Financial Analysis Report: UK Carved Wooden Ornaments Venture, Year 1

VerifiedAdded on 2020/06/05

|28

|6272

|102

Report

AI Summary

This report provides a detailed financial analysis of a carved wooden ornament business venture in the UK. It encompasses various aspects of financial management, including a summary of assumptions, break-even analysis, profit and loss statements, balance sheets, monthly and annual cash flow statements, and sensitivity analysis. The report also addresses the initial cash requirements for the venture and offers suggestions for managing upfront supplier fees. The analysis is based on the financial data provided, including sales figures, cost estimations, and investment details. The report concludes with a reflection on the analysis and recommendations for the business's financial strategy, including a breakdown of fixed and variable costs, and a discussion of factors affecting the break-even point and profitability.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Summary of all the assumptions.................................................................................................1

Break- even analysis...................................................................................................................4

Profit and Loss and Balance sheet statements.............................................................................6

Monthly cash flow for the first year of operation.......................................................................7

Annual Cash Flow Statement ...................................................................................................12

A clear explanation, of how much cash the venture will need to get started............................14

Sensitivity Analysis...................................................................................................................17

Suggestions to pay upfront fees to Clearcut supplier................................................................20

Recommendations.....................................................................................................................21

Reflection of the Analysis.........................................................................................................22

CONCLUSIONS.......................................................................................................................24

REFERENCES..............................................................................................................................25

INTRODUCTION...........................................................................................................................1

Summary of all the assumptions.................................................................................................1

Break- even analysis...................................................................................................................4

Profit and Loss and Balance sheet statements.............................................................................6

Monthly cash flow for the first year of operation.......................................................................7

Annual Cash Flow Statement ...................................................................................................12

A clear explanation, of how much cash the venture will need to get started............................14

Sensitivity Analysis...................................................................................................................17

Suggestions to pay upfront fees to Clearcut supplier................................................................20

Recommendations.....................................................................................................................21

Reflection of the Analysis.........................................................................................................22

CONCLUSIONS.......................................................................................................................24

REFERENCES..............................................................................................................................25

INTRODUCTION

Financial management refers to the planning organising, directing and controlling of the

monitory resources of the organisation in such a manner that it helps in achieving the goals and

objectives of the organisation. This function is directly associated to the top level management.

Financial activities of the organisation includes utilization and procurement of the organisational

funds. Elements of financial management includes various types of decisions that are -

investment decisions that includes fixed assets known as capital budgeting, investment in current

assets known as working capital; financial decision that includes finance related decisions that

are raised from various resources; dividend decision that includes decision related to the

distribution of net profits. The objectives of financial management are to ensure adequate and

regular supply of funds to the organisation, create wealth for the business, generate cash,

adequate return to the shareholders, optimum utilisation of funds, safety on investments and to

plan a sound capital structure.

Functions of financial management are estimation of capital requirement, to determine

capital structure, choice of sources and investments of funds, distribution of surplus profits, cash

management and financial controls. Management of the organisation need to ensure the

availability of funds at the time of meeting business requirements. Short term requirements of

business includes stock, equipments, cost of sales and employees. Long term need includes

increase in assets.

In the below study accounting for financial management is done for Nancy who is willing

to start her own venture of carved wooden ornaments in UK. She is been retired from services

with an amount of £325000 and is willing to start a new business with this amount. The below

report providing full analysis of its financial activities as per the information provided by her.

The report includes break even analysis, income statement and balance sheet, cash flow

statement for monthly as well as yearly and also the sensitivity analysis of its financial

information.

Financial management refers to the planning organising, directing and controlling of the

monitory resources of the organisation in such a manner that it helps in achieving the goals and

objectives of the organisation. This function is directly associated to the top level management.

Financial activities of the organisation includes utilization and procurement of the organisational

funds. Elements of financial management includes various types of decisions that are -

investment decisions that includes fixed assets known as capital budgeting, investment in current

assets known as working capital; financial decision that includes finance related decisions that

are raised from various resources; dividend decision that includes decision related to the

distribution of net profits. The objectives of financial management are to ensure adequate and

regular supply of funds to the organisation, create wealth for the business, generate cash,

adequate return to the shareholders, optimum utilisation of funds, safety on investments and to

plan a sound capital structure.

Functions of financial management are estimation of capital requirement, to determine

capital structure, choice of sources and investments of funds, distribution of surplus profits, cash

management and financial controls. Management of the organisation need to ensure the

availability of funds at the time of meeting business requirements. Short term requirements of

business includes stock, equipments, cost of sales and employees. Long term need includes

increase in assets.

In the below study accounting for financial management is done for Nancy who is willing

to start her own venture of carved wooden ornaments in UK. She is been retired from services

with an amount of £325000 and is willing to start a new business with this amount. The below

report providing full analysis of its financial activities as per the information provided by her.

The report includes break even analysis, income statement and balance sheet, cash flow

statement for monthly as well as yearly and also the sensitivity analysis of its financial

information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Summary of all the assumptions

Assumptions:

In the absence of information, following assumptions have been made:

All the amount which she received from her past services has been invested in this

venture because she was not willing to take loans from bank and financial institutions.

In the below calculation it is been assumed that the in plinths and presentation cases are

expenses of variable in nature for Nancy because these were purchased only for the

purpose of sales to Jeremy.

Plinths and presentation cases are required only for her friend's Jeremy demand.

All the Calculations below are based on per month figures.

It has been Estimated that the 1st month sales through online is 35 units with an average

selling price of £120 per unit and sales to Jeremy throughout the year was 50 units at an

average selling price of £85 per unit.

Online sales and sales to Jeremy has been merged.

As per the market demand, it seen in the trend that the online sales of Carved wooden

ornaments has been increased by 20%.

Nancy approached her financial advisor for her business and asked her financial advisor

to make an estimated project for her business, which stated that she need more amount to

invest other than she received from her past service, therefore, she found it necessary to

borrow £50,000 .

For the purpose of annual calculations, sales are taken as constant. Sales is 35 + 50 i.e. 85

per month throughout the year.

Purchases from clear cut are based on the orders that Nancy get. She purchases only that

much amount of units for which she gets order.

