Finance in Management and Leadership - Analysis of 3M Financial Data

VerifiedAdded on 2021/01/02

|11

|3123

|361

Report

AI Summary

This report provides a comprehensive analysis of financial management and leadership, focusing on the practical application of financial principles within an organizational context, using 3M as a case study. It begins by identifying stakeholders interested in financial information and maps their needs. The report then delves into the financial data and information necessary for decision-making in contemporary organizations, differentiating between the requirements of internal and external stakeholders. It explores various types of financial data, including sales results, cash dividend reports, and key performance indicators. The report concludes with an evaluation and comparison of financial data using income statements, highlighting how financial managers utilize cash receipts and accrual techniques to inform investment decisions. The analysis provides insights into how financial information is communicated to various stakeholders, and how different types of financial statements are used to support decision-making processes. The report uses the 3M company's financial data to illustrate key concepts.

FINANCE IN MANAGEMENT

AND LEADERSHIP

AND LEADERSHIP

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Which users are interested in receiving financial information’s contains stakeholder map. .1

TASK 2............................................................................................................................................3

Financial data and information required for decision making in the contemporary organisation

................................................................................................................................................3

TASK 3............................................................................................................................................4

Different type of financial data and information required for decision making.....................4

TASK 4............................................................................................................................................6

Evaluation and comparison of data using financial statements subject to stakeholder’s

perspective..............................................................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Which users are interested in receiving financial information’s contains stakeholder map. .1

TASK 2............................................................................................................................................3

Financial data and information required for decision making in the contemporary organisation

................................................................................................................................................3

TASK 3............................................................................................................................................4

Different type of financial data and information required for decision making.....................4

TASK 4............................................................................................................................................6

Evaluation and comparison of data using financial statements subject to stakeholder’s

perspective..............................................................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Financial management is said to be an efficient and effective administration of capital. It

will assist an organisation to accomplish the objectives which are set for the period of time.

While, financial leadership helps to guiding a non-profitable firm to attain future sustainability.

Both management and leader is held responsible for all financial aspects of an organisation and

plan to increase profitability of the company (Brigham and Houston, 2012). In this report,

leadership and management concept is structured according to financial perspective. 3M

organisation which is a science based technology company engaging in emphasising the lives of

communities and business operations in right way. A critical discussion is being provided

regarding communication with 3M stakeholders. Various types of financial data are being taken

in context to the chosen organisation. Apart from this, comparison with types of financial

statements those are prepared by 3M is also being mentioned under this report.

TASK 1

Which users are interested in receiving financial information’s contains stakeholder map

There are two type of main users as internal users and external users remain interested to

get financial information of organisation. The information related to financial operations remains

essential for both the users, Internal users which are also considered as managers and

accountants use accounting information for making effective decisions policies and plans

associated with the organisation's operations and management. For managers it is required to

analyse the financial information to evaluate performance in finance terms. It is analysed

whether the financial resources are being used in proper manner or utilised at required area.

External users contain owners, creditors, lenders, investors, government, general public

of organisation. These stakeholders do not take interest in internal operations and management.

The financial information related to return on investment, profitability and market share,

financial position in terms of assets, long term debts, equities and shareholders’ funds are the

main information’s important for external users. Investors are the most common external users of

financial statements. Both credit and equity investors make and assess their investment decision

through using relevant financial data of the company.

Stakeholders' map of 3M company

1

Financial management is said to be an efficient and effective administration of capital. It

will assist an organisation to accomplish the objectives which are set for the period of time.

While, financial leadership helps to guiding a non-profitable firm to attain future sustainability.

Both management and leader is held responsible for all financial aspects of an organisation and

plan to increase profitability of the company (Brigham and Houston, 2012). In this report,

leadership and management concept is structured according to financial perspective. 3M

organisation which is a science based technology company engaging in emphasising the lives of

communities and business operations in right way. A critical discussion is being provided

regarding communication with 3M stakeholders. Various types of financial data are being taken

in context to the chosen organisation. Apart from this, comparison with types of financial

statements those are prepared by 3M is also being mentioned under this report.

TASK 1

Which users are interested in receiving financial information’s contains stakeholder map

There are two type of main users as internal users and external users remain interested to

get financial information of organisation. The information related to financial operations remains

essential for both the users, Internal users which are also considered as managers and

accountants use accounting information for making effective decisions policies and plans

associated with the organisation's operations and management. For managers it is required to

analyse the financial information to evaluate performance in finance terms. It is analysed

whether the financial resources are being used in proper manner or utilised at required area.

External users contain owners, creditors, lenders, investors, government, general public

of organisation. These stakeholders do not take interest in internal operations and management.

The financial information related to return on investment, profitability and market share,

financial position in terms of assets, long term debts, equities and shareholders’ funds are the

main information’s important for external users. Investors are the most common external users of

financial statements. Both credit and equity investors make and assess their investment decision

through using relevant financial data of the company.

