Financial Management Report: Cost of Capital, Valuation, and Debt

VerifiedAdded on 2020/06/06

|13

|3222

|69

Report

AI Summary

This report delves into key aspects of financial management, commencing with an exploration of methods for estimating the cost of capital, including the weighted average cost of capital (WACC), cost of debt, and cost of equity using the CAPM model. The report then transitions into business valuation methods, discussing the discounted cash flow (DCF) model and price-earnings ratio, while also addressing the limitations and issues associated with each approach. The DCF model is applied to forecast cash flows, and the report calculates the intrinsic value of shares. Finally, the report examines the evaluation of senior secured debt in relation to overall sources of finance, providing a comprehensive analysis of the financial health and valuation of a firm.

FINANCIAL MANAGEMENT FOR

ORGANISATIONS

ORGANISATIONS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Methods of estimating cost of capital..............................................................................................1

Business valuation methods and issues associated with them.........................................................3

Evaluation of senior secured debt in January 2017 in relation to overall source of finance...........8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

Methods of estimating cost of capital..............................................................................................1

Business valuation methods and issues associated with them.........................................................3

Evaluation of senior secured debt in January 2017 in relation to overall source of finance...........8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

LIST OF TABLES

Table 1: Calculation of cost of equity..............................................................................................2

Table 2: Calculation of enterprise value..........................................................................................2

Table 3: Calculation of WACC.......................................................................................................2

Table 4: Computation of cash flows................................................................................................3

Table 5: Percentage growth rate of cash outflow elements.............................................................4

Table 6: Present value of cash flows...............................................................................................4

Table 7: Computation of terminal value..........................................................................................5

Table 8: Equity overall value...........................................................................................................5

Table 9: Intrinsic value calculation..................................................................................................5

Table 10: Price earning ratio............................................................................................................7

Table 11: Calculation of EPS..........................................................................................................7

Table 1: Calculation of cost of equity..............................................................................................2

Table 2: Calculation of enterprise value..........................................................................................2

Table 3: Calculation of WACC.......................................................................................................2

Table 4: Computation of cash flows................................................................................................3

Table 5: Percentage growth rate of cash outflow elements.............................................................4

Table 6: Present value of cash flows...............................................................................................4

Table 7: Computation of terminal value..........................................................................................5

Table 8: Equity overall value...........................................................................................................5

Table 9: Intrinsic value calculation..................................................................................................5

Table 10: Price earning ratio............................................................................................................7

Table 11: Calculation of EPS..........................................................................................................7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Corporate finance is the one of growing domain on which currently are placing due

attention so as to make accurate business decisions. In the current report, different approaches

are discussed in detail that are related to computation of cost of capital in the business. In middle

part of the report, DCF, earning per share and price earning ratio are computed and issues

associated with these approaches are discussed in detail. At end of the report, secured debt that

firm raised from market is discussed in respect to overall sources of finance.

METHODS OF ESTIMATING COST OF CAPITAL

There are number of methods of estimating cost of capital. It must be noted that cost of

capital is measured in number of ways and there are advantage and disadvantage of all these

methods for the business firms. Some of the methods that can be used to meaure cost of capital

are explained below. Weighted average cost of capital: Weigthed average cost of capital is the one of the

important model of computing cost of capital. Under this method, cost of equity and cost

of debt is computed. Weight is given to debt and equity in the capital structure and cost of

debt and cost of equity is multiplied to weights (Benninga, 2010). Finally, corporate tax

percentage is deducted from relvant value and in this way weighted average cost of

capital is computed. It can be said that weighted average cost of capital is the one of the

important method of computing cost of capital in the business. Cost of debt: In case of cost of debt formula interest rate and corporate tax rate is taken in

to acount. In this approach from one first of all from 1 corporate tax rate is deducted and

relvant value is multiplied byb rate of interest. Finally, computed value is multiplied to

100 and in this way cost of debt is computed. Tax rate is deduced because in case loan is

taken in business it is not necessary to pay tax to the government. Cost of equity: Cost of equity is computed by using CAPM model which is also known

as capital asset pricing model. Under this model beta, market premium and risk free rate

of return is taken in to acount (Baldwin and Von Hippel, 2011). By using this approach

return percentage that must be atleast earned on equity is computed. That percentage is

considerd as cost of equity by the business firms and investors.

1 | P a g e

Corporate finance is the one of growing domain on which currently are placing due

attention so as to make accurate business decisions. In the current report, different approaches

are discussed in detail that are related to computation of cost of capital in the business. In middle

part of the report, DCF, earning per share and price earning ratio are computed and issues

associated with these approaches are discussed in detail. At end of the report, secured debt that

firm raised from market is discussed in respect to overall sources of finance.

METHODS OF ESTIMATING COST OF CAPITAL

There are number of methods of estimating cost of capital. It must be noted that cost of

capital is measured in number of ways and there are advantage and disadvantage of all these

methods for the business firms. Some of the methods that can be used to meaure cost of capital

are explained below. Weighted average cost of capital: Weigthed average cost of capital is the one of the

important model of computing cost of capital. Under this method, cost of equity and cost

of debt is computed. Weight is given to debt and equity in the capital structure and cost of

debt and cost of equity is multiplied to weights (Benninga, 2010). Finally, corporate tax

percentage is deducted from relvant value and in this way weighted average cost of

capital is computed. It can be said that weighted average cost of capital is the one of the

important method of computing cost of capital in the business. Cost of debt: In case of cost of debt formula interest rate and corporate tax rate is taken in

to acount. In this approach from one first of all from 1 corporate tax rate is deducted and

relvant value is multiplied byb rate of interest. Finally, computed value is multiplied to

100 and in this way cost of debt is computed. Tax rate is deduced because in case loan is

taken in business it is not necessary to pay tax to the government. Cost of equity: Cost of equity is computed by using CAPM model which is also known

as capital asset pricing model. Under this model beta, market premium and risk free rate

of return is taken in to acount (Baldwin and Von Hippel, 2011). By using this approach

return percentage that must be atleast earned on equity is computed. That percentage is

considerd as cost of equity by the business firms and investors.

