Financial Management: Dividend Policy, Investment Appraisal Analysis

VerifiedAdded on 2020/06/04

|14

|3768

|33

Report

AI Summary

This report delves into financial management, focusing on dividend policy and investment appraisal techniques. It begins with a discussion of the dividend discount model, calculating the fair value of shares and exploring the impact of changes in shareholder required returns. The report also highlights the limitations of the dividend discount model. The second part of the report applies project evaluation methods to cash flows, assessing project viability, and discussing the advantages and disadvantages of different investment appraisal techniques. Calculations are provided to illustrate the concepts. The report concludes with a summary of the limitations of the methods discussed, offering a comprehensive overview of financial analysis and investment strategies.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Question 1: Dividend policy............................................................................................................1

(a)Computation of fair value of shares........................................................................................1

(b)Computation of fair value when shareholder required return get changed.............................2

© Limitation of dividend discount model....................................................................................2

Question 3: Investment appraisal techniques..................................................................................4

Calculation of project evaluation methods..................................................................................4

Benfit and limitation of different investment apprisal methods..................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

Working notes............................................................................................................................10

INTRODUCTION...........................................................................................................................1

Question 1: Dividend policy............................................................................................................1

(a)Computation of fair value of shares........................................................................................1

(b)Computation of fair value when shareholder required return get changed.............................2

© Limitation of dividend discount model....................................................................................2

Question 3: Investment appraisal techniques..................................................................................4

Calculation of project evaluation methods..................................................................................4

Benfit and limitation of different investment apprisal methods..................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

APPENDIX....................................................................................................................................10

Working notes............................................................................................................................10

INTRODUCTION

Investment is one of process that is undertaken by any business firm or an individual.

While making investment in any security it is not sufficient to just estimate whether in future it

will grow or price it will decline. It is also very important to identify whether shares that

individual intend to purchase is available in market at right price. In this regard varied models

like dividend discount model is taken in to account by investors. In the current report, by using

dividend discount model fair price of shares is computed and limitation of approach is also

discussed in detail. Apart from this, in second section of report project evaluation methods are

applied on cash flows and viability of project is measured. At end of the report, limitations of

different project evaluation methods is discussed in detail.