Stakeholders' map of 3M company

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Stakeholders mapping is said to be collaborative process of research, debate and

discussion that are made from multiple perspectives in order to determine a key list of

stakeholders across the entire stakeholder’s range. It is categories into various parts:

Identifying: Under this particular stage company need to determine who are the primary

stakeholders of 3M company. Such as:

Owner: It consists of investors, shareholders, rating agencies and so on.

Customers: Under this, direct and indirect customers and legal advocates.

Employees: Present and potential employees, retirees and representatives of the

company.

Industry: It consists of suppliers, competitors and industries opinion leaders.

Analysing: Once an individual identified proper lists of stakeholders, it is helpful to do further

analysis to better examination of their relevance and perspective they offer to the company. 3M

has developed complete lists of specific criteria to assist individual to determine stakeholders

such as:

Contribution: All the stakeholders of 3M company is having information on the issues

that could be helpful to the company is being analyse effectively.

Legitimacy: Position in organisation is primary surest avenues to power. It is related with

the follower’s beliefs that higher authority is having right to influence person and has an

obligation to deal with the decision made by the top management.

Willingness to engage: It means that how stakeholders of 3M is willingly coordinating

with the decision making or policy formulation they are associated with the company

(Molina and Preve, 2012).

Mapping: Under this stakeholder is a visual exercise and evaluation tool that can use to

determine which stakeholders are most useful to engaged with the decision making within the

department. By this, it can easy to analyse where stakeholder stand in the complex situations. It

is basically done to examine the key stakeholders which is giving maximum attention in overall

growth of the company.

Prioritizing stakeholders: It has been seen that usually, it is not essential to engage with all

stakeholder’s groups with the same level of intensity of the time. it can save time and cost in

case, company can determine clearly regarding whom they are engaging with and why within an

2

discussion that are made from multiple perspectives in order to determine a key list of

stakeholders across the entire stakeholder’s range. It is categories into various parts:

Identifying: Under this particular stage company need to determine who are the primary

stakeholders of 3M company. Such as:

Owner: It consists of investors, shareholders, rating agencies and so on.

Customers: Under this, direct and indirect customers and legal advocates.

Employees: Present and potential employees, retirees and representatives of the

company.

Industry: It consists of suppliers, competitors and industries opinion leaders.

Analysing: Once an individual identified proper lists of stakeholders, it is helpful to do further

analysis to better examination of their relevance and perspective they offer to the company. 3M

has developed complete lists of specific criteria to assist individual to determine stakeholders

such as:

Contribution: All the stakeholders of 3M company is having information on the issues

that could be helpful to the company is being analyse effectively.

Legitimacy: Position in organisation is primary surest avenues to power. It is related with

the follower’s beliefs that higher authority is having right to influence person and has an

obligation to deal with the decision made by the top management.

Willingness to engage: It means that how stakeholders of 3M is willingly coordinating

with the decision making or policy formulation they are associated with the company

(Molina and Preve, 2012).

Mapping: Under this stakeholder is a visual exercise and evaluation tool that can use to

determine which stakeholders are most useful to engaged with the decision making within the

department. By this, it can easy to analyse where stakeholder stand in the complex situations. It

is basically done to examine the key stakeholders which is giving maximum attention in overall

growth of the company.

Prioritizing stakeholders: It has been seen that usually, it is not essential to engage with all

stakeholder’s groups with the same level of intensity of the time. it can save time and cost in

case, company can determine clearly regarding whom they are engaging with and why within an

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation. A specific action can be taken by the company through closely analyse the

stakeholder’s issues and decide whether they are material to company engagement aims.

TASK 2

Financial data and information required for decision making in the contemporary organisation

Financial information is communicated with different stakeholders of organisation to

analyse the actual performance and position within organisation. Financial information is

communicating to both the internal stake holders and external stakeholders.

For internal stakeholders

A clear reporting structure is followed by organisation in terms of addressing the

financial information correctly and properly. A clearing reporting standard assist to deliver the

information and details to stakeholders effectively and efficiently (Allen, Hemming and Potter,

2013). In internal stakeholder group board of directors, management and leadership team are the

main elements used financial information for making financial plans and strategies. For effective

strategic planning and decision making type of information remains important like performance

data and evaluation reports, innovation and technological development report, revised mission

and vision statement. This information’s are communicated among 3M's stakeholders as follows

In the form of statutory reports and disclosure documents

By releasing the annual prospectus or annual reports

Through sustainability report and transcription data

Managerial reports contain the information related to annual team performance chart,

targeted groups and annual spending upon innovation and development.

Financial KPI (Key Performance Indicators) are used for explaining the reports and

information in summarised way. For instance, information related to use of liquid assets

is presented in particular format which is called as cash flow statement.

A management dashboard is to be prepared to categorise the financial information in

more effective and better manner.

Financial information isolated according to particular financial period.

Infographic, graphical representation and pictures are some convenient methods to

addressing the financial information to internal stakeholders.

For external stakeholders

3

stakeholder’s issues and decide whether they are material to company engagement aims.

TASK 2

Financial data and information required for decision making in the contemporary organisation

Financial information is communicated with different stakeholders of organisation to

analyse the actual performance and position within organisation. Financial information is

communicating to both the internal stake holders and external stakeholders.

