Financial Resources Management: Investment Appraisal Methods

VerifiedAdded on 2023/06/10

|17

|2862

|56

Report

AI Summary

This report provides a detailed analysis of managing financial resources, covering various aspects such as break-even point calculations, margin of safety, and target profit analysis. It delves into the limitations of cost volume profit analysis and explores different investment appraisal methods, including payback period, accounting rate of return, net present value, and internal rate of return. The report includes calculations, comments on each calculation, and an evaluation of the benefits and limitations of each investment appraisal method. It also examines the cost of capital, efficient market hypothesis, and present value of cash flows, providing a comprehensive overview of financial resource management and investment decision-making. Access this and more solved assignments on Desklib, your go-to platform for study resources.

Managing Financial

Resources

Resources

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

PART 1............................................................................................................................................4

1...................................................................................................................................................4

2...................................................................................................................................................4

3...................................................................................................................................................4

4...................................................................................................................................................4

5...................................................................................................................................................4

6...................................................................................................................................................4

7...................................................................................................................................................4

8...................................................................................................................................................4

Q9................................................................................................................................................4

Q10..............................................................................................................................................5

Q11..............................................................................................................................................5

Q12..............................................................................................................................................5

Q13..............................................................................................................................................5

Q.14.............................................................................................................................................5

Q.15.............................................................................................................................................6

Q.16.............................................................................................................................................6

Q.17.............................................................................................................................................6

Q.18.............................................................................................................................................6

Q.19.............................................................................................................................................7

Q.20.............................................................................................................................................7

Q.21.............................................................................................................................................7

Q.22.............................................................................................................................................7

Q.23.............................................................................................................................................7

Q.24.............................................................................................................................................8

Q.25.............................................................................................................................................8

PART 2............................................................................................................................................8

Question 2........................................................................................................................................8

1...................................................................................................................................................8

PART 1............................................................................................................................................4

1...................................................................................................................................................4

2...................................................................................................................................................4

3...................................................................................................................................................4

4...................................................................................................................................................4

5...................................................................................................................................................4

6...................................................................................................................................................4

7...................................................................................................................................................4

8...................................................................................................................................................4

Q9................................................................................................................................................4

Q10..............................................................................................................................................5

Q11..............................................................................................................................................5

Q12..............................................................................................................................................5

Q13..............................................................................................................................................5

Q.14.............................................................................................................................................5

Q.15.............................................................................................................................................6

Q.16.............................................................................................................................................6

Q.17.............................................................................................................................................6

Q.18.............................................................................................................................................6

Q.19.............................................................................................................................................7

Q.20.............................................................................................................................................7

Q.21.............................................................................................................................................7

Q.22.............................................................................................................................................7

Q.23.............................................................................................................................................7

Q.24.............................................................................................................................................8

Q.25.............................................................................................................................................8

PART 2............................................................................................................................................8

Question 2........................................................................................................................................8

1...................................................................................................................................................8

(a) Calculation of Break-even point in revenue (£) and in quantity (in units)............................8

(b) Calculation of margin of safety..............................................................................................9

(C) Calculation of units of vehicles to be sold for a target profit of £200000...........................10

2.................................................................................................................................................11

Limitation of Cost Volume Profit Analysis...............................................................................11

QUESTION 3................................................................................................................................11

Payback period...........................................................................................................................12

Accounting rate of return...........................................................................................................12

Net present value.......................................................................................................................13

Internal rate of return.................................................................................................................14

Providing the comment on each calculation..............................................................................14

Evaluating benefits and limitations of using each of the investment appraisal methods..........15

REFERENCES................................................................................................................................1

(b) Calculation of margin of safety..............................................................................................9

(C) Calculation of units of vehicles to be sold for a target profit of £200000...........................10

2.................................................................................................................................................11

Limitation of Cost Volume Profit Analysis...............................................................................11

QUESTION 3................................................................................................................................11

Payback period...........................................................................................................................12

Accounting rate of return...........................................................................................................12

Net present value.......................................................................................................................13

Internal rate of return.................................................................................................................14

Providing the comment on each calculation..............................................................................14

Evaluating benefits and limitations of using each of the investment appraisal methods..........15

REFERENCES................................................................................................................................1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