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

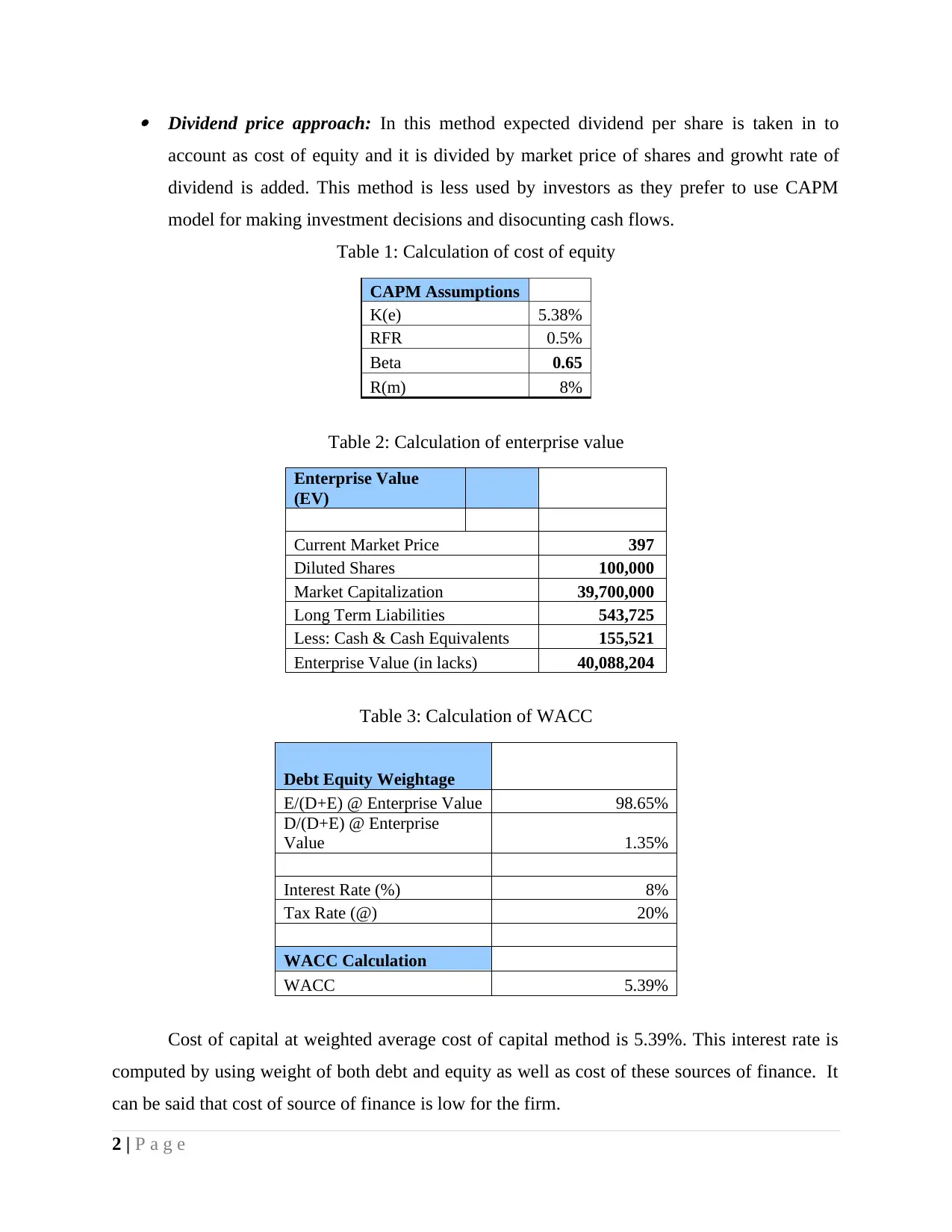

Dividend price approach: In this method expected dividend per share is taken in to

account as cost of equity and it is divided by market price of shares and growht rate of

dividend is added. This method is less used by investors as they prefer to use CAPM

model for making investment decisions and disocunting cash flows.

Table 1: Calculation of cost of equity

CAPM Assumptions

K(e) 5.38%

RFR 0.5%

Beta 0.65

R(m) 8%

Table 2: Calculation of enterprise value

Enterprise Value

(EV)

Current Market Price 397

Diluted Shares 100,000

Market Capitalization 39,700,000

Long Term Liabilities 543,725

Less: Cash & Cash Equivalents 155,521

Enterprise Value (in lacks) 40,088,204

Table 3: Calculation of WACC

Debt Equity Weightage

E/(D+E) @ Enterprise Value 98.65%

D/(D+E) @ Enterprise

Value 1.35%

Interest Rate (%) 8%

Tax Rate (@) 20%

WACC Calculation

WACC 5.39%

Cost of capital at weighted average cost of capital method is 5.39%. This interest rate is

computed by using weight of both debt and equity as well as cost of these sources of finance. It

can be said that cost of source of finance is low for the firm.

2 | P a g e

account as cost of equity and it is divided by market price of shares and growht rate of

dividend is added. This method is less used by investors as they prefer to use CAPM

model for making investment decisions and disocunting cash flows.

Table 1: Calculation of cost of equity

CAPM Assumptions

K(e) 5.38%

RFR 0.5%

Beta 0.65

R(m) 8%

Table 2: Calculation of enterprise value

Enterprise Value

(EV)

Current Market Price 397

Diluted Shares 100,000

Market Capitalization 39,700,000

Long Term Liabilities 543,725

Less: Cash & Cash Equivalents 155,521

Enterprise Value (in lacks) 40,088,204

Table 3: Calculation of WACC

Debt Equity Weightage

E/(D+E) @ Enterprise Value 98.65%

D/(D+E) @ Enterprise

Value 1.35%

Interest Rate (%) 8%

Tax Rate (@) 20%

WACC Calculation

WACC 5.39%

Cost of capital at weighted average cost of capital method is 5.39%. This interest rate is

computed by using weight of both debt and equity as well as cost of these sources of finance. It

can be said that cost of source of finance is low for the firm.

