Financial Management and Accounting Report: Cost Analysis and Ratios

VerifiedAdded on 2020/01/07

|17

|4625

|164

Report

AI Summary

This report presents a comprehensive analysis of financial management and accounting principles, focusing on the influence of legal and regulatory factors on financial statements. It includes an examination of the Companies Act 2006 and International Financial Reporting Standards (IFRS), detailing their implications for various stakeholders. The report also features a cost of production analysis for Howorth Ltd., calculating equivalent units and total costs, and identifies key performance indicators for potential improvements. Furthermore, it provides income statements, consolidated statements, and a financial ratio analysis of Ager Ltd. for 2012 and 2013, along with a memorandum report advising management. The analysis covers various aspects of financial reporting, from cost accounting to the interpretation of financial ratios, offering valuable insights for financial decision-making.

FINANCIAL MANAGEMENT AND

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

FINANCIAL MANAGEMENT AND ACCOUNTING.................................................................1

INTRODUCTION ..........................................................................................................................1

11.1 Legal and regulatory influences on the financial statements and dealt with accounting

and reporting standard.................................................................................................................1

21.2 Implications of legal and regulatory measures on the users using financial statements and

how information needs of the users vary....................................................................................2

TASK 2............................................................................................................................................3

11) Calculation of Cost of production ........................................................................................3

22) Performance indicators to identify the potential improvements..........................................6

3A) Income statements for the year ended.................................................................................6

4B) Comprehensive income statements......................................................................................7

TASK 3............................................................................................................................................9

1Consolidated and summarized statement of comprehensive income financial position

statements for X parent company................................................................................................9

TASK 4..........................................................................................................................................10

1A] Calculation of ratios for the year ended on 30/9/2013.......................................................10

2b) Interpretation of the ratios computed for the year 2013.....................................................11

3C] Memorandum report advising the management of the company.......................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

FINANCIAL MANAGEMENT AND ACCOUNTING.................................................................1

INTRODUCTION ..........................................................................................................................1

11.1 Legal and regulatory influences on the financial statements and dealt with accounting

and reporting standard.................................................................................................................1

21.2 Implications of legal and regulatory measures on the users using financial statements and

how information needs of the users vary....................................................................................2

TASK 2............................................................................................................................................3

11) Calculation of Cost of production ........................................................................................3

22) Performance indicators to identify the potential improvements..........................................6

3A) Income statements for the year ended.................................................................................6

4B) Comprehensive income statements......................................................................................7

TASK 3............................................................................................................................................9

1Consolidated and summarized statement of comprehensive income financial position

statements for X parent company................................................................................................9

TASK 4..........................................................................................................................................10

1A] Calculation of ratios for the year ended on 30/9/2013.......................................................10

2b) Interpretation of the ratios computed for the year 2013.....................................................11

3C] Memorandum report advising the management of the company.......................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial management is the process that is highly concern with summarizing, recording

and analysing all the accounting transactions in order to examine the accurate picture of

organisation (Barton and Simko, 2002). By using data extracted from the above processes,

financial statements are prepared by the company and same are communicated to the general

public. In the present project report, influence of legal and regulatory factors on financial

statements is explained. Along with this, implication of these legal and regulatory factors on

financial statements will also be depicted. Further, cost of production report has prepared for

Howorth and some of the suggestions has been given to the company with an aim to minimize

the costs as well as enhance the value and quality. Apart from this, consolidated income and

financial position statements have been prepared. Besides this, financial ratios of Ager ltd. for

the year 2012 and 2013 have been computed and the same have been compared.

TASK 1

11.1 Legal and regulatory influences on the financial statements and dealt with accounting and

reporting standard

Companies act 2006: This act was established by the parliament of UK which includes

the primary sources of Company law. This act handles the working of all the companies. This

act includes 1300 sections covered in 700 pages and includes 16 schedules. Further, it was

finally came into existence on 1st October 2009 (Bromwich and Bhimani, 2005). This act

includes various provisions related to the duties and responsibilities of directors. Companies act,

2006 also includes various provisions related to the public and private companies.

As per this law, every organisation is required to maintain a complete record of all its

assets, liabilities, income, expenses, sales and inventories. In addition to this, they are required to

combine the subsidiaries account and then, publish all these statements for the general public. If,

company is not able to do this then as per the section 386, officer is liable to be punished and

imprisoned. Section 388 says that every organisation is required to keep the complete record of

all the transactions so that they can be checked anytime by the inspected officer. Section 386

says that it is mandatory for all the companies to prepare balance sheet and income statements

which tell about the profit and loss of business.

Financial management is the process that is highly concern with summarizing, recording

and analysing all the accounting transactions in order to examine the accurate picture of

organisation (Barton and Simko, 2002). By using data extracted from the above processes,

financial statements are prepared by the company and same are communicated to the general

public. In the present project report, influence of legal and regulatory factors on financial

statements is explained. Along with this, implication of these legal and regulatory factors on

financial statements will also be depicted. Further, cost of production report has prepared for

Howorth and some of the suggestions has been given to the company with an aim to minimize

the costs as well as enhance the value and quality. Apart from this, consolidated income and

financial position statements have been prepared. Besides this, financial ratios of Ager ltd. for

the year 2012 and 2013 have been computed and the same have been compared.

TASK 1

11.1 Legal and regulatory influences on the financial statements and dealt with accounting and

reporting standard

Companies act 2006: This act was established by the parliament of UK which includes

the primary sources of Company law. This act handles the working of all the companies. This

act includes 1300 sections covered in 700 pages and includes 16 schedules. Further, it was

finally came into existence on 1st October 2009 (Bromwich and Bhimani, 2005). This act

includes various provisions related to the duties and responsibilities of directors. Companies act,

2006 also includes various provisions related to the public and private companies.

As per this law, every organisation is required to maintain a complete record of all its

assets, liabilities, income, expenses, sales and inventories. In addition to this, they are required to

combine the subsidiaries account and then, publish all these statements for the general public. If,

company is not able to do this then as per the section 386, officer is liable to be punished and

imprisoned. Section 388 says that every organisation is required to keep the complete record of

all the transactions so that they can be checked anytime by the inspected officer. Section 386

says that it is mandatory for all the companies to prepare balance sheet and income statements

which tell about the profit and loss of business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

International accounting standards: This is one of the oldest set of standards which states

a particular types of transactions that influence the financial statements. These standards were

issued by the International Board of Accounting and Standard Committee (IASC). In the year

2001, new and more advanced standards were set which were known as International Financial

Reporting Standards (IFRS). This act includes various clauses about transcription the assets,

liabilities, inventories, earning per share, dividend per share, foreign exchange rate, expenditure,

income, joint ventures, staff benefits, lease contract, intangible assets, fixed assets, investment

and many more things (Burns and Scapens, 2000).

