Financial Management Report: Investment Appraisal Techniques

VerifiedAdded on 2020/06/03

|13

|3732

|52

Report

AI Summary

This report provides a detailed analysis of financial management, focusing on valuation techniques and investment appraisal methods. It begins with an introduction to financial management, outlining key processes like planning, organizing, and controlling financial activities. The report then delves into mergers and acquisitions, specifically valuing Trojan plc using the price/earnings ratio, dividend valuation method, and discounted cash flow method. Each method is explained with calculations and working notes. The report also discusses the limitations of each valuation technique. Furthermore, the report examines investment appraisal techniques, including the payback period, accounting rate of return, net present value, and internal rate of return, evaluating their benefits and limitations. The report concludes by summarizing the key findings and implications of the analysis.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Question 2 : Mergers and Acquisitions............................................................................................1

a) Valuation of Trojan plc by using Price/earning ratio :............................................................1

b) Valuation of Trojan plc by using Dividend valuation method :.............................................2

c) Valuation of Trojan plc by using Discounted cash flow method :..........................................3

d) Problems related to the various techniques that have been used above :................................4

Question 3 .......................................................................................................................................6

1. (a) The payback period :.........................................................................................................6

b) the accounting rate of return...................................................................................................7

C & d ) The net present value and Internal rate of return...........................................................7

2. Evaluation of the benefits and limitations of each investment appraisal technique................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

Question 2 : Mergers and Acquisitions............................................................................................1

a) Valuation of Trojan plc by using Price/earning ratio :............................................................1

b) Valuation of Trojan plc by using Dividend valuation method :.............................................2

c) Valuation of Trojan plc by using Discounted cash flow method :..........................................3

d) Problems related to the various techniques that have been used above :................................4

Question 3 .......................................................................................................................................6

1. (a) The payback period :.........................................................................................................6

b) the accounting rate of return...................................................................................................7

C & d ) The net present value and Internal rate of return...........................................................7

2. Evaluation of the benefits and limitations of each investment appraisal technique................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Financial management is the process in which various processes such as planning,

directing, organizing and controlling are performed in order to manage the financial activities of

a business. Financial activities include the procurement and utilization of the finance for the

company (Agard, 2007). This is done so that the funds can be utilised in the most effective and

efficient manner which will be beneficial in achieving the objectives of the company and all

these functions are performed by the top management of the company. In this various decisions

are required to be taken which include financial, investment and dividend decisions. In this

report the investment aspect will be discussed in relation to acquisition of fixed asset and another

entity. For this purpose there are various techniques that can be used and all those methods

together with their advantages and disadvantages are described here under.

Question 2: Mergers and Acquisitions

a) Valuation of Trojan plc by using Price/earnings ratio

Price earnings ratio which is also known as price to earnings ratio is the ratio that

considers the market prospects and by this the market value of the stock is calculated and this is

done by comparing the market price of the share with its relative earning. In this it can be said

that this ratio will represent the value of the stock that market is ready to pay on the basis of the

earning that are made in the current situation (Allen, 2012). This method is used while making an

investment to evaluate the fair market value that should be present on the basis of future earnings

per share that have been predicted. If the earnings that are made by any company are high than

that company will be willing to pay its investors a dividend at higher rate. With the help of this

ratio it will be possible for the investors to identify that what is the amount that is required to

paid by them on the basis of the earnings that are currently made by it and it is the reason due to

which this ratio is called as earnings multiple or price multiple. The manner in which this ratio

will be calculated is by dividing the market price per share with the earnings per share. The

formula for this is:

Price earnings ratio: Market price per share

Earnings per share

This can be better understood with the given problem.

Price earnings ratio = 2.05 / 0.275

= 7.4545

1

Financial management is the process in which various processes such as planning,

directing, organizing and controlling are performed in order to manage the financial activities of

a business. Financial activities include the procurement and utilization of the finance for the

company (Agard, 2007). This is done so that the funds can be utilised in the most effective and

efficient manner which will be beneficial in achieving the objectives of the company and all

these functions are performed by the top management of the company. In this various decisions

are required to be taken which include financial, investment and dividend decisions. In this

report the investment aspect will be discussed in relation to acquisition of fixed asset and another

entity. For this purpose there are various techniques that can be used and all those methods

together with their advantages and disadvantages are described here under.

Question 2: Mergers and Acquisitions

a) Valuation of Trojan plc by using Price/earnings ratio

Price earnings ratio which is also known as price to earnings ratio is the ratio that

considers the market prospects and by this the market value of the stock is calculated and this is

done by comparing the market price of the share with its relative earning. In this it can be said

that this ratio will represent the value of the stock that market is ready to pay on the basis of the

earning that are made in the current situation (Allen, 2012). This method is used while making an

investment to evaluate the fair market value that should be present on the basis of future earnings

per share that have been predicted. If the earnings that are made by any company are high than

that company will be willing to pay its investors a dividend at higher rate. With the help of this

ratio it will be possible for the investors to identify that what is the amount that is required to

paid by them on the basis of the earnings that are currently made by it and it is the reason due to

which this ratio is called as earnings multiple or price multiple. The manner in which this ratio

will be calculated is by dividing the market price per share with the earnings per share. The

formula for this is:

Price earnings ratio: Market price per share

Earnings per share

This can be better understood with the given problem.

