

the said fixed cost. Further, the cash breakeven point has been computed to be 572 units,

which was absent in the earlier scenario. Hence, it can be concluded that for the entity to

cover the fixed and the variable costs, the additional units would be required to be sold.

Project proposal evaluation

One of the significant decisions regarding the financial management of an entity are the

investing decisions. The relevance lies not only in the long term strategic implications, but

also the huge amount and the efforts involved. A project proposal can be examined with the

aid of the various capital budgeting techniques such as Pay Back Period, Net Present Value,

Internal Rate of Return, Profitability Index, Accounting Rate of Return, and others. The

method of the evaluation of the newly developed, fully automated production technology in

the plant is the Net Present Value Method. The choice of the method is because of the

superiority over other techniques as listed below.

Firstly, there is an assumption of reinvestment in the NPV technique, which is important and

real as in the case of the practical application of the technique (Brigham and Ehrhardt, 2013).

The said assumption is absent in the payback period technique. Further, to state the concept

of the time value of money is used in the technique. This is significant advantage as the funds

are capable of earning the interest. The second advantage is that all the cash flows are

considered that occur even after the covering of the initial investment costs. Again, may

techniques do not consider the cash flows occurring after the life of the proposal. This is

followed by the ignoring of the sunk costs in the evaluation of the project proposals. In

addition to the above, it is an absolute measure of profitability and the not only the selection

or the rejection of the proposal is suggested, but also the exact profits are determined (Gὂtze,

Northcott and Schuster, 2015).

