Financial Resource Management and Performance Analysis Report

VerifiedAdded on 2020/09/17

|10

|2791

|39

Report

AI Summary

This report provides a detailed analysis of financial resource management, covering key aspects such as the differences between financial and management accounting, the purpose of financial statements for both profit and non-profit organizations, and the identification of various stakeholder groups and their information needs. The report also includes a practical application of ratio analysis to assess the financial performance of Stratford Yachts Ltd, comparing its profitability and liquidity ratios with industry averages. The analysis provides insights into the company's financial health and performance, highlighting areas for improvement and strategic decision-making. The report is a comprehensive overview of financial management principles and their application in a real-world business context.

MANGING FINANCIAL

RESOURCES

RESOURCES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Difference between financial accounts and management accounts........................................1

b) Purpose of various financial statements in profit and non profit organisation.......................3

c) Various groups of stakeholders and evaluate the different information needs.......................5

TASK 2............................................................................................................................................6

a) Ratio analysis..........................................................................................................................6

b) Detailed report subject to analysing performance of organisation.........................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

a) Difference between financial accounts and management accounts........................................1

b) Purpose of various financial statements in profit and non profit organisation.......................3

c) Various groups of stakeholders and evaluate the different information needs.......................5

TASK 2............................................................................................................................................6

a) Ratio analysis..........................................................................................................................6

b) Detailed report subject to analysing performance of organisation.........................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Financial resources are most important part for business and organisations. It is important

for managers and accountant officers to manage the financial resources and tools in effective

way to attain desired results and outcomes (Ashwell, 2014). This report is prepared to explain

importance of financial accounts subject to analyse financial performance of organisation.

Purpose of financial statements for profit and non profit organisations also defined in this

context. Information and details which remain essential for stakeholders also defined. Financial

performance of Startford Yachts Ltd defined with the use of ratio analysis. A summery report is

provided to managers of organisation in terms of comparing profitability and liquidity with the

average of the sector over the period.

TASK 1

a) Difference between financial accounts and management accounts

Financial accounts

Financial accounts of an organisation indicates towards the financial performance and

growth of an organisation. Financial account helps to analyse information and details which

remain linked with financial transactions and events. Presenting financial information in numeric

form is one of the prime objective of financial accounts (Bridoux and Stoelhorst, 2014). In the

end of every year financial accounts are prepared and consolidated to evaluate the performance

of organisation.

Management accounts

Management accounting is a part of management decisions and helps to understand the

managerial decisions and effectiveness for better control and operation. Management accounts

holds the basic structure of management and function (Jackie, 2012). Managerial accounting

process which support management decisions and decision making process in order to make

better forecast and estimation. With the helps of management accounts managers and accounts

be able to sort out complex situations and managerial actions (Cascio, 2018).

Management accounts and financial accounts are two different aspects. Difference

between management accounts and financial accounts can be bifurcated as follows

Basis of

difference

Financial accounting Management accounts

1

Financial resources are most important part for business and organisations. It is important

for managers and accountant officers to manage the financial resources and tools in effective

way to attain desired results and outcomes (Ashwell, 2014). This report is prepared to explain

importance of financial accounts subject to analyse financial performance of organisation.

Purpose of financial statements for profit and non profit organisations also defined in this

context. Information and details which remain essential for stakeholders also defined. Financial

performance of Startford Yachts Ltd defined with the use of ratio analysis. A summery report is

provided to managers of organisation in terms of comparing profitability and liquidity with the

average of the sector over the period.

TASK 1

a) Difference between financial accounts and management accounts

Financial accounts

Financial accounts of an organisation indicates towards the financial performance and

growth of an organisation. Financial account helps to analyse information and details which

remain linked with financial transactions and events. Presenting financial information in numeric

form is one of the prime objective of financial accounts (Bridoux and Stoelhorst, 2014). In the

end of every year financial accounts are prepared and consolidated to evaluate the performance

of organisation.

Management accounts

Management accounting is a part of management decisions and helps to understand the

managerial decisions and effectiveness for better control and operation. Management accounts

holds the basic structure of management and function (Jackie, 2012). Managerial accounting

process which support management decisions and decision making process in order to make

better forecast and estimation. With the helps of management accounts managers and accounts

be able to sort out complex situations and managerial actions (Cascio, 2018).

