Financial Management and Control: Pro Bio PLC Performance Analysis

VerifiedAdded on 2023/01/17

|21

|4489

|71

Report

AI Summary

This report provides a comprehensive financial analysis of Pro Bio PLC, evaluating its performance through various financial ratios, including profitability, liquidity, gearing, assets utilization, and investor potential ratios. It calculates and analyzes the working capital cycle, comparing the company's efficiency in converting current assets into cash over two years. The report also discusses the limitations of ratio analysis in both cross-sectional and time-series comparisons. Furthermore, it explores different investment appraisal techniques and various traditional budgeting methods. The analysis is based on the provided financial statements and aims to assess the company's financial health and identify areas for improvement. The report is structured into three parts, covering different aspects of financial management and control, and includes tables and graphs to support the analysis.

FINANCIAL

MANAGEMENT AND

CONTROL

MANAGEMENT AND

CONTROL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Part (A)........................................................................................................................................3

1. Evaluation of performance of Pro Bio plc in terms of different types of ratios......................3

2. Calculation of working capital cycle.....................................................................................10

3. Limitation of ratio analysis for both cross-sectional and time-series comparisons..............12

Part (B) .....................................................................................................................................13

1. Use of different types of investment appraisal techniques....................................................13

Part (C)......................................................................................................................................17

2. Use of various kinds of traditional budgeting methods........................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Part (A)........................................................................................................................................3

1. Evaluation of performance of Pro Bio plc in terms of different types of ratios......................3

2. Calculation of working capital cycle.....................................................................................10

3. Limitation of ratio analysis for both cross-sectional and time-series comparisons..............12

Part (B) .....................................................................................................................................13

1. Use of different types of investment appraisal techniques....................................................13

Part (C)......................................................................................................................................17

2. Use of various kinds of traditional budgeting methods........................................................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................18

INTRODUCTION

In the current business scenario, it is essential to make an effective utilisation of

resources so that level of profitability can be increase. The term financial management can be

defined as a way of assessing need of financial resources in companies and providing funds from

best resources. In this aspect controlling of monetary funds is also essential so that it can be

allocated to different activities in a better way (Doinea and Lapadat, 2012). Main objective of

report is to assessing the performance of given company. The project report is categorised into

different parts in which part A, covers information about various ratios, and working capital

cycle. As well as part B, includes description of investment appraisal techniques and part C,

contains information about role of traditional budgeting methods.

MAIN BODY

Part (A)

1. Evaluation of performance of Pro Bio plc in terms of different types of ratios.

Profitability ratio- This is a type of ratio which is calculated by business entities in order

to assess efficiency of generating revenues (Chan, Chau and Chan, 2012). Herein, below

some ratios are mentioned that are as follows:

(I) Gross profit ratio = Gross profit / Net sales * 100

All data in £000 except gross

profit ratio

2018 2019

Gross profit 9850 9485

Net sales 17890 19345

Calculation 9850/17890*100 9485/19345*100

Gross profit ratio 55.06% 49.03%

In the current business scenario, it is essential to make an effective utilisation of

resources so that level of profitability can be increase. The term financial management can be

defined as a way of assessing need of financial resources in companies and providing funds from

best resources. In this aspect controlling of monetary funds is also essential so that it can be

allocated to different activities in a better way (Doinea and Lapadat, 2012). Main objective of

report is to assessing the performance of given company. The project report is categorised into

different parts in which part A, covers information about various ratios, and working capital

cycle. As well as part B, includes description of investment appraisal techniques and part C,

contains information about role of traditional budgeting methods.

MAIN BODY

Part (A)

1. Evaluation of performance of Pro Bio plc in terms of different types of ratios.

Profitability ratio- This is a type of ratio which is calculated by business entities in order

to assess efficiency of generating revenues (Chan, Chau and Chan, 2012). Herein, below

some ratios are mentioned that are as follows:

(I) Gross profit ratio = Gross profit / Net sales * 100

All data in £000 except gross

profit ratio

2018 2019

Gross profit 9850 9485

Net sales 17890 19345

Calculation 9850/17890*100 9485/19345*100

Gross profit ratio 55.06% 49.03%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