For internal stakeholders

A clear reporting structure is followed by organisation in terms of addressing the

financial information correctly and properly. A clearing reporting standard assist to deliver the

information and details to stakeholders effectively and efficiently (Allen, Hemming and Potter,

2013). In internal stakeholder group board of directors, management and leadership team are the

main elements used financial information for making financial plans and strategies. For effective

strategic planning and decision making type of information remains important like performance

data and evaluation reports, innovation and technological development report, revised mission

and vision statement. This information’s are communicated among 3M's stakeholders as follows

In the form of statutory reports and disclosure documents

By releasing the annual prospectus or annual reports

Through sustainability report and transcription data

Managerial reports contain the information related to annual team performance chart,

targeted groups and annual spending upon innovation and development.

Financial KPI (Key Performance Indicators) are used for explaining the reports and

information in summarised way. For instance, information related to use of liquid assets

is presented in particular format which is called as cash flow statement.

A management dashboard is to be prepared to categorise the financial information in

more effective and better manner.

Financial information isolated according to particular financial period.

Infographic, graphical representation and pictures are some convenient methods to

addressing the financial information to internal stakeholders.

For external stakeholders

3

For external stakeholders it is important to determine the value of investment at present.

Stakeholders, Investors, bankers and financial institutions, owners, lenders and customers seeks

for better returns and consideration in exchange of their investments contributed with in

organisation (Cole, 2013). Financial information related to returns, interest, dividend payout,

market share and current market price of share are some key information executed as per the

guidelines given by GAAP (Generally Accepted Accounting Principles). It is important for long

term growth and development of organisation by considering these financial information and

details.

3M company is one of the wider organisation provides vital technological and research

services to different communities. The communication of financial information for 3M is

categorised as follows;

Banks: Type of financial credits are provided by banks and financial institutions. Data

related to flow of cash is the main information related important for banks that is produced in the

form of cash flow statement.

Investors: For investors it is important to determine the income and profitability of

organisation in terms of managing the operations and management of business. Income statement

as per guidelines of GAAP.

Strategic partners: A strategic partner are required to determine the resources which

remain essential for determining the resources for communicating this information. Certain

financial report such as inventory, account receivable job costing reports are important resources

for the partners.

TASK 3

Different type of financial data and information required for decision making

There are various kind of information which is provided in the form of income statement,

financial position statement and cash flow statement (Martin, 2016). These information plays

vital role in terms of making the decision and effective plans for better growth and development.

A sustainable success and growth of organisation based upon effective strategic decision plans

and policies. A proper management and control is done by analysing the requirements of

resources for addressing the task and projects. There is type of financial statements produce

4

Stakeholders, Investors, bankers and financial institutions, owners, lenders and customers seeks

for better returns and consideration in exchange of their investments contributed with in

organisation (Cole, 2013). Financial information related to returns, interest, dividend payout,

market share and current market price of share are some key information executed as per the

guidelines given by GAAP (Generally Accepted Accounting Principles). It is important for long

term growth and development of organisation by considering these financial information and

details.

3M company is one of the wider organisation provides vital technological and research

services to different communities. The communication of financial information for 3M is

categorised as follows;

Banks: Type of financial credits are provided by banks and financial institutions. Data

related to flow of cash is the main information related important for banks that is produced in the

form of cash flow statement.

Investors: For investors it is important to determine the income and profitability of

organisation in terms of managing the operations and management of business. Income statement

as per guidelines of GAAP.

Strategic partners: A strategic partner are required to determine the resources which

remain essential for determining the resources for communicating this information. Certain

financial report such as inventory, account receivable job costing reports are important resources

for the partners.

TASK 3

Different type of financial data and information required for decision making

There are various kind of information which is provided in the form of income statement,

financial position statement and cash flow statement (Martin, 2016). These information plays

vital role in terms of making the decision and effective plans for better growth and development.

A sustainable success and growth of organisation based upon effective strategic decision plans

and policies. A proper management and control is done by analysing the requirements of

resources for addressing the task and projects. There is type of financial statements produce