Price earnings ratio = 2.05 / 0.275

= 7.4545

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Value of Trojan Plc = Price earnings ratio * earnings made during year

= 7.4545 * 40.4

= £ 301.1618 m

Working Notes:

1. Calculation of Earnings per share :

Earnings per share = Total earnings / Number of shares

= 40.4 / 147

= £ 0.275

2. Calculation of market price per share :

Market price per share = £ 2.05

b) Valuation of Trojan plc by using Dividend valuation method

Dividend valuation is one of another method that is used by the investors for the

valuation of stock. In this method all the future dividends are used in order to predict the share

value. In this it is assumed that the sole purpose for which the investment is made is to receive

the dividends (Allio and Randall, 2010). There are lot of more other assumptions that are made

in this method while calculating the value. For the purpose of using this method it will be

required that firstly the approximate future dividends will be ascertained and after that the

discount rate for the future period will be determined which will be used to calculate the present

value. If there is any growth that is found than that will also be used in the calculation process.

The formula that will be used to calculate the value by using this model will be:

P0 = D1 / (Ke – G)

Where,

P0 = current value of share

D1 = dividend at the year end

Ke = cost of equity

G = Growth rate

Below is given the calculation of value by using this method:

P0 = 13.26 / (11.6 % - 2 % )

= 13.26 / 9.6 %

= £ 138.125 m

2

= 7.4545 * 40.4

= £ 301.1618 m

Working Notes:

1. Calculation of Earnings per share :

Earnings per share = Total earnings / Number of shares

= 40.4 / 147

= £ 0.275

2. Calculation of market price per share :

Market price per share = £ 2.05

b) Valuation of Trojan plc by using Dividend valuation method

Dividend valuation is one of another method that is used by the investors for the

valuation of stock. In this method all the future dividends are used in order to predict the share

value. In this it is assumed that the sole purpose for which the investment is made is to receive

the dividends (Allio and Randall, 2010). There are lot of more other assumptions that are made

in this method while calculating the value. For the purpose of using this method it will be

required that firstly the approximate future dividends will be ascertained and after that the

discount rate for the future period will be determined which will be used to calculate the present

value. If there is any growth that is found than that will also be used in the calculation process.

The formula that will be used to calculate the value by using this model will be:

P0 = D1 / (Ke – G)

Where,

P0 = current value of share

D1 = dividend at the year end

Ke = cost of equity

G = Growth rate

Below is given the calculation of value by using this method:

P0 = 13.26 / (11.6 % - 2 % )

= 13.26 / 9.6 %

= £ 138.125 m

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Working Notes:

1. Calculation of D1:

D1 = current dividend + growth rate

= 13 + 2%

= 13 + 0.26

= 13.26 p

2. Calculation of Ke :

Ke = Rf + Beta (Rm – Rf)

where,

Rf = risk free rate of return

Rm = market rate of return

Ke = 5 + 1.1 (11 – 5)

Ke = 5 + 1.1 * 6

Ke = 5 + 6.6

Ke = 11.6 %

c) Valuation of Trojan plc by using discounted cash flow method

Discounted cash flow method is the method in which value of any project or investment

can be carried out by using the time value of money as a concept. In this method all the cash

flows that will be arising in the future are estimated and then on the basis of the cost of capital

the present value of all the cash flows will be calculated (Araujo, Finch and Kjellberg, 2010).

The aggregate value of all the present values will be taken to be the value of the stock. In this

method it will be necessary to ascertain that whether the cash flows will be arising on continuous

basis and if it is, than the growth rate will also be required to be taken into consideration. The

formula that will be used in this will be:

Discounted present value = future value / (Ko – g)

= 4.437 / (9.63 % - 2 %)

= 4.437 / 7.63 %

= 58.15

Value of Trojan = discounted present value + value of asset sold

= 58.15 + 21

= £ 79.15 m

3

1. Calculation of D1:

D1 = current dividend + growth rate

= 13 + 2%

= 13 + 0.26

= 13.26 p

2. Calculation of Ke :

Ke = Rf + Beta (Rm – Rf)

where,

Rf = risk free rate of return

Rm = market rate of return

Ke = 5 + 1.1 (11 – 5)

Ke = 5 + 1.1 * 6

Ke = 5 + 6.6

Ke = 11.6 %

c) Valuation of Trojan plc by using discounted cash flow method

Discounted cash flow method is the method in which value of any project or investment

can be carried out by using the time value of money as a concept. In this method all the cash

flows that will be arising in the future are estimated and then on the basis of the cost of capital

the present value of all the cash flows will be calculated (Araujo, Finch and Kjellberg, 2010).