Question 1: Dividend policy

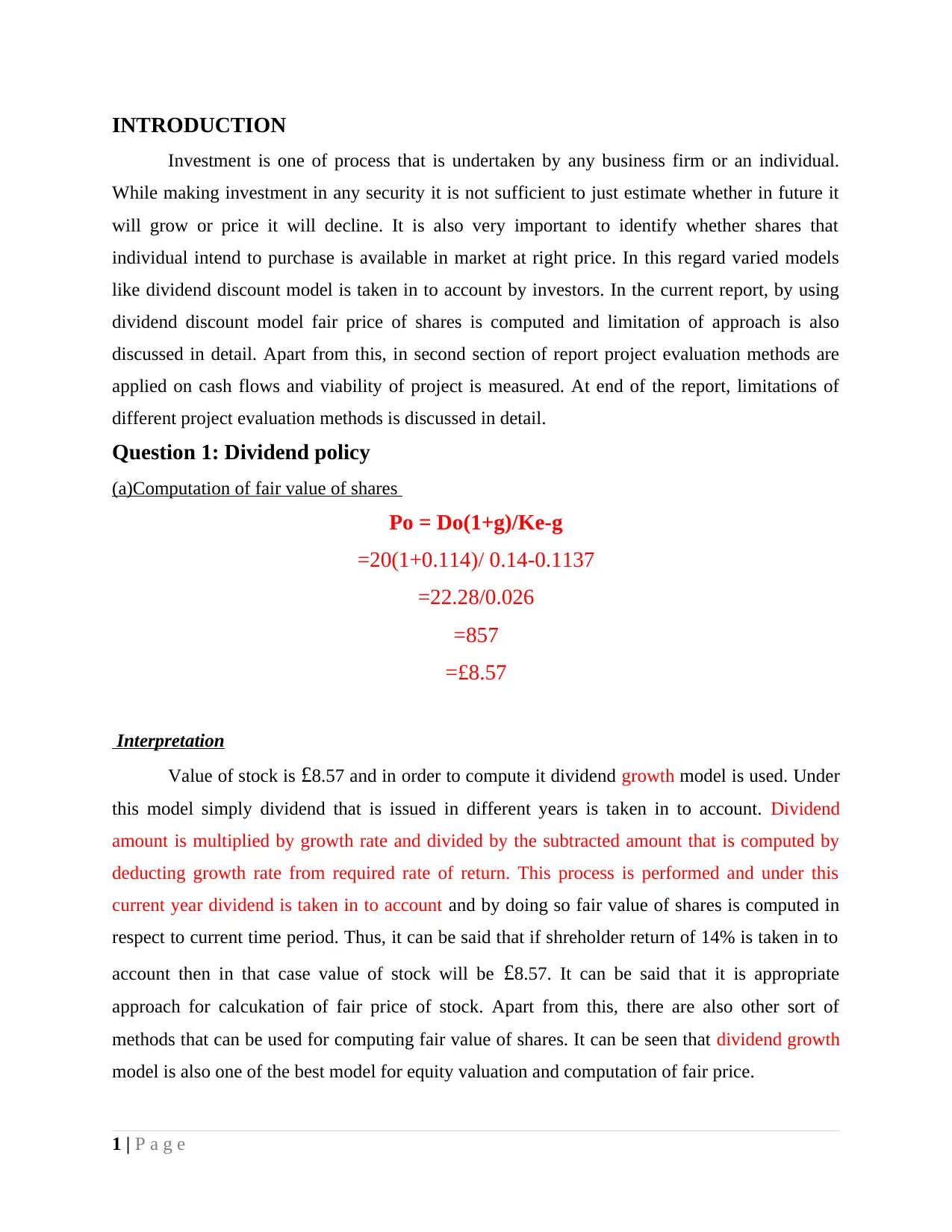

(a)Computation of fair value of shares

Po = Do(1+g)/Ke-g

=20(1+0.114)/ 0.14-0.1137

=22.28/0.026

=857

=£8.57

Interpretation

Value of stock is £8.57 and in order to compute it dividend growth model is used. Under

this model simply dividend that is issued in different years is taken in to account. Dividend

amount is multiplied by growth rate and divided by the subtracted amount that is computed by

deducting growth rate from required rate of return. This process is performed and under this

current year dividend is taken in to account and by doing so fair value of shares is computed in

respect to current time period. Thus, it can be said that if shreholder return of 14% is taken in to

account then in that case value of stock will be £8.57. It can be said that it is appropriate

approach for calcukation of fair price of stock. Apart from this, there are also other sort of

methods that can be used for computing fair value of shares. It can be seen that dividend growth

model is also one of the best model for equity valuation and computation of fair price.

1 | P a g e

Investment is one of process that is undertaken by any business firm or an individual.

While making investment in any security it is not sufficient to just estimate whether in future it

will grow or price it will decline. It is also very important to identify whether shares that

individual intend to purchase is available in market at right price. In this regard varied models

like dividend discount model is taken in to account by investors. In the current report, by using

dividend discount model fair price of shares is computed and limitation of approach is also

discussed in detail. Apart from this, in second section of report project evaluation methods are

applied on cash flows and viability of project is measured. At end of the report, limitations of

different project evaluation methods is discussed in detail.

Question 1: Dividend policy

(a)Computation of fair value of shares

Po = Do(1+g)/Ke-g

=20(1+0.114)/ 0.14-0.1137

=22.28/0.026

=857

=£8.57

Interpretation

Value of stock is £8.57 and in order to compute it dividend growth model is used. Under

this model simply dividend that is issued in different years is taken in to account. Dividend

amount is multiplied by growth rate and divided by the subtracted amount that is computed by

deducting growth rate from required rate of return. This process is performed and under this

current year dividend is taken in to account and by doing so fair value of shares is computed in

respect to current time period. Thus, it can be said that if shreholder return of 14% is taken in to

account then in that case value of stock will be £8.57. It can be said that it is appropriate

approach for calcukation of fair price of stock. Apart from this, there are also other sort of

methods that can be used for computing fair value of shares. It can be seen that dividend growth

model is also one of the best model for equity valuation and computation of fair price.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