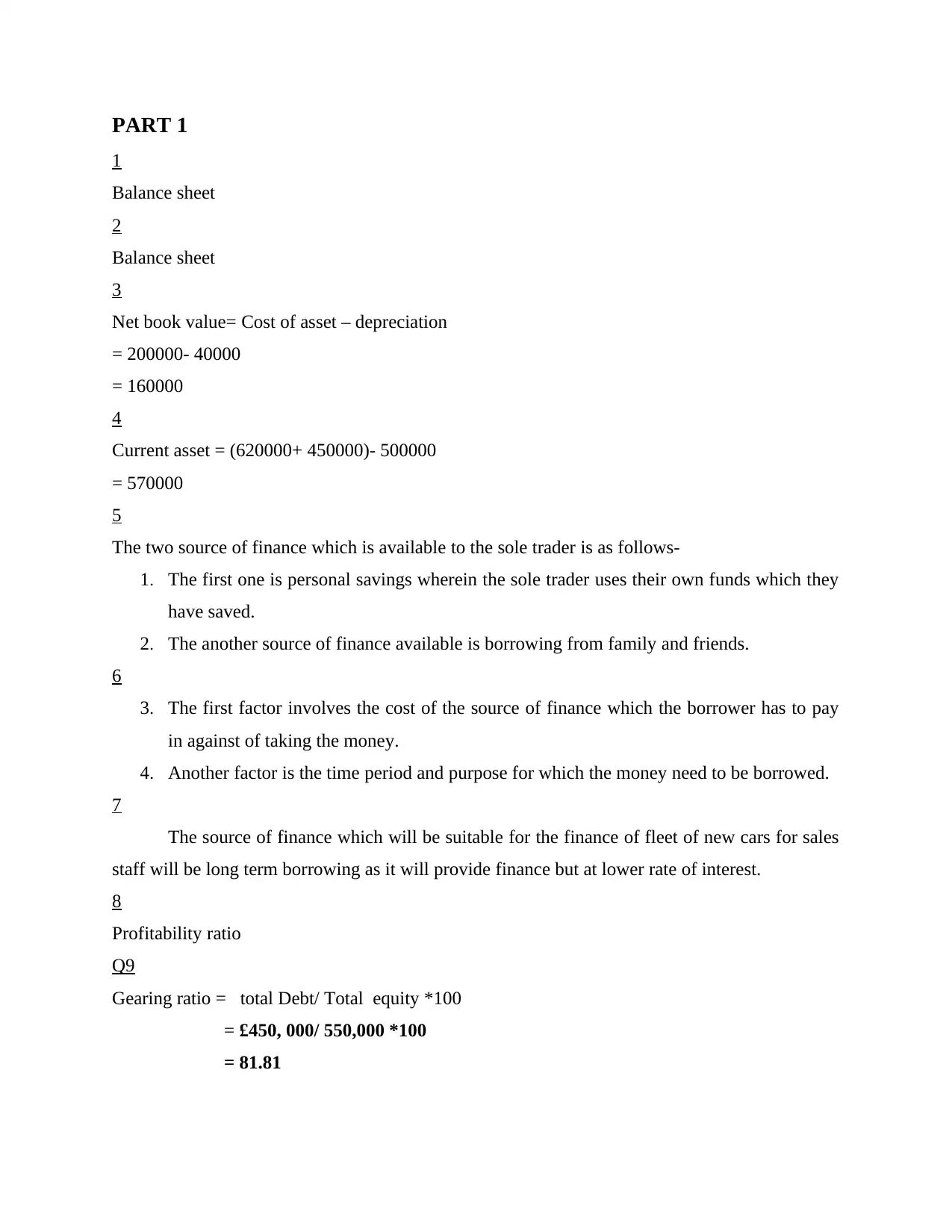

PART 1

1

Balance sheet

2

Balance sheet

3

Net book value= Cost of asset – depreciation

= 200000- 40000

= 160000

4

Current asset = (620000+ 450000)- 500000

= 570000

5

The two source of finance which is available to the sole trader is as follows-

1. The first one is personal savings wherein the sole trader uses their own funds which they

have saved.

2. The another source of finance available is borrowing from family and friends.

6

3. The first factor involves the cost of the source of finance which the borrower has to pay

in against of taking the money.

4. Another factor is the time period and purpose for which the money need to be borrowed.

7

The source of finance which will be suitable for the finance of fleet of new cars for sales

staff will be long term borrowing as it will provide finance but at lower rate of interest.

8

Profitability ratio

Q9

Gearing ratio = total Debt/ Total equity *100

= £450, 000/ 550,000 *100

= 81.81

1

Balance sheet

2

Balance sheet

3

Net book value= Cost of asset – depreciation

= 200000- 40000

= 160000

4

Current asset = (620000+ 450000)- 500000

= 570000

5

The two source of finance which is available to the sole trader is as follows-

1. The first one is personal savings wherein the sole trader uses their own funds which they

have saved.

2. The another source of finance available is borrowing from family and friends.

6

3. The first factor involves the cost of the source of finance which the borrower has to pay

in against of taking the money.

4. Another factor is the time period and purpose for which the money need to be borrowed.

7

The source of finance which will be suitable for the finance of fleet of new cars for sales

staff will be long term borrowing as it will provide finance but at lower rate of interest.

8

Profitability ratio

Q9

Gearing ratio = total Debt/ Total equity *100

= £450, 000/ 550,000 *100

= 81.81

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

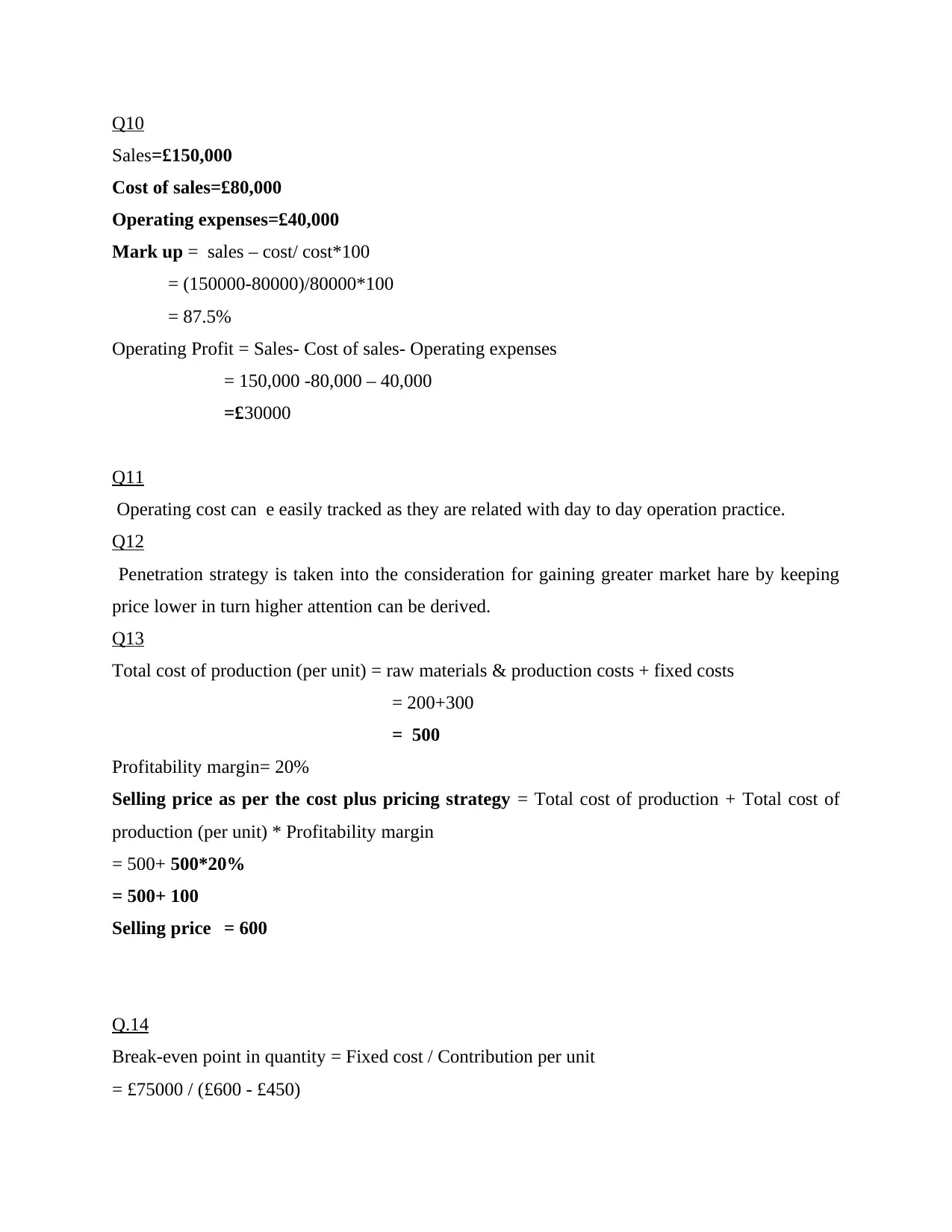

Q10

Sales=£150,000

Cost of sales=£80,000

Operating expenses=£40,000

Mark up = sales – cost/ cost*100

= (150000-80000)/80000*100

= 87.5%

Operating Profit = Sales- Cost of sales- Operating expenses

= 150,000 -80,000 – 40,000

=£30000

Q11

Operating cost can e easily tracked as they are related with day to day operation practice.