The aggregate value of all the present values will be taken to be the value of the stock. In this

method it will be necessary to ascertain that whether the cash flows will be arising on continuous

basis and if it is, than the growth rate will also be required to be taken into consideration. The

formula that will be used in this will be:

Discounted present value = future value / (Ko – g)

= 4.437 / (9.63 % - 2 %)

= 4.437 / 7.63 %

= 58.15

Value of Trojan = discounted present value + value of asset sold

= 58.15 + 21

= £ 79.15 m

3

Working notes:

1. Calculation of Ko :

Ko = (equity * cost of equity) + (debt * cost of debt)/capital employed

Cost of debt = interest rate (1 – tax rate)

= 7 (1 - .20)

= 5.6 %

Ko = (147 * 11.6) + (72 * 5.6)/219

= 1705.2 + 403.2 /219 *100

= 2108.4 / 219

= 9.63 %

2. Calculation of future value :

Future value = Synergy benefits + growth

= 4.35 + 2 %

= 4.35 + 0.087

= 4.437

d) Problems related to the various techniques that have been used above

There are various valuation methods that can be used in order to calculate the value of the

company but there are certain problems that will be faced in those methods (Bamford and

Forrester, 2015). It is necessary for the Aztec to have an understanding about all those problems

so that the method that will be best will have to be used in order to calculate the value of trojan

plc. Below are given the limitations associated with each method:

Price earnings ratio: This is the simplest tool that can be used for the purpose of

valuation of stock. But a part from it there are certain problems that are associated with

this method which are described below :

Short term market prices can be erratic: The prices in the short term are affected by

the rumours and expectations and as a result of it price earnings ratio that will be

calculated will not be considered to be appropriate. To deal with this problem it will be

required that the information that will be used in the calculation of the ratios is related to

period of time and not for any single year.

Frequent management of reported earnings: It is known that if the reported earnings

will be consistent tan the ratio will be arrived at higher level and if the earnings will be

4

1. Calculation of Ko :

Ko = (equity * cost of equity) + (debt * cost of debt)/capital employed

Cost of debt = interest rate (1 – tax rate)

= 7 (1 - .20)

= 5.6 %

Ko = (147 * 11.6) + (72 * 5.6)/219

= 1705.2 + 403.2 /219 *100

= 2108.4 / 219

= 9.63 %

2. Calculation of future value :

Future value = Synergy benefits + growth

= 4.35 + 2 %

= 4.35 + 0.087

= 4.437

d) Problems related to the various techniques that have been used above

There are various valuation methods that can be used in order to calculate the value of the

company but there are certain problems that will be faced in those methods (Bamford and

Forrester, 2015). It is necessary for the Aztec to have an understanding about all those problems

so that the method that will be best will have to be used in order to calculate the value of trojan

plc. Below are given the limitations associated with each method:

Price earnings ratio: This is the simplest tool that can be used for the purpose of

valuation of stock. But a part from it there are certain problems that are associated with

this method which are described below :

Short term market prices can be erratic: The prices in the short term are affected by

the rumours and expectations and as a result of it price earnings ratio that will be

calculated will not be considered to be appropriate. To deal with this problem it will be

required that the information that will be used in the calculation of the ratios is related to

period of time and not for any single year.

Frequent management of reported earnings: It is known that if the reported earnings

will be consistent tan the ratio will be arrived at higher level and if the earnings will be

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

uncertain than it will not be possible (Bolton, 2013). Due to this reason it is required that

the earnings should be maintained on consistent basis and this can be done by using such

accounting decisions that will help them in meeting the expectations of the investors.

High growth rates: High growth will also be problem as with this more number of the

competitors will be attracted that will be harmful for the industry as by it the margin will

be reduced (Eom, 2012). The high rate will not be maintained for long period of time as

when the earnings will decline, the price of the stock will also fall along with it.

Impact of debt is not considered: Major disadvantage of using this problem is that in

this only the equity component is considered while a company is formed by using both

the equity and debt so it is important that both aspects should be covered which is not

followed in this method.

Dividend valuation method: There are various problems that are associated with this

method and that are firstly in this method it is assumed that the investment are made with

the intention to earn dividend but this not the reality as all the investors have different

reasons and all do not make the investment with this intention only (Craighead and

Meredith, 2008). It is difficult to forecast the dividend as there is no certainty in this

context and this is because the dividends that are paid by the company are not fixed and

company can pay any amount. This method will not be possible to be used in those cases

where there is no dividend that is being paid in the current position and nor there are any

future expectations in this regard.

Discounted cash flow method: In this method all the cash flows that will be arising in

the future are brought at the present value by using the appropriate discount rate (Chary,

2009). But the major problem that is faced in this are that the discount rate that is used is

based on the market and that keeps on changing so there is no certainty and as in this it is

considered that the growth will be consistent in the future period but it is not possible in

real terms as growth keeps on changing.

According to the description that is mentioned above it can be ascertained that there are some

or the other problem in each method but then also in comparison to others the discounted cash

method is most appropriate. So, it will be good if Azetec uses this method for the valuation

purpose.

5

the earnings should be maintained on consistent basis and this can be done by using such

accounting decisions that will help them in meeting the expectations of the investors.

High growth rates: High growth will also be problem as with this more number of the

competitors will be attracted that will be harmful for the industry as by it the margin will

be reduced (Eom, 2012). The high rate will not be maintained for long period of time as

when the earnings will decline, the price of the stock will also fall along with it.

Impact of debt is not considered: Major disadvantage of using this problem is that in

this only the equity component is considered while a company is formed by using both

the equity and debt so it is important that both aspects should be covered which is not

followed in this method.

Dividend valuation method: There are various problems that are associated with this

method and that are firstly in this method it is assumed that the investment are made with

the intention to earn dividend but this not the reality as all the investors have different

reasons and all do not make the investment with this intention only (Craighead and

Meredith, 2008). It is difficult to forecast the dividend as there is no certainty in this

context and this is because the dividends that are paid by the company are not fixed and

company can pay any amount. This method will not be possible to be used in those cases

where there is no dividend that is being paid in the current position and nor there are any

future expectations in this regard.