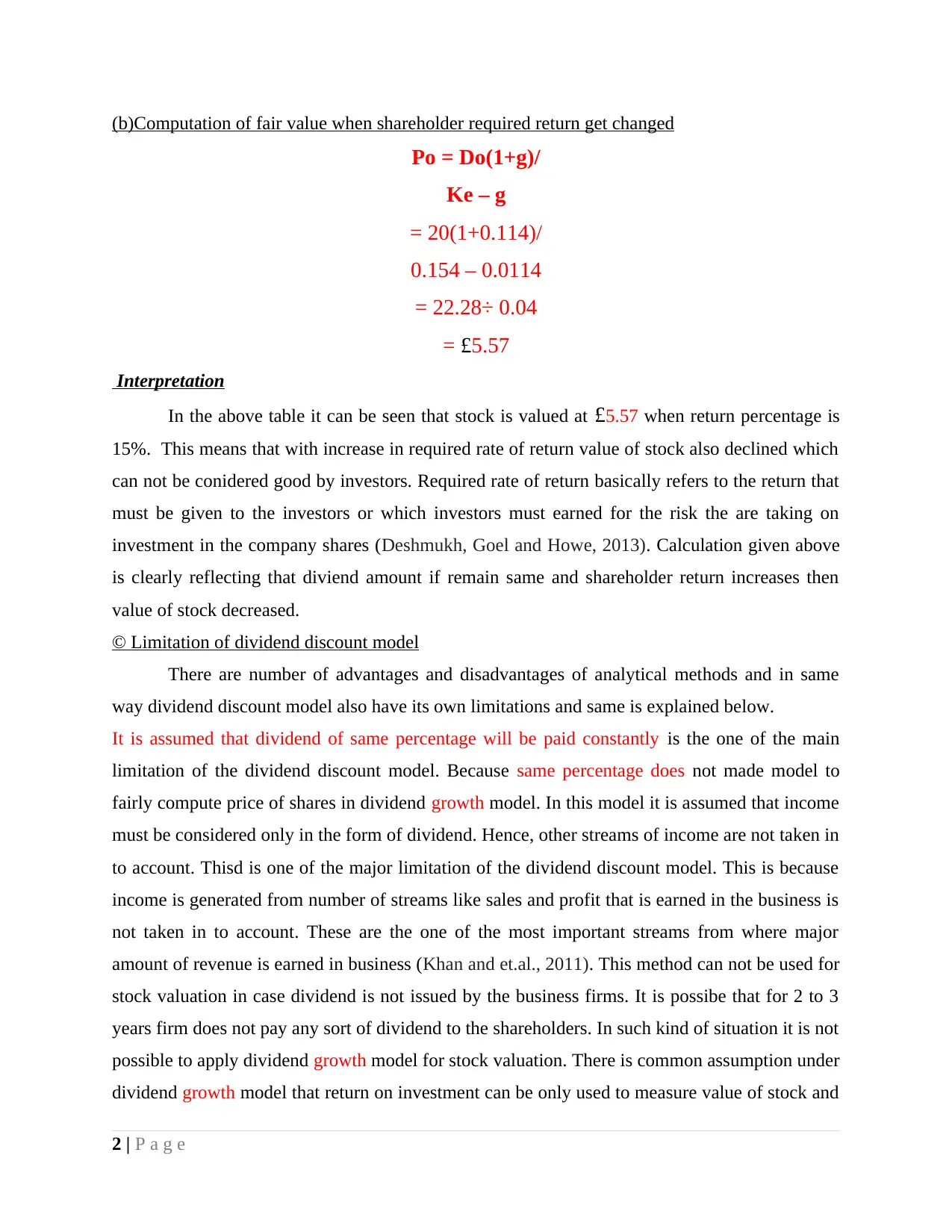

(b)Computation of fair value when shareholder required return get changed

Po = Do(1+g)/

Ke – g

= 20(1+0.114)/

0.154 – 0.0114

= 22.28÷ 0.04

= £5.57

Interpretation

In the above table it can be seen that stock is valued at £5.57 when return percentage is

15%. This means that with increase in required rate of return value of stock also declined which

can not be conidered good by investors. Required rate of return basically refers to the return that

must be given to the investors or which investors must earned for the risk the are taking on

investment in the company shares (Deshmukh, Goel and Howe, 2013). Calculation given above

is clearly reflecting that diviend amount if remain same and shareholder return increases then

value of stock decreased.

© Limitation of dividend discount model

There are number of advantages and disadvantages of analytical methods and in same

way dividend discount model also have its own limitations and same is explained below.

It is assumed that dividend of same percentage will be paid constantly is the one of the main

limitation of the dividend discount model. Because same percentage does not made model to

fairly compute price of shares in dividend growth model. In this model it is assumed that income

must be considered only in the form of dividend. Hence, other streams of income are not taken in

to account. Thisd is one of the major limitation of the dividend discount model. This is because

income is generated from number of streams like sales and profit that is earned in the business is

not taken in to account. These are the one of the most important streams from where major

amount of revenue is earned in business (Khan and et.al., 2011). This method can not be used for

stock valuation in case dividend is not issued by the business firms. It is possibe that for 2 to 3

years firm does not pay any sort of dividend to the shareholders. In such kind of situation it is not

possible to apply dividend growth model for stock valuation. There is common assumption under

dividend growth model that return on investment can be only used to measure value of stock and

2 | P a g e

Po = Do(1+g)/

Ke – g

= 20(1+0.114)/

0.154 – 0.0114

= 22.28÷ 0.04

= £5.57

Interpretation

In the above table it can be seen that stock is valued at £5.57 when return percentage is

15%. This means that with increase in required rate of return value of stock also declined which

can not be conidered good by investors. Required rate of return basically refers to the return that

must be given to the investors or which investors must earned for the risk the are taking on

investment in the company shares (Deshmukh, Goel and Howe, 2013). Calculation given above

is clearly reflecting that diviend amount if remain same and shareholder return increases then

value of stock decreased.