International financial and reporting standards (IFRS): These standards are set to

understand and compare the financial statements of all the companies across the geographical

boundaries. Increase in international shareholding and trade is one of the main causes for the

establishment of these standards. IFRS is successfully replacing the national accounting

standards of various countries. The main motive of IFRS is to furnish all the information related

to assets, liabilities, revenue, income, profit & loss and so on. Set up of these standards provide

assistance to the company to make the international transaction easily (Burns and Vaivio, 2001).

Some of the basis characteristics of IFRS include going concern concept, offsetting, consistency,

fair presentation, reporting frequency and accrual accounting basis. IFRS also requires that every

organisation should prepare the cash flow statements, income statements, balance sheet,

statements related to equity, retained earnings etc.

21.2 Implications of legal and regulatory measures on the users using financial statements and

how information needs of the users vary.

There are different types of users of the financial statements of company. Some of them are

internally present and some are the external users. Internal users include directors, employees

and owners while external users include creditors, suppliers, investors, government, competitor

and many more. These all users require different types of financial information.

Internal users

Directors: Directors are the ones who form various strategies with an aim to operate the

organisational activities in an effective manner, which in turn will help company to achieve its

desired objectives. They use financial statements to examine the financial performance and

position of company. On the basis of income statements, they try to analysis in detail about the

2

a particular types of transactions that influence the financial statements. These standards were

issued by the International Board of Accounting and Standard Committee (IASC). In the year

2001, new and more advanced standards were set which were known as International Financial

Reporting Standards (IFRS). This act includes various clauses about transcription the assets,

liabilities, inventories, earning per share, dividend per share, foreign exchange rate, expenditure,

income, joint ventures, staff benefits, lease contract, intangible assets, fixed assets, investment

and many more things (Burns and Scapens, 2000).

International financial and reporting standards (IFRS): These standards are set to

understand and compare the financial statements of all the companies across the geographical

boundaries. Increase in international shareholding and trade is one of the main causes for the

establishment of these standards. IFRS is successfully replacing the national accounting

standards of various countries. The main motive of IFRS is to furnish all the information related

to assets, liabilities, revenue, income, profit & loss and so on. Set up of these standards provide

assistance to the company to make the international transaction easily (Burns and Vaivio, 2001).

Some of the basis characteristics of IFRS include going concern concept, offsetting, consistency,

fair presentation, reporting frequency and accrual accounting basis. IFRS also requires that every

organisation should prepare the cash flow statements, income statements, balance sheet,

statements related to equity, retained earnings etc.

21.2 Implications of legal and regulatory measures on the users using financial statements and

how information needs of the users vary.

There are different types of users of the financial statements of company. Some of them are

internally present and some are the external users. Internal users include directors, employees

and owners while external users include creditors, suppliers, investors, government, competitor

and many more. These all users require different types of financial information.

Internal users

Directors: Directors are the ones who form various strategies with an aim to operate the

organisational activities in an effective manner, which in turn will help company to achieve its

desired objectives. They use financial statements to examine the financial performance and

position of company. On the basis of income statements, they try to analysis in detail about the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

income and expenditure made by the company and then, make policies accordingly in order to

reduce the cost (Burritt and Schaltegger, 2010).

Employees: They are the important resources of company. They provide various services

to the customers of company. Their main motive is to get the job security, bonus, performance

appraisals, fair salary and various non-monetary rewards. In lieu of which they prefer to see the

probability statement of company in order to get better earning as per the business profit.

Increase in probability level indicates that company is growing and there are the chances of

increasing salary in the next financial year.

External users

Investors: They are the one who invest their saving in the company with an aim to earn

more return on their investment. They want that company should generate more and more profit

and should increase the market value of shares. In lieu of which they see the financial statements

of business. Existing investors examine the business profit to conclude the return earned by

them. However, existing shareholders use financial statements published by the company.

Government: Government wants information about the profit and loss generated by

company and the growth rate it in various sectors. They use financial statements of the

organization in order to calculate the amount of tax needed to be paid by them (Dechow and

Skinner, 2000). Various government authorities ascertain the firm’s tax debts and then compare

the same with the tax paid. Government provides resources to the company to develop better

policies for the economic growth.