Q12

Penetration strategy is taken into the consideration for gaining greater market hare by keeping

price lower in turn higher attention can be derived.

Q13

Total cost of production (per unit) = raw materials & production costs + fixed costs

= 200+300

= 500

Profitability margin= 20%

Selling price as per the cost plus pricing strategy = Total cost of production + Total cost of

production (per unit) * Profitability margin

= 500+ 500*20%

= 500+ 100

Selling price = 600

Q.14

Break-even point in quantity = Fixed cost / Contribution per unit

= £75000 / (£600 - £450)

Sales=£150,000

Cost of sales=£80,000

Operating expenses=£40,000

Mark up = sales – cost/ cost*100

= (150000-80000)/80000*100

= 87.5%

Operating Profit = Sales- Cost of sales- Operating expenses

= 150,000 -80,000 – 40,000

=£30000

Q11

Operating cost can e easily tracked as they are related with day to day operation practice.

Q12

Penetration strategy is taken into the consideration for gaining greater market hare by keeping

price lower in turn higher attention can be derived.

Q13

Total cost of production (per unit) = raw materials & production costs + fixed costs

= 200+300

= 500

Profitability margin= 20%

Selling price as per the cost plus pricing strategy = Total cost of production + Total cost of

production (per unit) * Profitability margin

= 500+ 500*20%

= 500+ 100

Selling price = 600

Q.14

Break-even point in quantity = Fixed cost / Contribution per unit

= £75000 / (£600 - £450)

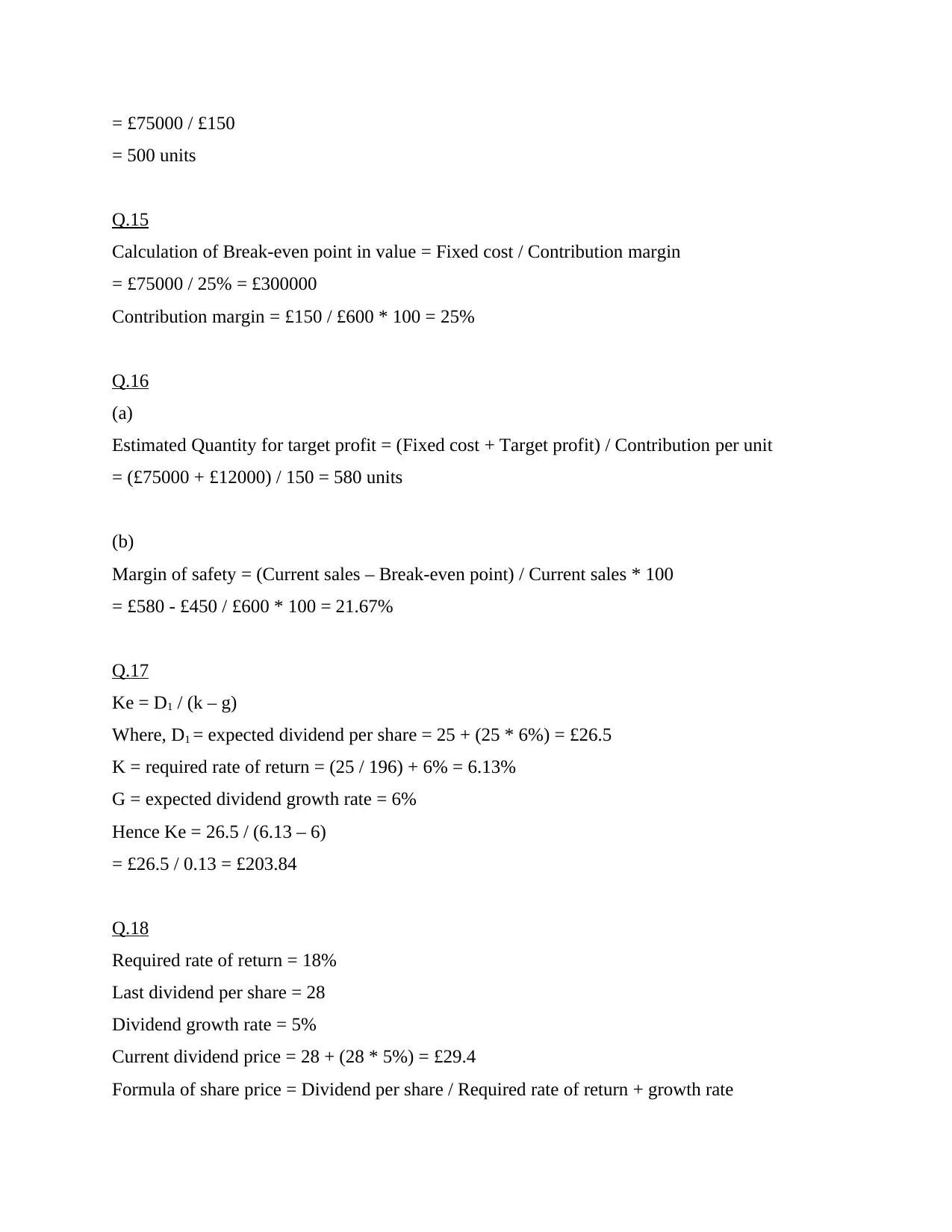

= £75000 / £150

= 500 units

Q.15

Calculation of Break-even point in value = Fixed cost / Contribution margin

= £75000 / 25% = £300000

Contribution margin = £150 / £600 * 100 = 25%

Q.16

(a)

Estimated Quantity for target profit = (Fixed cost + Target profit) / Contribution per unit

= (£75000 + £12000) / 150 = 580 units

(b)

Margin of safety = (Current sales – Break-even point) / Current sales * 100

= £580 - £450 / £600 * 100 = 21.67%

Q.17

Ke = D1 / (k – g)

Where, D1 = expected dividend per share = 25 + (25 * 6%) = £26.5

K = required rate of return = (25 / 196) + 6% = 6.13%

G = expected dividend growth rate = 6%

Hence Ke = 26.5 / (6.13 – 6)