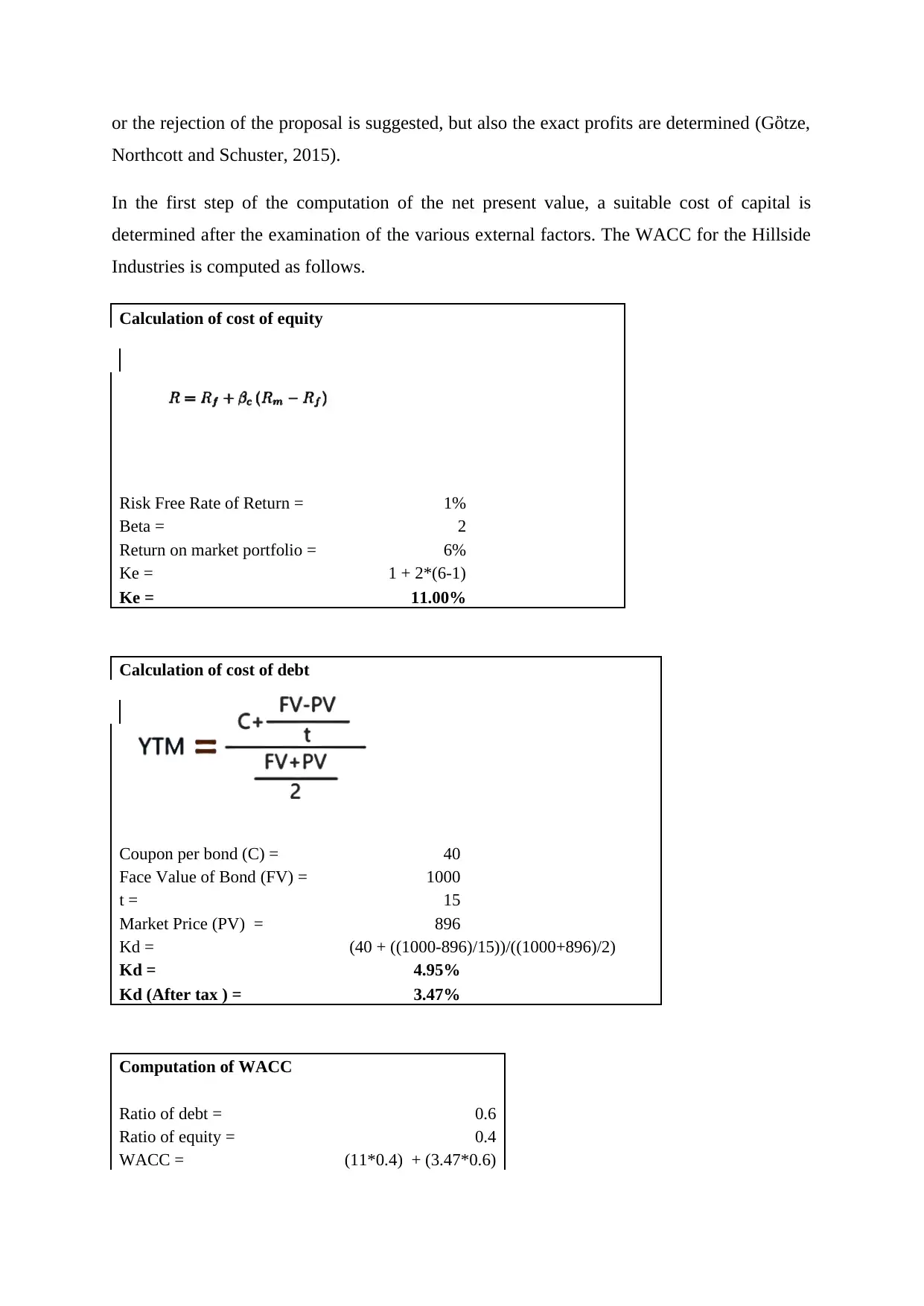

In the first step of the computation of the net present value, a suitable cost of capital is

determined after the examination of the various external factors. The WACC for the Hillside

Industries is computed as follows.

Calculation of cost of equity

Risk Free Rate of Return = 1%

Beta = 2

Return on market portfolio = 6%

Ke = 1 + 2*(6-1)

Ke = 11.00%

Calculation of cost of debt

Coupon per bond (C) = 40

Face Value of Bond (FV) = 1000

t = 15

Market Price (PV) = 896

Kd = (40 + ((1000-896)/15))/((1000+896)/2)

Kd = 4.95%

Kd (After tax ) = 3.47%

Computation of WACC

Ratio of debt = 0.6

Ratio of equity = 0.4

WACC = (11*0.4) + (3.47*0.6)

Northcott and Schuster, 2015).

In the first step of the computation of the net present value, a suitable cost of capital is

determined after the examination of the various external factors. The WACC for the Hillside

Industries is computed as follows.

Calculation of cost of equity

Risk Free Rate of Return = 1%

Beta = 2

Return on market portfolio = 6%

Ke = 1 + 2*(6-1)

Ke = 11.00%

Calculation of cost of debt

Coupon per bond (C) = 40

Face Value of Bond (FV) = 1000

t = 15

Market Price (PV) = 896

Kd = (40 + ((1000-896)/15))/((1000+896)/2)

Kd = 4.95%

Kd (After tax ) = 3.47%

Computation of WACC

Ratio of debt = 0.6

Ratio of equity = 0.4

WACC = (11*0.4) + (3.47*0.6)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