TASK 2

PART A

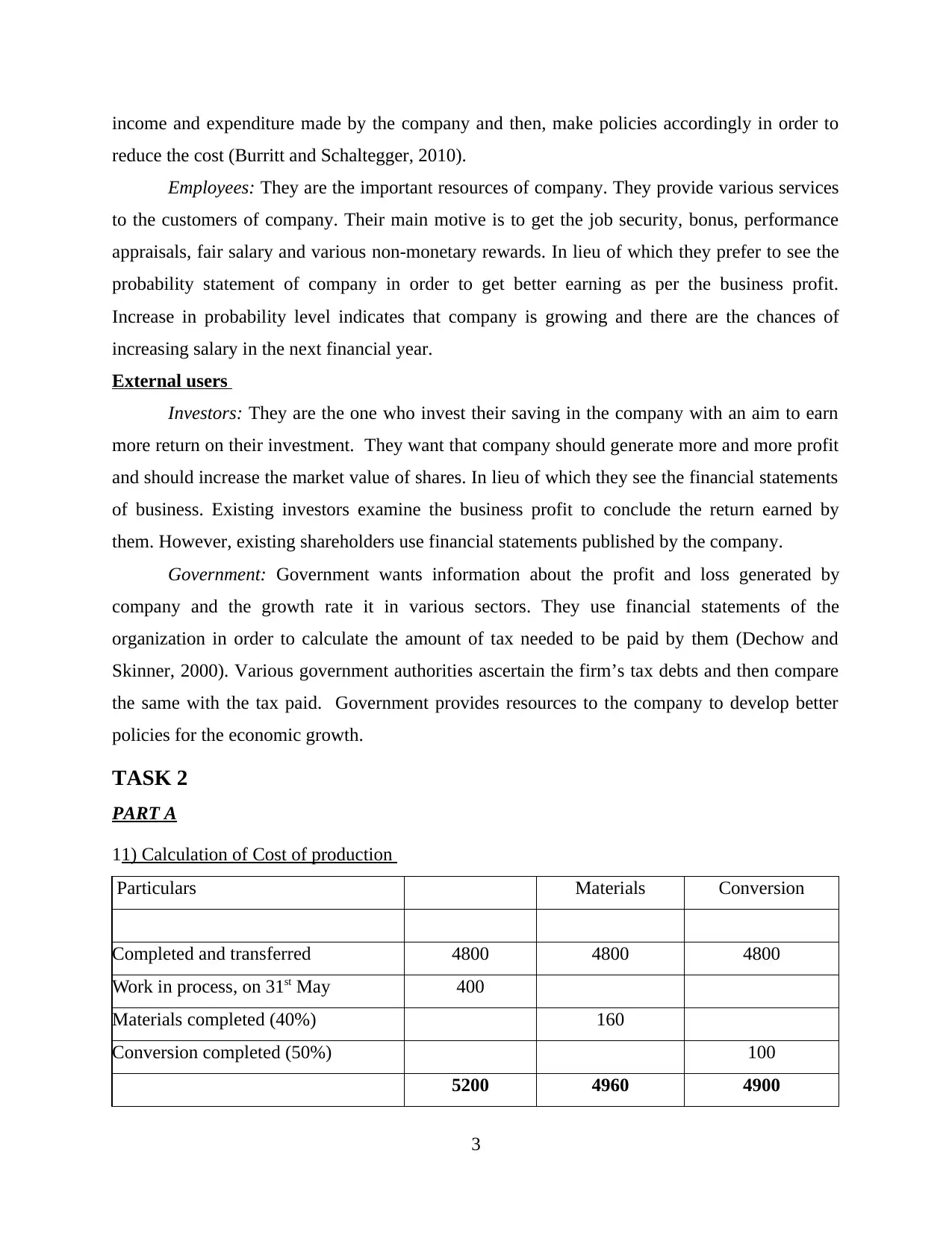

11) Calculation of Cost of production

Particulars Materials Conversion

Completed and transferred 4800 4800 4800

Work in process, on 31st May 400

Materials completed (40%) 160

Conversion completed (50%) 100

5200 4960 4900

3

reduce the cost (Burritt and Schaltegger, 2010).

Employees: They are the important resources of company. They provide various services

to the customers of company. Their main motive is to get the job security, bonus, performance

appraisals, fair salary and various non-monetary rewards. In lieu of which they prefer to see the

probability statement of company in order to get better earning as per the business profit.

Increase in probability level indicates that company is growing and there are the chances of

increasing salary in the next financial year.

External users

Investors: They are the one who invest their saving in the company with an aim to earn

more return on their investment. They want that company should generate more and more profit

and should increase the market value of shares. In lieu of which they see the financial statements

of business. Existing investors examine the business profit to conclude the return earned by

them. However, existing shareholders use financial statements published by the company.

Government: Government wants information about the profit and loss generated by

company and the growth rate it in various sectors. They use financial statements of the

organization in order to calculate the amount of tax needed to be paid by them (Dechow and

Skinner, 2000). Various government authorities ascertain the firm’s tax debts and then compare

the same with the tax paid. Government provides resources to the company to develop better

policies for the economic growth.