Discounted cash flow method: In this method all the cash flows that will be arising in

the future are brought at the present value by using the appropriate discount rate (Chary,

2009). But the major problem that is faced in this are that the discount rate that is used is

based on the market and that keeps on changing so there is no certainty and as in this it is

considered that the growth will be consistent in the future period but it is not possible in

real terms as growth keeps on changing.

According to the description that is mentioned above it can be ascertained that there are some

or the other problem in each method but then also in comparison to others the discounted cash

method is most appropriate. So, it will be good if Azetec uses this method for the valuation

purpose.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

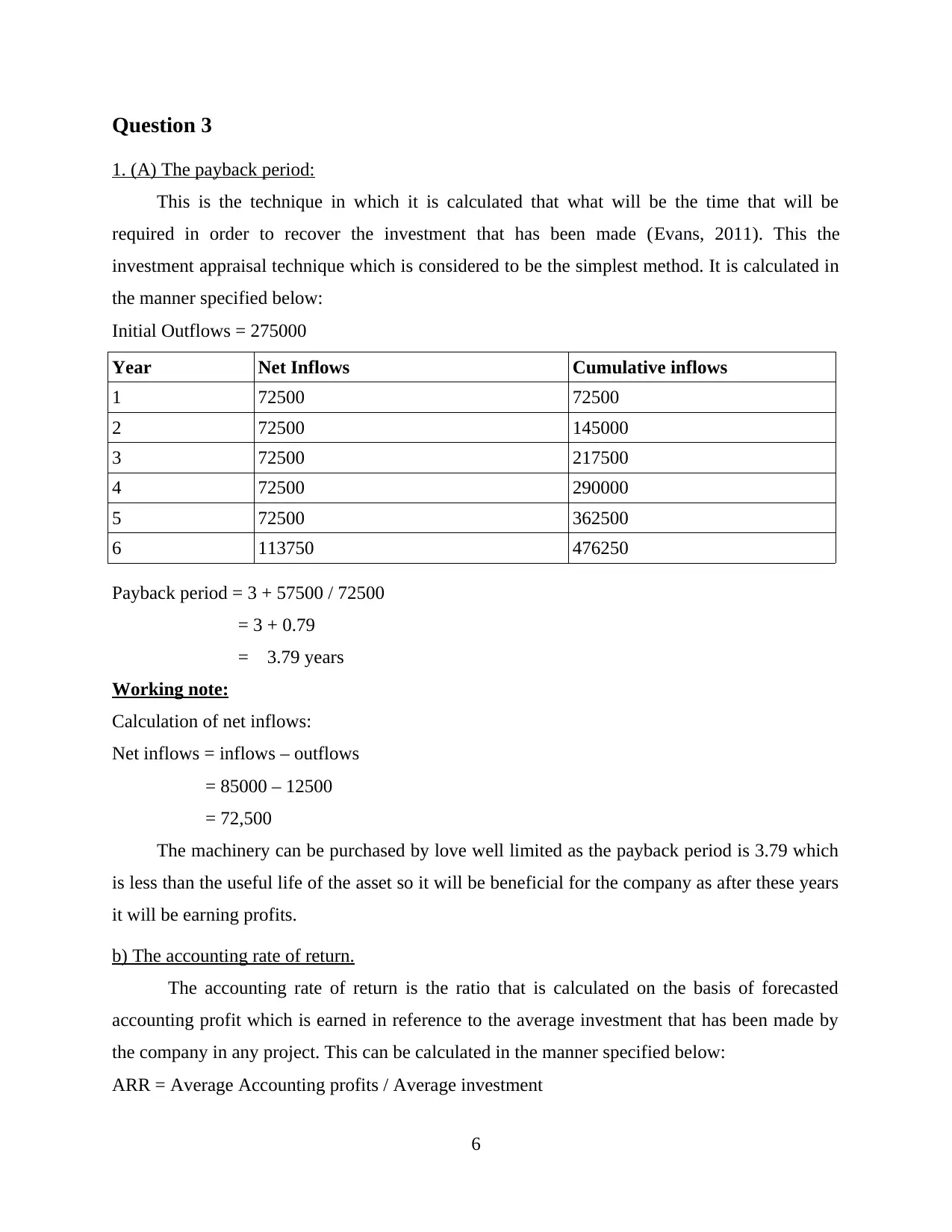

Question 3

1. (A) The payback period:

This is the technique in which it is calculated that what will be the time that will be

required in order to recover the investment that has been made (Evans, 2011). This the

investment appraisal technique which is considered to be the simplest method. It is calculated in

the manner specified below:

Initial Outflows = 275000

Year Net Inflows Cumulative inflows

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 113750 476250

Payback period = 3 + 57500 / 72500

= 3 + 0.79

= 3.79 years

Working note:

Calculation of net inflows:

Net inflows = inflows – outflows

= 85000 – 12500

= 72,500

The machinery can be purchased by love well limited as the payback period is 3.79 which

is less than the useful life of the asset so it will be beneficial for the company as after these years

it will be earning profits.

b) The accounting rate of return.