2 | P a g e

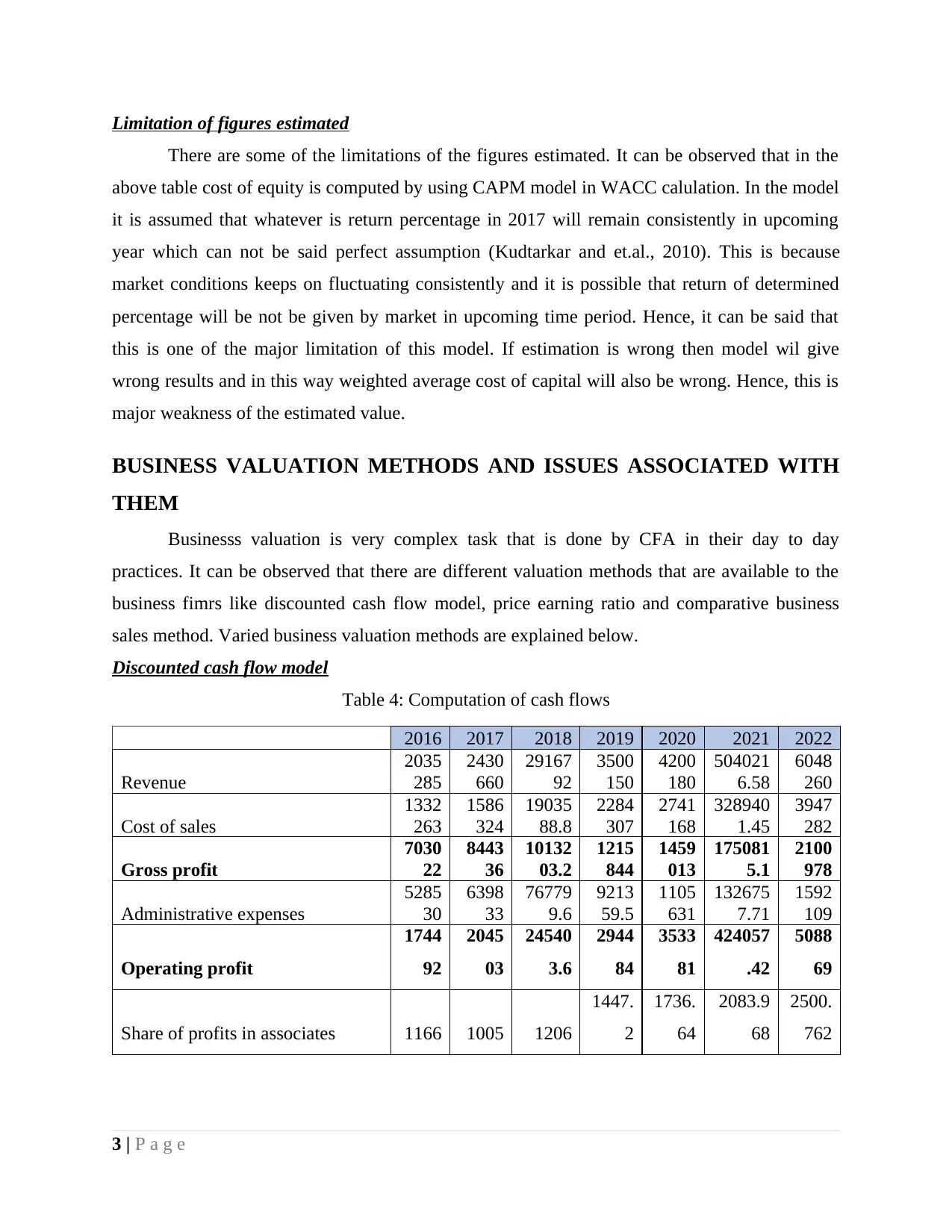

Limitation of figures estimated

There are some of the limitations of the figures estimated. It can be observed that in the

above table cost of equity is computed by using CAPM model in WACC calulation. In the model

it is assumed that whatever is return percentage in 2017 will remain consistently in upcoming

year which can not be said perfect assumption (Kudtarkar and et.al., 2010). This is because

market conditions keeps on fluctuating consistently and it is possible that return of determined

percentage will be not be given by market in upcoming time period. Hence, it can be said that

this is one of the major limitation of this model. If estimation is wrong then model wil give

wrong results and in this way weighted average cost of capital will also be wrong. Hence, this is

major weakness of the estimated value.

BUSINESS VALUATION METHODS AND ISSUES ASSOCIATED WITH

THEM

Businesss valuation is very complex task that is done by CFA in their day to day

practices. It can be observed that there are different valuation methods that are available to the

business fimrs like discounted cash flow model, price earning ratio and comparative business

sales method. Varied business valuation methods are explained below.

Discounted cash flow model

Table 4: Computation of cash flows

2016 2017 2018 2019 2020 2021 2022

Revenue

2035

285

2430

660

29167

92

3500

150

4200

180

504021

6.58

6048

260

Cost of sales

1332

263

1586

324

19035

88.8

2284

307

2741

168

328940

1.45

3947

282

Gross profit

7030

22

8443

36

10132

03.2

1215

844

1459

013

175081

5.1

2100

978

Administrative expenses

5285

30

6398

33

76779

9.6

9213

59.5

1105

631

132675

7.71

1592

109

Operating profit

1744

92

2045

03

24540

3.6

2944

84

3533

81

424057

.42

5088

69

Share of profits in associates 1166 1005 1206

1447.

2

1736.

64

2083.9

68

2500.