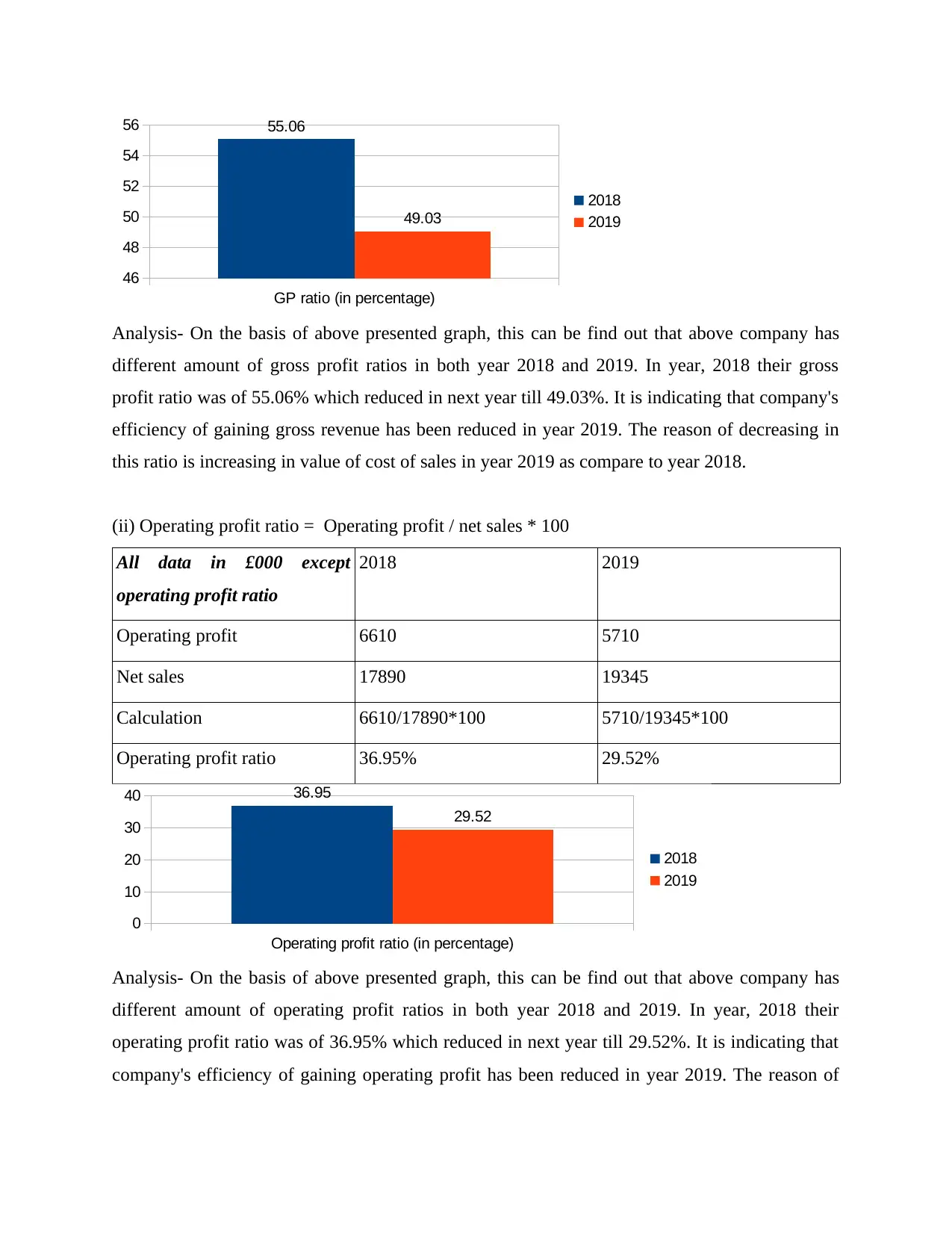

GP ratio (in percentage)

46

48

50

52

54

56 55.06

49.03

2018

2019

Analysis- On the basis of above presented graph, this can be find out that above company has

different amount of gross profit ratios in both year 2018 and 2019. In year, 2018 their gross

profit ratio was of 55.06% which reduced in next year till 49.03%. It is indicating that company's

efficiency of gaining gross revenue has been reduced in year 2019. The reason of decreasing in

this ratio is increasing in value of cost of sales in year 2019 as compare to year 2018.

(ii) Operating profit ratio = Operating profit / net sales * 100

All data in £000 except

operating profit ratio

2018 2019

Operating profit 6610 5710

Net sales 17890 19345

Calculation 6610/17890*100 5710/19345*100

Operating profit ratio 36.95% 29.52%

Operating profit ratio (in percentage)

0

10

20

30

40 36.95

29.52

2018

2019

Analysis- On the basis of above presented graph, this can be find out that above company has

different amount of operating profit ratios in both year 2018 and 2019. In year, 2018 their

operating profit ratio was of 36.95% which reduced in next year till 29.52%. It is indicating that

company's efficiency of gaining operating profit has been reduced in year 2019. The reason of

46

48

50

52

54

56 55.06

49.03

2018

2019

Analysis- On the basis of above presented graph, this can be find out that above company has

different amount of gross profit ratios in both year 2018 and 2019. In year, 2018 their gross

profit ratio was of 55.06% which reduced in next year till 49.03%. It is indicating that company's

efficiency of gaining gross revenue has been reduced in year 2019. The reason of decreasing in

this ratio is increasing in value of cost of sales in year 2019 as compare to year 2018.

(ii) Operating profit ratio = Operating profit / net sales * 100

All data in £000 except

operating profit ratio

2018 2019

Operating profit 6610 5710

Net sales 17890 19345

Calculation 6610/17890*100 5710/19345*100

Operating profit ratio 36.95% 29.52%

Operating profit ratio (in percentage)

0

10

20

30

40 36.95

29.52

2018

2019

Analysis- On the basis of above presented graph, this can be find out that above company has

different amount of operating profit ratios in both year 2018 and 2019. In year, 2018 their

operating profit ratio was of 36.95% which reduced in next year till 29.52%. It is indicating that

company's efficiency of gaining operating profit has been reduced in year 2019. The reason of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