Management accounts and financial accounts are two different aspects. Difference

between management accounts and financial accounts can be bifurcated as follows

Basis of

difference

Financial accounting Management accounts

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

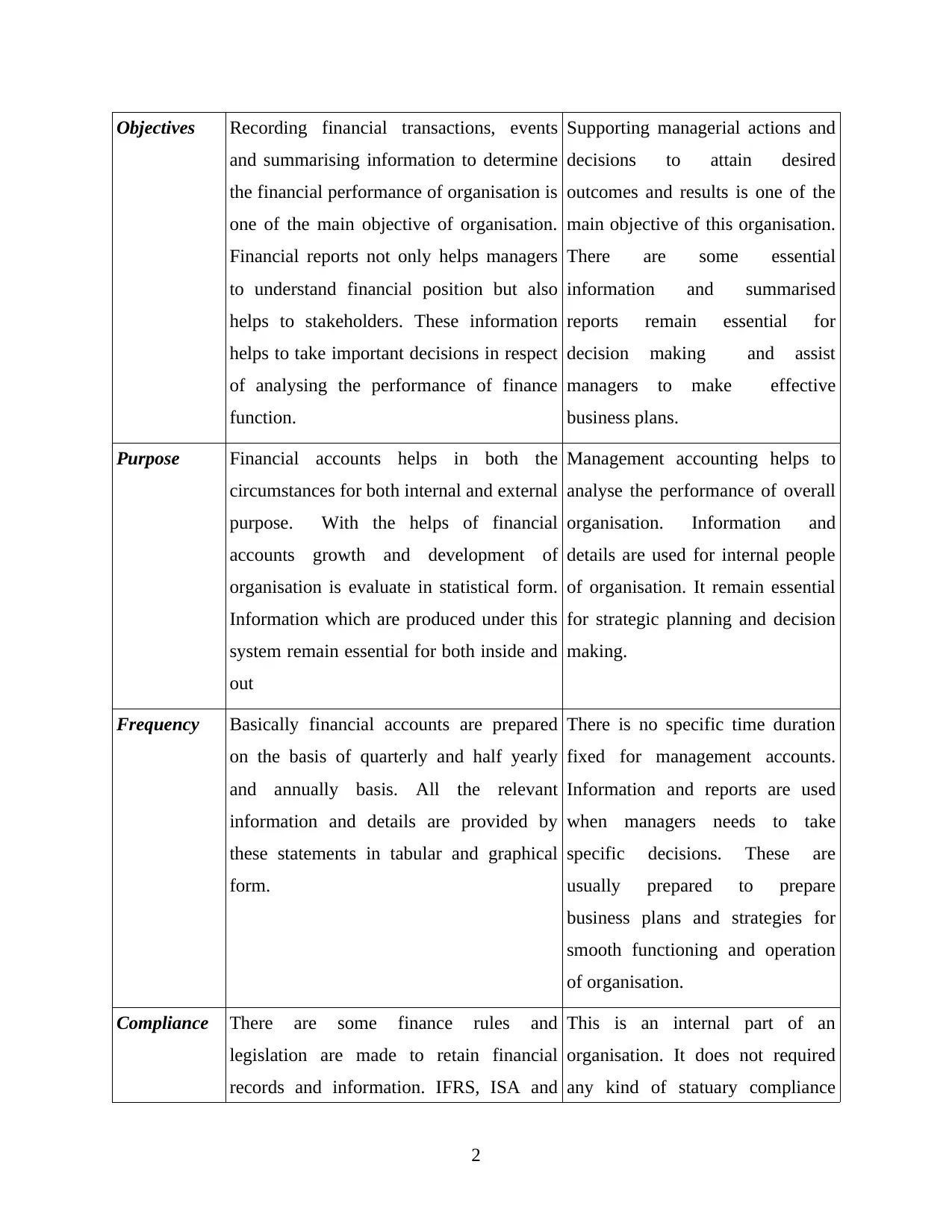

Objectives Recording financial transactions, events

and summarising information to determine

the financial performance of organisation is

one of the main objective of organisation.

Financial reports not only helps managers

to understand financial position but also

helps to stakeholders. These information

helps to take important decisions in respect

of analysing the performance of finance

function.

Supporting managerial actions and

decisions to attain desired

outcomes and results is one of the

main objective of this organisation.

There are some essential

information and summarised

reports remain essential for

decision making and assist

managers to make effective

business plans.

Purpose Financial accounts helps in both the

circumstances for both internal and external

purpose. With the helps of financial

accounts growth and development of

organisation is evaluate in statistical form.

Information which are produced under this

system remain essential for both inside and

out

Management accounting helps to

analyse the performance of overall

organisation. Information and

details are used for internal people

of organisation. It remain essential

for strategic planning and decision

making.

Frequency Basically financial accounts are prepared

on the basis of quarterly and half yearly

and annually basis. All the relevant

information and details are provided by

these statements in tabular and graphical

form.