762

3 | P a g e

There are some of the limitations of the figures estimated. It can be observed that in the

above table cost of equity is computed by using CAPM model in WACC calulation. In the model

it is assumed that whatever is return percentage in 2017 will remain consistently in upcoming

year which can not be said perfect assumption (Kudtarkar and et.al., 2010). This is because

market conditions keeps on fluctuating consistently and it is possible that return of determined

percentage will be not be given by market in upcoming time period. Hence, it can be said that

this is one of the major limitation of this model. If estimation is wrong then model wil give

wrong results and in this way weighted average cost of capital will also be wrong. Hence, this is

major weakness of the estimated value.

BUSINESS VALUATION METHODS AND ISSUES ASSOCIATED WITH

THEM

Businesss valuation is very complex task that is done by CFA in their day to day

practices. It can be observed that there are different valuation methods that are available to the

business fimrs like discounted cash flow model, price earning ratio and comparative business

sales method. Varied business valuation methods are explained below.

Discounted cash flow model

Table 4: Computation of cash flows

2016 2017 2018 2019 2020 2021 2022

Revenue

2035

285

2430

660

29167

92

3500

150

4200

180

504021

6.58

6048

260

Cost of sales

1332

263

1586

324

19035

88.8

2284

307

2741

168

328940

1.45

3947

282

Gross profit

7030

22

8443

36

10132

03.2

1215

844

1459

013

175081

5.1

2100

978

Administrative expenses

5285

30

6398

33

76779

9.6

9213

59.5

1105

631

132675

7.71

1592

109

Operating profit

1744

92

2045

03

24540

3.6

2944

84

3533

81

424057

.42

5088

69

Share of profits in associates 1166 1005 1206

1447.

2

1736.

64

2083.9

68

2500.

762

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

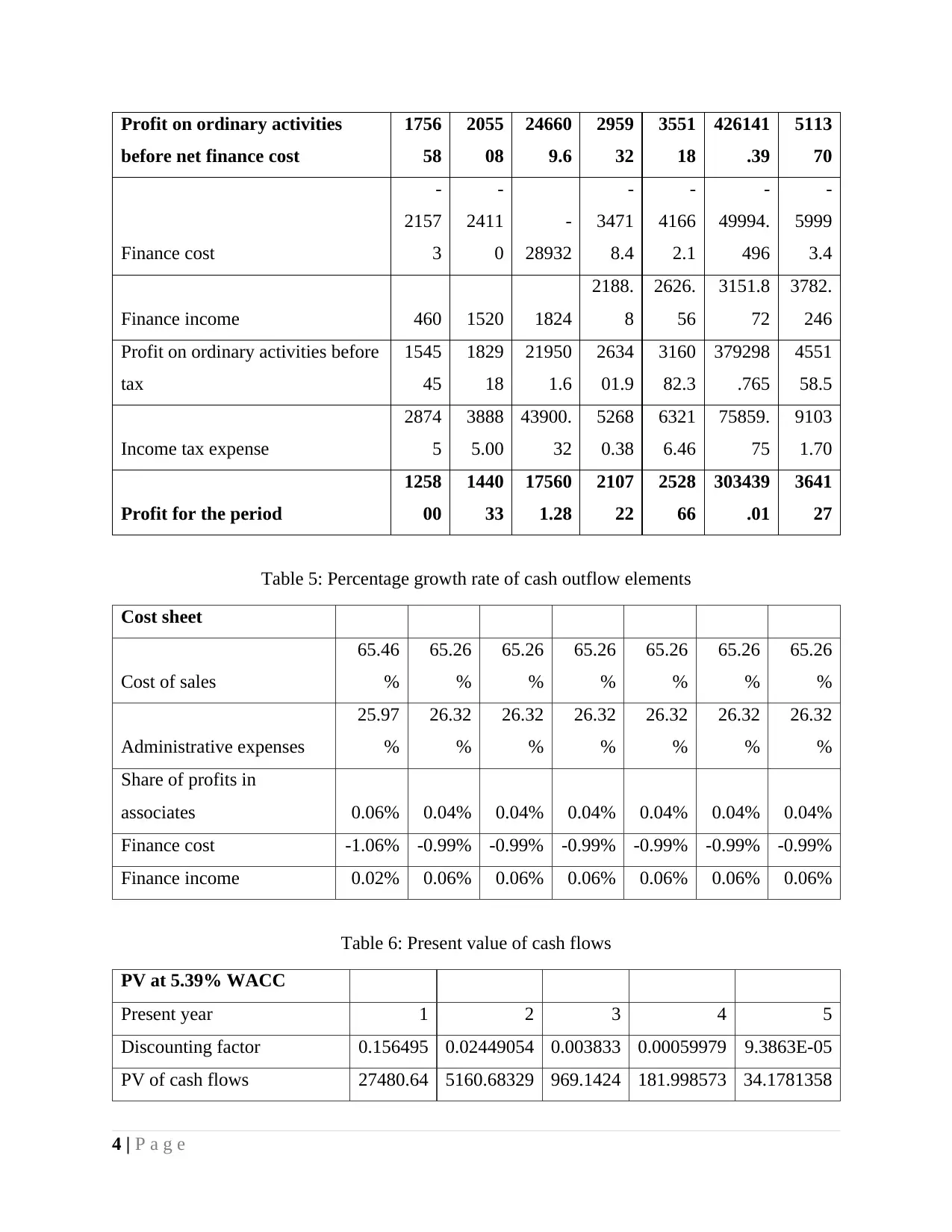

Profit on ordinary activities

before net finance cost

1756

58

2055

08

24660

9.6

2959

32

3551

18

426141

.39

5113

70

Finance cost

-

2157

3

-

2411

0

-

28932

-

3471

8.4

-

4166

2.1

-

49994.

496

-

5999

3.4

Finance income 460 1520 1824

2188.

8

2626.

56

3151.8

72

3782.

246

Profit on ordinary activities before

tax

1545

45

1829

18

21950

1.6

2634

01.9

3160

82.3

379298

.765

4551

58.5

Income tax expense

2874

5

3888

5.00

43900.

32

5268

0.38

6321

6.46

75859.