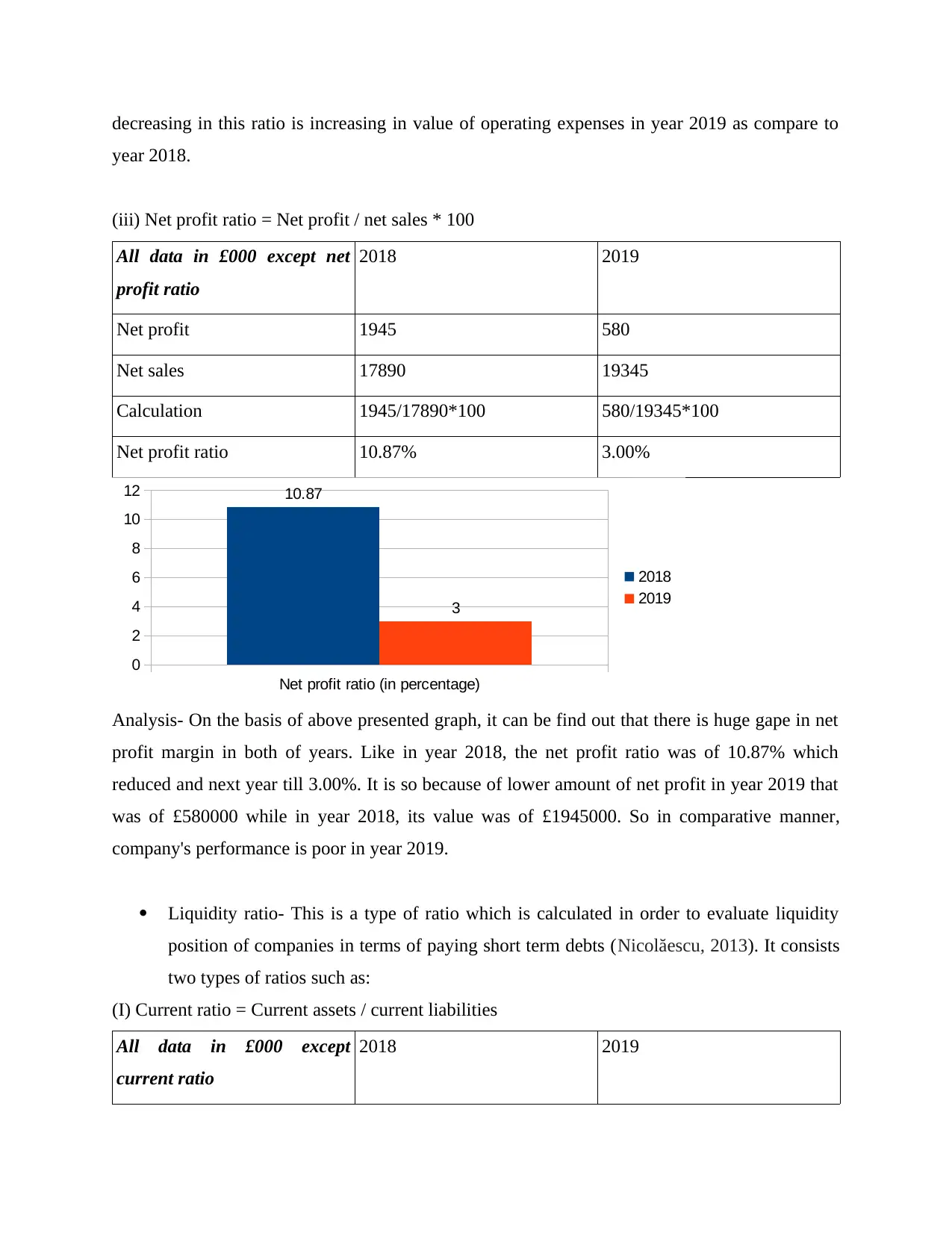

decreasing in this ratio is increasing in value of operating expenses in year 2019 as compare to

year 2018.

(iii) Net profit ratio = Net profit / net sales * 100

All data in £000 except net

profit ratio

2018 2019

Net profit 1945 580

Net sales 17890 19345

Calculation 1945/17890*100 580/19345*100

Net profit ratio 10.87% 3.00%

Net profit ratio (in percentage)

0

2

4

6

8

10

12 10.87

3

2018

2019

Analysis- On the basis of above presented graph, it can be find out that there is huge gape in net

profit margin in both of years. Like in year 2018, the net profit ratio was of 10.87% which

reduced and next year till 3.00%. It is so because of lower amount of net profit in year 2019 that

was of £580000 while in year 2018, its value was of £1945000. So in comparative manner,

company's performance is poor in year 2019.

Liquidity ratio- This is a type of ratio which is calculated in order to evaluate liquidity

position of companies in terms of paying short term debts (Nicolăescu, 2013). It consists

two types of ratios such as:

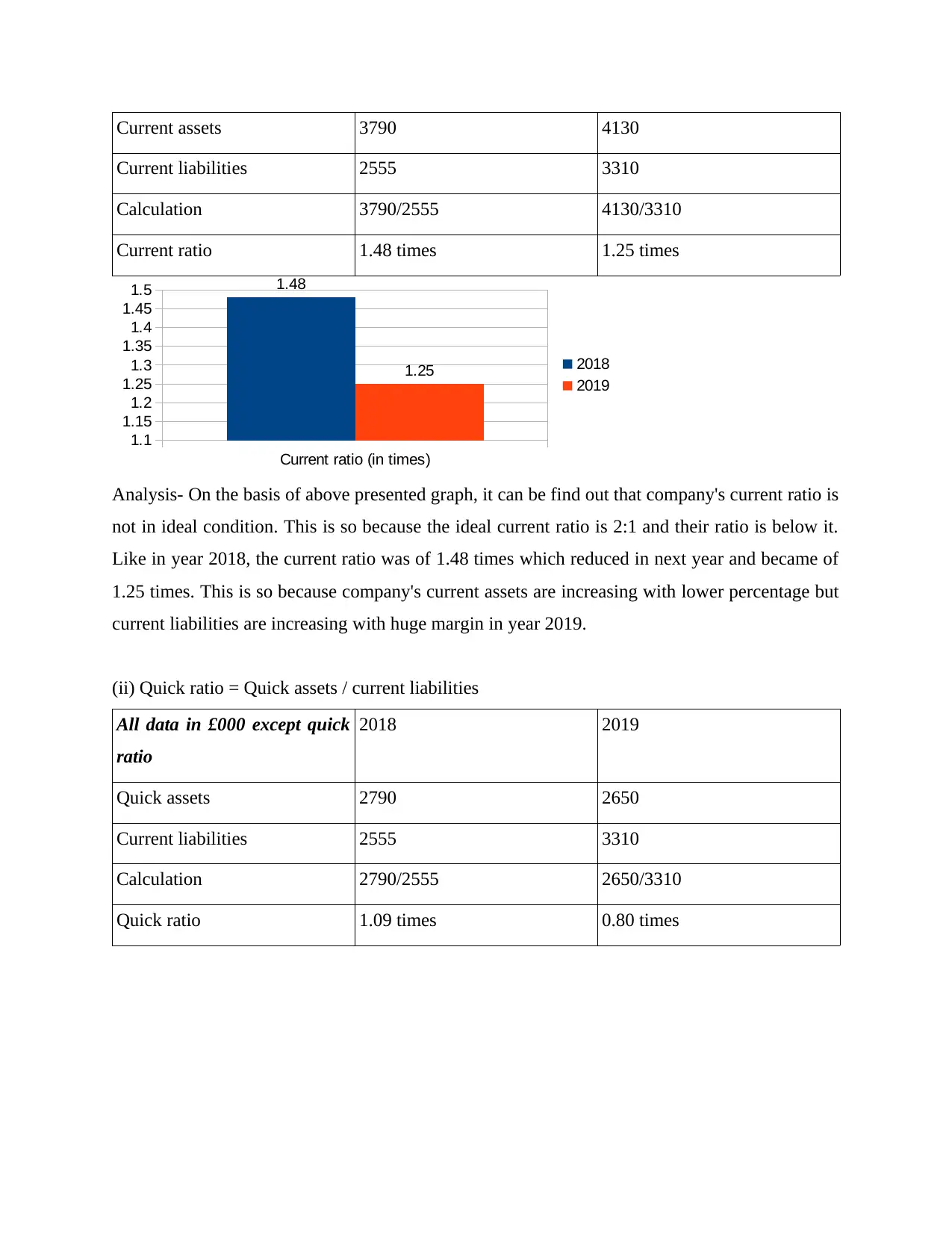

(I) Current ratio = Current assets / current liabilities

All data in £000 except

current ratio

2018 2019

year 2018.