There is no specific time duration

fixed for management accounts.

Information and reports are used

when managers needs to take

specific decisions. These are

usually prepared to prepare

business plans and strategies for

smooth functioning and operation

of organisation.

Compliance There are some finance rules and

legislation are made to retain financial

records and information. IFRS, ISA and

This is an internal part of an

organisation. It does not required

any kind of statuary compliance

2

and summarising information to determine

the financial performance of organisation is

one of the main objective of organisation.

Financial reports not only helps managers

to understand financial position but also

helps to stakeholders. These information

helps to take important decisions in respect

of analysing the performance of finance

function.

Supporting managerial actions and

decisions to attain desired

outcomes and results is one of the

main objective of this organisation.

There are some essential

information and summarised

reports remain essential for

decision making and assist

managers to make effective

business plans.

Purpose Financial accounts helps in both the

circumstances for both internal and external

purpose. With the helps of financial

accounts growth and development of

organisation is evaluate in statistical form.

Information which are produced under this

system remain essential for both inside and

out

Management accounting helps to

analyse the performance of overall

organisation. Information and

details are used for internal people

of organisation. It remain essential

for strategic planning and decision

making.

Frequency Basically financial accounts are prepared

on the basis of quarterly and half yearly

and annually basis. All the relevant

information and details are provided by

these statements in tabular and graphical

form.

There is no specific time duration

fixed for management accounts.

Information and reports are used

when managers needs to take

specific decisions. These are

usually prepared to prepare

business plans and strategies for

smooth functioning and operation

of organisation.

Compliance There are some finance rules and

legislation are made to retain financial

records and information. IFRS, ISA and

This is an internal part of an

organisation. It does not required

any kind of statuary compliance

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

GAAP provides rules and standards subject

to preparing financial accounts. Statuary

compliance is mandatory for financial

accounts.

and legislations to prepare plans

and strategies. Management

decision and information remain

related to growth and development

of organisation.

Focus Financial accounts are made to summarise

financial information and data for better

implementation and utilisation of financial

resources. It provides a path to analyse

financial requirements and needs for for

performing financial actions and plans.

Management reports and

information are beneficial for better

forecasting and analysis of overall

business operations. With the help

of management accounts and

mangers become eligible to identify

required area of improvement for

better management and operation.

Skill sets It requires strong base and structure for

better presentation and formation of

financial records and information. All the

relevant rules and standards are used by

finance accountants. Rules and principles

provided by IFRS, GAAP and ISA are

basically used by organisation.

Various type of management

accounting systems and techniques

are used by organisation for

effective management and

operations such as cost accounting

system, preparation of management

reports and cost reports, inventory

and budget reports. These reports

make smooth the process of

decision making process.

Certified

courses

There are some certified courses made such

as charted accountants (CA), Association of

charted certified accountants (ACCA) and

certified public accountants (CPA), etc.

Charted institute of management

accountants (CIMA), cost

management and accountants

(CMA) are the courses which

certified management accountants

and managers.

3

to preparing financial accounts. Statuary

compliance is mandatory for financial

accounts.

and legislations to prepare plans

and strategies. Management

decision and information remain

related to growth and development

of organisation.

Focus Financial accounts are made to summarise

financial information and data for better

implementation and utilisation of financial

resources. It provides a path to analyse

financial requirements and needs for for

performing financial actions and plans.

Management reports and

information are beneficial for better

forecasting and analysis of overall

business operations. With the help

of management accounts and

mangers become eligible to identify

required area of improvement for

better management and operation.

Skill sets It requires strong base and structure for

better presentation and formation of

financial records and information. All the

relevant rules and standards are used by

finance accountants. Rules and principles

provided by IFRS, GAAP and ISA are

basically used by organisation.

Various type of management

accounting systems and techniques

are used by organisation for

effective management and

operations such as cost accounting

system, preparation of management

reports and cost reports, inventory

and budget reports. These reports

make smooth the process of

decision making process.

Certified

courses

There are some certified courses made such

as charted accountants (CA), Association of

charted certified accountants (ACCA) and

certified public accountants (CPA), etc.

Charted institute of management

accountants (CIMA), cost

management and accountants

(CMA) are the courses which

certified management accountants

and managers.