= £26.5 / 0.13 = £203.84

Q.18

Required rate of return = 18%

Last dividend per share = 28

Dividend growth rate = 5%

Current dividend price = 28 + (28 * 5%) = £29.4

Formula of share price = Dividend per share / Required rate of return + growth rate

= 500 units

Q.15

Calculation of Break-even point in value = Fixed cost / Contribution margin

= £75000 / 25% = £300000

Contribution margin = £150 / £600 * 100 = 25%

Q.16

(a)

Estimated Quantity for target profit = (Fixed cost + Target profit) / Contribution per unit

= (£75000 + £12000) / 150 = 580 units

(b)

Margin of safety = (Current sales – Break-even point) / Current sales * 100

= £580 - £450 / £600 * 100 = 21.67%

Q.17

Ke = D1 / (k – g)

Where, D1 = expected dividend per share = 25 + (25 * 6%) = £26.5

K = required rate of return = (25 / 196) + 6% = 6.13%

G = expected dividend growth rate = 6%

Hence Ke = 26.5 / (6.13 – 6)

= £26.5 / 0.13 = £203.84

Q.18

Required rate of return = 18%

Last dividend per share = 28

Dividend growth rate = 5%

Current dividend price = 28 + (28 * 5%) = £29.4

Formula of share price = Dividend per share / Required rate of return + growth rate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

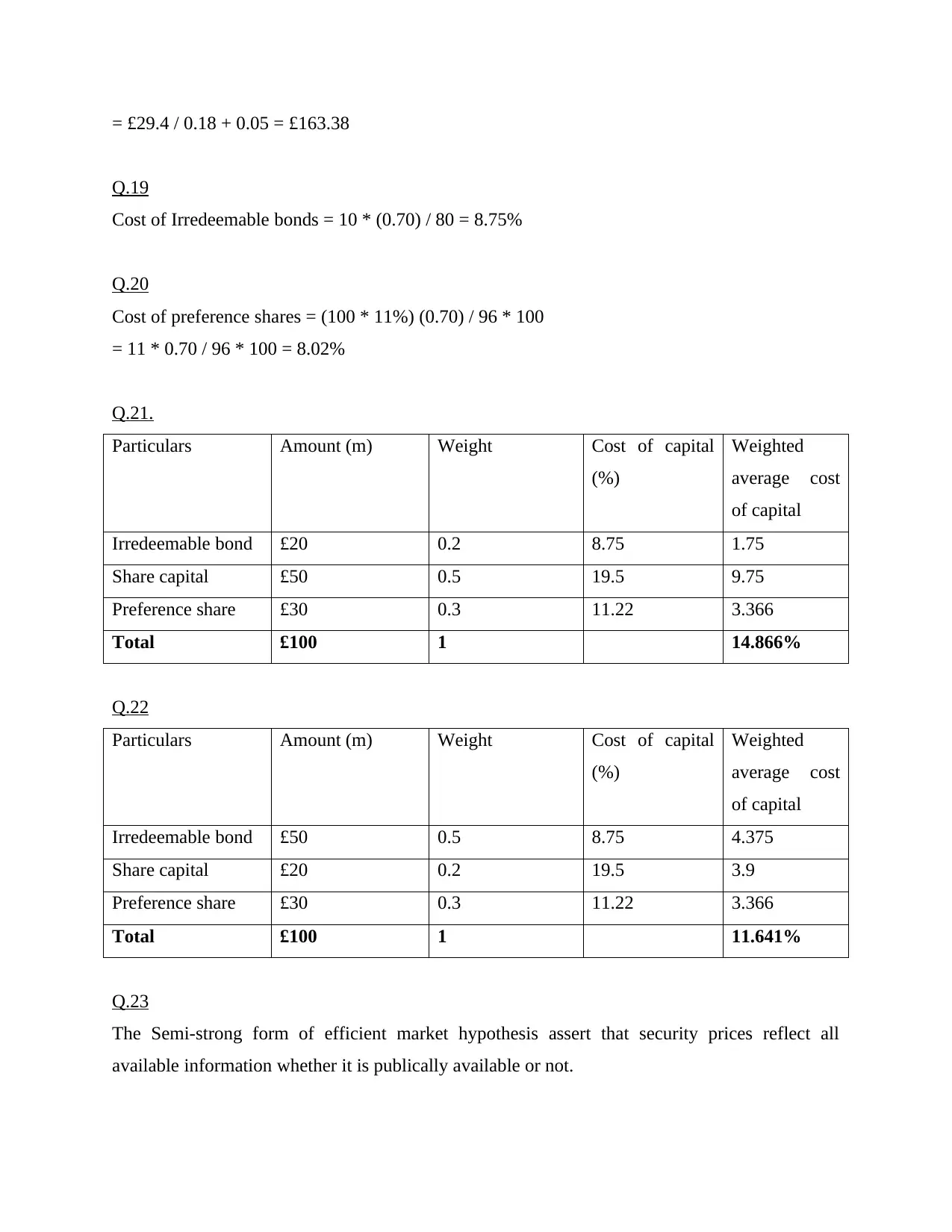

= £29.4 / 0.18 + 0.05 = £163.38

Q.19

Cost of Irredeemable bonds = 10 * (0.70) / 80 = 8.75%

Q.20

Cost of preference shares = (100 * 11%) (0.70) / 96 * 100

= 11 * 0.70 / 96 * 100 = 8.02%

Q.21.

Particulars Amount (m) Weight Cost of capital

(%)

Weighted

average cost

of capital

Irredeemable bond £20 0.2 8.75 1.75

Share capital £50 0.5 19.5 9.75

Preference share £30 0.3 11.22 3.366

Total £100 1 14.866%

Q.22

Particulars Amount (m) Weight Cost of capital

(%)

Weighted

average cost

of capital

Irredeemable bond £50 0.5 8.75 4.375

Share capital £20 0.2 19.5 3.9

Preference share £30 0.3 11.22 3.366

Total £100 1 11.641%

Q.23

The Semi-strong form of efficient market hypothesis assert that security prices reflect all

available information whether it is publically available or not.

Q.19

Cost of Irredeemable bonds = 10 * (0.70) / 80 = 8.75%

Q.20

Cost of preference shares = (100 * 11%) (0.70) / 96 * 100

= 11 * 0.70 / 96 * 100 = 8.02%

Q.21.