© Limitation of dividend discount model

There are number of advantages and disadvantages of analytical methods and in same

way dividend discount model also have its own limitations and same is explained below.

It is assumed that dividend of same percentage will be paid constantly is the one of the main

limitation of the dividend discount model. Because same percentage does not made model to

fairly compute price of shares in dividend growth model. In this model it is assumed that income

must be considered only in the form of dividend. Hence, other streams of income are not taken in

to account. Thisd is one of the major limitation of the dividend discount model. This is because

income is generated from number of streams like sales and profit that is earned in the business is

not taken in to account. These are the one of the most important streams from where major

amount of revenue is earned in business (Khan and et.al., 2011). This method can not be used for

stock valuation in case dividend is not issued by the business firms. It is possibe that for 2 to 3

years firm does not pay any sort of dividend to the shareholders. In such kind of situation it is not

possible to apply dividend growth model for stock valuation. There is common assumption under

dividend growth model that return on investment can be only used to measure value of stock and

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

due to this reason only dividend income is taken in to account for valuation of stock in the

business. This is not be considered as one of the right approach. This is because sales revenue is

also one of the major souce of income. Hence, until sales revenue is not taken in to account it is

not possible to make accurate valuation of stock. Apart from this another limitation in respect to

dividend growth model is assumption that is related to required rate of return. It is very hard task

to make estimation of the required rate of return that is associated with specific company stock.

It can be noted that thinking of all investors are different from each other (Ramalingegowda,

Wang and Yu, 2013). Means that for each investor required rate of return will be different and

due to this reason it is not possible to take accurate required rate of return. Thus, there is high

probability that manager can take wrong required rate of return. If required rate of return will not

be accurate then in that case wrong invstment decision can be taken by the managers. Either

stock will be assumed undervalued or overvalued. In both cases decisions taken will be in wrong

direction. Hence, there are high degree of chances that wrong decisions can be taken by

managers. Due to all these reasons investor or manager can make investment in stocks that are

already heavily priced and may decline in the upcoming time period. Contrary to this, they can

also make investment in stocks that are already underpriced in nature (Shao, Kwok and

Guedhami, 2010). Hence, there is totally situation of uncertainity and due to this reason dividend

growth model can not be used in the business for making investment related decisions. Apart

from this, use of growth rate is the one of the major drawback of the dividend growth model

because it is very hard task for the firm to maintain same rate of dividend every year. This is

because dividend growth rate keeps on fluctuating consistently on yearly basis. Thus, it is not

possible to make accurate estimation about rate at which dividend may grow in the upcoming

time period. Hence, due to this reason dividend discount model alone can not be used for equity

valuation because reliable results can not be obtained by using this technique and investor can

make wrong decisions in respect to investment. Under the approach to identify whether stocks

are overvalued or undervalued in nature simple price that is revealed by the dividend growth

model will be compared to market price and on that basis it is identified whether it will be better

time to make investment (Agyei and Marfo-Yiadom, 2011). If due to some reasons like wrong

judgement of growth rate stock seems undervalued or overvalued then wrong investment

decision can be taken by the manager in their business.

3 | P a g e

business. This is not be considered as one of the right approach. This is because sales revenue is

also one of the major souce of income. Hence, until sales revenue is not taken in to account it is

not possible to make accurate valuation of stock. Apart from this another limitation in respect to

dividend growth model is assumption that is related to required rate of return. It is very hard task

to make estimation of the required rate of return that is associated with specific company stock.