3

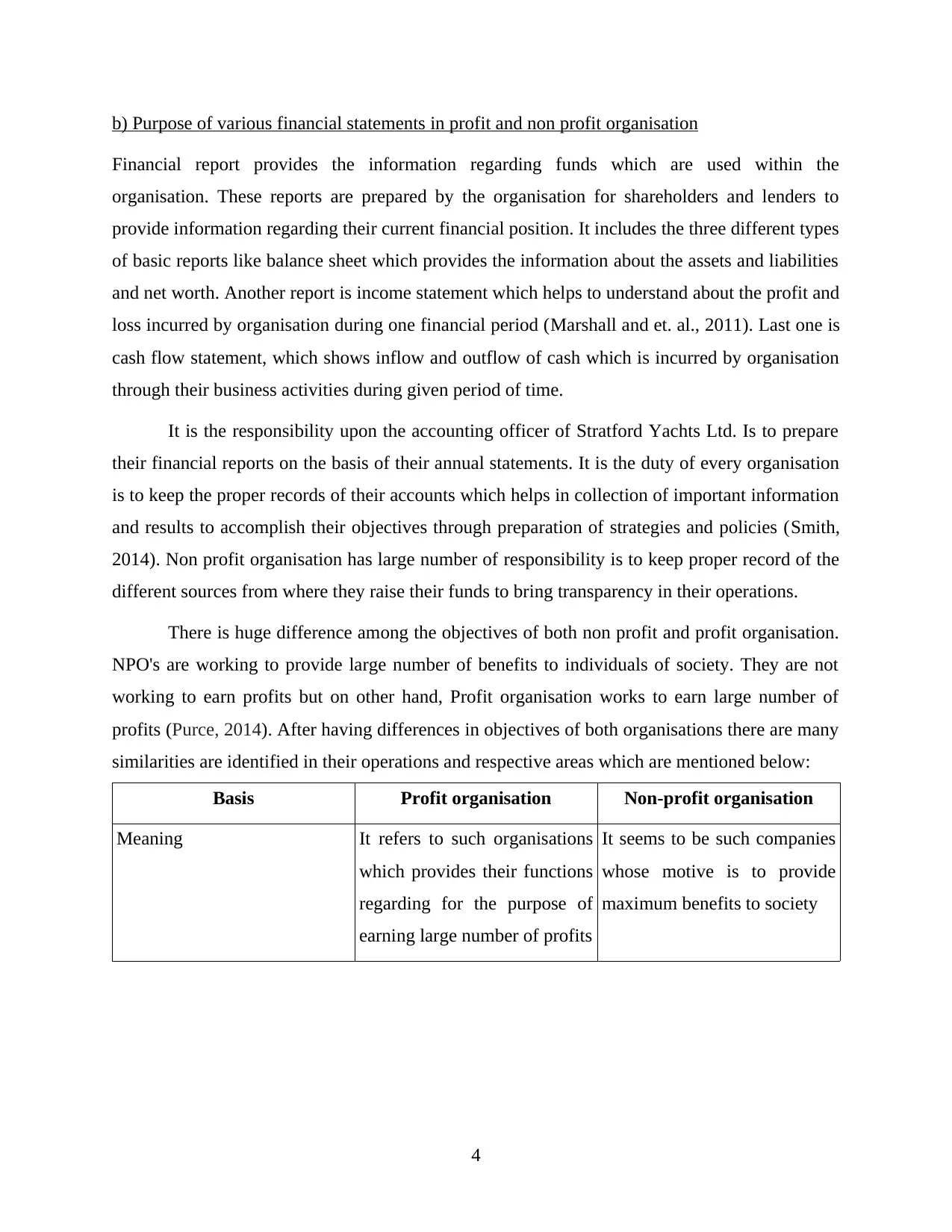

b) Purpose of various financial statements in profit and non profit organisation

Financial report provides the information regarding funds which are used within the

organisation. These reports are prepared by the organisation for shareholders and lenders to

provide information regarding their current financial position. It includes the three different types

of basic reports like balance sheet which provides the information about the assets and liabilities

and net worth. Another report is income statement which helps to understand about the profit and

loss incurred by organisation during one financial period (Marshall and et. al., 2011). Last one is

cash flow statement, which shows inflow and outflow of cash which is incurred by organisation

through their business activities during given period of time.

It is the responsibility upon the accounting officer of Stratford Yachts Ltd. Is to prepare

their financial reports on the basis of their annual statements. It is the duty of every organisation

is to keep the proper records of their accounts which helps in collection of important information

and results to accomplish their objectives through preparation of strategies and policies (Smith,

2014). Non profit organisation has large number of responsibility is to keep proper record of the

different sources from where they raise their funds to bring transparency in their operations.

There is huge difference among the objectives of both non profit and profit organisation.