75

9103

1.70

Profit for the period

1258

00

1440

33

17560

1.28

2107

22

2528

66

303439

.01

3641

27

Table 5: Percentage growth rate of cash outflow elements

Cost sheet

Cost of sales

65.46

%

65.26

%

65.26

%

65.26

%

65.26

%

65.26

%

65.26

%

Administrative expenses

25.97

%

26.32

%

26.32

%

26.32

%

26.32

%

26.32

%

26.32

%

Share of profits in

associates 0.06% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04%

Finance cost -1.06% -0.99% -0.99% -0.99% -0.99% -0.99% -0.99%

Finance income 0.02% 0.06% 0.06% 0.06% 0.06% 0.06% 0.06%

Table 6: Present value of cash flows

PV at 5.39% WACC

Present year 1 2 3 4 5

Discounting factor 0.156495 0.02449054 0.003833 0.00059979 9.3863E-05

PV of cash flows 27480.64 5160.68329 969.1424 181.998573 34.1781358

4 | P a g e

before net finance cost

1756

58

2055

08

24660

9.6

2959

32

3551

18

426141

.39

5113

70

Finance cost

-

2157

3

-

2411

0

-

28932

-

3471

8.4

-

4166

2.1

-

49994.

496

-

5999

3.4

Finance income 460 1520 1824

2188.

8

2626.

56

3151.8

72

3782.

246

Profit on ordinary activities before

tax

1545

45

1829

18

21950

1.6

2634

01.9

3160

82.3

379298

.765

4551

58.5

Income tax expense

2874

5

3888

5.00

43900.

32

5268

0.38

6321

6.46

75859.

75

9103

1.70

Profit for the period

1258

00

1440

33

17560

1.28

2107

22

2528

66

303439

.01

3641

27

Table 5: Percentage growth rate of cash outflow elements

Cost sheet

Cost of sales

65.46

%

65.26

%

65.26

%

65.26

%

65.26

%

65.26

%

65.26

%

Administrative expenses

25.97

%

26.32

%

26.32

%

26.32

%

26.32

%

26.32

%

26.32

%

Share of profits in

associates 0.06% 0.04% 0.04% 0.04% 0.04% 0.04% 0.04%

Finance cost -1.06% -0.99% -0.99% -0.99% -0.99% -0.99% -0.99%

Finance income 0.02% 0.06% 0.06% 0.06% 0.06% 0.06% 0.06%

Table 6: Present value of cash flows

PV at 5.39% WACC

Present year 1 2 3 4 5

Discounting factor 0.156495 0.02449054 0.003833 0.00059979 9.3863E-05

PV of cash flows 27480.64 5160.68329 969.1424 181.998573 34.1781358

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table 7: Computation of terminal value

Terminal Value

Sum of PV of FCF for explicit forecast 33,827

WACC 5.39%

Long term growth in Revenues 20%

Present Value of terminal value (0.022)

Terminal Value as % of Total Value -0.00006%

Table 8: Equity overall value

Equity Value

Enterprise

Value 33,827

- Debt 543,725

+ Cash 155,521

Net Debt 699,246

Equity Value 733,073

Table 9: Intrinsic value calculation

Intrinsic

Value

Equity

Value 733,073

Diluted

Shares 100,000

5 | P a g e

Terminal Value

Sum of PV of FCF for explicit forecast 33,827

WACC 5.39%

Long term growth in Revenues 20%

Present Value of terminal value (0.022)

Terminal Value as % of Total Value -0.00006%

Table 8: Equity overall value

Equity Value

Enterprise

Value 33,827

- Debt 543,725

+ Cash 155,521

Net Debt 699,246

Equity Value 733,073

Table 9: Intrinsic value calculation

Intrinsic

Value

Equity

Value 733,073

Diluted

Shares 100,000

5 | P a g e

Intrinsic

Value 7

Interpretation

Discounted cash flow model is applied on above tables and it can be seen that fair value

of shares is estimated at 7. Current value of firm shares is 398.2 and comparison of both prices

reflects that shares of the firm are overvalued and due to this reason investment must not made if

any indvidual is planning to make investment in releavnt company shares. It can be seen from

table that company gross profit value increased consistently from 703022 to 2100978. Operating

profit value also increased from 174492 to 508869. This reflect that there is strong control on

expenses in the business and due to this reason operating profit increased at fast rate in the

business. Cost of sales cover 65.46% of sales and it is one of the major expenditure that is made

in the business. Administrative expenses cover 25.97% of overall sales amount and it is assumed

that always these expesnses will cover almost same percentage of sales. Usually, in the business

it happened that sales are made at specific rate and due to this expenses are made at same

percentage (Menascé, Casalicchio and Dubey, 2010). Hence, similar rate is assumed for

expenses and due to this reason constant rate is assumed for all sort of expenses in the business.

Fair value of equity is computed at 7 which is lower then market rate and it can be said that

shares are overvalued in the market.

Issues in disocunted cash flow model

There are some of the issues that are associated with discounted cash flow model. One of

the main issue associated with the model is growth rate that is taken in to account to compute

cash flow for the upcoming time period. Many time analysts make mistake in estimating growth

rate of cash flows and due to this reason wrong value is computed as fair value by the company

or analyst. All these things lead to making wrong business and investment decisions. This is one

of the big issue that is associated with discounted cash flow model. Hence, one need to

cautiously determine the appropriate growth rate and in this regard number of steps must be

taken. First of all business environment analysis must be done and it must be identified that in

which direction changes are happening in same and to what extent it will have impact on firm

6 | P a g e

Value 7

Interpretation

Discounted cash flow model is applied on above tables and it can be seen that fair value

of shares is estimated at 7. Current value of firm shares is 398.2 and comparison of both prices

reflects that shares of the firm are overvalued and due to this reason investment must not made if

any indvidual is planning to make investment in releavnt company shares. It can be seen from

table that company gross profit value increased consistently from 703022 to 2100978. Operating

profit value also increased from 174492 to 508869. This reflect that there is strong control on

expenses in the business and due to this reason operating profit increased at fast rate in the

business. Cost of sales cover 65.46% of sales and it is one of the major expenditure that is made

in the business. Administrative expenses cover 25.97% of overall sales amount and it is assumed

that always these expesnses will cover almost same percentage of sales. Usually, in the business

it happened that sales are made at specific rate and due to this expenses are made at same

percentage (Menascé, Casalicchio and Dubey, 2010). Hence, similar rate is assumed for

expenses and due to this reason constant rate is assumed for all sort of expenses in the business.