TASK 2

PART A

11) Calculation of Cost of production

Particulars Materials Conversion

Completed and transferred 4800 4800 4800

Work in process, on 31st May 400

Materials completed (40%) 160

Conversion completed (50%) 100

5200 4960 4900

3

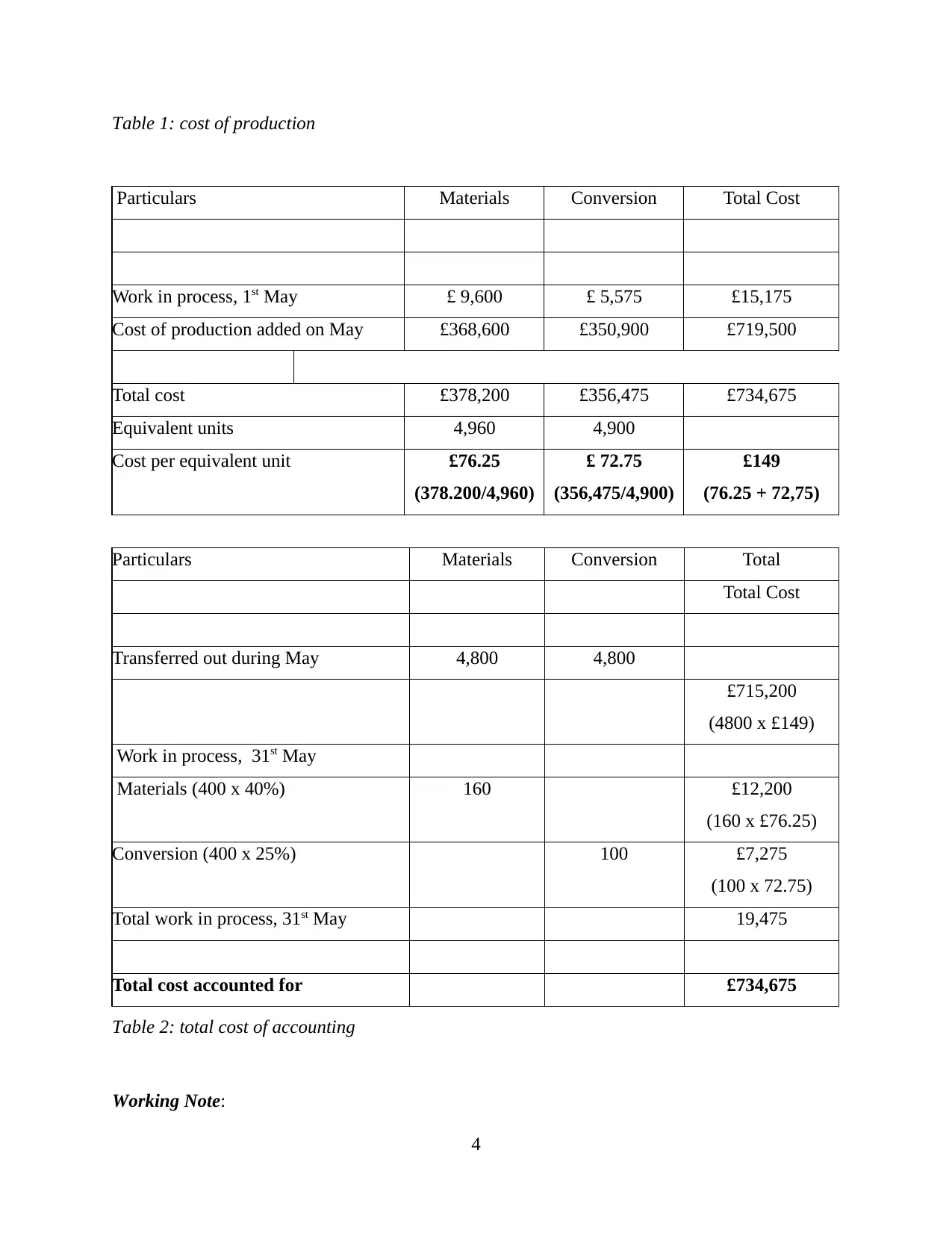

Table 1: cost of production

Particulars Materials Conversion Total Cost

Work in process, 1st May £ 9,600 £ 5,575 £15,175

Cost of production added on May £368,600 £350,900 £719,500

Total cost £378,200 £356,475 £734,675

Equivalent units 4,960 4,900

Cost per equivalent unit £76.25

(378.200/4,960)

£ 72.75

(356,475/4,900)

£149

(76.25 + 72,75)

Particulars Materials Conversion Total

Total Cost

Transferred out during May 4,800 4,800

£715,200

(4800 x £149)

Work in process, 31st May

Materials (400 x 40%) 160 £12,200

(160 x £76.25)

Conversion (400 x 25%) 100 £7,275

(100 x 72.75)

Total work in process, 31st May 19,475

Total cost accounted for £734,675

Table 2: total cost of accounting

Working Note:

4

Particulars Materials Conversion Total Cost

Work in process, 1st May £ 9,600 £ 5,575 £15,175

Cost of production added on May £368,600 £350,900 £719,500

Total cost £378,200 £356,475 £734,675

Equivalent units 4,960 4,900

Cost per equivalent unit £76.25

(378.200/4,960)

£ 72.75

(356,475/4,900)

£149

(76.25 + 72,75)

Particulars Materials Conversion Total

Total Cost

Transferred out during May 4,800 4,800

£715,200

(4800 x £149)

Work in process, 31st May

Materials (400 x 40%) 160 £12,200

(160 x £76.25)

Conversion (400 x 25%) 100 £7,275

(100 x 72.75)

Total work in process, 31st May 19,475

Total cost accounted for £734,675

Table 2: total cost of accounting

Working Note:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

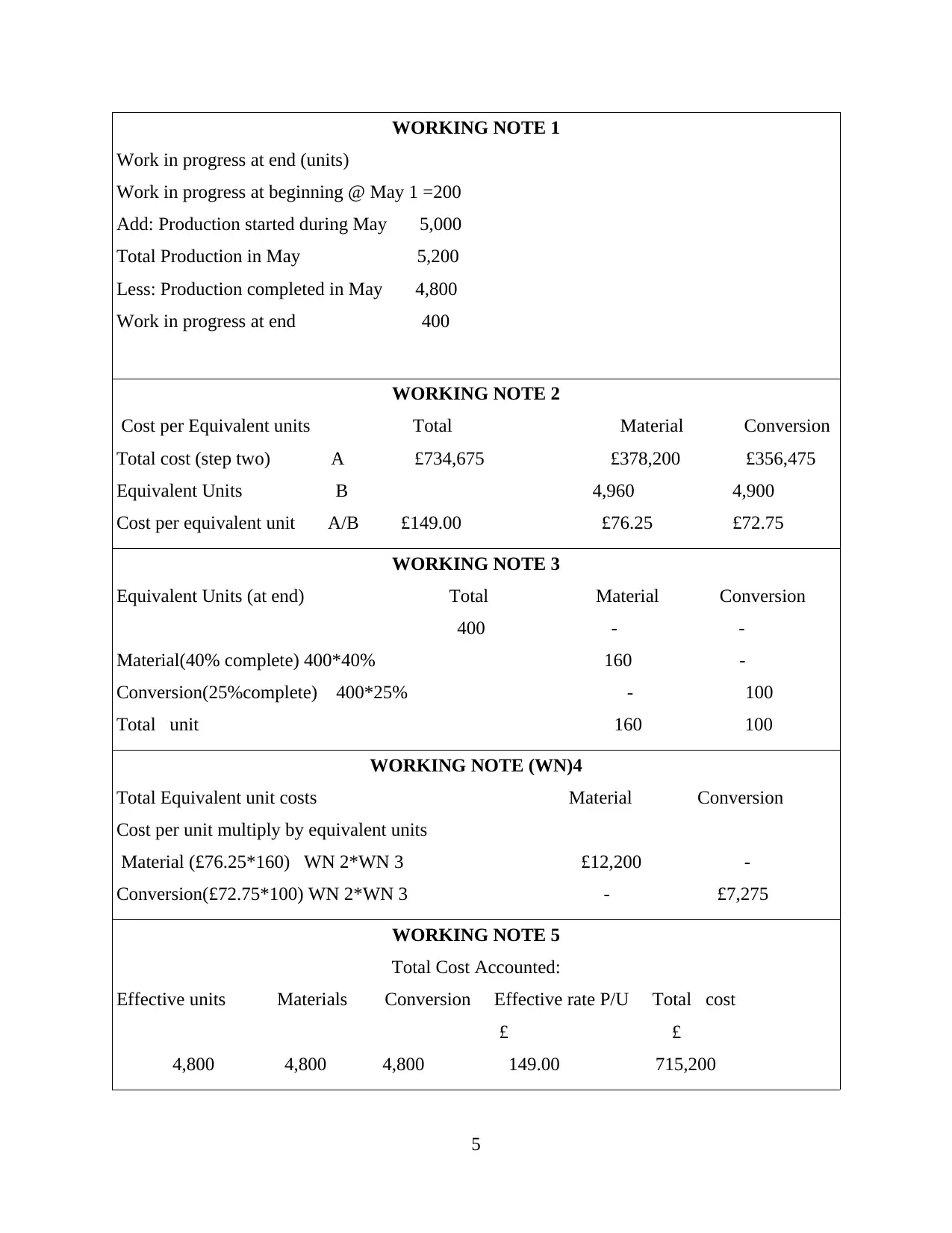

WORKING NOTE 1

Work in progress at end (units)