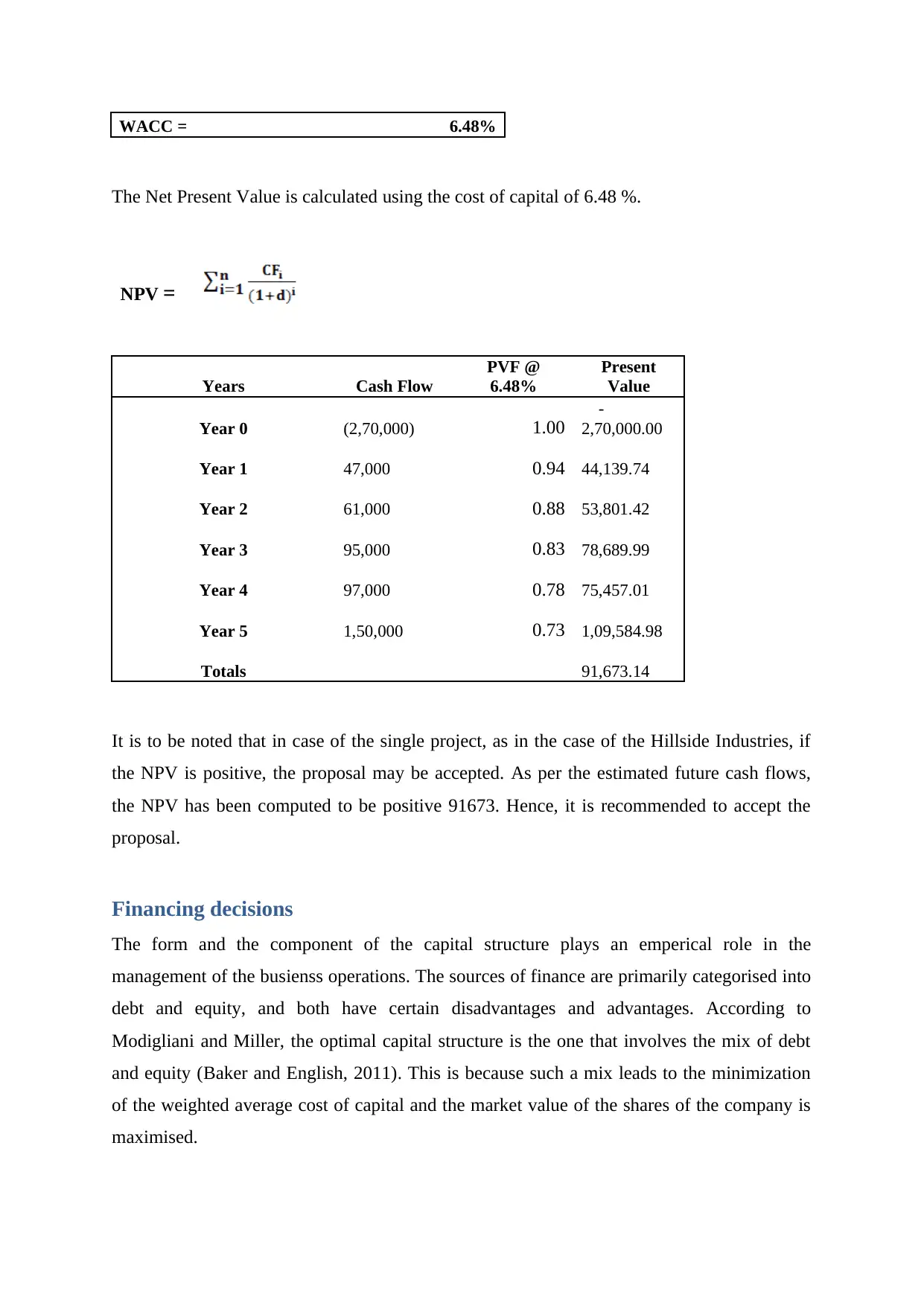

WACC = 6.48%

The Net Present Value is calculated using the cost of capital of 6.48 %.

NPV =

Years Cash Flow

PVF @

6.48%

Present

Value

Year 0 (2,70,000) 1.00

-

2,70,000.00

Year 1 47,000 0.94 44,139.74

Year 2 61,000 0.88 53,801.42

Year 3 95,000 0.83 78,689.99

Year 4 97,000 0.78 75,457.01

Year 5 1,50,000 0.73 1,09,584.98

Totals 91,673.14

It is to be noted that in case of the single project, as in the case of the Hillside Industries, if

the NPV is positive, the proposal may be accepted. As per the estimated future cash flows,

the NPV has been computed to be positive 91673. Hence, it is recommended to accept the

proposal.

Financing decisions

The form and the component of the capital structure plays an emperical role in the

management of the busienss operations. The sources of finance are primarily categorised into

debt and equity, and both have certain disadvantages and advantages. According to

Modigliani and Miller, the optimal capital structure is the one that involves the mix of debt

and equity (Baker and English, 2011). This is because such a mix leads to the minimization

of the weighted average cost of capital and the market value of the shares of the company is

maximised.

The Net Present Value is calculated using the cost of capital of 6.48 %.

NPV =

Years Cash Flow

PVF @

6.48%

Present

Value

Year 0 (2,70,000) 1.00

-

2,70,000.00

Year 1 47,000 0.94 44,139.74

Year 2 61,000 0.88 53,801.42

Year 3 95,000 0.83 78,689.99

Year 4 97,000 0.78 75,457.01

Year 5 1,50,000 0.73 1,09,584.98

Totals 91,673.14

It is to be noted that in case of the single project, as in the case of the Hillside Industries, if

the NPV is positive, the proposal may be accepted. As per the estimated future cash flows,

the NPV has been computed to be positive 91673. Hence, it is recommended to accept the

proposal.

Financing decisions

The form and the component of the capital structure plays an emperical role in the

management of the busienss operations. The sources of finance are primarily categorised into

debt and equity, and both have certain disadvantages and advantages. According to

Modigliani and Miller, the optimal capital structure is the one that involves the mix of debt

and equity (Baker and English, 2011). This is because such a mix leads to the minimization

of the weighted average cost of capital and the market value of the shares of the company is

maximised.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

As stated in the previous parts, the overall cost of capital of the company was calculated to be

6.48 %. The advantage of taxation in the cost of debt led to the reduction in the overall cost

of captial while the cost of equity was much higher than the cost of debt. Accordingly, it has

been recommended to the board of directors to raise the additional funds for the expansion

through the debt mode itself, to create a tax shelter on the increased earnings of the company.

The benefits of the debt financing are highlighted in brief as follows.