NPO's are working to provide large number of benefits to individuals of society. They are not

working to earn profits but on other hand, Profit organisation works to earn large number of

profits (Purce, 2014). After having differences in objectives of both organisations there are many

similarities are identified in their operations and respective areas which are mentioned below:

Basis Profit organisation Non-profit organisation

Meaning It refers to such organisations

which provides their functions

regarding for the purpose of

earning large number of profits

It seems to be such companies

whose motive is to provide

maximum benefits to society

4

Financial report provides the information regarding funds which are used within the

organisation. These reports are prepared by the organisation for shareholders and lenders to

provide information regarding their current financial position. It includes the three different types

of basic reports like balance sheet which provides the information about the assets and liabilities

and net worth. Another report is income statement which helps to understand about the profit and

loss incurred by organisation during one financial period (Marshall and et. al., 2011). Last one is

cash flow statement, which shows inflow and outflow of cash which is incurred by organisation

through their business activities during given period of time.

It is the responsibility upon the accounting officer of Stratford Yachts Ltd. Is to prepare

their financial reports on the basis of their annual statements. It is the duty of every organisation

is to keep the proper records of their accounts which helps in collection of important information

and results to accomplish their objectives through preparation of strategies and policies (Smith,

2014). Non profit organisation has large number of responsibility is to keep proper record of the

different sources from where they raise their funds to bring transparency in their operations.

There is huge difference among the objectives of both non profit and profit organisation.

NPO's are working to provide large number of benefits to individuals of society. They are not

working to earn profits but on other hand, Profit organisation works to earn large number of

profits (Purce, 2014). After having differences in objectives of both organisations there are many

similarities are identified in their operations and respective areas which are mentioned below:

Basis Profit organisation Non-profit organisation

Meaning It refers to such organisations

which provides their functions

regarding for the purpose of

earning large number of profits

It seems to be such companies

whose motive is to provide

maximum benefits to society

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Form of organisation The different types of

organisation which are

included in this are

partnership, sole traders and

other organisation.

It includes Club, charitable

trust and public hospitals. Such

organisations works with the

support of government.

Sources of income Such organisations earn their

profits from the selling of their

different products and services

to end customers

Such types of organisations

attains their funds from

donations, subscriptions,

government funds etc.

Money earned over and above The amount of profit which

earned above the limits is

transfers to the capital reserve

accounts to plan about their

future activities

The surplus which is earned by

organisation is ascertained as

capital gains.

For ex., comparison of the financial statements of the profit and non profit organisation

helps in determination of their financial strengths and helps in creation of more value to attain

their objectives within stipulated period of time.

For-Profit Non-Profit

The financial reports which are prepared by

accounting officer of such organisation are

mentioned below:

Balance sheet

Profit and loss account

cash flow statements

The major reports which are prepared by the

accounting officers of such organisation are

mentioned below:

Statement of financial position

Activity detail summary

Cash flow report

c) Various groups of stakeholders and evaluate the different information needs

Stake holders: these are the parties, person and people who contains some interest in

growth and development of organisation. They are the person who remain responsible for

sustainable success of organisation (Massingham, 2014). Stake holders plays vital role in respect

5

organisation which are

included in this are

partnership, sole traders and

other organisation.

It includes Club, charitable

trust and public hospitals. Such

organisations works with the

support of government.

Sources of income Such organisations earn their

profits from the selling of their

different products and services

to end customers

Such types of organisations

attains their funds from

donations, subscriptions,

government funds etc.

Money earned over and above The amount of profit which

earned above the limits is

transfers to the capital reserve

accounts to plan about their

future activities

The surplus which is earned by

organisation is ascertained as

capital gains.

For ex., comparison of the financial statements of the profit and non profit organisation

helps in determination of their financial strengths and helps in creation of more value to attain

their objectives within stipulated period of time.

For-Profit Non-Profit

The financial reports which are prepared by

accounting officer of such organisation are

mentioned below:

Balance sheet

Profit and loss account

cash flow statements

The major reports which are prepared by the

accounting officers of such organisation are

mentioned below:

Statement of financial position

Activity detail summary

Cash flow report

c) Various groups of stakeholders and evaluate the different information needs

Stake holders: these are the parties, person and people who contains some interest in

growth and development of organisation. They are the person who remain responsible for

sustainable success of organisation (Massingham, 2014). Stake holders plays vital role in respect