Work in progress at beginning @ May 1 =200

Add: Production started during May 5,000

Total Production in May 5,200

Less: Production completed in May 4,800

Work in progress at end 400

WORKING NOTE 2

Cost per Equivalent units Total Material Conversion

Total cost (step two) A £734,675 £378,200 £356,475

Equivalent Units B 4,960 4,900

Cost per equivalent unit A/B £149.00 £76.25 £72.75

WORKING NOTE 3

Equivalent Units (at end) Total Material Conversion

400 - -

Material(40% complete) 400*40% 160 -

Conversion(25%complete) 400*25% - 100

Total unit 160 100

WORKING NOTE (WN)4

Total Equivalent unit costs Material Conversion

Cost per unit multiply by equivalent units

Material (£76.25*160) WN 2*WN 3 £12,200 -

Conversion(£72.75*100) WN 2*WN 3 - £7,275

WORKING NOTE 5

Total Cost Accounted:

Effective units Materials Conversion Effective rate P/U Total cost

£ £

4,800 4,800 4,800 149.00 715,200

5

Work in progress at end (units)

Work in progress at beginning @ May 1 =200

Add: Production started during May 5,000

Total Production in May 5,200

Less: Production completed in May 4,800

Work in progress at end 400

WORKING NOTE 2

Cost per Equivalent units Total Material Conversion

Total cost (step two) A £734,675 £378,200 £356,475

Equivalent Units B 4,960 4,900

Cost per equivalent unit A/B £149.00 £76.25 £72.75

WORKING NOTE 3

Equivalent Units (at end) Total Material Conversion

400 - -

Material(40% complete) 400*40% 160 -

Conversion(25%complete) 400*25% - 100

Total unit 160 100

WORKING NOTE (WN)4

Total Equivalent unit costs Material Conversion

Cost per unit multiply by equivalent units

Material (£76.25*160) WN 2*WN 3 £12,200 -

Conversion(£72.75*100) WN 2*WN 3 - £7,275

WORKING NOTE 5

Total Cost Accounted:

Effective units Materials Conversion Effective rate P/U Total cost

£ £

4,800 4,800 4,800 149.00 715,200

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

- 160 - 76.25 12,200

- - 100 72.75 7,275

Total 4,960 4,900 734,675

On the basis of the above calculation it can be concluded that cost of production of

Howorth Ltd. for material and conversion work in progress is 70% and 45% respectively which

has been completed in the month of May. Besides this Howorth expected to produce 5000 units

at the start of the month but was only able to produce 4800 units. Therefore, cost of 200 units

that are not produced during the month will not be included. Which in turn obtain the total cost

of £734,675.

22) Performance indicators to identify the potential improvements.

It is very important for the company to assess its financial performance on a regular basis

in order to examine whether the company is operating its business in an effective manner or not

(Ewert and Wagenhofer, 2005). Therefore, it can be said that use of this tool is very important for

analysing the financial position of the company and then develop the various strategies with an

aim to achieve the financial goals and objectives of the company. Some of the performance

indicators that can be used by manufacturing unit are:-

Quality: - This is one of the most beneficial performance indicators for the companies

who want to produce the quality goods and services. The performance of the whole organisation

can be measured according to the quality offered by them to different users.

Production time: - It is used by the company to examine the time period that is required

to manufacture a finished goods. The main motto of using this indicator is that company can

easily monitor the procedure and is able to ensure that the work has been completed in an

effective and efficient manner or not.

Output: - It is another important performance indicators that is used by the company to

achieve its set target. By using this indicators company can calculate the difference between

actual and budgeted level of output (Hansen, Mowen and Guan, 2007). And if any drawbacks

has been found than in that case they can easily be resolved.

PART B

6

- - 100 72.75 7,275

Total 4,960 4,900 734,675

On the basis of the above calculation it can be concluded that cost of production of

Howorth Ltd. for material and conversion work in progress is 70% and 45% respectively which

has been completed in the month of May. Besides this Howorth expected to produce 5000 units

at the start of the month but was only able to produce 4800 units. Therefore, cost of 200 units

that are not produced during the month will not be included. Which in turn obtain the total cost

of £734,675.

22) Performance indicators to identify the potential improvements.

It is very important for the company to assess its financial performance on a regular basis

in order to examine whether the company is operating its business in an effective manner or not

(Ewert and Wagenhofer, 2005). Therefore, it can be said that use of this tool is very important for

analysing the financial position of the company and then develop the various strategies with an

aim to achieve the financial goals and objectives of the company. Some of the performance

indicators that can be used by manufacturing unit are:-

Quality: - This is one of the most beneficial performance indicators for the companies

who want to produce the quality goods and services. The performance of the whole organisation

can be measured according to the quality offered by them to different users.

Production time: - It is used by the company to examine the time period that is required

to manufacture a finished goods. The main motto of using this indicator is that company can

easily monitor the procedure and is able to ensure that the work has been completed in an

effective and efficient manner or not.

Output: - It is another important performance indicators that is used by the company to

achieve its set target. By using this indicators company can calculate the difference between

actual and budgeted level of output (Hansen, Mowen and Guan, 2007). And if any drawbacks

has been found than in that case they can easily be resolved.