It can be noted that thinking of all investors are different from each other (Ramalingegowda,

Wang and Yu, 2013). Means that for each investor required rate of return will be different and

due to this reason it is not possible to take accurate required rate of return. Thus, there is high

probability that manager can take wrong required rate of return. If required rate of return will not

be accurate then in that case wrong invstment decision can be taken by the managers. Either

stock will be assumed undervalued or overvalued. In both cases decisions taken will be in wrong

direction. Hence, there are high degree of chances that wrong decisions can be taken by

managers. Due to all these reasons investor or manager can make investment in stocks that are

already heavily priced and may decline in the upcoming time period. Contrary to this, they can

also make investment in stocks that are already underpriced in nature (Shao, Kwok and

Guedhami, 2010). Hence, there is totally situation of uncertainity and due to this reason dividend

growth model can not be used in the business for making investment related decisions. Apart

from this, use of growth rate is the one of the major drawback of the dividend growth model

because it is very hard task for the firm to maintain same rate of dividend every year. This is

because dividend growth rate keeps on fluctuating consistently on yearly basis. Thus, it is not

possible to make accurate estimation about rate at which dividend may grow in the upcoming

time period. Hence, due to this reason dividend discount model alone can not be used for equity

valuation because reliable results can not be obtained by using this technique and investor can

make wrong decisions in respect to investment. Under the approach to identify whether stocks

are overvalued or undervalued in nature simple price that is revealed by the dividend growth

model will be compared to market price and on that basis it is identified whether it will be better

time to make investment (Agyei and Marfo-Yiadom, 2011). If due to some reasons like wrong

judgement of growth rate stock seems undervalued or overvalued then wrong investment

decision can be taken by the manager in their business.

3 | P a g e

It can be concluded that there are number of limitations of the dividend growth model

and due to this reason discounted free cash flow model must be used in the equity valuation.

Under this model first of all model is developed under which from sales revenue all sort of

expenses are deducted and net profit is computed for earlier years. Then growth rate is estimated

at which sales revenue may grow in upcoming time period. By considering this growth rate sales

revenue and expenses for future time period and terminal year is computed. Finally after

development of this model discount rate is taken in to account to compute present value of cash

flows. On other hand, in next stage in model weighted average cost of capital is previously

calculated and under this weight is given to debt and equity in the capital structure and same is

multiplied to interest rate and cost of equity (Posavac, 2015). In this way discount rate or

weighted average cost of capital is computed. In last stage all present values of cash flows are

summed up and by considering same present value is computed. Thereafter, at last stage by using

debt and equity amount as well as summed present value intrinsic value of equity is computed. In

this way by using discounted cash flow model in better way equity value is computed.

Question 3: Investment appraisal techniques

Calculation of project evaluation methods

Current market value of brands plc

= 400,000 ×£1.90 = £760,000

Fund proposed to be raised from market = £160,000

Final market value after issue of shares = £760,000 + £160,000

= £920,000.

Interpretation

Current market value of equity is £760000 and proposed fund amount that company

intends to raise from the market is £1,60,000 and on this basis it is find out that after issue of

equity total computed market value will be £920000. Hence, it can be said that total amount of

equity will increase in business.

Ii. Earnings before right issue

= £600,000 ×15%

4 | P a g e

and due to this reason discounted free cash flow model must be used in the equity valuation.

Under this model first of all model is developed under which from sales revenue all sort of

expenses are deducted and net profit is computed for earlier years. Then growth rate is estimated

at which sales revenue may grow in upcoming time period. By considering this growth rate sales

revenue and expenses for future time period and terminal year is computed. Finally after

development of this model discount rate is taken in to account to compute present value of cash

flows. On other hand, in next stage in model weighted average cost of capital is previously

calculated and under this weight is given to debt and equity in the capital structure and same is

multiplied to interest rate and cost of equity (Posavac, 2015). In this way discount rate or

weighted average cost of capital is computed. In last stage all present values of cash flows are

summed up and by considering same present value is computed. Thereafter, at last stage by using

debt and equity amount as well as summed present value intrinsic value of equity is computed. In

this way by using discounted cash flow model in better way equity value is computed.

Question 3: Investment appraisal techniques

Calculation of project evaluation methods

Current market value of brands plc

= 400,000 ×£1.90 = £760,000

Fund proposed to be raised from market = £160,000

Final market value after issue of shares = £760,000 + £160,000

= £920,000.

Interpretation

Current market value of equity is £760000 and proposed fund amount that company

intends to raise from the market is £1,60,000 and on this basis it is find out that after issue of

equity total computed market value will be £920000. Hence, it can be said that total amount of

equity will increase in business.

Ii. Earnings before right issue

= £600,000 ×15%

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= £90,000

iii. Earnings from new funds

= £160,000 ×15% = £24,000.

iv. Total Earnings after right issue

=£90,000 + £24,000

= £114,000

Interpretation

Total amount of earning on new fund will be £90,000 as earning percentage is 15% on

total amount of shareholder equity. In right issue further shares are issued to the employees or

exisitng shareholders first of all. If additionally invested amount will be taken in to account then

earning on new fund will be £24000 and therefore total amount of earning after right issue will

be £114000. It can be said that firm is generating good amount of return amount on shareholders

fund.