Particulars Amount (m) Weight Cost of capital

(%)

Weighted

average cost

of capital

Irredeemable bond £20 0.2 8.75 1.75

Share capital £50 0.5 19.5 9.75

Preference share £30 0.3 11.22 3.366

Total £100 1 14.866%

Q.22

Particulars Amount (m) Weight Cost of capital

(%)

Weighted

average cost

of capital

Irredeemable bond £50 0.5 8.75 4.375

Share capital £20 0.2 19.5 3.9

Preference share £30 0.3 11.22 3.366

Total £100 1 11.641%

Q.23

The Semi-strong form of efficient market hypothesis assert that security prices reflect all

available information whether it is publically available or not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

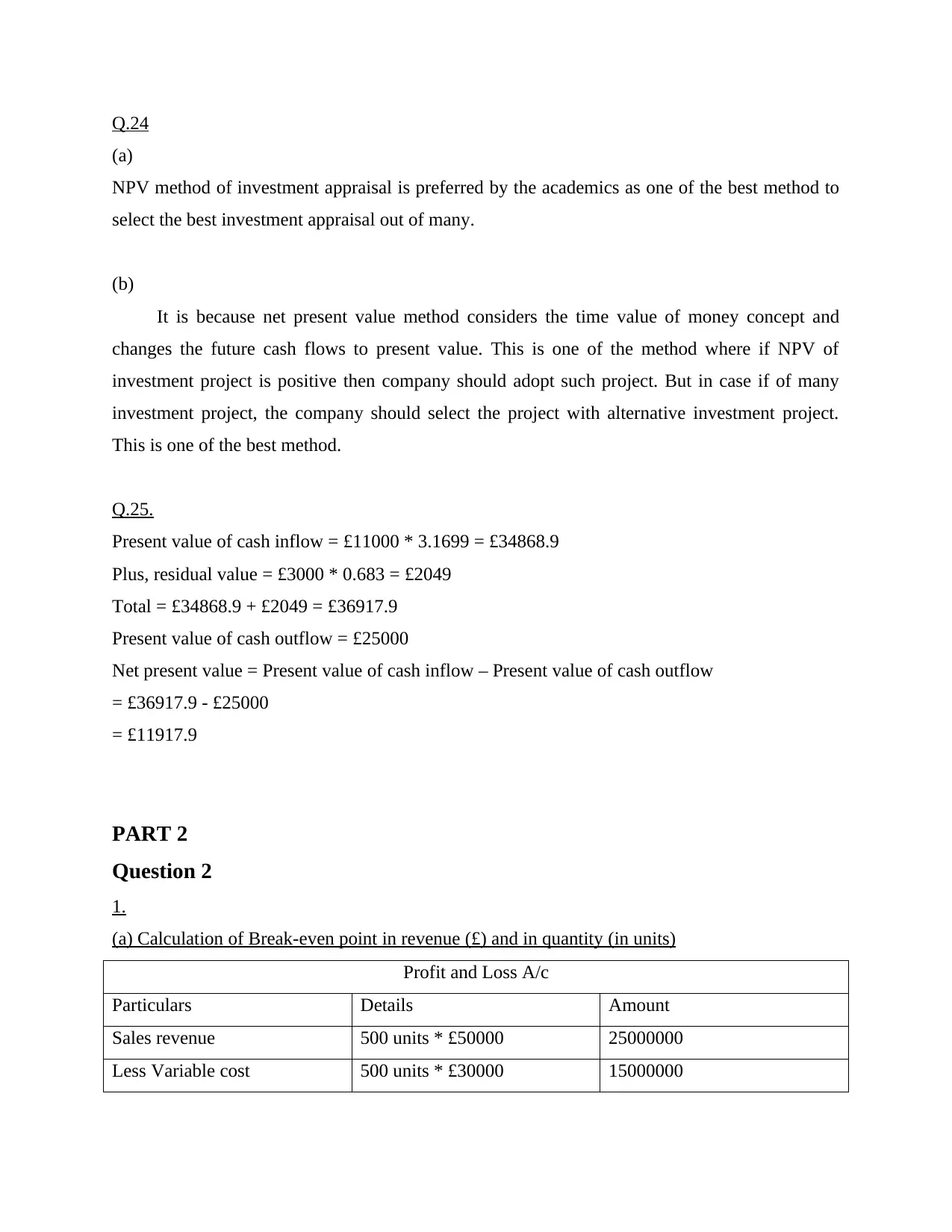

Q.24

(a)

NPV method of investment appraisal is preferred by the academics as one of the best method to

select the best investment appraisal out of many.

(b)

It is because net present value method considers the time value of money concept and

changes the future cash flows to present value. This is one of the method where if NPV of

investment project is positive then company should adopt such project. But in case if of many

investment project, the company should select the project with alternative investment project.

This is one of the best method.

Q.25.

Present value of cash inflow = £11000 * 3.1699 = £34868.9

Plus, residual value = £3000 * 0.683 = £2049

Total = £34868.9 + £2049 = £36917.9

Present value of cash outflow = £25000

Net present value = Present value of cash inflow – Present value of cash outflow

= £36917.9 - £25000

= £11917.9

PART 2

Question 2

1.