PART B

6

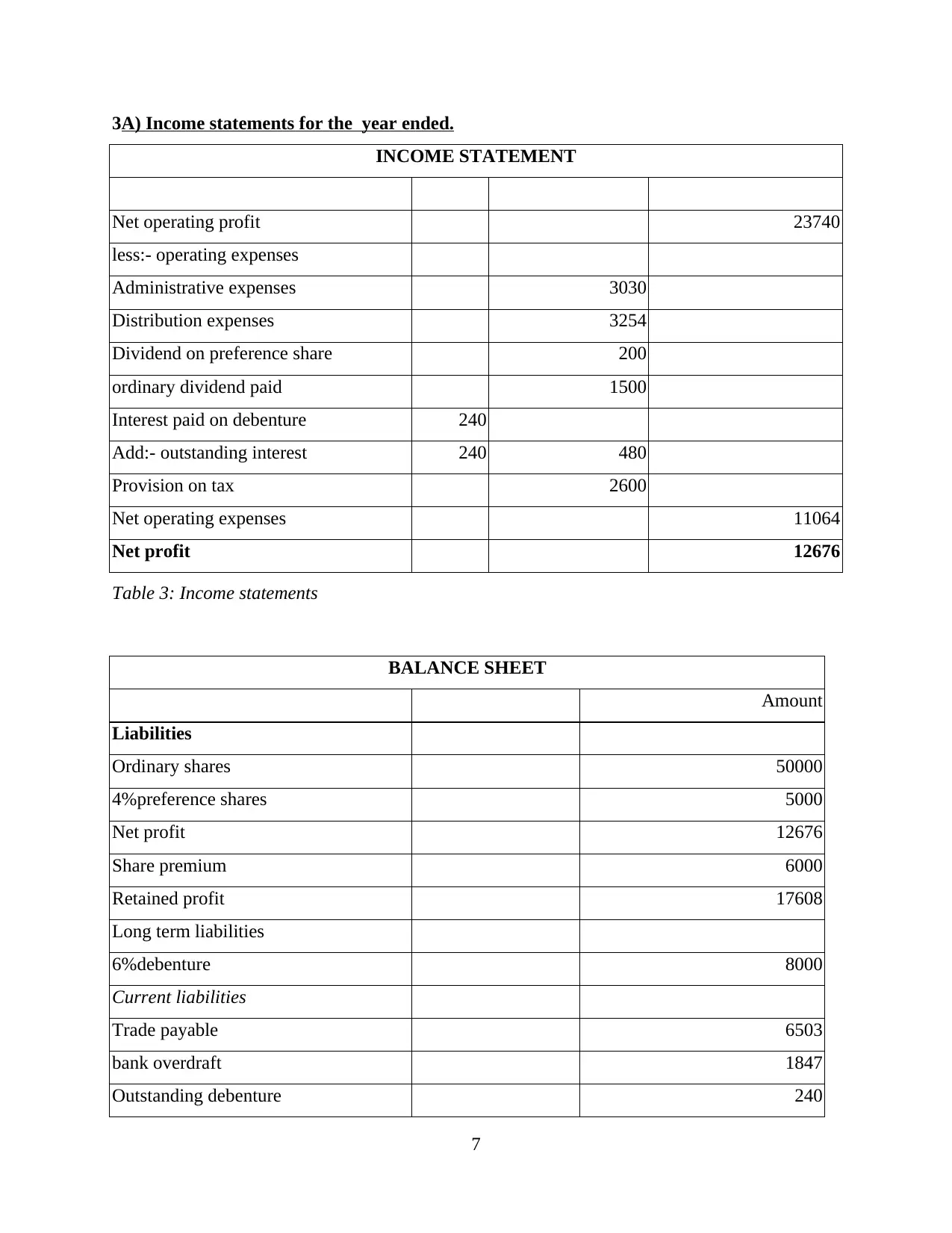

3A) Income statements for the year ended.