Case 1: Share price £1.80

2a. i. Issue price = £1.80.

No of new shares

= £160,000 ÷£1.80

= £88, 888

Total shares in use

= 400,000 + 88,889

= 488,889

2A. ii. Theoretical Ex- Rights price

Final market value = 920,000 ÷488,889

= £1.88 per share.

2A. iii. New EPS

5 | P a g e

iii. Earnings from new funds

= £160,000 ×15% = £24,000.

iv. Total Earnings after right issue

=£90,000 + £24,000

= £114,000

Interpretation

Total amount of earning on new fund will be £90,000 as earning percentage is 15% on

total amount of shareholder equity. In right issue further shares are issued to the employees or

exisitng shareholders first of all. If additionally invested amount will be taken in to account then

earning on new fund will be £24000 and therefore total amount of earning after right issue will

be £114000. It can be said that firm is generating good amount of return amount on shareholders

fund.

Case 1: Share price £1.80

2a. i. Issue price = £1.80.

No of new shares

= £160,000 ÷£1.80

= £88, 888

Total shares in use

= 400,000 + 88,889

= 488,889

2A. ii. Theoretical Ex- Rights price

Final market value = 920,000 ÷488,889

= £1.88 per share.

2A. iii. New EPS

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total earning after right issue =

100 ×114,000 / 488,889

= 23.32 pence.

2A, iv. Form of right issue

Shares = 400,000

Total shares= 88,889

400,000 ÷88,889

= 4.5

Interpretation

In case issue price become £1.80 then in that case number of fresh issued shares will be

88,888 and due to this reason total shares issued will be 488,889. Ex right share issue price now

is £1.88 because total new market value of shares is divided by old + new issued shares and in

this way new price is computed. Earning per share on issued shares is 23.32 pence and form of

right issue value is 4.5 which means that for each unit investor previously hold receive 4.5 units

new additional units.

Case 2: Share price £1.60

2B. i. Issue price = £1.60

No of new shares = £160,000 ÷£1.60

= 100,000.

Total shares in issue

= 400,000 + 100,000

= 500,000.

Bii. Theoretical Ex-right price

Final market value = 920,000 ÷500,000

= £1.84 per share.

Biii. New Earning per share

Total earning after right issue = 100 ×114,000 / 500,000

= 22.8 pence.

6 | P a g e

100 ×114,000 / 488,889

= 23.32 pence.

2A, iv. Form of right issue

Shares = 400,000

Total shares= 88,889

400,000 ÷88,889

= 4.5

Interpretation

In case issue price become £1.80 then in that case number of fresh issued shares will be

88,888 and due to this reason total shares issued will be 488,889. Ex right share issue price now

is £1.88 because total new market value of shares is divided by old + new issued shares and in

this way new price is computed. Earning per share on issued shares is 23.32 pence and form of

right issue value is 4.5 which means that for each unit investor previously hold receive 4.5 units

new additional units.

Case 2: Share price £1.60

2B. i. Issue price = £1.60

No of new shares = £160,000 ÷£1.60

= 100,000.

Total shares in issue

= 400,000 + 100,000

= 500,000.

Bii. Theoretical Ex-right price

Final market value = 920,000 ÷500,000

= £1.84 per share.

Biii. New Earning per share

Total earning after right issue = 100 ×114,000 / 500,000

= 22.8 pence.

6 | P a g e

B.iv. Form of rights issue

Shares = 400,000

New shares= 100,000

400,000 ÷100,000

= 4

Interpretation

At price of £1.60 total issued shres are 100000 and now after addition of new shares total

issued shares now become 500000. If final market value that will be obtained on right issue is

taken in to consideration then Ex right price is £1.84. New earning per share value is 22.8 pence

and form of right issue valued at 4 which means that for each unit that investor earlier have with

it additionally 4 new units are received.

Case 3: Share price £1.40

2C. i. Issue Price = £1.40

Number of new shares = £160,000 ÷£1.40

= 114,286.

Total Shares in use:

= 400,000 + 114, 286

= 514, 286.

2C ii. Theoretical Ex-Right Price.

920,000 ÷514,286

= £1.79 per share.

2C iii. New Earning per shares.

100 × 114,000 / 514,286

= 22.17 pence.

2C. iv. Form of Rights issue.