For the purpose of balance sheet, Profit after tax has been considered.

Assumptions:

In the absence of information, following assumptions have been made:

All the amount which she received from her past services has been invested in this

venture because she was not willing to take loans from bank and financial institutions.

In the below calculation it is been assumed that the in plinths and presentation cases are

expenses of variable in nature for Nancy because these were purchased only for the

purpose of sales to Jeremy.

Plinths and presentation cases are required only for her friend's Jeremy demand.

All the Calculations below are based on per month figures.

It has been Estimated that the 1st month sales through online is 35 units with an average

selling price of £120 per unit and sales to Jeremy throughout the year was 50 units at an

average selling price of £85 per unit.

Online sales and sales to Jeremy has been merged.

As per the market demand, it seen in the trend that the online sales of Carved wooden

ornaments has been increased by 20%.

Nancy approached her financial advisor for her business and asked her financial advisor

to make an estimated project for her business, which stated that she need more amount to

invest other than she received from her past service, therefore, she found it necessary to

borrow £50,000 .

For the purpose of annual calculations, sales are taken as constant. Sales is 35 + 50 i.e. 85

per month throughout the year.

Purchases from clear cut are based on the orders that Nancy get. She purchases only that

much amount of units for which she gets order.

For the purpose of balance sheet, Profit after tax has been considered.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

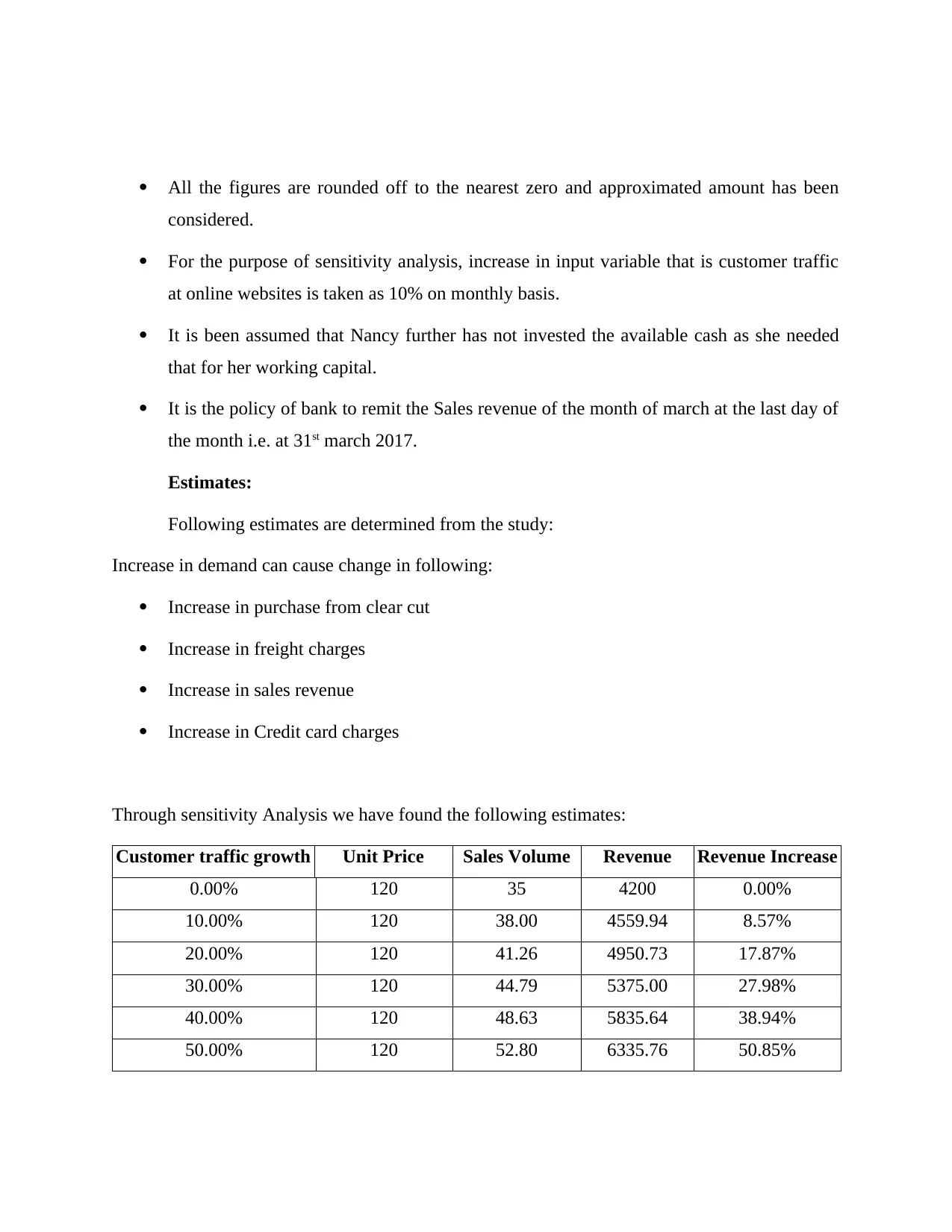

All the figures are rounded off to the nearest zero and approximated amount has been

considered.

For the purpose of sensitivity analysis, increase in input variable that is customer traffic

at online websites is taken as 10% on monthly basis.

It is been assumed that Nancy further has not invested the available cash as she needed

that for her working capital.

It is the policy of bank to remit the Sales revenue of the month of march at the last day of

the month i.e. at 31st march 2017.

