Financial and Management Accounting Analysis Report - University

VerifiedAdded on 2023/06/04

|8

|2232

|398

Report

AI Summary

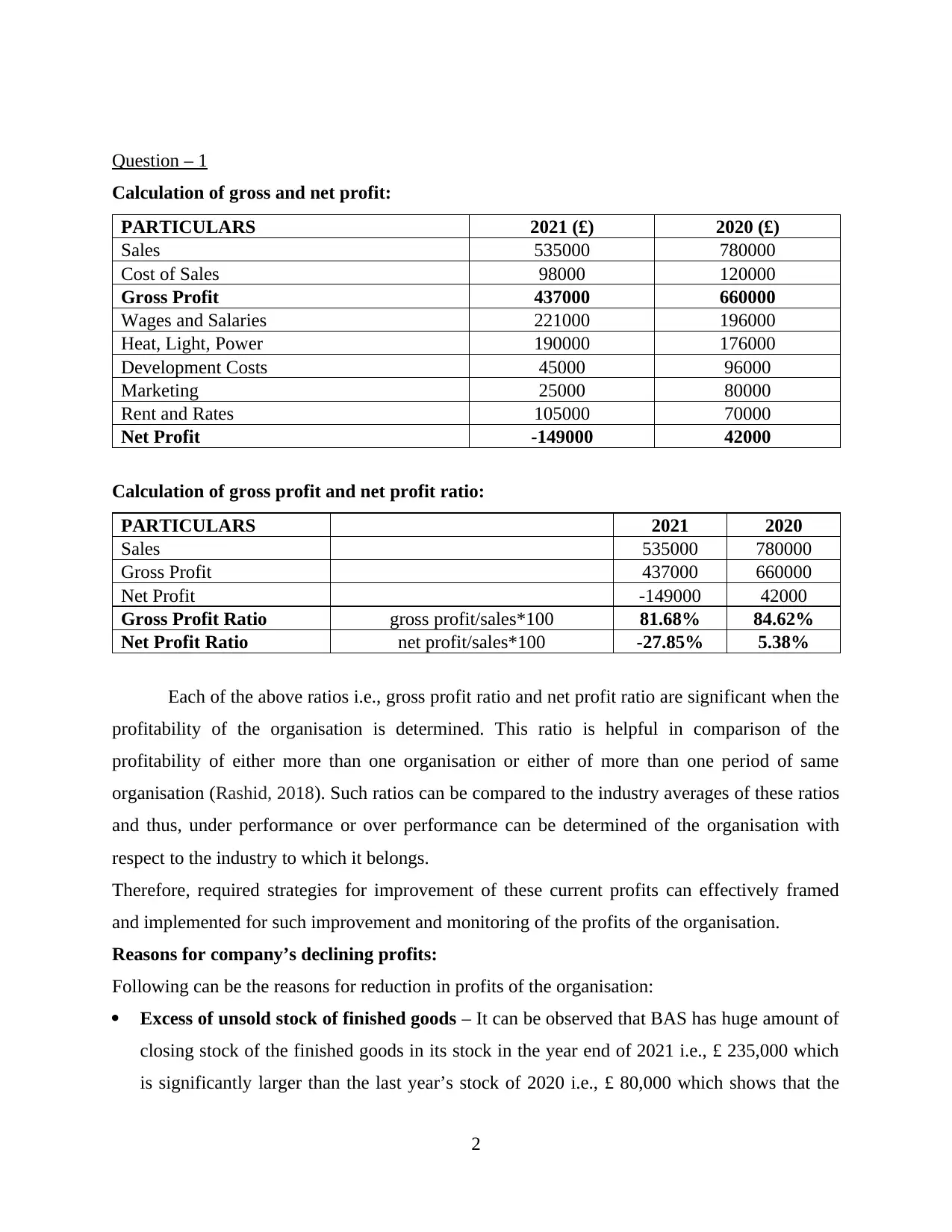

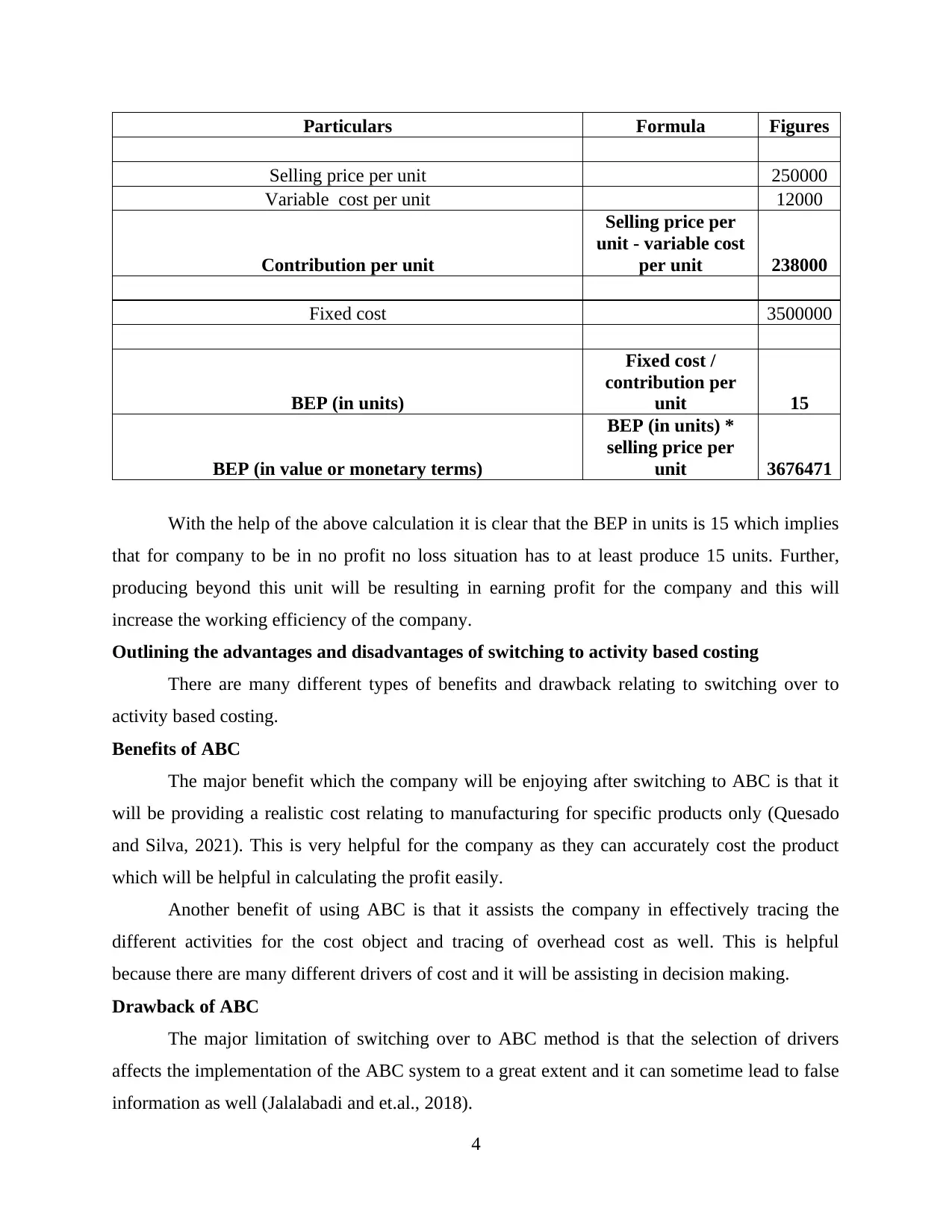

This report provides a comprehensive analysis of financial and management accounting principles. It begins with the calculation of gross and net profit, including the computation of relevant ratios to assess the profitability of a business. The report then identifies the reasons for declining profits, such as excess inventory, delayed payments from debtors, and inefficient rent expenses. Strategies to improve the financial position are proposed, including better debt collection control, updated marketing techniques, and offering discounts. Furthermore, the report delves into break-even analysis, outlining the advantages and disadvantages of activity-based costing. Finally, it examines variance analysis, identifying significant variances in direct power costs, indirect administration costs, and premises costs, along with their potential causes. The report concludes with strategies to correct these variances, such as implementing zero-based budgeting, and discusses its advantages and disadvantages. References to relevant academic sources are provided throughout the report.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.