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

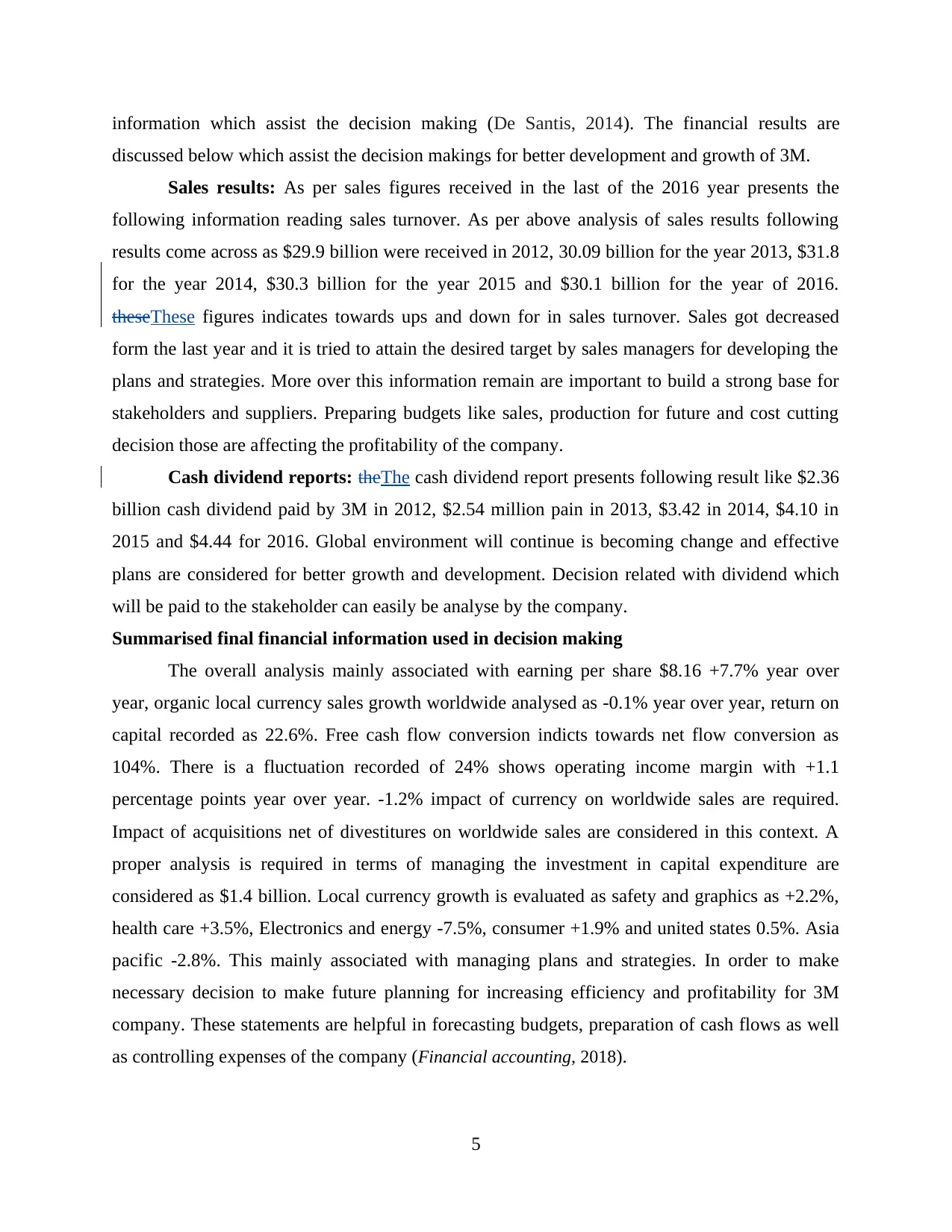

information which assist the decision making (De Santis, 2014). The financial results are

discussed below which assist the decision makings for better development and growth of 3M.

Sales results: As per sales figures received in the last of the 2016 year presents the

following information reading sales turnover. As per above analysis of sales results following

results come across as $29.9 billion were received in 2012, 30.09 billion for the year 2013, $31.8

for the year 2014, $30.3 billion for the year 2015 and $30.1 billion for the year of 2016.

theseThese figures indicates towards ups and down for in sales turnover. Sales got decreased

form the last year and it is tried to attain the desired target by sales managers for developing the

plans and strategies. More over this information remain are important to build a strong base for

stakeholders and suppliers. Preparing budgets like sales, production for future and cost cutting

decision those are affecting the profitability of the company.

Cash dividend reports: theThe cash dividend report presents following result like $2.36

billion cash dividend paid by 3M in 2012, $2.54 million pain in 2013, $3.42 in 2014, $4.10 in

2015 and $4.44 for 2016. Global environment will continue is becoming change and effective

plans are considered for better growth and development. Decision related with dividend which

will be paid to the stakeholder can easily be analyse by the company.

Summarised final financial information used in decision making

The overall analysis mainly associated with earning per share $8.16 +7.7% year over

year, organic local currency sales growth worldwide analysed as -0.1% year over year, return on

capital recorded as 22.6%. Free cash flow conversion indicts towards net flow conversion as

104%. There is a fluctuation recorded of 24% shows operating income margin with +1.1

percentage points year over year. -1.2% impact of currency on worldwide sales are required.

Impact of acquisitions net of divestitures on worldwide sales are considered in this context. A

proper analysis is required in terms of managing the investment in capital expenditure are

considered as $1.4 billion. Local currency growth is evaluated as safety and graphics as +2.2%,

health care +3.5%, Electronics and energy -7.5%, consumer +1.9% and united states 0.5%. Asia

pacific -2.8%. This mainly associated with managing plans and strategies. In order to make

necessary decision to make future planning for increasing efficiency and profitability for 3M

company. These statements are helpful in forecasting budgets, preparation of cash flows as well

as controlling expenses of the company (Financial accounting, 2018).

5

discussed below which assist the decision makings for better development and growth of 3M.