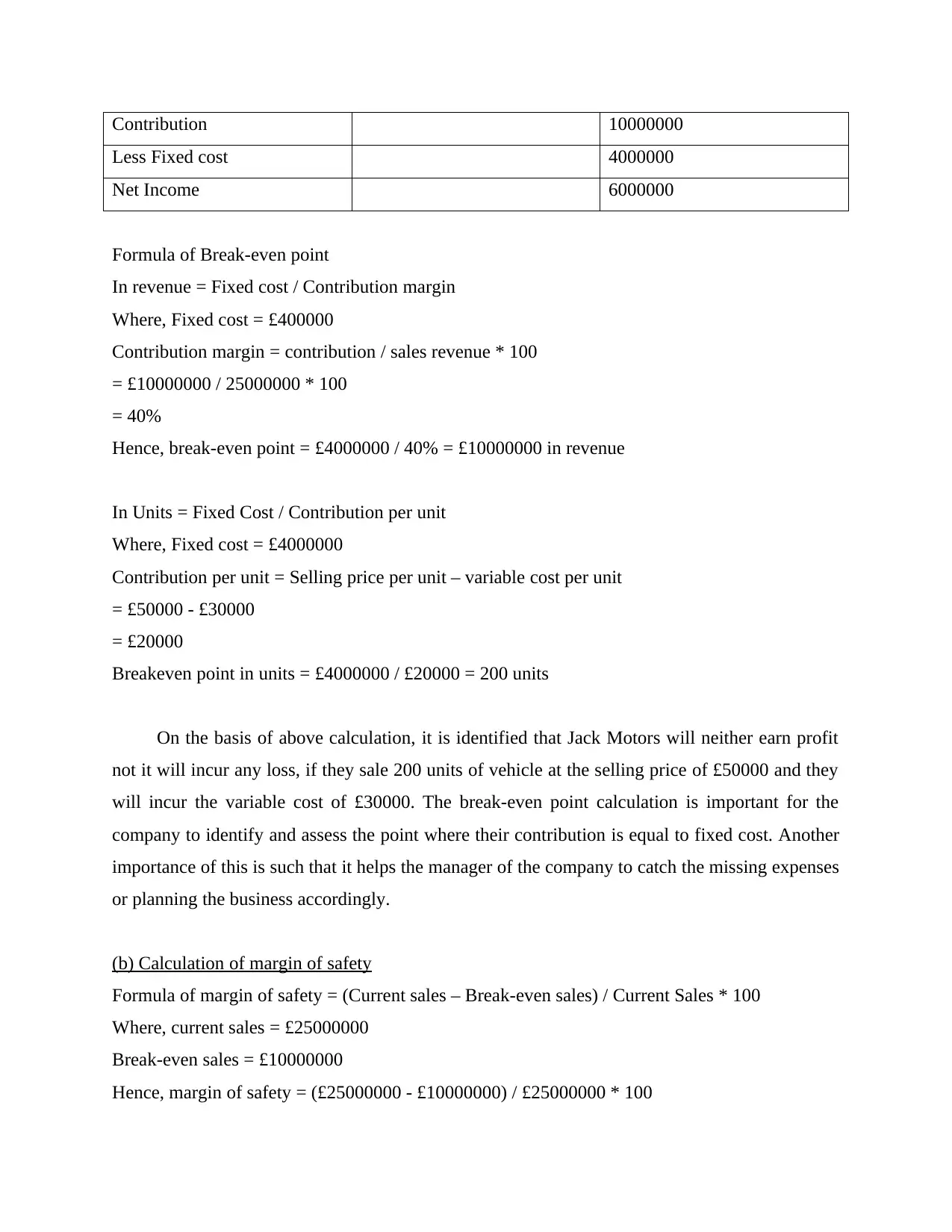

(a) Calculation of Break-even point in revenue (£) and in quantity (in units)

Profit and Loss A/c

Particulars Details Amount

Sales revenue 500 units * £50000 25000000

Less Variable cost 500 units * £30000 15000000

(a)

NPV method of investment appraisal is preferred by the academics as one of the best method to

select the best investment appraisal out of many.

(b)

It is because net present value method considers the time value of money concept and

changes the future cash flows to present value. This is one of the method where if NPV of

investment project is positive then company should adopt such project. But in case if of many

investment project, the company should select the project with alternative investment project.

This is one of the best method.

Q.25.

Present value of cash inflow = £11000 * 3.1699 = £34868.9

Plus, residual value = £3000 * 0.683 = £2049

Total = £34868.9 + £2049 = £36917.9

Present value of cash outflow = £25000

Net present value = Present value of cash inflow – Present value of cash outflow

= £36917.9 - £25000

= £11917.9

PART 2

Question 2

1.

(a) Calculation of Break-even point in revenue (£) and in quantity (in units)

Profit and Loss A/c

Particulars Details Amount

Sales revenue 500 units * £50000 25000000

Less Variable cost 500 units * £30000 15000000

Contribution 10000000

Less Fixed cost 4000000

Net Income 6000000

Formula of Break-even point

In revenue = Fixed cost / Contribution margin

Where, Fixed cost = £400000

Contribution margin = contribution / sales revenue * 100

= £10000000 / 25000000 * 100

= 40%

Hence, break-even point = £4000000 / 40% = £10000000 in revenue

In Units = Fixed Cost / Contribution per unit

Where, Fixed cost = £4000000

Contribution per unit = Selling price per unit – variable cost per unit

= £50000 - £30000

= £20000

Breakeven point in units = £4000000 / £20000 = 200 units

On the basis of above calculation, it is identified that Jack Motors will neither earn profit

not it will incur any loss, if they sale 200 units of vehicle at the selling price of £50000 and they

will incur the variable cost of £30000. The break-even point calculation is important for the

company to identify and assess the point where their contribution is equal to fixed cost. Another

importance of this is such that it helps the manager of the company to catch the missing expenses

or planning the business accordingly.

(b) Calculation of margin of safety

Formula of margin of safety = (Current sales – Break-even sales) / Current Sales * 100

Where, current sales = £25000000

Break-even sales = £10000000

Hence, margin of safety = (£25000000 - £10000000) / £25000000 * 100

Less Fixed cost 4000000

Net Income 6000000

Formula of Break-even point

In revenue = Fixed cost / Contribution margin

Where, Fixed cost = £400000

Contribution margin = contribution / sales revenue * 100

= £10000000 / 25000000 * 100

= 40%

Hence, break-even point = £4000000 / 40% = £10000000 in revenue

In Units = Fixed Cost / Contribution per unit

Where, Fixed cost = £4000000

Contribution per unit = Selling price per unit – variable cost per unit

= £50000 - £30000

= £20000

Breakeven point in units = £4000000 / £20000 = 200 units

On the basis of above calculation, it is identified that Jack Motors will neither earn profit

not it will incur any loss, if they sale 200 units of vehicle at the selling price of £50000 and they

will incur the variable cost of £30000. The break-even point calculation is important for the

company to identify and assess the point where their contribution is equal to fixed cost. Another

importance of this is such that it helps the manager of the company to catch the missing expenses

or planning the business accordingly.

(b) Calculation of margin of safety

Formula of margin of safety = (Current sales – Break-even sales) / Current Sales * 100

Where, current sales = £25000000

Break-even sales = £10000000

Hence, margin of safety = (£25000000 - £10000000) / £25000000 * 100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= 60%

The margin of safety in the break-even analysis is the amount of sales that are above the

break-even sales. On the basis of above calculation, it is identified that Jack Motors margin of

safety is 60%. It means 60% of the sales units or revenue of company is higher than the break-

even sales that generate earnings or net income for the company (Kravchyk, Okur and

Kovalenko, 2021). Hence, this answer is important for the management of Jack Motors to

analyse whether they need to continue with the product or not.

(C) Calculation of units of vehicles to be sold for a target profit of £200000

Let, assume units of vehicles to be sold at a target profit of £200000 is x

Profit and Loss A/c

Particulars Details Amount

Sales revenue x units * £50000 50000x

Less Variable cost x units * £30000 30000x

Contribution 20000x

Less Fixed cost 4000000

Net Income 200000

On the basis of above P&L, the equation will become 20000x – 4000000 = 200000

= 20000x = 200000 + 4000000

= 20000x = 600000

X = 4200000 / 20000

= 210 units of vehicles.