INCOME STATEMENT

Net operating profit 23740

less:- operating expenses

Administrative expenses 3030

Distribution expenses 3254

Dividend on preference share 200

ordinary dividend paid 1500

Interest paid on debenture 240

Add:- outstanding interest 240 480

Provision on tax 2600

Net operating expenses 11064

Net profit 12676

Table 3: Income statements

BALANCE SHEET

Amount

Liabilities

Ordinary shares 50000

4%preference shares 5000

Net profit 12676

Share premium 6000

Retained profit 17608

Long term liabilities

6%debenture 8000

Current liabilities

Trade payable 6503

bank overdraft 1847

Outstanding debenture 240

7

INCOME STATEMENT

Net operating profit 23740

less:- operating expenses

Administrative expenses 3030

Distribution expenses 3254

Dividend on preference share 200

ordinary dividend paid 1500

Interest paid on debenture 240

Add:- outstanding interest 240 480

Provision on tax 2600

Net operating expenses 11064

Net profit 12676

Table 3: Income statements

BALANCE SHEET

Amount

Liabilities

Ordinary shares 50000

4%preference shares 5000

Net profit 12676

Share premium 6000

Retained profit 17608

Long term liabilities

6%debenture 8000

Current liabilities

Trade payable 6503

bank overdraft 1847

Outstanding debenture 240

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Provision of tax 2600

Total liabilities 110474

Assets

fixed assets

Property 67000

Add:- profit on revaluation 8000 75000

Plant and equipment 27525

Total fixed assets 102525

Current assets

Trade receivable 4339

inventory 3610

Total Current assets 7949

total assets 110474

Table 4: Balance sheet

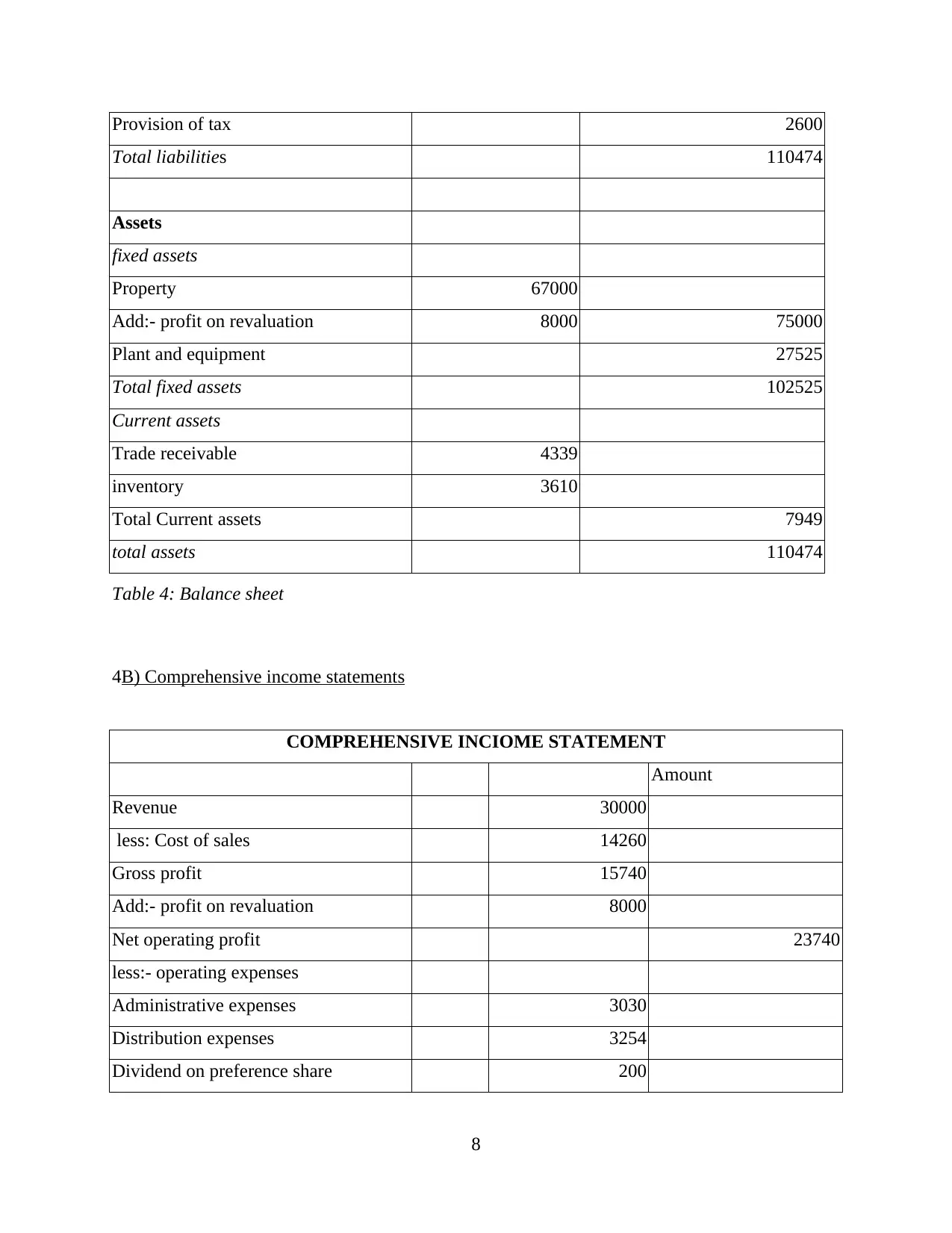

4B) Comprehensive income statements

COMPREHENSIVE INCIOME STATEMENT

Amount

Revenue 30000

less: Cost of sales 14260

Gross profit 15740

Add:- profit on revaluation 8000

Net operating profit 23740

less:- operating expenses

Administrative expenses 3030

Distribution expenses 3254

Dividend on preference share 200

8

Total liabilities 110474

Assets

fixed assets

Property 67000

Add:- profit on revaluation 8000 75000

Plant and equipment 27525

Total fixed assets 102525

Current assets

Trade receivable 4339

inventory 3610

Total Current assets 7949

total assets 110474

Table 4: Balance sheet

4B) Comprehensive income statements

COMPREHENSIVE INCIOME STATEMENT

Amount

Revenue 30000

less: Cost of sales 14260

Gross profit 15740

Add:- profit on revaluation 8000

Net operating profit 23740

less:- operating expenses

Administrative expenses 3030

Distribution expenses 3254

Dividend on preference share 200

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ordinary dividend paid 1500

Interest paid on debenture 240

Add:- outstanding interest 240 480

Provision on tax 2600

Net operating expenses 11064

Net profit 12676

Table 5: Comprehensive income statements

TASK 3

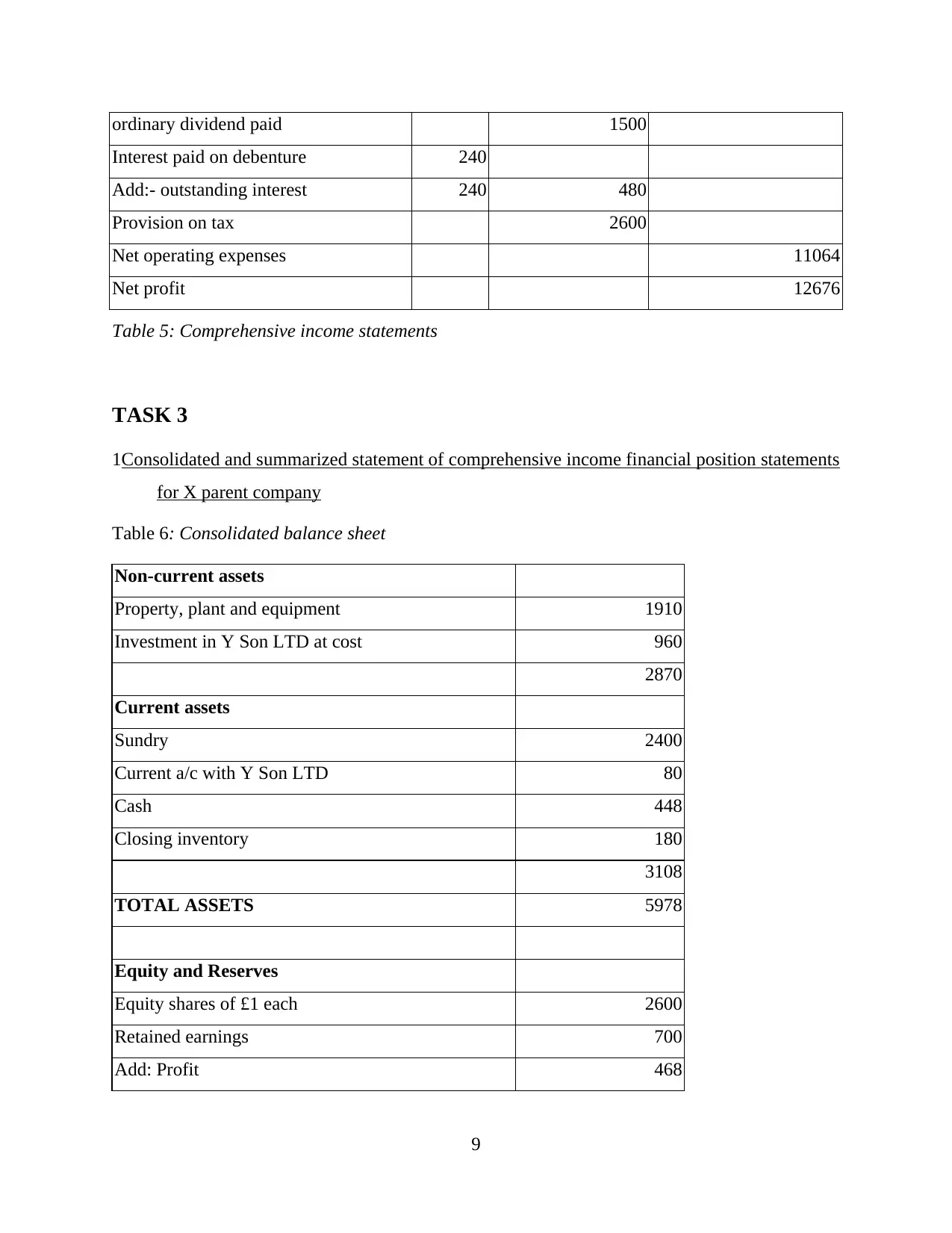

1Consolidated and summarized statement of comprehensive income financial position statements