Sales results: As per sales figures received in the last of the 2016 year presents the

following information reading sales turnover. As per above analysis of sales results following

results come across as $29.9 billion were received in 2012, 30.09 billion for the year 2013, $31.8

for the year 2014, $30.3 billion for the year 2015 and $30.1 billion for the year of 2016.

theseThese figures indicates towards ups and down for in sales turnover. Sales got decreased

form the last year and it is tried to attain the desired target by sales managers for developing the

plans and strategies. More over this information remain are important to build a strong base for

stakeholders and suppliers. Preparing budgets like sales, production for future and cost cutting

decision those are affecting the profitability of the company.

Cash dividend reports: theThe cash dividend report presents following result like $2.36

billion cash dividend paid by 3M in 2012, $2.54 million pain in 2013, $3.42 in 2014, $4.10 in

2015 and $4.44 for 2016. Global environment will continue is becoming change and effective

plans are considered for better growth and development. Decision related with dividend which

will be paid to the stakeholder can easily be analyse by the company.

Summarised final financial information used in decision making

The overall analysis mainly associated with earning per share $8.16 +7.7% year over

year, organic local currency sales growth worldwide analysed as -0.1% year over year, return on

capital recorded as 22.6%. Free cash flow conversion indicts towards net flow conversion as

104%. There is a fluctuation recorded of 24% shows operating income margin with +1.1

percentage points year over year. -1.2% impact of currency on worldwide sales are required.

Impact of acquisitions net of divestitures on worldwide sales are considered in this context. A

proper analysis is required in terms of managing the investment in capital expenditure are

considered as $1.4 billion. Local currency growth is evaluated as safety and graphics as +2.2%,

health care +3.5%, Electronics and energy -7.5%, consumer +1.9% and united states 0.5%. Asia

pacific -2.8%. This mainly associated with managing plans and strategies. In order to make

necessary decision to make future planning for increasing efficiency and profitability for 3M

company. These statements are helpful in forecasting budgets, preparation of cash flows as well

as controlling expenses of the company (Financial accounting, 2018).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

Evaluation and comparison of data using financial statements subject to stakeholder’s