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

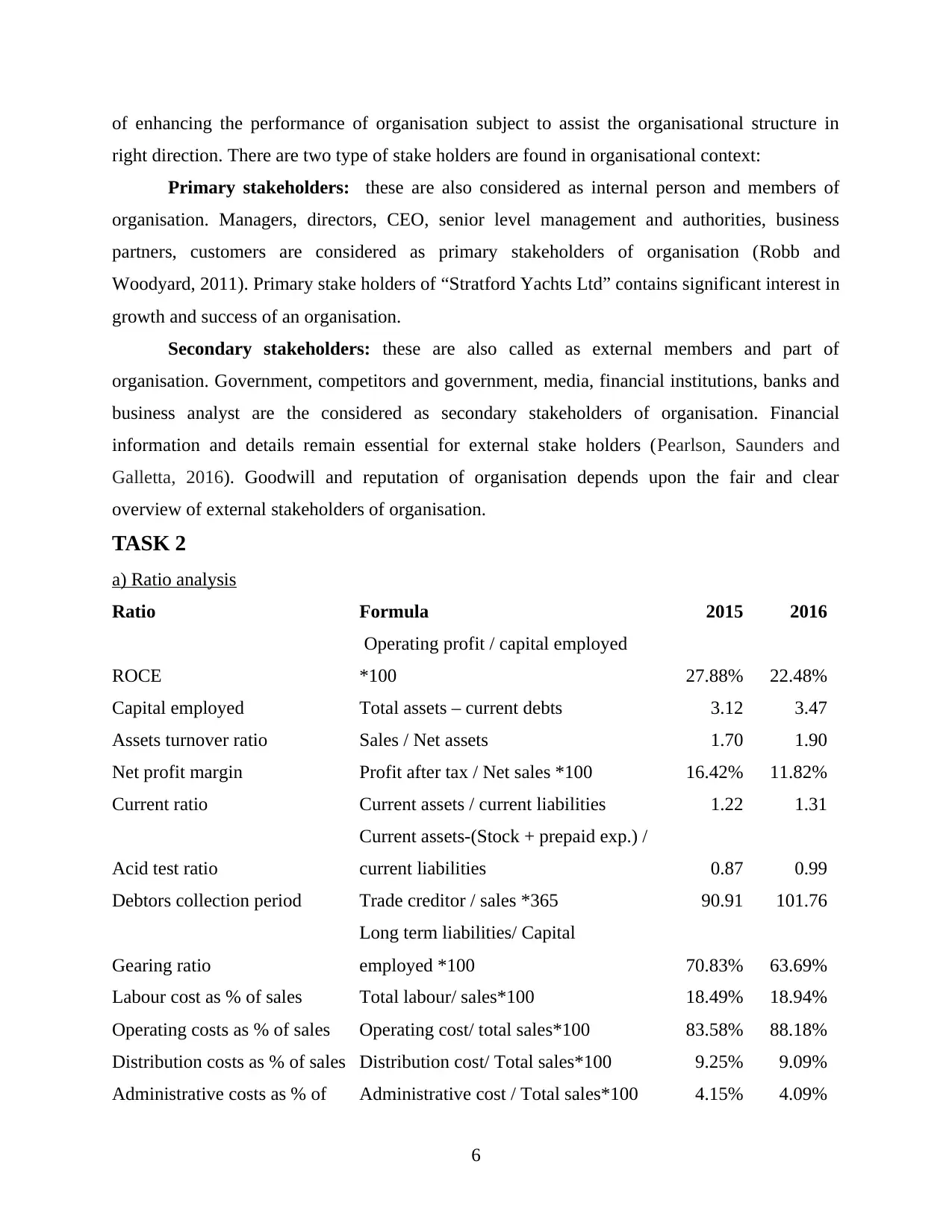

of enhancing the performance of organisation subject to assist the organisational structure in

right direction. There are two type of stake holders are found in organisational context:

Primary stakeholders: these are also considered as internal person and members of

organisation. Managers, directors, CEO, senior level management and authorities, business

partners, customers are considered as primary stakeholders of organisation (Robb and

Woodyard, 2011). Primary stake holders of “Stratford Yachts Ltd” contains significant interest in

growth and success of an organisation.

Secondary stakeholders: these are also called as external members and part of

organisation. Government, competitors and government, media, financial institutions, banks and

business analyst are the considered as secondary stakeholders of organisation. Financial

information and details remain essential for external stake holders (Pearlson, Saunders and

Galletta, 2016). Goodwill and reputation of organisation depends upon the fair and clear

overview of external stakeholders of organisation.