The accounting rate of return is the ratio that is calculated on the basis of forecasted

accounting profit which is earned in reference to the average investment that has been made by

the company in any project. This can be calculated in the manner specified below:

ARR = Average Accounting profits / Average investment

6

1. (A) The payback period:

This is the technique in which it is calculated that what will be the time that will be

required in order to recover the investment that has been made (Evans, 2011). This the

investment appraisal technique which is considered to be the simplest method. It is calculated in

the manner specified below:

Initial Outflows = 275000

Year Net Inflows Cumulative inflows

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 113750 476250

Payback period = 3 + 57500 / 72500

= 3 + 0.79

= 3.79 years

Working note:

Calculation of net inflows:

Net inflows = inflows – outflows

= 85000 – 12500

= 72,500

The machinery can be purchased by love well limited as the payback period is 3.79 which

is less than the useful life of the asset so it will be beneficial for the company as after these years

it will be earning profits.

b) The accounting rate of return.

The accounting rate of return is the ratio that is calculated on the basis of forecasted

accounting profit which is earned in reference to the average investment that has been made by

the company in any project. This can be calculated in the manner specified below:

ARR = Average Accounting profits / Average investment

6

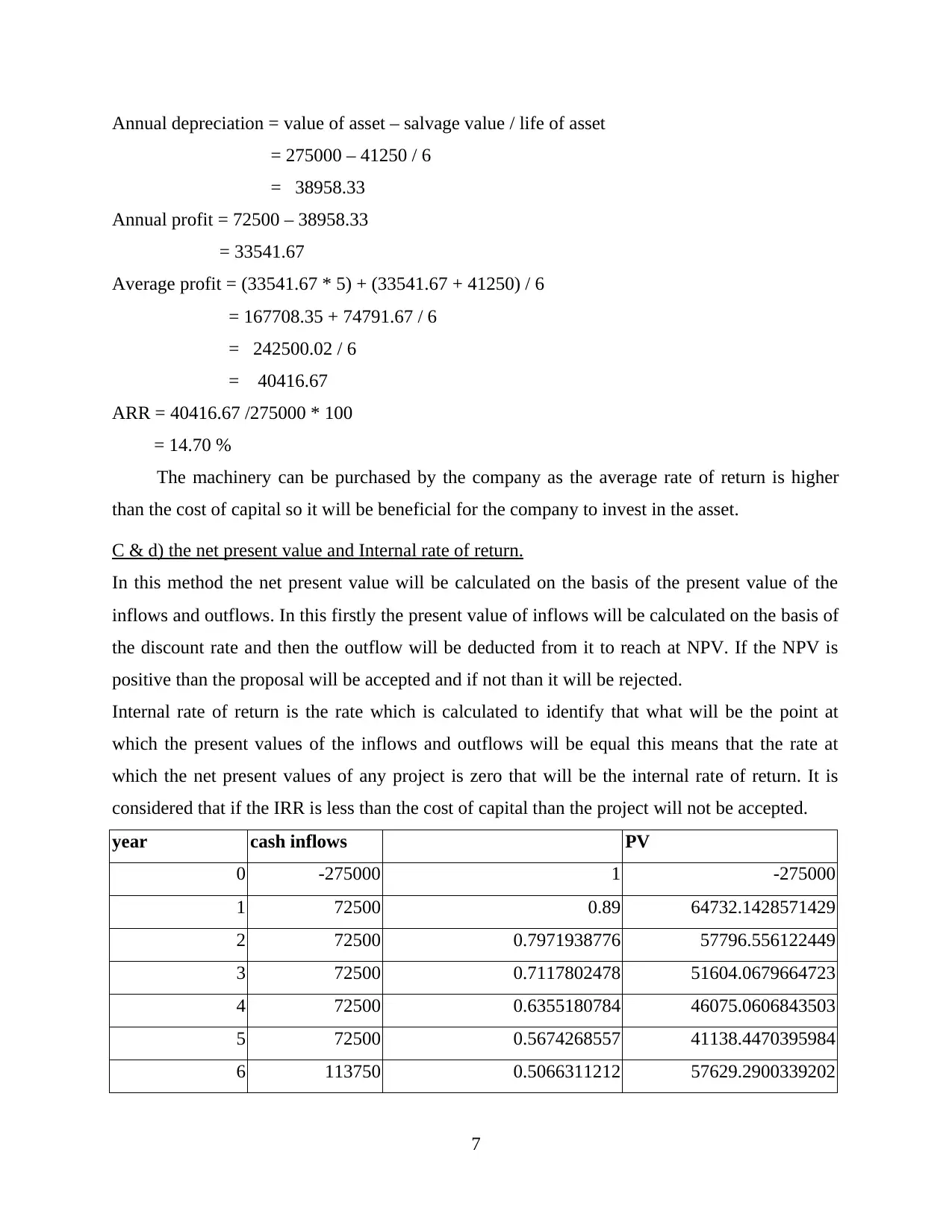

Annual depreciation = value of asset – salvage value / life of asset

= 275000 – 41250 / 6

= 38958.33

Annual profit = 72500 – 38958.33

= 33541.67

Average profit = (33541.67 * 5) + (33541.67 + 41250) / 6

= 167708.35 + 74791.67 / 6

= 242500.02 / 6

= 40416.67

ARR = 40416.67 /275000 * 100

= 14.70 %

The machinery can be purchased by the company as the average rate of return is higher

than the cost of capital so it will be beneficial for the company to invest in the asset.