perspective

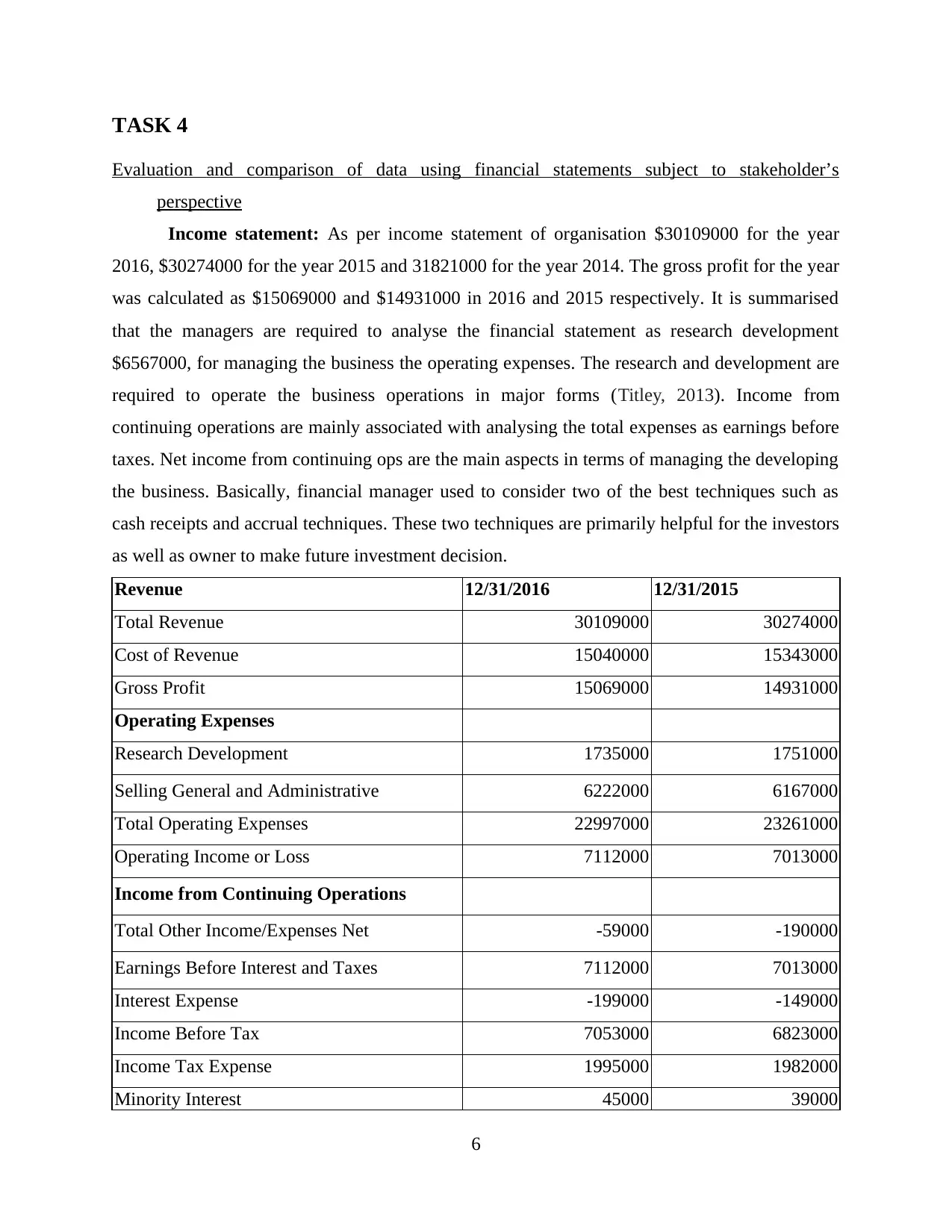

Income statement: As per income statement of organisation $30109000 for the year

2016, $30274000 for the year 2015 and 31821000 for the year 2014. The gross profit for the year

was calculated as $15069000 and $14931000 in 2016 and 2015 respectively. It is summarised

that the managers are required to analyse the financial statement as research development

$6567000, for managing the business the operating expenses. The research and development are

required to operate the business operations in major forms (Titley, 2013). Income from

continuing operations are mainly associated with analysing the total expenses as earnings before

taxes. Net income from continuing ops are the main aspects in terms of managing the developing

the business. Basically, financial manager used to consider two of the best techniques such as

cash receipts and accrual techniques. These two techniques are primarily helpful for the investors

as well as owner to make future investment decision.

Revenue 12/31/2016 12/31/2015

Total Revenue 30109000 30274000

Cost of Revenue 15040000 15343000

Gross Profit 15069000 14931000

Operating Expenses

Research Development 1735000 1751000

Selling General and Administrative 6222000 6167000

Total Operating Expenses 22997000 23261000

Operating Income or Loss 7112000 7013000

Income from Continuing Operations

Total Other Income/Expenses Net -59000 -190000

Earnings Before Interest and Taxes 7112000 7013000

Interest Expense -199000 -149000

Income Before Tax 7053000 6823000

Income Tax Expense 1995000 1982000

Minority Interest 45000 39000

6

Evaluation and comparison of data using financial statements subject to stakeholder’s

perspective

Income statement: As per income statement of organisation $30109000 for the year

2016, $30274000 for the year 2015 and 31821000 for the year 2014. The gross profit for the year

was calculated as $15069000 and $14931000 in 2016 and 2015 respectively. It is summarised

that the managers are required to analyse the financial statement as research development

$6567000, for managing the business the operating expenses. The research and development are

required to operate the business operations in major forms (Titley, 2013). Income from

continuing operations are mainly associated with analysing the total expenses as earnings before

taxes. Net income from continuing ops are the main aspects in terms of managing the developing

the business. Basically, financial manager used to consider two of the best techniques such as

cash receipts and accrual techniques. These two techniques are primarily helpful for the investors

as well as owner to make future investment decision.

Revenue 12/31/2016 12/31/2015

Total Revenue 30109000 30274000

Cost of Revenue 15040000 15343000

Gross Profit 15069000 14931000

Operating Expenses

Research Development 1735000 1751000

Selling General and Administrative 6222000 6167000

Total Operating Expenses 22997000 23261000

Operating Income or Loss 7112000 7013000

Income from Continuing Operations

Total Other Income/Expenses Net -59000 -190000

Earnings Before Interest and Taxes 7112000 7013000

Interest Expense -199000 -149000

Income Before Tax 7053000 6823000

Income Tax Expense 1995000 1982000

Minority Interest 45000 39000

6

Net Income From Continuing Ops 5058000 4841000

Non-recurring Events

Net Income

Net Income 5050000 4833000

Net Income Applicable To Common Shares 5050000 4833000

Cash flow statement: The cash flow from operations was recorded as $6662000 for the

year 2016 and $64200000 for the year 2015. For decision making perspective it is required to

analyse the aspects of capital expenditure to be utilised in future (Girvin and Murphy, 2013).

Cash flow from investing activity present the figures and data related to investment done in near

future. Cash flow from investing activity is evaluated as -$14030000 for the year 2016 and -

$2817000 for the year 2015. cash flow from financing activity is calculated as -$46260000 in

2016 and -$36480000 for the year 2015.As, cash flow statements are prepared by the taking only

cash related amount from various activity so by taking only cash receipts techniques they can

present this to the creditors and banks to analyse the follow of cash.