Fair value of equity is computed at 7 which is lower then market rate and it can be said that

shares are overvalued in the market.

Issues in disocunted cash flow model

There are some of the issues that are associated with discounted cash flow model. One of

the main issue associated with the model is growth rate that is taken in to account to compute

cash flow for the upcoming time period. Many time analysts make mistake in estimating growth

rate of cash flows and due to this reason wrong value is computed as fair value by the company

or analyst. All these things lead to making wrong business and investment decisions. This is one

of the big issue that is associated with discounted cash flow model. Hence, one need to

cautiously determine the appropriate growth rate and in this regard number of steps must be

taken. First of all business environment analysis must be done and it must be identified that in

which direction changes are happening in same and to what extent it will have impact on firm

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

profitability (Healy and Palepu, 2012). In this regard, different years cash flows must be taken in

to acount and also information of business environment. By doing so it can be identified that

what appropriate growth rate may be for projecting cash flows. In this way one of the big issue

that is associated with discounted cash flow model can be solved. Apart from this number of

other approaches and tools can be used to solve this problem. In this regard, analytics can be

used by the firm at its workplace and by using same esimation can be made about cash flows in

proper manner.

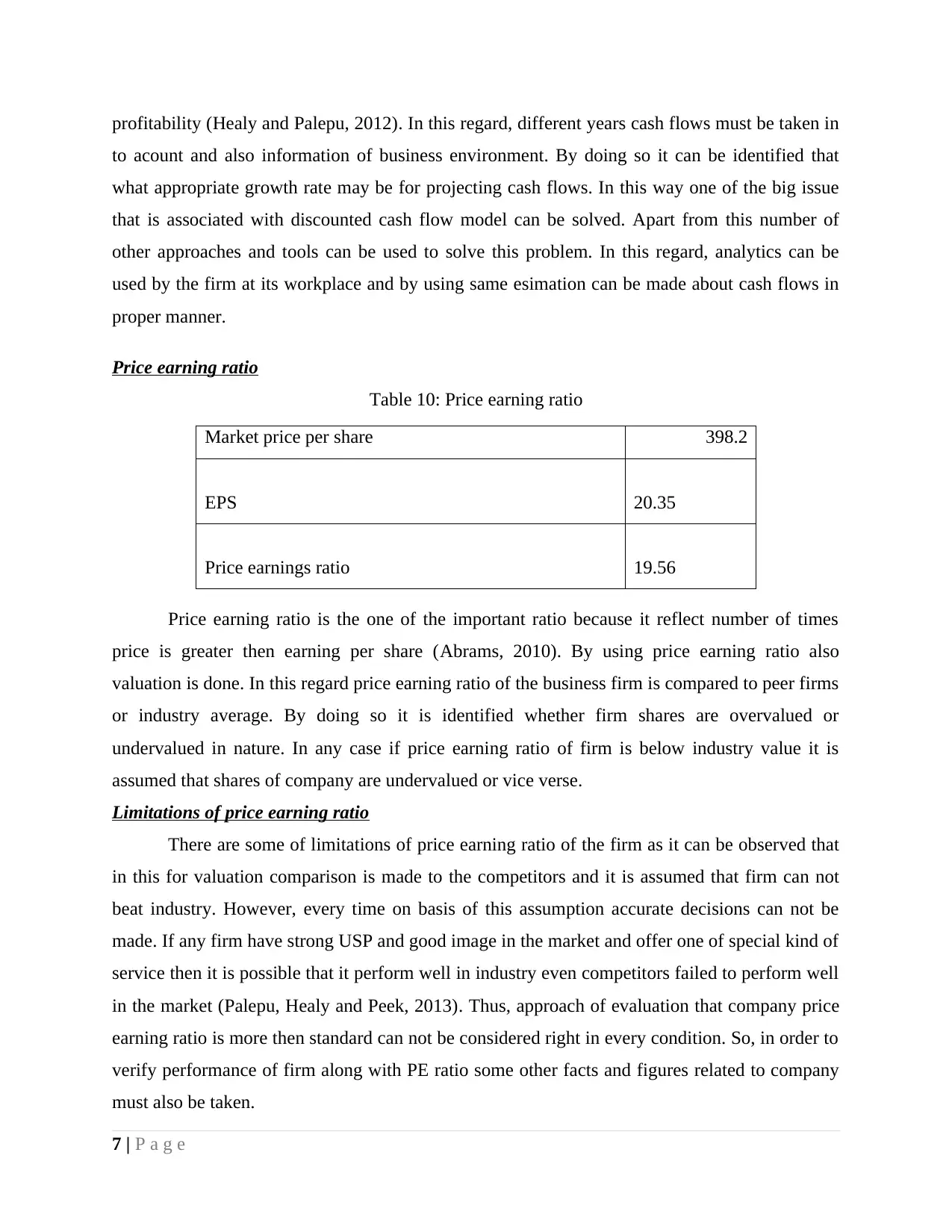

Price earning ratio

Table 10: Price earning ratio

Market price per share 398.2

EPS 20.35

Price earnings ratio 19.56

Price earning ratio is the one of the important ratio because it reflect number of times

price is greater then earning per share (Abrams, 2010). By using price earning ratio also

valuation is done. In this regard price earning ratio of the business firm is compared to peer firms

or industry average. By doing so it is identified whether firm shares are overvalued or

undervalued in nature. In any case if price earning ratio of firm is below industry value it is

assumed that shares of company are undervalued or vice verse.