for X parent company

Table 6: Consolidated balance sheet

Non-current assets

Property, plant and equipment 1910

Investment in Y Son LTD at cost 960

2870

Current assets

Sundry 2400

Current a/c with Y Son LTD 80

Cash 448

Closing inventory 180

3108

TOTAL ASSETS 5978

Equity and Reserves

Equity shares of £1 each 2600

Retained earnings 700

Add: Profit 468

9

Interest paid on debenture 240

Add:- outstanding interest 240 480

Provision on tax 2600

Net operating expenses 11064

Net profit 12676

Table 5: Comprehensive income statements

TASK 3

1Consolidated and summarized statement of comprehensive income financial position statements

for X parent company

Table 6: Consolidated balance sheet

Non-current assets

Property, plant and equipment 1910

Investment in Y Son LTD at cost 960

2870

Current assets

Sundry 2400

Current a/c with Y Son LTD 80

Cash 448

Closing inventory 180

3108

TOTAL ASSETS 5978

Equity and Reserves

Equity shares of £1 each 2600

Retained earnings 700

Add: Profit 468

9

3768

Current liabilities

Trade payables 2150

Current a/c with X Parent Plc 60

2210

TOTAL EQUITY AND RESERVES 5978

Table 7: Consolidated income statement

Revenue 1300

Cost of sales 632

Gross Profit 668

Other income - dividends received 50

Expenses 153

Dividend 10

Cheque 20

575

Finance cost 52

Profit before Taxation 523

Taxation 55

Profit for the year 46

TASK 4

PART A

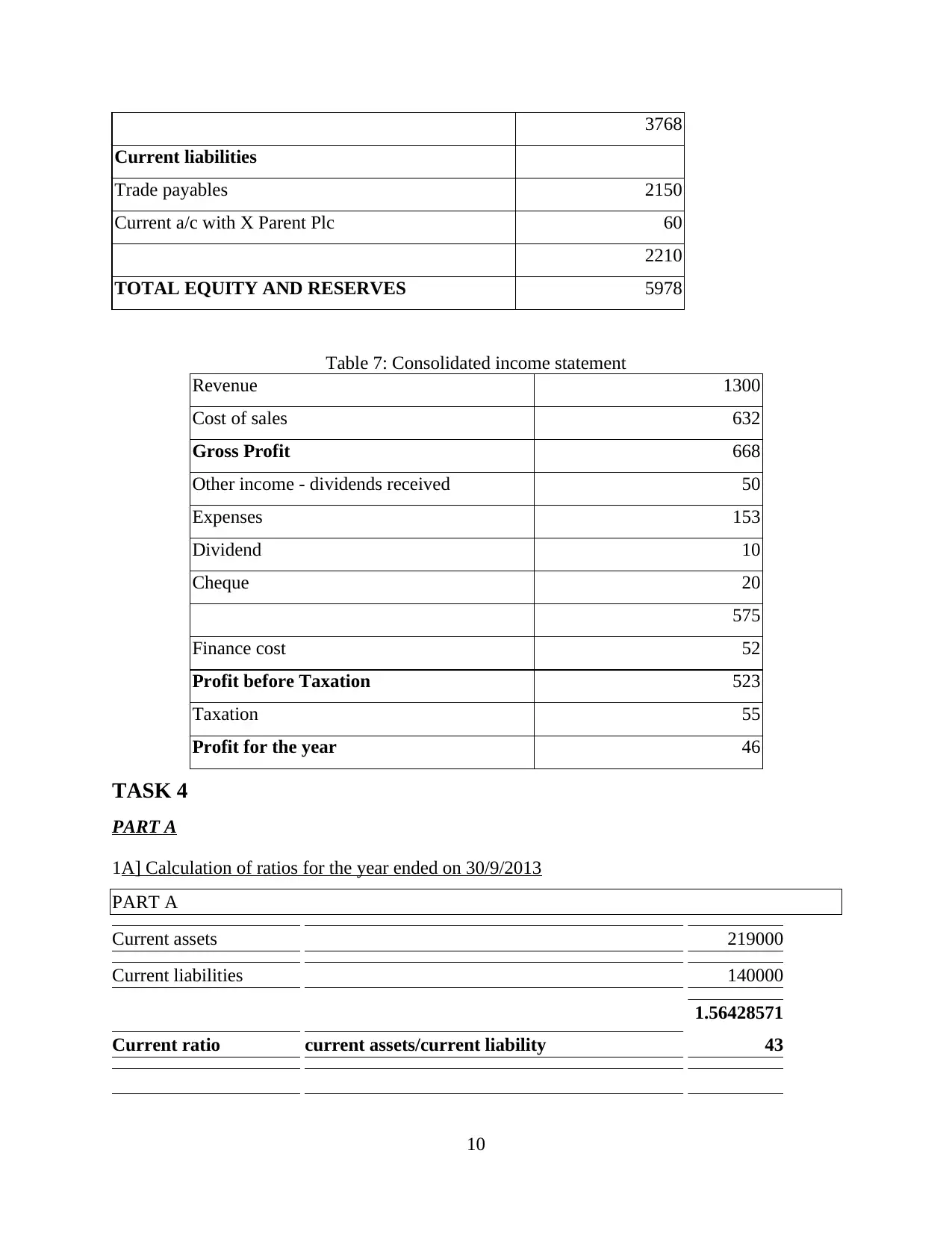

1A] Calculation of ratios for the year ended on 30/9/2013

PART A

Current assets 219000

Current liabilities 140000

Current ratio current assets/current liability

1.56428571

43

10

Current liabilities

Trade payables 2150

Current a/c with X Parent Plc 60

2210

TOTAL EQUITY AND RESERVES 5978

Table 7: Consolidated income statement

Revenue 1300

Cost of sales 632

Gross Profit 668

Other income - dividends received 50

Expenses 153

Dividend 10

Cheque 20

575

Finance cost 52

Profit before Taxation 523

Taxation 55

Profit for the year 46

TASK 4

PART A

1A] Calculation of ratios for the year ended on 30/9/2013

PART A

Current assets 219000

Current liabilities 140000

Current ratio current assets/current liability

1.56428571

43

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.