(iii) Net profit ratio = Net profit / net sales * 100

All data in £000 except net

profit ratio

2018 2019

Net profit 1945 580

Net sales 17890 19345

Calculation 1945/17890*100 580/19345*100

Net profit ratio 10.87% 3.00%

Net profit ratio (in percentage)

0

2

4

6

8

10

12 10.87

3

2018

2019

Analysis- On the basis of above presented graph, it can be find out that there is huge gape in net

profit margin in both of years. Like in year 2018, the net profit ratio was of 10.87% which

reduced and next year till 3.00%. It is so because of lower amount of net profit in year 2019 that

was of £580000 while in year 2018, its value was of £1945000. So in comparative manner,

company's performance is poor in year 2019.

Liquidity ratio- This is a type of ratio which is calculated in order to evaluate liquidity

position of companies in terms of paying short term debts (Nicolăescu, 2013). It consists

two types of ratios such as:

(I) Current ratio = Current assets / current liabilities

All data in £000 except

current ratio

2018 2019

Current assets 3790 4130

Current liabilities 2555 3310

Calculation 3790/2555 4130/3310

Current ratio 1.48 times 1.25 times

Current ratio (in times)

1.1

1.15

1.2

1.25

1.3

1.35

1.4

1.45

1.5 1.48

1.25 2018

2019

Analysis- On the basis of above presented graph, it can be find out that company's current ratio is

not in ideal condition. This is so because the ideal current ratio is 2:1 and their ratio is below it.

Like in year 2018, the current ratio was of 1.48 times which reduced in next year and became of

1.25 times. This is so because company's current assets are increasing with lower percentage but

current liabilities are increasing with huge margin in year 2019.

(ii) Quick ratio = Quick assets / current liabilities

All data in £000 except quick

ratio

2018 2019

Quick assets 2790 2650

Current liabilities 2555 3310

Calculation 2790/2555 2650/3310

Quick ratio 1.09 times 0.80 times

Current liabilities 2555 3310

Calculation 3790/2555 4130/3310

Current ratio 1.48 times 1.25 times

Current ratio (in times)

1.1

1.15

1.2

1.25

1.3

1.35

1.4

1.45

1.5 1.48

1.25 2018

2019

Analysis- On the basis of above presented graph, it can be find out that company's current ratio is

not in ideal condition. This is so because the ideal current ratio is 2:1 and their ratio is below it.

Like in year 2018, the current ratio was of 1.48 times which reduced in next year and became of

1.25 times. This is so because company's current assets are increasing with lower percentage but

current liabilities are increasing with huge margin in year 2019.

(ii) Quick ratio = Quick assets / current liabilities

All data in £000 except quick

ratio

2018 2019

Quick assets 2790 2650

Current liabilities 2555 3310

Calculation 2790/2555 2650/3310

Quick ratio 1.09 times 0.80 times

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Quick ratio (in times)