Estimates:

Following estimates are determined from the study:

Increase in demand can cause change in following:

Increase in purchase from clear cut

Increase in freight charges

Increase in sales revenue

Increase in Credit card charges

Through sensitivity Analysis we have found the following estimates:

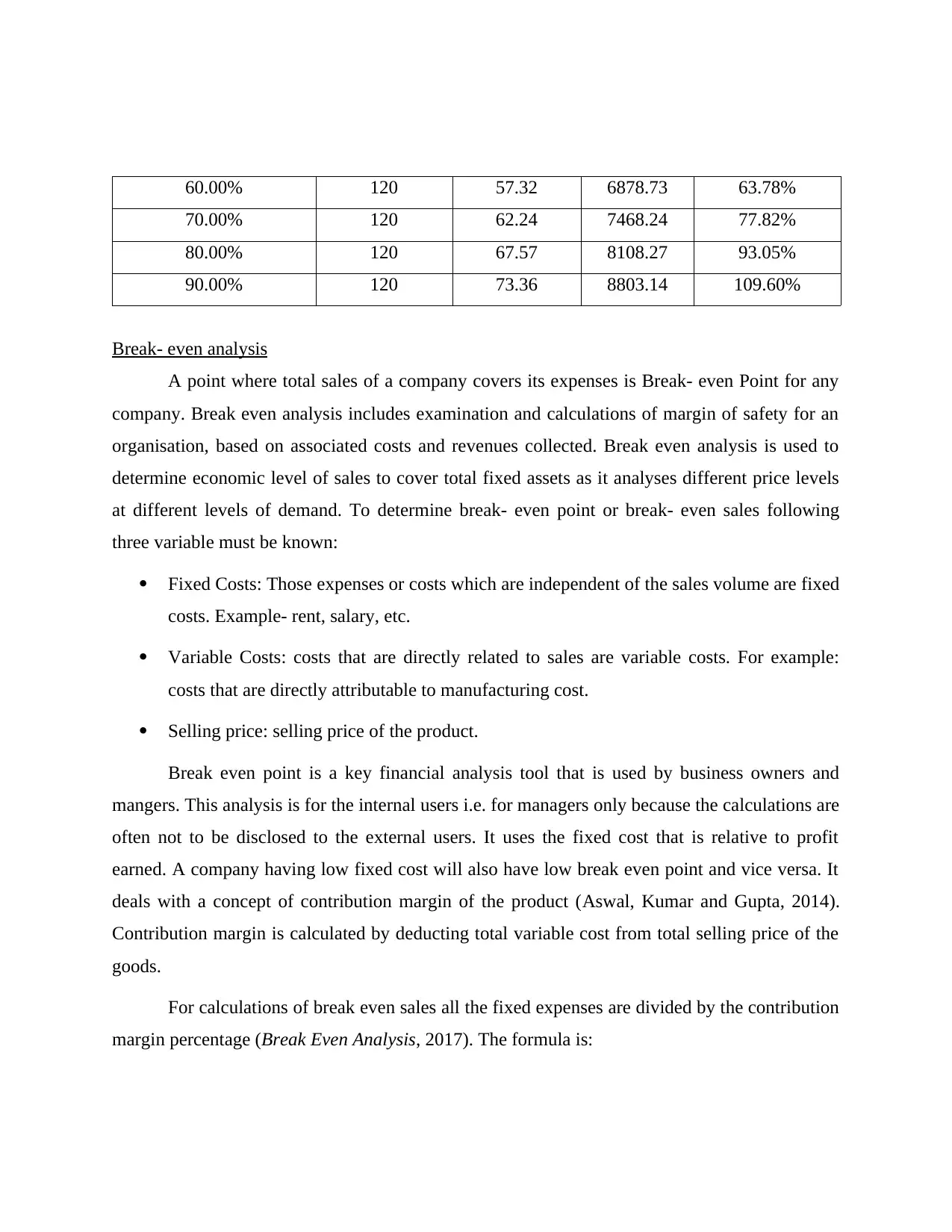

Customer traffic growth Unit Price Sales Volume Revenue Revenue Increase

0.00% 120 35 4200 0.00%

10.00% 120 38.00 4559.94 8.57%

20.00% 120 41.26 4950.73 17.87%

30.00% 120 44.79 5375.00 27.98%

40.00% 120 48.63 5835.64 38.94%

50.00% 120 52.80 6335.76 50.85%

considered.

For the purpose of sensitivity analysis, increase in input variable that is customer traffic

at online websites is taken as 10% on monthly basis.

It is been assumed that Nancy further has not invested the available cash as she needed

that for her working capital.

It is the policy of bank to remit the Sales revenue of the month of march at the last day of

the month i.e. at 31st march 2017.

Estimates:

Following estimates are determined from the study:

Increase in demand can cause change in following:

Increase in purchase from clear cut

Increase in freight charges

Increase in sales revenue

Increase in Credit card charges

Through sensitivity Analysis we have found the following estimates:

Customer traffic growth Unit Price Sales Volume Revenue Revenue Increase

0.00% 120 35 4200 0.00%

10.00% 120 38.00 4559.94 8.57%

20.00% 120 41.26 4950.73 17.87%

30.00% 120 44.79 5375.00 27.98%

40.00% 120 48.63 5835.64 38.94%

50.00% 120 52.80 6335.76 50.85%

60.00% 120 57.32 6878.73 63.78%

70.00% 120 62.24 7468.24 77.82%

80.00% 120 67.57 8108.27 93.05%

90.00% 120 73.36 8803.14 109.60%

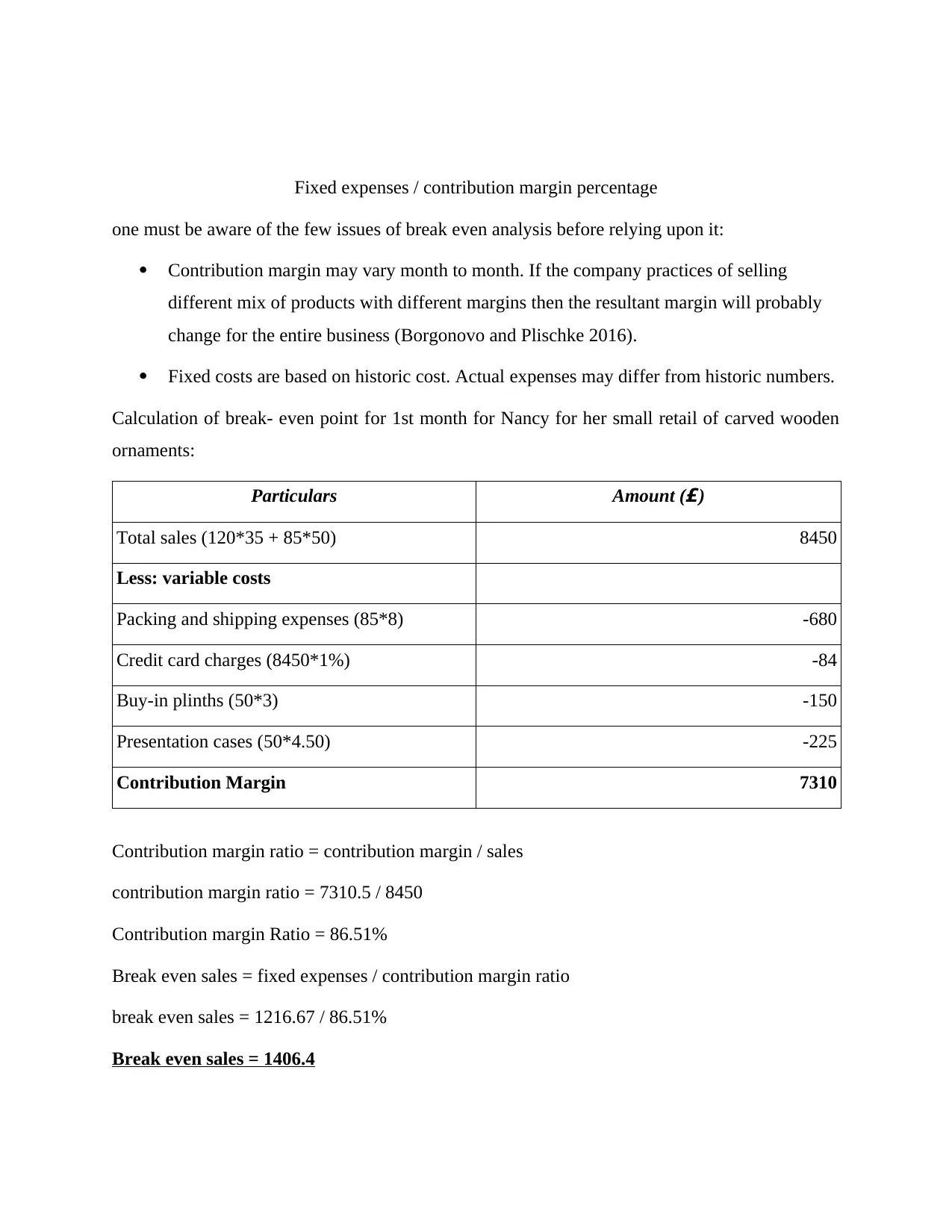

Break- even analysis

A point where total sales of a company covers its expenses is Break- even Point for any

company. Break even analysis includes examination and calculations of margin of safety for an

organisation, based on associated costs and revenues collected. Break even analysis is used to

determine economic level of sales to cover total fixed assets as it analyses different price levels

at different levels of demand. To determine break- even point or break- even sales following

three variable must be known:

Fixed Costs: Those expenses or costs which are independent of the sales volume are fixed

costs. Example- rent, salary, etc.

Variable Costs: costs that are directly related to sales are variable costs. For example:

costs that are directly attributable to manufacturing cost.

Selling price: selling price of the product.

Break even point is a key financial analysis tool that is used by business owners and

mangers. This analysis is for the internal users i.e. for managers only because the calculations are

often not to be disclosed to the external users. It uses the fixed cost that is relative to profit

earned. A company having low fixed cost will also have low break even point and vice versa. It

deals with a concept of contribution margin of the product (Aswal, Kumar and Gupta, 2014).

Contribution margin is calculated by deducting total variable cost from total selling price of the

goods.

For calculations of break even sales all the fixed expenses are divided by the contribution

margin percentage (Break Even Analysis, 2017). The formula is:

70.00% 120 62.24 7468.24 77.82%

80.00% 120 67.57 8108.27 93.05%

90.00% 120 73.36 8803.14 109.60%

Break- even analysis

A point where total sales of a company covers its expenses is Break- even Point for any

company. Break even analysis includes examination and calculations of margin of safety for an

organisation, based on associated costs and revenues collected. Break even analysis is used to

determine economic level of sales to cover total fixed assets as it analyses different price levels

at different levels of demand. To determine break- even point or break- even sales following

three variable must be known:

Fixed Costs: Those expenses or costs which are independent of the sales volume are fixed

costs. Example- rent, salary, etc.

Variable Costs: costs that are directly related to sales are variable costs. For example:

costs that are directly attributable to manufacturing cost.

Selling price: selling price of the product.

Break even point is a key financial analysis tool that is used by business owners and

mangers. This analysis is for the internal users i.e. for managers only because the calculations are

often not to be disclosed to the external users. It uses the fixed cost that is relative to profit

earned. A company having low fixed cost will also have low break even point and vice versa. It

deals with a concept of contribution margin of the product (Aswal, Kumar and Gupta, 2014).

Contribution margin is calculated by deducting total variable cost from total selling price of the

goods.

For calculations of break even sales all the fixed expenses are divided by the contribution

margin percentage (Break Even Analysis, 2017). The formula is:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fixed expenses / contribution margin percentage

one must be aware of the few issues of break even analysis before relying upon it:

Contribution margin may vary month to month. If the company practices of selling

different mix of products with different margins then the resultant margin will probably

change for the entire business (Borgonovo and Plischke 2016).

Fixed costs are based on historic cost. Actual expenses may differ from historic numbers.

Calculation of break- even point for 1st month for Nancy for her small retail of carved wooden

ornaments:

Particulars Amount (£)

Total sales (120*35 + 85*50) 8450

Less: variable costs

Packing and shipping expenses (85*8) -680

Credit card charges (8450*1%) -84

Buy-in plinths (50*3) -150

Presentation cases (50*4.50) -225

Contribution Margin 7310

Contribution margin ratio = contribution margin / sales

contribution margin ratio = 7310.5 / 8450

Contribution margin Ratio = 86.51%

Break even sales = fixed expenses / contribution margin ratio

break even sales = 1216.67 / 86.51%

Break even sales = 1406.4

one must be aware of the few issues of break even analysis before relying upon it:

Contribution margin may vary month to month. If the company practices of selling

different mix of products with different margins then the resultant margin will probably

change for the entire business (Borgonovo and Plischke 2016).