Limitations of price earning ratio

There are some of limitations of price earning ratio of the firm as it can be observed that

in this for valuation comparison is made to the competitors and it is assumed that firm can not

beat industry. However, every time on basis of this assumption accurate decisions can not be

made. If any firm have strong USP and good image in the market and offer one of special kind of

service then it is possible that it perform well in industry even competitors failed to perform well

in the market (Palepu, Healy and Peek, 2013). Thus, approach of evaluation that company price

earning ratio is more then standard can not be considered right in every condition. So, in order to

verify performance of firm along with PE ratio some other facts and figures related to company

must also be taken.

7 | P a g e

to acount and also information of business environment. By doing so it can be identified that

what appropriate growth rate may be for projecting cash flows. In this way one of the big issue

that is associated with discounted cash flow model can be solved. Apart from this number of

other approaches and tools can be used to solve this problem. In this regard, analytics can be

used by the firm at its workplace and by using same esimation can be made about cash flows in

proper manner.

Price earning ratio

Table 10: Price earning ratio

Market price per share 398.2

EPS 20.35

Price earnings ratio 19.56

Price earning ratio is the one of the important ratio because it reflect number of times

price is greater then earning per share (Abrams, 2010). By using price earning ratio also

valuation is done. In this regard price earning ratio of the business firm is compared to peer firms

or industry average. By doing so it is identified whether firm shares are overvalued or

undervalued in nature. In any case if price earning ratio of firm is below industry value it is

assumed that shares of company are undervalued or vice verse.

Limitations of price earning ratio

There are some of limitations of price earning ratio of the firm as it can be observed that

in this for valuation comparison is made to the competitors and it is assumed that firm can not

beat industry. However, every time on basis of this assumption accurate decisions can not be

made. If any firm have strong USP and good image in the market and offer one of special kind of

service then it is possible that it perform well in industry even competitors failed to perform well

in the market (Palepu, Healy and Peek, 2013). Thus, approach of evaluation that company price

earning ratio is more then standard can not be considered right in every condition. So, in order to

verify performance of firm along with PE ratio some other facts and figures related to company

must also be taken.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

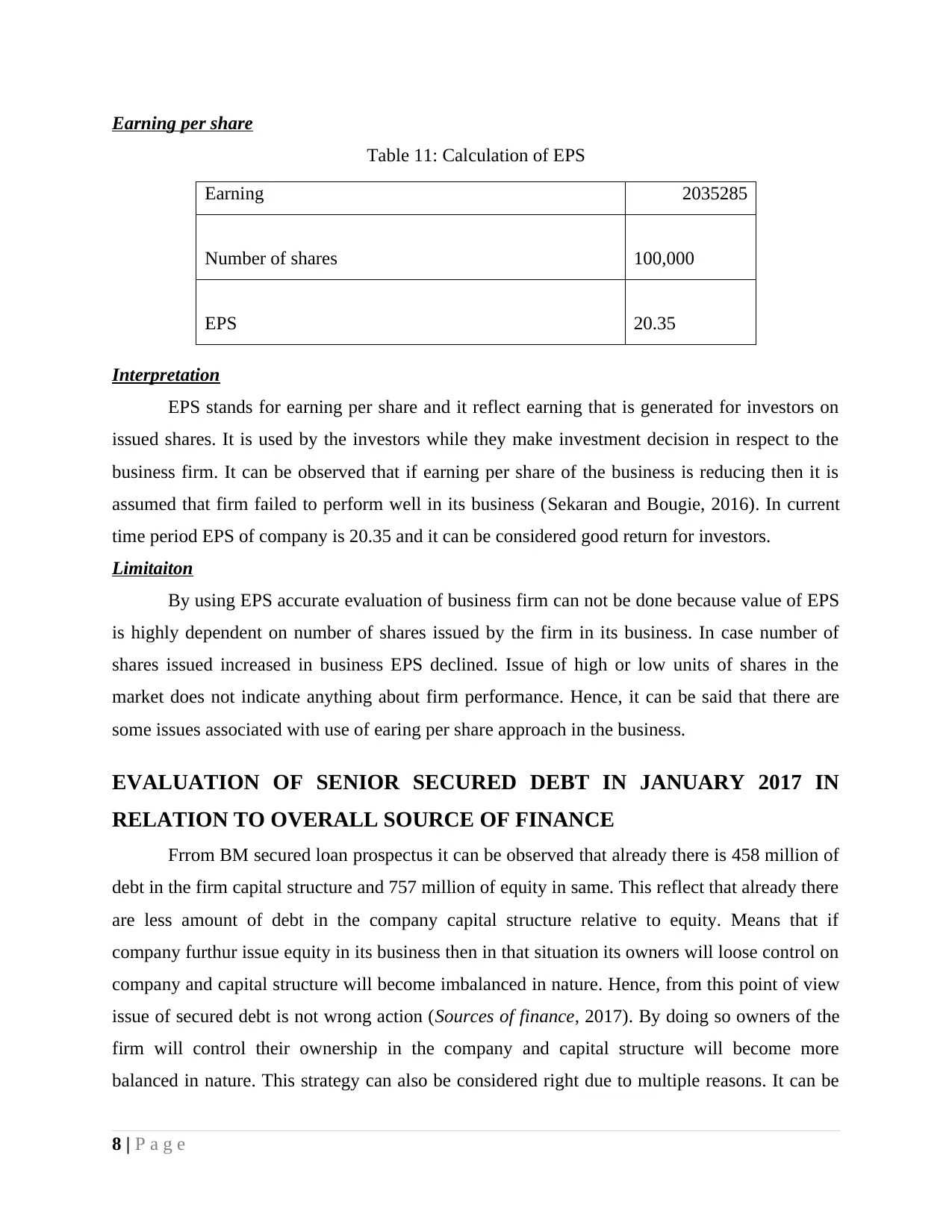

Earning per share

Table 11: Calculation of EPS

Earning 2035285

Number of shares 100,000

EPS 20.35

Interpretation

EPS stands for earning per share and it reflect earning that is generated for investors on

issued shares. It is used by the investors while they make investment decision in respect to the

business firm. It can be observed that if earning per share of the business is reducing then it is

assumed that firm failed to perform well in its business (Sekaran and Bougie, 2016). In current

time period EPS of company is 20.35 and it can be considered good return for investors.