Hence, as per above calculation of equation, it can be said that the company need to sold 210

units of vehicles in order to earn the target profit of £200000. This calculation or result is

important for the production line manager of Jack Motors to understand and analyse the number

of vehicles they need to sale in order to earn the target profit of business (Sintha, 2020).

The margin of safety in the break-even analysis is the amount of sales that are above the

break-even sales. On the basis of above calculation, it is identified that Jack Motors margin of

safety is 60%. It means 60% of the sales units or revenue of company is higher than the break-

even sales that generate earnings or net income for the company (Kravchyk, Okur and

Kovalenko, 2021). Hence, this answer is important for the management of Jack Motors to

analyse whether they need to continue with the product or not.

(C) Calculation of units of vehicles to be sold for a target profit of £200000

Let, assume units of vehicles to be sold at a target profit of £200000 is x

Profit and Loss A/c

Particulars Details Amount

Sales revenue x units * £50000 50000x

Less Variable cost x units * £30000 30000x

Contribution 20000x

Less Fixed cost 4000000

Net Income 200000

On the basis of above P&L, the equation will become 20000x – 4000000 = 200000

= 20000x = 200000 + 4000000

= 20000x = 600000

X = 4200000 / 20000

= 210 units of vehicles.

Hence, as per above calculation of equation, it can be said that the company need to sold 210

units of vehicles in order to earn the target profit of £200000. This calculation or result is

important for the production line manager of Jack Motors to understand and analyse the number

of vehicles they need to sale in order to earn the target profit of business (Sintha, 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.

Limitation of Cost Volume Profit Analysis

The various limitation of cost volume profit analysis are as follows:

Under cost volume profit analysis, the identification and distribution of total cost to fixed

and variable cost is difficult for the company.

Another limitation of CVP analysis is such that it assumes that the selling price and

variable cost per unit will remain constant at all level of output which is not possible in

real life.

The cost volume profit analysis is not suitable for the multiproduct firm. It means the

organization that are producing and selling multiproduct face difficulty in adopting this

technique.

This technique also ignores the impact or influence of other factors on cost and profit

which result into the non-reliable result.

It is also not effective in the long run and the presence of inventory is one of the

significant limitation of the cost volume profit analysis.

This technique is more emphasized on sales thus sometime ignores the customer demand

and leads to spoilage of goods (Hafizan and et.al., 2020).

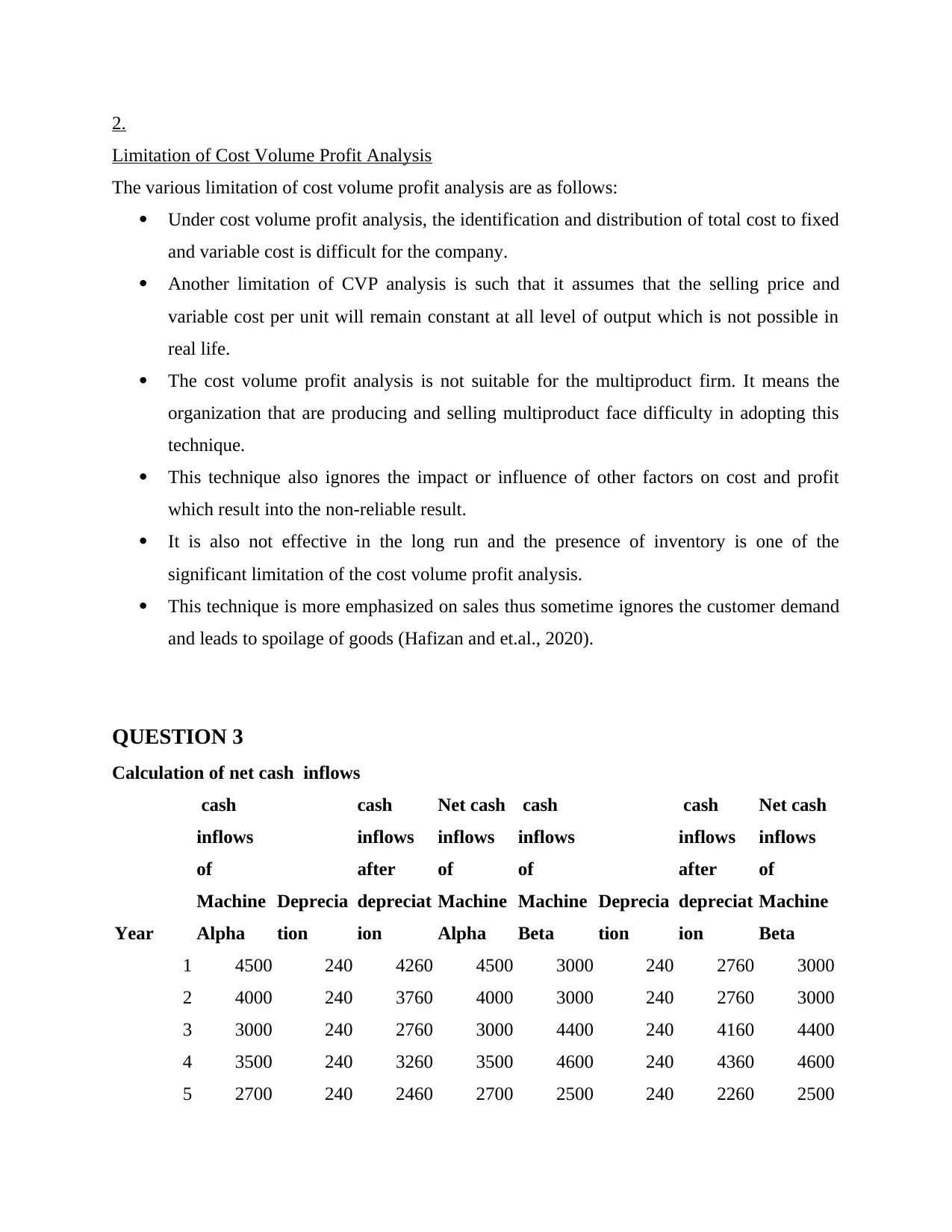

QUESTION 3

Calculation of net cash inflows

Year

cash

inflows

of

Machine

Alpha

Deprecia

tion

cash

inflows

after

depreciat

ion

Net cash

inflows

of

Machine

Alpha

cash

inflows

of

Machine

Beta

Deprecia

tion

cash

inflows

after

depreciat

ion

Net cash

inflows

of

Machine

Beta

1 4500 240 4260 4500 3000 240 2760 3000

2 4000 240 3760 4000 3000 240 2760 3000

3 3000 240 2760 3000 4400 240 4160 4400

4 3500 240 3260 3500 4600 240 4360 4600

5 2700 240 2460 2700 2500 240 2260 2500

Limitation of Cost Volume Profit Analysis

The various limitation of cost volume profit analysis are as follows:

Under cost volume profit analysis, the identification and distribution of total cost to fixed

and variable cost is difficult for the company.