Fixed costs are based on historic cost. Actual expenses may differ from historic numbers.

Calculation of break- even point for 1st month for Nancy for her small retail of carved wooden

ornaments:

Particulars Amount (£)

Total sales (120*35 + 85*50) 8450

Less: variable costs

Packing and shipping expenses (85*8) -680

Credit card charges (8450*1%) -84

Buy-in plinths (50*3) -150

Presentation cases (50*4.50) -225

Contribution Margin 7310

Contribution margin ratio = contribution margin / sales

contribution margin ratio = 7310.5 / 8450

Contribution margin Ratio = 86.51%

Break even sales = fixed expenses / contribution margin ratio

break even sales = 1216.67 / 86.51%

Break even sales = 1406.4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

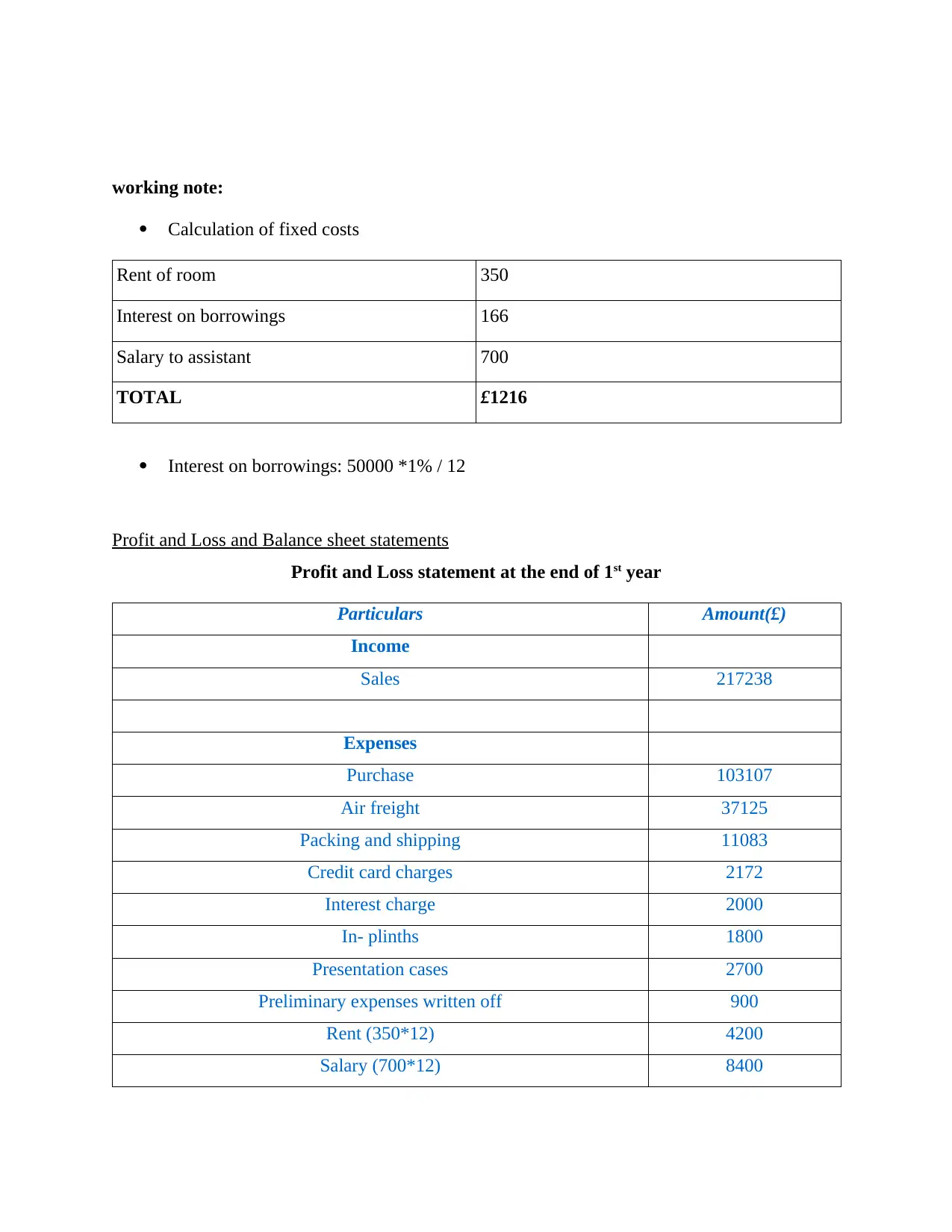

working note:

Calculation of fixed costs

Rent of room 350

Interest on borrowings 166

Salary to assistant 700

TOTAL £1216

Interest on borrowings: 50000 *1% / 12

Profit and Loss and Balance sheet statements

Profit and Loss statement at the end of 1st year

Particulars Amount(£)

Income

Sales 217238

Expenses

Purchase 103107

Air freight 37125

Packing and shipping 11083

Credit card charges 2172

Interest charge 2000

In- plinths 1800

Presentation cases 2700

Preliminary expenses written off 900

Rent (350*12) 4200

Salary (700*12) 8400

Calculation of fixed costs

Rent of room 350

Interest on borrowings 166

Salary to assistant 700

TOTAL £1216

Interest on borrowings: 50000 *1% / 12

Profit and Loss and Balance sheet statements

Profit and Loss statement at the end of 1st year

Particulars Amount(£)

