Financial Management Report: Ratio Analysis and Investment

VerifiedAdded on 2021/12/14

|27

|6586

|84

Report

AI Summary

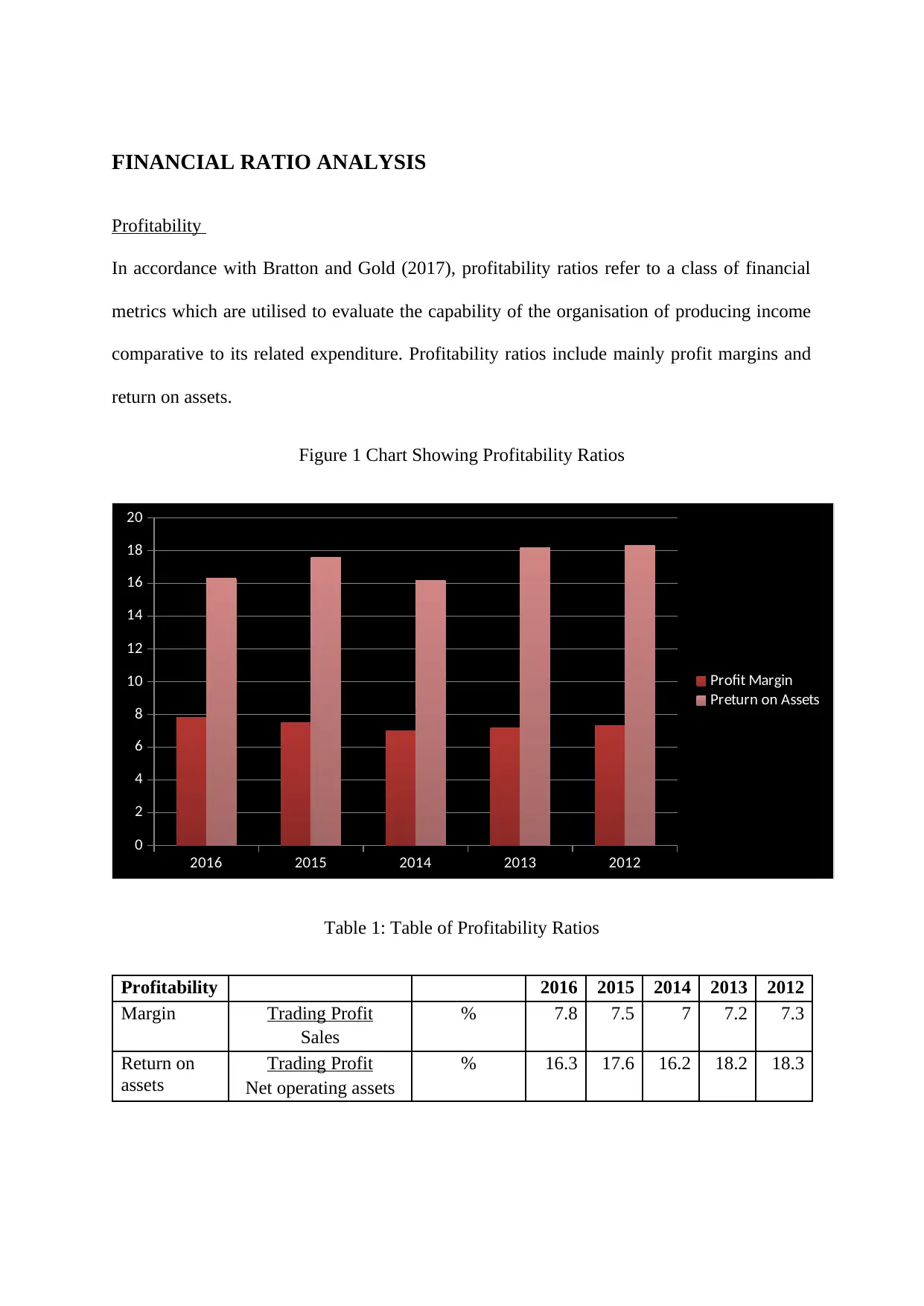

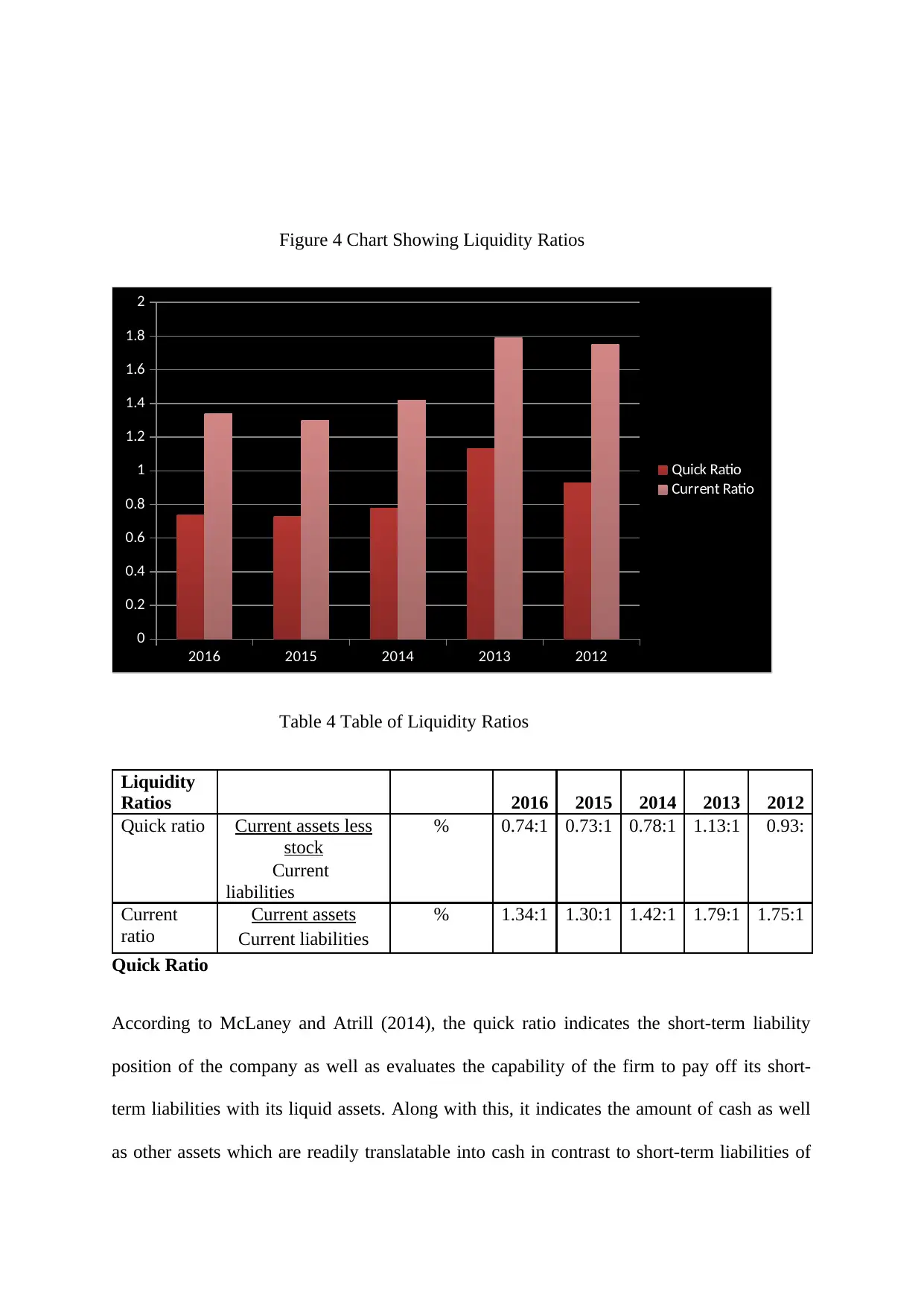

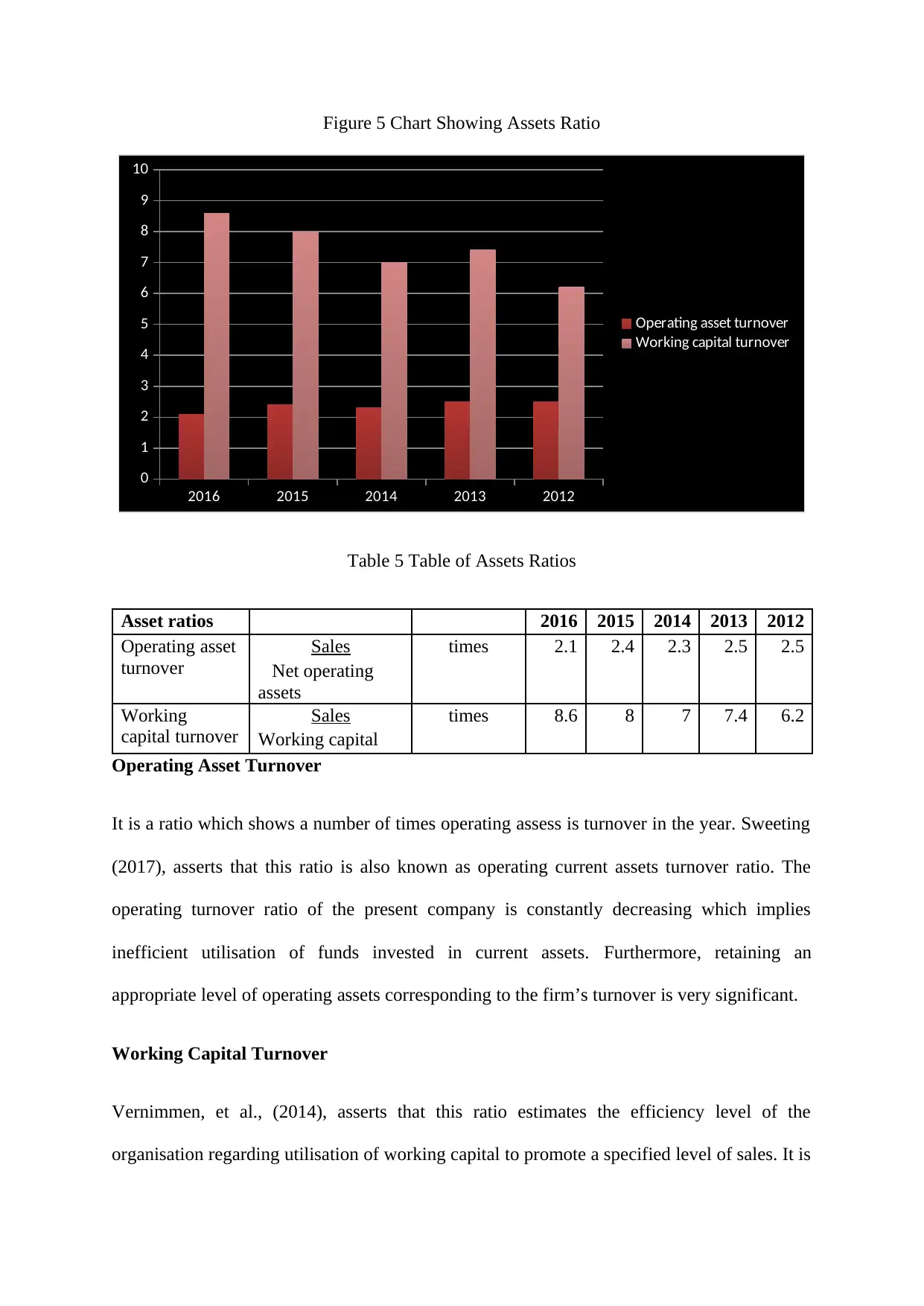

This financial management report presents a comprehensive analysis of Outdoor Plc.'s financial performance, utilizing various financial ratio analysis techniques and investment appraisal methods. The report begins by examining profitability ratios, including margin and return on assets, to assess the company's ability to generate income relative to its expenditures and assets. It then delves into interest and dividend coverage ratios, evaluating the company's capacity to meet its debt obligations and distribute dividends. Further, the report analyzes the debt-to-equity ratio and liquidity ratios to gauge the company's financial stability and short-term solvency. Asset ratios are also evaluated to determine the efficiency of asset utilization. The second part of the report focuses on investment appraisal techniques, specifically calculating the Net Present Value (NPV) and Internal Rate of Return (IRR) for different projects, and then comparing these methods to assess the best investment options. The report concludes with an overview of the main sources of finance, including owned and borrowed capital.

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.