The debt financing does not leads to the dilution of the control of the existing owners, and

thus reduces the conflicting decisions in the management of the enterprise. This is followed

by the leverage effect on the cost of capital. Further, apart from the regular interest payments,

there is no burdern of sharing of the profits, and the market value is not affected.

Conclusion

The previous parts of the report highighted the evaluation of varius areas that woud be

impacted with the new project proposal into consideration, that are the workin capital,

productivity, and the captial structure. Based on the qualitative and the quantitavive factors as

analysed in the report, it has been recommended to the management to accept the project

proposal and carry on the expansion of the enterprise with the new automated technology.

The said proposal is efficient from the NPV point of view, and must be financed by debt.

Additionally the working capital changes are manageable and board must ensure to maintain

the liquidity in the financing.

6.48 %. The advantage of taxation in the cost of debt led to the reduction in the overall cost

of captial while the cost of equity was much higher than the cost of debt. Accordingly, it has

been recommended to the board of directors to raise the additional funds for the expansion

through the debt mode itself, to create a tax shelter on the increased earnings of the company.

The benefits of the debt financing are highlighted in brief as follows.

The debt financing does not leads to the dilution of the control of the existing owners, and

thus reduces the conflicting decisions in the management of the enterprise. This is followed

by the leverage effect on the cost of capital. Further, apart from the regular interest payments,

there is no burdern of sharing of the profits, and the market value is not affected.

Conclusion

The previous parts of the report highighted the evaluation of varius areas that woud be

impacted with the new project proposal into consideration, that are the workin capital,

productivity, and the captial structure. Based on the qualitative and the quantitavive factors as

analysed in the report, it has been recommended to the management to accept the project

proposal and carry on the expansion of the enterprise with the new automated technology.

The said proposal is efficient from the NPV point of view, and must be financed by debt.

Additionally the working capital changes are manageable and board must ensure to maintain

the liquidity in the financing.

References

Attari, M.A. and Raza, K., (2012) The optimal relationship of cash conversion cycle with

firm size and profitability. International Journal of Academic Research in Business and

Social Sciences, 2(4), p. 189.

Baker, H. K., and English, P. (2011) Capital Budgeting Valuation: Financial Analysis for

Today's Investment Projects. New Jersey: John Wiley & Sons Inc.

Brigham, E. F. and Ehrhardt, M. C. (2013) Financial management: Theory & practice.

Boston MA: Cengage Learning.

Drury, C. M. (2013) Management and cost accounting. UK: Springer.

Ebben, J. J. and Johnson, A. C. (2011) Cash conversion cycle management in small firms:

Relationships with liquidity, invested capital, and firm performance. Journal of Small

Business & Entrepreneurship, 24(3), pp. 381-396.

Goyat, S., and Nain, A. (2016) Methods of Evaluating Investment Proposals. International

Journal of Engineering and Management Research (IJEMR), 6(5), p. 279.

Gὂtze, U., Northcott, D., and Schuster, P. (2015) Investment Appraisal: Methods and Models.

2nd ed. London: Springer, p. 63.

Pogue, M. (2010) Corporate Investment Decisions: Principles and Practice. New York:

Business Expert Press, p. 53.

Scott, P. (2012) Accounting for Business: An Integrated Print and Online Solution. Oxford:

Oxford University Press, p. 342.

Attari, M.A. and Raza, K., (2012) The optimal relationship of cash conversion cycle with

firm size and profitability. International Journal of Academic Research in Business and

Social Sciences, 2(4), p. 189.

Baker, H. K., and English, P. (2011) Capital Budgeting Valuation: Financial Analysis for

Today's Investment Projects. New Jersey: John Wiley & Sons Inc.

Brigham, E. F. and Ehrhardt, M. C. (2013) Financial management: Theory & practice.

Boston MA: Cengage Learning.

Drury, C. M. (2013) Management and cost accounting. UK: Springer.

Ebben, J. J. and Johnson, A. C. (2011) Cash conversion cycle management in small firms:

Relationships with liquidity, invested capital, and firm performance. Journal of Small

Business & Entrepreneurship, 24(3), pp. 381-396.

Goyat, S., and Nain, A. (2016) Methods of Evaluating Investment Proposals. International

Journal of Engineering and Management Research (IJEMR), 6(5), p. 279.

Gὂtze, U., Northcott, D., and Schuster, P. (2015) Investment Appraisal: Methods and Models.

2nd ed. London: Springer, p. 63.

Pogue, M. (2010) Corporate Investment Decisions: Principles and Practice. New York:

Business Expert Press, p. 53.

Scott, P. (2012) Accounting for Business: An Integrated Print and Online Solution. Oxford:

Oxford University Press, p. 342.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.