C & d) the net present value and Internal rate of return.

In this method the net present value will be calculated on the basis of the present value of the

inflows and outflows. In this firstly the present value of inflows will be calculated on the basis of

the discount rate and then the outflow will be deducted from it to reach at NPV. If the NPV is

positive than the proposal will be accepted and if not than it will be rejected.

Internal rate of return is the rate which is calculated to identify that what will be the point at

which the present values of the inflows and outflows will be equal this means that the rate at

which the net present values of any project is zero that will be the internal rate of return. It is

considered that if the IRR is less than the cost of capital than the project will not be accepted.

year cash inflows PV

0 -275000 1 -275000

1 72500 0.89 64732.1428571429

2 72500 0.7971938776 57796.556122449

3 72500 0.7117802478 51604.0679664723

4 72500 0.6355180784 46075.0606843503

5 72500 0.5674268557 41138.4470395984

6 113750 0.5066311212 57629.2900339202

7

= 275000 – 41250 / 6

= 38958.33

Annual profit = 72500 – 38958.33

= 33541.67

Average profit = (33541.67 * 5) + (33541.67 + 41250) / 6

= 167708.35 + 74791.67 / 6

= 242500.02 / 6

= 40416.67

ARR = 40416.67 /275000 * 100

= 14.70 %

The machinery can be purchased by the company as the average rate of return is higher

than the cost of capital so it will be beneficial for the company to invest in the asset.

C & d) the net present value and Internal rate of return.

In this method the net present value will be calculated on the basis of the present value of the

inflows and outflows. In this firstly the present value of inflows will be calculated on the basis of

the discount rate and then the outflow will be deducted from it to reach at NPV. If the NPV is

positive than the proposal will be accepted and if not than it will be rejected.

Internal rate of return is the rate which is calculated to identify that what will be the point at

which the present values of the inflows and outflows will be equal this means that the rate at

which the net present values of any project is zero that will be the internal rate of return. It is

considered that if the IRR is less than the cost of capital than the project will not be accepted.