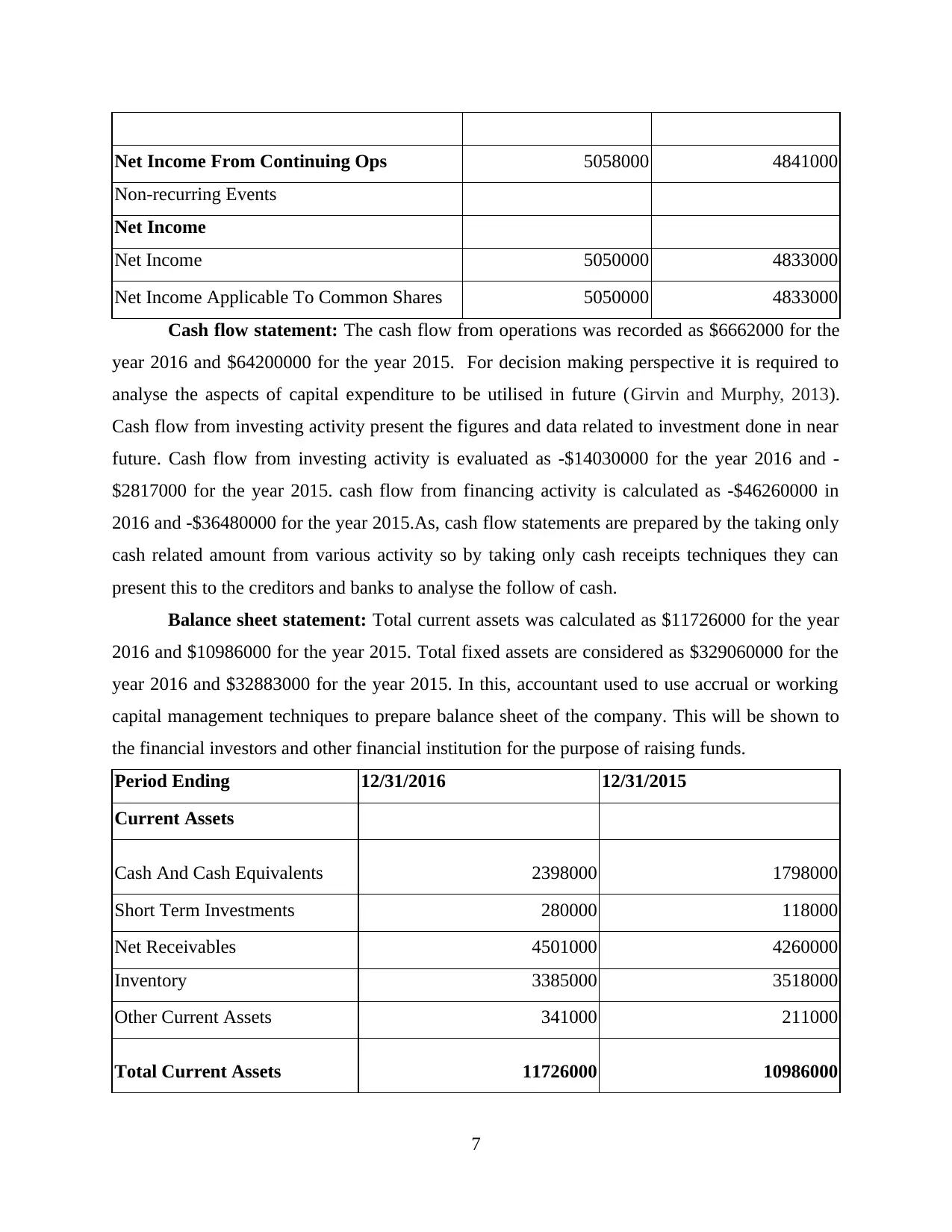

Balance sheet statement: Total current assets was calculated as $11726000 for the year

2016 and $10986000 for the year 2015. Total fixed assets are considered as $329060000 for the

year 2016 and $32883000 for the year 2015. In this, accountant used to use accrual or working

capital management techniques to prepare balance sheet of the company. This will be shown to

the financial investors and other financial institution for the purpose of raising funds.

Period Ending 12/31/2016 12/31/2015

Current Assets

Cash And Cash Equivalents 2398000 1798000

Short Term Investments 280000 118000

Net Receivables 4501000 4260000

Inventory 3385000 3518000

Other Current Assets 341000 211000

Total Current Assets 11726000 10986000

7

Non-recurring Events

Net Income

Net Income 5050000 4833000

Net Income Applicable To Common Shares 5050000 4833000

Cash flow statement: The cash flow from operations was recorded as $6662000 for the

year 2016 and $64200000 for the year 2015. For decision making perspective it is required to

analyse the aspects of capital expenditure to be utilised in future (Girvin and Murphy, 2013).

Cash flow from investing activity present the figures and data related to investment done in near

future. Cash flow from investing activity is evaluated as -$14030000 for the year 2016 and -

$2817000 for the year 2015. cash flow from financing activity is calculated as -$46260000 in

2016 and -$36480000 for the year 2015.As, cash flow statements are prepared by the taking only

cash related amount from various activity so by taking only cash receipts techniques they can

present this to the creditors and banks to analyse the follow of cash.

Balance sheet statement: Total current assets was calculated as $11726000 for the year

2016 and $10986000 for the year 2015. Total fixed assets are considered as $329060000 for the

year 2016 and $32883000 for the year 2015. In this, accountant used to use accrual or working

capital management techniques to prepare balance sheet of the company. This will be shown to

the financial investors and other financial institution for the purpose of raising funds.