Income

Sales 217238

Expenses

Purchase 103107

Air freight 37125

Packing and shipping 11083

Credit card charges 2172

Interest charge 2000

In- plinths 1800

Presentation cases 2700

Preliminary expenses written off 900

Rent (350*12) 4200

Salary (700*12) 8400

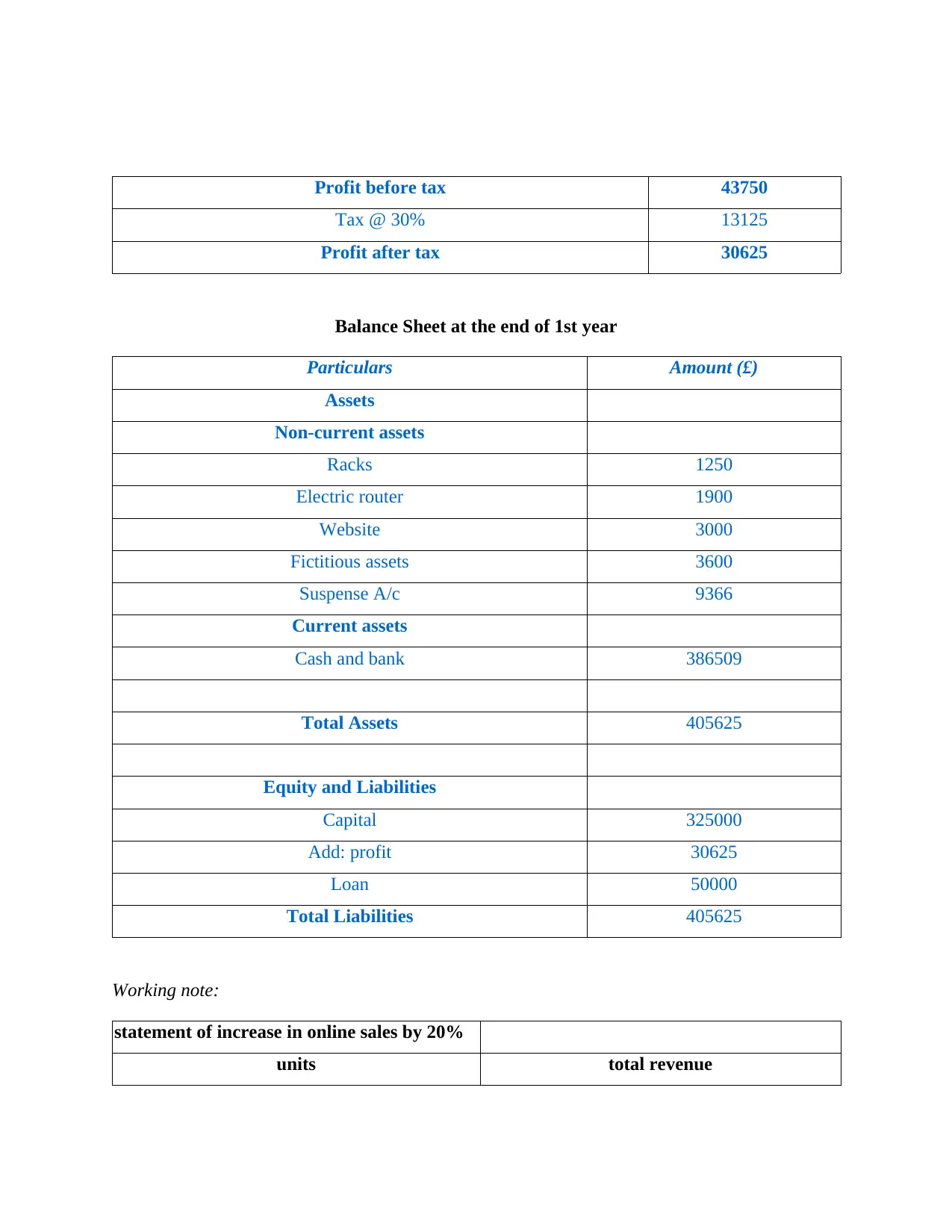

Profit before tax 43750

Tax @ 30% 13125

Profit after tax 30625

Balance Sheet at the end of 1st year

Particulars Amount (£)

Assets

Non-current assets

Racks 1250

Electric router 1900

Website 3000

Fictitious assets 3600

Suspense A/c 9366

Current assets

Cash and bank 386509

Total Assets 405625

Equity and Liabilities

Capital 325000

Add: profit 30625

Loan 50000

Total Liabilities 405625

Working note:

statement of increase in online sales by 20%

units total revenue

Tax @ 30% 13125

Profit after tax 30625

Balance Sheet at the end of 1st year

Particulars Amount (£)

Assets

Non-current assets

Racks 1250

Electric router 1900

Website 3000

Fictitious assets 3600

Suspense A/c 9366

Current assets

Cash and bank 386509

Total Assets 405625

Equity and Liabilities

Capital 325000

Add: profit 30625

Loan 50000

Total Liabilities 405625

Working note:

statement of increase in online sales by 20%

units total revenue

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

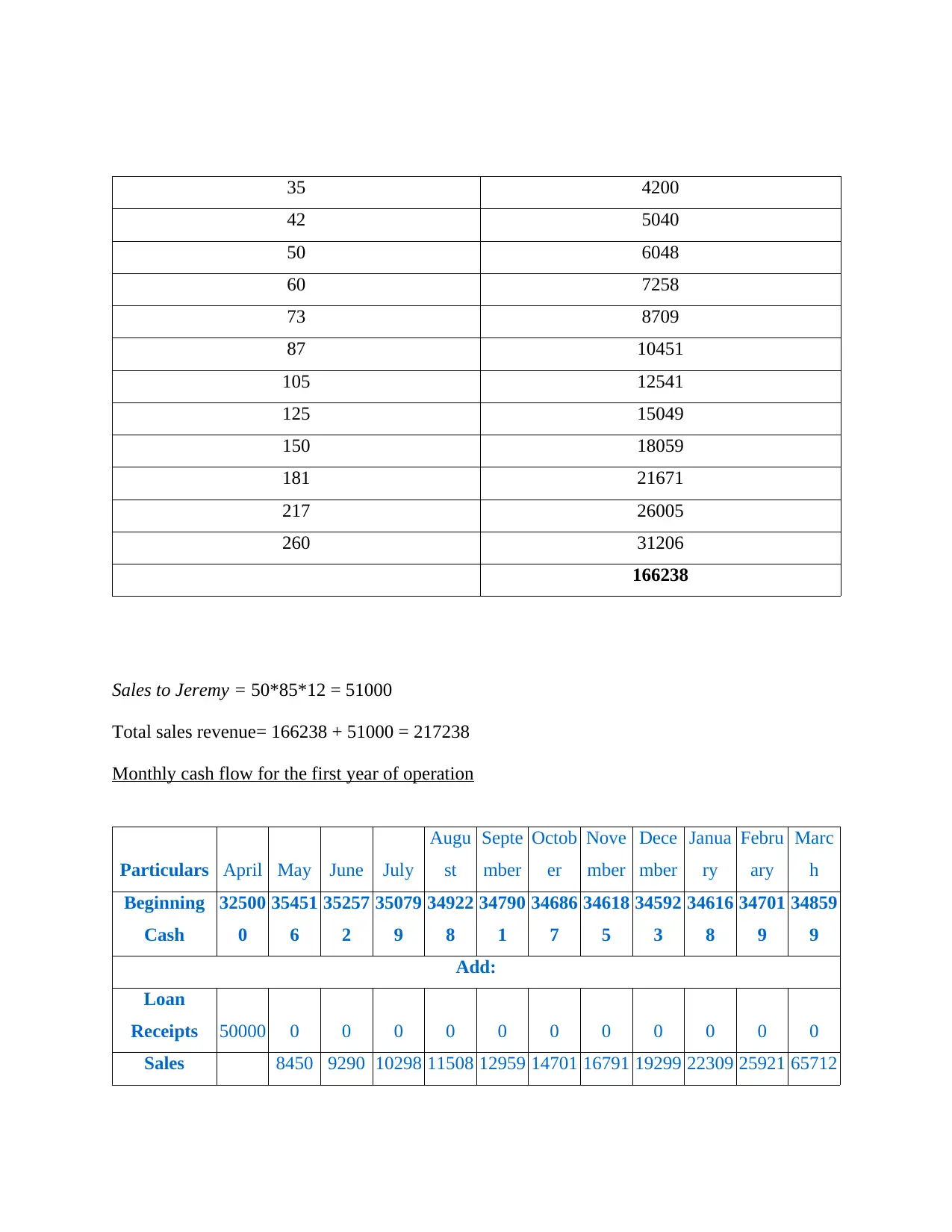

35 4200

42 5040

50 6048

60 7258

73 8709

87 10451

105 12541

125 15049

150 18059

181 21671

217 26005

260 31206

166238

Sales to Jeremy = 50*85*12 = 51000

Total sales revenue= 166238 + 51000 = 217238

Monthly cash flow for the first year of operation

Particulars April May June July

Augu

st

Septe

mber

Octob

er

Nove

mber

Dece

mber

Janua

ry

Febru

ary

Marc

h

Beginning

Cash

32500

0

35451

6

35257

2

35079

9

34922

8

34790

1

34686

7

34618

5

34592

3

34616

8

34701

9

34859

9

Add:

Loan

Receipts 50000 0 0 0 0 0 0 0 0 0 0 0

Sales 8450 9290 10298 11508 12959 14701 16791 19299 22309 25921 65712

42 5040

50 6048

60 7258

73 8709

87 10451

105 12541

125 15049

150 18059

181 21671

217 26005

260 31206

166238

Sales to Jeremy = 50*85*12 = 51000

Total sales revenue= 166238 + 51000 = 217238

Monthly cash flow for the first year of operation

Particulars April May June July

Augu

st

Septe

mber

Octob

er

Nove

mber

Dece

mber

Janua

ry

Febru

ary

Marc

h

Beginning

Cash

32500

0

35451

6

35257

2

35079

9

34922

8

34790

1

34686

7

34618

5

34592

3

34616

8

34701

9

34859

9

Add:

Loan

Receipts 50000 0 0 0 0 0 0 0 0 0 0 0

Sales 8450 9290 10298 11508 12959 14701 16791 19299 22309 25921 65712

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

receipts*

Cash

available

37500

0

36296

6

36186

2

36109

7

36073

6

36086

0

36156

8

36297

6

36522

3

36847

7

37294

1

41431

1

less: disbursements

operation

cost* 1917 1917 1917 1917 1917 1917 1917 1917 1917 1917 1917 1917

Material

purchases* 4414 4778 5214 5738 6366 7120 8024 9110 10413 11976 13852 16103

freight

expenses* 1590 1720 1877 2066 2292 2564 2889 3280 3749 4312 4987 5798

packaging

and

shipping* 280 336 403 484 581 697 836 1003 1204 1445 1734 2080

credit card

expense* 42 50 60 73 87 105 125 150 181 217 260 312

Salary to

assistant 700 700 700 700 700 700 700 700 700 700 700 700

Rent 350 350 350 350 350 350 350 350 350 350 350 350

Loan

interest 167 167 167 167 167 167 167 167 167 167 167 167

purchase

presentation

cases* 225 225 225 225 225 225 225 225 225 225 225 225

purchase

plinths* 150 150 150 150 150 150 150 150 150 150 150 150

automated

electric

router 1900 0 0 0 0 0 0 0 0 0 0 0

Cash

available

37500

0

36296

6

36186

2

36109

7

36073

6

36086

0

36156

8

36297

6

36522

3

36847

7

37294

1

41431

1

less: disbursements

operation

cost* 1917 1917 1917 1917 1917 1917 1917 1917 1917 1917 1917 1917

Material

purchases* 4414 4778 5214 5738 6366 7120 8024 9110 10413 11976 13852 16103

freight

expenses* 1590 1720 1877 2066 2292 2564 2889 3280 3749 4312 4987 5798

packaging

and

shipping* 280 336 403 484 581 697 836 1003 1204 1445 1734 2080

credit card

expense* 42 50 60 73 87 105 125 150 181 217 260 312

Salary to

assistant 700 700 700 700 700 700 700 700 700 700 700 700

Rent 350 350 350 350 350 350 350 350 350 350 350 350

Loan

interest 167 167 167 167 167 167 167 167 167 167 167 167

purchase

presentation

cases* 225 225 225 225 225 225 225 225 225 225 225 225

purchase

plinths* 150 150 150 150 150 150 150 150 150 150 150 150

automated

electric

router 1900 0 0 0 0 0 0 0 0 0 0 0

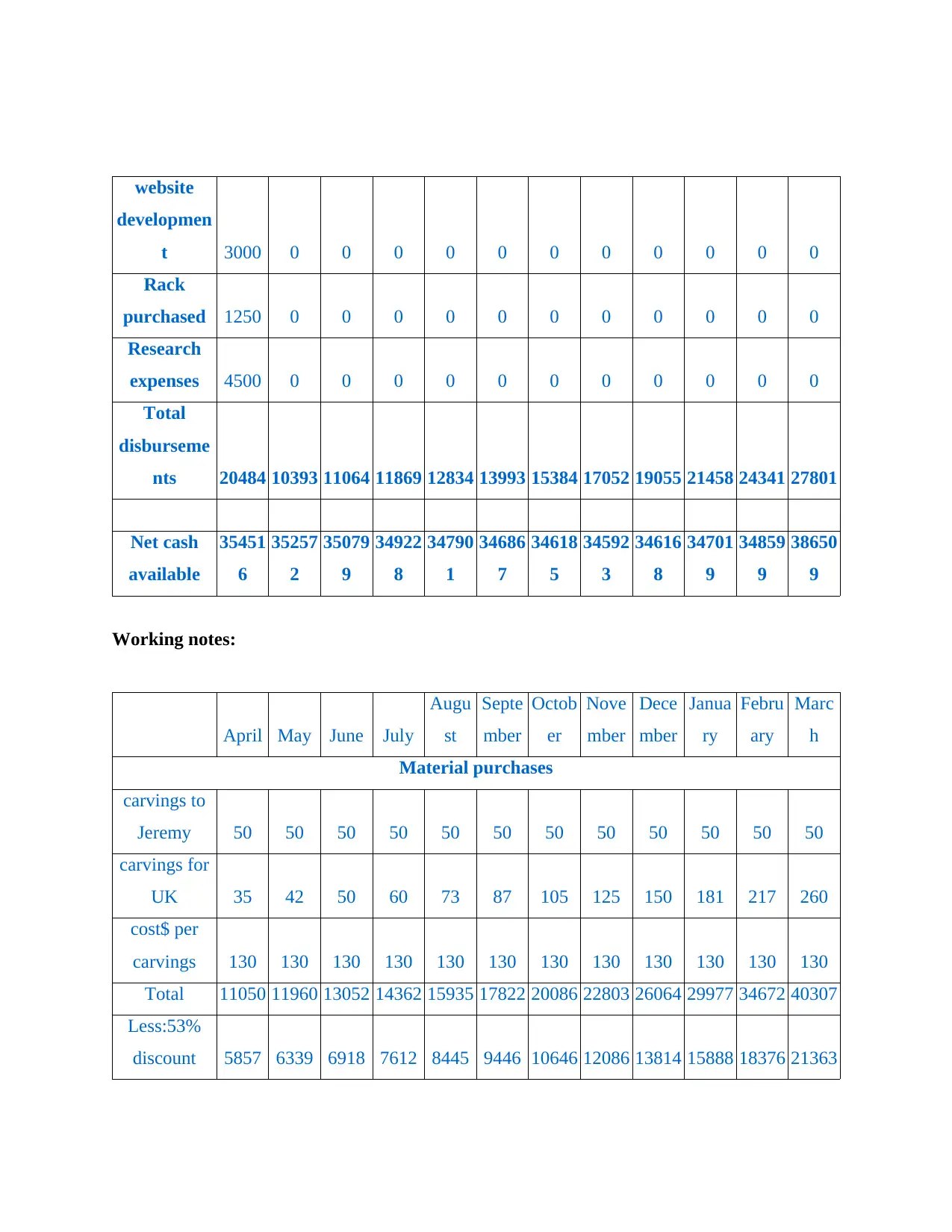

website

developmen

t 3000 0 0 0 0 0 0 0 0 0 0 0

Rack

purchased 1250 0 0 0 0 0 0 0 0 0 0 0

Research

expenses 4500 0 0 0 0 0 0 0 0 0 0 0

Total

disburseme

nts 20484 10393 11064 11869 12834 13993 15384 17052 19055 21458 24341 27801

Net cash

available

35451

6

35257

2

35079

9

34922

8

34790

1

34686

7

34618

5

34592

3

34616

8

34701

9

34859

9

38650

9

Working notes:

April May June July

Augu

st

Septe

mber

Octob

er

Nove

mber

Dece

mber

Janua

ry

Febru

ary

Marc

h

Material purchases

carvings to

Jeremy 50 50 50 50 50 50 50 50 50 50 50 50

carvings for

UK 35 42 50 60 73 87 105 125 150 181 217 260

cost$ per

carvings 130 130 130 130 130 130 130 130 130 130 130 130

Total 11050 11960 13052 14362 15935 17822 20086 22803 26064 29977 34672 40307

Less:53%

discount 5857 6339 6918 7612 8445 9446 10646 12086 13814 15888 18376 21363

developmen

t 3000 0 0 0 0 0 0 0 0 0 0 0

Rack

purchased 1250 0 0 0 0 0 0 0 0 0 0 0

Research

expenses 4500 0 0 0 0 0 0 0 0 0 0 0

Total

disburseme

nts 20484 10393 11064 11869 12834 13993 15384 17052 19055 21458 24341 27801

Net cash

available

35451

6

35257

2

35079

9

34922

8

34790

1

34686

7

34618

5

34592

3

34616

8

34701

9

34859

9

38650

9

Working notes:

April May June July

Augu

st

Septe

mber

Octob

er

Nove

mber

Dece

mber

Janua

ry

Febru

ary

Marc

h

Material purchases

carvings to

Jeremy 50 50 50 50 50 50 50 50 50 50 50 50

carvings for

UK 35 42 50 60 73 87 105 125 150 181 217 260

cost$ per

carvings 130 130 130 130 130 130 130 130 130 130 130 130

Total 11050 11960 13052 14362 15935 17822 20086 22803 26064 29977 34672 40307

Less:53%

discount 5857 6339 6918 7612 8445 9446 10646 12086 13814 15888 18376 21363

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.