year cash inflows PV

0 -275000 1 -275000

1 72500 0.89 64732.1428571429

2 72500 0.7971938776 57796.556122449

3 72500 0.7117802478 51604.0679664723

4 72500 0.6355180784 46075.0606843503

5 72500 0.5674268557 41138.4470395984

6 113750 0.5066311212 57629.2900339202

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

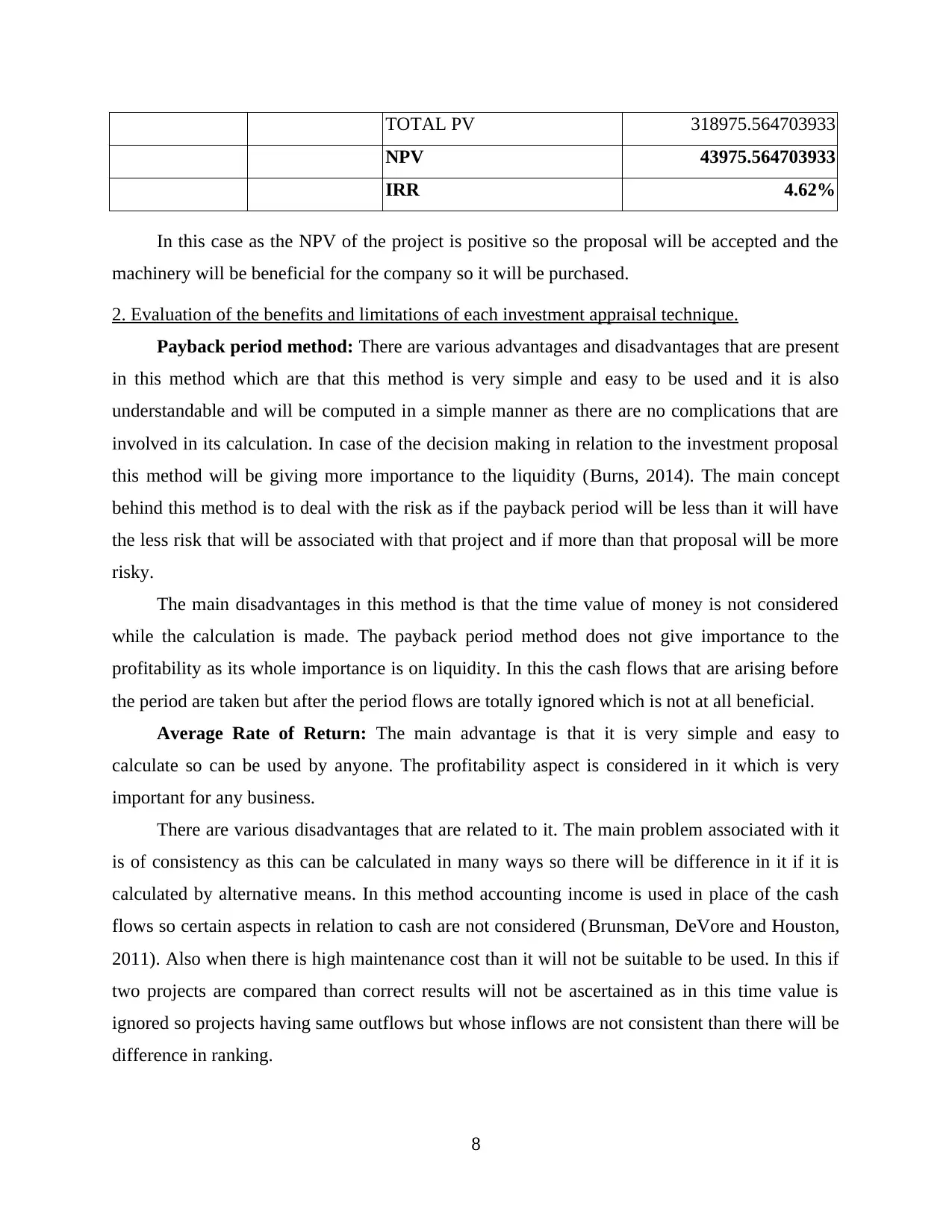

TOTAL PV 318975.564703933

NPV 43975.564703933

IRR 4.62%

In this case as the NPV of the project is positive so the proposal will be accepted and the

machinery will be beneficial for the company so it will be purchased.

2. Evaluation of the benefits and limitations of each investment appraisal technique.

Payback period method: There are various advantages and disadvantages that are present

in this method which are that this method is very simple and easy to be used and it is also

understandable and will be computed in a simple manner as there are no complications that are

involved in its calculation. In case of the decision making in relation to the investment proposal

this method will be giving more importance to the liquidity (Burns, 2014). The main concept

behind this method is to deal with the risk as if the payback period will be less than it will have

the less risk that will be associated with that project and if more than that proposal will be more

risky.

The main disadvantages in this method is that the time value of money is not considered

while the calculation is made. The payback period method does not give importance to the

profitability as its whole importance is on liquidity. In this the cash flows that are arising before

the period are taken but after the period flows are totally ignored which is not at all beneficial.

Average Rate of Return: The main advantage is that it is very simple and easy to

calculate so can be used by anyone. The profitability aspect is considered in it which is very

important for any business.

There are various disadvantages that are related to it. The main problem associated with it

is of consistency as this can be calculated in many ways so there will be difference in it if it is

calculated by alternative means. In this method accounting income is used in place of the cash

flows so certain aspects in relation to cash are not considered (Brunsman, DeVore and Houston,

2011). Also when there is high maintenance cost than it will not be suitable to be used. In this if

two projects are compared than correct results will not be ascertained as in this time value is

ignored so projects having same outflows but whose inflows are not consistent than there will be

difference in ranking.

8

NPV 43975.564703933

IRR 4.62%

In this case as the NPV of the project is positive so the proposal will be accepted and the

machinery will be beneficial for the company so it will be purchased.

2. Evaluation of the benefits and limitations of each investment appraisal technique.

Payback period method: There are various advantages and disadvantages that are present

in this method which are that this method is very simple and easy to be used and it is also

understandable and will be computed in a simple manner as there are no complications that are

involved in its calculation. In case of the decision making in relation to the investment proposal

this method will be giving more importance to the liquidity (Burns, 2014). The main concept

behind this method is to deal with the risk as if the payback period will be less than it will have

the less risk that will be associated with that project and if more than that proposal will be more

risky.

The main disadvantages in this method is that the time value of money is not considered

while the calculation is made. The payback period method does not give importance to the

profitability as its whole importance is on liquidity. In this the cash flows that are arising before

the period are taken but after the period flows are totally ignored which is not at all beneficial.

Average Rate of Return: The main advantage is that it is very simple and easy to

calculate so can be used by anyone. The profitability aspect is considered in it which is very

important for any business.

There are various disadvantages that are related to it. The main problem associated with it

is of consistency as this can be calculated in many ways so there will be difference in it if it is

calculated by alternative means. In this method accounting income is used in place of the cash

flows so certain aspects in relation to cash are not considered (Brunsman, DeVore and Houston,

2011). Also when there is high maintenance cost than it will not be suitable to be used. In this if

two projects are compared than correct results will not be ascertained as in this time value is

ignored so projects having same outflows but whose inflows are not consistent than there will be

difference in ranking.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net present value method: Major advantage is that in this time value of money is

considered. In this method both the profitability and risk aspect of the proposal are given a high

priority. With the help of NPV the value of the company will be maximised.

The major disadvantage of this is that it is a complicated process and very difficult to calculate.

The calculation of the appropriate discount rate is not easy. When the projects have unequal life

than NPV will not be able to provide the correct results.

Internal rate of return: Main advantage that is associated with this method is that in this

the time value of money is considered and given importance which will be helpful in analysing

the big projects. This method is very simple to use which is also a merit of this (Bowhill, 2008).

In addition to advantages there are various disadvantages also which are in this the economies in

relation to scale are ignored. The actual value is not considered in it and mainly it is calculated

on the basis of assumptions. In some cases when there are mutually exclusive projects than this

method will not be helpful as in that percentage interpretation is done which is not considered as

appropriate.

CONCLUSION

From the above mentioned report it can be concluded that in case of financial

management there are various techniques that are present which can be used for the purpose of

deciding that which proposal is beneficial for the company and which is not. In that there are

various aspects that are considered which will be very helpful. Also there are many methods by

which the valuation of stock can be done and the investment decision can be made. The method

that will give the most appropriate result is the discounted cash flow method as in this the present

value of all the cash flows is considered which means that time value is given importance.