TASK 2

a) Ratio analysis

Ratio Formula 2015 2016

ROCE

Operating profit / capital employed

*100 27.88% 22.48%

Capital employed Total assets – current debts 3.12 3.47

Assets turnover ratio Sales / Net assets 1.70 1.90

Net profit margin Profit after tax / Net sales *100 16.42% 11.82%

Current ratio Current assets / current liabilities 1.22 1.31

Acid test ratio

Current assets-(Stock + prepaid exp.) /

current liabilities 0.87 0.99

Debtors collection period Trade creditor / sales *365 90.91 101.76

Gearing ratio

Long term liabilities/ Capital

employed *100 70.83% 63.69%

Labour cost as % of sales Total labour/ sales*100 18.49% 18.94%

Operating costs as % of sales Operating cost/ total sales*100 83.58% 88.18%

Distribution costs as % of sales Distribution cost/ Total sales*100 9.25% 9.09%

Administrative costs as % of Administrative cost / Total sales*100 4.15% 4.09%

6

right direction. There are two type of stake holders are found in organisational context:

Primary stakeholders: these are also considered as internal person and members of

organisation. Managers, directors, CEO, senior level management and authorities, business

partners, customers are considered as primary stakeholders of organisation (Robb and

Woodyard, 2011). Primary stake holders of “Stratford Yachts Ltd” contains significant interest in

growth and success of an organisation.

Secondary stakeholders: these are also called as external members and part of

organisation. Government, competitors and government, media, financial institutions, banks and

business analyst are the considered as secondary stakeholders of organisation. Financial

information and details remain essential for external stake holders (Pearlson, Saunders and

Galletta, 2016). Goodwill and reputation of organisation depends upon the fair and clear

overview of external stakeholders of organisation.