Period Ending 12/31/2016 12/31/2015

Current Assets

Cash And Cash Equivalents 2398000 1798000

Short Term Investments 280000 118000

Net Receivables 4501000 4260000

Inventory 3385000 3518000

Other Current Assets 341000 211000

Total Current Assets 11726000 10986000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Long Term Investments 153000 150000

Property Plant and Equipment 8516000 8515000

Goodwill 9166000 9249000

Intangible Assets 2320000 2601000

Other Assets 1025000 1382000

Deferred Long Term Asset

Charges 422000 675000

Total Assets 32906000 32883000

Current Liabilities

Accounts Payable 1798000 1694000

Short/Current Long Term Debt 11695000 10844000

Other Current Liabilities 1844000 1873000

Total Current Liabilities 6219000 7118000

Long Term Debt 10678000 8754000

Other Liabilities 5621000 5497000

Minority Interest 45000 39000

Total Liabilities 22563000 21415000

Change in equity position statements: Change in equity present net tangible assets as -

1188000 for the tear 2016 and -4210000 for the year 2015.

CONCLUSION

The above report summarises the information which remain related to stakeholder’s

perspective. There is an evaluation of financial information from stakeholder’s perspective in

above report. There is a use of type of financial statements for making decisions and financial

plans are also summarised in this report.

8

Property Plant and Equipment 8516000 8515000

Goodwill 9166000 9249000

Intangible Assets 2320000 2601000

Other Assets 1025000 1382000

Deferred Long Term Asset

Charges 422000 675000

Total Assets 32906000 32883000

Current Liabilities

Accounts Payable 1798000 1694000

Short/Current Long Term Debt 11695000 10844000

Other Current Liabilities 1844000 1873000

Total Current Liabilities 6219000 7118000

Long Term Debt 10678000 8754000

Other Liabilities 5621000 5497000

Minority Interest 45000 39000

Total Liabilities 22563000 21415000

Change in equity position statements: Change in equity present net tangible assets as -

1188000 for the tear 2016 and -4210000 for the year 2015.

CONCLUSION

The above report summarises the information which remain related to stakeholder’s

perspective. There is an evaluation of financial information from stakeholder’s perspective in

above report. There is a use of type of financial statements for making decisions and financial

plans are also summarised in this report.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Allen, R., Hemming, R. and Potter, B. eds., 2013. The international handbook of public financial

management. Springer.

Brigham, E. F. and Houston, J. F., 2012. Fundamentals of financial management. Cengage

Learning.

Cole, R. A., 2013. What do we know about the capital structure of privately held US firms?

Evidence from the surveys of small business finance. Financial Management. 42(4).

pp.777-813.

De Santis, R. A., 2014. The euro area sovereign debt crisis: Identifying flight-to-liquidity and the

spillover mechanisms. Journal of Empirical Finance. 26. pp.150-170.

Girvin, B. and Murphy, G. eds., 2013. Continuity, change and crisis in contemporary Ireland.

Routledge.

Martin, L. L., 2016. Financial management for human service administrators. Waveland Press.

Molina, C. A. and Preve, L. A., 2012. An empirical analysis of the effect of financial distress on

trade credit. Financial Management. 41(1). pp.187-205.

Titley, G., 2013. Budgetjam! A communications intervention in the political-economic crisis in

Ireland. Journalism. 14(2), pp.292-306.

Winand, M., Zintz, T. and Scheerder, J., 2012. A financial management tool for sport federations.

Sport, business and management: an international journal. 2(3). pp.225-240.

Online

Financial accounting, 2018. [Online]. Available through: <

https://thismatter.com/money/tax/accounting-methods.html>.

9

Books and Journals:

Allen, R., Hemming, R. and Potter, B. eds., 2013. The international handbook of public financial

management. Springer.

Brigham, E. F. and Houston, J. F., 2012. Fundamentals of financial management. Cengage

Learning.

Cole, R. A., 2013. What do we know about the capital structure of privately held US firms?

Evidence from the surveys of small business finance. Financial Management. 42(4).

pp.777-813.

De Santis, R. A., 2014. The euro area sovereign debt crisis: Identifying flight-to-liquidity and the

spillover mechanisms. Journal of Empirical Finance. 26. pp.150-170.

Girvin, B. and Murphy, G. eds., 2013. Continuity, change and crisis in contemporary Ireland.

Routledge.

Martin, L. L., 2016. Financial management for human service administrators. Waveland Press.

Molina, C. A. and Preve, L. A., 2012. An empirical analysis of the effect of financial distress on

trade credit. Financial Management. 41(1). pp.187-205.

Titley, G., 2013. Budgetjam! A communications intervention in the political-economic crisis in

Ireland. Journalism. 14(2), pp.292-306.

Winand, M., Zintz, T. and Scheerder, J., 2012. A financial management tool for sport federations.

Sport, business and management: an international journal. 2(3). pp.225-240.

Online

Financial accounting, 2018. [Online]. Available through: <

https://thismatter.com/money/tax/accounting-methods.html>.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.