9

considered. In this method both the profitability and risk aspect of the proposal are given a high

priority. With the help of NPV the value of the company will be maximised.

The major disadvantage of this is that it is a complicated process and very difficult to calculate.

The calculation of the appropriate discount rate is not easy. When the projects have unequal life

than NPV will not be able to provide the correct results.

Internal rate of return: Main advantage that is associated with this method is that in this

the time value of money is considered and given importance which will be helpful in analysing

the big projects. This method is very simple to use which is also a merit of this (Bowhill, 2008).

In addition to advantages there are various disadvantages also which are in this the economies in

relation to scale are ignored. The actual value is not considered in it and mainly it is calculated

on the basis of assumptions. In some cases when there are mutually exclusive projects than this

method will not be helpful as in that percentage interpretation is done which is not considered as

appropriate.

CONCLUSION

From the above mentioned report it can be concluded that in case of financial

management there are various techniques that are present which can be used for the purpose of

deciding that which proposal is beneficial for the company and which is not. In that there are

various aspects that are considered which will be very helpful. Also there are many methods by

which the valuation of stock can be done and the investment decision can be made. The method

that will give the most appropriate result is the discounted cash flow method as in this the present

value of all the cash flows is considered which means that time value is given importance.

9

REFERENCES

Journals and Books

Agard, C., 2007. Getting the Real Out of Starting a Business. Adelphi Publishing & Media.

Pp.156.

Allen, K., 2012. New Venture Creation. South Western Cengage Learning.

Allio, J. R and Randall, M. R., 2010. Kiechel's history of corporate strategy. Strategy &

Leadership. 38(3). pp.29 – 34.

Araujo, L., Finch, A and Kjellberg, H., 2010. Reconnecting Marketing to Markets. OUP Oxford.

Bamford, R. D and Forrester, L. P., 2015. Managing planned and emergent change within an

operations management environment. International Journal of Operations &

Production Management. 23(5). pp.546 – 564.

Bolton, B., 2013. Entrepreneurs: talent, temperament and opportunity. Routledge.

Bowhill, B., 2008. Business Planning and Control: Integrating Accounting, Strategy, and

People. John Wiley and Sons.

Brunsman, B., DeVore, S and Houston, A., 2011. The corporate strategy function: improving its

value and effectiveness. Journal of Business Strategy. 32(5). pp.43 – 50.

Burns, P., 2014. New Venture Creation. Palgrave / Macmillan.

Chary, S. N., 2009. Production and Operations Management. 4th Ed. New Delhi: Tata Mc Graw

Hill.

Craighead, W. C and Meredith, J., 2008. Operations management research: evolution and

alternative future paths. International Journal of Operations & Production

Management. 28(8). pp.710-726.

Eom, B. S., 2012. Effects of LMS, self-efficacy, and self-regulated learning on LMS

effectiveness in business education. Journal of International Education in

Business. 5(2). pp. 129 – 144.

Evans, V., 2011. FT Essential Guide to Writing a Business Plan: How to Win Backing to Start

Up or Grow Your Business. FT/ Prentice Hall.

Online

Business Model Generation. 2017. [Online]. Available through<http://business model

generation.com/toolbox> [Accessed on 13th June 2017].

10

Journals and Books

Agard, C., 2007. Getting the Real Out of Starting a Business. Adelphi Publishing & Media.

Pp.156.

Allen, K., 2012. New Venture Creation. South Western Cengage Learning.

Allio, J. R and Randall, M. R., 2010. Kiechel's history of corporate strategy. Strategy &

Leadership. 38(3). pp.29 – 34.

Araujo, L., Finch, A and Kjellberg, H., 2010. Reconnecting Marketing to Markets. OUP Oxford.

Bamford, R. D and Forrester, L. P., 2015. Managing planned and emergent change within an

operations management environment. International Journal of Operations &

Production Management. 23(5). pp.546 – 564.

Bolton, B., 2013. Entrepreneurs: talent, temperament and opportunity. Routledge.

Bowhill, B., 2008. Business Planning and Control: Integrating Accounting, Strategy, and

People. John Wiley and Sons.

Brunsman, B., DeVore, S and Houston, A., 2011. The corporate strategy function: improving its

value and effectiveness. Journal of Business Strategy. 32(5). pp.43 – 50.

Burns, P., 2014. New Venture Creation. Palgrave / Macmillan.

Chary, S. N., 2009. Production and Operations Management. 4th Ed. New Delhi: Tata Mc Graw

Hill.

Craighead, W. C and Meredith, J., 2008. Operations management research: evolution and

alternative future paths. International Journal of Operations & Production

Management. 28(8). pp.710-726.

Eom, B. S., 2012. Effects of LMS, self-efficacy, and self-regulated learning on LMS

effectiveness in business education. Journal of International Education in

Business. 5(2). pp. 129 – 144.

Evans, V., 2011. FT Essential Guide to Writing a Business Plan: How to Win Backing to Start

Up or Grow Your Business. FT/ Prentice Hall.

Online

Business Model Generation. 2017. [Online]. Available through<http://business model

generation.com/toolbox> [Accessed on 13th June 2017].

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.