TASK 2

a) Ratio analysis

Ratio Formula 2015 2016

ROCE

Operating profit / capital employed

*100 27.88% 22.48%

Capital employed Total assets – current debts 3.12 3.47

Assets turnover ratio Sales / Net assets 1.70 1.90

Net profit margin Profit after tax / Net sales *100 16.42% 11.82%

Current ratio Current assets / current liabilities 1.22 1.31

Acid test ratio

Current assets-(Stock + prepaid exp.) /

current liabilities 0.87 0.99

Debtors collection period Trade creditor / sales *365 90.91 101.76

Gearing ratio

Long term liabilities/ Capital

employed *100 70.83% 63.69%

Labour cost as % of sales Total labour/ sales*100 18.49% 18.94%

Operating costs as % of sales Operating cost/ total sales*100 83.58% 88.18%

Distribution costs as % of sales Distribution cost/ Total sales*100 9.25% 9.09%

Administrative costs as % of Administrative cost / Total sales*100 4.15% 4.09%

6

sales

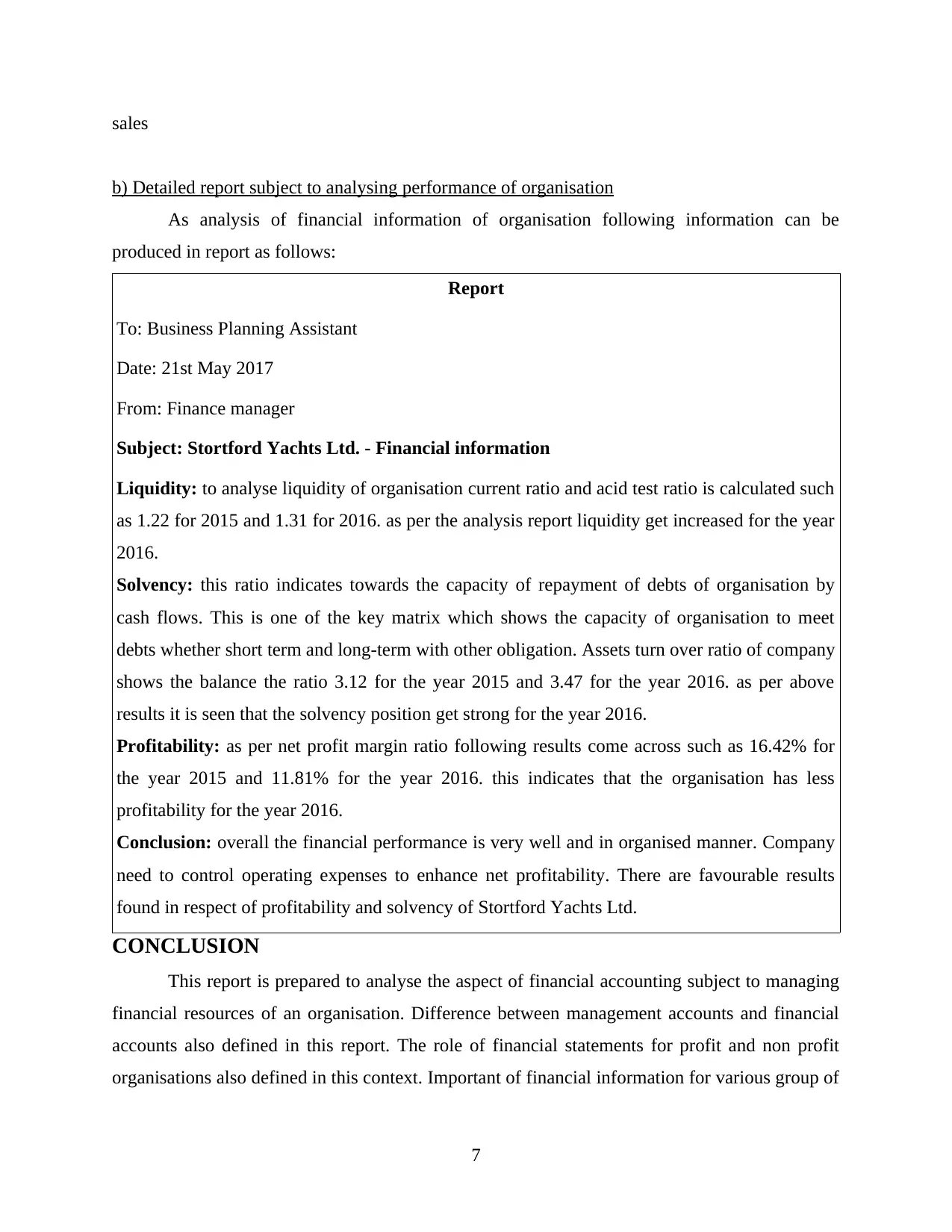

b) Detailed report subject to analysing performance of organisation

As analysis of financial information of organisation following information can be

produced in report as follows:

Report

To: Business Planning Assistant

Date: 21st May 2017

From: Finance manager

Subject: Stortford Yachts Ltd. - Financial information

Liquidity: to analyse liquidity of organisation current ratio and acid test ratio is calculated such

as 1.22 for 2015 and 1.31 for 2016. as per the analysis report liquidity get increased for the year

2016.

Solvency: this ratio indicates towards the capacity of repayment of debts of organisation by

cash flows. This is one of the key matrix which shows the capacity of organisation to meet

debts whether short term and long-term with other obligation. Assets turn over ratio of company

shows the balance the ratio 3.12 for the year 2015 and 3.47 for the year 2016. as per above

results it is seen that the solvency position get strong for the year 2016.

Profitability: as per net profit margin ratio following results come across such as 16.42% for

the year 2015 and 11.81% for the year 2016. this indicates that the organisation has less

profitability for the year 2016.

Conclusion: overall the financial performance is very well and in organised manner. Company

need to control operating expenses to enhance net profitability. There are favourable results

found in respect of profitability and solvency of Stortford Yachts Ltd.

CONCLUSION

This report is prepared to analyse the aspect of financial accounting subject to managing

financial resources of an organisation. Difference between management accounts and financial

accounts also defined in this report. The role of financial statements for profit and non profit

organisations also defined in this context. Important of financial information for various group of

7

b) Detailed report subject to analysing performance of organisation

As analysis of financial information of organisation following information can be

produced in report as follows:

Report

To: Business Planning Assistant

Date: 21st May 2017

From: Finance manager

Subject: Stortford Yachts Ltd. - Financial information

Liquidity: to analyse liquidity of organisation current ratio and acid test ratio is calculated such

as 1.22 for 2015 and 1.31 for 2016. as per the analysis report liquidity get increased for the year

2016.

Solvency: this ratio indicates towards the capacity of repayment of debts of organisation by

cash flows. This is one of the key matrix which shows the capacity of organisation to meet

debts whether short term and long-term with other obligation. Assets turn over ratio of company

shows the balance the ratio 3.12 for the year 2015 and 3.47 for the year 2016. as per above

results it is seen that the solvency position get strong for the year 2016.

Profitability: as per net profit margin ratio following results come across such as 16.42% for

the year 2015 and 11.81% for the year 2016. this indicates that the organisation has less

profitability for the year 2016.

Conclusion: overall the financial performance is very well and in organised manner. Company

need to control operating expenses to enhance net profitability. There are favourable results

found in respect of profitability and solvency of Stortford Yachts Ltd.

CONCLUSION

This report is prepared to analyse the aspect of financial accounting subject to managing

financial resources of an organisation. Difference between management accounts and financial

accounts also defined in this report. The role of financial statements for profit and non profit

organisations also defined in this context. Important of financial information for various group of

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

stakeholders also elaborated in this report. Financial performance of Stratford Yachts Ltd

presented by ratio analysis and a financial report is prepared for enhancing financial performance

of organisation.

8

presented by ratio analysis and a financial report is prepared for enhancing financial performance

of organisation.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.