Shares = 400,000

New shares = 114,286

7 | P a g e

Shares = 400,000

New shares= 100,000

400,000 ÷100,000

= 4

Interpretation

At price of £1.60 total issued shres are 100000 and now after addition of new shares total

issued shares now become 500000. If final market value that will be obtained on right issue is

taken in to consideration then Ex right price is £1.84. New earning per share value is 22.8 pence

and form of right issue valued at 4 which means that for each unit that investor earlier have with

it additionally 4 new units are received.

Case 3: Share price £1.40

2C. i. Issue Price = £1.40

Number of new shares = £160,000 ÷£1.40

= 114,286.

Total Shares in use:

= 400,000 + 114, 286

= 514, 286.

2C ii. Theoretical Ex-Right Price.

920,000 ÷514,286

= £1.79 per share.

2C iii. New Earning per shares.

100 × 114,000 / 514,286

= 22.17 pence.

2C. iv. Form of Rights issue.

Shares = 400,000

New shares = 114,286

7 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

400,000 ÷114, 286

= 3.5

Interpretation

In case price of 1.40 is determined then in that case total shares in issue will be 514286

and like done above if entire equity amount will be taken in to consideration then new price will

be £1.79 per share. Earning per share is 22.17 pence and form of right issue is 3.5 which means

that for every single unit 3.5 units more are received by investor.

On comparison of different proposed share prices it can be said that more will be issue

price investors will receive more amount of holding on right issue. Earning per share is also high

in case high price is determined for right issue. Hence, it can be said that investors will observe

more profit if right issue price will be high.

Advantage of scrip dividend for company and investors

There are number of advantages of scrip dividend for company and investors. It depend

on company whether it issue or not issue scrip dividend to the the investors. Usually, it is

observed that scrip dividend prove beneficial to both company and investors. Advantages that

company and investors can receive from scrip dividend are given below. Company: One of the main advantage of scrip dividend is that in case shares are issued

as dividend by company and if investor want cash then dividend is paid in cash form to

them. Firm will prefer that most investors choose stock as form of dividend because it is

possible that firm earn huge amount of profit in its business which will be reinvested for

expansion of same across wide geographic area. Next year on successful completion of

project firm may earn good amount of profit in its business and same can be used to pay

high amount of dividend on issued shares. It must be noted that issue of scrip shares acts

as strategy for the firm because in first year even firm earn super normal profit in its

business it does not give dividend to investors if investor choose not to receive dividend

in form of cash. Hence, lots of amount is saved in the business and reinvested in same

and use to discharge from debt liabilities. This help firm to restructure its capital structure

to some extent and reduce cost of debt. Moreover, this strategy also help company to

accumlate more and more amount of money in the business which will be used to expand

8 | P a g e

= 3.5

Interpretation

In case price of 1.40 is determined then in that case total shares in issue will be 514286

and like done above if entire equity amount will be taken in to consideration then new price will

be £1.79 per share. Earning per share is 22.17 pence and form of right issue is 3.5 which means

that for every single unit 3.5 units more are received by investor.

On comparison of different proposed share prices it can be said that more will be issue

price investors will receive more amount of holding on right issue. Earning per share is also high

in case high price is determined for right issue. Hence, it can be said that investors will observe

more profit if right issue price will be high.

Advantage of scrip dividend for company and investors

There are number of advantages of scrip dividend for company and investors. It depend

on company whether it issue or not issue scrip dividend to the the investors. Usually, it is

observed that scrip dividend prove beneficial to both company and investors. Advantages that

company and investors can receive from scrip dividend are given below. Company: One of the main advantage of scrip dividend is that in case shares are issued

as dividend by company and if investor want cash then dividend is paid in cash form to

them. Firm will prefer that most investors choose stock as form of dividend because it is

possible that firm earn huge amount of profit in its business which will be reinvested for

expansion of same across wide geographic area. Next year on successful completion of

project firm may earn good amount of profit in its business and same can be used to pay

high amount of dividend on issued shares. It must be noted that issue of scrip shares acts

as strategy for the firm because in first year even firm earn super normal profit in its

business it does not give dividend to investors if investor choose not to receive dividend

in form of cash. Hence, lots of amount is saved in the business and reinvested in same

and use to discharge from debt liabilities. This help firm to restructure its capital structure

to some extent and reduce cost of debt. Moreover, this strategy also help company to

accumlate more and more amount of money in the business which will be used to expand

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business at rapid rate. All these things suerly will generate huge profit in next year and

investors received good amount of dividend. Hence, it can be said company successfully

satisfied its investors by giving then good profit making opportunity in multiple years.