Another limitation of CVP analysis is such that it assumes that the selling price and

variable cost per unit will remain constant at all level of output which is not possible in

real life.

The cost volume profit analysis is not suitable for the multiproduct firm. It means the

organization that are producing and selling multiproduct face difficulty in adopting this

technique.

This technique also ignores the impact or influence of other factors on cost and profit

which result into the non-reliable result.

It is also not effective in the long run and the presence of inventory is one of the

significant limitation of the cost volume profit analysis.

This technique is more emphasized on sales thus sometime ignores the customer demand

and leads to spoilage of goods (Hafizan and et.al., 2020).

QUESTION 3

Calculation of net cash inflows

Year

cash

inflows

of

Machine

Alpha

Deprecia

tion

cash

inflows

after

depreciat

ion

Net cash

inflows

of

Machine

Alpha

cash

inflows

of

Machine

Beta

Deprecia

tion

cash

inflows

after

depreciat

ion

Net cash

inflows

of

Machine

Beta

1 4500 240 4260 4500 3000 240 2760 3000

2 4000 240 3760 4000 3000 240 2760 3000

3 3000 240 2760 3000 4400 240 4160 4400

4 3500 240 3260 3500 4600 240 4360 4600

5 2700 240 2460 2700 2500 240 2260 2500

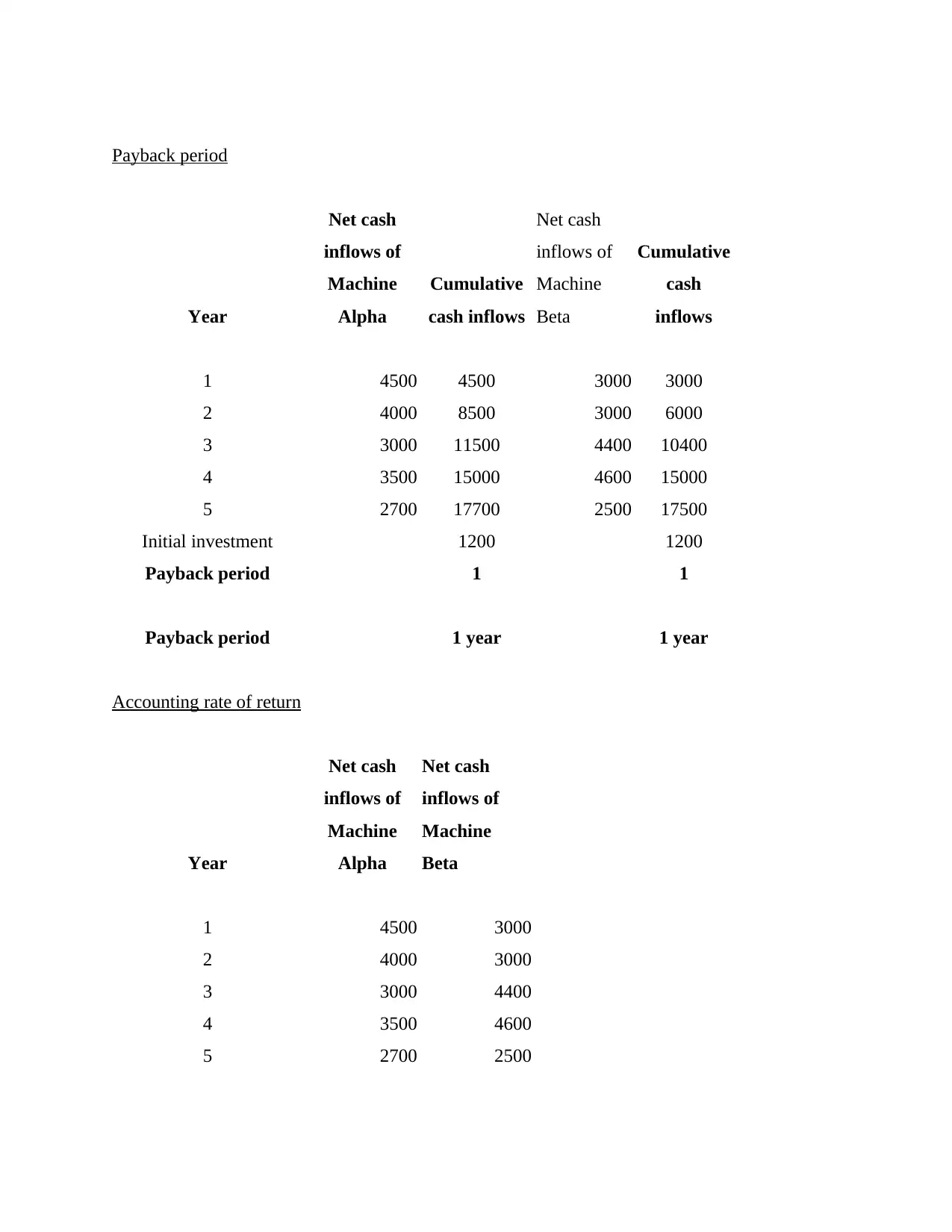

Payback period

Year

Net cash

inflows of

Machine

Alpha

Cumulative

cash inflows

Net cash

inflows of

Machine

Beta

Cumulative

cash

inflows

1 4500 4500 3000 3000

2 4000 8500 3000 6000

3 3000 11500 4400 10400

4 3500 15000 4600 15000

5 2700 17700 2500 17500

Initial investment 1200 1200

Payback period 1 1

Payback period 1 year 1 year

Accounting rate of return

Year

Net cash

inflows of

Machine

Alpha

Net cash

inflows of

Machine

Beta

1 4500 3000

2 4000 3000

3 3000 4400

4 3500 4600

5 2700 2500

Year

Net cash

inflows of

Machine

Alpha

Cumulative

cash inflows

Net cash

inflows of

Machine

Beta

Cumulative

cash

inflows

1 4500 4500 3000 3000

2 4000 8500 3000 6000

3 3000 11500 4400 10400

4 3500 15000 4600 15000

5 2700 17700 2500 17500

Initial investment 1200 1200

Payback period 1 1

Payback period 1 year 1 year

Accounting rate of return

Year

Net cash

inflows of

Machine

Alpha

Net cash

inflows of

Machine

Beta

1 4500 3000

2 4000 3000

3 3000 4400

4 3500 4600

5 2700 2500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.