Limitaiton

By using EPS accurate evaluation of business firm can not be done because value of EPS

is highly dependent on number of shares issued by the firm in its business. In case number of

shares issued increased in business EPS declined. Issue of high or low units of shares in the

market does not indicate anything about firm performance. Hence, it can be said that there are

some issues associated with use of earing per share approach in the business.

EVALUATION OF SENIOR SECURED DEBT IN JANUARY 2017 IN

RELATION TO OVERALL SOURCE OF FINANCE

Frrom BM secured loan prospectus it can be observed that already there is 458 million of

debt in the firm capital structure and 757 million of equity in same. This reflect that already there

are less amount of debt in the company capital structure relative to equity. Means that if

company furthur issue equity in its business then in that situation its owners will loose control on

company and capital structure will become imbalanced in nature. Hence, from this point of view

issue of secured debt is not wrong action (Sources of finance, 2017). By doing so owners of the

firm will control their ownership in the company and capital structure will become more

balanced in nature. This strategy can also be considered right due to multiple reasons. It can be

8 | P a g e

Table 11: Calculation of EPS

Earning 2035285

Number of shares 100,000

EPS 20.35

Interpretation

EPS stands for earning per share and it reflect earning that is generated for investors on

issued shares. It is used by the investors while they make investment decision in respect to the

business firm. It can be observed that if earning per share of the business is reducing then it is

assumed that firm failed to perform well in its business (Sekaran and Bougie, 2016). In current

time period EPS of company is 20.35 and it can be considered good return for investors.

Limitaiton

By using EPS accurate evaluation of business firm can not be done because value of EPS

is highly dependent on number of shares issued by the firm in its business. In case number of

shares issued increased in business EPS declined. Issue of high or low units of shares in the

market does not indicate anything about firm performance. Hence, it can be said that there are

some issues associated with use of earing per share approach in the business.

EVALUATION OF SENIOR SECURED DEBT IN JANUARY 2017 IN

RELATION TO OVERALL SOURCE OF FINANCE

Frrom BM secured loan prospectus it can be observed that already there is 458 million of

debt in the firm capital structure and 757 million of equity in same. This reflect that already there

are less amount of debt in the company capital structure relative to equity. Means that if

company furthur issue equity in its business then in that situation its owners will loose control on

company and capital structure will become imbalanced in nature. Hence, from this point of view

issue of secured debt is not wrong action (Sources of finance, 2017). By doing so owners of the

firm will control their ownership in the company and capital structure will become more

balanced in nature. This strategy can also be considered right due to multiple reasons. It can be

8 | P a g e

observed that firm fund its operations through number of sources of finance like Put/Call

options, shares and through short term loan. Locking deal through call and put option is very

risky. Profit and loss are observed in millions in case of this source of finance. In comparison to

this bank loan is safe side as company already know about its debt payment liability in advance

and accordingly it prepare plan in its business. On other hand, in case of call and put options it is

not possible to make such kind of plans and due to this reason risk of failure or loss in business

are very high and payment liability may also increase suddenly. Hence, by considering this

source of finance it can be said that senior secured debt is the one of the best source of finance in

respect to overall source of finance. Receivables, trade payables and lease are also sources of

finance that are available in the firm capital structure (Criteria for evaluating different sources of

finance available to a business, 2017). These sources of finance can not be used for long term

and can not be used consistently in the business to fund business. Hence, it can be said that firm

decision to issue senior secured debt in January 2017 is correct and it will ensure that firm is able

to make effective use of varied sources of finance in its business. Issue of debt security will also

make capital structure more balanced then before and due to this reason it can be said that senior

secured debt is the one of best choice relative to overall source of finance.

CONCLUSION

On the basis of above discussion it is concluded that there is signficent importance of

business valuation methods because by using same business value can be measure that must be

in market. However, there are some of the limitations of each of the busines valuation approach

and due to this reason after considering number of factors specific approach of business

valuation must be used by the firm. It is also concluded that there are varied approaches of

computing cost of capital but weigthed average cost of capital is one of the best approach to do

equity valuation.

9 | P a g e

options, shares and through short term loan. Locking deal through call and put option is very

risky. Profit and loss are observed in millions in case of this source of finance. In comparison to

this bank loan is safe side as company already know about its debt payment liability in advance

and accordingly it prepare plan in its business. On other hand, in case of call and put options it is

not possible to make such kind of plans and due to this reason risk of failure or loss in business

are very high and payment liability may also increase suddenly. Hence, by considering this

source of finance it can be said that senior secured debt is the one of the best source of finance in

respect to overall source of finance. Receivables, trade payables and lease are also sources of

finance that are available in the firm capital structure (Criteria for evaluating different sources of

finance available to a business, 2017). These sources of finance can not be used for long term

and can not be used consistently in the business to fund business. Hence, it can be said that firm

decision to issue senior secured debt in January 2017 is correct and it will ensure that firm is able

to make effective use of varied sources of finance in its business. Issue of debt security will also

make capital structure more balanced then before and due to this reason it can be said that senior

secured debt is the one of best choice relative to overall source of finance.

CONCLUSION

On the basis of above discussion it is concluded that there is signficent importance of

business valuation methods because by using same business value can be measure that must be

in market. However, there are some of the limitations of each of the busines valuation approach

and due to this reason after considering number of factors specific approach of business

valuation must be used by the firm. It is also concluded that there are varied approaches of

computing cost of capital but weigthed average cost of capital is one of the best approach to do

equity valuation.

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.