However, even though there are number of benefits of scrip dividend to the business

firms but same have some disadvantages for same. Means that issue of new shares lead to

reduction in shareholding of currrent shareholders in the company. It can be observed that

issue of right issue lead to reduction in control of real business owners in the company

that established it in past year. It can be said that issue of new shares under right issue

have heavy impact on control that real owners have on the company. All these things

does not allow real owners to make business decisions with full freedom. Many times

interest of different stakeholders collide with each other and it become hard task to make

accurate decision. In such situation if majority of shareholders are against company Co

founders opinion or view then in that case mentioend party can not execute its decision.

Hence, it can be said that right issue lead to reduction in decision makings capability of

individuals which are cofounder of company. Shareholders: Scrip dividend benefit a lot to the investors because due to this practice

that is followed by the firm their portfolio size increased overnight if they want to receive

dividend in form of stock then cash. Hence, in case share price increased in the market

value of shares that investors hold also increase and due to addition of new shares in

portfolio capital gain amount also increased at fast pace for the investors. Hence, it can be

said that if an individual decide to sale its units then in that case there is high probability

that it will earn good return on invested amount. Thus, in this way issue of scrip dividend

by the company benefit a lot to the investors. Apart from this, there maybe some

investors that may like to received cash on stock. Then company take care of them and

give them dividend in form of cash. So, in this scheme investors according to their

preference receive return from company and remain satisfied. Thus, scrip dividend is

beneficial for both shareholder and company. There are number of investors that always

prefer stock dividend of shares then cash dividend. This is because they does not think

that sufficient amount of dividend is given to them. On other hand, in case of stock

dividend there is common assumption among investors that if its value increase in future

time period then good amount of return can be earned in form of capital gain. Hence,

9 | P a g e

investors received good amount of dividend. Hence, it can be said company successfully

satisfied its investors by giving then good profit making opportunity in multiple years.

However, even though there are number of benefits of scrip dividend to the business

firms but same have some disadvantages for same. Means that issue of new shares lead to

reduction in shareholding of currrent shareholders in the company. It can be observed that

issue of right issue lead to reduction in control of real business owners in the company

that established it in past year. It can be said that issue of new shares under right issue

have heavy impact on control that real owners have on the company. All these things

does not allow real owners to make business decisions with full freedom. Many times

interest of different stakeholders collide with each other and it become hard task to make

accurate decision. In such situation if majority of shareholders are against company Co

founders opinion or view then in that case mentioend party can not execute its decision.

Hence, it can be said that right issue lead to reduction in decision makings capability of

individuals which are cofounder of company. Shareholders: Scrip dividend benefit a lot to the investors because due to this practice

that is followed by the firm their portfolio size increased overnight if they want to receive

dividend in form of stock then cash. Hence, in case share price increased in the market

value of shares that investors hold also increase and due to addition of new shares in

portfolio capital gain amount also increased at fast pace for the investors. Hence, it can be

said that if an individual decide to sale its units then in that case there is high probability

that it will earn good return on invested amount. Thus, in this way issue of scrip dividend

by the company benefit a lot to the investors. Apart from this, there maybe some

investors that may like to received cash on stock. Then company take care of them and

give them dividend in form of cash. So, in this scheme investors according to their

preference receive return from company and remain satisfied. Thus, scrip dividend is

beneficial for both shareholder and company. There are number of investors that always

prefer stock dividend of shares then cash dividend. This is because they does not think

that sufficient amount of dividend is given to them. On other hand, in case of stock

dividend there is common assumption among investors that if its value increase in future

time period then good amount of return can be earned in form of capital gain. Hence,

9 | P a g e

investors prefer to receive shares under right issue instead of cash dividend. Thus, in

order to show investors that company is concerned about them there are number of firms

that in specific years when good amount of profit is earned prefered to give additional

shares to shareholders.

CONCLUSION

On the basis of above discussion it is concluded that there are number of limitations of

dividend discount model and instead of this discounted cash flow model must be taken in to

account in order to compute fair value of equity. It is also concluded that there are limitations of

the project evaluation methods and all of them must be used to evaluate project because

weakness of one technique is strength of other method. Hence, it can be said that there is great

importance of project evaluation method.

10 | P a g e

order to show investors that company is concerned about them there are number of firms

that in specific years when good amount of profit is earned prefered to give additional

shares to shareholders.

CONCLUSION

On the basis of above discussion it is concluded that there are number of limitations of

dividend discount model and instead of this discounted cash flow model must be taken in to

account in order to compute fair value of equity. It is also concluded that there are limitations of

the project evaluation methods and all of them must be used to evaluate project because

weakness of one technique is strength of other method. Hence, it can be said that there is great

importance of project evaluation method.

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.