0

0.2

0.4

0.6

0.8

1

1.2 1.09

0.8

2018

2019

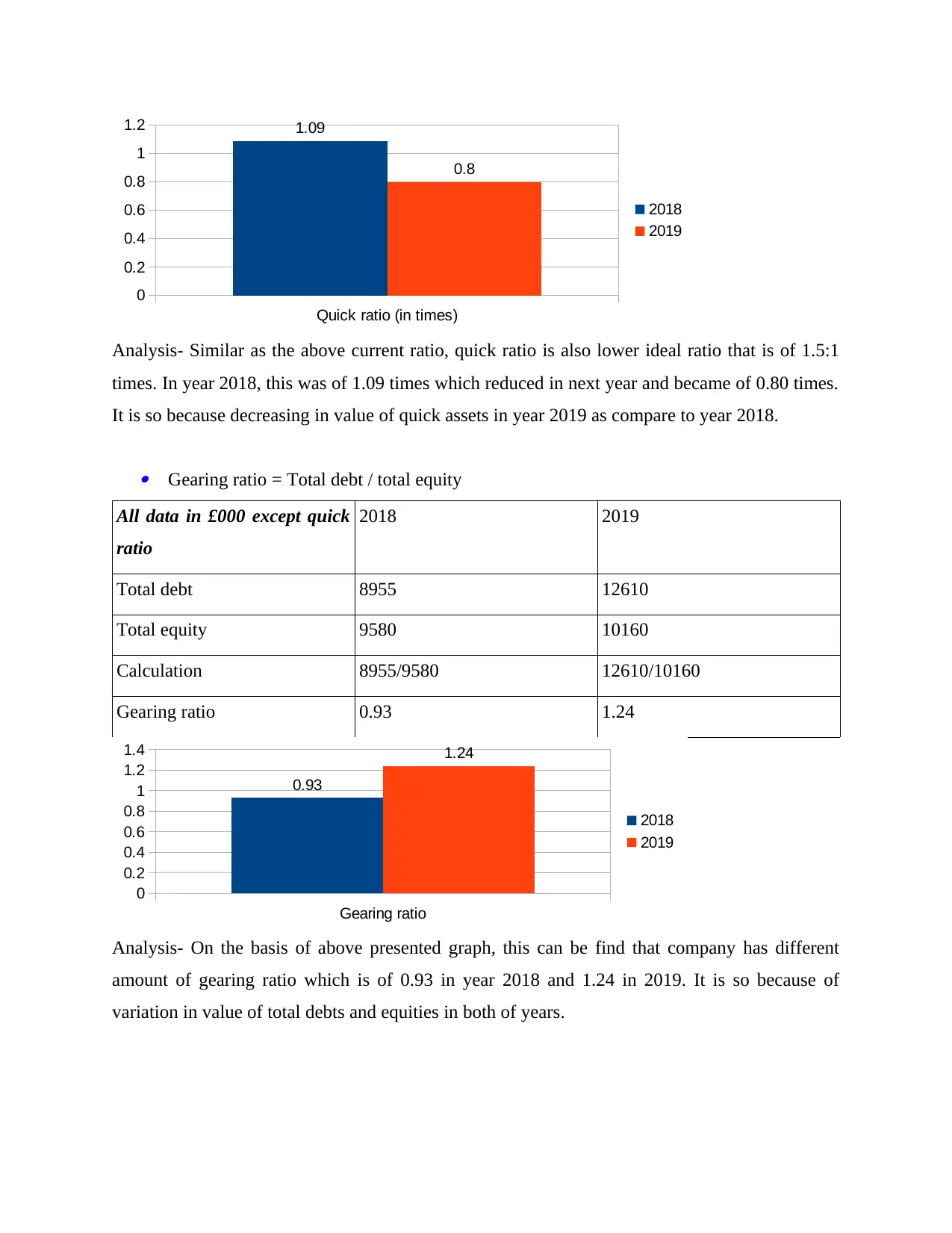

Analysis- Similar as the above current ratio, quick ratio is also lower ideal ratio that is of 1.5:1

times. In year 2018, this was of 1.09 times which reduced in next year and became of 0.80 times.

It is so because decreasing in value of quick assets in year 2019 as compare to year 2018.

Gearing ratio = Total debt / total equity

All data in £000 except quick

ratio

2018 2019

Total debt 8955 12610

Total equity 9580 10160

Calculation 8955/9580 12610/10160

Gearing ratio 0.93 1.24

Gearing ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

0.93

1.24

2018

2019

Analysis- On the basis of above presented graph, this can be find that company has different

amount of gearing ratio which is of 0.93 in year 2018 and 1.24 in 2019. It is so because of

variation in value of total debts and equities in both of years.

0

0.2

0.4

0.6

0.8

1

1.2 1.09

0.8

2018

2019

Analysis- Similar as the above current ratio, quick ratio is also lower ideal ratio that is of 1.5:1

times. In year 2018, this was of 1.09 times which reduced in next year and became of 0.80 times.

It is so because decreasing in value of quick assets in year 2019 as compare to year 2018.

Gearing ratio = Total debt / total equity

All data in £000 except quick

ratio

2018 2019

Total debt 8955 12610

Total equity 9580 10160

Calculation 8955/9580 12610/10160

Gearing ratio 0.93 1.24

Gearing ratio

0

0.2

0.4

0.6

0.8

1

1.2

1.4

0.93

1.24

2018

2019

Analysis- On the basis of above presented graph, this can be find that company has different

amount of gearing ratio which is of 0.93 in year 2018 and 1.24 in 2019. It is so because of

variation in value of total debts and equities in both of years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

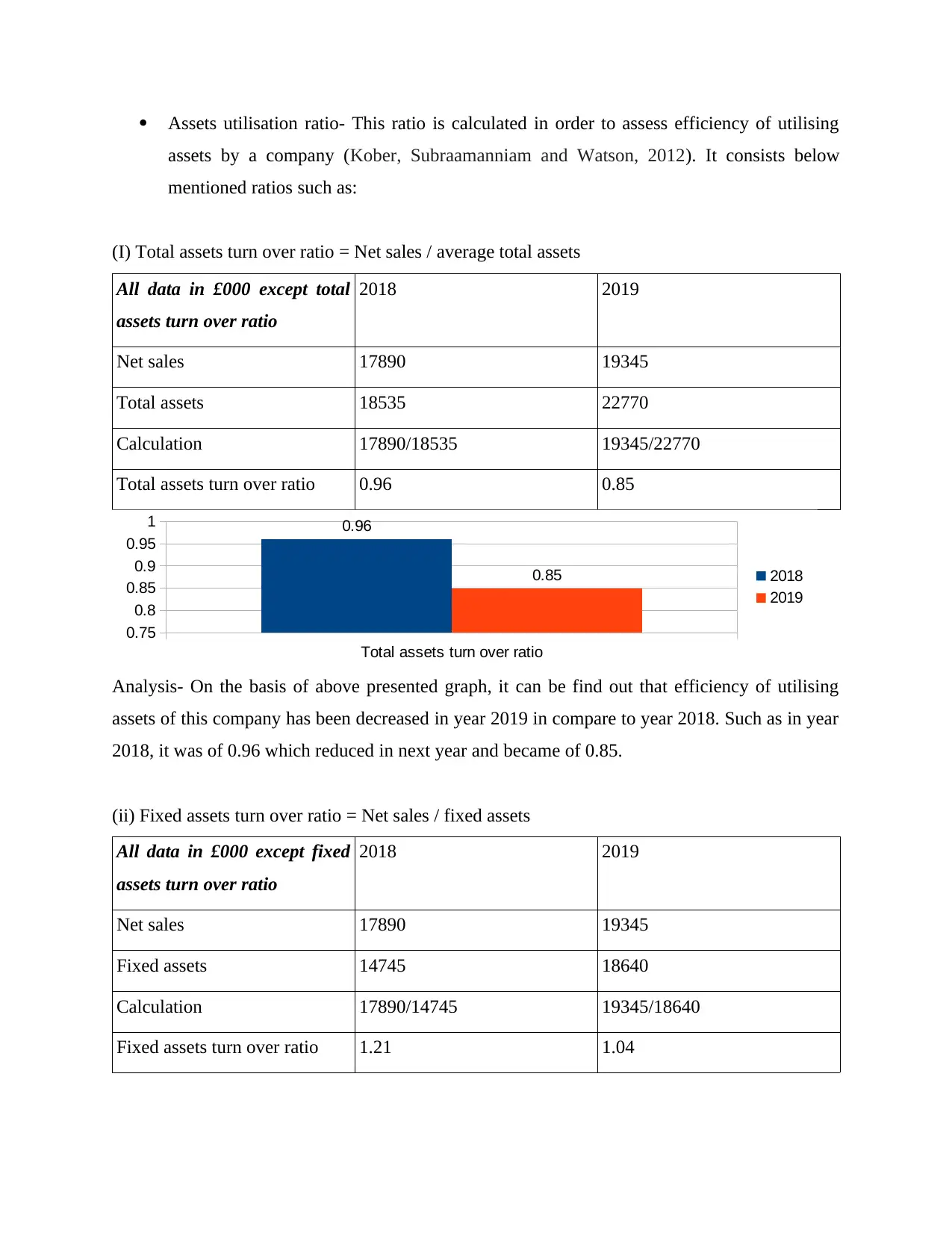

Assets utilisation ratio- This ratio is calculated in order to assess efficiency of utilising

assets by a company (Kober, Subraamanniam and Watson, 2012). It consists below

mentioned ratios such as:

(I) Total assets turn over ratio = Net sales / average total assets

All data in £000 except total

assets turn over ratio

2018 2019

Net sales 17890 19345

Total assets 18535 22770

Calculation 17890/18535 19345/22770

Total assets turn over ratio 0.96 0.85

Total assets turn over ratio

0.75

0.8

0.85

0.9

0.95

1 0.96

0.85 2018

2019

Analysis- On the basis of above presented graph, it can be find out that efficiency of utilising

assets of this company has been decreased in year 2019 in compare to year 2018. Such as in year

2018, it was of 0.96 which reduced in next year and became of 0.85.

(ii) Fixed assets turn over ratio = Net sales / fixed assets

All data in £000 except fixed

assets turn over ratio

2018 2019

Net sales 17890 19345

Fixed assets 14745 18640

Calculation 17890/14745 19345/18640

Fixed assets turn over ratio 1.21 1.04

assets by a company (Kober, Subraamanniam and Watson, 2012). It consists below

mentioned ratios such as:

(I) Total assets turn over ratio = Net sales / average total assets

All data in £000 except total

assets turn over ratio

2018 2019

Net sales 17890 19345

Total assets 18535 22770

Calculation 17890/18535 19345/22770

Total assets turn over ratio 0.96 0.85

Total assets turn over ratio

0.75

0.8

0.85

0.9

0.95

1 0.96

0.85 2018

2019

Analysis- On the basis of above presented graph, it can be find out that efficiency of utilising

assets of this company has been decreased in year 2019 in compare to year 2018. Such as in year

2018, it was of 0.96 which reduced in next year and became of 0.85.

(ii) Fixed assets turn over ratio = Net sales / fixed assets

All data in £000 except fixed

assets turn over ratio

2018 2019

Net sales 17890 19345

Fixed assets 14745 18640

Calculation 17890/14745 19345/18640

Fixed assets turn over ratio 1.21 1.04

Fixed assets turn over ratio

0.95

1

1.05

1.1

1.15

1.2

1.25 1.21

1.04 2018

2019

Analysis- On the basis of above presented graph, it can be find out that efficiency of utilising

fixed assets of this company has been decreased in year 2019 in compare to year 2018. Such as

in year 2018, it was of 1.21 which reduced in next year and became of 1.04.

Investor potential ratios- This is a type of ratio which is used by investors in order to

assess the efficiency of companies and to take investment decisions (Bodnar, Consolandi

and Jaiswal‐Dale, 2013). There are different types of ratios such as:

(I) Return on assets – Net income / total assets

All data in £000 except return

on assets ratio

2018 2019

Net income 1945 580

Total assets 18535 22770

Calculation 1945/18535 580/22770

Return on assets 0.1 0.02

Total assets turn over ratio

0

0.02

0.04

0.06

0.08

0.1

0.12 0.1

0.02

2018

2019

0.95

1

1.05

1.1

1.15

1.2

1.25 1.21

1.04 2018

2019

Analysis- On the basis of above presented graph, it can be find out that efficiency of utilising

fixed assets of this company has been decreased in year 2019 in compare to year 2018. Such as

in year 2018, it was of 1.21 which reduced in next year and became of 1.04.

Investor potential ratios- This is a type of ratio which is used by investors in order to

assess the efficiency of companies and to take investment decisions (Bodnar, Consolandi

and Jaiswal‐Dale, 2013). There are different types of ratios such as:

(I) Return on assets – Net income / total assets

All data in £000 except return

on assets ratio

2018 2019

Net income 1945 580

Total assets 18535 22770

Calculation 1945/18535 580/22770

Return on assets 0.1 0.02

Total assets turn over ratio

0

0.02

0.04

0.06

0.08

0.1

0.12 0.1

0.02

2018

2019

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

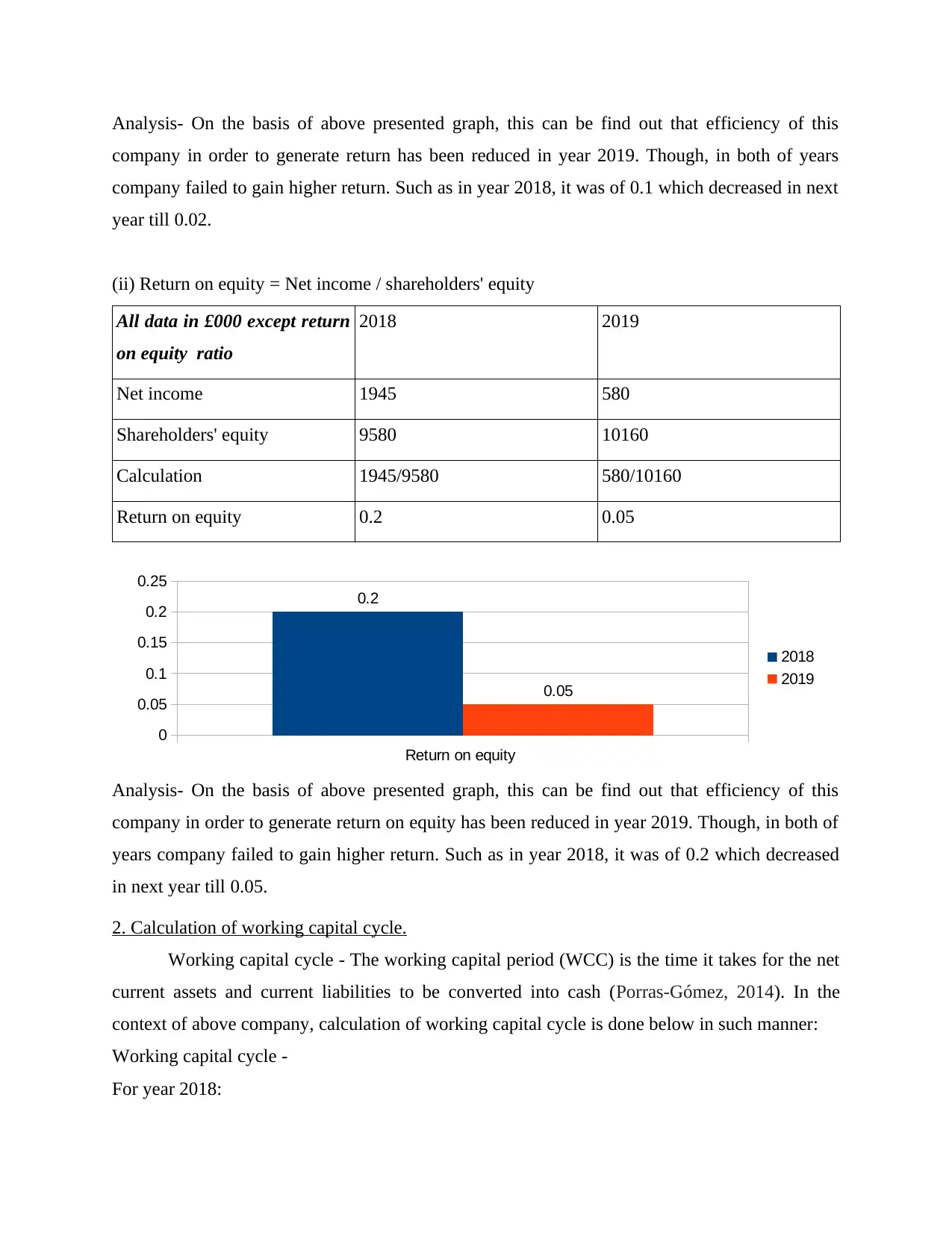

Analysis- On the basis of above presented graph, this can be find out that efficiency of this

company in order to generate return has been reduced in year 2019. Though, in both of years

company failed to gain higher return. Such as in year 2018, it was of 0.1 which decreased in next

year till 0.02.

(ii) Return on equity = Net income / shareholders' equity

All data in £000 except return

on equity ratio

2018 2019

Net income 1945 580

Shareholders' equity 9580 10160

Calculation 1945/9580 580/10160

Return on equity 0.2 0.05

Analysis- On the basis of above presented graph, this can be find out that efficiency of this

company in order to generate return on equity has been reduced in year 2019. Though, in both of

years company failed to gain higher return. Such as in year 2018, it was of 0.2 which decreased

in next year till 0.05.

2. Calculation of working capital cycle.

Working capital cycle - The working capital period (WCC) is the time it takes for the net

current assets and current liabilities to be converted into cash (Porras-Gómez, 2014). In the

context of above company, calculation of working capital cycle is done below in such manner:

Working capital cycle -

For year 2018:

Return on equity

0

0.05

0.1

0.15

0.2

0.25

0.2

0.05

2018

2019

company in order to generate return has been reduced in year 2019. Though, in both of years

company failed to gain higher return. Such as in year 2018, it was of 0.1 which decreased in next

year till 0.02.

(ii) Return on equity = Net income / shareholders' equity

All data in £000 except return

on equity ratio

2018 2019

Net income 1945 580

Shareholders' equity 9580 10160

Calculation 1945/9580 580/10160

Return on equity 0.2 0.05

Analysis- On the basis of above presented graph, this can be find out that efficiency of this

company in order to generate return on equity has been reduced in year 2019. Though, in both of

years company failed to gain higher return. Such as in year 2018, it was of 0.2 which decreased

in next year till 0.05.

2. Calculation of working capital cycle.

Working capital cycle - The working capital period (WCC) is the time it takes for the net

current assets and current liabilities to be converted into cash (Porras-Gómez, 2014). In the

context of above company, calculation of working capital cycle is done below in such manner:

Working capital cycle -

For year 2018:

Return on equity

0

0.05

0.1

0.15

0.2

0.25

0.2

0.05

2018

2019

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

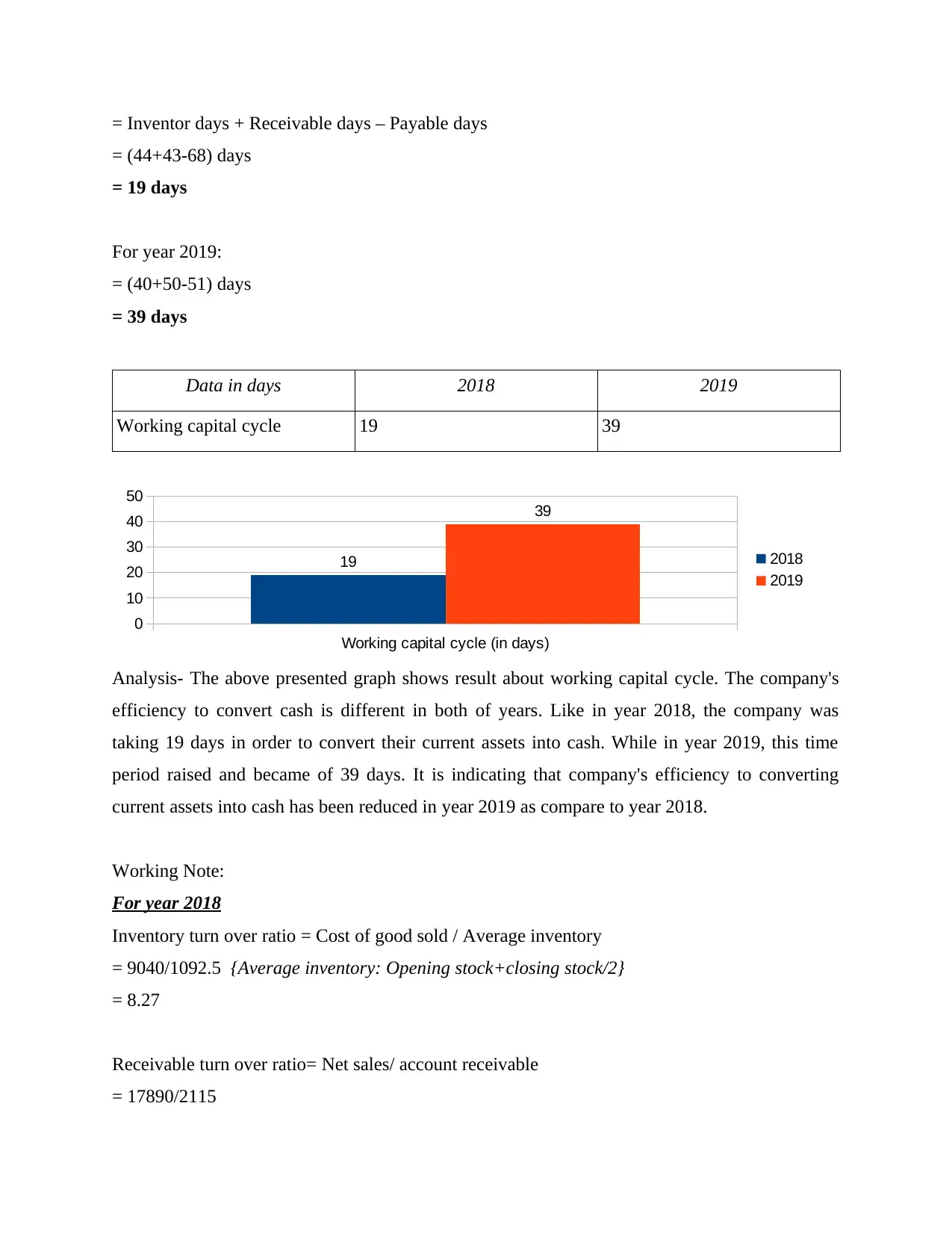

= Inventor days + Receivable days – Payable days

= (44+43-68) days

= 19 days

For year 2019:

= (40+50-51) days

= 39 days

Data in days 2018 2019

Working capital cycle 19 39

Working capital cycle (in days)

0

10

20

30

40

50

19

39

2018

2019

Analysis- The above presented graph shows result about working capital cycle. The company's

efficiency to convert cash is different in both of years. Like in year 2018, the company was

taking 19 days in order to convert their current assets into cash. While in year 2019, this time

period raised and became of 39 days. It is indicating that company's efficiency to converting

current assets into cash has been reduced in year 2019 as compare to year 2018.

Working Note:

For year 2018

Inventory turn over ratio = Cost of good sold / Average inventory

= 9040/1092.5 {Average inventory: Opening stock+closing stock/2}

= 8.27

Receivable turn over ratio= Net sales/ account receivable

= 17890/2115

= (44+43-68) days

= 19 days

For year 2019:

= (40+50-51) days

= 39 days

Data in days 2018 2019

Working capital cycle 19 39

Working capital cycle (in days)

0

10

20

30

40

50

19

39

2018

2019

Analysis- The above presented graph shows result about working capital cycle. The company's

efficiency to convert cash is different in both of years. Like in year 2018, the company was

taking 19 days in order to convert their current assets into cash. While in year 2019, this time

period raised and became of 39 days. It is indicating that company's efficiency to converting

current assets into cash has been reduced in year 2019 as compare to year 2018.

Working Note:

For year 2018

Inventory turn over ratio = Cost of good sold / Average inventory

= 9040/1092.5 {Average inventory: Opening stock+closing stock/2}

= 8.27

Receivable turn over ratio= Net sales/ account receivable

= 17890/2115

= 8.45

Payable turn over ratio = Total purchase/ accounts payables

= 8855/ 1655 {total purchase: cost of goods sold+closing stock-opening stock}

= 5.35

Inventory days = 365 days / Inventory turn over ratio

= 365 / 8.27

= 44.13 or 44 days

Receivable days = 365 days / receivable turn over ratio

= 365/8.45

= 43.19 or 43 days

Payable days = 365 days/ payable turn over ratio

= 365/5.35

= 68.22 or 68 days

For year 2019

Inventory turn over ratio = Cost of good sold / Average inventory

= 11340/1240 {Average inventory: Opening stock+closing stock/2}

= 9.14

Receivable turn over ratio= Net sales/ account receivable

= 19345/2650

= 7.3

Payable turn over ratio = Total purchase/ accounts payables

= 11820/ 1655 {total purchase: cost of goods sold+closing stock-opening stock}

= 7.14

Inventory days = 365 days / Inventory turn over ratio

= 365 / 9.14

Payable turn over ratio = Total purchase/ accounts payables

= 8855/ 1655 {total purchase: cost of goods sold+closing stock-opening stock}

= 5.35

Inventory days = 365 days / Inventory turn over ratio

= 365 / 8.27

= 44.13 or 44 days

Receivable days = 365 days / receivable turn over ratio

= 365/8.45

= 43.19 or 43 days

Payable days = 365 days/ payable turn over ratio

= 365/5.35

= 68.22 or 68 days

For year 2019

Inventory turn over ratio = Cost of good sold / Average inventory

= 11340/1240 {Average inventory: Opening stock+closing stock/2}

= 9.14

Receivable turn over ratio= Net sales/ account receivable

= 19345/2650

= 7.3

Payable turn over ratio = Total purchase/ accounts payables

= 11820/ 1655 {total purchase: cost of goods sold+closing stock-opening stock}

= 7.14

Inventory days = 365 days / Inventory turn over ratio

= 365 / 9.14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.